Market Definition

The Global Vehicle Operating Systems Market, also referred to as the Automotive OS Platforms Market, encompasses the development, licensing, integration, customization, and ongoing software maintenance of the foundational operating system layers that manage hardware resource allocation, real-time process scheduling, inter-process communication, memory management, device driver interfaces, and application execution environments across the diverse electronic control unit and high-performance compute platform architectures deployed within passenger vehicles, light commercial vehicles, heavy commercial vehicles, two-wheelers, and off-highway equipment. Automotive operating systems span a broad spectrum of deployment contexts, including safety-critical real-time operating systems governing powertrain control units, chassis safety modules, and body domain controllers where deterministic execution timing and functional safety compliance to ISO 26262 Automotive Safety Integrity Level standards are non-negotiable engineering requirements; high-performance operating systems underpinning cockpit domain controllers and central vehicle computers executing infotainment, instrument cluster, navigation, and connectivity applications requiring rich graphical user interface rendering and third-party application runtime environments; and automotive-grade operating system platforms designed to unify previously fragmented domain-specific electronic control architectures into centralized zone or vehicle-wide compute platforms that reduce hardware proliferation, simplify over-the-air software update management, and enable the continuous post-sale feature delivery model that defines the software-defined vehicle architecture paradigm. The market encompasses operating system kernel and middleware licensing fees, professional services revenues associated with operating system integration, porting, and safety certification support, software development kit and toolchain licensing, application store platform revenues, and recurring over-the-air update infrastructure subscription revenues. Key participants include automotive operating system software vendors, automotive-grade Linux consortium contributors, real-time operating system specialists, semiconductor platform providers supplying integrated system-on-chip solutions with bundled OS software stacks, automotive OEMs developing proprietary in-house operating system platforms, and Tier-1 electronic system integrators responsible for operating system adaptation and vehicle platform integration across OEM-nominated hardware architectures.

Market Insights

The global vehicle operating systems market is at the epicenter of the most consequential architectural transformation in automotive electronics history, as the industry-wide transition from deeply fragmented distributed electronic control unit architectures, in which individual domain-specific microcontrollers each ran isolated purpose-built software stacks with no shared operating system infrastructure, toward consolidated high-performance compute platforms executing centralized vehicle software on automotive-grade operating system foundations is fundamentally reordering the competitive dynamics between traditional automotive Tier-1 suppliers, semiconductor platform companies, technology-native software vendors, and vertically integrating OEMs who recognize operating system control as the decisive lever of software-defined vehicle platform differentiation and post-sale revenue generation. The global vehicle operating systems market was valued at approximately USD 5.8 billion in 2025 and is projected to reach USD 18.4 billion by 2034, advancing at a compound annual growth rate of 13.6% over the forecast period from 2027 to 2034, driven by the accelerating OEM transition toward zonal and centralized electrical architecture programs, the expanding over-the-air software update infrastructure requirements of software-defined vehicles, and the growing commercial importance of in-vehicle application ecosystems whose monetization depends critically on the application runtime environment, security model, and developer platform capabilities delivered by the vehicle operating system layer.

The software-defined vehicle paradigm is fundamentally altering the commercial logic of automotive operating system procurement, as OEMs that historically sourced operating system software as an embedded component within Tier-1 supplied electronic control unit assemblies with no independent licensing relationship or software upgrade lifecycle are now actively negotiating direct operating system platform licensing agreements, establishing in-house software centers with hundreds to thousands of software engineers focused on operating system adaptation and application development, and in the most advanced cases developing fully proprietary automotive operating system platforms designed to establish durable software platform differentiation that cannot be replicated by competitors sharing the same Tier-1 supplied operating system foundation. Volkswagen Group’s CARIAD software subsidiary, Stellantis STLA Brain platform, General Motors Ultifi software platform, and Toyota Woven Planet operating system development programs collectively represent an investment of over USD 50 billion in proprietary automotive software platform development committed by OEMs who concluded that dependence on externally supplied operating system platforms creates an unacceptable strategic vulnerability in a product competitive landscape where software update frequency, application ecosystem depth, and user experience differentiation are becoming primary vehicle purchase decision criteria for the consumer demographics driving premium segment volume growth globally.

The competitive landscape for automotive operating system platforms is bifurcated between real-time operating system platforms governing safety-critical vehicle control domains, where AUTOSAR Classic and Adaptive Platform specifications define the middleware and application interface standards that enable multi-supplier software component integration across OEM-defined hardware architectures, and high-level operating system platforms for cockpit and vehicle compute domains, where Android Automotive OS, Linux-based platforms including AGL Automotive Grade Linux, QNX Neutrino, and proprietary OEM-developed platforms compete for the infotainment, instrument cluster, and central compute deployments whose application ecosystem breadth, developer community scale, and third-party service integration capabilities most directly influence consumer perception of vehicle digital experience quality. Android Automotive OS deployments in passenger vehicles reached approximately 38 million cumulative vehicles in service globally by 2025, driven by OEM program nominations from Volvo, Polestar, Renault, General Motors, Honda, and multiple Chinese OEMs who selected Google’s automotive OS platform for its pre-integrated Google Play ecosystem, Google Maps navigation service, and Google Assistant voice interface capabilities that reduce OEM content licensing investment while delivering consumer-familiar digital service experiences, though at the strategic cost of ceding application ecosystem governance, user data ownership, and long-term platform roadmap control to a technology company whose automotive interests may not align with OEM competitive positioning requirements over multi-decade vehicle platform lifecycles.

From a regional perspective, China has emerged as the most dynamic and technologically aggressive market for automotive operating system development, with domestic OEMs including BYD, SAIC, Geely, Li Auto, NIO, and Xpeng each operating dedicated automotive software subsidiaries developing proprietary operating system platforms tailored to Chinese consumer preferences for deeply integrated smartphone ecosystem connectivity, voice-first interaction paradigms optimized for Mandarin natural language processing, and over-the-air feature delivery cadences that match the update frequency expectations established by Chinese consumer electronics platforms. Europe retains significant market weight as the home geography of operating system platform decisions for Volkswagen Group, Stellantis, BMW Group, Mercedes-Benz, and Renault Group, whose combined global vehicle production volume of approximately 22 million units annually makes their operating system platform selections among the highest-volume deployment decisions in the global market, with European regulatory frameworks including UNECE WP.29 cybersecurity regulation UN R155 and software update regulation UN R156 imposing vehicle type approval obligations for over-the-air update management systems that directly shape automotive operating system architecture requirements across all OEM programs sold in European markets. North America, anchored by General Motors, Ford, Stellantis North America, and the large Tesla installed base whose proprietary Linux-based operating system defines the reference architecture for vertically integrated automotive software platform development, generates the most commercially advanced software-defined vehicle business model experimentation globally, with subscription-based feature unlocking, over-the-air performance upgrade purchasing, and connected service revenue generation through the vehicle operating system platform already generating meaningful recurring revenue streams that validate the commercial logic of operating system investment for OEMs and platform software vendors alike.

Key Drivers

Automotive OEM Transition to Centralized Zonal Electrical Architectures Creating Structural Demand for Unified High-Performance Vehicle Operating System Platforms

The industry-wide migration from distributed domain-based electronic control unit architectures, in which a modern premium vehicle may contain 100 or more individual electronic control units each running isolated proprietary software on purpose-built microcontrollers with no shared software infrastructure, toward centralized zonal architectures consolidating vehicle compute onto three to five high-performance domain controllers or a single central vehicle computer running unified operating system environments is creating a structural and non-discretionary demand catalyst for automotive-grade operating system platforms capable of managing heterogeneous multi-core processor resources, real-time and non-real-time application coexistence, hardware abstraction across diverse semiconductor platforms, and ISO 26262 safety-partitioned execution environments within a single converged software stack. The zonal architecture transition is being driven simultaneously by the escalating cost and weight of the wiring harness complexity required to interconnect large numbers of distributed electronic control units, which has become a production bottleneck and vehicle weight contributor incompatible with battery electric vehicle range optimization targets, and by the software update lifecycle management requirements of software-defined vehicles that demand a unified operating system foundation enabling atomic over-the-air updates across the complete vehicle software stack rather than the complex multi-ECU update orchestration required in distributed architectures. Major OEM electrical architecture transition programs including Volkswagen Group E3 2.0, BMW EE Next, Mercedes-Benz MB.OS, and Toyota Arene are each predicated on operating system platform standardization as the foundational enabler of software-defined vehicle capability delivery, confirming the architectural demand for unified automotive OS platforms as an OEM investment priority rather than a discretionary technology enhancement.

Over-the-Air Software Update and Post-Sale Feature Monetization Requirements Elevating Automotive Operating System Platform Strategic Importance for OEM Revenue Architecture

The commercial imperative to generate recurring post-sale software and service revenues through over-the-air feature delivery, subscription-based capability unlocking, and connected service monetization is transforming the automotive operating system from a commodity embedded software component into a strategic revenue infrastructure asset whose capabilities directly determine the addressable post-sale revenue opportunity available to OEMs and their software ecosystem partners across the vehicle ownership lifecycle. Tesla demonstrated the commercial proof of concept for over-the-air operating system-enabled revenue generation by delivering Full Self-Driving capability upgrades, acceleration performance enhancements, and premium connectivity feature subscriptions through its proprietary Linux-based vehicle OS, generating an estimated USD 3.5 billion in software and services revenue in 2024 that carries gross margins substantially exceeding vehicle hardware sales and that has prompted every major global OEM to accelerate operating system platform investment as the prerequisite infrastructure for equivalent recurring revenue programs. General Motors OnStar and Ultifi platform generated approximately USD 2.6 billion in connected services revenue in 2024, BMW ConnectedDrive subscription services exceeded USD 1.8 billion in annual recurring revenue, and Stellantis targets USD 20 billion in software and subscription revenues annually by 2030, collectively demonstrating that operating system platform investment decisions made at the vehicle program architecture phase translate directly into recurring revenue generation capability across vehicle ownership lifecycles measured in 10 to 15 years, creating a commercial justification for operating system platform investment that extends well beyond the traditional cost-of-goods framing applied to embedded software procurement in the pre-software-defined vehicle era.

Increasing Vehicle Cybersecurity Regulatory Requirements Under UNECE WP.29 Mandates Driving Systematic Operating System Security Architecture Investment Across Global OEM Programs

The entry into force of United Nations Economic Commission for Europe Regulation UN R155 on cybersecurity management systems and Regulation UN R156 on software update management systems as mandatory vehicle type approval conditions for new vehicle models in the European Union, Japan, South Korea, and other adopting jurisdictions from July 2024 is creating a compliance-driven demand imperative for automotive operating system platforms with certified cybersecurity architecture capabilities including secure boot, hardware security module integration, trusted execution environment isolation, cryptographic key management, intrusion detection, and secure over-the-air update delivery pipelines that satisfy the automotive cybersecurity standard ISO 21434 implementation requirements embedded within the UN R155 type approval framework. Automotive operating systems lacking documented cybersecurity architecture aligned to UN R155 technical requirements are categorically excluded from new vehicle type approval nominations in compliant markets, transforming cybersecurity capability from a desirable differentiating feature into a binary market access prerequisite that is compelling operating system platform vendors to invest in systematic cybersecurity certification programs whose cost and complexity significantly exceed conventional embedded software quality assurance processes. The expanding geographic adoption of UN R155 and R156 frameworks, with China, India, and Brazil progressively aligning national vehicle cybersecurity regulations with the UNECE framework, is amplifying the commercial value of cybersecurity-certified automotive operating system platforms across the global vehicle market and creating sustained investment demand for operating system security architecture development, third-party penetration testing, cybersecurity certification maintenance, and incident response capability that generates recurring engagement revenue for operating system platform vendors beyond initial licensing.

Key Challenges

Software Development Talent Scarcity and the Escalating Engineering Investment Required to Develop and Maintain Competitive Automotive Operating System Platforms

The global scarcity of software engineers with the specialized combination of real-time operating system expertise, automotive functional safety certification experience, embedded systems architecture knowledge, and automotive domain understanding required to develop, integrate, and certify automotive-grade operating system platforms is creating a structural talent bottleneck that constrains the development velocity of both OEM in-house OS platform programs and independent automotive operating system software vendors competing for the same limited pool of qualified engineering talent against well-resourced technology sector employers offering compensation packages, equity upside, and working culture attributes that automotive organizations find structurally difficult to match within their traditional engineering employment frameworks. OEMs and automotive software vendors attempting to staff automotive operating system development programs report unfilled software engineering vacancy rates of 20% to 35% for specialized embedded OS, hypervisor, and safety-critical software architect roles in 2025, with competition for AUTOSAR Adaptive Platform architects, QNX and Linux kernel engineers with automotive safety certification experience, and vehicle cybersecurity architects generating salary inflation of 25% to 40% above general software engineering market rates in automotive software center locations including Munich, Stuttgart, Detroit, Shanghai, and Shenzhen. The engineering investment required to develop an automotive operating system platform from initial architecture through series production readiness and ISO 26262 ASIL-B or ASIL-D certification, including the extensive hardware-in-the-loop testing, fault injection validation, and independent safety assessment processes mandated by functional safety certification, is estimated at USD 800 million to USD 2.5 billion depending on platform scope, creating a capital barrier that restricts credible platform development capability to a small number of well-capitalized competitors.

Functional Safety Certification Complexity and the Extended Development Timelines Required to Achieve ISO 26262 Compliance for Safety-Critical Automotive OS Deployments

Achieving ISO 26262 functional safety certification for automotive operating system components deployed in safety-critical vehicle control applications requires systematic application of a safety lifecycle methodology that encompasses safety requirement specification, architectural design with demonstrable freedom from interference between safety-relevant and non-safety-relevant software partitions, implementation conforming to safe coding guidelines, unit and integration testing with structural code coverage measurement at the MC/DC level for ASIL-C and ASIL-D components, and independent safety assessment by a third-party assessor whose review scope, documentation depth, and technical scrutiny are calibrated to the target ASIL level in ways that add 12 to 24 months to operating system platform development timelines beyond what equivalent general-purpose embedded OS development programs require. The challenge is compounded by the architectural complexity of modern automotive operating system platforms that simultaneously support safety-critical real-time control partitions and non-safety-relevant infotainment or connected service execution environments within a shared hardware compute substrate, requiring the implementation and certification of hypervisor-based hardware resource partitioning solutions that can demonstrably prevent freedom from interference violations between ASIL-rated and quality-managed software domains at the spatial, temporal, and information interference categories defined by ISO 26262 Part 6 requirements. Each modification to a certified automotive operating system version, including security patches, feature additions, and hardware support updates, triggers a structured safety impact analysis and potentially a full or partial re-certification process that consumes engineering resources and calendar time incompatible with the rapid software update cadences that software-defined vehicle consumer expectations and cybersecurity compliance obligations simultaneously demand.

OEM Fragmentation of Proprietary Automotive OS Platform Investments Creating a Multiplicity of Incompatible Vehicle Software Ecosystems That Constrain Developer Productivity and Application Portability

The concurrent investment by more than a dozen major automotive OEMs in proprietary vehicle operating system platforms, each with distinct application programming interfaces, hardware abstraction layer specifications, application runtime environments, and developer toolchain requirements, is creating a fragmented automotive software ecosystem in which application developers, content providers, and connected service vendors must maintain separate codebases, certification processes, and integration relationships for each OEM platform they target, generating a developer economics challenge that limits the breadth of third-party application and service content available to any individual OEM platform relative to what consolidated platform ecosystems with larger developer community scale could attract. The automotive industry’s historical precedent in hardware standardization through AUTOSAR demonstrates both the feasibility and the limitations of consortia-driven standardization as a response to platform fragmentation, as AUTOSAR Classic achieved meaningful hardware abstraction standardization for domain controller software components while simultaneously generating standards complexity and toolchain cost that imposed their own adoption barriers, particularly for smaller OEMs and suppliers with limited software engineering scale economies. The absence of a dominant automotive operating system platform with the developer ecosystem scale of iOS or Android creates a persistent application content gap between automotive infotainment platforms and smartphone environments that consumer expectations calibrated against mobile device experiences increasingly render conspicuous, as third-party application developers rationally prioritize smartphone platform development over automotive platform porting given the multi-billion user addressable markets of mobile OS platforms compared to the tens of millions of active users achievable on any individual automotive OS deployment, limiting automotive OS application ecosystem depth and reinforcing consumer preference for smartphone projection solutions over native automotive application environments.

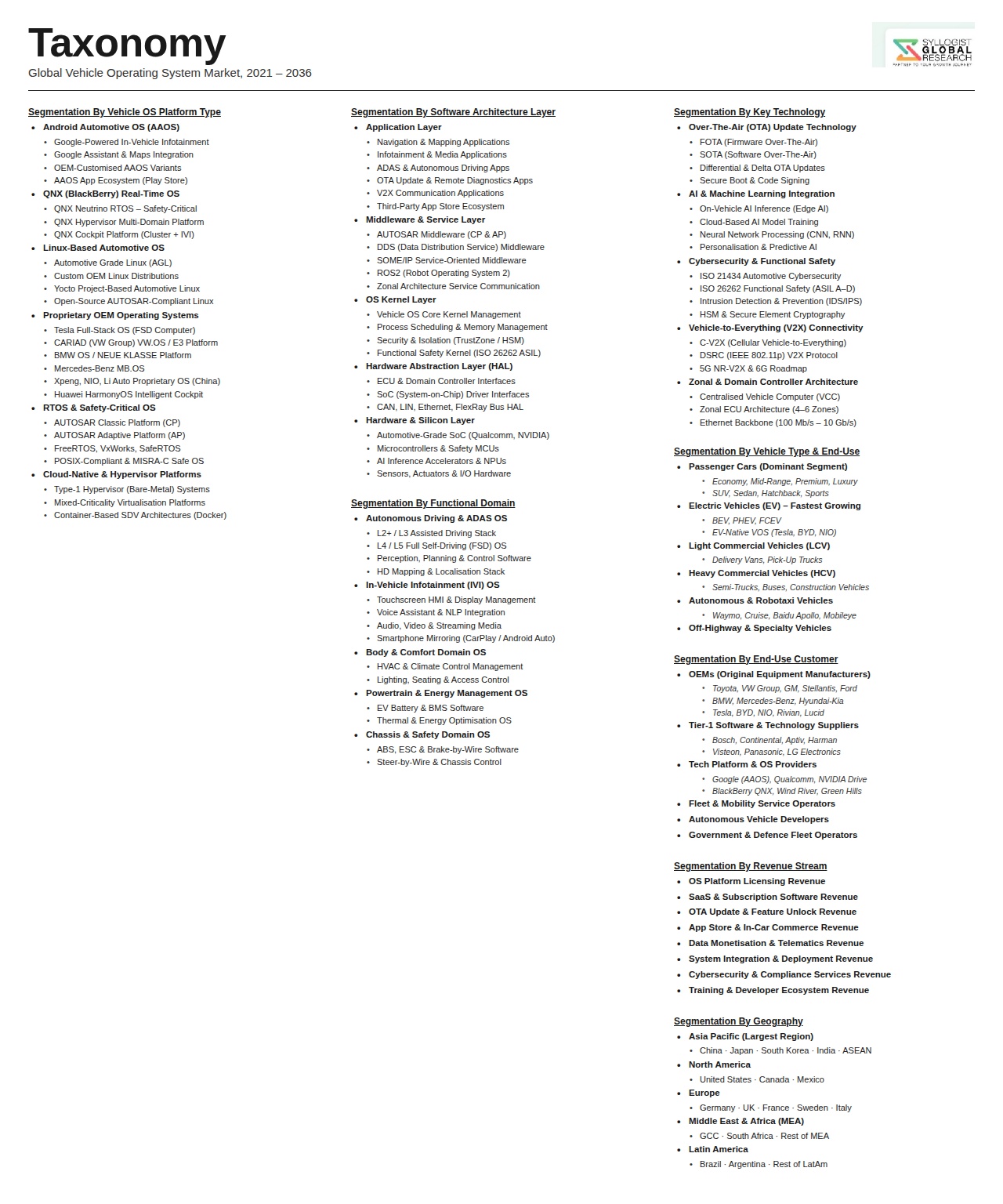

Market Segmentation

- Segmentation By Operating System Type

- Real-Time Operating Systems (RTOS) for Safety-Critical Domain Controllers

- High-Level Operating Systems for Infotainment and Cockpit Domains

- Hypervisor-Based Mixed-Criticality Operating System Platforms

- AUTOSAR Classic Platform-Based Operating System Environments

- AUTOSAR Adaptive Platform-Based Operating System Environments

- Proprietary OEM-Developed Automotive Operating System Platforms

- Open-Source Automotive Linux Platforms (AGL and GENIVI Derivatives)

- Others

- Segmentation By Application Domain

- Powertrain and Engine Control Unit Operating Environments

- Chassis and Active Safety Domain Controllers

- Infotainment and In-Vehicle Infotainment (IVI) Systems

- Digital Instrument Cluster and Head-Up Display Platforms

- Advanced Driver Assistance System (ADAS) and Autonomous Driving Compute

- Body and Comfort Domain Controllers

- Telematics and Connectivity Control Units

- Over-the-Air Update Management Systems

- Battery Management System (BMS) Controllers

- Central Vehicle Computer and Zonal Controller Platforms

- Others

- Segmentation By Architecture Type

- Distributed Domain-Based Electronic Control Unit Architecture

- Consolidated Domain Controller Architecture

- Zonal Electrical Architecture With Central Compute

- Centralized Vehicle Computer Architecture

- Service-Oriented Architecture (SOA) Based Vehicle OS Platforms

- Others

- Segmentation By Deployment Model

- OEM In-House Proprietary Platform Development

- Licensed Third-Party Automotive OS Platform

- Open-Source Platform With OEM or Tier-1 Customization

- Hybrid Proprietary and Open-Source Platform Strategy

- Semiconductor Vendor-Bundled OS Platform

- Others

- Segmentation By Functional Safety Level

- ASIL-D Rated Safety-Critical Operating Environments

- ASIL-C Rated Operating Environments

- ASIL-B Rated Operating Environments

- ASIL-A Rated Operating Environments

- Quality Management (QM) Non-Safety-Critical Environments

- Mixed-Criticality Platforms Spanning Multiple ASIL Levels

- Others

- Segmentation By Vehicle Type

- Passenger Cars (Compact and Sub-Compact)

- Passenger Cars (Mid-Size and Full-Size)

- Premium and Luxury Passenger Cars

- Sport Utility Vehicles (SUVs) and Crossovers

- Light Commercial Vehicles (LCVs) and Pickup Trucks

- Medium and Heavy Commercial Trucks

- Buses and Coaches

- Two-Wheelers and Three-Wheelers

- Off-Highway and Agricultural Equipment

- Others

- Segmentation By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Full Hybrid Electric Vehicles (HEV)

- Plug-In Hybrid Electric Vehicles (PHEV)

- Battery Electric Vehicles (BEV)

- Fuel Cell Electric Vehicles (FCEV)

- Others

- Segmentation By Revenue Model

- Perpetual OS License and One-Time Integration Fees

- Annual Subscription and Recurring License Fees

- Royalty-Per-Vehicle Revenue Model

- Open-Source Platform With Paid Support and Certification Services

- Software Development Kit and Toolchain Licensing

- Over-the-Air Update Infrastructure and Application Store Revenue Sharing

- Others

- Segmentation By End User

- Passenger Vehicle OEMs

- Commercial Vehicle OEMs

- Two-Wheeler OEMs

- Tier-1 Electronic System Integrators

- Semiconductor Platform Vendors

- Automotive Software Middleware and Application Developers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Vehicle Operating Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by OS type across real-time operating systems, high-level infotainment and cockpit platforms, hypervisor-based mixed-criticality environments, AUTOSAR Adaptive platforms, and proprietary OEM-developed platforms, and by application domain across powertrain control, ADAS and autonomous driving compute, infotainment and instrument cluster, body and comfort, and central vehicle computer deployments, to enable automotive OS platform vendors, semiconductor companies, OEM software investment decision-makers, Tier-1 electronic system integrators, and technology investors to identify which OS platform categories and application domains will generate the highest absolute revenue and the most defensible competitive positioning across the forecast period as the industry transitions from distributed ECU to centralized compute architectures?

- How is the OEM transition from distributed domain-based electronic control unit architectures toward zonal and centralized vehicle compute platforms expected to reshape the automotive operating system procurement landscape on a model year and vehicle program basis through 2034, including the projected timeline and volume trajectory of zonal architecture program launches by major OEM groups in Europe, China, North America, Japan, and South Korea, the OS platform selection patterns being established across these programs between proprietary in-house platforms, licensed third-party platforms, and open-source derived platforms, and the resulting competitive share shifts among established RTOS vendors, Android Automotive OS, QNX, Linux-based platforms, and emerging OEM proprietary platforms whose volume nominations are defining the long-term installed base distribution of automotive OS deployments globally?

- What is the projected market size and revenue trajectory of the over-the-air update infrastructure and post-sale software monetization segment enabled by vehicle operating system platforms through 2034, including the revenue models being successfully deployed by leading OEMs for subscription-based feature unlocking, performance upgrade purchasing, connected service delivery, and application store commission revenue, the per-vehicle annual software and services revenue benchmarks achieved by Tesla, General Motors, BMW, Mercedes-Benz, and Stellantis as reference points for the commercial opportunity, and the operating system platform architecture capabilities including secure OTA delivery, cryptographic signing, staged rollout management, and A/B partition update resilience that are prerequisites for the most commercially advanced post-sale software revenue programs being pursued by OEMs targeting meaningful recurring revenue contributions from in-vehicle software platforms by 2030?

- How are UNECE WP.29 cybersecurity regulation UN R155 and software update regulation UN R156, ISO 21434 automotive cybersecurity standard requirements, and the expanding geographic adoption of these frameworks across Europe, Japan, South Korea, China, India, and Brazil reshaping the cybersecurity architecture requirements, certification investment obligations, and competitive qualification barriers for automotive operating system platform vendors, and which specific cybersecurity platform capabilities including secure boot, hardware security module integration, trusted execution environment isolation, intrusion detection and prevention, and over-the-air update cryptographic signing are emerging as binary market access prerequisites rather than differentiating features for automotive OS platforms nominated in new vehicle type approval programs across major regulatory jurisdictions through the forecast period?

- Who are the leading automotive operating system platform vendors, AUTOSAR solution providers, automotive hypervisor developers, semiconductor companies bundling OS software platforms with system-on-chip solutions, open-source automotive Linux contributors, and OEM proprietary platform development organizations currently defining the competitive landscape of the global vehicle operating systems market, and what are their respective platform technology portfolios across RTOS, high-level OS, and mixed-criticality hypervisor categories, ISO 26262 functional safety certification status and ASIL coverage, OEM program nomination pipelines and confirmed series production deployment volumes, revenue model strategies across licensing, subscription, and royalty structures, developer ecosystem investment and third-party application partner programs, and strategic responses to the OEM in-house platform development trend that threatens to disintermediate established automotive OS platform vendors from the highest-volume centralized vehicle compute deployment opportunities emerging from major OEM electrical architecture transition programs globally?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Cybersecurity, Remote Exploitation & Over-the-Air (OTA) Software Vulnerability Risk

- Platform Fragmentation, Ecosystem Lock-In & OEM Dependency Risk

- Functional Safety Certification Complexity, ISO 26262 & SOTIF Compliance Risk

- Data Privacy, Telematics Data Ownership & Cross-Border Data Sovereignty Risk

- Rapid Technology Obsolescence, Software-Defined Vehicle Transition & Legacy Integration Risk

- Regulatory Framework & Standards

- UNECE WP.29 Cybersecurity & Software Update Management Regulations for Vehicle Operating Systems

- Functional Safety Standards: ISO 26262 ASIL Classification & SOTIF (ISO 21448) for OS-Dependent Functions

- Automotive SPICE, AUTOSAR Adaptive & Classic Platform Architecture Compliance Requirements

- Data Protection, GDPR & Cross-Border Vehicle Data Governance Frameworks Applicable to Vehicle OS

- Type Approval, Homologation & Over-the-Air (OTA) Update Regulatory Frameworks by Region

- Global Vehicle Operating Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Licences Deployed & Units Shipped)

- Market Size & Forecast by OS Type

- Real-Time Operating Systems (RTOS): QNX, VxWorks, FreeRTOS & AUTOSAR Classic-Based OS

- Linux-Based Automotive OS: Automotive Grade Linux (AGL), Yocto & Custom OEM Linux Distributions

- Android Automotive OS (AAOS) & Google-Derived Infotainment & Cockpit Platforms

- Proprietary OEM Operating Systems: Tesla OS, Volkswagen VW.OS, GM VHAL & Ford Sync Platform

- AUTOSAR Adaptive Platform: Service-Oriented Architecture & High-Performance Compute OS

- Hypervisor & Virtualisation Platforms: Type 1 & Type 2 Hypervisors for Multi-Domain Consolidation

- Autonomous Driving & ADAS-Specific OS: ROS 2, NVIDIA DriveOS & Mobileye EyeQ Platform OS

- Market Size & Forecast by Component

- Kernel & Core OS Layer: Scheduling, Memory Management & Hardware Abstraction Layer (HAL)

- Middleware & Communication Stack: SOME/IP, DDS, V2X Protocol Stack & Diagnostic Middleware

- Hypervisor & Virtualisation Layer

- Application Framework & API Layer: HMI Framework, App Runtime & Voice Assistant Integration

- Security Module: Secure Boot, HSM Integration, Intrusion Detection & OTA Security Framework

- OTA Update Management & Software Lifecycle Management Platform

- Development Tools, SDKs, IDEs & Simulation Environments

- Market Size & Forecast by Architecture

- Domain-Centralised Architecture: Domain Control Units (DCU) & Zone Controller-Based OS

- Zonal Architecture: High-Performance Central Vehicle Computer & Zonal ECU OS

- Distributed ECU Architecture: Classic AUTOSAR-Based Multi-ECU OS Deployment

- Service-Oriented Architecture (SOA): Adaptive AUTOSAR & Microservice-Based Vehicle OS

- Market Size & Forecast by Application Domain

- Infotainment, Cockpit & In-Vehicle Experience (IVI) OS

- Advanced Driver Assistance Systems (ADAS) & Automated Driving OS

- Powertrain & Battery Management System (BMS) OS

- Body, Comfort, Lighting & Convenience Control OS

- Chassis, Braking & Stability Control OS

- Telematics, Connectivity & V2X Communication OS

- Gateway, Cybersecurity & Vehicle Network Management OS

- Market Size & Forecast by Deployment Model

- On-Board Embedded OS: Factory-Installed & Hardware-Integrated Deployment

- Cloud-Connected & Hybrid OS: Remote Service Integration & OTA Update-Enabled Deployment

- Software-Defined Vehicle (SDV) Platform: Feature-on-Demand & Continuous Update Deployment

- Market Size & Forecast by Vehicle Type

- Passenger Cars: Hatchbacks, Sedans, SUVs & MPVs

- Light Commercial Vehicles (LCVs): Vans, Pick-Ups & Small Trucks

- Heavy Commercial Vehicles (HCVs): Long-Haul Trucks, Buses & Coaches

- Electric Vehicles (BEV, PHEV & HEV)

- Autonomous & Robotaxi Vehicles

- Two-Wheelers, Three-Wheelers & Micromobility Platforms

- Market Size & Forecast by Sales Channel

- OEM Direct Integration & Platform Licensing

- Tier 1 Automotive Supplier & System Integrator Channel

- Independent Software Vendor (ISV) & App Ecosystem Channel

- Aftermarket OTA Update & Software Subscription Channel

- North America Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Vehicle Operating Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Licences Deployed & Units Shipped)

- By OS Type

- By Component

- By Architecture

- By Application Domain

- By Deployment Model

- By Vehicle Type

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- AUTOSAR Adaptive Platform, Service-Oriented Architecture & Microservice-Based Vehicle OS Deep-Dive

- Hypervisor & Virtualisation Technology: Multi-Domain Consolidation & Mixed-Criticality OS Coexistence

- Software-Defined Vehicle (SDV) Platform Architecture: Feature-on-Demand, OTA Update & Continuous Delivery

- Autonomous Driving OS: ROS 2, NVIDIA DriveOS, Mobileye EyeQ & Safety-Certified AD Stack Technology

- Cybersecurity Architecture: Secure Boot, HSM, IDPS & OTA Security Framework Technology

- AI & Machine Learning Integration in Vehicle OS: On-Board Inference, Edge AI & In-Cabin Intelligence

- V2X & Connectivity Stack: C-V2X, DSRC, 5G-V2X & Integrated Telematics OS Layer Technology

- Patent & IP Landscape in Vehicle Operating System Technologies

- Value Chain & Supply Chain Analysis

- OS Kernel, RTOS & Hypervisor Software Development & Licensing Supply Chain

- Middleware, Communication Stack & Diagnostic Software Supply Chain

- High-Performance Compute SoC, MCU & Hardware Platform Supply Chain Supporting Vehicle OS

- OEM In-House OS Development, Platform Strategy & Software-Defined Vehicle Programme

- Tier 1 System Integrator, ECU Supplier & OS Integration Services Supply Chain

- App Ecosystem, Third-Party Developer & ISV Channel

- OTA Update Infrastructure, Cloud Backend & Lifecycle Management Platform Channel

- Pricing Analysis

- RTOS & Safety-Certified OS Licence Pricing: Per Unit, Per Platform & Enterprise Licence Models

- Android Automotive OS & Linux-Based OS: Royalty-Free vs. Commercial Support Cost Analysis

- Hypervisor & Virtualisation Platform Licensing & Integration Cost Analysis

- AUTOSAR Adaptive Platform Toolchain, Configuration & Integration Cost Structure

- OTA Update Platform & Software Lifecycle Management SaaS Pricing & Revenue Model Analysis

- Total Software Cost per Vehicle Analysis: OS Licence, Middleware, Security & OTA Lifecycle Cost

- Sustainability & Environmental Analysis

- Software-Defined Vehicle OS Contribution to Fuel Efficiency, Powertrain Optimisation & CO2 Reduction

- OTA Update & Remote Feature Activation: Reducing Physical Service Visits, Parts Usage & Vehicle Lifecycle Extension

- Energy-Efficient OS Scheduling, Low-Power State Management & Thermal Optimisation for EV Range

- Data Centre & Cloud Backend Carbon Footprint of Connected Vehicle OS & OTA Infrastructure

- ESG Commitments, Open-Source Contribution, Responsible AI & Ethical Data Use Frameworks in Vehicle OS

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by OS Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by OS Type, Application Domain & Geography

- Player Classification

- Established RTOS & Safety-Critical OS Vendors

- Linux Foundation, Open-Source Consortia & Automotive Grade Linux Contributors

- Big Tech Platform Providers: Google Android Automotive, Huawei HarmonyOS & Amazon AWS for Vehicles

- OEM Proprietary OS & In-House Software Platform Developers

- Hypervisor & Virtualisation Technology Providers

- Autonomous Driving OS & AI-Integrated Platform Providers

- Cybersecurity, OTA Update & Software Lifecycle Management Platform Providers

- Start-ups & Deep-Tech Companies in Next-Generation Vehicle OS

- Competitive Analysis Frameworks

- Market Share Analysis by OS Type, Application Domain & Region

- Company Profile

- Company Overview & Headquarters

- Vehicle OS Products & Software Platform Portfolio

- Key Customer Relationships & OEM Design Wins

- Development Centre Locations & Engineering Headcount

- Revenue (Vehicle OS Segment) & Licence Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Platform Launches, Design Wins, OTA Milestones)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By OS Type, Component, Architecture, Application Domain, Vehicle Type & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output