Market Definition

The Global Automotive Thermal Management Systems Market encompasses the design, engineering, manufacturing, integration, and aftermarket servicing of all hardware, software, and control system components responsible for regulating, transferring, and dissipating thermal energy within and across the mechanical, electrical, and electronic subsystems of passenger vehicles, commercial vehicles, and off-highway equipment. Thermal management in the automotive context addresses the full spectrum of heat generation and thermal conditioning requirements that arise across a vehicle’s operational lifecycle, including engine and powertrain cooling, transmission fluid temperature regulation, exhaust heat recovery, battery pack and power electronics thermal conditioning in electrified vehicles, cabin climate control encompassing heating ventilation and air conditioning systems, and the thermal management of advanced driver assistance systems, onboard computing platforms, and high-voltage electrical distribution infrastructure. The market encompasses a broad array of system components and technologies, including liquid cooling circuits with water and glycol-based coolants, electric coolant pumps and electronically controlled thermostats, radiators and charge air coolers, heat exchangers and thermal energy storage units, refrigerant-based vapor compression systems for both cabin and battery conditioning, heat pumps operating across ambient temperature ranges, positive temperature coefficient heaters, phase change material thermal buffers, coolant control valves and integrated thermal management modules, insulation and encapsulation systems, and the embedded software and algorithms governing thermal system control strategy across vehicle operating modes and ambient conditions. Key market participants include automotive OEMs exercising system-level thermal architecture integration responsibility, Tier-1 thermal system module suppliers, Tier-2 component manufacturers specializing in heat exchangers, pumps, valves, and refrigerant circuit hardware, HVAC system developers, refrigerant and thermal fluid chemical suppliers, and software and controls technology developers providing thermal management optimization algorithms and digital thermal modeling capabilities that are increasingly central to achieving regulatory fuel consumption and emissions compliance targets across both internal combustion engine and battery electric vehicle platforms.

Market Insights

The global automotive thermal management systems market is undergoing its most significant structural transformation since the introduction of the closed-loop engine cooling system, driven by the simultaneous disruption of the vehicle powertrain architecture from internal combustion dominance toward electrification, the escalation of in-vehicle computing and semiconductor content that generates substantial new heat loads within constrained vehicle packaging spaces, and the tightening of global vehicle energy efficiency and carbon emissions regulations that are converting thermal management from a secondary engineering discipline into a primary determinant of vehicle range, performance, and regulatory compliance outcomes. Global battery electric vehicle sales reached approximately 17.1 million units in 2025, representing 19.4% of total new vehicle registrations, and are projected to constitute 42% of global new vehicle sales by 2030, with each battery electric vehicle containing approximately 2.3 times the thermal management system content value of an equivalent internal combustion engine vehicle, driven by the addition of battery pack thermal conditioning, power electronics cooling, and heat pump-based cabin heating systems absent from conventional vehicle thermal architectures. The global automotive thermal management systems market was valued at approximately USD 52.4 billion in 2025 and is projected to reach USD 89.6 billion by 2034, advancing at a compound annual growth rate of 6.2% over the forecast period from 2027 to 2034, with battery electric and plug-in hybrid vehicle thermal management sub-segments growing at a substantially higher rate of approximately 14.8% annually as electrified vehicle production volumes scale and thermal system content per vehicle increases with successive platform generations.

The thermal management requirements of battery electric vehicles are qualitatively and quantitatively more complex than those of internal combustion engine vehicles, demanding integrated system architectures that simultaneously manage the thermal conditioning of battery packs, power electronics, electric motors, onboard chargers, and cabin climate systems within a unified thermal circuit governed by sophisticated control software that continuously optimizes heat flow allocation across competing thermal loads under varying ambient temperatures, driving conditions, and charging scenarios. Battery pack thermal management is the most performance-critical subsystem, as lithium-ion battery cells achieve their optimal electrochemical performance, maximum cycle life, and safest operating characteristics within a narrow temperature window of approximately 15 to 35 degrees Celsius, below which charging acceptance and discharge power capability degrade substantially, and above which accelerated degradation and thermal runaway risk increase to operationally and safety-unacceptable levels. The transition from passive air cooling in early-generation battery electric vehicles to active liquid cooling using plate-type cooling circuits embedded within battery module structures is now essentially universal across premium and volume segment battery electric vehicle platforms, with the next frontier being the adoption of immersion cooling using dielectric fluids that achieve superior thermal uniformity and heat dissipation performance at the cell level, reducing maximum cell temperature gradients within large-format battery packs from approximately 5 to 8 degrees Celsius achievable with optimized liquid plate cooling to below 2 degrees Celsius with immersion cooling architectures. The heat pump system, which extracts thermal energy from ambient air or vehicle waste heat sources to deliver cabin heating with a coefficient of performance substantially exceeding that of resistive positive temperature coefficient heaters, has become a strategically important differentiator in battery electric vehicle range performance at low ambient temperatures, with vehicles equipped with heat pump systems demonstrating 10% to 20% greater winter range compared to equivalent vehicles relying on resistive heating, a range differential that is commercially significant in Northern European, North American, and Northeast Asian markets where winter operating conditions account for a substantial portion of annual vehicle usage.

The rapid escalation of electronic and computing content within modern vehicles, spanning advanced driver assistance system sensor fusion processors, domain controller and zone controller compute platforms, over-the-air update capable communication modules, and the centralized high-performance computing architectures being deployed by leading automotive software-defined vehicle programs, is generating a new and rapidly growing thermal management challenge within the automotive electronics domain that is structurally distinct from the powertrain thermal management challenge and that is compelling the development of novel cooling solutions adapted from data center and high-performance computing thermal management practice into the automotive operating environment. Modern automotive-grade system-on-chip processors used in level-2 and level-3 automated driving applications generate thermal design power outputs ranging from 30 to over 150 watts per chip, with next-generation centralized compute platforms for level-4 capable vehicles projecting aggregate electronic cooling loads exceeding 500 watts per vehicle, thermal levels that cannot be managed by conventional passive heatsink and forced air convection approaches and that require direct liquid-cooled cold plate integration with the vehicle’s main coolant circuit or dedicated electronics cooling loops. The development of integrated electronic thermal management architectures that connect the cooling loops of high-performance automotive processors, power inverters, onboard chargers, and DC-DC converters into optimized shared cooling circuits, recovering waste heat from power electronics during winter operation for cabin heating and battery preconditioning while ensuring adequate cooling capacity during summer high-load scenarios, represents an advanced systems engineering challenge that is generating significant development investment among both Tier-1 thermal system suppliers and automotive OEM powertrain and electronic integration engineering teams.

From a regional standpoint, Asia-Pacific constitutes the largest and most dynamically evolving regional market for automotive thermal management systems, driven by China’s position as both the world’s largest automotive production market, accounting for approximately 31% of global vehicle output, and the most advanced national battery electric vehicle market in terms of penetration rate, platform technology maturity, and the concentration of domestically developed battery electric vehicle OEMs that are rapidly developing and commercializing sophisticated integrated thermal management architectures. China’s domestic thermal management supplier ecosystem, anchored by companies that have developed deep technical partnerships with leading battery electric vehicle OEMs including BYD, Nio, Li Auto, and Xiaomi Automotive, is producing integrated thermal management modules and heat pump systems of increasing sophistication at price points that are establishing cost benchmarks that European and North American Tier-1 suppliers are finding structurally challenging to match. Europe represents the second-largest and technically most demanding regional market, where stringent vehicle carbon dioxide emission fleet average targets, mandatory real driving emissions compliance, and the European Union’s 2035 effective ban on new internal combustion engine vehicle sales are creating an unambiguous regulatory roadmap that is driving European OEMs to commit to electrified platform investments that generate sustained thermal management system content growth. North America is the third major regional market, where the United States Inflation Reduction Act’s domestic content requirements for electric vehicle battery and component supply chains are stimulating investment in North American thermal management component manufacturing capacity and generating a regional supply chain restructuring that is creating new commercial opportunities for both established Tier-1 suppliers and new-entrant thermal technology developers with domestically produced content capable of qualifying for federal clean vehicle tax credit eligibility.

Key Drivers

Accelerating Battery Electric Vehicle Adoption and the Step-Change Increase in Thermal Management System Content Per Vehicle

The single most consequential structural driver of revenue growth in the global automotive thermal management systems market is the accelerating penetration of battery electric vehicles in the global new vehicle sales mix, which drives a fundamental and commercially significant increase in thermal management system content value per vehicle that is compounding market revenue growth well beyond what vehicle production volume growth alone would generate. A battery electric vehicle platform requires a thermal management system architecture of substantially greater complexity and component content than an equivalent internal combustion engine vehicle, adding a battery pack liquid cooling circuit with coolant pump, cooling plate assemblies, chiller, and coolant control valves; a heat pump system replacing or supplementing resistive cabin heating; dedicated power electronics and electric motor cooling circuits; an onboard charger thermal conditioning system; and an integrated thermal management module that coordinates heat flow allocation across all subsystems through software-controlled valve actuation and pump speed modulation. The incremental thermal management system content value of a battery electric vehicle relative to a conventional internal combustion engine vehicle is estimated at approximately USD 380 to USD 650 per vehicle depending on platform architecture, climate control specification, and battery thermal conditioning approach, representing a revenue opportunity per vehicle that accrues entirely to the thermal management supply chain and that scales proportionally with battery electric vehicle production volume growth. With global battery electric vehicle production projected to reach approximately 31 million units annually by 2030, the cumulative incremental thermal management content opportunity relative to a no-electrification baseline is estimated at USD 11.8 billion in additional annual market revenue by the end of the decade, establishing electrification as the dominant long-cycle growth driver for automotive thermal management system suppliers across all vehicle categories and geographies.

Tightening Global Vehicle Fuel Economy and Carbon Dioxide Emissions Regulations Elevating Thermal Efficiency as a Powertrain Optimization Priority

Increasingly stringent vehicle fuel economy and carbon dioxide emissions standards across all major automotive markets are compelling OEMs to treat thermal management system efficiency as a tier-one vehicle development priority rather than a supporting engineering discipline, as the incremental fuel consumption and emissions improvements achievable through advanced thermal management, including waste heat recovery, rapid engine warm-up optimization, reduced parasitic cooling losses, and improved air conditioning system efficiency, are among the most cost-effective pathways available to OEM powertrain engineering teams operating within defined development budget and vehicle architecture constraints. The European Union’s fleet average carbon dioxide target of 93.6 grams per kilometer effective from 2025, declining to zero for new internal combustion engine vehicles effective from 2035, the United States Corporate Average Fuel Economy standards requiring passenger car fleet averages approaching 50 miles per gallon equivalent by 2031, and China’s fuel consumption limits under its passenger car fuel consumption regulation are each creating quantified compliance pressure that directly elevates the commercial value of thermal management innovations capable of measurable fuel consumption reduction. Waste heat recovery systems, including thermoelectric generators converting engine exhaust heat directly into electrical energy and Rankine cycle-based organic heat recovery systems recovering exhaust enthalpy for mechanical energy input to the drivetrain, represent emerging thermal management technology categories whose adoption is being accelerated specifically by the regulatory need to extract maximum efficiency from every joule of fuel energy within the constrained development timelines imposed by tightening annual emissions target ratchet mechanisms across major automotive regulatory jurisdictions.

Growth of Software-Defined Vehicle Architectures and the Thermal Management Demand Generated by Rising In-Vehicle Computing Loads

The automotive industry’s structural transition toward software-defined vehicle architectures, in which vehicle functionality is increasingly delivered through software running on centralized high-performance computing platforms rather than through proliferating dedicated electronic control units, is generating a new and rapidly growing thermal management demand category centered on the cooling of automotive-grade high-performance processors, domain controllers, and zone controllers that generate heat flux densities approaching those of enterprise server hardware within the constrained packaging and harsh vibration and temperature environments of vehicle installations. Automotive system-on-chip developers including Nvidia, Qualcomm, and Mobileye are deploying successive generations of automotive compute platforms with increasing transistor densities and thermal design power outputs, Nvidia’s Drive Thor platform delivers up to 2,000 TOPS of compute performance at a thermal design power approaching 200 watts, requiring direct liquid cooling integration that extends the vehicle’s liquid cooling infrastructure from the powertrain domain into the electronic architecture domain in ways that require fundamental thermal architecture redesign at the vehicle platform level. The commercial opportunity created by the confluence of vehicle electrification and software-defined vehicle architecture transition is that both trends simultaneously increase thermal management system complexity, component content, and per-vehicle supplier value, creating a compounding revenue growth dynamic for thermal management system developers that is structurally independent of total vehicle production volume growth and that will sustain above-market revenue growth rates for suppliers capable of delivering the integrated electro-thermal management system solutions that next-generation vehicle platforms require across both conventional and battery electric vehicle architectures.

Key Challenges

Thermal Management System Integration Complexity in Battery Electric Vehicles and the Engineering Challenge of Multi-Domain Heat Flow Optimization

The thermal management architecture of a modern battery electric vehicle integrates a significantly larger number of heat-generating and heat-consuming subsystems within a more spatially constrained vehicle package than any preceding automotive powertrain generation, creating a system integration challenge of exceptional complexity that is straining the engineering capabilities of both automotive OEMs and Tier-1 thermal system suppliers and extending vehicle development timelines and validation costs in ways that are compressing the profitability of new battery electric vehicle platform programs. A battery electric vehicle thermal system must simultaneously satisfy potentially conflicting thermal conditioning requirements, maintaining battery pack temperature within a narrow electrochemical optimum window while delivering adequate cabin heating and cooling comfort, protecting power electronics from overheating during sustained high-power charging and driving events, preconditioning the battery before DC fast charging sessions to maximize charge acceptance rate, and recovering waste heat from power electronics and motor for cabin heating during cold ambient operation, all within a refrigerant and coolant circuit architecture that must be optimized for minimum energy consumption to preserve vehicle range. The control software governing a battery electric vehicle integrated thermal management system must make real-time heat flow allocation decisions across five or more independent thermal domains simultaneously, responding to driver demand changes, ambient temperature variations, state of charge transitions, and charging event initiations within response windows of seconds while optimizing for energy efficiency objectives that require look-ahead predictive thermal preconditioning strategies based on navigation route data, traffic conditions, and charging station location information, representing a controls engineering challenge that is driving substantial investment in model-based thermal control software development and hardware-in-the-loop validation infrastructure at both OEM and Tier-1 supplier engineering organizations.

Refrigerant Transition Regulatory Pressure, Supply Chain Disruption Risk, and the Certification Cost of Next-Generation Low Global Warming Potential Refrigerant Adoption

The automotive air conditioning and heat pump market is navigating a mandatory refrigerant transition away from the hydrofluorocarbon refrigerant R-134a and its successor R-1234yf toward next-generation refrigerants with substantially lower global warming potential values, driven by the European Union’s F-Gas Regulation, the Kigali Amendment to the Montreal Protocol, and equivalent national regulations in China, Japan, South Korea, and India that impose progressively tightening restrictions on the use of high global warming potential refrigerants in new vehicle air conditioning systems across successive model year cycles. Carbon dioxide refrigerant operating in transcritical cycles, designated R-744, offers a global warming potential of exactly 1 compared to R-134a’s global warming potential of 1,430 and R-1234yf’s global warming potential of 4, making it the most environmentally favorable automotive refrigerant option available, but its transcritical operating pressures of up to 130 bar require heat exchanger, compressor, expansion valve, and refrigerant circuit hardware designs that are substantially heavier, more expensive, and more complex than equivalent R-1234yf components, imposing a vehicle-level cost premium estimated at USD 180 to USD 340 per vehicle for a complete R-744 air conditioning system relative to an R-1234yf baseline that constrains OEM adoption willingness in cost-sensitive vehicle segments. The certification and homologation of new refrigerant formulations and their associated system components across the multiple national and regional type-approval frameworks applicable to vehicles sold in global markets adds development cost, engineering resource requirements, and launch timeline risk to refrigerant transition programs that must be carefully managed within vehicle model cycle investment budgets that are simultaneously absorbing the engineering cost of electrification, connectivity, and automated driving technology integration.

Cost Reduction Pressure from Automotive OEMs and the Structural Margin Compression Affecting Thermal Management Tier-1 Suppliers in a Competitive Global Supply Market

Automotive thermal management system suppliers are operating within a procurement environment of intensifying cost pressure in which OEM purchasing organizations are leveraging the increased number of qualified suppliers in the battery electric vehicle thermal management segment, including new-entrant Chinese thermal system developers offering system-level module pricing that is 20% to 35% below the cost structures of established European and North American Tier-1 suppliers, to compress component and system-level pricing in ways that are directly eroding the margin profiles of established suppliers who are simultaneously bearing substantial engineering development investment costs for next-generation thermal system technology programs. The transition to battery electric vehicle platforms is disrupting previously stable thermal management supply relationships, as OEMs developing clean-sheet battery electric vehicle architectures are evaluating their thermal system supply base without the historical program continuity preferences that characterized internal combustion engine vehicle platform thermal management sourcing, and are in many instances awarding battery electric vehicle thermal management business to new-entrant Chinese suppliers or to established suppliers willing to accept below-historical-average margin levels as a condition of securing anchor program volume. The capital investment required to develop, validate, and scale manufacturing for next-generation integrated thermal management modules, including the tooling, test equipment, and manufacturing cell investments required to produce refrigerant circuit assemblies, heat pump systems, and battery cooling plates to the dimensional and leak-rate specifications demanded by leading battery electric vehicle programs, is substantial and must be amortized over program volumes and across pricing structures that are simultaneously under competitive pressure, creating a structural margin compression dynamic that is forcing Tier-1 thermal management suppliers to accelerate consolidation, pursue manufacturing footprint rationalization, and intensify value engineering efforts to maintain commercially viable financial returns on their thermal management business portfolios.

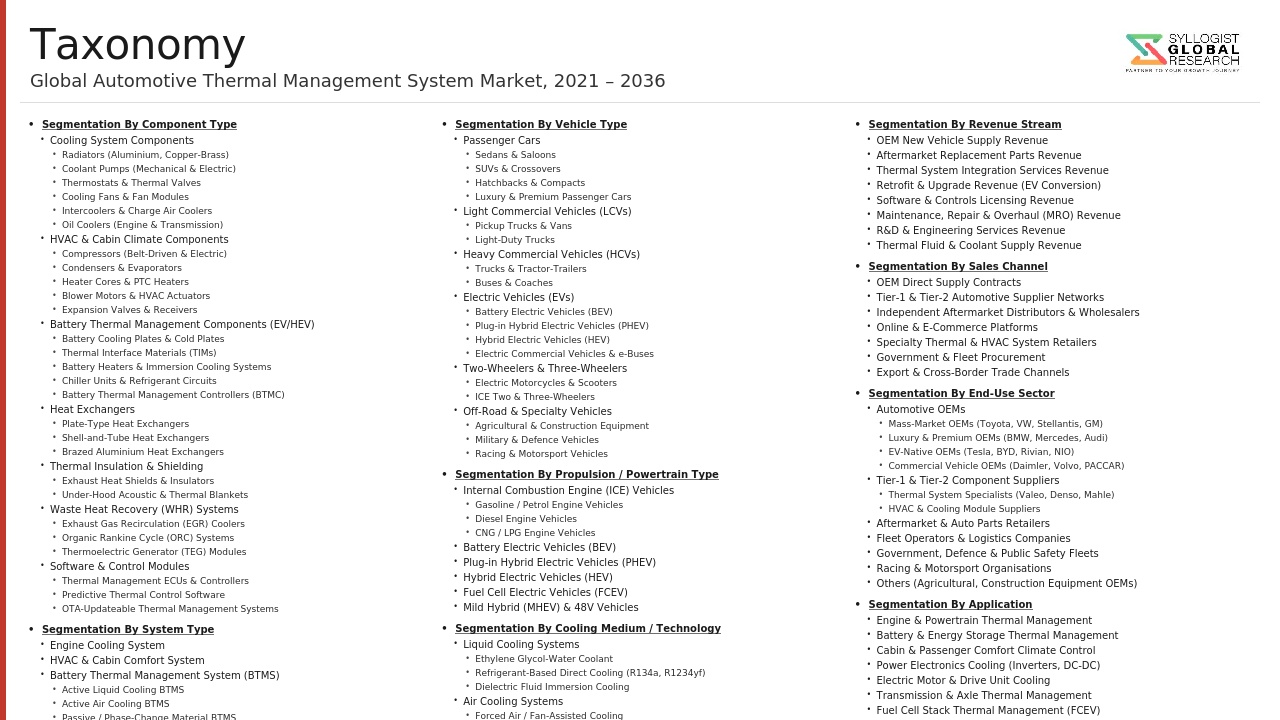

Market Segmentation

- Segmentation By System Type

- Engine and Powertrain Cooling Systems

- Battery Thermal Management Systems (BTMS)

- Power Electronics and Electric Motor Cooling Systems

- Cabin Heating, Ventilation, and Air Conditioning (HVAC) Systems

- Heat Pump Systems

- Exhaust and Waste Heat Recovery Systems

- Transmission and Drivetrain Cooling Systems

- Integrated Thermal Management Modules (iTMM)

- Others

- Segmentation By Battery Cooling Technology

- Liquid Cooling (Cooling Plate and Jacket Systems)

- Air Cooling

- Immersion Cooling (Dielectric Fluid)

- Refrigerant Direct Cooling

- Phase Change Material (PCM) Thermal Buffering

- Others

- Segmentation By Component

- Radiators and Heat Exchangers

- Electric Coolant Pumps

- Electronically Controlled Thermostats and Coolant Control Valves

- Compressors (Electric and Belt-Driven)

- Condensers and Evaporators

- Chillers and Refrigerant-Coolant Heat Exchangers

- Thermal Expansion Valves and Electronic Expansion Valves

- Positive Temperature Coefficient (PTC) Heaters

- Thermal Insulation and Encapsulation Materials

- Thermal Management Control Software and ECUs

- Others

- Segmentation By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Battery Electric Vehicles (BEV)

- Plug-In Hybrid Electric Vehicles (PHEV)

- Full Hybrid Electric Vehicles (HEV)

- Mild Hybrid Electric Vehicles (MHEV)

- Fuel Cell Electric Vehicles (FCEV)

- Others

- Segmentation By Refrigerant Type

- R-134a (HFC Refrigerant)

- R-1234yf (HFO Refrigerant)

- R-744 (Carbon Dioxide, CO2)

- R-290 (Propane)

- R-152a

- Others

- Segmentation By Vehicle Type

- Passenger Cars (Compact and Sub-Compact)

- Passenger Cars (Mid-Size and Full-Size)

- Premium and Luxury Passenger Cars

- Sport Utility Vehicles (SUVs) and Crossovers

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles and Trucks

- Buses and Coaches

- Off-Highway and Construction Equipment

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Direct Supply

- Aftermarket Replacement and Repair

- Online Retail and E-Commerce Distribution

- Others

- Segmentation By Technology

- Active Thermal Management Systems

- Passive Thermal Management Systems

- Predictive and AI-Enabled Thermal Control Systems

- Waste Heat Recovery and Thermoelectric Systems

- Model-Based Thermal Management Optimization

- Others

- Segmentation By End User

- Automotive OEMs (Passenger Vehicle Manufacturers)

- Commercial Vehicle OEMs

- Electric Vehicle Startups and New-Entrant OEMs

- Aftermarket Service Providers and Independent Repair Shops

- Fleet Operators and Leasing Companies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Automotive Thermal Management Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by system type, engine cooling, battery thermal management, power electronics cooling, HVAC, heat pump, and waste heat recovery, and by propulsion type, ICE, BEV, PHEV, HEV, and FCEV, to enable Tier-1 thermal system suppliers, automotive OEMs, and component investors to precisely identify the highest-growth thermal management sub-segments and technology transition investment priorities across the forecast period?

- How is the transition from conventional internal combustion engine vehicle thermal architectures to integrated battery electric vehicle thermal management systems, encompassing battery pack cooling, heat pump cabin heating, power electronics thermal conditioning, and onboard charger cooling within unified multi-domain thermal circuit architectures, reshaping the competitive dynamics, sourcing strategies, and supplier consolidation trends among established Tier-1 thermal system developers and new-entrant Chinese and Asian thermal module suppliers through 2034?

- What is the projected adoption trajectory of next-generation battery thermal management technologies, specifically immersion cooling using dielectric fluids, refrigerant direct cooling, and phase change material thermal buffering, across battery electric vehicle platform generations from 2027 to 2034, and at what battery pack energy density, fast charging rate, and vehicle segment entry points does each technology achieve commercial cost-competitiveness relative to established liquid plate cooling architectures?

- How are evolving refrigerant transition regulatory frameworks, including the EU F-Gas Regulation phase-down schedule, the Kigali Amendment implementation timelines across major automotive markets, and national low global warming potential refrigerant mandates in China, Japan, and India, expected to reshape the competitive positioning of R-1234yf, R-744, R-290, and next-generation refrigerant chemistries within automotive air conditioning and heat pump system applications, and what are the associated component technology investment requirements and vehicle-level cost implications for OEMs navigating the refrigerant transition across diverse global vehicle programs?

- Who are the leading automotive thermal management system Tier-1 suppliers, integrated thermal module developers, heat pump system specialists, battery cooling technology providers, and thermal management software and controls companies currently defining the competitive landscape of the global automotive thermal management systems market, and what are their respective technology development roadmaps, battery electric vehicle program award portfolios, manufacturing capacity expansion plans, geographic market strategies, and competitive responses to the pricing pressure exerted by new-entrant Chinese thermal system suppliers across passenger vehicle, commercial vehicle, and premium segment thermal management business lines?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Readiness & Performance Risk

- Regulatory & Compliance Risk

- Supply Chain & Material Risk

- Design & Integration Risk

- Market & Commercial Risk

- Regulatory Framework & Standards

- Global Refrigerant & HVAC Regulations for Automotive

- Battery Thermal Safety Standards

- Vehicle Thermal System & HVAC Performance Standards

- Engine Cooling & Powertrain Thermal System Standards

- Environmental & Product Regulations

- Global Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by System Type

- Engine & Powertrain Cooling System

- Battery Thermal Management System (BTMS)

- Cabin HVAC & Climate Control System

- Electric Drivetrain Thermal Management System

- Integrated Vehicle Thermal Management System (VTMS)

- ADAS & Electronics Thermal Management System

- Fuel Cell Vehicle Thermal Management System

- Exhaust Thermal Management & Aftertreatment System

- Market Size & Forecast by Component

- Heat Exchangers

- Fluid Management & Circulation Components

- HVAC & Refrigeration Components

- Thermal Interface & Insulation Materials

- Electrical Heating Components

- Blowers, Fans & Air Management

- Thermal Management Control Units & Software

- Market Size & Forecast by Powertrain / Vehicle Type

- Internal Combustion Engine (ICE) Vehicle

- Gasoline (Petrol) Vehicle

- Diesel Vehicle

- CNG / LPG & Alternative Fuel Vehicle

- Hybrid Electric Vehicle (HEV)

- Mild HEV (48V)

- Full HEV

- Plug-In Hybrid Electric Vehicle (PHEV)

- PHEV Passenger Car

- PHEV Light Commercial Vehicle

- Battery Electric Vehicle (BEV)

- BEV Passenger Car

- BEV Light Commercial Vehicle (LCV)

- BEV Heavy Truck & Bus

- BEV Two-Wheeler & Micro-Mobility

- Fuel Cell Electric Vehicle (FCEV)

- FCEV Passenger Car

- FCEV Commercial Vehicle & Bus

- Commercial Vehicle ICE & Hybrid

- Light Commercial Vehicle (LCV) ICE & Hybrid

- Medium & Heavy Truck ICE & Hybrid

- Bus & Coach ICE, Hybrid & Electric

- Off-Road, Construction & Agricultural Vehicle

- Motorsport & High-Performance Vehicle

- Internal Combustion Engine (ICE) Vehicle

- Market Size & Forecast by Vehicle Segment

- Passenger Cars

- Hatchback & Subcompact

- Sedan & Compact

- SUV & Crossover

- MPV & Minivan

- Sports Car & Performance

- Light Commercial Vehicles (LCV)

- Vans & Minibuses

- Pick-Up Trucks & Utility Vehicles

- Heavy Commercial Vehicles (HCV)

- Medium & Heavy Trucks

- Buses & Coaches

- Two-Wheelers & Micro-Mobility

- Passenger Cars

- Market Size & Forecast by Coolant Type

- Ethylene Glycol-Based Coolant

- Propylene Glycol-Based Coolant

- Waterless Coolant & Engine Ice

- Dielectric & Immersion Cooling Fluids

- Battery Coolant

- Market Size & Forecast by Technology

- Conventional Passive Thermal Management

- Active Thermal Management

- Integrated Thermal Management System

- Predictive & AI-Driven Thermal Management

- Immersion Cooling Technology

- Waste Heat Recovery & Thermoelectric Technology

- Market Size & Forecast by Sales Channel

- Original Equipment Manufacturer

- Independent Aftermarket

- OES

- North America Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

- Europe Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

- Latin America Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Automotive Thermal Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By System Type

- By Component

- By Powertrain / Vehicle Type

- By Vehicle Segment

- By Coolant Type

- By Technology

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Spain, Sweden, Poland, Czech Republic, China, Japan, South Korea, India, Thailand, Indonesia, Australia, Brazil, Argentina, Saudi Arabia, UAE, South Africa

- Battery Thermal Management System (BTMS) Deep-Dive Analysis

- BTMS Technology Architecture Overview

- BTMS Performance Parameters & Design Targets

- Battery Pre-Conditioning & Fast Charge Thermal Management

- BTMS Integration with Vehicle Thermal Architecture

- Heat Pump & HVAC System Deep-Dive Analysis

- Automotive Heat Pump Technology Overview

- Refrigerant Selection for Automotive Heat Pump Systems

- Heat Pump System Configurations

- Electric A/C Compressor Technology

- Cabin Air Quality & Ventilation

- Technology Landscape & Innovation Analysis

- Integrated Vehicle Thermal Management System (VTMS) Technology

- Advanced Thermal Interface Material (TIM) Technology

- Waste Heat Recovery & Thermoelectric Technology

- Predictive & AI-Driven Thermal Management

- 3D Printing & Advanced Manufacturing for Thermal Components

- Thermal Simulation & CAE Technology

- Patent & IP Landscape in Automotive Thermal Management

- Value Chain & Supply Chain Analysis

- Raw Materials & Key Input Materials

- Tier-2 & Tier-3 Component Suppliers

- Tier-1 Thermal Management System Suppliers

- OEM Vehicle Assembly & Thermal System Integration

- Aftermarket & Replacement Parts Distribution

- Pricing Analysis

- Thermal Management System Pricing by System Type

- Component-Level Pricing Analysis

- Aftermarket Pricing Analysis

- Total Thermal Management System Cost per Vehicle: Platform Comparison

- Sustainability & Energy Efficiency

- Environmental Impact of Automotive Thermal Management on Fuel Economy & Emissions

- Refrigerant Transition & GWP Reduction

- Automotive Coolant Environmental Management

- Thermal Management System Lifecycle Sustainability

- ESG & Sustainability Reporting in Automotive Thermal Management

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Sub-Segment)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type & Geography

- Player Classification

- Tier-1 Global Full-System Automotive Thermal Management Suppliers

- Specialist Engine Cooling & Heat Exchanger Manufacturers

- Specialist Battery Thermal Management System Suppliers

- Specialist Automotive HVAC & Compressor Manufacturers

- Thermal Interface Material & Specialty Chemical Suppliers

- Electric Coolant Pump & Fluid Management Component Suppliers

- Emerging Startups & Disruptive Technology Innovators (Immersion Cooling, AI TMS)

- OEM In-House Thermal Management Technology Development Teams

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Component & Geography

- Company Profile

- Company Overview & Headquarters

- Automotive Thermal Management Products & Systems Portfolio

- Key OEM Customers & Vehicle Platform Wins

- Technology Capabilities & R&D Investment

- Revenue (Automotive Thermal Management Segment) & Order Backlog

- Manufacturing Locations & Production Capacity

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Products, Platform Wins, Acquisitions, Expansions)

- SWOT Analysis

- Strategic Focus Areas & Technology Roadmap

- Competitive Positioning Map (Technology Leadership vs. Market Share)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix – By System Type, Powertrain & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Investment & R&D Prioritisation Strategy

- EV Platform Transition Strategy

- OEM Engagement & Platform Win Strategy

- Supply Chain & Manufacturing Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Regulatory Compliance Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)