Market Definition

The Global Military Radar Systems Market encompasses the design, engineering, development, manufacturing, integration, testing, and sustainment of ground-based, airborne, naval, and space-based radio detection and ranging systems developed and procured by defense ministries, armed forces, coast guards, and national security agencies for the detection, tracking, classification, identification, and engagement cueing of airborne, surface, subsurface, and ballistic targets across all operational domains and threat environments. A military radar system is an electromagnetic sensor platform engineered to transmit radio frequency energy pulses or continuous waveforms into the operational environment, receive and process the reflected or backscattered energy returned from target objects, and generate actionable track, range, azimuth, elevation, and velocity data outputs that populate air and missile defense command and control networks, fire control systems, airborne early warning and control architectures, maritime surveillance infrastructures, and ground battlefield management systems with the target state information required for threat assessment, engagement authorization, and weapons guidance. The market encompasses the complete military radar system value chain, including transmitter and receiver hardware, antenna and phased array assemblies, transmit and receive modules, signal and data processing electronics, waveform generation and exciter subsystems, radar data extraction and tracking software, identification friend or foe interrogator and transponder systems, power supply and cooling infrastructure, platform integration and mounting structures, and the operational software, maintenance tooling, and logistic support services that constitute the full lifecycle delivery of a deployed military radar capability. Key participants include prime defense electronics contractors, specialist radar system developers, gallium nitride and gallium arsenide semiconductor component suppliers, phased array antenna and transmit-receive module manufacturers, signal processing hardware and embedded computing suppliers, defense procurement agencies of major military powers, and international standardization bodies whose electromagnetic compatibility, frequency allocation, and export control frameworks define the regulatory parameters governing military radar system development and procurement globally.

Market Insights

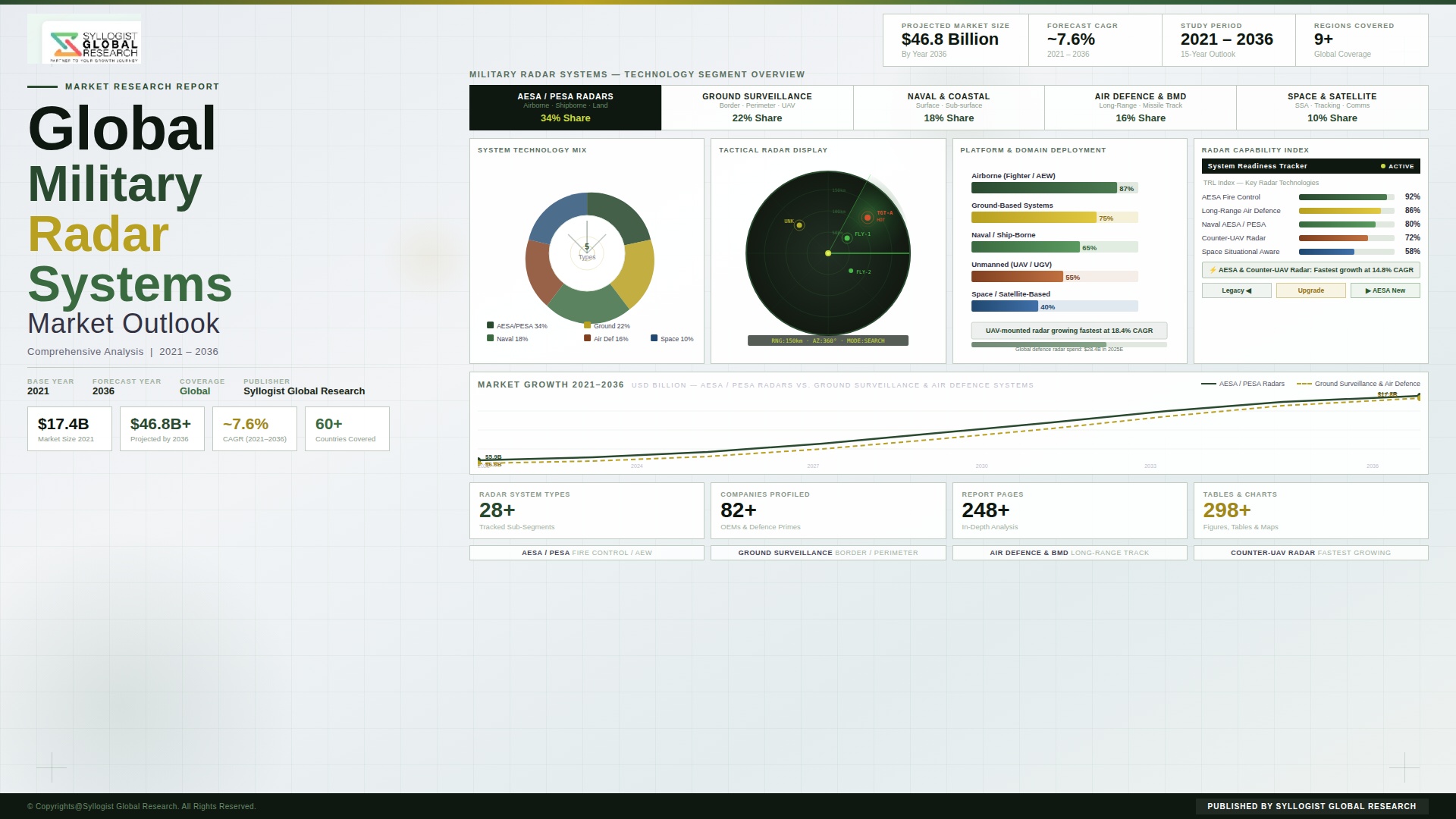

The global military radar systems market is experiencing a period of sustained structural expansion driven by the convergence of escalating near-peer threat environments that demand next-generation detection and tracking capability against advanced stealth aircraft, hypersonic glide vehicles, and supersonic anti-ship missiles, an accelerating global defense spending cycle anchored in the defense budget growth commitments of NATO member states, major Indo-Pacific defense powers, and Gulf Cooperation Council nations, and a generational technology transition from legacy mechanically scanned array radar architectures toward active electronically scanned array platforms whose superior performance, reliability, and multi-mission flexibility are compelling procurement authorities to accelerate fleet replacement programs across all platform domains. The global military radar systems market was valued at approximately USD 16.8 billion in 2025 and is projected to reach USD 31.4 billion by 2034, advancing at a compound annual growth rate of 7.2% over the forecast period from 2027 to 2034, as defense establishments across North America, Europe, Asia-Pacific, and the Middle East execute multi-year procurement programs for active electronically scanned array ground-based air defense radars, airborne early warning and control system upgrades, naval fire control and volume search radar replacements, and next-generation ballistic missile defense sensor networks. The structural demand durability of the military radar market is reinforced by the long platform lifecycle characteristics of major defense radar programs, in which initial system procurement is followed by a sustained multi-decade upgrade, modification, and spare parts support revenue stream that provides defense radar system developers and prime contractors with durable, program-anchored revenue visibility extending well beyond initial production contract award milestones.

The technology landscape of military radar systems is undergoing a decisive and accelerating transition from passive electronically scanned array and mechanically scanned array architectures toward active electronically scanned array platforms across all military radar application categories and platform domains, driven by the fundamental performance advantages of active electronically scanned array technology in terms of beam agility, waveform diversity, simultaneous multi-mission capability, resistance to electronic countermeasures, and reliability through elimination of single-point failure mechanical rotation and high-power transmitter components that have historically defined the operational availability constraints of legacy radar generations. Active electronically scanned array radars now constitute approximately 58% of total military radar procurement revenue globally in 2025, with penetration accelerating most rapidly in airborne fighter aircraft fire control radar replacement programs, ground-based long-range air surveillance and air defense radar upgrades, and naval multi-function radar procurement for surface combatant modernization, driven by the demonstrated operational performance advantages of active electronically scanned array systems in contested electronic warfare environments where beam agility and low probability of intercept waveform management directly translate into survivability and mission effectiveness advantages over legacy mechanically scanned and passive array predecessors. Gallium nitride semiconductor technology has emerged as the defining material advancement enabling the current generation of high-performance active electronically scanned array military radars, with gallium nitride transmit-receive modules offering power density, efficiency, and operating temperature advantages over legacy gallium arsenide components that enable the development of radar systems combining significantly higher average transmit power, wider instantaneous bandwidth, and greater detection range within platform size, weight, and power envelopes that are compatible with integration into tactical aircraft, surface combatants, and mobile ground-based air defense vehicles whose physical constraints precluded the integration of comparable capability in gallium arsenide-based predecessor systems.

From a regional standpoint, North America constitutes the largest and most technologically advanced regional market for military radar systems, driven by sustained United States Department of Defense investment across all service branches encompassing the Air Force Long Range Discrimination Radar and Next Generation Overhead Persistent Infrared radar integration programs, the Navy AN/SPY-6 Air and Missile Defense Radar fleet-wide installation across Arleigh Burke-class destroyers and Gerald R. Ford-class aircraft carriers, the Army Lower Tier Air and Missile Defense Sensor program, and the broad recapitalization of United States Air Force airborne early warning and fighter aircraft radar capabilities, collectively representing the most concentrated and highest-value military radar procurement pipeline globally. Asia-Pacific represents the fastest-growing regional procurement market, driven by Chinese People Liberation Army radar capability development across all operational domains encompassing next-generation phased array air defense radars, over-the-horizon backscatter and surface wave radar systems for maritime domain awareness, airborne early warning and control aircraft radar programs, and the expanding Chinese ballistic missile defense sensor network, alongside substantial procurement growth in India, Japan, South Korea, Australia, and Taiwan whose defense establishments are executing major radar system acquisition programs in response to the deteriorating regional security environment and the demonstrated radar capability advancements of potential adversaries. Europe has experienced a marked acceleration in military radar investment following the strategic recalibration of continental defense priorities, with Germany, France, Poland, the Netherlands, and the United Kingdom advancing ground-based air defense radar, naval combat system radar, and airborne surveillance radar procurement programs at budget growth rates substantially above pre-2022 baseline planning levels.

The integration of cognitive radar capability, encompassing machine learning-enabled adaptive waveform selection, artificial intelligence-driven clutter and interference suppression, and automated target recognition and classification algorithms, into the signal and data processing architectures of next-generation military radar systems represents the most transformative near-term capability advancement trajectory in the market, as defense radar programs increasingly specify cognitive processing requirements that enable radar systems to autonomously optimize their operating parameters in response to detected electronic warfare threats, dynamic clutter environments, and evolving target characteristics without requiring manual operator intervention, delivering detection and tracking performance in complex electromagnetic environments that static waveform and processing parameter radar architectures are unable to achieve. The counter-stealth radar capability development imperative is simultaneously reshaping the frequency band, waveform diversity, and multi-static network architecture requirements of ground-based air defense and airborne early warning radar procurement programs across major military powers, as the demonstrated operational deployment of fifth-generation stealth aircraft and the accelerating development of sixth-generation stealth platforms by near-peer competitors create a structural requirement for radar systems capable of generating actionable track quality data on low-observable targets through the combination of very high frequency and ultra high frequency band operation that exploits stealth shaping limitations at longer wavelengths, multi-static network geometries that defeat monostatic radar cross-section reduction techniques, and high-power advanced signal processing that extracts target signatures from clutter and interference environments specifically designed to protect stealth aircraft from radar detection, generating a technically demanding and commercially significant procurement requirement that is driving substantial research and development investment and competitive product development activity across the leading military radar system developers.

Key Drivers

Escalating Near-Peer Threat Environments and the Proliferation of Advanced Stealth, Hypersonic, and Cruise Missile Threats Compelling Next-Generation Radar Capability Investment

The accelerating development and operational deployment of fifth-generation stealth aircraft, hypersonic glide vehicles, supersonic and sea-skimming anti-ship cruise missiles, and maneuvering reentry vehicle ballistic missile payloads by near-peer competitor military forces is creating a structural obsolescence imperative for legacy military radar systems whose detection and tracking performance characteristics were defined against threat signatures and kinematic profiles substantially less challenging than those presented by current and next-generation adversary weapon systems, generating a defense procurement urgency for next-generation radar capability investments that cannot be deferred without accepting operationally unacceptable gaps in air and missile defense coverage, airborne surveillance effectiveness, and naval force protection capability. The hypersonic glide vehicle threat category is particularly consequential for military radar procurement programs, as the combination of high velocity, low altitude, and highly maneuverable trajectory profiles that characterize hypersonic glide vehicles challenges the detection and tracking performance of existing air defense radar networks whose scan rates, data refresh intervals, and track initiation algorithms were optimized for ballistic missile and subsonic cruise missile threat profiles rather than for the continuous maneuvering, altitude variation, and ground-clutter proximity that hypersonic glide vehicle engagement scenarios require radar systems to accommodate within the compressed engagement timelines available between initial detection and intercept execution. The operational experience of recent conflicts has provided defense establishments with direct empirical evidence of the vulnerability of legacy radar networks to saturation attacks, electronic jamming, and anti-radiation missile suppression, generating procurement priority for radar systems incorporating electronic protection measures, frequency agility, low probability of intercept waveform management, and hardened processing architectures that sustain operational effectiveness in the contested electromagnetic environments characterizing modern high-intensity conflict scenarios.

Sustained Global Defense Budget Expansion and Multi-Year Capital Procurement Programs Anchoring Long-Duration Demand for Advanced Radar System Procurement

Global defense expenditure reached approximately USD 2.4 trillion in 2025, driven by the most broad-based and sustained defense budget expansion cycle since the Cold War era, with NATO member states accelerating progress toward the 2% of gross domestic product defense spending target, major Indo-Pacific defense powers executing defense modernization investment programs at historically elevated budget growth rates, and Middle East defense establishments sustaining high radar procurement activity anchored in air and missile defense threat environment requirements, collectively generating a multi-year defense capital procurement pipeline whose scale and duration provide military radar system developers with investment planning visibility sufficient to support the advanced engineering development, manufacturing capacity expansion, and supply chain maturation investments required to deliver next-generation radar system capability within contracted program schedules. The structural characteristic of major military radar programs, in which platform procurement typically spans five to fifteen years of production deliveries followed by a sustainment and upgrade revenue stream extending twenty to thirty years beyond initial delivery, creates a commercially durable demand profile for radar system developers whose current production program portfolio translates into multi-decade revenue visibility that is substantially more predictable than the revenue profile associated with commercial technology product markets subject to discretionary purchase cycle volatility. The increasing integration of air and missile defense radar systems into networked multi-national defense architectures, including the NATO Integrated Air and Missile Defense System and Indo-Pacific theater air defense networks, creates procurement interdependencies among allied defense establishments that reinforce and synchronize radar modernization procurement timelines across national defense budgets, as interoperability requirements and collective defense commitments drive aligned modernization schedules across alliance members.

Active Electronically Scanned Array Technology Maturation and Gallium Nitride Semiconductor Advancement Driving Performance-Led Platform Replacement Across All Military Radar Domains

The maturation of active electronically scanned array radar technology from a high-cost capability available only in the most demanding and well-funded military radar programs toward a commercially competitive standard architecture whose unit cost reduction trajectory now makes it accessible across a broad range of military radar application categories and platform classes is driving a performance-led replacement cycle for legacy mechanically scanned and passive electronically scanned array radar systems whose operational capability deficit relative to current-generation active electronically scanned array platforms is sufficiently large to justify procurement authorities accelerating fleet replacement programs ahead of legacy system end-of-life schedules. The transition to gallium nitride transmit-receive module technology has been the single most impactful technology advancement enabling active electronically scanned array radar performance improvement and cost reduction in the current generation of military radar programs, with gallium nitride modules offering three to five times the power density of equivalent gallium arsenide components, significantly higher operating temperature tolerance that reduces cooling system complexity and weight, and wideband frequency coverage that enables a single radar aperture to cover multiple frequency bands and support diverse waveform requirements within a unified hardware architecture. The resulting active electronically scanned array radar systems offer defense procurement authorities a combination of multi-mission flexibility, enabling a single radar hardware installation to simultaneously or interleaved perform long-range air surveillance, fire control, electronic warfare support, and communications relay functions previously requiring multiple separate sensor systems, electronic protection performance in contested electromagnetic environments, and operational availability improvements through solid-state architecture elimination of high-failure-rate mechanical and high-voltage transmitter components that has made active electronically scanned array replacement of legacy radar systems compelling across fighter aircraft, naval combatants, and ground-based air defense platform categories simultaneously.

Key Challenges

Electronic Warfare Threat Escalation and the Growing Sophistication of Adversary Jamming, Spoofing, and Anti-Radiation Missile Capabilities Threatening Radar Operational Effectiveness

The operational effectiveness of deployed and next-generation military radar systems is confronted by a continuously escalating electronic warfare threat environment in which near-peer adversary electronic attack capabilities, encompassing high-power noise jamming systems, deceptive spoofing transmitters, terrain-masking low-altitude ingress tactics designed to exploit radar coverage gaps, and precision anti-radiation missiles capable of homing on radar emissions to destroy radiating sensor systems, are advancing at a pace that compresses the operational utility lifetime of radar systems and requires continuous electronic protection technology investment to maintain adequate performance margins against adversary countermeasure capabilities. The development of cognitive electronic warfare systems by near-peer competitors that employ machine learning algorithms to rapidly analyze intercepted radar emissions, identify waveform characteristics and frequency patterns, and adaptively optimize jamming waveforms in near real time to exploit detected radar processing vulnerabilities represents a qualitative escalation in the electronic attack threat that challenges the waveform agility and electronic protection measures of current-generation active electronically scanned array radar systems in ways that static electronic protection architectures cannot adequately address, requiring military radar developers to respond with cognitive radar processing capability that can match and counter cognitive electronic warfare adaptation with equivalent or faster autonomous countermeasure adaptation. The anti-radiation missile threat is compelling ground-based radar system operators to adopt low probability of intercept operating modes, networked passive sensor cueing, and emitter control protocols that limit radar transmission activity to the minimum operationally necessary intervals, creating operational constraints that reduce the radar coverage continuity and track quality achievable from individual radar systems and increase the network complexity and sensor fusion requirement of effective ground-based air surveillance architectures.

Semiconductor Supply Chain Concentration Risks, Gallium Nitride Production Capacity Constraints, and Export Control Restrictions Limiting Program Delivery Timelines

Military radar system development and production programs are exposed to a concentrated and strategically sensitive semiconductor supply chain in which gallium nitride epitaxial wafer production, high-electron-mobility transistor fabrication, and transmit-receive module assembly are performed by a limited number of specialized facilities whose production capacity is simultaneously serving the accelerating demand of multiple competing military radar programs across United States, European, and allied defense establishments, generating supply allocation competition, extended delivery lead times, and unit cost inflation pressure that are creating program schedule risk for radar procurement contracts with fixed delivery milestone commitments based on supply chain availability assumptions that are no longer valid in the current defense procurement environment. The geographic concentration of advanced semiconductor fabrication capability in a small number of nations, combined with the export control and foreign direct investment restriction frameworks that governments are implementing to protect military-grade semiconductor technology from adversary acquisition, creates a supply chain security challenge for allied and partner nation military radar programs that depend on access to United States or other restricted-jurisdiction gallium nitride component technology whose export licensing requirements add program timeline uncertainty and geopolitical dependency to radar development and production supply chains. The capital intensity and long lead time of new gallium nitride fabrication facility construction, with the development and qualification of a new military-grade gallium nitride wafer production line requiring investment in the range of USD 300 million to USD 800 million and a construction and qualification timeline exceeding five years, constrains the pace at which the defense gallium nitride supply base can expand to meet the growing demand generated by accelerating active electronically scanned array radar procurement programs, creating a structural supply constraint that is expected to persist as a program execution risk factor through the near to medium term of the forecast period.

Software Complexity, Cybersecurity Vulnerability, and the Certification Cost of Embedded Processing Architecture Upgrades in Safety-Critical Military Radar Systems

The increasing software intensity of modern military radar systems, whose operational capability is defined as much by the sophistication of embedded signal processing algorithms, tracking software, target recognition logic, and electronic protection waveform management code as by the underlying hardware transmit power and antenna aperture parameters, is generating software development, verification, validation, and certification cost and timeline challenges that are becoming a significant program execution risk factor for major military radar procurement programs whose software content has expanded by orders of magnitude relative to predecessor system generations. The integration of machine learning and artificial intelligence components into military radar signal and data processing chains introduces software certification methodology challenges analogous to those confronting AI deployment in other safety-critical defense applications, as the non-deterministic behavior of trained neural network models under novel input conditions is difficult to bound and verify using the deterministic software assurance methods that defense system certification frameworks have historically relied upon, requiring radar program offices and certification authorities to develop new validation approaches that can provide adequate assurance of AI component behavior across the operational input space without requiring exhaustive test case enumeration that is computationally impractical for high-dimensional AI model architectures. The cybersecurity vulnerability of networked military radar systems, whose operational data outputs are integrated into air and missile defense command and control networks, naval combat management systems, and airborne battle management architectures, creates a cyberattack surface through which adversary intrusion could corrupt track data, inject false targets, suppress genuine threat alerts, or disable radar processing systems, requiring radar developers and defense network operators to invest in continuous cybersecurity architecture hardening, penetration testing, and software integrity monitoring that adds sustained lifecycle cost to military radar program ownership and imposes software change management constraints that complicate the agile capability upgrade insertion that modern operational requirements demand.

Market Segmentation

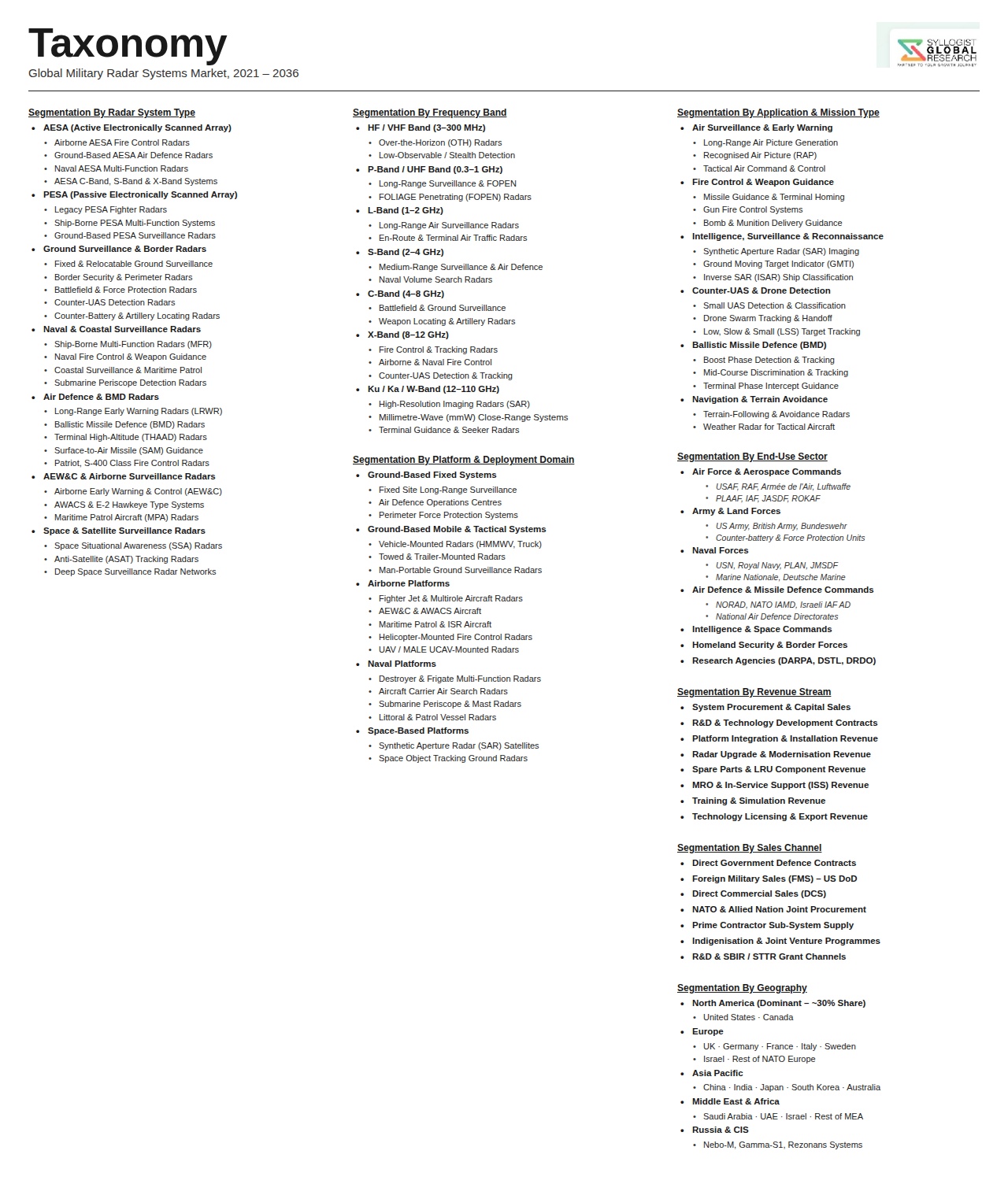

- Segmentation By Technology Type

- Active Electronically Scanned Array (AESA) Radar

- Passive Electronically Scanned Array (PESA) Radar

- Mechanically Scanned Array (MSA) Radar

- Synthetic Aperture Radar (SAR)

- Ground Penetrating Radar (GPR)

- Over-the-Horizon (OTH) Radar

- Multi-Static and Netted Radar Systems

- Others

- Segmentation By Platform

- Ground-Based Fixed Installation Radar Systems

- Ground-Based Mobile and Transportable Radar Systems

- Airborne Radar Systems (Fighter Aircraft and Attack Aircraft)

- Airborne Early Warning and Control (AEW&C) Systems

- Naval Surface Vessel Radar Systems

- Submarine and Underwater Radar Systems

- Unmanned Aerial Vehicle-Integrated Radar Systems

- Space-Based Radar Systems

- Others

- Segmentation By Frequency Band

- HF and VHF Band (Counter-Stealth and OTH)

- UHF Band

- L-Band (Long-Range Surveillance)

- S-Band (Medium-Range Air Defense)

- C-Band

- X-Band (Fire Control and Airborne)

- Ku, Ka, and Millimeter-Wave Band

- Multi-Band and Wideband Systems

- Segmentation By Application

- Air Surveillance and Early Warning

- Air and Missile Defense Fire Control

- Ballistic Missile Defense and Space Surveillance

- Naval Surface Search and Fire Control

- Airborne Intercept and Fire Control

- Ground Surveillance and Battlefield Management

- Counter-Unmanned Aerial System (C-UAS) Radar

- Weather and Terrain Avoidance Radar

- Electronic Intelligence and Signals Exploitation

- Others

- Segmentation By Component

- Transmitter and Receiver Hardware

- Antenna and Phased Array Assembly

- Transmit-Receive (T/R) Modules

- Signal and Data Processor

- Waveform Generator and Exciter

- Identification Friend or Foe (IFF) Subsystem

- Power Supply and Cooling Infrastructure

- Radar Software and Data Extraction Systems

- Others

- Segmentation By Range

- Short Range (Below 100 km)

- Medium Range (100 km to 500 km)

- Long Range (500 km to 2,000 km)

- Very Long Range and Strategic (Above 2,000 km)

- Segmentation By End User

- Army and Land Forces

- Navy and Maritime Forces

- Air Force and Aerospace Commands

- Space Force and Strategic Defense Commands

- Coast Guard and Maritime Security Agencies

- Intelligence and National Security Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Military Radar Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, active electronically scanned array, passive electronically scanned array, synthetic aperture radar, and over-the-horizon radar, and by platform, ground-based, airborne, naval, and space-based, to enable defense prime contractors, radar component suppliers, semiconductor manufacturers, defense procurement agencies, and strategic investors to identify which technology and platform segment will generate the highest absolute revenue and the most durable procurement growth trajectory across the forecast period in the context of the global air and missile defense modernization cycle?

- How is the escalating near-peer threat environment, specifically the operational deployment of fifth-generation stealth aircraft, hypersonic glide vehicles, and advanced cruise missiles by major competitor military powers, reshaping the detection performance requirements, frequency band selection, waveform diversity specifications, and multi-static network architecture approaches of ground-based air defense radar, airborne early warning, and naval fire control radar procurement programs across North America, Europe, Asia-Pacific, and the Middle East, and what is the aggregate defense investment being directed toward counter-stealth and counter-hypersonic radar capability development across the major national military radar modernization programs through 2034?

- What is the projected market size, compound annual growth rate, and competitive landscape of the active electronically scanned array radar segment across fighter aircraft fire control, naval multi-function radar, and ground-based air defense radar application categories through 2034, and which specific platform integration programs, including United States Navy AN/SPY-6 fleet-wide installation, European air defense radar recapitalization, and Indo-Pacific theater radar network expansion, are expected to generate the largest procurement volumes at what per-system unit values as gallium nitride technology maturation continues to reduce active electronically scanned array system cost and expand its addressable platform categories?

- How are gallium nitride semiconductor supply chain concentration risks, export control restriction frameworks governing military-grade component technology transfer, and fabrication capacity constraints affecting the development timeline, production ramp rate, and unit cost trajectory of active electronically scanned array transmit-receive module supply chains serving major military radar programs, and what supply chain diversification strategies, domestic fabrication investment programs, and allied industrial cooperation arrangements are major defense radar procurement nations pursuing to reduce their strategic dependency on concentrated or restricted-jurisdiction gallium nitride supply sources through 2034?

- Who are the leading prime defense electronics contractors, specialist radar system developers, gallium nitride and transmit-receive module manufacturers, signal processing hardware suppliers, and radar software and tracking algorithm developers currently defining the competitive landscape of the global military radar systems market, and what are their respective program portfolios across ground-based, airborne, naval, and space-based radar application categories, manufacturing capacity and technology investment strategies, cognitive radar and artificial intelligence processing development roadmaps, and competitive positioning in the major national radar modernization procurement programs expected to generate the largest contract awards through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Geopolitical Instability, Arms Escalation & Export Control Risk

- Electronic Warfare, Jamming, Spoofing & Counter-Radar Vulnerability Risk

- Technology Obsolescence, Software Dependency & Cybersecurity Risk

- Supply Chain Concentration, Semiconductor Availability & Critical Component Risk

- Budget Volatility, Procurement Delays & Programme Cancellation Risk

- Regulatory Framework & Standards

- National Defence Procurement Frameworks & Military Radar Acquisition Policy

- Export Control Regulations: ITAR, EAR & Wassenaar Arrangement Applicability to Radar Systems

- Electromagnetic Compatibility (EMC), Spectrum Allocation & Radio Frequency Interference Standards

- NATO Interoperability Standards, STANAG Requirements & Allied Procurement Frameworks

- Cybersecurity, Data Security & Software Assurance Standards for Mission-Critical Radar Systems

- Global Military Radar Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Procured & Systems Deployed)

- Market Size & Forecast by System Type

- Ground-Based Air Surveillance & Early Warning Radar

- Airborne Early Warning & Control (AEW&C) Radar

- Fire Control & Weapon Guidance Radar

- Battlefield Surveillance, Ground Moving Target Indicator (GMTI) & Counterfire Radar

- Naval Surface Search, Fire Control & Missile Guidance Radar

- Synthetic Aperture Radar (SAR) & Inverse SAR (ISAR) Imaging Radar

- Air Defence & Ballistic Missile Defence (BMD) Tracking Radar

- Weather & Navigation Radar for Military Platforms

- Market Size & Forecast by Technology

- Active Electronically Scanned Array (AESA) Radar Technology

- Passive Electronically Scanned Array (PESA) Radar Technology

- Gallium Nitride (GaN) & Gallium Arsenide (GaAs) Solid-State Transmit-Receive Module Technology

- Low Probability of Intercept & Low Probability of Detection (LPI/LPD) Radar Technology

- Cognitive Radar, AI-Enabled Signal Processing & Adaptive Waveform Technology

- Multi-Function & Multimode Radar Technology

- Passive & Bistatic Radar Technology

- Quantum Radar & Photonic Radar Emerging Technology

- Market Size & Forecast by Frequency Band

- HF & VHF Band (3 MHz to 300 MHz): Over-the-Horizon & Long-Range Surveillance

- UHF Band (300 MHz to 1 GHz): Ballistic Missile Defence & Space Surveillance

- L-Band (1 GHz to 2 GHz): Long-Range Air Surveillance & ATC

- S-Band (2 GHz to 4 GHz): Medium-Range Surveillance & Weapon Control

- C-Band (4 GHz to 8 GHz): Battlefield & Naval Fire Control

- X-Band (8 GHz to 12 GHz): Fire Control, SAR & Airborne Radar

- Ku, K & Ka-Band (12 GHz to 40 GHz): High-Resolution Imaging & Missile Seeker

- Millimetre Wave (MMW) Band (Above 40 GHz): Short-Range Precision & Terminal Guidance

- Market Size & Forecast by Platform

- Ground-Based Fixed & Mobile Land Platforms

- Airborne Platforms: Fixed-Wing Aircraft, Rotary-Wing & UAV

- Naval Platforms: Surface Combatants, Submarines & Unmanned Surface Vessels

- Space-Based Platforms: Satellite-Mounted Radar & Space Surveillance

- Man-Portable & Lightweight Deployable Systems

- Market Size & Forecast by Application

- Air Surveillance, Threat Detection & Early Warning

- Fire Control, Weapon Guidance & Target Tracking

- Ballistic Missile Defence (BMD) & Anti-Ballistic Missile (ABM) Tracking

- Intelligence, Surveillance & Reconnaissance (ISR) & SAR Imaging

- Battlefield Situational Awareness, Counterfire & Artillery Locating

- Naval Surface & Subsurface Surveillance

- Electronic Intelligence (ELINT), Signals Intelligence (SIGINT) & Electronic Warfare Support

- Navigation, Obstacle Avoidance & Terrain Following for Military Platforms

- Market Size & Forecast by End-User

- Army & Land Forces

- Air Force & Air Defence Commands

- Navy & Maritime Forces

- Space Forces & Strategic Surveillance Commands

- National Security, Border Surveillance & Homeland Defence Agencies

- Market Size & Forecast by Sales Channel

- Direct Government-to-Government (G2G) & Foreign Military Sales (FMS)

- Prime Defence Contractor & OEM Direct Supply

- System Integration, Technology Licensing & Co-Development Partnership

- Maintenance, Upgrade, Spares & Through-Life Support Contract

- North America Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Military Radar Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Procured & Systems Deployed)

- By System Type

- By Technology

- By Frequency Band

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Israel, Russia, China, Japan, India, South Korea, Australia, Turkey, Saudi Arabia, UAE, Brazil, Poland, Sweden, Italy, Norway

- Technology Landscape & Innovation Analysis

- Active Electronically Scanned Array (AESA) & GaN-Based Transmit-Receive Module Technology Deep-Dive

- Cognitive Radar, AI Signal Processing & Adaptive Waveform Generation Technology

- Low Probability of Intercept (LPI) & Low Probability of Detection (LPD) Radar Technology

- Synthetic Aperture Radar (SAR), ISAR & Ground Moving Target Indicator (GMTI) Technology

- Ballistic Missile Defence & Space Surveillance Radar Technology

- Passive, Bistatic & Multistatic Radar Network Technology

- Quantum Radar, Photonic Radar & Next-Generation Emerging Sensing Technology

- Patent & IP Landscape in Military Radar Systems Technologies

- Value Chain & Supply Chain Analysis

- RF & Microwave Component, GaN/GaAs Wafer & Transmit-Receive Module Supply Chain

- Antenna, Phased Array Structure & Aperture Manufacturing Supply Chain

- Signal Processing Hardware, FPGA, ASIC & Embedded Computing Supply Chain

- Power Electronics, Transmitter & High-Voltage Power Supply Chain

- Software, Algorithm Development & Radar Data Processing Supply Chain

- Prime Defence Contractor, System Integrator & OEM Landscape

- MRO, Obsolescence Management, Upgrades & Through-Life Support Channel

- Pricing Analysis

- Ground-Based Air Surveillance & Early Warning Radar System Unit & Programme Cost Analysis

- Airborne Radar System: AESA Fighter & AEW&C Platform Procurement Cost Analysis

- Naval Radar System Unit Pricing & Integration Cost Analysis

- Ballistic Missile Defence Tracking Radar Capital & Operations Cost Analysis

- GaN Transmit-Receive Module & Phased Array Sub-System Cost Structure Analysis

- Total Programme Economics: Development, Qualification, Production & Lifecycle Support Cost Modelling

- Sustainability & Environmental Analysis

- Lifecycle Environmental Impact Assessment of Military Radar Systems: Energy, Materials & Emissions

- GaN Solid-State Technology: Power Efficiency Gains & Reduction in Thermal Management Footprint

- Electromagnetic Radiation, RF Exposure & Environmental Safety Compliance for Ground-Based Radar

- Conflict Zone Environmental Impact, Spectrum Pollution & Post-Conflict Decommissioning Considerations

- Defence Industry ESG Commitments, Sustainability Reporting & Responsible Sourcing Policy Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Technology & Geography

- Player Classification

- Prime Defence Contractors with Integrated Radar Divisions

- Specialist Ground-Based Air Surveillance & Early Warning Radar Developers

- Airborne Radar & AESA System Manufacturers

- Naval Radar & Combat Management System Providers

- Ballistic Missile Defence & Space Surveillance Radar Specialists

- GaN & RF Component, Transmit-Receive Module Manufacturers

- Signal Processing, Software & AI-Enabled Radar Solution Providers

- Defence Technology Start-ups & Dual-Use Sensing Companies

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Military Radar Products & System Portfolio

- Key Customer Relationships & Reference Programme Deliveries

- Manufacturing Footprint & Production Capacity

- Revenue (Military Radar Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Programme Milestones, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Responsible Innovation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output