Market Definition

Truck and Bus Tires (often categorized as TBR, Truck and Bus Radial) are heavy-duty pneumatic structures specifically engineered for medium- and heavy-commercial vehicles, including freight trucks, delivery vans, city buses, and long-haul coaches. Unlike passenger tires, these are designed with significantly higher load-carrying capacities, reinforced sidewalls to resist curbing, and multiple steel belts to facilitate retreading, the process of replacing a worn tread to extend the casing’s life. These tires are optimized for high-mileage durability, heat dissipation during long-distance hauling, and traction across diverse terrains and weather conditions.

Market Insights

The most transformative trend in 2026 is the electrification-led redesign of heavy-duty tires. As electric trucks and buses are typically 20% to 30% heavier than their internal combustion counterparts due to massive battery packs, traditional tire architectures are being replaced by high-load (HL) variants. These EV-specific tires feature specialized rubber compounds to handle instant torque, which causes faster tread wear, and quiet-tread technologies to maintain the acoustic benefits of electric drivetrains. This segment is currently the fastest-growing niche, as fleet operators transition to zero-emission vehicles to meet stringent urban air quality mandates.

A second critical insight is the rise of Smart Tire telemetry and IoT integration. Modern truck and bus tires are increasingly equipped with embedded sensors that provide real-time data on pressure, internal temperature, and tread depth directly to fleet management software. In 2026, this has shifted from a premium add-on to a standard operational requirement for large-scale logistics providers. By predicting blowouts before they occur and optimizing inflation for fuel efficiency, these smart systems reduce tire-related downtime by up to 30%, effectively transforming the tire from a passive rubber component into a sophisticated data-gathering asset.

The industry is also witnessing a massive move toward Circular Economy and Retreading Economics. With the rising costs of raw materials like natural rubber and butadiene, fleet operators are prioritizing retreadability in their initial purchase criteria. High-quality casings are now designed to undergo two or even three retreading cycles, which can reduce the total cost of ownership (TCO) by nearly 50% compared to buying new tires every time. This trend is supported by a growing global network of certified retreading facilities, particularly in Europe and North America, where sustainability reporting and waste reduction are now part of corporate ESG mandates.

The geographical center of gravity remains firmly in the Asia-Pacific region, which accounts for over 50% of global demand. Driven by the infrastructure booms in India and Southeast Asia and the world-leading e-commerce logistics network in China, this region serves as both the largest production hub and the most significant consumption market. While Western markets are focusing on high-tech, low-rolling-resistance tires to lower carbon taxes, the APAC market is characterized by a demand for mixed-service tires that can handle both high-speed highways and unpaved rural roads, reflecting the region’s diverse and rapidly expanding infrastructure.

Key Drivers

The Truck and Bus Radial (TBR) market in 2026 is primarily driven by the exponential growth of e-commerce and the restructuring of global logistics networks. As the last-mile delivery and long-haul freight sectors expand to meet the demands of a digitized global economy, the intensity of vehicle usage has reached an all-time high. This surge in ton-miles directly correlates to a faster replacement cycle for tires, which are the highest-wear components in a fleet. Furthermore, the push for fleet operational efficiency is driving the adoption of Smart Tires, units embedded with RFID and IoT sensors that provide real-time telemetry on pressure and temperature. These technologies allow fleet managers to transition from reactive to predictive maintenance, reducing fuel consumption and preventing costly roadside blowouts, effectively turning tire procurement into a strategic data-driven investment.

A second major driver is the aggressive electrification of public transit and urban freight. In 2026, many major global cities have implemented Green Zones, forcing the transition to electric buses and delivery trucks. Because electric drivetrains are significantly heavier due to battery mass and deliver higher instant torque, they require specialized high-load (HL) tires with reinforced casings and advanced tread compounds. These premium-tier tires are engineered to provide lower rolling resistance (to extend battery range) while offering the high traction necessary to manage electric motor performance. This regulatory-driven shift toward electrification is creating a high-value growth corridor for manufacturers, as these specialized tires command higher margins and require more frequent, high-precision maintenance than legacy internal combustion engine (ICE) variants.

Key Challenges

The industry faces a significant challenge in raw material price volatility and supply chain fragmentation. In 2026, the costs of natural rubber, synthetic butadiene, and high-grade carbon black remain highly sensitive to geopolitical tensions and fluctuating energy prices. Since raw materials typically account for 60% to 70% of total production costs, even minor shifts in commodity prices can severely squeeze manufacturer margins and disrupt long-term pricing agreements with large-scale fleets. Additionally, the industry is grappling with stringent environmental and PFAS-free mandates. Regulators are increasingly scrutinizing the chemical additives used in tire vulcanization and the environmental impact of tire-wear particles (microplastics). This necessitates expensive, non-stop R&D into bio-sourced alternatives and circular manufacturing processes, creating a high-cost sustainability barrier that complicates the roadmap for smaller, less-capitalized players.

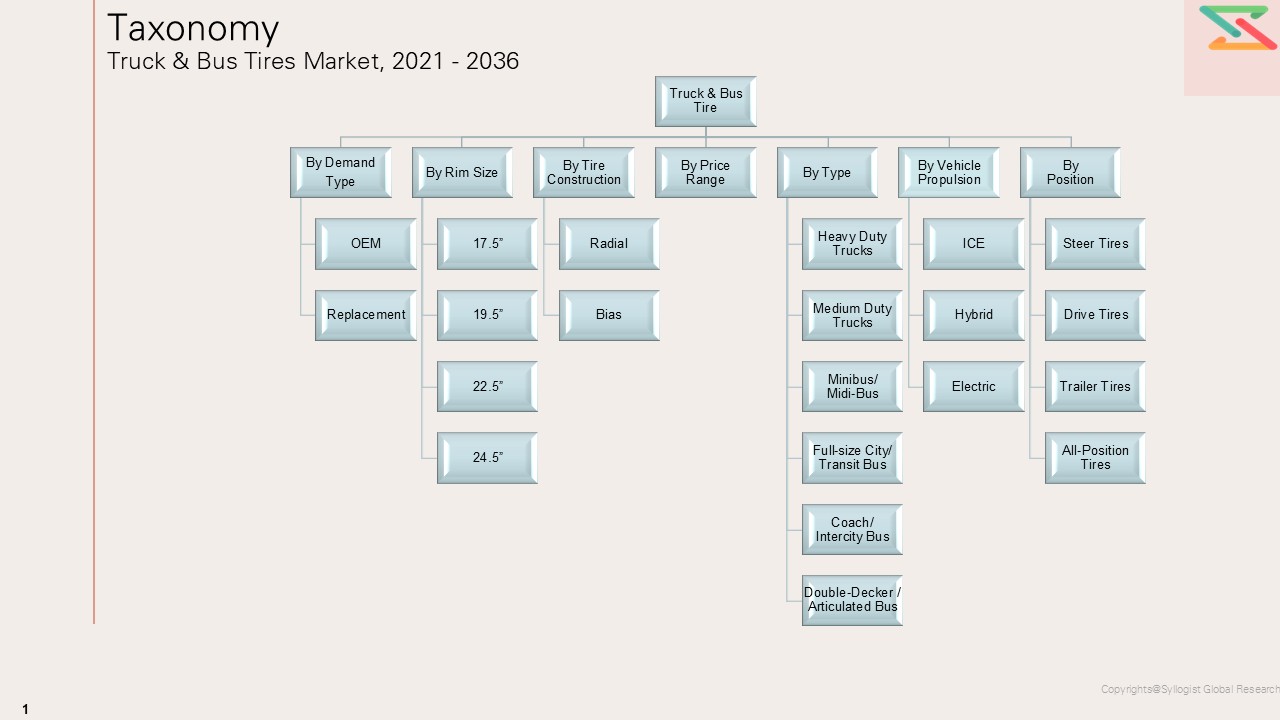

Market Segmentation

- Segmentation by Demand Type

- OEM

- Replacement

- Segmentation by Rim Size

- 17.5

- 19.5

- 22.5

- 24.5

- Segmentation by Tire Construction

- Radial

- Bias

- Segmentation by Type

- Heavy Duty Trucks

- Medium Duty Trucks

- Minibus/Midi-Bus

- Full-size City/Transit Bus

- Coach/Intercity Bus

- Double-Decker / Articulated Bus

- Segmentation by Vehicle Propulsion

- ICE

- Hybrid

- Electric

- Segmentation by Position

- Steer Tires

- Drive Tires

- Trailer Tires

- All-Position Tires

All market revenues are presented in USD and volume in units

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Truck & Bus Tire Market, including revenue size, volume sales, and average selling prices, with performance segmentation across Tire Type (Steer, Drive, Trailer, All-Position, Mixed Service, On-/Off-Road), Demand Category (OEM vs. Replacement), Rim Size (Up to 20, 20.1–22.5, 22.6–24, Above 24), Tire Construction (Radial vs. Bias), Vehicle Class (Light Truck, Medium Truck, Heavy Truck, Bus, Coach), Price Segment (Budget, Mid-Range, Premium), Sales Channel (OEM Supply, Authorized Dealers, Independent Dealers, Fleet Accounts, Online / Digital Platforms), and Application / Usage (Long-Haul, Regional Haul, Urban Delivery, Mining / Construction Support, Intercity Bus, City Bus, Winter / All-Weather, Fuel-Efficient / Low Rolling Resistance)?

- How do supply–demand fundamentals vary across key regions and major commercial vehicle markets, and what role do truck and bus production, vehicle parc growth, freight activity, passenger transport demand, fleet replacement cycles, retreading penetration, axle-load intensity, road infrastructure quality, and regulatory standards for safety, emissions, and fuel efficiency play in shaping regional competitiveness, alongside local manufacturing capability in tire compounding, casing durability, tread design, curing, reinforcement materials integration, and downstream distribution networks, as well as procurement structures across OEM supply contracts, fleet tenders, replacement distributors, dealer networks, and retread ecosystems?

- In what ways are raw material and energy price volatility and lead-time constraints (Natural Rubber, Synthetic Rubber, Carbon Black, Steel Cord, Textile Reinforcements, Silica, Petrochemical Derivatives, and Specialty Additives) influencing production costs, pricing strategies, supplier margins, delivery schedules, and profitability, especially for premium radial truck tires, long-haul tires, fuel-efficient / low-rolling-resistance tires, high-load bus tires, and retreadable casing-focused product lines?

- Who are the leading global and regional truck & bus tire manufacturers, retread-focused suppliers, private-label players, and distribution companies, and how do they benchmark across durability, mileage, retreadability, rolling resistance, load-carrying capacity, wet and dry grip, heat resistance, casing strength, fuel efficiency, price competitiveness, brand strength, regulatory compliance, and portfolio breadth across standalone tire supply versus value-added offerings such as fleet management programs, tire monitoring systems, mileage guarantees, roadside assistance, retreading support, and dealer service solutions?

- What strategic insights emerge from primary discussions with tire manufacturers, OEMs, fleet operators, replacement dealers, distributors, retreaders, logistics companies, and commercial vehicle aftermarket participants regarding demand shifts toward high-mileage tires, fuel-efficient / low-rolling-resistance products, premium radialization, smart tire monitoring adoption, retreadable casing demand, regional sourcing strategies, inventory and lead-time management, and key purchase criteria such as price competitiveness, total cost of ownership, mileage performance, durability, load capacity, brand trust, retreadability, safety performance, and supply assurance?

- Market Overview

- Product Overview

- Research Methodology

- Executive Summary

- Market Dynamics

- Market Dynamics (Drivers, Restraints, Opportunities, Challenges, Porter’s Five Forces Analysis, PESTLE Analysis)

- Market Trends & Developments

- Risk Assessment Framework

- Political / Geopolitical Risk

- Feedstock Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Truck and Bus Tires Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Demand Type

- OEM

- Replacement

- Market Size & Forecast by Rim Size

- 17.5”

- 19.5”

- 22.5”

- 24.5”

- Market Size & Forecast by Tire Construction

- Radial

- Bias

- Market Size & Forecast by Type

- Heavy Duty Trucks

- Medium Duty Trucks

- Minibus/Midi-Bus

- Full-size City/Transit Bus

- Coach/Intercity Bus

- Double-Decker / Articulated Bus

- Market Size & Forecast by Vehicle Propulsion

- ICE

- Hybrid

- Electric

- Market Size & Forecast by Position

- Steer Tires

- Drive Tires

- Trailer Tires

- All-Position Tires

- Asia-Pacific Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

- Europe Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

- North America Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

- Latin America Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

- Middle East & Africa Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

- Country Wise* Truck and Bus Tires Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Demand Type

- By Rim Size

- By Tire Construction

- By Type

- By Vehicle Propulsion

- By Position

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, United Kingdom, Japan, Australia, France, The Netherlands, Singapore, India, Canada, Brazil, South Korea, UAE, Sweden, Ireland, Malaysia, Indonesia, Italy, Poland, Mexico, South Africa, Saudi Arabia, Finland, Thailand, Chile, Norway, Kenya, Vietnam, Qatar

- Technology & Innovation Analysis

- Tire Technology Evolution

- Smart & Connected Tires

- Airless / Non-Pneumatic Tires (NPT)

- Sustainable Tire Technologies

- Tire Compound & Material Innovation

- Manufacturing Technology

- Automation & Robotics in Tire Manufacturing

- AI-Based Quality Control

- 3D Printing in Tire Prototyping

- Industry 4.0 Adoption in Tire Plants

- Value Chain & Supply Chain Analysis

- Raw Material Suppliers

- Tire Manufacturers

- Distributors & Wholesalers

- Retailers & Fitment Centers

- OEM Supply Chain

- End Users (Consumers)

- Ecosystem Map

- Supply Chain Analysis

- Natural Rubber Supply (Southeast Asia Dependency)

- Synthetic Rubber & Petrochemical Inputs

- Carbon Black Supply Chain

- Steel Cord & Textile Cord

- Supply Chain Risk & Disruption Analysis

- Trade Flow Analysis

- Major Tire Exporting Countries

- Major Tire Importing Countries

- Tariff & Trade Barrier Analysis

- Raw Material Analysis

- Natural Rubber

- Global Production & Supply Dynamics

- Key Producing Countries (Thailand, Indonesia, Vietnam)

- Price Trend Analysis

- Supply Risk & Alternative Sourcing

- Synthetic Rubber

- Styrene-Butadiene Rubber (SBR)

- Butadiene Rubber (BR)

- Key Producers & Price Trends

- Petrochemical Feedstock Dependency

- Carbon Black

- Role in Tire Performance

- Price Trends & Supply Dynamics

- Recovered / Recycled Carbon Black (RCB) Emergence

- Silica

- Growing Use as Carbon Black Replacement

- Performance Benefits (Rolling Resistance, Wet Grip)

- Key Silica Suppliers

- Steel Cord & Textile Reinforcement

- Steel Cord for Belts & Bead

- Polyester, Nylon, Aramid Fiber Usage

- Key Suppliers

- Raw Material Cost Structure

- % Breakdown of Raw Material in Tire Cost

- Sensitivity Analysis, Impact of Rubber Price on Tire Pricing

- Natural Rubber

- Pricing Analysis

- Average Selling Price by Tier

- Premium Tier Pricing

- Mid-Tier Pricing

- Value / Economy Tier Pricing

- Price Trend Analysis (2021–2036)

- Sales & Distribution Channel Analysis

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Revenue & Cooling Segment Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Recommendations

- For Tire Manufacturers

- Product & Technology Strategy

- Ev Tire Portfolio Prioritization

- Sustainability & Circular Economy Strategy

- Geographic Expansion Priorities

- M&A & Partnership Strategy

- For OEMs & Automakers

- EV Tire Specification & Homologation Strategy

- Tire Supplier Diversification

- Sustainable Tire Procurement Commitments

- For Aftermarket & Retail Players

- E-Commerce & Omnichannel Strategy

- Private Label Tire Strategy

- Tire-As-A-Service (Taas) Opportunity

- For Investors & Private Equity

- High-Priority Investment Themes

- Smart Tire & Sustainable Material Startups

- Geographic Investment Priorities

- Risk Considerations

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2023–2036)

- For Tire Manufacturers