Market Definition

The Global Hydrogen-Powered Regional Aircraft Infrastructure Market encompasses the planning, engineering, procurement, construction, certification, and operation of the complete ground-based and airside infrastructure ecosystem required to enable the commercial deployment of hydrogen-powered regional aircraft, including liquid hydrogen and compressed gaseous hydrogen production facilities, cryogenic liquefaction and compression plants, high-capacity hydrogen storage tanks and on-airport buffer storage systems, hydrogen fueling and dispensing infrastructure incorporating cryogenic transfer systems and high-flow dispensing arms, hydrogen distribution pipelines and mobile transport solutions connecting production sources to airport fueling points, ground support equipment adapted for hydrogen aircraft operations, and the safety, monitoring, and leak detection systems mandated by aviation authority certification frameworks governing hydrogen aircraft ground operations. The market additionally encompasses hydrogen-compatible aircraft maintenance, repair, and overhaul infrastructure, pilot and ground crew training facilities adapted for hydrogen aircraft operations, and the digital integration platforms, hydrogen quality monitoring systems, and real-time fuel management systems that constitute the operational backbone of hydrogen-ready regional airports. Key participants in this market include airport authorities and infrastructure developers responsible for airside hydrogen facility planning and construction, hydrogen production technology providers and industrial gas companies supplying aviation-grade liquid and gaseous hydrogen, aerospace OEMs developing hydrogen-powered regional aircraft platforms whose infrastructure requirements define ground system specifications, engineering procurement and construction firms delivering turnkey hydrogen fueling infrastructure, aviation regulatory bodies including the European Union Aviation Safety Agency, the Federal Aviation Administration, and national civil aviation authorities whose certification standards govern hydrogen aircraft ground operations, and public and private capital providers financing the substantial infrastructure investment required to enable commercial hydrogen aviation operations across regional route networks globally.

Market Insights

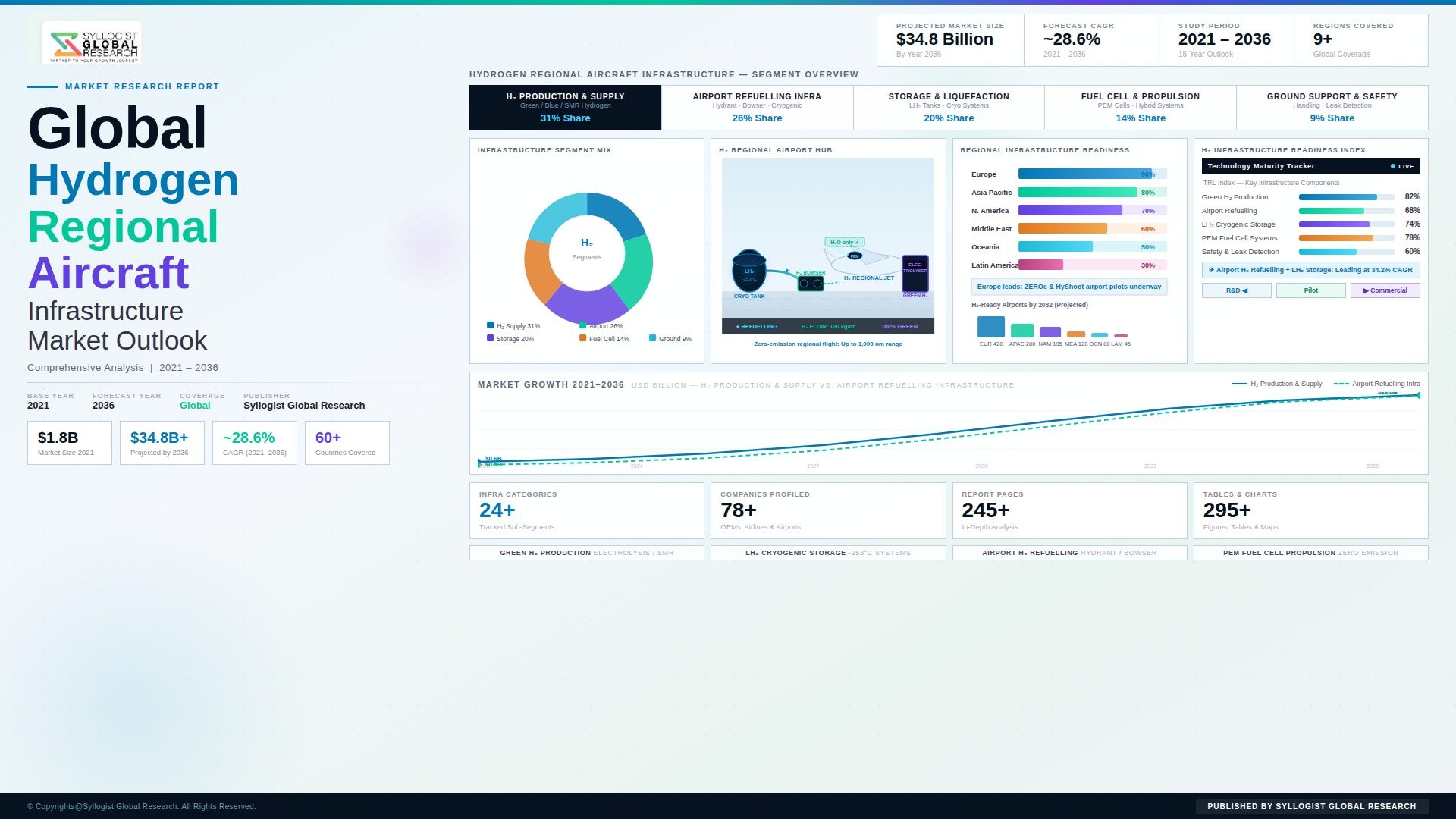

The global hydrogen-powered regional aircraft infrastructure market is emerging at the intersection of decarbonization imperatives in commercial aviation and the accelerating commercial readiness of hydrogen propulsion technology for regional aircraft platforms with seat capacities of 19 to 100 passengers and stage lengths of up to 1,000 kilometers, a segment defined by flight frequencies, turnaround times, and fuel volumes that are particularly well-suited to the operational characteristics of cryogenic liquid hydrogen and compressed gaseous hydrogen fueling systems. The market was valued at approximately USD 1.8 billion in 2025 and is projected to reach USD 14.6 billion by 2034, advancing at a compound annual growth rate of 26.3% over the forecast period from 2027 to 2034, driven by progressive commercial aircraft deliveries, expanding airport hydrogen infrastructure mandates across Europe and North America, and the scaling of green hydrogen production capacity that is progressively narrowing the cost differential between hydrogen and conventional jet fuel on a per-energy-unit basis across the most hydrogen-favorable regional aviation markets globally.

The infrastructure technology landscape is bifurcated between liquid hydrogen systems, which offer superior volumetric energy density and are favored for higher-capacity regional aircraft platforms requiring larger fuel loads per turnaround, and compressed gaseous hydrogen systems operating at 350 bar and 700 bar pressure, which are technically simpler and already established in ground transportation applications but require approximately three times the storage volume of liquid hydrogen for equivalent energy content, creating an airport footprint constraint that limits compressed gaseous hydrogen infrastructure to smaller turboprop and hybrid-electric aircraft applications with shorter stage lengths and lower per-turnaround fuel volumes. Liquid hydrogen airport fueling systems must achieve transfer rates of at least 100 kilograms per minute to maintain the turnaround time economics required by regional airline schedule integrity, demanding cryogenic transfer hardware of substantially greater technical sophistication than existing aviation fuel hydrant and bowser systems, and requiring airport operators to invest in operator training, equipment certification, and safety management systems with no direct precedent in conventional jet fuel airport operations.

From a regional perspective, Europe leads global hydrogen-powered regional aviation infrastructure development, supported by the European Union ReFuelEU Aviation regulation, with Norway, Germany, France, and the United Kingdom operating the most advanced hydrogen airport demonstration programs and concentrating the largest pipeline of committed infrastructure investment supported by national hydrogen strategies and EU Innovation Fund grants. North America is accelerating, with the United States Federal Aviation Administration advancing hydrogen aircraft certification frameworks and multiple airports in the Pacific Northwest, California, and Northeast corridor initiating hydrogen infrastructure feasibility studies supported by federal Bipartisan Infrastructure Law and Inflation Reduction Act funding programs. Asia-Pacific is an emerging market led by Japan and South Korea, where national hydrogen strategies explicitly target aviation as a priority sector for hydrogen demand creation and where existing industrial hydrogen production and liquefaction infrastructure provides a supply chain foundation that accelerates the economics of airport hydrogen infrastructure deployment relative to markets requiring greenfield hydrogen supply chain development.

The competitive landscape for hydrogen airport infrastructure encompasses a convergent set of participants from the industrial gas, aerospace ground support, and clean energy infrastructure sectors, with industrial gas companies possessing established liquefaction and cryogenic distribution competencies pursuing strategic partnerships with airport operators and aircraft OEMs to develop proprietary hydrogen fueling system designs that create long-term exclusive supply relationships, while specialist aviation ground equipment manufacturers are adapting hydrogen fueling technologies from automotive and maritime applications to meet the safety certification and operational reliability standards required in commercial airport environments. The emergence of dedicated hydrogen aviation infrastructure developers as a distinct competitive category, combining project development, equipment procurement, infrastructure financing, and long-term operations and maintenance services into integrated infrastructure concession offerings, is progressively providing airport operators with a viable alternative to direct capital ownership of hydrogen fueling assets, enabling faster infrastructure deployment timelines by transferring technology risk and capital investment responsibility to infrastructure specialists with cross-sector hydrogen deployment experience.

Key Drivers

Mandatory Decarbonization Targets in Commercial Aviation Compelling Investment in Hydrogen Propulsion Infrastructure Across Regional Airport Networks

The commercial aviation sector faces binding decarbonization commitments that create a structural and time-bound investment mandate for hydrogen infrastructure across regional aviation networks, as regulatory frameworks including the European Union ReFuelEU Aviation regulation, the International Civil Aviation Organization Carbon Offsetting and Reduction Scheme for International Aviation, and national sustainable aviation transition plans adopted by the United Kingdom, Norway, France, Japan, and Australia establish progressive hydrogen and sustainable aviation fuel blending mandates and zero-emission aircraft introduction timelines that create regulatory-backed demand visibility for airport infrastructure investment planning and financing. Regional aviation is particularly targeted within hydrogen transition policy frameworks because shorter stage lengths and lighter maximum takeoff weights make hydrogen propulsion technically and economically viable sooner than for long-haul wide-body aircraft, and because regional airports serve as logistically practical hydrogen infrastructure deployment nodes where production facilities and cryogenic storage systems can be sized to match near-term aircraft demand while preserving expansion headroom for full commercial deployment. The alignment of regulatory mandates with committed aircraft development programs from multiple regional aircraft manufacturers with targeted entry-into-service dates between 2028 and 2035 is generating an unprecedented level of committed infrastructure planning activity, translating regulatory intent into contracted infrastructure projects across European regional airports and progressively into North American and Asia-Pacific airport systems, providing the investment pipeline visibility required to mobilize private capital into hydrogen airport infrastructure at the project scale required for commercial operations.

Declining Green Hydrogen Production Costs Improving the Commercial Viability of Hydrogen Aviation Infrastructure Investment

The progressive reduction in green hydrogen production costs, driven by falling renewable electricity prices, advancing alkaline and proton exchange membrane electrolysis stack efficiencies, and scaling manufacturing volumes for electrolysis equipment, is steadily improving the project economics of airport-based and near-airport hydrogen production infrastructure and narrowing the fuel cost competitiveness gap between green hydrogen and sustainable aviation fuel alternatives for regional aviation applications. Green hydrogen production costs declined from approximately USD 8.50 per kilogram in 2020 to approximately USD 4.20 per kilogram in 2025 and are projected to reach USD 2.10 to USD 2.60 per kilogram by 2030 in regions with abundant renewable electricity resources, approaching the commercial viability threshold for regional aviation applications when the higher energy efficiency of hydrogen fuel cell propulsion relative to combustion-based sustainable aviation fuel systems is factored into total cost of ownership calculations at the fleet level. The geographic concentration of cost-competitive renewable electricity resources in Norway, Iceland, the Iberian Peninsula, southwestern United States, and Australia aligns meaningfully with existing regional aviation route network density in these regions, supporting the development of on-site and near-airport green hydrogen production facilities that eliminate long-distance hydrogen transport logistics and reduce the delivered cost of aviation-grade hydrogen to levels approaching commercial competitiveness with conventional jet fuel at projected 2030 production cost benchmarks for the most favorably located regional airport hydrogen infrastructure projects.

Airport Operator and Airline Sustainability Commitments Accelerating Hydrogen Infrastructure Capital Expenditure Planning and Procurement

Airport operators and regional airlines are translating corporate sustainability commitments and investor environmental, social, and governance requirements into committed capital expenditure plans for hydrogen infrastructure, with European airport groups including Avinor in Norway, Groupe ADP in France, Manchester Airports Group in the United Kingdom, and Frankfurt Airport operator Fraport establishing hydrogen infrastructure master plans and entering development agreements with hydrogen technology providers and regional aircraft OEMs that commit airport capital and land allocation to hydrogen fueling facility construction in advance of initial aircraft deliveries. The business case for airport-led hydrogen infrastructure investment is reinforced by the competitive differentiation value of hydrogen-readiness certification for regional airports competing to attract hydrogen aircraft launch operators seeking confirmed infrastructure partners for initial commercial service entry, with airports that achieve hydrogen fueling infrastructure commissioning prior to aircraft entry-into-service positioned to secure long-term anchor airline agreements that provide the contracted fuel volume throughput revenue required to underwrite infrastructure capital recovery. Airline sustainability commitments have produced binding hydrogen aircraft procurement agreements from regional operators including Scandinavian Airlines regional subsidiaries, Air New Zealand, and multiple European regional carriers whose publicized hydrogen fleet transition timelines create infrastructure demand certainty that airport operators can underwrite within hydrogen fueling facility project finance structures, progressively replacing speculative infrastructure planning with contracted demand-backed investment programs supported by credible airline fleet transition schedules.

Key Challenges

Absence of Standardized Hydrogen Aircraft Fueling Interface and Ground Operations Certification Frameworks Creating Infrastructure Investment Uncertainty

The global hydrogen-powered regional aircraft infrastructure market confronts a foundational challenge in the absence of internationally harmonized standards for hydrogen aircraft fueling interfaces, cryogenic coupling specifications, ground operations safety protocols, and airport hydrogen facility certification requirements, creating a fragmented regulatory and technical environment in which infrastructure investments made prior to standards finalization risk costly redesign or obsolescence when regulatory harmonization ultimately occurs. The European Union Aviation Safety Agency, the Federal Aviation Administration, and the International Civil Aviation Organization are at different stages of developing hydrogen aircraft type certification and ground operations standards, with the divergence in their respective technical approaches to hydrogen aircraft fueling safety requirements creating a scenario in which airports serving transatlantic or international regional routes may ultimately need to install parallel or dual-specification fueling infrastructure to satisfy the certification requirements of aircraft certified under different regulatory jurisdictions. The lack of standardized fueling interface specifications also prevents the development of a competitive multi-supplier ecosystem for hydrogen fueling equipment components, limiting procurement options for airport infrastructure developers and constraining the cost reduction trajectory of hydrogen fueling system capital costs that would otherwise benefit from multi-supplier competition and manufacturing scale economies as infrastructure deployment volumes grow progressively through the forecast period.

Cryogenic Liquid Hydrogen Infrastructure Capital Cost and Airport Space Requirements Constraining Financial Viability at Smaller Regional Airports

The capital intensity of cryogenic liquid hydrogen infrastructure, including liquefaction plants, vacuum-insulated storage tanks, cryogenic transfer pipelines, and specialized fueling vehicles capable of handling liquid hydrogen at temperatures of minus 253 degrees Celsius, represents a substantial barrier to economically viable hydrogen infrastructure deployment at the smaller regional airports that constitute the majority of the addressable network for hydrogen-powered regional aircraft, where annual passenger throughput and aircraft movement volumes generate hydrogen fuel demand projections that are insufficient to support the minimum economic scale required for on-site liquefaction infrastructure. A minimum viable liquid hydrogen airport fueling facility capable of supporting 10 to 15 daily regional aircraft turnarounds requires an estimated capital investment of USD 35 million to USD 65 million depending on hydrogen supply configuration, storage capacity, and fueling system automation level, an investment quantum that exceeds the annual capital expenditure budgets of many smaller regional airport operators and that requires external grant funding, public-private partnership structures, or long-term anchor airline offtake agreements to achieve financeable project economics. This deployment speed constraint may limit initial commercial hydrogen aviation operations to a subset of better-resourced regional airports with the financial capacity and strategic motivation to lead infrastructure investment ahead of confirmed aircraft availability, creating a geographic concentration of early hydrogen aviation operations that reinforces infrastructure investment decisions at leading airports while deferring broader network coverage to later deployment phases.

Green Hydrogen Supply Chain Immaturity and the Risk of Aviation-Grade Liquid Hydrogen Supply Shortfalls During Initial Commercial Deployment Phases

The hydrogen supply chain required to deliver aviation-grade liquid hydrogen to regional airports at the purity levels, delivery temperatures, and throughput volumes demanded by commercial aircraft fueling operations does not yet exist at the geographic scale or logistical reliability required to support simultaneous hydrogen aircraft launch operations across multiple airports within a regional airline network, creating a supply security risk that is structurally distinct from the mature and geographically distributed jet fuel supply chains that hydrogen airport infrastructure must ultimately replace. Aviation-grade liquid hydrogen requires a minimum purity of 99.999% to protect fuel cell stack components and combustion engine components from contaminant-induced degradation, a specification that demands purpose-built liquefaction and purification infrastructure rather than adaptation of existing industrial liquid hydrogen supply chains that produce hydrogen to lower purity standards for metallurgical, chemical, and electronics manufacturing applications. The development of dedicated aviation-grade green hydrogen supply chains requires coordinated investment across electrolysis capacity, renewable electricity generation, liquefaction infrastructure, and cryogenic transport logistics that must be planned and financed simultaneously to achieve the supply reliability required for commercial airline operations, a coordination challenge compounded by the geographic dispersion of regional airports, the capital intensity of each supply chain component, and the absence of established long-term green hydrogen offtake pricing frameworks that would provide the revenue visibility required to underwrite supply chain investment at the scale and reliability standard demanded by commercial aviation operators globally.

Market Segmentation

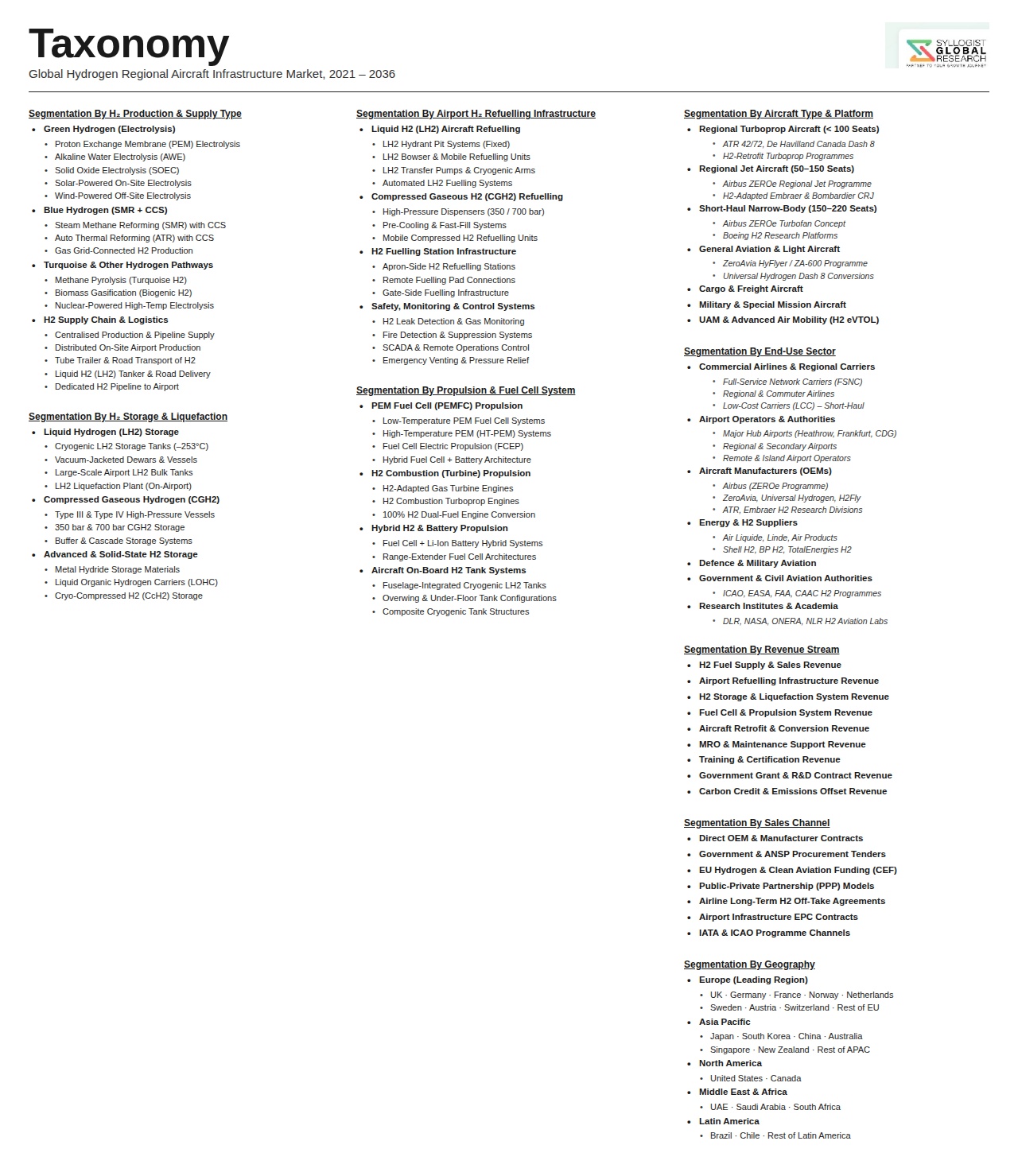

- Segmentation By Hydrogen State and Storage Technology

- Liquid Hydrogen (LH2) Infrastructure

- Compressed Gaseous Hydrogen (CGH2) at 350 Bar

- Compressed Gaseous Hydrogen (CGH2) at 700 Bar

- Slush Hydrogen and Advanced Cryogenic Storage Technologies

- Others

- Segmentation By Infrastructure Component

- On-Site Green Hydrogen Production Facilities (Electrolysis-Based)

- Hydrogen Liquefaction Plants and Cryogenic Processing Units

- Cryogenic Storage Tanks and On-Airport Buffer Storage Systems

- Hydrogen Fueling and Dispensing Systems

- Cryogenic Transfer Pipelines and Airside Distribution Networks

- Mobile Hydrogen Fueling Vehicles and Hydrant Carts

- Hydrogen Quality Monitoring and Purity Assurance Systems

- Leak Detection and Safety Management Systems

- Ground Power and Thermal Conditioning Support Equipment

- Digital Fuel Management and Airport Integration Platforms

- Others

- Segmentation By Airport Category

- Large International Airports With Dedicated Regional Operations

- Primary Regional Airports (Above 5 Million Annual Passengers)

- Secondary Regional Airports (1 Million to 5 Million Annual Passengers)

- Small Regional and Community Airports (Below 1 Million Annual Passengers)

- Others

- Segmentation By Aircraft Type Served

- Hydrogen Turboprop Regional Aircraft (19 to 50 Seats)

- Hydrogen Turbofan Regional Jet Aircraft (50 to 100 Seats)

- Hydrogen-Electric Hybrid Regional Aircraft

- Hydrogen Fuel Cell Regional Aircraft

- Others

- Segmentation By Hydrogen Supply Model

- On-Site Green Hydrogen Production (Electrolysis-Based)

- Pipeline-Delivered Hydrogen from Central Production Facilities

- Truck-Delivered Liquid Hydrogen

- Truck-Delivered Compressed Gaseous Hydrogen

- Integrated Renewable Energy and Hydrogen Co-Production Systems

- Others

- Segmentation By Application

- Commercial Scheduled Passenger Regional Aviation

- Air Cargo and Freight Regional Operations

- Charter and Business Aviation

- Military and Defense Regional Aviation

- Emergency Services and Medical Evacuation Aviation

- Others

- Segmentation By Ownership and Operation Model

- Airport Authority-Owned and Operated Infrastructure

- Airline-Owned Dedicated Hydrogen Fueling Facilities

- Third-Party Infrastructure Developer and Operator

- Joint Venture and Public-Private Partnership Models

- Others

- Segmentation By End User

- Regional Airlines and Scheduled Carriers

- Air Cargo and Freight Operators

- Airport Operators and Ground Handling Companies

- Military and Government Aviation Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Hydrogen-Powered Regional Aircraft Infrastructure Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by infrastructure component, hydrogen state and storage technology, and airport category, to enable airport operators, hydrogen technology providers, infrastructure developers, aerospace OEMs, and institutional investors to identify which infrastructure sub-segments will generate the highest absolute capital deployment requirements and the most durable long-term revenue growth trajectory in the context of progressive regional hydrogen aircraft entry-into-service timelines between 2028 and 2035?

- How are the divergent technical specifications and regulatory certification approaches of liquid hydrogen and compressed gaseous hydrogen airport fueling systems expected to shape airport infrastructure investment decisions across different regional aviation market geographies, and which hydrogen storage and fueling technology configurations are projected to capture the dominant share of infrastructure capital expenditure by 2034 when evaluated against aircraft OEM hydrogen propulsion technology selection patterns, airport footprint and capital budget constraints, and the relative maturity of cryogenic and high-pressure gaseous hydrogen supply chain ecosystems in leading deployment markets?

- What is the projected airport-by-airport and country-by-country deployment trajectory of hydrogen fueling infrastructure across European, North American, and Asia-Pacific regional aviation networks through 2034, including the specific airports committed to first-phase hydrogen infrastructure commissioning, the hydrogen supply models selected by leading airport operators, the capital investment structures and funding mechanisms being employed to finance hydrogen infrastructure development, and the commercial agreements between airport operators and regional airline launch customers that are providing the contracted fuel throughput revenue required to underwrite infrastructure investment at individual airport sites?

- How is the green hydrogen production cost reduction trajectory expected to affect the competitive economics of on-site airport electrolysis facilities relative to pipeline-delivered and truck-delivered liquid hydrogen supply models across different regional airport scale categories and geographic locations through 2034, and at what green hydrogen production cost threshold does airport-integrated electrolysis infrastructure achieve financial viability without grant funding support for primary regional airports serving more than 5 million annual passengers in high-renewable-electricity-resource regions including Scandinavia, the Iberian Peninsula, and the Pacific Northwest of North America?

- Who are the leading hydrogen infrastructure technology providers, industrial gas companies, airport ground equipment manufacturers, engineering procurement and construction firms, and infrastructure project developers currently defining the competitive landscape of the global hydrogen-powered regional aircraft infrastructure market, and what are their respective technology portfolios across liquid hydrogen and compressed gaseous hydrogen fueling systems, project development pipelines and committed airport partnerships, manufacturing capacity and certification status for aviation-grade hydrogen fueling equipment, financial structuring capabilities for infrastructure concession and public-private partnership transactions, and strategic positioning relative to the hydrogen aircraft OEM partnerships that are expected to drive infrastructure specification and procurement decisions across the initial commercial deployment phase through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Hydrogen Production, Purity, Storage & Cryogenic Handling Safety Risk

- Aircraft Airworthiness Certification, Regulatory Approval & Type Certification Risk

- Airport Infrastructure Readiness, Capital Investment & Retrofit Feasibility Risk

- Green Hydrogen Supply Chain Immaturity, Cost Volatility & Availability Risk

- Public Acceptance, Passenger Safety Perception & Hydrogen Technology Trust Risk

- Regulatory Framework & Standards

- ICAO Hydrogen Aviation Roadmap, Carbon Offsetting & Reduction Scheme (CORSIA) & Net Zero 2050 Policy Framework

- EASA & FAA Hydrogen Aircraft Airworthiness, Type Certification & Special Condition Standards

- Hydrogen Fuelling Infrastructure Safety Standards: ISO, IEC, NFPA & Airport Hydrogen Handling Codes

- National Hydrogen Strategies, Aviation Decarbonisation Mandates & Green Hydrogen Incentive Frameworks

- Environmental Permitting, NOx & Water Vapour Emission Standards for Hydrogen Combustion & Fuel Cell Aircraft

- Global Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Infrastructure Units Installed & Aircraft Supported)

- Market Size & Forecast by Infrastructure Type

- Airport Hydrogen Fuelling Stations & Dispensing Infrastructure

- Liquid Hydrogen (LH2) Storage Tanks, Cryogenic Vessels & Vaporisation Systems

- Compressed Gaseous Hydrogen (CGH2) Storage, Compression & Dispensing Systems

- Hydrogen Production Facilities: On-Site Electrolysis & Steam Methane Reforming with CCS

- Hydrogen Transport, Pipeline & Truck Delivery Logistics Infrastructure

- Aircraft Ground Support Equipment (GSE) Adapted for Hydrogen Fuelling Operations

- Fuel Cell Power Units, Auxiliary Power & Ground Power Infrastructure

- Digital Monitoring, Leak Detection, Safety & Control Systems for Hydrogen Airside Operations

- Market Size & Forecast by Technology

- Proton Exchange Membrane Fuel Cell (PEMFC) Propulsion Technology

- Solid Oxide Fuel Cell (SOFC) Auxiliary Power & Range Extender Technology

- Liquid Hydrogen (LH2) Cryogenic Storage & Thermal Insulation Technology

- Compressed Gaseous Hydrogen (CGH2) High-Pressure Tank & Type IV Composite Cylinder Technology

- Hydrogen Combustion Turbine & Turboprop Retrofit Technology

- Green Hydrogen Electrolysis: PEM Electrolyser & Alkaline Electrolyser Technology

- Hydrogen Boil-Off Management, Vapour Recovery & Zero-Loss Transfer Technology

- Digital Twin, AI-Enabled Predictive Maintenance & Hydrogen System Health Monitoring Technology

- Market Size & Forecast by Hydrogen Production Pathway

- Green Hydrogen (Renewable Electricity-Powered Electrolysis)

- Blue Hydrogen (Natural Gas Reforming with Carbon Capture & Storage)

- Turquoise Hydrogen (Methane Pyrolysis with Solid Carbon By-Product)

- Pink Hydrogen (Nuclear-Powered Electrolysis)

- Market Size & Forecast by Aircraft Range Category

- Very Short-Haul & Commuter Routes (Below 200 km): Hydrogen Fuel Cell Aircraft

- Short-Haul Regional Routes (200 km to 600 km): Hybrid Hydrogen-Electric & Turboprop

- Medium-Range Regional Routes (600 km to 1,500 km): Hydrogen Combustion Turbofan

- Market Size & Forecast by Application

- Regional Passenger Aviation: Scheduled & Charter Services

- Air Cargo, Express Freight & Logistics on Regional Routes

- Emergency Medical Services, Search & Rescue & Government Aviation

- Flight Training, Pilot Certification & Hydrogen Aviation Academy Operations

- Airport Apron, Ground Handling & Airside Equipment Hydrogen Conversion

- Market Size & Forecast by Airport Category

- Major International Hubs: Pioneer Hydrogen Infrastructure & Technology Demonstration

- Secondary & Regional Airports: Hub-and-Spoke Hydrogen Network Nodes

- Remote, Island & Off-Grid Aerodromes: Green Hydrogen Self-Sufficiency Infrastructure

- Market Size & Forecast by End-User

- Airport Operators & Ground Handling Organisations

- Regional Airlines & Wet-Lease Aircraft Operators

- Hydrogen Infrastructure Developers & Energy Companies

- Aircraft OEMs, MRO Providers & Engine Manufacturers

- Government Aviation Authorities & National Hydrogen Programme Bodies

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Infrastructure Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), Grant Co-Funding & Government Subsidy Programme

- Direct Equipment Supply & System Integration

- Operations & Maintenance (O&M) Service & Long-Term Service Agreement

- North America Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Hydrogen-Powered Regional Aircraft Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Infrastructure Units Installed & Aircraft Supported)

- By Infrastructure Type

- By Technology

- By Hydrogen Production Pathway

- By Aircraft Range Category

- By Application

- By Airport Category

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Proton Exchange Membrane Fuel Cell (PEMFC) Propulsion & Power System Technology Deep-Dive

- Liquid Hydrogen (LH2) Cryogenic Storage, Insulation & Boil-Off Management Technology

- Hydrogen Combustion Turbine & Turboprop Engine Adaptation Technology

- Green Hydrogen Electrolysis: PEM & Alkaline Electrolyser Scaling for Aviation Applications

- Compressed Gaseous Hydrogen (CGH2) High-Pressure Composite Cylinder & Dispensing Technology

- Digital Twin, AI Predictive Maintenance & Hydrogen Airside Safety Monitoring Technology

- Hybrid Hydrogen-Electric Propulsion & Energy Management System Technology

- Patent & IP Landscape in Hydrogen Aviation Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Green & Blue Hydrogen Production Equipment & Electrolyser Manufacturing Supply Chain

- Cryogenic Storage Vessel, Insulation Material & LH2 Equipment Supply Chain

- Fuel Cell Stack, Membrane Electrode Assembly & Balance-of-Plant Component Supply Chain

- High-Pressure Composite Cylinder, Valve & Regulator Supply Chain

- Hydrogen Dispensing, Metering & Airport Fuelling Equipment Supply Chain

- EPC Contractor, System Integrator & Infrastructure Developer Landscape

- O&M Service Provider, Safety Inspection & Through-Life Support Channel

- Pricing Analysis

- Airport Hydrogen Fuelling Station & LH2 Storage Infrastructure Capital Cost Analysis

- Green Hydrogen Production Cost: Levelised Cost of Hydrogen (LCOH) at Aviation Scale

- Fuel Cell Propulsion System & Cryogenic Tank Aircraft Integration Cost Analysis

- CGH2 vs. LH2 Infrastructure: Capital, Operating & Total Cost of Ownership Comparison

- Hydrogen vs. Sustainable Aviation Fuel (SAF) vs. Battery-Electric: Levelised Cost per Seat-km Analysis

- Total Infrastructure Programme Economics: Development, Construction, Commissioning & Lifecycle Cost Modelling

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Hydrogen Aviation Infrastructure: Well-to-Wake Carbon Footprint by Production Pathway

- Green Hydrogen Aviation vs. Jet-A Kerosene & SAF: CO2, NOx & Contrail Impact Comparison

- Water Vapour Emissions, High-Altitude Contrail Formation & Climate Impact of Hydrogen Combustion

- Circular Economy Considerations: Fuel Cell Stack Recycling, Platinum Group Metal Recovery & Component End-of-Life

- CORSIA Compliance, EU Emissions Trading Scheme (ETS) Aviation Scope & Green Hydrogen Eligibility for Carbon Credits

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Energy Companies & Green Hydrogen Producers Entering Aviation Infrastructure

- Specialist Hydrogen Fuelling Infrastructure & Cryogenic Equipment Developers

- Fuel Cell System Manufacturers & Propulsion Technology Providers

- Aircraft OEMs & Airframe Developers with Hydrogen Platform Programmes

- Airport Operators & Ground Services Companies Piloting Hydrogen Infrastructure

- EPC Contractors & Project Developers Specialising in Hydrogen Aviation Infrastructure

- Digital Monitoring, Safety Systems & AI Platform Providers for Hydrogen Airside Operations

- Start-ups, Spin-Offs & Government-Backed Research Consortia in Hydrogen Aviation

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Hydrogen Aviation Infrastructure Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Hydrogen Aviation Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Pilot Projects, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output