Market Definition

The Global Electronics Recycling Market encompasses the collection, sorting, preprocessing, dismantling, material recovery, and responsible disposal of end-of-life electrical and electronic equipment and components across consumer electronics, information technology hardware, telecommunications devices, household appliances, industrial electronics, medical equipment, and energy generation and storage technology. Electronics recycling is distinguished from general solid waste management by its deliberate focus on recovering commercially valuable materials embedded within discarded devices, managing hazardous substances including lead, cadmium, mercury, hexavalent chromium, brominated flame retardants, and polychlorinated biphenyls that require specialized treatment to prevent environmental and human health harm, and complying with the extended producer responsibility regulations, waste electrical and electronic equipment directives, and hazardous waste management frameworks that govern how end-of-life electronics must be handled across the jurisdictions where they are collected and processed. The market spans the complete electronics recycling value chain from consumer and business drop-off collection, municipal curbside pickup, retailer and manufacturer take-back programs, and corporate asset disposal services through manual and automated dismantling and preprocessing operations, shredding and mechanical size reduction, density and eddy current separation, sensor-based sorting and optical recognition systems, hydrometallurgical and pyrometallurgical metal recovery for precious metals, copper, aluminum, and steel extraction, plastics separation and secondary material sales, and the environmentally sound treatment and disposal of residual hazardous fractions that cannot be economically recovered. The product scope encompasses computers, laptops, servers and data center hardware, mobile phones and tablets, televisions and display equipment, printers and peripherals, household appliances including refrigerators and washing machines, power tools, audio and video equipment, photovoltaic panels, and electric vehicle batteries as they enter the end-of-life waste stream. Key participants include electronics recycling operators, original equipment manufacturer take-back programs, certified e-stewards and R2-certified processors, reverse logistics providers, commodity metal trading houses, and national and regional regulatory bodies administering producer responsibility schemes.

Market Insights

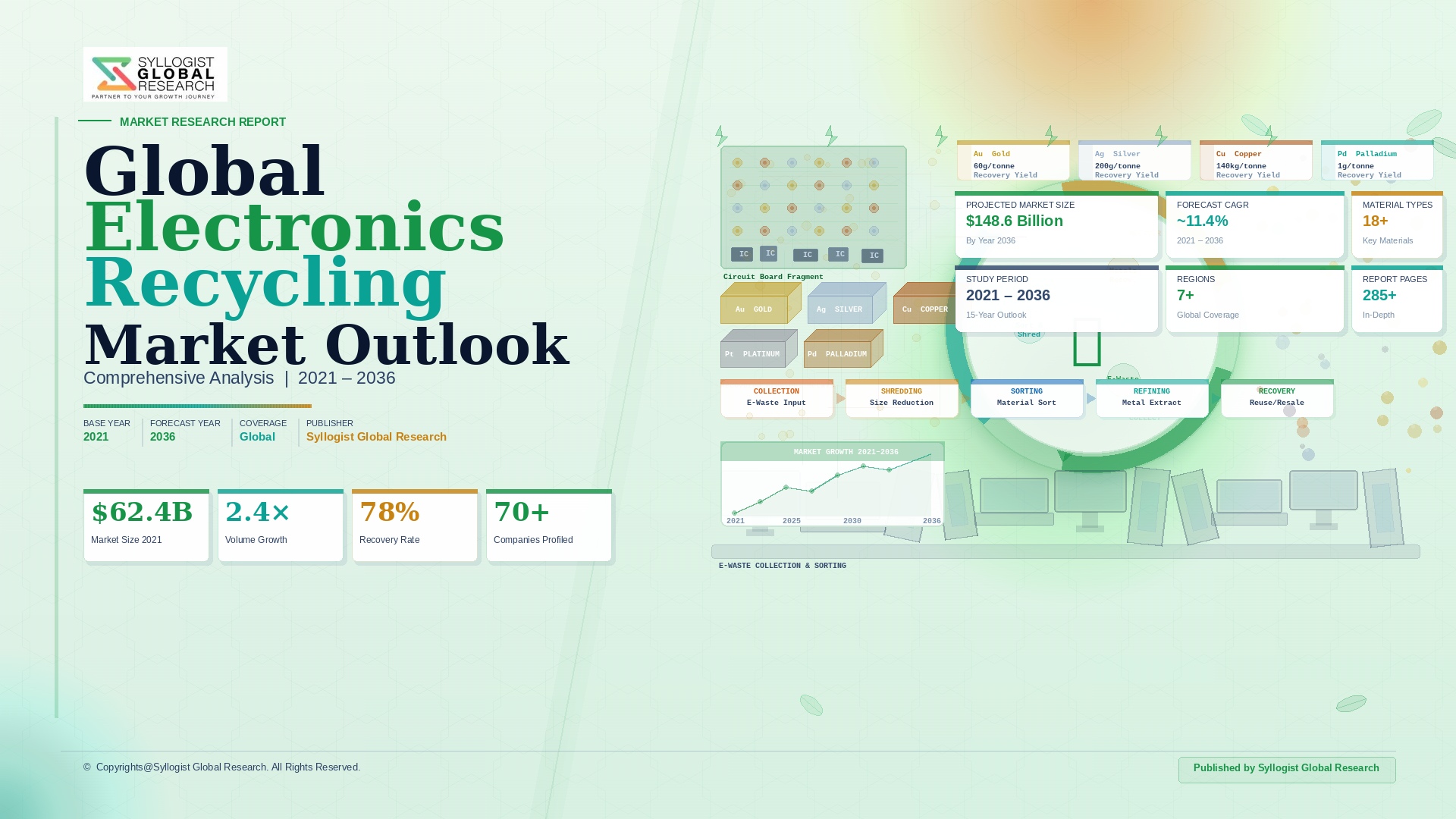

The global electronics recycling market was valued at approximately USD 22.6 billion in 2025 and is projected to reach USD 52.4 billion by 2034, advancing at a compound annual growth rate of 9.8% over the forecast period from 2027 to 2034, driven by the escalating global generation of electrical and electronic equipment waste, the tightening of extended producer responsibility legislation across the European Union, Asia-Pacific, and increasingly across Latin America and Africa, the growing commercial value of critical and precious metals recoverable from electronic waste streams, and the strategic imperative of corporate sustainability commitments and circular economy policy frameworks that are mandating higher collection rates, expanded material recovery targets, and demonstrated recycled content integration within new electronic product designs. Global e-waste generation reached approximately 62.4 million metric tons in 2025, with projections indicating growth to approximately 82 million metric tons annually by 2034 as the global installed base of electronic devices expands, product replacement cycles shorten in consumer electronics categories, and the first large-scale wave of end-of-life photovoltaic panels and electric vehicle battery packs enters the recycling waste stream. The collection rate gap remains the most critical structural deficiency within the global electronics recycling market, with only approximately 22.3% of total generated e-waste processed through formal, environmentally compliant recycling channels in 2025, meaning approximately 48 million metric tons of e-waste annually is either landfilled, incinerated without material recovery, or processed through informal sector operations that capture a fraction of available metal value while creating significant occupational health and environmental contamination impacts in receiving communities. The aggregate recoverable material value embedded within the global annual e-waste stream is estimated at approximately USD 62 billion at 2025 commodity prices, encompassing gold, silver, palladium, copper, aluminum, steel, rare earth elements, and battery metals whose recovery represents the fundamental commercial engine of the global electronics recycling industry.

The information technology and telecommunications equipment segment constitutes the highest-value processing category within the global electronics recycling market, accounting for approximately 42% of total formal recycling market revenue in 2025, anchored by the exceptional precious metal concentration of printed circuit boards in computers, servers, smartphones, and networking equipment that contain gold at approximately 200 to 350 grams per metric ton, silver at approximately 1,500 to 2,500 grams per metric ton, and palladium at approximately 100 to 200 grams per metric ton, concentration levels that are respectively 50 to 100 times, 10 to 20 times, and 30 to 60 times higher than economically exploitable primary ore grades for these metals, making high-grade printed circuit board processing the most economically attractive activity in the electronics recycling sector per unit of material processed. The data center decommissioning and corporate information technology asset disposal sub-segment has emerged as a rapidly growing and commercially concentrated source of high-grade electronics recycling feedstock, with the hyperscale cloud computing expansion driving accelerated server and networking hardware refresh cycles at major data center operators whose decommissioned hardware portfolios represent dense, pre-sorted, and geographically accessible collections of high-precious-metal-content printed circuit boards and copper-bearing infrastructure components that command premium processing economics relative to the mixed and contaminated electronic waste streams collected through municipal and consumer channels. The transition to solid-state storage media, reduction of gold wire bonding in semiconductor packaging in favor of copper bonding, and miniaturization trends reducing precious metal mass per device are creating a secular headwind to per-unit precious metal content in consumer electronics that makes the collection volume growth and processing scale expansion achieved by leading recyclers an essential offset to the declining per-unit material value trend affecting the information technology recycling segment.

The electric vehicle battery recycling segment is the most strategically significant emerging growth driver within the global electronics recycling market, with end-of-life electric vehicle battery packs entering the formal recycling waste stream at volumes projected to grow from approximately 280,000 metric tons in 2025 to approximately 1.4 million metric tons by 2034 as the first large-scale cohorts of electric vehicles sold between 2015 and 2024 reach their eight to twelve year battery service life thresholds, generating a battery recycling feedstock ramp whose scale, material value concentration, and strategic importance to electric vehicle supply chain sustainability are attracting multi-billion-dollar capacity investment from automotive manufacturers, chemical companies, and dedicated battery recycling technology developers. The contained critical mineral value within the projected 2034 electric vehicle battery recycling feedstock stream at 1.4 million metric tons per year is estimated at approximately USD 18 billion annually at 2025 metal prices for the recoverable lithium, cobalt, nickel, manganese, and copper within spent battery black mass, with hydrometallurgical processing routes achieving lithium recovery rates of 80% to 90% and cobalt and nickel recovery rates above 95% at commercial scale operations operated by processors including Li-Cycle, Redwood Materials, Umicore, and Fortum. The European Union Battery Regulation adopted in 2023 establishes mandatory minimum recycled content thresholds for new batteries of 6% for cobalt, 6% for lithium, 6% for lead, and 6% for nickel by 2031, rising to 12% for cobalt, 12% for lithium, and 15% for nickel by 2036, creating a legally mandated demand stream for certified secondary battery materials from electronics recycling processors that is the most commercially decisive regulatory intervention in the electronics recycling industry’s history and is underpinning the large-scale battery recycling capacity investments progressing across Europe and North America.

The photovoltaic panel recycling segment represents a nascent but rapidly expanding component of the global electronics recycling market whose commercial scale is approaching a critical inflection point as the large-scale solar photovoltaic installations deployed during the industry’s first major growth wave of 2010 to 2016 approach their twenty to twenty-five year design life and begin entering the end-of-life waste stream, with global cumulative end-of-life solar panel volumes projected to reach approximately 78 million metric tons by 2034 from approximately 8 million metric tons in 2025, generating a recycling feedstock growth trajectory whose contained material value, processing infrastructure requirements, and regulatory compliance obligations are only beginning to be systematically addressed through dedicated photovoltaic recycling program development globally. The geographic concentration of formal electronics recycling processing capacity remains significantly skewed toward developed economies despite the rapid growth of e-waste generation in developing markets, with the European Union, United States, Japan, South Korea, and Australia collectively hosting the majority of certified and environmentally compliant electronics recycling infrastructure while China, India, Nigeria, Ghana, and other major developing market e-waste generators continue to manage significant proportions of their domestic e-waste through informal sector operations that are progressively being targeted for formalization through regulatory enforcement, financial incentive programs, and technology transfer initiatives. The competitive landscape of the global electronics recycling market is characterized by a tiered structure comprising large integrated recyclers with smelting and refining capabilities, mid-tier certified processors specializing in information technology asset disposal and data destruction, and a fragmented long tail of smaller regional operators handling locally collected mixed e-waste streams, with consolidation activity increasing as processing scale economics, capital requirements for advanced separation technology, and environmental compliance costs favor larger operators capable of investing in sensor-based sorting, automated dismantling, and integrated precious metal recovery infrastructure that deliver superior material recovery rates and environmental performance.

Key Drivers

Exponential Growth in Global E-Waste Generation, Shortening Consumer Electronics Product Replacement Cycles, and Expanding Electronic Device Penetration in Emerging Markets Creating Structural Feedstock Volume Growth

The structural growth in global electronics recycling feedstock volumes is driven by the compound effect of an expanding installed base of electronic devices across all device categories, accelerating consumer product replacement cycles driven by planned obsolescence, rapid technological advancement, and mobile carrier upgrade programs that reduce average smartphone replacement intervals to approximately two to three years, and the progressive saturation of electronic device ownership in rapidly growing emerging market consumer populations in China, India, Southeast Asia, Latin America, and Sub-Saharan Africa whose adoption of smartphones, household appliances, and information technology equipment is generating rapidly growing e-waste volumes in geographies that lack the recycling infrastructure capacity to manage them through formal channels. Global smartphone shipments reached approximately 1.24 billion units in 2025, with an installed base of approximately 6.8 billion active devices globally, meaning that the annual replacement and disposal volume from smartphones alone generates approximately 1.5 to 2.0 million metric tons of electronic waste containing significant concentrations of precious metals, rare earth elements in permanent magnets, cobalt in lithium-ion batteries, and specialized semiconductor materials that represent valuable secondary resource streams for electronics recyclers with the processing capability to extract and refine them. The rapid growth of the cloud computing and artificial intelligence infrastructure sector is creating an accelerating data center hardware replacement cycle, with hyperscale operators refreshing server generations every four to five years and networking equipment on three to four year cycles to maintain competitive performance density, generating large volumes of high-grade server and networking hardware entering the corporate asset disposal and electronics recycling market at rates that are growing substantially faster than overall e-waste volume metrics and providing electronics recyclers with premium feedstock streams that deliver superior economics per unit of material processed.

Tightening Extended Producer Responsibility Legislation, Mandatory Recycled Content Requirements, and Corporate Circular Economy Commitments Creating Legally Binding Demand for Formal Recycling Services

The global expansion of extended producer responsibility legislation requiring electronics manufacturers and importers to fund, organize, and demonstrate the collection and recycling of end-of-life products equivalent to a mandated percentage of their annual sales volumes is creating legally enforceable demand for formal electronics recycling services that is insulating participating recyclers from market price volatility and providing the contractual volume certainty required to justify investment in advanced processing infrastructure at commercial scale. The European Union Waste Electrical and Electronic Equipment Directive requires member states to achieve collection rates of 65% of the average weight of electrical and electronic equipment placed on the market in the three preceding years, with individual producer responsibility organizations contracting electronics recyclers across national markets to fulfill collection and treatment obligations that collectively represent hundreds of millions of euros of annual contracted recycling service revenue in the European Union alone. Corporate sustainability commitments by major electronics manufacturers including Apple, Samsung, Microsoft, HP, and Dell that incorporate specific targets for recycled material content, take-back program coverage, and certified responsible recycling of products at end of life are creating direct pull-through demand for certified electronics recycling services from manufacturers seeking to demonstrate supply chain circularity credentials to investors, regulators, and consumers who are increasingly evaluating electronics brands on the environmental performance of their end-of-life management programs. The European Union Battery Regulation’s mandatory recycled content thresholds for cobalt, lithium, and nickel in new batteries from 2031 represents the most commercially transformative regulatory mandate for electronics recycling economics, directly linking new battery manufacturing compliance to the availability of certified secondary material from electronics recycling operations and creating a demand floor for battery recycling services that strengthens processing economics independently of spot commodity price fluctuations.

Escalating Critical and Precious Metal Prices, Strategic Supply Chain Diversification Imperatives, and Corporate Supply Security Investment Elevating the Commercial Value of Secondary Metal Recovery

The combination of rising commodity metal prices reflecting tightening primary supply relative to clean energy transition and electronics manufacturing demand, corporate and government supply chain diversification strategies targeting reduced dependency on geopolitically concentrated primary mineral supply, and the improving economics of hydrometallurgical battery metal recovery approaching cost parity with primary production in several metal categories is progressively elevating the commercial attractiveness of electronics recycling as a secondary metal supply source whose domestic geographic availability, ethical sourcing credentials, and reduced carbon footprint relative to primary mined production increasingly justify premium processing investment and offtake pricing structures that improve the economics of formal electronics recycling operations. Gold prices reaching approximately USD 2,400 per troy ounce in 2025 directly improve the economics of printed circuit board precious metal recovery, as the gold content of a metric ton of high-grade printed circuit boards from server equipment of approximately 300 grams valued at approximately USD 23,000 per metric ton of input material at 2025 gold prices, combined with silver and palladium co-product revenues, creates processing economics that comfortably justify investment in advanced printed circuit board smelting and refining infrastructure. The United States Inflation Reduction Act’s domestic content requirements for battery critical minerals, which require progressively higher proportions of lithium, cobalt, nickel, and manganese in electric vehicle batteries to be sourced from domestic or free-trade-agreement partner country production to qualify for consumer and manufacturer tax credits, has directly elevated the strategic value of domestically produced secondary battery metals from electronics recycling as a source of critical mineral supply that simultaneously satisfies domestic content qualification requirements and supports the circular economy objectives of federal clean energy policy.

Key Challenges

Persistent Dominance of Informal Sector Processing and Transboundary Illegal E-Waste Shipments Diverting High-Value Feedstock from Formal Recyclers and Creating Environmental and Social Harm

The global electronics recycling industry operates in a fundamentally uneven competitive environment in which informal sector operators in developing countries, who process e-waste through environmentally destructive methods including open cable burning, acid stripping of printed circuit boards without fume treatment, and amalgam processing of precious metals using mercury, maintain a structural cost advantage over formal certified recyclers by avoiding the environmental compliance, worker health and safety, hazardous waste management, and regulatory reporting costs that constitute a significant proportion of formal sector operating expenses, enabling informal operators to pay higher collection prices to generators and intermediaries and capturing an estimated 60% to 70% of global e-waste volume that should flow through formal processing channels. The Basel Convention on the Control of Transboundary Movements of Hazardous Wastes and their Disposal, whose 2019 amendment extended coverage to include mixed and contaminated plastic waste alongside previously regulated hazardous electronic waste, provides the international legal framework for restricting illegal e-waste exports from developed to developing countries, but enforcement capacity in both exporting and importing nations is frequently insufficient to intercept the significant volumes of e-waste that continue to move through informal export channels mislabeled as second-hand goods, functional equipment donations, or mixed scrap metal shipments, perpetuating the diversion of high-value feedstock from formal recyclers in developed markets to unregulated processing operations in West Africa, South Asia, and Southeast Asia. The livelihood dependency of large numbers of informal recycling workers on continued informal sector operations, particularly in major informal processing centers in Accra, Lagos, Mumbai, and Jakarta, creates social and political constraints on regulatory enforcement approaches that would abruptly eliminate informal recycling activity without providing alternative employment and technology upgrade pathways for the affected worker communities.

Rapid Product Design Complexity Increase, Adhesive Bonding and Miniaturization Trends, and Mixed Material Construction Reducing Manual Dismantling Efficiency and Automated Disassembly Feasibility

The relentless trend toward thinner, lighter, and more integrated consumer electronics product designs that prioritize form factor and aesthetics over end-of-life disassembly is progressively reducing the manual and automated dismantling efficiency of electronics recyclers by creating product architectures in which batteries are adhesive-bonded into device housings, displays are fused with digitizer assemblies using optically clear adhesive, components are soldered directly to motherboards without socketed connectors, and material-mixing construction methods combine thermoplastics, glass, ceramics, aluminum, and magnesium alloys in ways that resist efficient mechanical separation into clean material streams recoverable at commercial quality specifications. Modern smartphones represent a particularly acute design-for-recycling challenge, with batteries bonded using pull-tab adhesives that require specialized heating tools and manual dexterity to remove safely without damaging adjacent components, displays requiring heat application and suction cup separation tools for non-destructive removal, and internal component layouts optimized entirely for device size and weight minimization rather than disassembly sequence logic, creating labor-intensive dismantling processes whose cost at formal sector wage rates in developed countries approaches or exceeds the material value recoverable from individual devices, undermining the economics of manual preprocessing relative to whole-unit shredding approaches that sacrifice component-level material segregation quality for processing throughput. The European Union Ecodesign for Sustainable Products Regulation, which introduces mandatory disassembly design requirements for batteries in portable devices and establishes minimum repairability scores for selected consumer electronics categories, represents the most promising regulatory response to the design-for-recycling challenge, but implementation timelines extending to 2027 and beyond mean that the majority of devices entering the recycling waste stream through the forecast period will continue to reflect design philosophies developed without end-of-life considerations.

Commodity Price Volatility, Processing Economics Sensitivity to Precious Metal and Base Metal Price Cycles, and Capital Investment Uncertainty Constraining Formal Recycling Capacity Expansion

The financial viability of formal electronics recycling operations is heavily dependent on the prevailing prices of the recovered metals that constitute the primary revenue stream of the recycling business model, with precious metal prices and copper prices exhibiting significant interannual volatility that creates uncertainty in recycling operation profitability projections and complicates the investment appraisal for the substantial capital expenditures required to establish and expand certified processing infrastructure. A decline of 20% in gold prices from USD 2,400 to USD 1,920 per troy ounce reduces the revenue per metric ton of high-grade printed circuit board input by approximately USD 4,600, a reduction that can transform a marginally profitable processing operation into a loss-generating one without any change in operating costs, creating financial fragility in processing businesses that have invested in specialized smelting and refining infrastructure on the basis of business plans developed at peak precious metal price assumptions. The capital investment required to establish a commercially viable integrated electronics recycling facility with shredding, eddy current and density separation, sensor-based sorting, and precious metal smelting and refining capabilities ranges from USD 30 million to USD 150 million depending on processing scale and metal recovery technology depth, with payback periods of seven to twelve years that require stable commodity price assumptions and reliable long-term feedstock supply agreements that are difficult to secure in a market characterized by fragmented collection systems, competitive feedstock procurement, and volatile commodity pricing, creating investment hesitation among potential new entrants and constraining capacity expansion among existing operators whose balance sheets have been weakened by periods of commodity price depression.

Market Segmentation

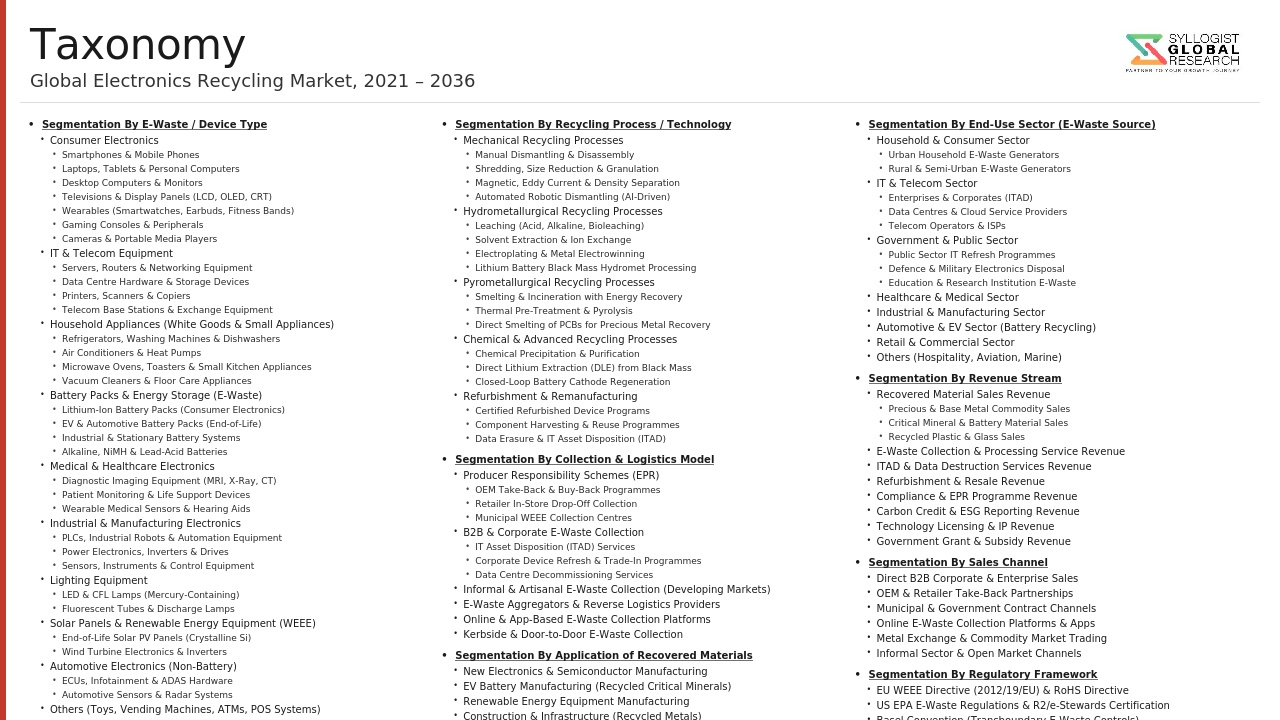

- Segmentation By Product Category

- Information Technology Equipment (Computers, Servers, Laptops, and Peripherals)

- Mobile Phones, Smartphones, and Tablets

- Consumer Electronics (Televisions, Audio Equipment, and Gaming Devices)

- Household Appliances (Large and Small Appliances)

- Electric Vehicle Batteries and Battery Packs

- Photovoltaic (Solar) Panels

- Telecommunications and Networking Infrastructure Equipment

- Industrial and Medical Electronics

- Power Tools and Portable Devices

- Others

- Segmentation By Recovered Material

- Precious Metals (Gold, Silver, and Platinum Group Metals)

- Copper and Copper Alloys

- Aluminum and Aluminum Alloys

- Steel and Ferrous Metals

- Battery Metals (Lithium, Cobalt, Nickel, and Manganese)

- Rare Earth Elements and Critical Minerals

- Engineered Plastics and Polymers

- Glass and Display Materials (Indium and Others)

- Others

- Segmentation By Processing Technology

- Manual Dismantling and Component Segregation

- Mechanical Shredding and Size Reduction

- Sensor-Based Sorting and Automated Separation (Eddy Current, Density, and Optical)

- Pyrometallurgical Smelting and Refining

- Hydrometallurgical Leaching, Solvent Extraction, and Electrowinning

- Direct Recycling and Battery Active Material Recovery

- Mechanical-Hydrometallurgical Hybrid Processing

- Others

- Segmentation By Collection Channel

- Original Equipment Manufacturer (OEM) Take-Back Programs

- Retailer and E-Commerce Platform Take-Back Schemes

- Municipal Collection Points and Curbside Programs

- Corporate IT Asset Disposal and Data Destruction Services

- Specialized E-Waste Drop-Off Centers

- Reverse Logistics and Broker Aggregation

- Others

- Segmentation By End User of Recovered Materials

- Electronics and Semiconductor Manufacturers

- Battery and Electric Vehicle Manufacturers

- Jewelry and Precious Metal Fabricators

- Commodity Metal Markets and Trading Houses

- Plastics Compounders and Polymer Recyclers

- Others

- Segmentation By Certification and Compliance Standard

- R2 (Responsible Recycling) Certified Operations

- e-Stewards Certified Operations

- ISO 14001 Environmental Management System Certified

- EU Waste Electrical and Electronic Equipment Directive Compliant

- Non-Certified and Informal Sector Operations

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Electronics Recycling Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product category including information technology equipment, mobile phones, consumer electronics, household appliances, electric vehicle batteries, photovoltaic panels, and industrial electronics, by recovered material including precious metals, copper, battery metals, rare earth elements, and engineered plastics, and by processing technology including manual dismantling, mechanical shredding and separation, pyrometallurgical smelting, hydrometallurgical processing, and battery direct recycling, to enable electronics recyclers, original equipment manufacturers with take-back obligations, battery manufacturers requiring recycled content compliance, commodity trading houses, and infrastructure investors to identify the highest-value product and material categories generating the most commercially resilient recycling economics across the forecast period to 2034?

- How is the projected growth in end-of-life electric vehicle battery volumes from approximately 280,000 metric tons in 2025 to approximately 1.4 million metric tons by 2034 reshaping the investment priorities, technology platform selection, processing capacity scale, offtake agreement structures, and competitive positioning of the global electronics recycling industry, and what are the comparative processing economics, material recovery rates for lithium, cobalt, nickel, and manganese, output quality specifications, capital investment requirements, and carbon footprint profiles of hydrometallurgical battery recycling, pyrometallurgical smelting, and direct cathode active material recycling approaches across the key lithium-ion battery chemistries including nickel manganese cobalt, lithium iron phosphate, and nickel cobalt aluminum that will collectively define commercially dominant battery recycling technology and operator competitive positions through 2034?

- What are the specific collection rate obligations, treatment standard requirements, producer responsibility fund structures, recycled content mandates, and enforcement mechanisms of the European Union Waste Electrical and Electronic Equipment Directive, the European Union Battery Regulation, the United States state-level e-waste legislation programs, Japan’s Home Appliance Recycling Law and Small Home Appliance Recycling Law, South Korea’s Extended Producer Responsibility program, China’s Waste Electrical and Electronic Equipment management regulations, and India’s E-Waste Management Rules, and how are these regulatory frameworks collectively creating mandatory and commercially quantifiable demand streams for formal electronics recycling services, what compliance investment is being mobilized in each jurisdiction, and how are regulatory differences across markets creating arbitrage opportunities or compliance barriers for international electronics recycling operators?

- What is the scale, geographic distribution, processing methodology, regulatory compliance status, environmental and health impact, and competitive economic dynamics of the global informal electronics recycling sector across major informal processing centers in West Africa, South Asia, and Southeast Asia, and what policy interventions including extended producer responsibility enforcement strengthening, informal sector operator technology upgrade support programs, Basel Convention export restriction enforcement, consumer awareness and formal collection incentive schemes, and blended finance mechanisms for formal processing capacity investment in developing countries are proving most effective in redirecting e-waste volumes from informal to formal processing channels in ways that improve material recovery efficiency, eliminate toxic exposure to waste workers, and develop commercially sustainable formal electronics recycling industries in rapidly growing e-waste generating markets?

- What are the design-for-recycling requirements, battery removability standards, minimum recyclability score frameworks, and mandatory disassembly instruction provisions being introduced by the European Union Ecodesign for Sustainable Products Regulation and equivalent product design sustainability regulations in Japan, South Korea, and California, how are leading electronics manufacturers including Apple, Samsung, HP, Dell, and Lenovo responding to these requirements through product architecture changes, adhesive substitution, modular design adoption, and material standardization programs, and what quantified improvements in manual dismantling labor time, automated disassembly feasibility, and material stream purity are achievable through compliant product design changes that would materially improve electronics recycling processing economics across the mobile phone, laptop, and small appliance product categories through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- E-Waste Feedstock Supply Consistency, Quality Variability & Informal Sector Competition Risk

- Regulatory, Transboundary Shipment, Basel Convention & EPR Compliance Risk

- Commodity Price Volatility & Recovered Metal Market Demand Risk

- Technology Processing Yield, Hazardous Material Handling & Operational Safety Risk

- Reputational, Environmental Liability & Social Licence Risk

- Regulatory Framework & Standards

- E-Waste Extended Producer Responsibility (EPR) Legislation, Collection Targets & Take-Back Scheme Frameworks by Region

- Basel Convention & Transboundary E-Waste Shipment Control Regulations: Hazardous Waste Export Restrictions & Prior Informed Consent Requirements

- Battery Regulation & End-of-Life Battery Collection Mandates: EU Battery Regulation (2023/1542), US Battery Act & National Battery Recycling Schemes

- Critical Raw Material, Strategic Metal Recycling Policy & Supply Chain Due Diligence Frameworks (EU CRM Act, US CHIPS Act Material Provisions, OECD Guidelines)

- Facility Environmental Permitting, Worker Health & Safety Standards, Emission Controls & Waste Management Certification for Electronics Recycling Operations

- Global Electronics Recycling Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes of E-Waste Collected & Processed)

- Market Size & Forecast by E-Waste Category

- IT & Telecom Equipment (Computers, Laptops, Tablets, Servers, Phones & Networking)

- Consumer Electronics (Televisions, Audio, Video & Gaming Devices)

- Large Household Appliances (Refrigerators, Washing Machines, Dishwashers & Air Conditioners)

- Small Household Appliances (Microwaves, Toasters, Vacuum Cleaners & Power Tools)

- Lighting Equipment (LED, CFL, Fluorescent Lamps & Smart Lighting)

- End-of-Life EV Battery Packs & Stationary Battery Energy Storage Systems (BESS)

- Solar Photovoltaic (PV) Panels & Renewable Energy Electronic Components

- Medical, Healthcare & Diagnostic Electronic Devices

- Industrial, Monitoring, Control & Measurement Instruments

- Market Size & Forecast by Recovered Material Type

- Precious Metals (Gold, Silver, Platinum & Palladium)

- Base Metals (Copper, Aluminium, Iron & Steel, Lead, Zinc & Tin)

- Battery & Critical Metals (Lithium, Cobalt, Nickel & Manganese)

- Rare Earth Elements & Specialty Metals (Neodymium, Dysprosium, Indium, Gallium & Germanium)

- Plastics, Polymers & Rubber

- Glass, Display Panel & Optical Materials

- Market Size & Forecast by Recycling Process

- Mechanical Pre-Processing (Shredding, Size Reduction, Eddy Current, Magnetic & Gravity Separation)

- Pyrometallurgical Processing (Copper Smelting, Secondary Refining & Precious Metal Recovery)

- Hydrometallurgical Processing (Leaching, Solvent Extraction, Ion Exchange & Electrowinning)

- Integrated Pyro-Hydrometallurgical Hybrid Processing

- Direct Battery Recycling & Black Mass Processing (Lithium, Cobalt & Nickel Recovery)

- Refurbishment, Reuse & Direct Re-Marketing (Pre-Recycling Circular Economy Route)

- Market Size & Forecast by Processing Stage

- Collection, Reverse Logistics & Aggregation

- Manual Dismantling, Component Harvesting & Pre-Sorting

- Primary Mechanical Processing & Material Separation

- Metallurgical Refining & Secondary Metal Production

- Certified Material Output, Commodity Sale & Circular Re-Entry

- Market Size & Forecast by End-Use Application of Recovered Materials

- Battery & Energy Storage Cell Manufacturing (Recycled Li, Co, Ni, Mn)

- Electronics & Semiconductor Manufacturing (Recycled Au, Ag, Cu, In, Ga)

- Automotive & EV Manufacturing (Recycled Al, Cu, Pb, PGMs)

- Renewable Energy Technology Manufacturing (Recycled REEs, Te, In, Cu)

- Construction, Infrastructure & General Engineering (Recycled Al, Fe, Cu)

- Jewellery, Investment & Luxury Goods (Recycled Au, Ag, Pt)

- Market Size & Forecast by End-User

- Electronics OEM & Consumer Electronics Brand (EPR-Obligated Producer)

- Specialist Electronics Recycler & Urban Mining Operator

- IT Asset Disposition (ITAD) & Data Destruction Service Provider

- Battery Recycling Specialist & Black Mass Processor

- Government, Municipality & Public Sector Collection Programme

- Refurbisher, Reuse Platform & Second-Life Electronics Operator

- Market Size & Forecast by Sales Channel

- Direct B2B Metal Offtake Agreement (Recycler to Smelter & Refiner)

- EPR Scheme, Compliance Scheme & Producer Take-Back Programme

- Municipal Collection, Government Tender & Public Sector Contract

- Online Platform, Commodity Exchange & Spot Market Trading

- North America Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Electronics Recycling Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Million Tonnes of E-Waste Collected & Processed)

- By E-Waste Category

- By Recovered Material Type

- By Recycling Process

- By Processing Stage

- By End-Use Application of Recovered Materials

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Belgium, Sweden, Norway, Japan, South Korea, China, India, Australia, Singapore, Thailand, Indonesia, Philippines, Brazil, Chile, South Africa, Nigeria, Ghana

- Technology Landscape & Innovation Analysis

- Automated Disassembly, Robotic Dismantling & AI-Driven Component Harvesting Technology Deep-Dive

- Advanced Mechanical Processing, Eddy Current, XRF Sorting & AI-Based Material Identification Technology

- Pyrometallurgical Smelting, Secondary Refining & Precious Metal Recovery Technology

- Hydrometallurgical Leaching, Solvent Extraction, Ion Exchange & Electrowinning Technology

- End-of-Life Battery Black Mass Processing, Lithium Recovery & Precursor Cathode Active Material (pCAM) Production Technology

- Solar PV Panel, NdFeB Magnet & Rare Earth Element Recovery Technology

- Digital Traceability, EPR Compliance Platform, Material Passport & Chain-of-Custody Technology

- Patent & IP Landscape in Electronics Recycling Technologies

- Value Chain & Supply Chain Analysis

- E-Waste Collection, Reverse Logistics, Aggregation & Informal Sector Formalisation

- Pre-Processing, Dismantling, Shredding & Sorting Equipment Manufacturer Supply Chain

- Pyrometallurgical & Hydrometallurgical Processing Technology & Reagent Supply Chain

- Specialist Electronics Recycler, Urban Mining Operator & Secondary Smelter Landscape

- Refiner, Secondary Metal Producer & OEM Closed-Loop Integration

- Recovered Metal Offtake, Commodity Trading & Battery Circular Economy Loop

- Residue Treatment, Hazardous Waste Disposal & Zero-Waste Processing Strategy

- Pricing Analysis

- Precious Metal (Gold, Silver, Platinum & Palladium) Recovery from E-Waste Pricing Analysis

- Base Metal (Copper, Aluminium & Iron) Recovery from Electronics Pricing Analysis

- Battery Metal (Lithium, Cobalt & Nickel) Black Mass & Recovered Material Pricing Analysis

- E-Waste Processing Fee, Gate Fee & Tipping Fee Structure Analysis by Category & Region

- Rare Earth Element & Specialty Metal Recovery Pricing Analysis

- Total Electronics Recycling Project Economics & Recovered Material Value vs. Virgin Material Benchmark

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Electronics Recycling vs. Primary Metal Extraction: Carbon Footprint, Energy Intensity & Water Use Comparison

- GHG Emission Reduction, Circular Economy Contribution & Critical Material Supply Resilience of Electronics Recycling

- Hazardous Substance Management (Lead, Mercury, Cadmium, Brominated Flame Retardants), Worker Health & Community Safety

- Informal Sector Impact, Social Sustainability & Fair Trade Recycling Frameworks in Developing Economies

- Regulatory-Driven Sustainability, Digital Product Passport, Responsible Sourcing Certification & Extended Producer Responsibility Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by E-Waste Category & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by E-Waste Category, Recovered Metal & Geography

- Player Classification

- Integrated Metals & Mining Companies with Electronics Recycling Divisions

- Specialist Full-Service Electronics Recyclers & Urban Mining Operators

- End-of-Life Battery Recycling & Black Mass Processing Specialists

- IT Asset Disposition (ITAD), Data Destruction & Enterprise Electronics Recyclers

- Precious Metal Secondary Smelters & Refinery Operators

- Municipal, Government-Operated & NGO E-Waste Collection Programmes

- Reverse Logistics, Collection Platform & Informal Sector Formalisation Companies

- Electronics Recycling Equipment, Sorting Technology & Reagent Suppliers

- Competitive Analysis Frameworks

- Market Share Analysis by E-Waste Category, Recovered Material & Region

- Company Profile

- Company Overview & Headquarters

- Electronics Recycling Services, Products & Technology Portfolio

- Key Customer Relationships, OEM Partnerships & Offtake Agreements

- Processing Facility Footprint & Annual E-Waste Throughput Capacity

- Revenue (Electronics Recycling Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Certifications, Contract Wins)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By E-Waste Category, Recovered Material, Recycling Process, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & OEM Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)