Market Definition

The Global Printed Circuit Board Market encompasses the design, fabrication, assembly, testing, and commercial supply of rigid, flexible, and rigid-flex substrates that mechanically support and electrically interconnect electronic components through a network of conductive copper traces, pads, vias, and planes etched or plated onto and through dielectric laminate materials, serving as the foundational interconnect infrastructure within virtually every category of electronic device and system manufactured globally. Printed circuit boards are classified by their layer count from single-sided and double-sided boards through multilayer constructions of four to sixty or more layers, by their substrate material from standard FR-4 glass-reinforced epoxy laminate through high-frequency polytetrafluoroethylene, high-speed low-loss resin systems, and ceramic-filled substrates, and by their mechanical flexibility from rigid boards fabricated on glass-fiber-reinforced cores through flexible circuits built on polyimide or polyester film substrates and rigid-flex combinations that integrate both rigid and flexible zones within a single interconnect assembly. The market encompasses high-density interconnect boards with microvias below 100 micrometers in diameter and trace and space geometries below 75 micrometers that enable the dense component placement required by advanced mobile, wearable, and high-performance computing devices; any-layer high-density interconnect constructions with stacked blind and buried vias throughout all layers; substrate-like printed circuit boards with line and space dimensions approaching semiconductor package substrate geometries of 10 to 30 micrometers; and ultra-high-density integration boards for high-bandwidth memory, advanced packaging, and heterogeneous integration applications. The complete value chain encompasses laminate and prepreg raw material suppliers, copper foil and surface treatment chemical producers, drilling, imaging, plating, and etching equipment manufacturers, board fabricators, contract electronics manufacturers performing assembly, bare board test equipment providers, and the original equipment manufacturer end customers across consumer electronics, telecommunications, automotive, industrial, medical, defense, and data center market verticals. Key participants include printed circuit board manufacturers, laminate suppliers, equipment developers, contract manufacturers, design tool vendors, and end-use OEM customers.

Market Insights

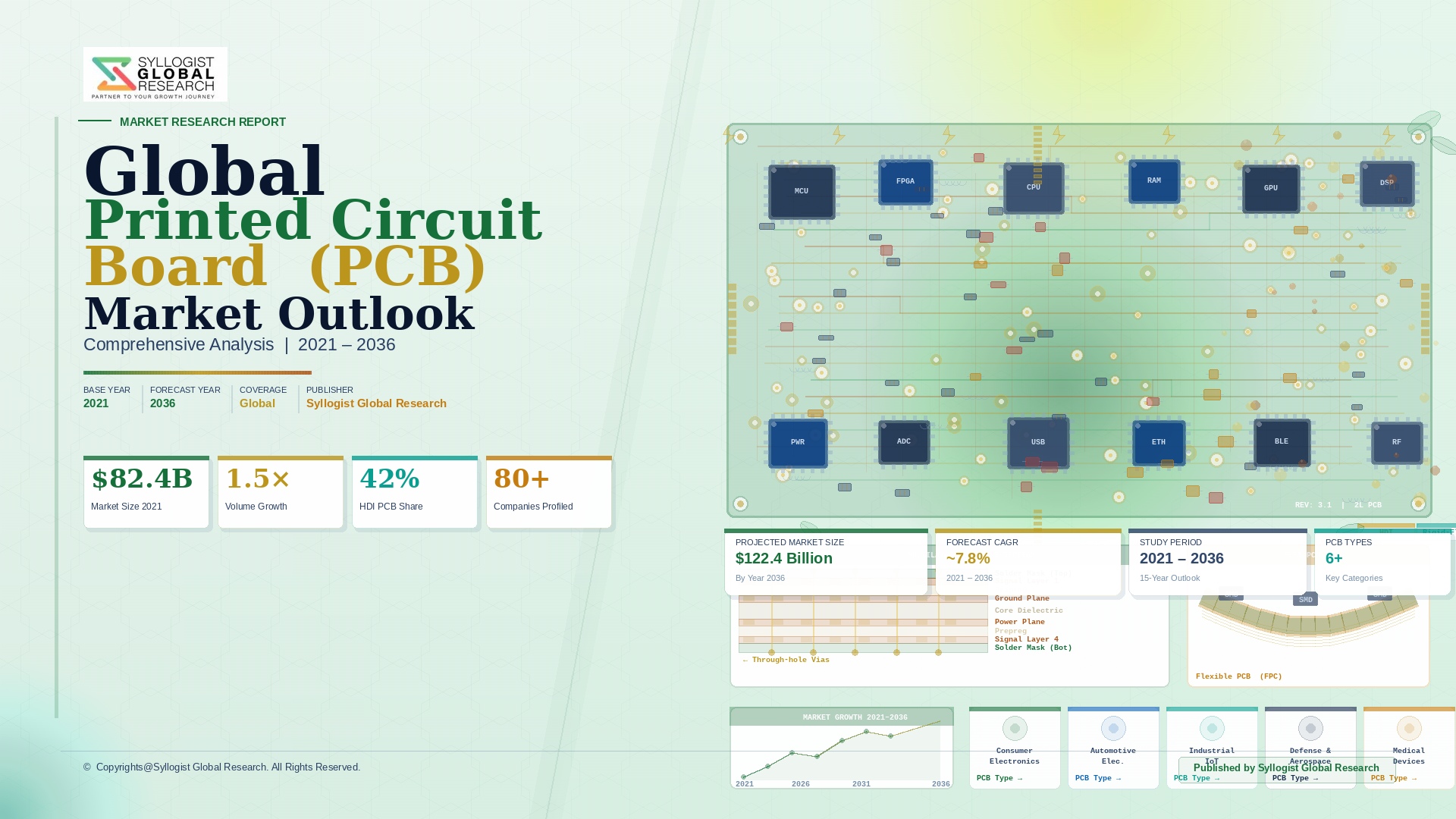

The global printed circuit board market was valued at approximately USD 82.4 billion in 2025 and is projected to reach USD 148.6 billion by 2034, advancing at a compound annual growth rate of 6.8% over the forecast period from 2027 to 2034, driven by the proliferation of electronic content across automotive electrification and advanced driver assistance systems, the expansion of artificial intelligence server and data center infrastructure requiring high-layer-count, high-speed, and thermally demanding printed circuit board constructions, the sustained growth of 5G telecommunications infrastructure deployment requiring low-loss, high-frequency circuit board materials, and the continuous advancement of miniaturization requirements across mobile, wearable, and Internet of Things device categories that is driving adoption of increasingly demanding high-density interconnect and any-layer high-density interconnect printed circuit board technologies. China maintains its position as the world’s dominant printed circuit board production geography, accounting for approximately 53% of global printed circuit board production output by value in 2025, with manufacturing clusters in Guangdong, Jiangsu, and Zhejiang provinces hosting the majority of both mass-market multilayer and advanced high-density interconnect production capacity, while Taiwan accounts for approximately 12% of global output through its concentration of high-technology substrate and advanced printed circuit board production serving the semiconductor packaging and advanced server markets. The global printed circuit board market is experiencing a structural technology migration toward higher-layer-count, finer-geometry, and higher-performance constructions driven by the simultaneous requirements of increasing circuit density, faster signal speeds, higher power delivery requirements, and improved thermal management in applications including server central processing units and graphics processing units, automotive ADAS domain controllers, and millimeter-wave radar and 5G radio frequency front-end modules that collectively represent the highest-value and fastest-growing segments of printed circuit board demand across the forecast period.

The automotive printed circuit board segment has emerged as the single most structurally significant growth driver within the global market, accounting for approximately 14% of total printed circuit board market revenue in 2025 and growing at approximately 11.4% annually, driven by the extraordinary increase in electronic content per vehicle as battery electric vehicles incorporate traction inverter control boards, battery management system circuits, onboard charger electronics, DC-DC converter control boards, and high-voltage junction box interconnects that collectively represent approximately USD 450 to USD 680 of printed circuit board content per battery electric vehicle compared to approximately USD 80 to USD 120 per conventional internal combustion engine vehicle, a content multiplier of approximately four to six times that mirrors the automotive power semiconductor content growth dynamic and reflects the fundamental transition of the vehicle from a mechanically dominated to an electronically dominated system architecture. Advanced driver assistance system domain controllers and the zonal and central computing architectures that are progressively replacing distributed electronic control unit networks in premium vehicles require printed circuit boards of extraordinary complexity, with ADAS central processing units incorporating layer counts of twenty to thirty-two layers, blind and buried via constructions, embedded component technologies for passive component integration, and backplane-quality signal integrity at data rates exceeding 56 gigabits per second per channel for high-bandwidth processor interconnects, specifications that place automotive printed circuit board content at the high end of the technology complexity and unit value distribution and require qualification and reliability standards including AEC-Q200 laminate certification and automotive-grade solder mask and surface finish specifications that command premium pricing over equivalent commercial-grade constructions. The electrification of vehicle architectures is additionally increasing the thermal management demands placed on automotive printed circuit boards, with high-current power electronics circuits requiring heavy copper inner layers of 2 to 8 ounces per square foot, thermally conductive dielectric materials, and embedded heat spreader constructions that add manufacturing complexity and material cost to automotive power electronics board fabrication.

The data center and artificial intelligence infrastructure segment is driving the most technically demanding and commercially valuable printed circuit board requirements in the global market, with artificial intelligence training clusters deploying hundreds of thousands of graphics processing units and custom artificial intelligence accelerators that each require server motherboards, graphics processing unit carrier boards, and high-bandwidth memory interposer substrates of layer counts between twenty and forty layers, very low-loss dielectric materials capable of supporting signal integrity at 112 gigabit per second per lane speeds across backplane and midplane connections, and precise impedance control tolerances of plus or minus 5% maintained across the full laminate lot and board fabrication process that challenge the manufacturing process capability of all but the most technically advanced printed circuit board producers globally. The transition to 800-gigabit and 1.6-terabit Ethernet switching in hyperscale data center fabric networks requires optical transceiver host boards and switch application-specific integrated circuit boards fabricated on ultra-low-loss laminate materials with dissipation factors below 0.002 at 10 gigahertz to maintain acceptable channel insertion loss across the backplane distances typical of high-radix leaf-spine network architectures, driving adoption of premium low-loss and very-low-loss resin system laminates from suppliers including Panasonic, Isola, Ventec, and TUC that command pricing premiums of 30% to 80% over standard FR-4 grade materials and generate disproportionate revenue contribution per unit area of fabricated board. The substrate-like printed circuit board segment, targeting the finest line and space geometries achievable through semi-additive and modified semi-additive process technologies approaching 10 to 30 micrometer trace widths, is growing at approximately 18.6% annually in 2025 as the demand for higher input-output density semiconductor packaging substrates for advanced artificial intelligence processors and networking chips drives adoption of substrate-like printed circuit board technology as a bridge between conventional printed circuit boards and full semiconductor package substrate processing.

The geopolitical realignment of global printed circuit board supply chains represents a defining structural force reshaping market geography, investment flows, and competitive dynamics through the forecast period, as the United States, European Union, Japan, India, and Southeast Asian governments implement industrial policy measures designed to reduce dependency on Chinese-dominated printed circuit board supply chains for domestically manufactured defense electronics, telecommunications infrastructure, automotive systems, and advanced computing hardware whose supply security is assessed as strategically important. The United States Department of Defense has identified printed circuit board supply chain concentration in China as a critical vulnerability in domestic defense electronics manufacturing, with the National Defense Authorization Act provisions and Industrial Base Analysis and Sustainment program funding supporting domestic and allied nation printed circuit board capacity investment to ensure availability of trusted and secure printed circuit board supply for military electronics programs. Vietnam, Thailand, Malaysia, and India are emerging as alternative printed circuit board manufacturing locations attracting investment from Taiwanese and Korean printed circuit board manufacturers seeking to diversify production geography in response to customer supply chain diversification requirements and favorable labor and operational cost structures relative to established Chinese manufacturing clusters, with Vietnamese printed circuit board production output growing at approximately 14.2% annually in 2025 from a base of approximately USD 3.8 billion in annual production value as manufacturers including AT&S, TTM Technologies, and Unimicron establish or expand Vietnamese production capacity. The transition of leading-edge printed circuit board technology development toward substrate-like printed circuit boards and advanced high-density interconnect constructions is creating competitive differentiation opportunities for technologically advanced producers in Taiwan, Japan, and South Korea whose process capabilities in modified semi-additive processes, laser direct imaging, and advanced via formation exceed those of mainstream Chinese volume producers and position them favorably for the highest-value segments of future printed circuit board demand growth.

Key Drivers

Automotive Electrification and Advanced Driver Assistance System Proliferation Generating a Four-to-Six Times Printed Circuit Board Content Multiplier Per Vehicle Relative to Conventional Platforms

The global automotive industry’s simultaneous transition toward battery electric vehicle powertrains and increasingly sophisticated advanced driver assistance and autonomous driving system architectures is generating a structural four-to-six times increase in printed circuit board content per vehicle relative to conventional internal combustion engine platforms, establishing automotive as the highest-growth end market in the global printed circuit board industry and creating a multi-year pipeline of design-in programs for automotive-grade printed circuit board manufacturers capable of meeting the combined electrical performance, thermal reliability, and automotive quality management system requirements demanded by vehicle original equipment manufacturers and tier-one electronics suppliers. A battery electric vehicle incorporating traction inverter, battery management system, onboard charger, DC-DC converter, and high-voltage junction box electronics consumes approximately USD 450 to USD 680 of printed circuit board content, compared to approximately USD 80 to USD 120 for an equivalent internal combustion engine vehicle, with global battery electric vehicle production reaching approximately 17.4 million units in 2025 and projected to grow toward 38 million units annually by 2034, generating an addressable automotive printed circuit board demand increment of approximately USD 6.4 billion to USD 9.2 billion annually from electric vehicle platform growth alone over the forecast period. The progressive adoption of zonal and centralized computing architectures in premium and mid-range vehicle platforms is simultaneously increasing the per-vehicle count of high-complexity, high-layer-count domain controller boards whose unit value of USD 80 to USD 350 per board substantially exceeds that of the distributed electronic control unit boards they replace, adding a technology content value increase on top of the volume growth driven by electric powertrain electronics, collectively positioning automotive as the most commercially compelling growth segment within the global printed circuit board market through 2034.

Artificial Intelligence Data Center Expansion and 5G Infrastructure Deployment Demanding High-Layer-Count, Ultra-Low-Loss, and High-Density Interconnect Printed Circuit Board Constructions at Premium Pricing

The extraordinary capital investment in artificial intelligence training and inference infrastructure by hyperscale cloud operators and enterprise data center builders is creating a rapidly growing demand segment for the most technically advanced and highest unit-value printed circuit board constructions available, as artificial intelligence server motherboards, graphics processing unit carrier boards, high-speed switch application-specific integrated circuit boards, and optical transceiver host boards require printed circuit board specifications that push the performance limits of laminate dielectric properties, copper conductor geometry precision, via formation accuracy, and surface finish quality that differentiate the most capable global printed circuit board manufacturers from volume commodity producers. Artificial intelligence server infrastructure deployed to support large language model training and inference is estimated to have consumed approximately USD 3.8 billion of printed circuit board content in 2025 at a growth rate of approximately 24.6% annually, driven by the doubling of graphics processing unit compute density per server rack generation and the associated doubling of signal layer count, copper weight, and dielectric performance requirements per server motherboard. The global 5G network infrastructure rollout, while decelerating from its initial deployment peak in leading markets, continues to drive sustained demand for radio access network base station circuit boards fabricated on low-loss and thermally conductive materials, millimeter-wave antenna array boards with precise impedance matching across large panel areas, and optical transport network boards requiring low-loss laminate at speeds above 400 gigabits per second, with the cumulative 5G base station installation count reaching approximately 7.4 million units globally in 2025 and continued expansion in India, Southeast Asia, Latin America, and the Middle East extending the 5G infrastructure printed circuit board demand cycle through the late 2020s.

Supply Chain Geopolitical Realignment, Trusted Electronics Sourcing Requirements, and Regional Manufacturing Incentive Programs Driving Printed Circuit Board Capacity Investment Outside China

The strategic designation of printed circuit boards as critical electronics manufacturing infrastructure by the United States, European Union, Japan, and India, combined with customer supply chain diversification mandates from major electronics original equipment manufacturers managing geopolitical concentration risk in their component procurement portfolios, is driving a sustained wave of printed circuit board manufacturing capacity investment in geographies outside the Chinese production clusters that have historically dominated global output, creating new production capacity in Vietnam, Thailand, Malaysia, India, Mexico, and Eastern Europe that represents a structural shift in the geographic distribution of printed circuit board supply that will accelerate through the forecast period. The United States CHIPS and Science Act’s provisions supporting domestic semiconductor and electronics manufacturing supply chain development, combined with the Department of Defense’s trusted printed circuit board supplier program requirements that mandate domestic or allied nation sourcing for printed circuit boards used in classified and sensitive defense electronic systems, are mobilizing direct government funding and procurement preference mechanisms that improve the investment economics of domestic printed circuit board manufacturing capacity for defense and national security market segments. India’s Production Linked Incentive scheme for electronics manufacturing, which provides financial incentives of 4% to 6% of incremental production value for printed circuit board and electronics component manufacturing established within India, combined with India’s large and rapidly growing domestic electronics consumption market for smartphones, consumer electronics, automotive electronics, and industrial equipment, is creating a commercially attractive environment for printed circuit board manufacturing investment that is drawing commitments from Taiwanese, Korean, and domestic Indian electronics manufacturers seeking to establish India-based production capacity for both domestic supply and export to global customers pursuing supply chain geographic diversification away from sole-source Chinese dependencies.

Key Challenges

Intense Price Competition from Chinese Manufacturers, Chronic Overcapacity in Standard Technology Segments, and Margin Pressure Across Commodity Printed Circuit Board Product Categories

The global printed circuit board industry is structurally challenged by persistent overcapacity in standard technology segments including single-sided, double-sided, and low-layer-count multilayer rigid boards that are produced at scale by a large number of Chinese manufacturers whose access to government-subsidized financing, lower labor costs, and favorable utility pricing structures enables them to sustain production at price points below the breakeven cost of equivalent capacity in higher-cost manufacturing jurisdictions, creating chronic margin pressure for non-Chinese producers competing in commodity printed circuit board segments and compressing the pricing power of the industry as a whole in product categories where technology differentiation is minimal. Chinese printed circuit board manufacturers collectively invested approximately USD 8.4 billion in new fabrication capacity between 2020 and 2024, adding substantial production capacity at a rate that has outpaced demand growth in standard technology segments and depressed average selling prices for four-layer, six-layer, and eight-layer FR-4 boards by approximately 12% to 18% in real terms over the same period, directly reducing the revenue per square meter achieved by all producers in these segments and forcing capacity rationalization among higher-cost producers in Taiwan, Japan, South Korea, and Europe who cannot achieve cost parity with Chinese producers on standard technology boards manufactured at equivalent quality specifications. The margin compression in commodity segments is forcing non-Chinese printed circuit board manufacturers to pursue deliberate technology migration strategies concentrating production investment in advanced high-density interconnect, any-layer high-density interconnect, substrate-like printed circuit boards, and specialty materials constructions where Chinese producers have not yet achieved equivalent technical capability, creating a bifurcated global industry in which commodity volume production concentrates increasingly in China while technology-differentiated premium segment production sustains viable economics in Taiwan, Japan, Korea, and emerging alternative locations.

Raw Material Supply Concentration, Specialty Laminate and Copper Foil Availability Constraints, and Chemical Supply Chain Vulnerabilities Affecting Advanced Printed Circuit Board Fabrication

The fabrication of advanced printed circuit boards for high-speed, high-frequency, and high-power applications depends on a supply chain of specialty raw materials whose production is geographically concentrated and technically constrained in ways that create supply security vulnerabilities and pricing volatility risks for printed circuit board manufacturers investing in advanced technology segments. Ultra-low-loss laminate materials required for artificial intelligence server, 5G, and millimeter-wave applications are produced by a limited number of specialty laminate manufacturers including Panasonic, Isola, Ventec, and Rogers Corporation, whose combined global production capacity is constrained by the specialized resin synthesis, glass fabric treatment, and lamination press infrastructure required for low-loss resin systems, creating supply tightness episodes and extended lead times when demand surges driven by artificial intelligence infrastructure build-outs coincide with laminate manufacturer capacity limitations. Rolled annealed copper foil used in high-frequency flexible circuits and very-low-profile electrolytic copper foil required for high-speed multilayer boards whose smooth surface topography minimizes conductor skin-effect losses at frequencies above 10 gigahertz are produced by fewer than ten qualified manufacturers globally, with Japanese producers including Fukuda Metal Foil and Powder, Mitsui Mining and Smelting, and Furukawa Electric controlling a disproportionate share of the highest-specification copper foil grades, creating a supply bottleneck for printed circuit board manufacturers requiring the finest-grade copper foils for advanced high-density interconnect and substrate-like printed circuit board production that cannot be resolved quickly through new entrant qualification given the multi-year technology development and qualification timelines involved. The concentrated geography of specialty chemistry supply chains for imaging photoresists, electroless copper plating chemistries, and organic solderability preservatives adds additional supply vulnerability dimensions that printed circuit board manufacturers must manage through strategic inventory and multi-supplier qualification programs.

Environmental Compliance Costs, Hazardous Chemical Use Restrictions, and Water and Energy Intensity of Printed Circuit Board Fabrication Creating Operational and Regulatory Burden

Printed circuit board fabrication is among the most chemically intensive and environmentally regulated manufacturing processes in the electronics industry, utilizing significant quantities of hazardous chemicals including sulfuric acid, hydrochloric acid, hydrogen peroxide, potassium permanganate, formaldehyde in electroless copper baths, organic solvents in photoresist stripping, and heavy metal-containing surface finish chemistries including electroless nickel, immersion gold, and electrolytic tin-lead or tin-silver-copper alloy that generate complex and highly regulated wastewater streams requiring extensive treatment infrastructure before discharge, creating compliance costs that represent approximately 8% to 15% of total manufacturing operating costs for facilities operating in jurisdictions with stringent industrial wastewater, air emissions, and hazardous waste management regulations. The European Union’s Restriction of Hazardous Substances directive and its successive revisions have progressively eliminated lead-containing solder and surface finishes from electronics manufacturing, creating reformulation requirements and qualification costs for printed circuit board manufacturers supplying European markets, while ongoing regulatory review processes evaluating additional brominated flame retardant restrictions, halogen-free laminate transition requirements, and chemical agent restrictions under the REACH regulation create a continuous compliance evolution burden that requires ongoing investment in chemistry reformulation, process re-qualification, and regulatory monitoring. Water consumption in printed circuit board fabrication is substantial, with a mid-size multilayer board fabrication facility processing approximately 10,000 square meters of panel per month consuming approximately 150,000 to 250,000 cubic meters of water annually for process rinsing, chemical dilution, and cooling applications, creating meaningful operating cost and regulatory compliance challenges in water-stressed manufacturing geographies and increasing the environmental footprint management obligations of printed circuit board manufacturers under corporate sustainability disclosure frameworks and customer supply chain environmental assessment programs.

Market Segmentation

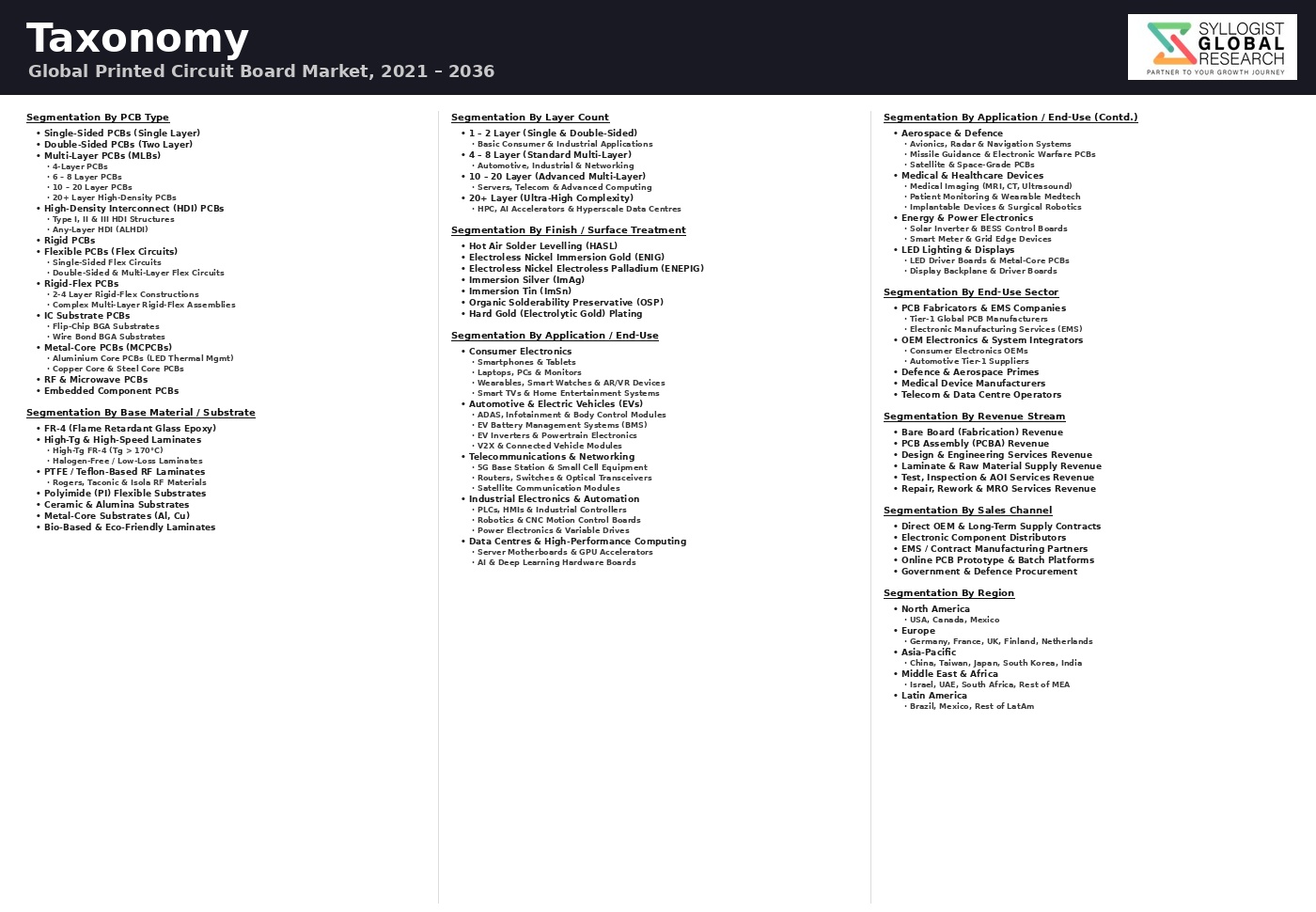

- Segmentation By Board Type

- Single-Sided Printed Circuit Boards

- Double-Sided Printed Circuit Boards

- Multilayer Rigid Printed Circuit Boards (4 to 16 Layers)

- High-Layer-Count Multilayer Boards (Above 16 Layers)

- High-Density Interconnect (HDI) Printed Circuit Boards

- Any-Layer HDI Printed Circuit Boards

- Flexible Printed Circuit Boards (FPC)

- Rigid-Flex Printed Circuit Boards

- Substrate-Like PCBs (SLP) and IC Substrates

- Metal Core and Thermally Conductive Printed Circuit Boards

- Others

- Segmentation By Base Material

- FR-4 Glass-Reinforced Epoxy Laminate

- High-Speed Low-Loss and Very-Low-Loss Resin Systems

- High-Frequency Materials (PTFE and Ceramic-Filled Substrates)

- Halogen-Free and Eco-Friendly Laminates

- Polyimide Flexible Substrates

- Metal Core Substrates (Aluminum and Copper Core)

- Others

- Segmentation By Layer Count

- 1 to 2 Layer Boards

- 4 to 8 Layer Boards

- 10 to 16 Layer Boards

- 18 to 32 Layer Boards

- Above 32 Layer Boards

- Segmentation By Application

- Consumer Electronics (Smartphones, Tablets, Laptops, and Wearables)

- Automotive (EV Powertrains, ADAS, Body Electronics, and Infotainment)

- Data Centers, Servers, and AI Infrastructure

- Telecommunications and 5G Infrastructure

- Industrial Automation and Control Systems

- Medical Devices and Healthcare Electronics

- Aerospace and Defense Electronics

- Energy and Power Electronics

- Internet of Things (IoT) and Smart Devices

- Others

- Segmentation By Surface Finish

- Electroless Nickel Immersion Gold (ENIG)

- Electroless Nickel Electroless Palladium Immersion Gold (ENEPIG)

- Immersion Silver

- Immersion Tin

- Hot Air Solder Leveling (HASL) and Lead-Free HASL

- Organic Solderability Preservative (OSP)

- Others

- Segmentation By End User

- Electronics Original Equipment Manufacturers (OEMs)

- Contract Electronics Manufacturers (CEMs) and EMS Providers

- Automotive OEMs and Tier-1 Suppliers

- Telecommunications Equipment Manufacturers

- Industrial Equipment Manufacturers

- Defense and Aerospace Prime Contractors

- Medical Device Manufacturers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Printed Circuit Board Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by board type including standard multilayer, high-density interconnect, any-layer high-density interconnect, flexible, rigid-flex, substrate-like printed circuit boards, and metal core boards, by base material including FR-4, high-speed low-loss laminates, high-frequency PTFE substrates, and polyimide flexible substrates, and by application including automotive, data center and AI infrastructure, telecommunications, consumer electronics, industrial, medical, and defense, to enable printed circuit board manufacturers, laminate and raw material suppliers, contract electronics manufacturers, automotive and electronics OEMs, and capital market investors to identify the highest-growth technology and application combinations generating the most commercially durable demand trajectories across the forecast period to 2034?

- How is the transition from conventional internal combustion engine vehicles to battery electric vehicles and the proliferation of advanced driver assistance system domain controllers and zonal computing architectures reshaping automotive printed circuit board content per vehicle, layer count requirements, thermal management specifications, and qualification standard obligations across traction inverter, battery management, onboard charger, ADAS central processor, and high-voltage junction box circuit board categories, and what are the total automotive printed circuit board addressable market projections by vehicle segment and technology category through 2034 as global battery electric vehicle production scales toward 38 million units annually and premium vehicle platform electronic architecture transitions from distributed to centralized computing designs drive per-vehicle printed circuit board content and complexity increases?

- What are the material property requirements, fabrication process challenges, qualification standards, supplier landscape, and pricing premium profiles of the ultra-low-loss and very-low-loss laminate materials required for artificial intelligence server motherboards, 5G radio frequency boards, and millimeter-wave antenna arrays operating at signal frequencies above 10 gigahertz and data rates above 56 gigabit per second per lane, and how are laminate manufacturers including Panasonic, Isola, Ventec, Rogers Corporation, and TUC differentiating their high-speed material portfolios through dielectric constant stability, dissipation factor performance, thermal reliability, and supply chain availability to capture design-in positions at the most demanding artificial intelligence and 5G printed circuit board customers whose material selection decisions determine the laminate technology adoption trajectories for these premium growth segments through 2034?

- How are geopolitical supply chain realignment trends, United States Department of Defense trusted electronics sourcing requirements, customer supply chain diversification mandates, and government manufacturing incentive programs including the United States CHIPS Act, European Union Chips Act, India Production Linked Incentive scheme, and Vietnam and Southeast Asian investment promotion frameworks reshaping the geographic distribution of global printed circuit board manufacturing capacity, and what production capacity investment commitments, technology specialization strategies, customer qualification program timelines, and operational cost structure comparisons characterize the printed circuit board manufacturing expansion programs being established in Vietnam, India, Thailand, Mexico, and Eastern Europe as alternatives to or complements to established Chinese, Taiwanese, and Japanese production clusters?

- What is the current technology readiness level, line and space geometry capability, via formation process, yield performance, manufacturing cost structure, and customer qualification activity of substrate-like printed circuit board and advanced package substrate technologies being developed by printed circuit board manufacturers as they compete with and complement traditional semiconductor package substrate producers for design-in positions in advanced artificial intelligence processors, high-bandwidth memory interposers, and next-generation networking chip packaging applications, and how is the technology boundary between printed circuit boards and semiconductor package substrates evolving through modified semi-additive process adoption, enabling printed circuit board fabricators to address the finer-geometry requirements of chiplet integration and advanced packaging that were previously exclusively within the capability domain of dedicated semiconductor substrate manufacturers?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material, Copper Foil, Glass Fabric & Laminate Supply Chain Concentration Risk

- Geopolitical, Trade Policy & PCB Manufacturing Geographic Concentration Risk

- Technology Transition, Advanced Substrate Yield & Qualification Risk

- Market Cyclicality, Inventory Correction & End-Market Demand Volatility Risk

- Environmental Compliance, Chemical Waste, Wastewater Treatment & Regulatory Risk

- Regulatory Framework & Standards

- IPC Standards for PCB Design, Fabrication & Acceptability (IPC-2221, IPC-6012, IPC-A-600, IPC-7711/7721 Series)

- RoHS (Restriction of Hazardous Substances), REACH & Halogen-Free PCB Material Compliance Regulations

- Automotive PCB Quality Standards: IATF 16949, AEC-Q200 Passive Component Qualification & VDA 6.3 Process Audit

- Aerospace & Defence PCB Certification: MIL-PRF-31032, MIL-PRF-55110, AS9100 & NADCAP Accreditation

- Conflict Mineral Reporting (SEC Section 1502, OECD Due Diligence), WEEE Directive & Environmental Manufacturing Standards for PCB Fabrication Facilities

- Global Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Square Metres of PCB Produced)

- Market Size & Forecast by PCB Type

- Single-Sided PCB

- Double-Sided PCB

- Multilayer PCB (4-Layer, 6-Layer, 8-Layer & 10-Layer Plus)

- High-Density Interconnect (HDI) PCB

- Any-Layer HDI PCB

- Flexible Printed Circuit (FPC)

- Rigid-Flex PCB

- Heavy Copper & Extreme Copper PCB

- High-Frequency & High-Speed PCB

- Embedded Component PCB

- Substrate-Like PCB (SLP) & IC Substrate

- Metal Core PCB (MCPCB) & Aluminium PCB

- Market Size & Forecast by Layer Count

- 1 to 2 Layer (Single & Double Sided)

- 4 to 6 Layer

- 8 to 16 Layer

- 18 Layer and Above (High Layer Count)

- Market Size & Forecast by Base Material

- FR-4 (Standard Glass Epoxy Laminate)

- High-Tg FR-4 & Halogen-Free FR-4

- Polyimide (PI) & Liquid Crystal Polymer (LCP)

- PTFE & High-Frequency Low-Loss Laminates (Rogers, Taconic, Isola)

- BT (Bismaleimide Triazine) Resin & Modified BT Substrate

- Aluminium & Copper Metal Core (MCPCB Substrate)

- Ceramic & Low-Temperature Co-Fired Ceramic (LTCC) Substrate

- Market Size & Forecast by Surface Finish

- HASL (Hot Air Solder Levelling, Lead-Free & Tin-Lead)

- ENIG (Electroless Nickel Immersion Gold)

- ENEPIG (Electroless Nickel Electroless Palladium Immersion Gold)

- OSP (Organic Solderability Preservative)

- Immersion Silver (ImAg)

- Immersion Tin (ImSn)

- Hard Gold & Selective Gold Plating

- Market Size & Forecast by Application

- Consumer Electronics (Smartphones, Laptops, Tablets, Wearables & Smart Home Devices)

- Automotive & Electric Vehicle (EV) (ADAS, Body Control, Powertrain, BMS & In-Vehicle Infotainment)

- Telecommunications & 5G / 6G Infrastructure (Base Stations, Antennas, Routers & Optical Networks)

- Industrial Automation, Robotics & Control Systems

- Data Centre, Server, Storage & Cloud Infrastructure

- Aerospace & Defence (Avionics, Radar, Missile Guidance & Satellite Systems)

- Medical & Healthcare Devices (Imaging, Diagnostics, Implantables & Monitoring Equipment)

- Renewable Energy & Power Electronics (Solar Inverter, Wind Turbine & EV Charging)

- Market Size & Forecast by End-User

- Electronics OEM (Original Equipment Manufacturer)

- Electronics Manufacturing Services (EMS) & Contract Manufacturer (CM)

- Automotive OEM & Tier-1 Supplier

- Telecommunications Equipment Manufacturer

- Aerospace & Defence Prime Contractor & Tier-1 Supplier

- Medical Device Manufacturer

- Market Size & Forecast by Sales Channel

- Direct OEM Long-Term Volume Supply Agreement

- EMS & Contract Manufacturer Procurement Channel

- Authorised Distributor & PCB Broker Network

- Online PCB Fabrication Platform & E-Commerce Channel

- North America Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Printed Circuit Board (PCB) Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Square Metres of PCB Produced)

- By PCB Type

- By Layer Count

- By Base Material

- By Surface Finish

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Italy, Netherlands, Sweden, Switzerland, Finland, China, Japan, South Korea, Taiwan, Hong Kong, India, Vietnam, Thailand, Malaysia, Singapore, Brazil, Mexico, Israel

- Technology Landscape & Innovation Analysis

- High-Density Interconnect (HDI) & Any-Layer HDI PCB Manufacturing Technology Deep-Dive

- Substrate-Like PCB (SLP), IC Package Substrate & Advanced Coreless Substrate Technology

- High-Frequency, High-Speed & Low-Loss Laminate Material Technology for 5G and mmWave Applications

- Flexible & Rigid-Flex PCB Process Technology: Coverlay, Adhesiveless Laminate & Roll-to-Roll Manufacturing

- Embedded Component, Embedded Die & In-Board Integration PCB Technology

- Advanced Via Technology: Laser Drilling, Via-in-Pad, Stacked Micro-Via, Copper Fill & Via Plugging

- PCB Design Automation (EDA), Design for Manufacturability (DFM), AOI, AXI & Electrical Test Technology

- Patent & IP Landscape in Printed Circuit Board Technologies

- Value Chain & Supply Chain Analysis

- Raw Material Supply Chain: Copper Foil, Glass Fibre, Epoxy Resin, Laminate & Chemical Supply

- PCB Fabrication Equipment Supply Chain: Laser Driller, Direct Imaging, Plating Line, AOI & Solder Mask Printer

- CCL (Copper Clad Laminate) & Prepreg Manufacturer Landscape

- PCB Fabricator & Board House Landscape (Captive, Independent & EMS-Affiliated)

- EMS, CM & OEM PCB Assembly & System Integration Channel

- Distributor, Broker & Online PCB Platform Procurement Channel

- PCB Repair, Rework, End-of-Life Recycling & E-Waste Management

- Pricing Analysis

- Standard FR-4 Multilayer PCB Average Selling Price (ASP) Analysis by Layer Count & Panel Size

- HDI & Any-Layer HDI PCB Pricing vs. Standard Multilayer: Premium Analysis by Build-Up Layer Count

- Flexible & Rigid-Flex PCB Pricing Analysis by Layer Count & Material

- High-Frequency & High-Speed Low-Loss Laminate PCB Price Premium Analysis

- Substrate-Like PCB (SLP) & IC Substrate Pricing Analysis vs. Conventional HDI Benchmark

- Total PCB System Cost Analysis: Fabrication, Assembly, Test & Supply Chain Logistics per Application Segment

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of PCB Manufacturing: Carbon Footprint, Water Consumption, Chemical Use & Energy Intensity per Board Type

- PCB Chemical Waste Management: Etchant Recovery, Copper Drag-Out Reduction, Wastewater Treatment & Zero Liquid Discharge Implementation

- RoHS, Halogen-Free & Lead-Free Soldering Compliance: Environmental Impact Reduction in PCB Material Composition

- PCB End-of-Life, Precious Metal Recovery, E-Waste Recycling Rate & Circular Economy Contribution

- Regulatory-Driven Sustainability: EU Green Deal, WEEE Directive, Conflict Mineral Reporting & ESG Disclosure for PCB Manufacturers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by PCB Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by PCB Type, Application & Geography

- Player Classification

- Global Diversified PCB Manufacturers with Full Product Range Capability

- Specialist HDI, SLP & Advanced Package Substrate PCB Manufacturers

- Specialist Flexible & Rigid-Flex PCB Manufacturers

- High-Frequency & Microwave PCB Specialists

- Automotive & Aerospace Grade PCB Certified Manufacturers

- CCL & Laminate Material Manufacturers (Upstream Substrate Suppliers)

- PCB Fabrication Equipment & Chemical Process Suppliers

- Online PCB Platform, Quick-Turn Prototyping & Small-Batch PCB Fabricators

- Competitive Analysis Frameworks

- Market Share Analysis by PCB Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- PCB Products & Technology Portfolio

- Key OEM & EMS Customer Relationships

- Manufacturing Footprint & Annual Production Capacity (MSM)

- Revenue (PCB Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Product Launches, Certifications)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By PCB Type, Base Material, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & OEM Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)