Market Definition

The Global Light Commercial Vehicle Tire Market encompasses the design, development, manufacturing, distribution, and aftermarket supply of tires engineered specifically for light commercial vehicles, a category that includes cargo vans, panel vans, minivans, pickup trucks used for commercial purposes, small delivery trucks, and multi-purpose vehicles with a gross vehicle weight rating typically not exceeding 3.5 tonnes and, in certain market classifications, up to 6 tonnes. Light commercial vehicle tires are purpose-engineered to operate under demanding conditions that distinguish them structurally and functionally from passenger car tires, including higher sustained payload loads, frequent urban stop-start duty cycles, mixed on-road and light off-road operation, prolonged highway running in long-haul last-mile delivery applications, and the lateral stresses imposed by loading and unloading operations at kerb edges and delivery bay ramps. The market encompasses the full product spectrum of light commercial vehicle tire types, including summer, winter, and all-season radial tires in standard load and reinforced construction ratings, all-terrain and highway-terrain tires for pickup trucks and dual-use commercial vehicles, run-flat tires for fleet vehicles requiring uninterrupted operational capability, and emerging airless or non-pneumatic tire technologies in early commercial development stages. The tire architecture encompasses the tread compound formulation, steel and textile belt and carcass reinforcement structures, sidewall construction and load-carrying capability, bead assembly, and inner liner, collectively engineered to meet regulatory requirements for load index, speed rating, rolling resistance, wet grip, and external rolling noise under European, American, Chinese, and other national type-approval frameworks. Key market participants include global and regional tire manufacturers operating original equipment and replacement market supply channels, automotive OEMs specifying tires for new vehicle production programs, fleet operators and logistics companies managing large commercial vehicle tire procurement, tire wholesale distributors and retail fitment networks, and raw material suppliers of synthetic rubber, natural rubber, carbon black, silica, and specialty chemicals whose commodity price dynamics directly govern tire manufacturing cost structures.

Market Insights

The global light commercial vehicle tire market is experiencing a period of sustained and structurally reinforced demand growth, underpinned by the convergence of three powerful macroeconomic and industry-specific trends: the continued global expansion of e-commerce and last-mile delivery infrastructure generating an unprecedented increase in light commercial vehicle fleet sizes across urban and suburban delivery networks, the sustained recovery and growth of construction, trade, and services sectors driving commercial van and pickup truck utilization rates to historically elevated levels in emerging and developed economies alike, and the accelerating fleet electrification of light commercial vehicles which, while transforming tire technology requirements, is simultaneously expanding the total installed tire base through the addition of electric vehicle-specific tire variants that carry higher unit values and faster replacement cycles than equivalent conventional tire fitments. The global light commercial vehicle parc reached approximately 310 million units in 2025, generating a replacement tire demand base of approximately 620 million tires annually when average tire service life and replacement intervals across the global light commercial vehicle fleet are applied, with this replacement market constituting approximately 78% of total light commercial vehicle tire revenues and providing a structurally resilient demand foundation that is substantially less sensitive to new vehicle production fluctuations than the original equipment supply channel. The global light commercial vehicle tire market was valued at approximately USD 34.7 billion in 2025 and is projected to reach USD 52.1 billion by 2034, advancing at a compound annual growth rate of 4.6% over the forecast period from 2027 to 2034, driven by fleet expansion in Asia-Pacific and Latin American emerging markets, increasing tire content value from electrification-specific tire adoption, and a sustained premiumization trend as fleet operators prioritize total cost of ownership performance over initial tire acquisition price across high-utilization urban delivery fleets.

The explosive growth of e-commerce and the structural transformation of last-mile delivery logistics it has generated represent the single most consequential demand driver reshaping both the volume and the technical performance requirements of the global light commercial vehicle tire market, as the operating duty cycle of an urban delivery van in a high-density e-commerce distribution application is fundamentally more demanding on tire wear, load carrying, and fuel efficiency performance than the usage patterns that defined the light commercial vehicle segment before the e-commerce era. A light commercial vehicle engaged in urban last-mile delivery operations in a major metropolitan market may complete between 80 and 150 individual delivery stops per shift, accumulating annual mileage of 35,000 to 50,000 kilometers under conditions of continuous low-speed stop-start operation, frequent maximum load cycling as the vehicle transitions between fully loaded outbound journeys and progressively lighter inbound returns, and repeated lateral scuffing forces from kerb contact during pedestrian zone delivery maneuvers, collectively generating tire wear rates that are 30% to 45% faster than comparable highway-biased commercial van operation and driving replacement frequency intervals that are materially shorter than those of conventionally deployed light commercial vehicle fleets. The tire performance requirements of high-intensity urban delivery operations have created commercial demand for purpose-engineered urban delivery van tire products incorporating wear-optimized tread compound formulations, reinforced sidewalls capable of withstanding repeated kerb contact without structural damage, high load index ratings supporting maximum payload capacity for extended periods, and low rolling resistance characteristics that contribute to fleet fuel cost and carbon emission reduction objectives, representing a distinct and commercially growing tire product sub-category that major tire manufacturers are addressing through dedicated urban delivery van tire range launches that command premium pricing relative to conventional all-season commercial van tire products.

The accelerating adoption of battery electric light commercial vehicles is creating a structurally distinct and commercially significant technology differentiation opportunity within the light commercial vehicle tire market, as electric vans and pickup trucks impose tire performance requirements in terms of load-bearing capability, rolling resistance sensitivity, acoustic noise management, and wear resistance under high instantaneous torque loading that differ materially from those of equivalent diesel or petrol-powered vehicles and that cannot be optimally satisfied by conventional commercial van tires designed without explicit consideration of the electric powertrain’s performance characteristics. Battery electric light commercial vehicles are typically 300 to 600 kilograms heavier than equivalent internal combustion engine models due to the mass of the traction battery pack, requiring tires with higher load indices and reinforced carcass structures to safely carry the additional vehicle kerb weight within the tire’s rated load capacity at the inflation pressures appropriate for the electric vehicle’s suspension geometry and weight distribution. Electric van powertrains deliver their maximum torque instantaneously from standstill, generating tread surface shear forces during acceleration events that are substantially higher than those produced by diesel powertrains of equivalent power output and that accelerate shoulder tread wear on conventional commercial van tire compounds not formulated to resist the specific wear mode associated with high-torque electric motor drive. Rolling resistance assumes heightened commercial importance in electric vehicle tire specifications because every percentage point reduction in tire rolling resistance coefficient directly translates into an approximately 0.3% to 0.5% improvement in electric vehicle range under combined cycle conditions, a relationship that fleet operators managing large electric van deployments are acutely aware of and that is driving specification of low rolling resistance tire variants even at a modest premium over standard commercial van tire pricing, creating a higher-value product category that supports margin improvement for tire manufacturers capable of delivering electric vehicle-optimized commercial tire performance at commercially competitive price points.

From a regional standpoint, Asia-Pacific dominates the global light commercial vehicle tire market by both volume and production capacity, with China constituting the world’s largest individual light commercial vehicle market, producing approximately 4.8 million light commercial vehicles annually and operating a domestic light commercial vehicle parc exceeding 105 million units that generates the world’s single largest national light commercial vehicle tire replacement demand pool. China’s domestic tire manufacturing industry, anchored by large-scale manufacturers operating multiple production facilities with aggregate capacity exceeding 600 million passenger and commercial tires annually, supplies both the domestic replacement market and significant export volumes to emerging markets across Southeast Asia, the Middle East, Africa, and Latin America at price points that consistently undercut the manufactured cost of equivalent products from European and North American tire producers, maintaining competitive pressure on pricing across the global light commercial vehicle tire market. Europe represents the second-largest regional market by revenue, characterized by the highest share of premium and branded tire fitments in the light commercial vehicle replacement channel, the most stringent regulatory environment for tire rolling resistance, wet grip, and noise performance under the EU Tire Labeling Regulation, and the most advanced transition toward electric light commercial vehicle fleets, with the European Union’s urban zero-emission zone mandates driving accelerated electric van adoption in major European cities that is generating early commercial demand for electric vehicle-optimized light commercial vehicle tire specifications. North America, anchored by the United States, represents a structurally distinct market in which pickup trucks configured for commercial use account for a disproportionately large share of light commercial vehicle tire demand, with the all-terrain and highway-terrain tire segment for pickup trucks and commercial SUVs constituting the highest per-unit revenue category within the North American light commercial vehicle tire market and supporting above-average gross margin structures for both domestic and international tire manufacturers serving this segment.

Key Drivers

E-Commerce Expansion and the Structural Growth of Last-Mile Delivery Fleets Driving Unprecedented Light Commercial Vehicle Tire Volume Demand

The sustained global expansion of e-commerce retail, which reached approximately USD 6.1 trillion in gross merchandise value in 2025 and is projected to exceed USD 9.4 trillion by 2030, is generating a structural and self-reinforcing demand expansion for light commercial vehicle tires through its direct causative link to light commercial vehicle fleet growth, elevated vehicle utilization intensity, and accelerated tire replacement cycles that collectively produce a volume demand increment of exceptional commercial durability. The number of parcels delivered globally via last-mile light commercial vehicle operations exceeded 315 billion units in 2025, a figure that logistics industry analyses project to approach 480 billion annually by 2030 as e-commerce penetration deepens across emerging market consumer populations in Southeast Asia, India, Latin America, and Sub-Saharan Africa that are currently in early e-commerce adoption phases. Last-mile logistics operators including Amazon Logistics, DHL, FedEx, UPS, Cainiao, JD Logistics, and a growing ecosystem of regional and hyperlocal delivery platform companies are collectively adding tens of thousands of light commercial vehicles to their global fleets annually, with total light commercial vehicle fleet procurement by the top 20 global logistics operators estimated at approximately 680,000 new units in 2025, each requiring four to six tires at the point of entry into service and generating replacement tire demand throughout operational service lives of four to seven years. The combination of fleet size growth and elevated replacement frequency in high-intensity urban delivery applications creates a compounding volume demand expansion for light commercial vehicle tires that is structurally independent of broader macroeconomic conditions and that provides tire manufacturers serving the fleet channel with a relatively predictable and contractually accessible demand stream amenable to long-term supply agreement structures.

Fleet Electrification and the Premium Tire Content Value Opportunity Created by Electric Light Commercial Vehicle-Specific Performance Requirements

The accelerating electrification of light commercial vehicle fleets is creating a commercially significant tire market value expansion opportunity that operates independently of unit volume growth, driven by the higher average selling price of electric vehicle-optimized light commercial vehicle tire variants relative to equivalent conventional commercial van tire products and by the faster replacement cycle of electric vehicle tires attributable to the elevated wear rate generated by high instantaneous torque loading and higher vehicle kerb weight. Major fleet operators including Amazon, DHL Express, Royal Mail, La Poste, and Deutsche Post have collectively committed to procuring over 350,000 electric light commercial vehicles annually by 2027 as components of their corporate fleet decarbonization programs, with each electric van requiring purpose-specified tires that command average selling price premiums of 12% to 22% relative to equivalent diesel van tire fitments, reflecting the additional engineering investment in wear-optimized compound formulations, reinforced carcass structures, and acoustic optimization required to meet the specific performance demands of electric powertrain integration. The tire industry is responding to this electrification-driven demand signal through targeted new product development, with all major global tire manufacturers having launched or announced dedicated electric commercial vehicle tire product lines by 2025, positioning the electric light commercial vehicle tire as a structurally premium product category within the broader light commercial vehicle tire portfolio that supports both revenue growth and gross margin improvement relative to the conventional commercial van tire business. The faster replacement cycle of electric light commercial vehicle tires, estimated at 20% to 30% shorter service life relative to conventional commercial van tire fitments of equivalent specification when operated on identical urban delivery duty cycles, further amplifies the per-vehicle tire revenue generation over a fleet vehicle’s operational service life, creating a structurally higher lifetime tire revenue stream per electric vehicle relative to its internal combustion engine equivalent.

Infrastructure Development, Construction Activity, and Commercial Vehicle Fleet Expansion in High-Growth Emerging Markets

The sustained investment in infrastructure development, urbanization, and industrial capacity expansion across high-growth emerging markets in Asia-Pacific, the Middle East, Africa, and Latin America is generating robust structural growth in light commercial vehicle fleet sizes and operational utilization across these geographies, creating durable volume demand expansion for light commercial vehicle tires that is progressing through an earlier and more sustained growth phase than the mature market dynamics characterizing North American and European light commercial vehicle tire demand. India’s infrastructure investment program, which allocated approximately USD 134 billion toward road, highway, and urban infrastructure development in fiscal year 2024-25, is supporting the expansion of commercial construction and materials transport activity that drives light commercial vehicle fleet growth across the country’s 22 million-unit light commercial vehicle parc, which is growing at approximately 7.8% annually and constitutes one of the world’s fastest-expanding light commercial vehicle tire replacement markets by incremental volume. Southeast Asian economies including Indonesia, Vietnam, Thailand, and the Philippines are experiencing rapid light commercial vehicle fleet expansion driven by the growth of manufacturing export sectors, the development of modern retail and food distribution supply chains, and the expansion of ride-hailing and commercial delivery platform ecosystems that collectively generate light commercial vehicle parc growth rates of 5% to 9% annually, creating compounding tire replacement demand that is attracting investment in local tire distribution infrastructure from both global premium tire brands and regional value-tier tire manufacturers competing for fleet procurement contracts in price-sensitive emerging market commercial vehicle segments.

Key Challenges

Raw Material Price Volatility and Supply Chain Concentration Risk Across Natural Rubber, Synthetic Rubber, and Carbon Black Inputs

The global light commercial vehicle tire manufacturing industry is structurally exposed to commodity price volatility across its primary raw material inputs, natural rubber, synthetic rubber derived from butadiene and styrene petrochemical feedstocks, carbon black produced from petroleum residues, and silica, whose prices are governed by independent supply and demand dynamics that can produce simultaneous adverse price movements imposing compounding margin pressure on tire manufacturers whose ability to pass through raw material cost increases to fleet customers operating under fixed multi-year tire supply contracts is constrained by both commercial relationship dynamics and competitive market pricing pressure from lower-cost regional manufacturers. Natural rubber, which constitutes approximately 30% to 40% of the rubber content of a typical light commercial vehicle tire by weight and is produced overwhelmingly in Thailand, Indonesia, and Malaysia, three countries that collectively account for approximately 67% of global natural rubber output, is subject to price volatility driven by monsoon rainfall patterns affecting latex yield, disease incidence in plantation stocks, smallholder planting and replanting decisions responding to multi-year price cycles, and speculative trading activity in rubber futures markets that can amplify price movements beyond what fundamental supply and demand dynamics would generate. The concentration of natural rubber production in a geographically narrow band of Southeast Asian countries creates supply security vulnerability for tire manufacturers whose production facilities are distributed across multiple continents, as weather events, disease outbreaks, labor disputes, or geopolitical disruptions affecting Thai and Indonesian rubber production can generate supply shortfalls that are difficult to address through short-term supplier substitution given the limited geographic diversity of viable natural rubber sourcing alternatives at the volumes demanded by large-scale tire manufacturing operations.

Intensifying Price Competition from Low-Cost Asian Tire Manufacturers and the Margin Compression Affecting Premium Brand Producers in the Replacement Channel

The global light commercial vehicle tire replacement market is experiencing structural and intensifying price competition driven by the sustained capacity expansion and improving product quality of lower-cost tire manufacturers headquartered primarily in China, India, and South Korea, whose ability to manufacture light commercial vehicle tires meeting minimum regulatory performance thresholds at production costs substantially below those achievable in European or North American manufacturing facilities is enabling them to capture a growing share of fleet replacement tire procurement and independent tire distributor inventories across multiple regional markets simultaneously. Chinese tire manufacturers, operating at scale advantages derived from large domestic market volumes, lower labor costs, vertically integrated raw material supply relationships, and government-supported export financing programs, have achieved market share gains in the European, North American, and Middle Eastern light commercial vehicle tire replacement markets that would have been commercially inconceivable a decade ago, with Chinese-origin light commercial vehicle tires now representing an estimated 18% to 24% of total replacement tire volume in the European mid-market and value segments across key commercial tire sizes. The EU Tire Labeling Regulation’s mandatory performance labeling requirement, while designed to inform purchase decisions based on rolling resistance, wet grip, and noise performance, has paradoxically reduced the purchasing barriers for lower-cost tire brands by providing consumers and fleet operators with a regulatory-validated performance comparison framework that enables them to identify lower-cost tire brands achieving equivalent label grades to premium competitors, thereby legitimizing value-tier procurement decisions in fleet procurement processes that previously defaulted to established premium brand specifications as a proxy for performance assurance in the absence of transparent comparative data.

Regulatory Complexity Across Multiple Jurisdictions and the Engineering Investment Required for Type-Approval Compliance Across Diverse Global Markets

Light commercial vehicle tire manufacturers serving global markets must navigate a regulatory compliance landscape of increasing complexity and divergence, in which the specific performance thresholds, test methodologies, labeling requirements, and type-approval certification processes applicable to light commercial vehicle tires differ materially across the European Union, United States, China, India, Japan, Brazil, and other significant markets, compelling tire manufacturers to maintain parallel product engineering, testing, and certification programs for regulatory variants that impose development cost, product portfolio complexity, and supply chain fragmentation burdens that fall disproportionately on manufacturers without the scale to amortize regulatory compliance investment efficiently across large production volumes. The European Union Tire Labeling Regulation 2020/740 and its associated UN Regulation ECE R117 wet grip, rolling resistance, and noise performance thresholds are calibrated at levels that require genuine engineering investment in tread compound and construction to achieve competitive label grades, while simultaneously differing from the equivalent performance standards applied in the United States under the National Highway Traffic Safety Administration tire grading system, the Chinese mandatory standard GB 9743, and the Indian Automotive Industry Standard AIS-142 in ways that require tire designs to be specifically optimized or validated for each major market’s regulatory framework rather than achieving simultaneous multi-market compliance with a single globally standardized product specification. The anticipated implementation of mandatory tire pressure monitoring system compatibility requirements, extended end-of-life tire producer responsibility obligations, and recycled rubber content mandates in emerging EU and national legislative proposals will further increase the regulatory compliance engineering and administrative burden for light commercial vehicle tire manufacturers through the forecast period, adding cost and complexity to tire development programs already managing the simultaneous challenge of electrification-driven product portfolio expansion.

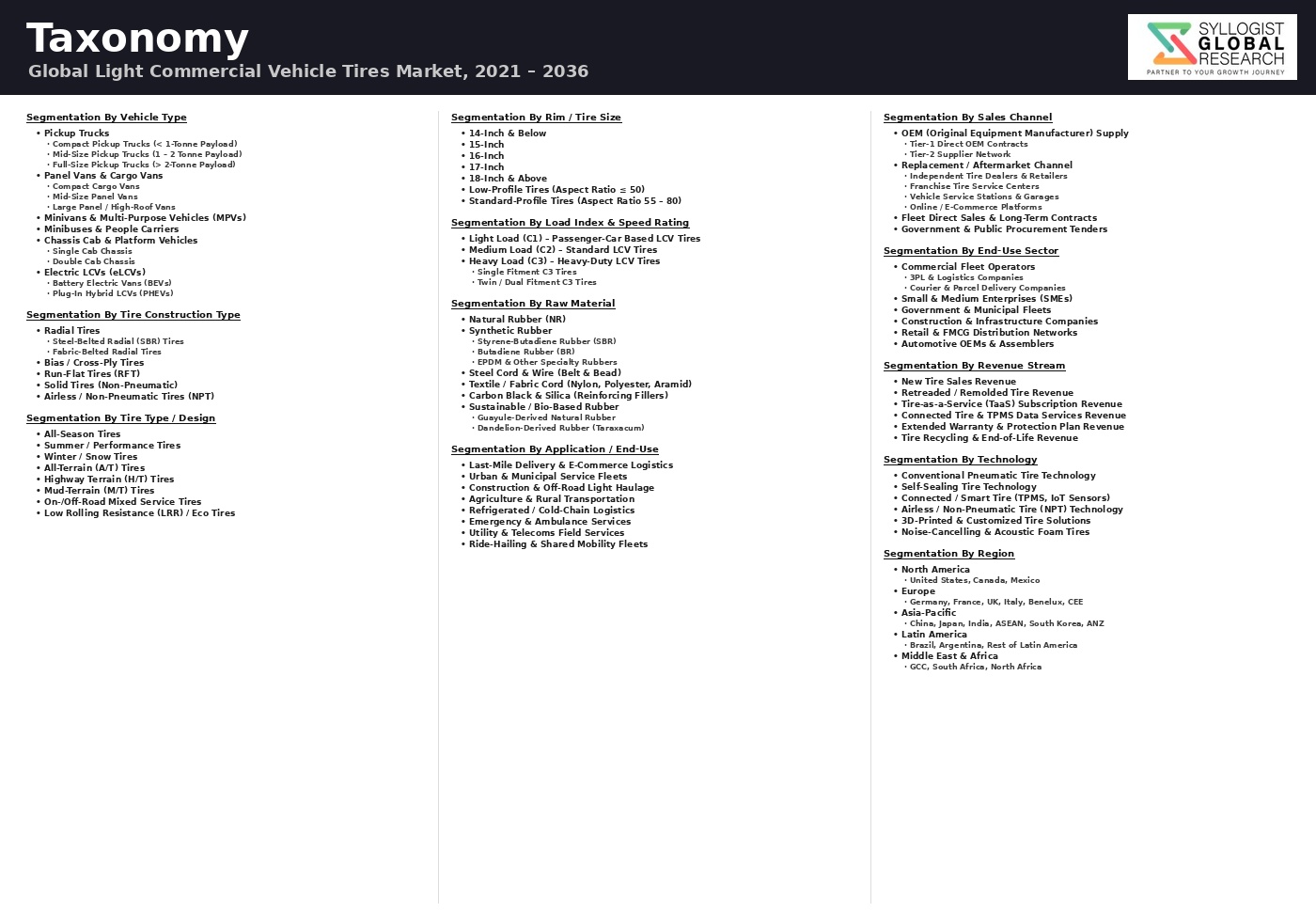

Market Segmentation

- Segmentation By Product Type

- Summer Tires

- Winter Tires

- All-Season Tires

- All-Terrain Tires

- Highway-Terrain Tires

- Run-Flat Tires

- Mud-Terrain Tires

- All-Weather Tires

- Others

- Segmentation By Construction Type

- Radial Tires (Standard Load)

- Radial Tires (Reinforced / Extra Load)

- Bias-Ply Tires

- Non-Pneumatic and Airless Tires (Developmental)

- Others

- Segmentation By Tire Size

- 14-Inch Rim Diameter

- 15-Inch Rim Diameter

- 16-Inch Rim Diameter

- 17-Inch Rim Diameter

- 18-Inch and Above Rim Diameter

- Segmentation By Vehicle Type

- Cargo Vans and Panel Vans

- Pickup Trucks (Commercial Use)

- Minivans and Multi-Purpose Commercial Vehicles

- Small Delivery Trucks and Cab-Over Vehicles

- Refrigerated and Temperature-Controlled Vans

- Others

- Segmentation By Propulsion Type

- Internal Combustion Engine (ICE) Light Commercial Vehicles

- Battery Electric Light Commercial Vehicles (eLCV)

- Plug-In Hybrid Light Commercial Vehicles (PHEV)

- Mild Hybrid Light Commercial Vehicles (MHEV)

- Compressed Natural Gas (CNG) Light Commercial Vehicles

- Others

- Segmentation By Sales Channel

- Original Equipment (OE) Supply to Vehicle Manufacturers

- Replacement Market, Branded Tire Retail and Fitment Centers

- Replacement Market, Fleet Direct Supply Agreements

- Replacement Market, Independent Tire Wholesalers and Distributors

- Online Retail and E-Commerce Tire Platforms

- Others

- Segmentation By Load Index Rating

- Load Index Below 100

- Load Index 100 to 109

- Load Index 110 to 119

- Load Index 120 and Above

- Segmentation By Tread Compound Technology

- Standard Rubber Compound

- Silica-Enhanced Low Rolling Resistance Compound

- EV-Optimized Wear-Resistant Compound

- Severe Service and Cut-Resistant Compound

- Others

- Segmentation By End User

- E-Commerce and Last-Mile Delivery Fleets

- Construction and Building Materials Transport

- Food and Beverage Distribution Fleets

- Retail and FMCG Supply Chain Operators

- Government and Municipal Fleet Operators

- Rental and Leasing Companies

- Individual Commercial Vehicle Owners and Small Businesses

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Light Commercial Vehicle Tire Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, summer, winter, all-season, all-terrain, and run-flat, and by sales channel, original equipment versus replacement market, to enable tire manufacturers, fleet operators, investors, and distribution channel participants to identify the highest-growth product categories, channel configurations, and geographic markets warranting priority investment and commercial focus across the forecast period?

- How is the accelerating adoption of battery electric light commercial vehicles across European, North American, and Asia-Pacific fleet operators reshaping tire performance specification requirements, average selling price structures, and replacement interval economics within the light commercial vehicle tire market, and what is the projected revenue premium and total addressable market size of EV-optimized light commercial vehicle tire variants, encompassing reinforced load construction, high-torque wear-resistant tread compounds, and low rolling resistance formulations, relative to conventional commercial van tire products through 2034?

- What is the current and projected market share distribution among the leading global premium tire manufacturers, established regional producers, and lower-cost Asian tire brands within the light commercial vehicle replacement tire channel across the European Union, North America, China, India, and key emerging markets in Southeast Asia, the Middle East, and Latin America, and how are competitive dynamics, including pricing pressure from Chinese manufacturers, EU Tire Labeling Regulation grade competition, and fleet procurement contract strategies, expected to reshape brand positioning and manufacturer market share through the forecast period?

- How are tightening EU Tire Labeling Regulation 2020/740 rolling resistance, wet grip, and external noise performance requirements, alongside emerging mandatory recycled content obligations, end-of-life tire producer responsibility frameworks, and equivalent regulatory developments in China, India, and the United States, expected to influence light commercial vehicle tire compound technology investment priorities, product development timelines, and manufacturing cost structures for both premium and value-tier tire producers serving global replacement and OE supply markets through 2034?

- Who are the leading global and regional light commercial vehicle tire manufacturers, specialty electric vehicle tire developers, fleet tire management service providers, and raw material suppliers of natural rubber, synthetic rubber, carbon black, and silica currently defining the competitive landscape of the global light commercial vehicle tire market, and what are their respective product portfolio strategies, manufacturing capacity expansion programs, electric vehicle tire development roadmaps, fleet channel partnership structures, and strategic responses to raw material cost volatility and pricing competition from lower-cost regional manufacturers across the forecast horizon?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Processing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price & Supply Risk

- Regulatory & Compliance Risk

- Technology & Product Risk

- Market & Competitive Risk

- Environmental & Climate Risk

- Regulatory Framework & Standards

- Global LCV Tire Safety & Performance Standards

- Regional Regulatory Standards

- Environmental & Sustainability Regulations

- Labelling, Marking & Traceability Standards

- Global Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Tire Type

- Radial Tires

- Steel Belt Radial (SBR) LCV Tires

- All-Steel Radial LCV Tires

- Fabric Belt Radial LCV Tires

- Bias / Cross-Ply Tires

- Conventional Bias LCV Tires

- Bias-Belted LCV Tires

- Specialty Tires

- Run-Flat LCV Tires (Extended Mobility Tires – EMT)

- Self-Sealing LCV Tires

- All-Terrain (A/T) LCV Tires

- Mud-Terrain (M/T) LCV Tires

- Winter / Snow LCV Tires

- All-Season / All-Weather LCV Tires

- Highway Terrain (H/T) LCV Tires

- EV-Specific LCV Tires

- Airless / Non-Pneumatic LCV Tires (Emerging)

- Market Size & Forecast by Vehicle Type

- Light Vans (Panel Van / Cargo Van)

- Compact Light Van (< 2 Tonnes GVW)

- Medium Light Van (2–3 Tonnes GVW)

- Large Light Van (3–3.5 Tonnes GVW)

- Pickup Trucks / Light Utility Trucks

- Compact Pickup Truck

- Mid-Size Pickup Truck

- Full-Size Light Pickup Truck

- Minibus / Minivan (Passenger-Carrying LCV)

- Crew Cab & Multi-Purpose LCV

- Chassis Cab & Platform LCV

- Tipper / Dropside Chassis LCV

- Luton Box / High Roof Van Chassis LCV

- Refrigerated / Cold Chain Van LCV

- Electric Light Commercial Vehicle (eLCV)

- Electric Cargo Van

- Electric Pickup Truck

- Electric Minibus / People Carrier

- Market Size & Forecast by Rim Size

- 13-Inch Rim

- 14-Inch Rim

- 15-Inch Rim

- 16-Inch Rim

- 17-Inch Rim

- 18-Inch Rim

- 19-Inch & Above Rim

- Market Size & Forecast by Load Index

- Single Load Index (SL) LCV Tires

- Extra Load / Reinforced (XL / C-Type) LCV Tires

- C-Type 6-Ply Rating LCV Tires

- C-Type 8-Ply Rating LCV Tires

- Light Truck (LT) Rated LCV Tires (US Market)

- Market Size & Forecast by Speed Rating

- P-Rating (150 kph)

- Q-Rating (160 kph)

- R-Rating (170 kph)

- S-Rating (180 kph)

- T-Rating (190 kph)

- H-Rating & Above (210 kph+)

- Market Size & Forecast by Season / Application

- Summer / Highway LCV Tires

- All-Season / All-Weather LCV Tires

- Winter / Snow LCV Tires

- All-Terrain LCV Tires (On/Off Road)

- Mud-Terrain LCV Tires (Off-Road Dominant)

- On-Road / Urban Delivery LCV Tires

- Cold Climate & Arctic LCV Tires

- Market Size & Forecast by Technology

- Conventional Pneumatic LCV Tires

- Low Rolling Resistance (LRR) LCV Tires

- Run-Flat Technology (RFT) LCV Tires

- Self-Sealing Technology LCV Tires

- Noise-Reducing / Acoustic Foam LCV Tires

- EV-Optimised LCV Tires

- Smart / Connected Tires with Embedded IoT / TPMS Sensors

- Retreaded LCV Tires (Remould / Retread)

- Airless / Non-Pneumatic LCV Tires (Emerging)

- Market Size & Forecast by Demand Channel

- Original Equipment (OE) LCV Tire Market

- Direct OEM Supply to Light Commercial Vehicle Manufacturers

- OE Fitment to Electric LCV (eLCV) Platforms

- Replacement / Aftermarket LCV Tire Market

- Dealer & Tire Retail Chain Replacement

- Online / E-Commerce Tire Retail Replacement

- Direct Fleet Supply & Fleet Tire Management Programme

- Automotive Service Centre & Fast-Fit Chain Replacement

- Retreaded LCV Tire Market

- Pre-Cure Retreaded LCV Tires

- Mold-Cure (Hot-Cure) Retreaded LCV Tires

- Market Size & Forecast by End-Use Sector

- Last-Mile & Urban Parcel Delivery (E-Commerce Logistics)

- Cold Chain & Refrigerated Goods Transport

- Construction, Building & Infrastructure

- Agriculture & Rural Transport

- Passenger Transport & Shuttle Services

- Utility, Maintenance & Field Service Operations

- Rental & Leasing Fleet

- Emergency Services, Government & Municipal Fleet

- Others (Catering, Hospitality, Moving & Removal Services)

- Market Size & Forecast by Distribution Channel

- Manufacturer-Owned Retail Network & Flagship Stores

- Independent Tire Dealers & Regional Wholesalers

- Multi-Brand Fast-Fit Chains & Auto Service Centres

- OEM-Authorised Dealership Service Departments

- Online / E-Commerce Tire Platforms (B2C & B2B)

- Petrol Station & Superstore Tire Services

- Fleet Direct Supply & Key Account Management

- Original Equipment (OE) LCV Tire Market

- Light Vans (Panel Van / Cargo Van)

- Radial Tires

- North America Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

- Europe Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

- Asia-Pacific Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

- Latin America Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

- Middle East & Africa Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

- Country-Wise* Light Commercial Vehicle Tire Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Tire Type

- By Vehicle Type

- By Rim Size

- By Load Index

- By Season / Application

- By Technology

- By Demand Channel

- By End-Use Sector

- By Distribution Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Poland, Netherlands, Russia, China, Japan, India, South Korea, Australia, Indonesia, Thailand, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- LCV Tire Compound Technology

- LCV Tire Architecture & Construction Technology

- LCV Tire Tread Pattern Design Technology

- Smart Tire & Connected LCV Tire Technology

- LCV Tire Testing & Validation Technology

- Retreading Technology for LCV Tires

- Patent & IP Landscape in LCV Tire Technology

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain

- Compound Mixing & Component Preparation

- Tire Building, Curing & Finishing

- LCV Tire Testing & Quality Assurance

- OE Tire Supply to LCV Manufacturers

- Aftermarket Distribution & Logistics

- End-of-Life Tire Collection, Retreading & Recycling

- Pricing Analysis

- LCV Tire Pricing by Brand Tier

- LCV Tire Pricing by Tire Type & Technology

- OE vs. Aftermarket LCV Tire Pricing

- Raw Material Cost Impact on LCV Tire Pricing

- Regional LCV Tire Price Analysis

- Sustainability & Environmental Profile

- Environmental Impact of LCV Tire Lifecycle

- Sustainable Raw Material Initiatives

- Energy Efficiency & Decarbonisation in LCV Tire Manufacturing

- End-of-Life Tire (ELT) Management

- ESG Reporting & Sustainability Disclosure

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated)

- Top 10 Players Global LCV Tire Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Brand Tier, Region & Channel

- Player Classification

- Tier-1 Global LCV Tire Majors (Full Product Portfolio, Global Manufacturing & Distribution)

- Tier-2 Regional LCV Tire Manufacturers (Strong in Home Region, Limited Global Reach)

- Tier-3 Local & Private Label LCV Tire Producers (Developing Market Focus)

- Chinese LCV Tire Manufacturers (Global Export Scale)

- EV LCV Tire Specialists & New Entrants

- Retread & End-of-Life Tire Specialist Companies

- Competitive Analysis Frameworks

- Market Share Analysis by Volume, Value, Brand Tier & Geography

- Company Profile

- Company Overview & Headquarters

- LCV Tire Product Portfolio (Tire Lines, Sizes, Load Ratings, Seasonal Range)

- Key LCV OEM Customer Relationships & Homologation Status

- Manufacturing Footprint & LCV Tire Production Capacity

- Revenue (LCV Tire Segment) & Market Share

- R&D Investment & EV LCV Tire Technology Roadmap

- Distribution Network & Channel Strategy for LCV Aftermarket

- Recent Developments (New Product Launches, Capacity Expansions, Partnerships, M&A)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map (Price Positioning vs. Performance Tier)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix – By Tire Type, Vehicle Type, Technology & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Innovation Strategy

- Technology Investment & R&D Strategy

- Supply Chain & Manufacturing Strategy

- Commercial & Distribution Strategy

- Sustainability & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2027)

- Mid-term (2028–2031)

- Long-term (2032–2036)