Market Definition

The India Urban Air Cargo Market encompasses the planning, development, operation, and commercialization of aerial freight delivery systems that transport packages, parcels, medical supplies, industrial components, perishables, and high-value goods within and between urban, peri-urban, and urban-rural corridors across Indian cities using unmanned aerial vehicles, electric vertical takeoff and landing aircraft, advanced air mobility platforms, and conventional helicopter-based cargo services. Urban air cargo represents the application of airspace as a logistics corridor to bypass the congested surface transportation network that characterizes India’s rapidly expanding metropolitan areas, tier-1, and tier-2 cities, delivering time-sensitive shipments at significantly compressed transit times relative to ground-based last-mile and intracity delivery routes operating under chronic traffic congestion, inadequate road infrastructure, and growing urban mobility demand that makes conventional surface logistics increasingly cost-inefficient and commercially uncompetitive for premium-urgency cargo categories.

The market encompasses drone delivery systems deployed by e-commerce operators, quick commerce platforms, pharmaceutical distributors, and diagnostic laboratory networks for last-mile parcel and medical specimen transport; eVTOL cargo platforms designed for mid-range intercity and intracity freight corridors connecting logistics hubs, warehouses, airports, and urban delivery stations across distances of 50 to 300 kilometers; unmanned aerial system operations for industrial inspection and small parcel delivery in manufacturing zones, special economic zones, and port logistics clusters; vertiport and skyport infrastructure enabling cargo loading, unloading, battery charging, and fleet maintenance for urban air cargo operations; and the air traffic management, urban airspace management, digital command and control, and communication technology systems that govern safe and scalable urban air cargo operations within India’s complex airspace environment. Key participants include drone delivery technology developers and operators, eVTOL aircraft manufacturers pursuing cargo certification, logistics and e-commerce companies piloting urban air cargo programs, airport and infrastructure development authorities, the Directorate General of Civil Aviation as the primary regulatory oversight body, and central and state government agencies whose aviation policy, airspace management frameworks, and smart city infrastructure investment decisions define the commercial and regulatory environment within which India’s urban air cargo market is developing.

Market Insights

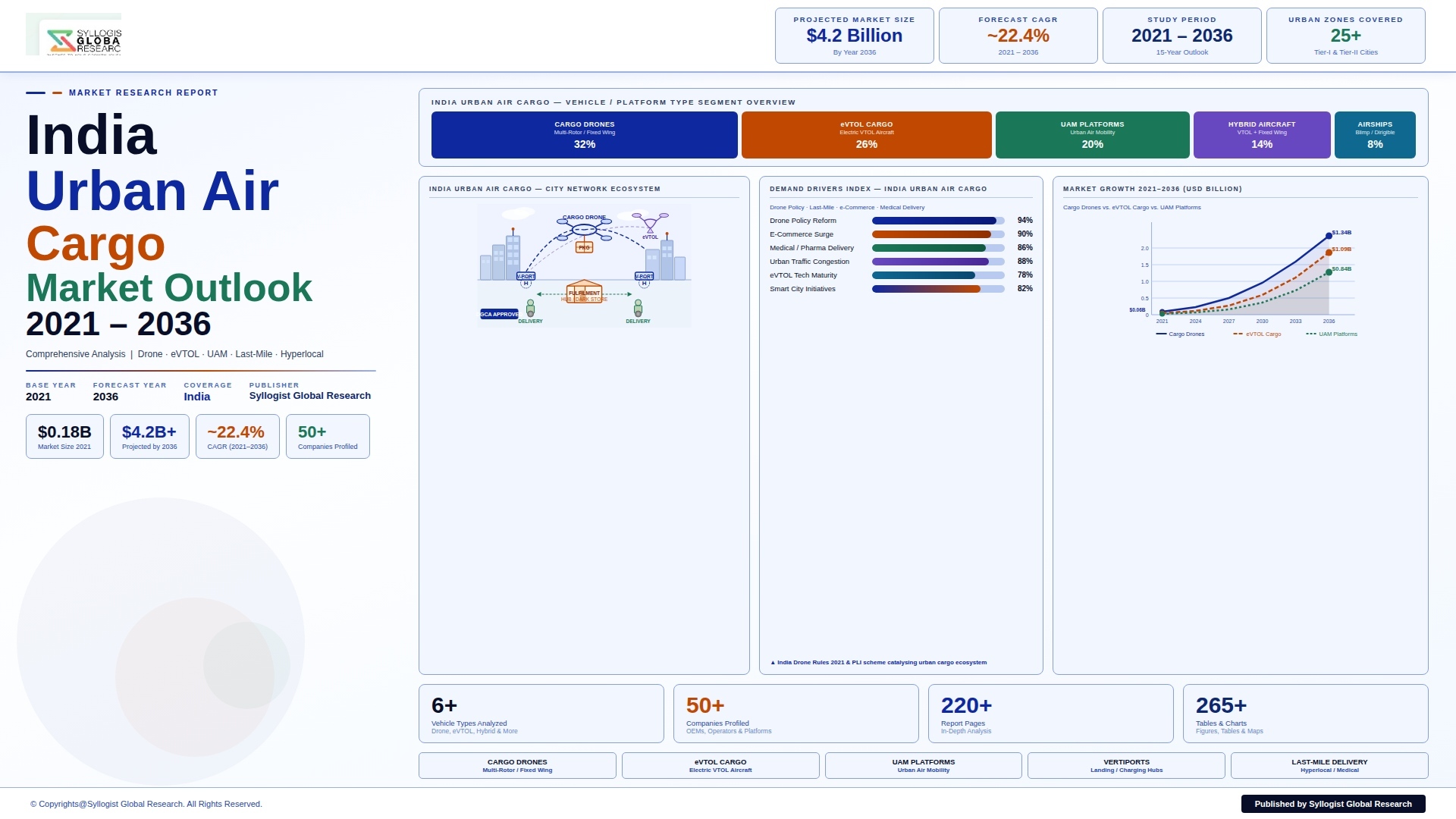

The India urban air cargo market is emerging as one of the most commercially consequential new logistics infrastructure segments within the country’s rapidly evolving supply chain landscape, driven by the structural convergence of India’s acute urban traffic congestion crisis, the explosive growth of e-commerce and quick commerce delivery demand requiring sub-hour fulfillment capabilities that surface networks cannot reliably deliver, the strategic urgency of extending reliable medical supply chains to underserved rural and peri-urban communities, and the progressive maturation of drone and eVTOL technology platforms to commercial operational readiness under India’s evolving regulatory framework for unmanned aircraft systems. The India urban air cargo market was valued at approximately USD 290 million in 2025 and is projected to reach USD 2.8 billion by 2034, advancing at a compound annual growth rate of 28.7% over the forecast period from 2027 to 2034, representing one of the fastest structural growth trajectories in India’s logistics sector as regulatory enablement under the Drone Rules 2021 and the UAS Traffic Management framework unlocks commercial deployment at scale, and as pioneering operator programs in medical drone delivery, e-commerce last-mile, and industrial logistics demonstrate commercially viable unit economics that attract capital investment and technology deployment at accelerating rates across Indian urban and peri-urban geographies.

The medical and healthcare cargo segment constitutes the most commercially advanced and operationally proven application within the India urban air cargo market, having achieved documented commercial deployment at scale through programs including the Telangana government’s Medicine from the Sky initiative operated in partnership with Medicines from the Sky consortium including HealthCube and Throttle Aerospace, the Manipur state government’s drone medical supply program for hill district primary health centers, and the Indian Council of Medical Research-supported drone delivery pilots for blood components, vaccines, and diagnostic specimens that have collectively demonstrated the viability and public health impact of drone-based medical logistics in Indian geographic and regulatory conditions. The healthcare drone delivery segment addresses a structurally compelling market need given that India’s public health infrastructure is characterized by a pronounced geographic inequality in medical supply chain reliability, with primary health centers and community health centers in remote, hilly, and flood-prone districts regularly experiencing stock-outs of essential medicines, blood products, and vaccines due to road connectivity limitations, seasonal accessibility barriers, and cold chain breakdown risks in conventional surface distribution that drone delivery directly and demonstrably resolves. Apollo Hospitals, Narayana Health, and diagnostic laboratory chains including Dr Lal PathLabs and Metropolis Healthcare have initiated drone delivery pilots for inter-facility medical specimen transport, pharmacy prescription fulfillment, and emergency blood unit delivery in urban and peri-urban environments where the time-critical nature of medical cargo justifies the premium delivery cost of aerial transport over surface alternatives, and the demonstrated clinical outcome improvements from faster specimen turnaround and emergency blood delivery are building the medical community acceptance that is essential for scaling healthcare urban air cargo programs commercially.

The e-commerce and quick commerce cargo segment represents the highest-volume addressable market opportunity within India’s urban air cargo landscape, driven by the structural demand of India’s rapidly expanding quick commerce sector, led by Blinkit, Zepto, Swiggy Instamart, and BigBasket’s BB Now, whose 10-minute grocery and essential goods delivery promise is operationally challenged by the surface traffic congestion of Indian metropolitan areas and whose unit economics would be substantially improved by drone delivery from dark store warehouse locations to residential and commercial delivery points within a 2 to 5 kilometer operational radius. India’s quick commerce market reached approximately USD 6.1 billion in gross merchandise value in 2025 and is growing at approximately 40% annually, with total quick commerce order volumes exceeding 10 million orders per day across India’s top 15 cities, representing a massive and commercially validated addressable market for drone last-mile delivery whose operational feasibility within regulatory frameworks permitting Beyond Visual Line of Sight operations in designated urban delivery corridors would enable platform providers to dramatically increase their delivery density per dark store location while reducing per-delivery ground fleet cost. Dunzo Digital, prior to its operational difficulties, had pioneered drone delivery trials in Bengaluru, while Amazon India has received Directorate General of Civil Aviation experimental approvals for drone delivery trials at its Bengaluru fulfillment operations, and Flipkart’s drone delivery program under its Yaari Delivery initiative has demonstrated sub-30-minute delivery performance from fulfillment center to customer doorstep in controlled trial conditions that validate the operational feasibility of e-commerce drone last-mile delivery at commercially relevant parcel weights of 500 grams to 3 kilograms.

From a technology and infrastructure development perspective, India’s urban air cargo market is being shaped by a distinctive combination of domestically developed drone platforms that have emerged in response to the government’s Atmanirbhar Bharat initiative and the Production Linked Incentive scheme for drones, international eVTOL manufacturers seeking India market entry, and a progressive regulatory framework evolution that is creating structured commercial deployment pathways for urban air cargo operators. The PLI scheme for drones, which committed INR 120 crore in incentives for drone manufacturing capacity development in India, has catalyzed the emergence of domestic drone manufacturers including Garuda Aerospace, ideaForge, TechEagle, Skye Air Mobility, and Throttle Aerospace whose platforms are designed for Indian operational conditions including high ambient temperatures, monsoon weather, and the specific payload and range requirements of Indian medical, agricultural, and logistics drone delivery applications. The Directorate General of Civil Aviation’s progressive expansion of BVLOS trial approvals from purely experimental programs toward conditional commercial operations permissions in designated green zones, the establishment of the Digital Sky platform as India’s unified UAS traffic management and flight permission management infrastructure, and the National Drone Policy’s vision of India as a global drone hub by 2030 are together creating a regulatory development trajectory that is progressively reducing the policy uncertainty constraining commercial urban air cargo investment while maintaining the safety and airspace security oversight standards appropriate for operations over densely populated urban environments. The development of vertiport and drone delivery station infrastructure within new smart city projects, logistics parks, and airport vicinity development zones by the National Industrial Corridor Development Corporation and state industrial development agencies is beginning to address the physical infrastructure gap that represents one of the binding constraints on commercial urban air cargo scaling beyond the experimental program stage.

Key Drivers

India’s Drone Rules 2021 and Progressive BVLOS Regulatory Liberalization Creating Commercial Deployment Framework for Urban Air Cargo Operators

The promulgation of the Drone Rules 2021 by the Ministry of Civil Aviation, replacing the restrictive UAS Rules 2021 with a substantially more enabling regulatory framework that reduced the certification and operational approval burden on drone operators, eliminated several prior operational restrictions, and established a risk-based permit architecture allowing commercial operations in green, yellow, and red airspace zones, represented a transformative regulatory development that directly unlocked commercial investment in urban air cargo technology development and operational program initiation across India. The Digital Sky platform, established as the single-window digital interface for UAS registration, remote pilot licensing, and flight permission management, has processed over 300,000 UAS registrations and issued millions of real-time flight permissions since its launch, demonstrating the administrative infrastructure capability to manage the volume of airspace access requests that commercial urban air cargo operations at scale will generate, and providing the regulatory confidence that encourages capital investment in drone delivery fleet development and logistics network design. The Ministry of Civil Aviation’s progressive issuance of conditional BVLOS operational approvals to qualified operators including TechEagle, Skye Air Mobility, and Throttle Aerospace for specific route-based medical and logistics delivery corridors is establishing operational precedents and safety performance data that are accelerating the transition from experimental approvals toward generalized commercial BVLOS permissions that are the prerequisite for economically viable urban air cargo operations at delivery density scales beyond what VLOS-constrained operations can achieve. The Indian government’s 2030 drone hub ambition, backed by PLI scheme manufacturing incentives and the National Counter Rogue Drone Guidelines framework addressing security concerns, is creating a coherent policy ecosystem that is attracting sustained commercial and investor attention to the urban air cargo opportunity.

Explosive Growth of Quick Commerce and E-Commerce Same-Day Delivery Demand Creating Structural Commercial Pull for Drone Last-Mile Solutions

India’s quick commerce sector, whose operational model of delivering grocery, pharmacy, and essential goods within 10 to 30 minutes from hyper-local dark store locations to customer delivery points is fundamentally dependent on minimizing last-mile delivery time and cost, is creating an urgent and commercially validated structural demand for drone delivery technology whose ability to bypass surface traffic congestion and deliver directly to residential and commercial rooftop or designated landing points would transform the unit economics, geographic coverage radius, and delivery consistency of quick commerce platform operations in India’s 15 to 20 largest metropolitan markets. The operational constraint facing quick commerce platforms is quantifiable: ground delivery agents operating motorcycles in peak-hour Mumbai, Delhi, Bengaluru, and Hyderabad traffic conditions achieve average delivery speeds of 8 to 12 kilometers per hour, limiting the effective dark store service radius to approximately 2 kilometers for 10-minute delivery commitments, while drone delivery at 60 to 80 kilometers per hour cruise speed with direct flight paths would extend the viable service radius to 5 to 8 kilometers from the same dark store location, dramatically improving the capital efficiency of dark store network deployment and the addressable consumer population per dark store unit. India’s e-commerce market, projected to reach USD 350 billion in gross merchandise value by 2030 from approximately USD 140 billion in 2025, is generating growing consumer expectation for same-day and next-day delivery fulfillment whose reliable execution in India’s congested urban centers is increasingly dependent on aerial delivery infrastructure supplementing and partially replacing the surface vehicle fleet networks that are reaching operational capacity limits in high-density urban delivery corridors.

Critical Healthcare Supply Chain Gaps and Government Medical Drone Delivery Program Expansion Generating Institutionally Backed Urban Air Cargo Demand

The Indian government’s recognition of drone delivery as a strategic healthcare infrastructure tool, demonstrated through state government-initiated medical drone delivery programs in Telangana, Manipur, Nagaland, and Meghalaya and the central government’s support for ICMR-backed medical drone delivery research, is creating an institutionally anchored and publicly funded demand stream for urban and rural air cargo services that provides the revenue visibility and operational scale required to establish the fleet infrastructure, maintenance networks, and regulatory track record that enable commercial program expansion beyond government-contracted healthcare logistics into commercial e-commerce and industrial cargo segments. The National Health Mission’s objective of ensuring reliable last-mile medical supply delivery to India’s 157,000 sub-centers and 25,000 primary health centers, a substantial proportion of which are located in geographically challenging terrain or connectivity-constrained districts, provides a massive addressable market for medical drone delivery whose combination of government procurement backing, public health impact visibility, and operational route regularity creates ideal conditions for drone cargo operators to develop commercially sustainable fleet utilization, maintenance infrastructure, and route network density. The COVID-19 pandemic’s demonstration of the strategic vulnerability of India’s medical supply chain to surface logistics disruption created lasting institutional awareness of the value of aerial medical cargo resilience infrastructure, and the Emergency Response Support System under the Ministry of Health and Family Welfare has incorporated drone-based medical resupply as a formally recognized component of India’s emergency healthcare logistics preparedness framework, creating a recurring procurement mechanism for urban air cargo operators with certified medical cargo handling capabilities.

Key Challenges

Airspace Management Complexity and Safety Certification Requirements in Dense Urban Environments Limiting Commercial BVLOS Deployment at Scale

The commercial scaling of urban air cargo operations in India’s densely populated metropolitan areas requires the resolution of complex airspace integration challenges arising from the need to coordinate unmanned cargo drone flight paths with existing civil aviation traffic around major international and domestic airports, military airspace restrictions covering large portions of Indian urban airspace, helicopter emergency medical services routes, and the physical infrastructure hazards including high-rise buildings, telecommunications towers, overhead power lines, and construction cranes that characterize India’s rapidly developing urban skylines, creating a three-dimensional operational environment whose safe management requires sophisticated detect-and-avoid technology, real-time weather monitoring, and urban air traffic management capabilities that exceed the current state of India’s Digital Sky platform infrastructure. The Directorate General of Civil Aviation’s safety certification requirements for BVLOS commercial cargo drone operations, which mandate demonstrated operational safety performance across thousands of trial flight hours before generalized commercial permission grant, represent a regulatory timeline constraint that limits the pace of commercial urban air cargo scaling irrespective of technology readiness or operator investment willingness, as the evidence base accumulation required for regulatory confidence in urban cargo drone safety at scale is inherently time-consuming in the context of India’s high-density urban flight environments where failure consequences for overflown populations are substantially more severe than in the rural or controlled-area drone operation contexts where most of India’s BVLOS safety evidence to date has been generated. The absence of a harmonized urban air traffic management framework capable of coordinating simultaneous multi-operator drone flights across shared urban airspace corridors, managing drone identification and tracking, enforcing no-fly zone compliance, and providing emergency response protocols, represents an infrastructure and regulatory coordination gap whose resolution requires coordinated investment by the DGCA, the Airports Authority of India, the Ministry of Defence, and state government urban development agencies whose priority alignment and coordination timeline are uncertain.

Limited Drone Payload Capacity and Battery Range Constraints Restricting Commercial Cargo Application Scope and Unit Economics

The current generation of commercially deployed cargo drone platforms in India operates within payload constraints of 500 grams to 5 kilograms and effective operational ranges of 10 to 30 kilometers per flight cycle before requiring battery recharging or swap, limiting the commercial cargo categories addressable by drone delivery to lightweight, high-value, or time-critical shipments whose delivery economics justify the premium cost of aerial transport relative to surface alternatives, and excluding the large majority of e-commerce parcel volumes, retail replenishment shipments, and industrial cargo consignments whose weight, dimensional, or per-unit value characteristics fall outside the operationally viable envelope of currently available cargo drone technology. The battery energy density limitations of current lithium-ion propulsion systems, which require approximately 30 to 45 minutes of recharging per flight cycle for medium-range cargo drones, constrain the daily utilization economics of cargo drone fleets to a smaller number of delivery cycles per drone per day than would be required to achieve the per-drone revenue productivity needed for commercial program financial viability without substantial fleet scale, creating a capital efficiency challenge for urban air cargo operators that is only partially addressable through battery swap station networks requiring their own infrastructure investment and spatial planning within dense urban environments. The transition to solid-state battery technology, hydrogen fuel cell propulsion, and hybrid electric systems currently under development by Indian and international aerospace technology companies promises to substantially expand the payload capacity, range, and operational endurance of next-generation cargo drone and eVTOL platforms, but the commercial availability of these propulsion technology upgrades within the Indian market at competitive price points is unlikely to materialize at scale before 2028 to 2030, constraining the commercial scope of the urban air cargo market in the near-term phase of its development.

Public Acceptance, Privacy Concerns, and Urban Community Opposition Creating Social License Barriers to Dense Urban Drone Cargo Operations

The commercial scaling of drone delivery operations in India’s dense residential urban neighborhoods requires the establishment of social license from urban communities whose acceptance of regular low-altitude drone overflights, associated acoustic footprint, visual intrusion, and perceived privacy risks from drone-mounted cameras is not guaranteed and whose organized opposition through resident welfare associations, municipal corporation representations, and public interest litigation has the potential to create localized deployment restrictions that fragment the continuous urban delivery network coverage that commercially viable drone cargo operations require. Indian residential communities in high-rise apartment complexes, which constitute the primary delivery destination for urban e-commerce and quick commerce drone delivery programs, present a particularly complex social license challenge given the concentration of residents at varying vertical floor levels, the shared rooftop infrastructure that would serve as delivery landing zones but whose access and safety management requires resident community consent and building management cooperation, and the acoustic sensitivity of apartment community environments to the persistent drone motor noise that accompanies high-frequency delivery operations in proximity to residential balconies and windows. The privacy concern dimension of urban cargo drone operations, arising from the camera payloads mounted on delivery drones for navigation, obstacle avoidance, and delivery confirmation documentation, is generating regulatory attention from the Ministry of Electronics and Information Technology and activist advocacy from digital rights organizations that are creating pressure for drone operation privacy safeguards including mandatory camera deactivation over residential areas, data retention limits for aerial imagery captured during delivery operations, and community notification requirements for new drone delivery route establishment that collectively add operational complexity and potential cost to urban air cargo program deployment in privacy-sensitive residential delivery environments.

Market Segmentation

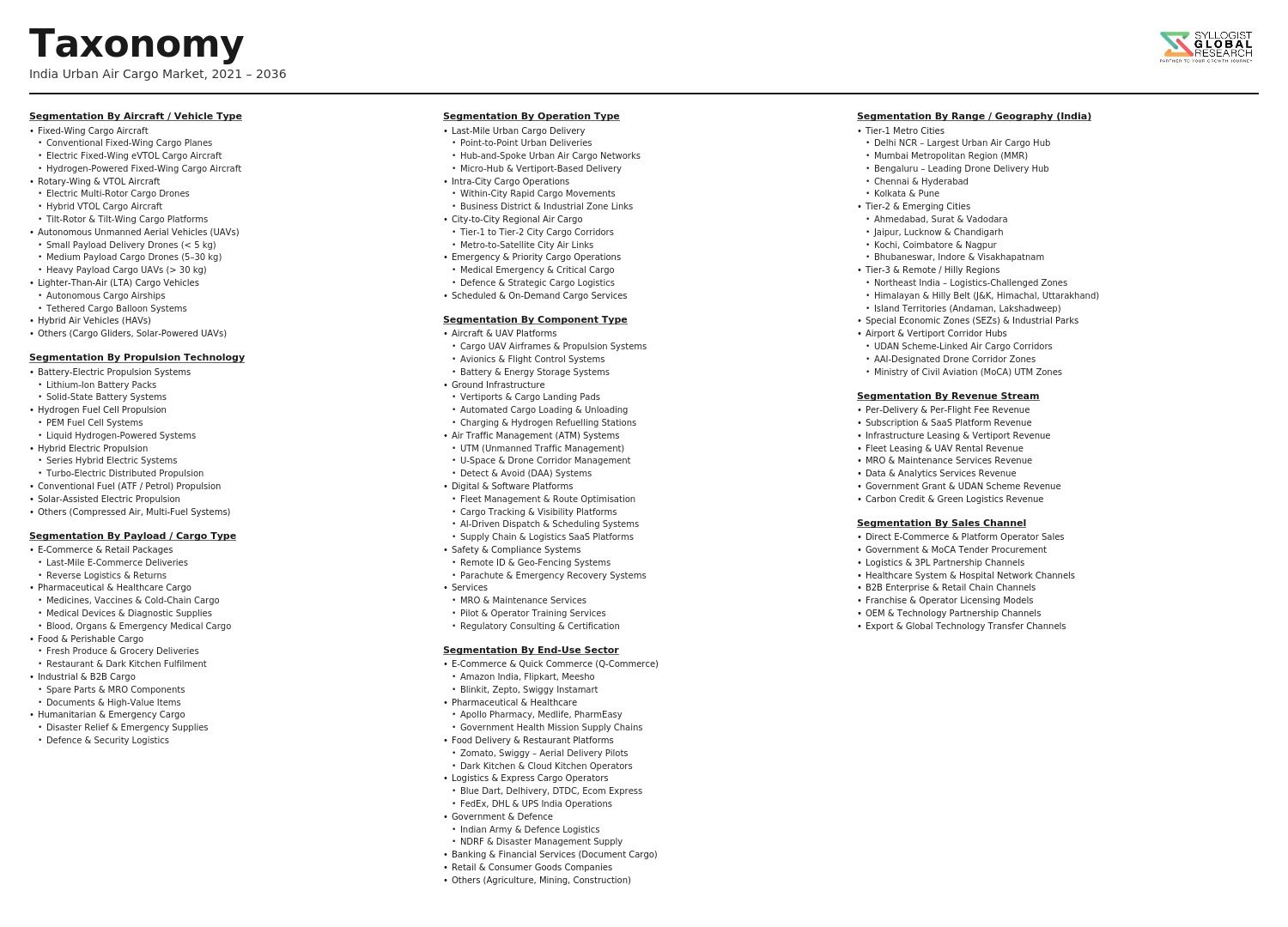

Segmentation By Platform Type

- Fixed-Wing Unmanned Aerial Vehicles (UAVs)

- Multi-Rotor and Hybrid Drones

- Electric Vertical Takeoff and Landing (eVTOL) Cargo Aircraft

- Helicopter-Based Cargo Services

- Autonomous Aerial Cargo Pods and Tethered Systems

- Others

Segmentation By Cargo Type

- Medical and Pharmaceutical Supplies (Medicines, Blood Products, Vaccines)

- Diagnostic Specimens and Laboratory Samples

- E-Commerce Parcels and Retail Goods

- Quick Commerce and Grocery Delivery

- Industrial Components and MRO Supplies

- Perishable Food and Agri Products

- Documents and High-Value Items

- Humanitarian and Emergency Relief Cargo

- Others

Segmentation By Operational Range

- Short Range (Up to 10 km)

- Medium Range (10 km to 50 km)

- Long Range (50 km to 150 km)

- Extended Range (Above 150 km)

- Others

Segmentation By Operation Type

- Visual Line of Sight (VLOS) Operations

- Beyond Visual Line of Sight (BVLOS) Operations

- Autonomous and AI-Guided Operations

- Remotely Piloted Operations

- Others

Segmentation By End-Use Application

- Healthcare and Medical Logistics

- E-Commerce Last-Mile Delivery

- Quick Commerce and On-Demand Delivery

- Industrial and Manufacturing Logistics

- Smart City and Government Services Delivery

- Agri-Input and Rural Supply Chain

- Disaster Relief and Emergency Response

- Others

Segmentation By Infrastructure

- Vertiports and Drone Delivery Stations

- Urban Air Traffic Management (UTM) Systems

- Ground Control Stations and Command Centers

- Battery Charging and Swapping Infrastructure

- Maintenance, Repair, and Overhaul (MRO) Facilities

- Others

Segmentation By End User

- E-Commerce and Quick Commerce Operators

- Hospitals, Diagnostic Labs, and Pharmaceutical Distributors

- Government Agencies and State Health Departments

- Logistics and Express Courier Companies

- Manufacturing and Industrial Enterprises

- Agricultural Input Suppliers and Agri-Businesses

- Others

Segmentation By City Tier

- Tier-1 Cities (Mumbai, Delhi, Bengaluru, Chennai, Hyderabad, Kolkata)

- Tier-2 Cities (Pune, Ahmedabad, Jaipur, Lucknow, Surat)

- Tier-3 and Emerging Cities

- Peri-Urban and Urban-Rural Corridors

- Remote and Hill District Connectivity Corridors

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Urban Air Cargo Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by platform type, cargo type, operational range, end-use application, and city tier, to enable drone technology developers, logistics companies, healthcare institutions, e-commerce operators, infrastructure investors, and government planners to identify which segments and geographies will generate the highest absolute revenue and the most commercially viable deployment opportunities across the forecast period?

- How is the Directorate General of Civil Aviation’s progressive evolution of the BVLOS regulatory approval framework, the Digital Sky UAS traffic management platform, and the National Drone Policy translating into commercial deployment timelines for urban cargo drone operators across green zone, yellow zone, and red zone airspace categories in Indian metropolitan and peri-urban geographies, and what specific regulatory milestones including generalized BVLOS permission issuance, urban air traffic management framework finalization, and drone corridor designation are required to unlock commercial scaling of urban air cargo operations at the density levels needed for viable platform economics?

- What are the current and projected unit economics of drone delivery operations across the medical cargo, e-commerce parcel, and quick commerce delivery segments in India, including per-delivery cost at different fleet utilization and payload utilization rates, breakeven delivery volume per drone per day, total cost of ownership for cargo drone fleets across battery replacement and maintenance cycles, and the cost per delivery reduction trajectory expected as technology matures, fleet scale increases, and operational learning curves are realized through the forecast period?

- How are India’s state government medical drone delivery programs in Telangana, Manipur, Nagaland, and Meghalaya demonstrating replicable healthcare logistics impact models that can inform national scale-up of medical urban air cargo networks, what public health outcome metrics including stock-out reduction rates, emergency blood delivery time improvements, and vaccine cold chain integrity are documented from operational programs, and what investment levels and public-private partnership structures are required to expand medical drone delivery coverage to India’s targeted 157,000 primary health sub-centers through the forecast period?

- Who are the leading domestic Indian drone manufacturers including Garuda Aerospace, ideaForge, TechEagle, Skye Air Mobility, and Throttle Aerospace, international eVTOL and cargo drone technology companies seeking India market entry, logistics companies pioneering urban air cargo programs, and infrastructure and vertiport developers currently defining the competitive and investment landscape of the India urban air cargo market, and what are their respective technology platforms and payload-range capabilities, DGCA certification status, commercial program deployments and route networks, fundraising and investment backing, government contract credentials, and strategic positioning in response to the transformative commercial opportunity presented by India’s converging regulatory enablement, healthcare demand, and quick commerce growth through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Regulatory Approval Delay, DGCA Certification Bottleneck & UAV Airspace Integration Risk for Urban Air Cargo in India

- Urban Airspace Congestion, Air Traffic Management Infrastructure Gap & Mid-Air Collision Risk

- Battery Technology Limitation, Payload Constraint & Range Restriction Risk for Electric Cargo UAV & AAM Operations

- High Capital Investment, Infrastructure Readiness Gap & Vertiport / Skyport Development Risk in Indian Cities

- Public Acceptance, Noise Pollution Concern, Privacy & Cargo Security Risk in Densely Populated Indian Urban Areas

- Regulatory Framework & Standards

- DGCA UAS Rules 2021, Drone Certification Scheme & Beyond Visual Line of Sight (BVLOS) Approval Framework for Cargo Drones in India

- Ministry of Civil Aviation National Drone Policy, PLI Scheme for Drones & Drone Shakti Initiative for Urban Air Cargo

- AAI Urban Air Mobility (UAM) Airspace Policy, UTM (Unmanned Traffic Management) Framework & Vertiport Infrastructure Standards

- CDSCO, FSSAI & Pharmaceutical Cold Chain Regulations Applicable to Medical & Perishable Urban Air Cargo Delivery

- Environment, Noise & Safety Regulations: CPCB Noise Norms, DGCA Air Safety Orders & Smart City Mission Integration for Urban Air Cargo

- India Urban Air Cargo Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes Carried & Number of Flights / Sorties)

- Market Size & Forecast by Aircraft & Vehicle Type

- Multi-Rotor Cargo Drones & UAVs (Electric, Below 25 kg Payload)

- Fixed-Wing Cargo Drones & UAVs (Hybrid VTOL, 25 kg to 150 kg Payload)

- Heavy-Lift Cargo Drones (Above 150 kg Payload)

- Electric Vertical Take-Off & Landing (eVTOL) Cargo Aircraft

- Autonomous Air Cargo Vehicles (Unmanned Fixed-Wing & Turboprop)

- Conventional Helicopter & Light Aircraft Adapted for Urban Cargo

- Market Size & Forecast by Operation Type

- Last-Mile Urban Delivery (Intra-City Cargo)

- Middle-Mile & Intra-Urban Logistics Hub Transfer

- Inter-City Short-Haul Urban Air Cargo (City-to-City within 200 km)

- Emergency & Time-Critical Mission Cargo Operations

- Beyond Visual Line of Sight (BVLOS) Autonomous Cargo Corridor Operations

- Market Size & Forecast by Cargo Type

- Medical & Healthcare Cargo (Blood, Vaccines, Medicines, Diagnostic Samples & Surgical Supplies)

- E-Commerce & Retail Package Delivery

- Perishable & Food Delivery (Grocery, Restaurant & Dark Kitchen Supply)

- Documents, Parcels & Small Package Cargo

- Industrial Components, Spare Parts & MRO Cargo

- Government, Defence & Disaster Relief Cargo

- Market Size & Forecast by Maximum Takeoff Weight (MTOW) Class

- Nano & Micro UAV (Below 2 kg MTOW)

- Small UAV (2 kg to 25 kg MTOW)

- Medium UAV & Cargo Drone (25 kg to 150 kg MTOW)

- Large UAV & eVTOL Cargo Aircraft (Above 150 kg MTOW)

- Market Size & Forecast by Propulsion Type

- Battery-Electric Propulsion

- Hybrid Electric (Battery & Combustion Engine) Propulsion

- Hydrogen Fuel Cell Propulsion

- Conventional Combustion Engine Propulsion

- Market Size & Forecast by Infrastructure Type

- Vertiport & Skyport Cargo Hub Infrastructure

- Rooftop Landing & Micro-Hub Integration

- Hospital Helipad & Medical Campus Integration

- Warehouse, Fulfilment Centre & Last-Mile Hub Integration

- UTM & Air Traffic Management Software & Communication Infrastructure

- Market Size & Forecast by End-User

- E-Commerce & Quick Commerce Logistics Companies

- Healthcare Systems, Hospitals & Pharmaceutical Distributors

- Government, Defence & Public Safety Agencies

- Express Courier, Parcel & Freight Companies

- Industrial, Manufacturing & MRO Operators

- Smart City Development Authorities & Urban Planners

- Market Size & Forecast by Sales Channel

- Direct Operator-to-End-User Service Agreement

- Third-Party Logistics (3PL) Platform Integration

- Government Tender & Public Procurement

- API-Based & Platform Marketplace Integration

- White-Label & Franchise Urban Air Cargo Network

- Northern India Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

- Western India Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

- Southern India Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

- Eastern India Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

- Central India Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

- City-Wise* Urban Air Cargo Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes Carried & Number of Flights / Sorties)

- By Aircraft & Vehicle Type

- By Cargo Type

- By Operation Type

- By End-User

- By City / Corridor

- By Sales Channel

- Market Size & Forecast

*Key Cities & Urban Agglomerations Analyzed in the Syllogist Global Research Portfolio: Delhi NCR, Mumbai Metropolitan Region, Bengaluru, Chennai, Hyderabad, Kolkata, Pune, Ahmedabad, Jaipur, Lucknow, Chandigarh, Kochi, Bhubaneswar, Indore, Nagpur, Surat, Visakhapatnam, Coimbatore, Guwahati, Varanasi

- Technology Landscape & Innovation Analysis

- Proton Exchange Membrane Fuel Cell (PEMFC) Propulsion & Power System Technology Deep-Dive

- Liquid Hydrogen (LH2) Cryogenic Storage, Insulation & Boil-Off Management Technology

- Hydrogen Combustion Turbine & Turboprop Engine Adaptation Technology

- Green Hydrogen Electrolysis: PEM & Alkaline Electrolyser Scaling for Aviation Applications

- Compressed Gaseous Hydrogen (CGH2) High-Pressure Composite Cylinder & Dispensing Technology

- Digital Twin, AI Predictive Maintenance & Hydrogen Airside Safety Monitoring Technology

- Hybrid Hydrogen-Electric Propulsion & Energy Management System Technology

- Patent & IP Landscape in Hydrogen Aviation Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Green & Blue Hydrogen Production Equipment & Electrolyser Manufacturing Supply Chain

- Cryogenic Storage Vessel, Insulation Material & LH2 Equipment Supply Chain

- Fuel Cell Stack, Membrane Electrode Assembly & Balance-of-Plant Component Supply Chain

- High-Pressure Composite Cylinder, Valve & Regulator Supply Chain

- Hydrogen Dispensing, Metering & Airport Fuelling Equipment Supply Chain

- EPC Contractor, System Integrator & Infrastructure Developer Landscape

- O&M Service Provider, Safety Inspection & Through-Life Support Channel

- Pricing Analysis

- Airport Hydrogen Fuelling Station & LH2 Storage Infrastructure Capital Cost Analysis

- Green Hydrogen Production Cost: Levelised Cost of Hydrogen (LCOH) at Aviation Scale

- Fuel Cell Propulsion System & Cryogenic Tank Aircraft Integration Cost Analysis

- CGH2 vs. LH2 Infrastructure: Capital, Operating & Total Cost of Ownership Comparison

- Hydrogen vs. Sustainable Aviation Fuel (SAF) vs. Battery-Electric: Levelised Cost per Seat-km Analysis

- Total Infrastructure Programme Economics: Development, Construction, Commissioning & Lifecycle Cost Modelling

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Hydrogen Aviation Infrastructure: Well-to-Wake Carbon Footprint by Production Pathway

- Green Hydrogen Aviation vs. Jet-A Kerosene & SAF: CO2, NOx & Contrail Impact Comparison

- Water Vapour Emissions, High-Altitude Contrail Formation & Climate Impact of Hydrogen Combustion

- Circular Economy Considerations: Fuel Cell Stack Recycling, Platinum Group Metal Recovery & Component End-of-Life

- CORSIA Compliance, EU Emissions Trading Scheme (ETS) Aviation Scope & Green Hydrogen Eligibility for Carbon Credits

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Energy Companies & Green Hydrogen Producers Entering Aviation Infrastructure

- Specialist Hydrogen Fuelling Infrastructure & Cryogenic Equipment Developers

- Fuel Cell System Manufacturers & Propulsion Technology Providers

- Aircraft OEMs & Airframe Developers with Hydrogen Platform Programmes

- Airport Operators & Ground Services Companies Piloting Hydrogen Infrastructure

- EPC Contractors & Project Developers Specialising in Hydrogen Aviation Infrastructure

- Digital Monitoring, Safety Systems & AI Platform Providers for Hydrogen Airside Operations

- Start-ups, Spin-Offs & Government-Backed Research Consortia in Hydrogen Aviation

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Hydrogen Aviation Infrastructure Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Hydrogen Aviation Segment) & Project Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Pilot Projects, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output