Market Definition

The Global AI-Driven Air Traffic Management Systems Market encompasses the design, development, integration, deployment, and sustainment of artificial intelligence, machine learning, deep learning, and advanced data analytics technologies embedded within or overlaid upon air traffic management infrastructure to automate, augment, and optimize the planning, sequencing, separation assurance, flow management, and safety monitoring functions performed by air traffic control authorities, airspace management agencies, and aeronautical navigation service providers across en-route, terminal, approach, and airport surface operational domains. An AI-driven air traffic management system is a decision-support or decision-automation platform engineered to ingest and process real-time surveillance data from radar, automatic dependent surveillance-broadcast, multilateration, and satellite navigation sources, meteorological feed data, flight plan databases, and airport operational status streams, applying trained predictive models and optimization algorithms to generate trajectory conflict alerts, demand-capacity balancing recommendations, runway sequencing advisories, weather deviation guidance, and flow restriction management outputs that enable air traffic controllers and airspace managers to maintain safe, efficient, and capacity-maximized aircraft separation across all phases of flight. The market encompasses the complete AI-enabled air traffic management value chain, including data fusion and correlation engines, machine learning model training and inference infrastructure, conflict detection and resolution algorithm modules, traffic flow management optimization platforms, digital tower and remote tower AI systems, unmanned aircraft system traffic management integration platforms, surface movement guidance and control AI modules, communication and surveillance data processing hardware, and the software integration, certification, validation, and training services that constitute the full lifecycle delivery of an AI-driven air traffic management capability. Key participants include air navigation service providers, civil aviation authorities and regulators, airport operators, air traffic management technology prime contractors, avionics and surveillance system suppliers, cloud and edge computing infrastructure providers, and international standardization bodies whose safety certification and interoperability frameworks define the qualification requirements governing AI system deployment in regulated airspace globally.

Market Insights

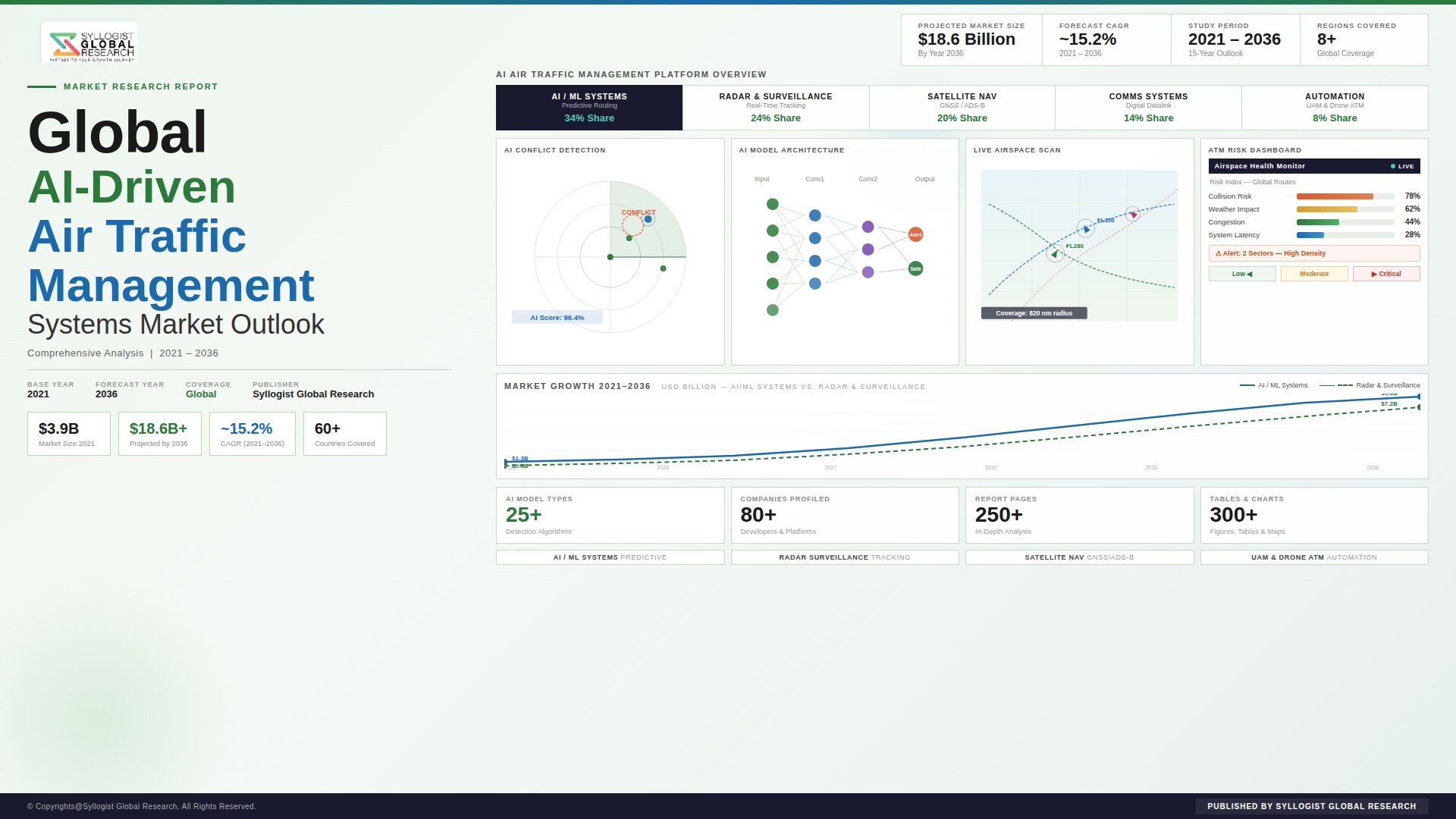

The global AI-driven air traffic management systems market is entering a period of accelerating structural expansion, underpinned by the simultaneous pressure of recovering and growing global air traffic volumes that are straining the capacity limits of legacy procedural and radar-based air traffic management infrastructure, the proliferation of unmanned aircraft systems and advanced air mobility vehicles that are introducing airspace complexity levels that human-only controller workloads are operationally incapable of managing at scale, and a broad recognition among air navigation service providers and civil aviation regulators that artificial intelligence and machine learning represent the only technically credible pathway to the step-change capacity, efficiency, and safety improvements required to accommodate forecast aviation demand growth without proportional increases in controller headcount or infrastructure capital expenditure. The global AI-driven air traffic management systems market was valued at approximately USD 2.4 billion in 2025 and is projected to reach USD 7.9 billion by 2034, advancing at a compound annual growth rate of 14.2% over the forecast period from 2027 to 2034, as air navigation service providers across North America, Europe, Asia-Pacific, and the Middle East accelerate procurement of AI-enabled traffic flow management, conflict detection and resolution, and digital tower platforms as modernization program priorities embedded within multi-year capital investment frameworks. The structural demand for AI-driven air traffic management capability is reinforced by binding international civil aviation regulatory modernization mandates, including the Federal Aviation Administration NextGen transformation program, the European Single European Sky ATM Research program known as SESAR, and equivalent modernization frameworks in China, India, Japan, and the Gulf Cooperation Council states, that collectively define legally anchored investment timelines and performance requirements compelling air navigation service providers to upgrade legacy system architectures with AI-capable data processing and decision support infrastructure within defined regulatory compliance deadlines.

The technology landscape of AI-driven air traffic management is structured around three principal capability layers whose deployment maturity and operational adoption trajectories are progressing at differentiated rates across the global air navigation service provider community. The traffic flow management and demand-capacity balancing layer, which applies machine learning forecasting models to predict sector capacity saturation, weather impact propagation, and airport departure and arrival demand imbalances with sufficient lead time to enable proactive flow restriction and rerouting interventions rather than reactive ground delay program responses, represents the most operationally mature and widely deployed AI application category within air traffic management, with several leading air navigation service providers in the United States and Europe having transitioned AI-assisted traffic flow management tools from experimental program status to operational deployment integrated into live air traffic control facility workflows. The conflict detection and resolution layer, encompassing AI algorithms that process surveillance data streams to generate short-term conflict alerts and medium-term trajectory conflict predictions with confidence scoring that prioritizes controller attention on the highest-probability separation events within dense traffic environments, represents the most safety-critical and therefore the most certification-intensive AI application domain within air traffic management, with regulatory approval frameworks requiring extensive operational safety assessment, failure mode analysis, and controller interaction validation before AI conflict detection outputs can be integrated into operational separation assurance workflows rather than deployed solely as advisory tools supplementing established radar separation procedures. The digital tower and remote tower AI layer, integrating computer vision, object detection, and situational awareness augmentation algorithms into camera-based airport surface surveillance and visual approach monitoring systems, is the most commercially dynamic segment at a projected compound annual growth rate of 18.3% through 2034, driven by airport operator demand for cost-effective alternatives to conventional staffed tower infrastructure and by demonstrated operational deployment of digital tower systems at airports across Sweden, Norway, Australia, and multiple other national aviation systems.

From a regional standpoint, North America constitutes the largest revenue-generating market for AI-driven air traffic management systems, anchored by the Federal Aviation Administration’s multi-billion-dollar NextGen modernization investment program whose Traffic Flow Management System replacement, En Route Automation Modernization successor program, and Terminal Flight Data Manager modernization collectively represent the largest single-authority procurement opportunity for AI-enabled air traffic management technology globally, supplemented by Nav Canada’s advanced trajectory-based operations and machine learning traffic forecasting capability development program and the substantial commercial aviation infrastructure investment of major United States airport operators pursuing digital tower and surface movement AI deployment. Europe represents the second-largest and most regulatory-driven regional market, with the SESAR deployment program defining a legally mandated modernization roadmap that requires European Union member state air navigation service providers to implement trajectory-based operations, AI-assisted demand-capacity balancing, and automated separation assurance tooling across the functional airspace blocks of European airspace within defined implementation milestones, generating a procurement demand stream that is contractually anchored in European Commission regulatory obligation rather than in discretionary technology investment decisions of individual air navigation service providers. Asia-Pacific is the fastest-growing regional procurement market, driven by the extraordinary scale of Chinese civil aviation infrastructure expansion in which the Civil Aviation Administration of China is simultaneously constructing new airports, expanding existing terminal and en-route air traffic management infrastructure, and procuring AI-enabled automation capability as an integrated design element of new facility builds rather than as a retrofit to legacy systems, alongside the rapid air traffic volume growth of Indian civil aviation that is compelling the Airports Authority of India to accelerate adoption of AI-assisted traffic flow and conflict detection tools to manage the expanding complexity of the Indian airspace system.

The integration of unmanned aircraft system traffic management and advanced air mobility vehicle coordination requirements into the scope of AI-driven air traffic management platforms represents the most transformative structural demand expansion driver emerging within the market over the forecast period, as the anticipated scaling of commercial drone delivery operations, urban air mobility passenger services, and unmanned cargo aircraft across controlled and uncontrolled airspace introduces traffic density, operational diversity, and dynamic airspace access management requirements that are categorically beyond the processing and response capacity of human-only air traffic control workflows, creating a structurally new and high-growth AI platform requirement for autonomous or near-autonomous unmanned traffic management capability that must interface with conventional manned air traffic management systems while independently managing millions of simultaneous unmanned vehicle operations across low-altitude urban and suburban airspace environments. The data governance, cybersecurity, and system resilience architecture requirements of AI-driven air traffic management platforms are simultaneously emerging as a significant procurement consideration, as the criticality of continuous, uninterrupted, and tamper-resistant AI system performance in safety-of-life airspace management applications requires AI platform developers to satisfy substantially more demanding cybersecurity certification, adversarial input robustness, and system failure graceful degradation requirements than those applicable to AI systems deployed in non-safety-critical commercial applications, generating a sustained investment requirement in AI platform hardening, redundancy architecture, and real-time performance monitoring capability that is a recurring feature of air traffic management AI procurement specifications across all major national programs and that creates a structurally higher barrier to entry for AI system suppliers without established aviation safety certification credentials and operational reliability track records in regulated air traffic management environments.

Key Drivers

Surging Global Air Traffic Volume Growth and Legacy System Capacity Constraints Compelling AI-Enabled Airspace Modernization Across Major Aviation Markets

Global air traffic volumes recovered to approximately 94% of pre-pandemic levels by the end of 2024 and are forecast to exceed prior peak traffic levels by 2026, with the International Civil Aviation Organization projecting sustained annual passenger traffic growth of approximately 3.6% through 2040, generating a cumulative traffic volume expansion that will require the global air traffic management system to accommodate approximately twice its current daily flight volume within the forecast horizon while maintaining or improving the safety, punctuality, and fuel efficiency performance benchmarks against which air navigation service providers are held accountable by regulators, airspace users, and national governments. Legacy procedural and radar-based air traffic management systems, designed around traffic density assumptions and operational complexity levels that prevailed at the time of their development decades ago, are encountering capacity ceiling constraints in the highest-density airspace environments of North America, Europe, and Asia-Pacific that are manifesting as increasing rates of traffic flow restriction, extended ground delay program activation frequency, and sector capacity saturation events that impose measurable economic costs on airlines, passengers, and national economies through fuel burn inefficiency and schedule disruption. AI-driven traffic flow management, conflict detection, and automated separation assurance systems offer the technically validated pathway to capacity expansion without proportional physical infrastructure investment or controller workforce scaling, by enabling higher traffic density operation within existing airspace structures through AI-optimized trajectory spacing, predictive demand management, and controller workload distribution algorithms that extract latent capacity from existing airspace architecture rather than requiring the physical restructuring of sector boundaries or the construction of additional control facility infrastructure.

Regulatory Modernization Mandates and Internationally Coordinated Airspace Transformation Programs Creating Binding Procurement Timelines for AI-Capable System Upgrades

The binding regulatory modernization frameworks established by major civil aviation authorities and regional airspace management bodies are generating a contractually anchored demand stream for AI-enabled air traffic management technology that is substantially insulated from the discretionary budget variability affecting commercial technology procurement in non-regulated industries, as air navigation service providers operating under Federal Aviation Administration NextGen compliance requirements, SESAR deployment regulation obligations, Civil Aviation Administration of China modernization mandates, and equivalent national frameworks are legally required to implement AI-capable trajectory-based operations, automated separation assurance tooling, and performance-based navigation infrastructure within defined implementation milestones regardless of short-term fiscal constraints. The European Single European Sky regulatory framework, reinforced by European Commission implementing regulations that establish legally binding performance targets for capacity, cost-efficiency, safety, and environmental sustainability across European Union member state air navigation service providers, creates a particularly powerful structural procurement driver by linking air navigation service provider revenue entitlement and regulatory compliance status to the demonstrated achievement of technology-enabled performance targets that are technically unachievable with legacy non-AI-assisted system architectures at the traffic density levels projected for the current and next regulatory reference period. The convergence of these nationally and regionally enacted regulatory modernization programs across the major global aviation markets is generating a synchronized global procurement cycle for AI-enabled air traffic management technology whose timing, scope, and minimum performance requirements are defined by regulatory compliance necessity rather than by technology adoption enthusiasm, providing AI system developers and integrators with a high-visibility, multi-year procurement pipeline characterized by defined program schedules and publicly documented technical requirements that enable investment in tailored solution development and certification program execution.

Proliferation of Unmanned Aircraft Systems and Advanced Air Mobility Vehicles Generating Structurally New AI Platform Requirements for Automated Traffic Management at Scale

The anticipated commercial scaling of unmanned aircraft system delivery operations, urban air mobility passenger services, unmanned cargo aircraft, and high-altitude platform station operations is introducing airspace user categories whose operational characteristics, traffic density, and dynamic airspace access requirements are categorically incompatible with management through conventional human-controller-based air traffic management procedures, creating a structurally new and large addressable market for AI-driven autonomous unmanned traffic management platforms that must simultaneously process thousands to millions of vehicle trajectory requests, allocate dynamic airspace blocks and flight corridors, detect and resolve conflicts within unmanned vehicle populations operating at separations substantially smaller than manned aviation minima, and interface the unmanned traffic management operating environment with conventional manned air traffic control systems to ensure coordinated and safe mixed-operations airspace management. The Federal Aviation Administration UAS Traffic Management research and development program, the European Union Aviation Safety Agency U-space regulatory framework, the Civil Aviation Administration of China unmanned aerial vehicle airspace integration initiative, and equivalent national unmanned traffic management development programs across Japan, Australia, Singapore, and the United Kingdom are collectively generating a globally coordinated development and procurement investment in AI-driven unmanned traffic management infrastructure that will represent a commercially significant incremental market segment layered on top of the existing conventional air traffic management AI modernization market. The per-operation AI processing and platform hosting cost structure of commercial unmanned traffic management services, which must be sufficiently low to enable economically viable drone delivery and urban air mobility business models while sustaining the AI platform infrastructure investment required for safe and reliable operation, is driving unmanned traffic management platform developers toward highly automated, cloud-native AI architectures with near-zero marginal cost per additional vehicle managed, creating a structurally distinct technology and commercial model that is generating a new entrant competitive dynamic within the broader AI-driven air traffic management market.

Key Challenges

Safety Certification Complexity and Regulatory Approval Timelines for AI Systems in Safety-of-Life Airspace Management Applications Constraining Deployment Pace

The deployment of artificial intelligence and machine learning systems within operational air traffic management workflows is subject to the most stringent and process-intensive safety certification requirements applicable to any commercial AI application domain, as the safety-of-life consequences of AI system malfunction, unexpected behavior, or adversarial manipulation in live air traffic control environments require regulators to validate not only the functional performance of AI systems under normal operating conditions but also their failure mode behavior, output reliability under out-of-distribution input conditions, and graceful degradation characteristics when operating with degraded input data quality or partial system failure, generating certification timelines and validation evidence production costs that substantially extend the development-to-deployment cycle of AI air traffic management products relative to AI systems deployed in non-safety-critical commercial applications. The absence of internationally harmonized AI-specific certification standards for air traffic management applications, with the European Union Aviation Safety Agency, the Federal Aviation Administration, and the Civil Aviation Administration of China each developing AI certification guidance frameworks on differentiated timelines and with partially divergent technical requirements, creates a multi-jurisdiction certification burden for AI system developers targeting global market deployment that multiplies the safety case documentation, operational evaluation evidence, and regulatory engagement resource requirements required to achieve operational approval across the major civil aviation regulatory jurisdictions representing the core global market opportunity. The fundamental explainability challenge associated with deep learning and neural network AI architectures, whose internal decision-making processes are not readily interpretable by human safety assessors using conventional deterministic software verification methods, creates a systemic certification methodology gap that current regulatory frameworks have not fully resolved, compelling AI system developers to pursue hybrid architectures combining explainable rule-based logic with constrained machine learning components that preserve certification tractability at the cost of limiting the performance ceiling achievable through unconstrained deep learning approaches.

Controller Acceptance, Human-Machine Teaming Transition Challenges, and Workforce Training Requirements Limiting Operational Integration of AI Decision Support Tools

The successful operational deployment of AI-driven decision support and automation tools within air traffic management facilities depends critically on the acceptance, trust calibration, and effective human-machine teaming behavior of the air traffic controller workforce whose professional judgment and situational awareness these tools are designed to augment, and the evidence from early AI tool deployment programs indicates that controller acceptance is frequently constrained by concerns about AI system reliability in rare or novel traffic scenarios, reluctance to alter well-established manual cognitive workflows developed over years of operational experience, and uncertainty about the appropriate degree of reliance on AI outputs in high-workload or degraded system performance situations, generating operational adoption gaps between technically deployed and operationally utilized AI capability that undermine the efficiency and capacity benefits that AI system procurement is intended to deliver. The air traffic controller workforce in major aviation markets is represented by professional unions whose collective bargaining agreements and operational safety protocols govern the introduction of new automation tools and whose endorsement or opposition to AI decision support system deployment significantly influences the pace and scope of operational adoption within facilities subject to labor agreement constraints, creating a stakeholder engagement and workforce consultation requirement that adds timeline and organizational complexity to AI system deployment programs that purely technical certification and procurement processes do not account for. The training investment required to develop the appropriate trust calibration, exception management skills, and AI system interaction competencies that enable controllers to use AI decision support tools effectively and safely in live operational environments is substantially higher than the training investment associated with introducing conventional procedural updates or non-AI software tools, requiring air navigation service providers to fund extended simulator-based AI interaction training programs and to manage the operational availability impacts of withdrawing experienced controllers from live traffic duty for AI proficiency development.

Cybersecurity Vulnerabilities, Data Integrity Risks, and Adversarial Attack Exposure of AI-Enabled Air Traffic Management Platforms in Safety-Critical Operational Environments

AI-driven air traffic management platforms represent high-consequence cybersecurity targets whose compromise, data manipulation, or service disruption could generate safety-critical airspace management failures affecting thousands of aircraft and millions of passengers simultaneously, creating a cybersecurity risk profile that substantially exceeds the threat exposure of conventional non-AI air traffic management systems by introducing adversarial machine learning attack vectors, training data poisoning vulnerabilities, and AI model input manipulation risks that are absent from the threat models applicable to deterministic rule-based air traffic management software architectures and for which current aviation cybersecurity certification frameworks were not designed. The dependency of AI air traffic management systems on continuous, high-integrity, and high-availability data feeds from surveillance sensors, meteorological services, flight data processors, and airport operational databases creates an expanded attack surface relative to conventional systems, as adversarial actors capable of injecting false or manipulated data into any of these upstream feeds can potentially corrupt AI model inputs in ways that cause AI systems to generate incorrect conflict alerts, erroneous flow management recommendations, or miscalibrated trajectory predictions that degrade controller situational awareness and compromise separation assurance without triggering the system error flags that would alert controllers to a data integrity failure. The requirement to continuously update, retrain, and patch AI model components as air traffic patterns evolve, new aircraft types enter service, and threat intelligence identifies emerging adversarial attack techniques creates a software lifecycle management and supply chain security challenge that air navigation service providers and their AI system suppliers must address through rigorous model validation, change management certification, and software integrity verification processes that are substantially more complex and resource-intensive than the patch management and software update processes applicable to conventional air traffic management system components.

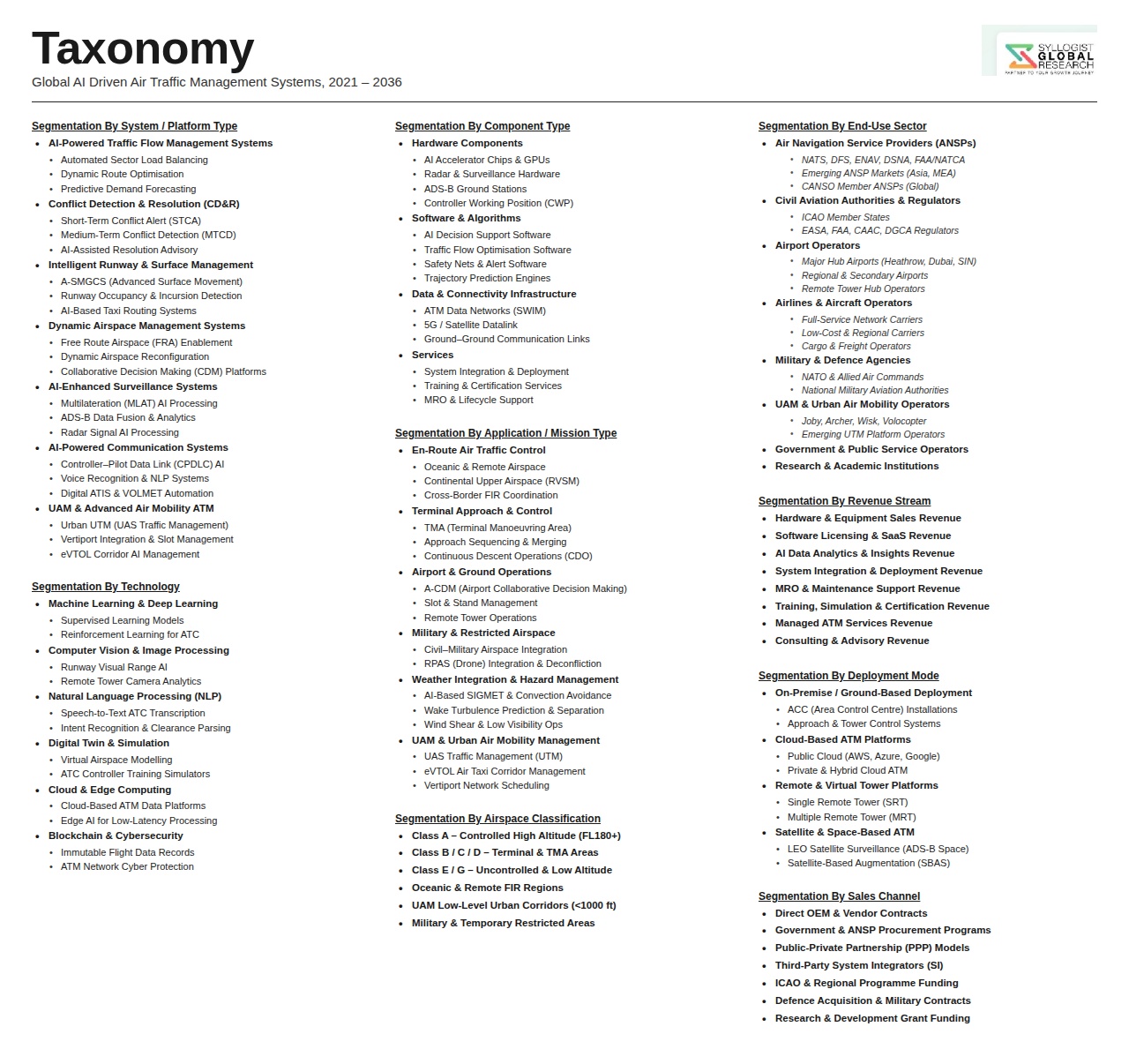

Market Segmentation

- Segmentation By Component

- AI Software Platforms and Algorithm Modules

- Data Fusion and Surveillance Processing Systems

- Hardware and Computing Infrastructure

- Integration, Implementation, and Consulting Services

- Maintenance, Support, and Managed Services

- Others

- Segmentation By AI Technology Type

- Machine Learning and Predictive Analytics

- Deep Learning and Neural Network Systems

- Natural Language Processing and Voice Recognition

- Computer Vision and Object Detection

- Reinforcement Learning and Optimization Algorithms

- Knowledge-Based and Expert AI Systems

- Others

- Segmentation By Application

- Traffic Flow Management and Demand-Capacity Balancing

- Conflict Detection and Resolution

- Trajectory Prediction and Optimization

- Digital Tower and Remote Tower Operations

- Surface Movement Guidance and Control

- Meteorological Impact Assessment and Weather Integration

- Unmanned Aircraft System Traffic Management (UTM)

- Advanced Air Mobility Integration

- Cybersecurity and System Integrity Monitoring

- Others

- Segmentation By Airspace Class and Operational Domain

- En-Route and Upper Airspace Management

- Terminal Maneuvering Area Operations

- Approach and Landing Management

- Airport Surface and Ground Movement Operations

- Low Altitude and Urban Airspace (Unmanned Traffic)

- Oceanic and Remote Airspace Management

- Segmentation By Deployment Model

- On-Premises and Facility-Integrated Deployment

- Cloud-Based and Hosted Platforms

- Hybrid On-Premises and Cloud Architecture

- Edge Computing-Based Deployment

- Segmentation By End User

- Air Navigation Service Providers (ANSPs)

- Civil Aviation Authorities and Regulatory Bodies

- Airport Operators and Ground Handlers

- Airlines and Aircraft Operators

- Military and Defense Aviation Authorities

- Unmanned Aircraft System Operators and UTM Service Providers

- Others

- Segmentation By Communication Infrastructure

- VHF and HF Voice and Data Communication Integration

- Automatic Dependent Surveillance-Broadcast (ADS-B) Integration

- System Wide Information Management (SWIM) Platforms

- Satellite-Based Communication and Navigation Integration

- 5G and Next-Generation Terrestrial Communication Integration

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the AI-Driven Air Traffic Management Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by component, AI software platforms, data fusion systems, hardware infrastructure, and services, and by application, traffic flow management, conflict detection and resolution, digital tower, and unmanned traffic management, to enable air navigation service providers, civil aviation technology contractors, AI platform developers, infrastructure investors, and aviation regulators to identify which application segment and deployment model will generate the highest absolute revenue and the most durable adoption growth trajectory across the forecast period?

- How are the Federal Aviation Administration NextGen program, the European Single European Sky ATM Research SESAR deployment regulation, the Civil Aviation Administration of China airspace modernization mandate, and equivalent national civil aviation regulatory frameworks shaping AI-enabled air traffic management procurement timelines, minimum technical performance requirements, and safety certification standards across the major global aviation markets, and what is the aggregate regulatory compliance-driven AI system procurement investment that air navigation service providers across North America, Europe, and Asia-Pacific are committed to executing between 2025 and 2034 under binding implementation schedules?

- What is the projected market size, compound annual growth rate, and competitive landscape of the unmanned aircraft system traffic management and advanced air mobility AI integration segment through 2034, and which national regulatory frameworks, commercial unmanned delivery and urban air mobility deployment programs, and AI platform architecture approaches, cloud-native autonomous management versus human-supervised advisory systems, are expected to generate the largest incremental AI platform procurement volumes and the most significant expansion of the total addressable AI-driven air traffic management market beyond its conventional manned aviation base?

- How are AI safety certification complexity, regulatory approval timelines, controller workforce acceptance constraints, and the absence of internationally harmonized AI-specific certification standards affecting the development-to-deployment cycle, market entry barriers, and competitive positioning of AI air traffic management system developers across the Federal Aviation Administration, European Union Aviation Safety Agency, and Civil Aviation Administration of China regulatory jurisdictions, and what certification strategy approaches and human-machine interface design choices are proving most effective in accelerating operational approval and controller adoption of AI decision support tools in live air traffic management facility environments?

- Who are the leading air traffic management technology prime contractors, AI software platform developers, surveillance and data fusion system suppliers, digital tower technology specialists, and unmanned traffic management platform providers currently defining the competitive landscape of the global AI-driven air traffic management systems market, and what are their respective program portfolios across traffic flow management, conflict detection, digital tower, and unmanned traffic management application segments, strategic partnerships with air navigation service providers and civil aviation authorities, technology development roadmaps for next-generation autonomous separation assurance and AI-native air traffic management capability, and competitive positioning in the major national modernization procurement programs expected to generate the largest contract awards through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cybersecurity, Data Integrity & Critical Infrastructure Vulnerability Risk

- AI Algorithm Reliability, Failure Modes & Safety Certification Risk

- Regulatory Fragmentation, Cross-Border Airspace Sovereignty & Harmonisation Risk

- Legacy System Integration, Interoperability & Technology Transition Risk

- Workforce Displacement, Human-Machine Trust & Controller Acceptance Risk

- Regulatory Framework & Standards

- ICAO Standards & Recommended Practices (SARPs) for ATM Modernisation & AI Integration

- FAA NextGen Programme, Performance-Based Navigation (PBN) & AI Deployment Regulatory Framework

- European SESAR Programme, Single European Sky (SES) & EASA AI Airworthiness Standards

- Asia-Pacific ICAO Regional ATM Implementation Plans & National Civil Aviation Authority AI Frameworks

- Cybersecurity Standards, AI Safety Certification & Data Governance Frameworks for ATM Systems

- Global AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (System Installations & Software Licences)

- Market Size & Forecast by Component

- AI Software Platforms: Conflict Detection, Traffic Flow Optimisation & Predictive Analytics

- Hardware Infrastructure: Servers, Edge Computing Nodes & Sensor Integration Units

- Communication Systems: VHF/UHF Datalink, ACARS & Satellite Communication Integration

- Surveillance Systems: ADS-B, Multilateration (MLAT), Radar & Remote Sensing Integration

- Navigation & Positioning Systems: GNSS, ILS, VOR & Performance-Based Navigation Integration

- Data Fusion, Display & Controller Working Position (CWP) Systems

- Maintenance, Support & Managed Service Solutions

- Market Size & Forecast by Technology

- Machine Learning & Deep Learning for Traffic Pattern Recognition & Conflict Prediction

- Natural Language Processing (NLP) for Controller-Pilot Datalink Communication (CPDLC) Automation

- Digital Twin & Simulation Technology for Airspace Modelling & Scenario Planning

- Reinforcement Learning for Dynamic Airspace Sectorisation & Flow Management

- Computer Vision & Remote Tower Technology for Virtual Air Traffic Control

- Blockchain & Distributed Ledger Technology for Secure ATM Data Exchange

- Cloud Computing, Edge AI & Hybrid Deployment Architecture for ATM Systems

- Quantum Computing & Advanced Optimisation Algorithms for Airspace Capacity Management

- Market Size & Forecast by Autonomy Level

- Decision-Support Systems: AI-Augmented Human Controller Assistance

- Semi-Automated Systems: Human-on-the-Loop Conflict Resolution & Flow Management

- Highly Automated Systems: AI-Initiated Actions with Human Oversight & Approval

- Fully Autonomous ATM: Unsupervised AI Operations in Designated Airspace Segments

- Market Size & Forecast by Application

- En-Route Traffic Flow Management & Airspace Capacity Optimisation

- Terminal Manoeuvring Area (TMA) & Approach Sequencing Automation

- Airport Surface Movement Guidance & Runway Optimisation

- Conflict Detection & Resolution (CD&R) and Separation Assurance

- Demand-Capacity Balancing (DCB) & Network Flow Management

- Unmanned Traffic Management (UTM) & Urban Air Mobility (UAM) Integration

- Remote & Virtual Tower Operations for Small & Regional Aerodromes

- Emergency, Search & Rescue Coordination & Contingency Traffic Management

- Market Size & Forecast by Airspace Class & Operation Type

- Controlled Airspace: Class A, B & C High-Density Operations

- Terminal Control Area & Approach Control Operations

- Oceanic & Remote Airspace Operations

- Low-Level & Urban Airspace: UTM, UAM & Advanced Air Mobility (AAM) Corridors

- Market Size & Forecast by End-User

- Air Navigation Service Providers (ANSPs)

- Civil Aviation Authorities (CAAs) & National Regulatory Bodies

- Airport Operators & Ground Handling Organisations

- Airlines & Flight Operations Centres

- Military & Defence Aviation Commands

- UAM, AAM & Drone Logistics Operators

- Market Size & Forecast by Sales Channel

- Direct OEM Supply & System Integration Contract

- Government Tender, Public Procurement & Regulatory Mandate Programme

- Public-Private Partnership (PPP) & Build-Operate-Transfer (BOT) Framework

- Software-as-a-Service (SaaS), Managed Service & Cloud Subscription Model

- North America AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* AI-Driven Air Traffic Management Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (System Installations & Software Licences)

- By Component

- By Technology

- By Autonomy Level

- By Application

- By Airspace Class & Operation Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Machine Learning & Predictive Analytics for Conflict Detection & Traffic Flow Optimisation Deep-Dive

- Natural Language Processing & CPDLC Automation for Controller-Pilot Communication

- Digital Twin, Simulation & Synthetic Training Environment Technology for ATM

- Remote & Virtual Tower Technology: Computer Vision, AI Decision Support & Multi-Airport Management

- Unmanned Traffic Management (UTM) & Urban Air Mobility (UAM) AI Integration Technology

- Cloud, Edge AI & Hybrid Deployment Architecture for Scalable ATM Infrastructure

- Cybersecurity, AI Explainability & Safety Certification Technology for ATM Systems

- Patent & IP Landscape in AI-Driven Air Traffic Management Technologies

- Value Chain & Supply Chain Analysis

- AI Software, Algorithm Development & Autonomy Stack Supply Chain

- Surveillance Equipment: Radar, ADS-B, MLAT & Sensor Hardware Supply Chain

- Communication & Datalink Equipment Supply Chain

- Computing Infrastructure, Servers & Edge Hardware Supply Chain

- System Integration, Test & Validation Services Supply Chain

- ANSP, Civil Aviation Authority & Airport Operator Procurement Landscape

- MRO, Software Updates, Upgrades & Through-Life Support Channel

- Pricing Analysis

- AI Decision-Support & Traffic Flow Optimisation Software Licensing & Subscription Cost Analysis

- Remote & Virtual Tower System Capital & Operating Cost Analysis

- End-to-End ATM Modernisation Programme Capital & Integration Cost Analysis

- UTM & UAM Platform Deployment & Operational Cost Analysis

- Cloud-Based ATM SaaS vs. On-Premise Deployment Total Cost of Ownership Comparison

- Total Programme Economics: Development, Certification, Deployment & Lifecycle Cost Modelling

- Sustainability & Environmental Analysis

- AI-Optimised Routing, Continuous Climb & Descent Operations: Aviation Fuel Burn & CO2 Reduction Contribution

- Dynamic Airspace Configuration & Capacity Management: Congestion Reduction & Noise Abatement Benefits

- Remote Tower & Virtualisation: Infrastructure Footprint Reduction & Energy Efficiency at Regional Aerodromes

- Sustainable Aviation Fuel (SAF) Route Planning & Carbon-Neutral Flight Path Integration in AI-ATM Systems

- ICAO Carbon Offsetting & Reduction Scheme for International Aviation (CORSIA) Compliance & ATM Contribution

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Component & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Component, Technology & Geography

- Player Classification

- Established ATM OEMs & System Integrators with AI Capabilities

- Pure-Play AI & Machine Learning Platform Providers for Aviation

- Surveillance, Communication & Navigation Equipment Manufacturers

- Remote & Virtual Tower Technology Specialists

- UTM & Urban Air Mobility Platform Developers

- Cloud, Data Analytics & Digital Twin Platform Providers for ATM

- Cybersecurity & AI Safety Certification Solution Providers

- Aviation Technology Start-ups & Academic Spin-Offs

- Competitive Analysis Frameworks

- Market Share Analysis by Component, Technology & Region

- Company Profile

- Company Overview & Headquarters

- AI-Driven ATM Products & System Portfolio

- Key Customer Relationships & Reference Deployments

- Manufacturing Footprint & Development Centre Locations

- Revenue (ATM Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, System Go-Lives, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Component, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output