Market Definition

The Global Automotive Interior Materials Market encompasses the design, formulation, manufacturing, processing, and supply of all substrate, surface, cushioning, acoustic, and functional materials applied across the interior cabin environment of passenger vehicles, light commercial vehicles, heavy commercial vehicles, buses, and specialty vehicles, including the instrument panel, door panels, headliner, floor systems, seating assemblies, center console, pillar trim, cargo area liners, and steering wheel surfaces that collectively define the tactile, visual, acoustic, and olfactory characteristics of the in-vehicle experience. Automotive interior materials span a diverse range of material categories encompassing thermoplastic and thermoset polymers used for hard and semi-rigid trim substrates including polypropylene, acrylonitrile butadiene styrene, polycarbonate blends, and thermoplastic olefins; polyurethane foam formulations supplying seating cushion, headrest, armrest, and instrument panel soft-touch padding; woven, knitted, and nonwoven textile fabrics supplying seat upholstery, headliner, and carpet applications; genuine leather and synthetic leather alternatives including polyurethane-coated and polyvinyl chloride-based artificial leather and the emerging category of bio-based and animal-free leather substitutes; natural fiber composite materials including kenaf, flax, hemp, and sisal fiber reinforced polymer panels used in door substrates and package trays; acoustic management materials including fibrous absorbers, mass loaded barriers, and viscoelastic damping compounds governing interior noise, vibration, and harshness performance; and surface finishing materials including paint, soft-touch coating, chrome trim, wood veneer, carbon fiber decorative inlay, and metallic insert components that deliver premium surface quality differentiation across vehicle grade and trim level hierarchies. Key participants include specialty polymer and chemical companies supplying base resins and foam precursors, material converters and laminators, tier-one interior system integrators, automotive OEM interior design and engineering teams, and regulatory bodies whose volatile organic compound emission, flammability, and end-of-life recyclability standards govern material selection across all major global markets.

Market Insights

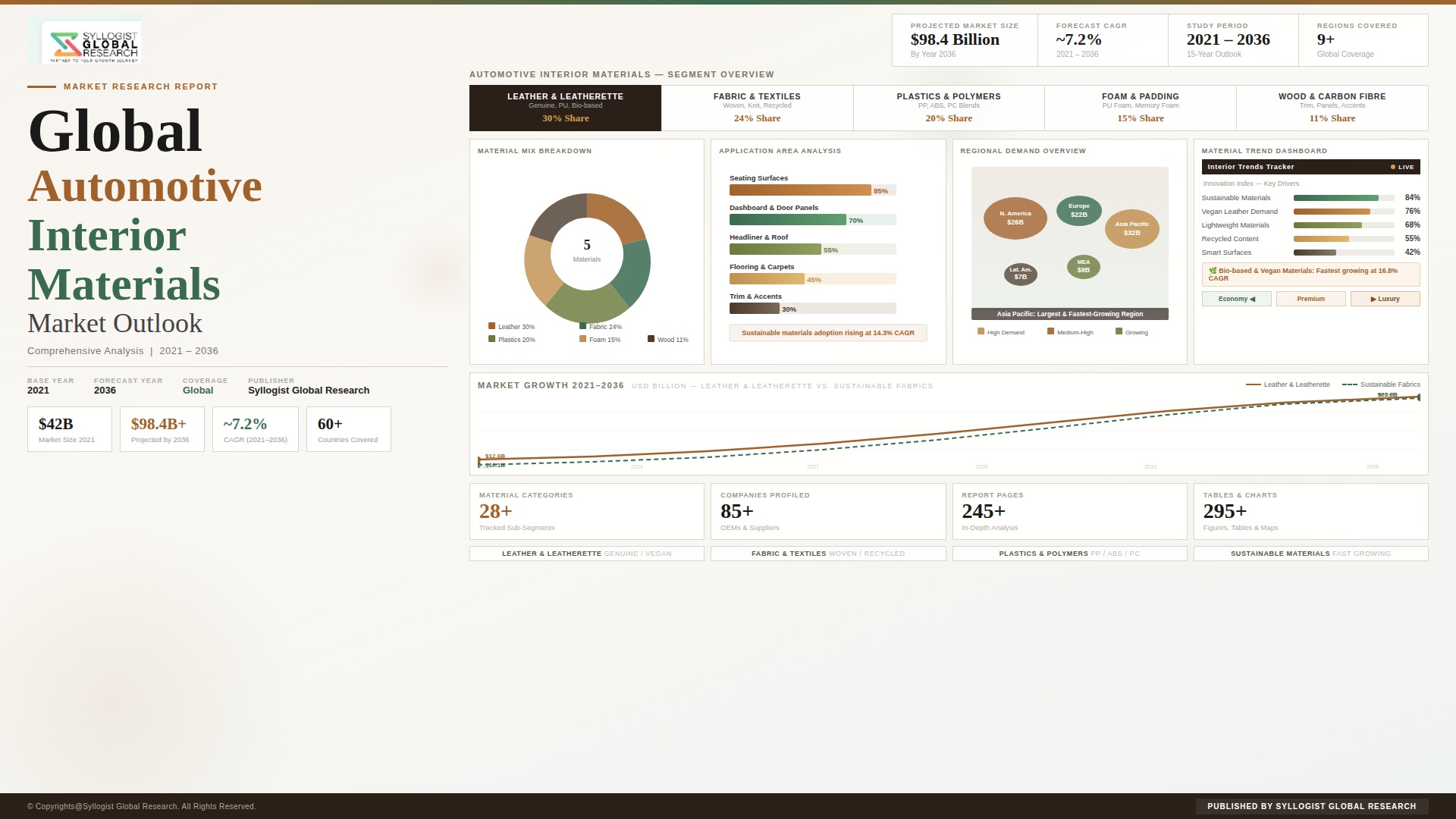

The global automotive interior materials market is undergoing a fundamental redefinition of its value proposition as the convergence of three structural forces reshapes material selection priorities simultaneously across the global vehicle production base: the electrification of powertrains eliminating the powertrain noise masking function of the combustion engine and thereby raising acoustic management material performance requirements to an entirely new threshold; the premiumization of interior cabin expectations across mid-market and entry-level vehicle segments as electric vehicle incumbents and Chinese OEM challengers compete aggressively on interior quality and material sophistication as primary purchase decision criteria; and the intensifying sustainability regulatory and brand commitment requirements compelling systematic substitution of petroleum-derived, high-VOC-emitting, and non-recyclable interior materials with bio-based, recycled-content, and end-of-life recoverable alternatives across OEM material specifications globally. The global automotive interior materials market was valued at approximately USD 52.6 billion in 2025 and is projected to reach USD 78.3 billion by 2034, advancing at a compound annual growth rate of 4.5% over the forecast period from 2027 to 2034, as per-vehicle interior material value escalates driven by premiumization content upgrades, acoustic material specification increases in battery electric vehicles, and the higher unit cost of sustainable material alternatives replacing conventional petroleum-derived substrates across an expanding share of OEM vehicle program material specifications.

The acoustic environment transformation created by battery electric vehicle powertrains represents the most technically demanding materials challenge in automotive interior design, as the elimination of internal combustion engine masking noise exposes a spectrum of previously inaudible interior sound sources including road surface texture noise transmitted through the floor and wheelarch, wind noise ingressing through body seals and glass interfaces, HVAC blower and compressor operating noise, electric motor whine at specific frequency harmonics, and high-voltage power electronics switching noise that collectively create an unfamiliar and often consumer-perceived-as-uncomfortable acoustic signature if not systematically managed through purpose-designed acoustic material solutions. Battery electric vehicles require acoustic material content per vehicle that is approximately 35% to 50% higher by weight and value than equivalent internal combustion engine vehicles, driving a structural per-unit value uplift in floor acoustic systems, dash insulators, door panel acoustic absorbers, wheel arch liners, underbody acoustic treatments, and headliner acoustic management layers whose specifications must be fundamentally redesigned rather than simply incremented from internal combustion engine baseline formulations. The average acoustic and thermal material content per battery electric vehicle reached approximately USD 680 per vehicle in 2025 and is projected to increase to approximately USD 890 per vehicle by 2034, as OEM acoustic comfort targets for battery electric vehicles are progressively elevated toward the ultra-quiet reference benchmarks established by premium segment leaders and consumer expectation calibration continues to advance ahead of mass-market battery electric vehicle interior acoustic performance delivery.

The sustainability transformation of automotive interior material specifications is progressing from a voluntary brand differentiation initiative concentrated in premium vehicle segments toward a systematic material substitution imperative affecting mainstream vehicle programs across all global OEM production volumes, driven by the combination of European Union end-of-life vehicle directive revision requirements mandating minimum recycled content percentages in new vehicle material specifications, OEM corporate sustainability commitments establishing interior material VOC emission reduction targets, consumer sentiment data from major automotive markets showing material origin and sustainability credentials as active purchase consideration factors in sub-40-year-old vehicle buyer segments, and the commercial scaling of bio-based and recycled-content alternative materials whose unit cost premiums relative to conventional equivalents are progressively compressing as production volumes expand. Recycled polyethylene terephthalate fiber derived from post-consumer plastic bottle waste has achieved commercial-scale deployment in automotive seat fabric, trunk liner, and floor carpet applications across OEM programs at multiple global manufacturers including BMW, Volkswagen, Toyota, and Hyundai-Kia, with recycled PET fiber content in automotive textile applications reaching approximately 18% of total automotive fiber demand in 2025 and projected to exceed 31% by 2034 as OEM specification mandates for recycled fiber content in upholstery and carpet applications become standard across vehicle line material guidelines rather than isolated sustainability showcase programs.

From a regional standpoint, Asia-Pacific constitutes the largest and most production-intensive regional market for automotive interior materials, accounting for approximately 47.1% of global market revenue in 2025, anchored by China’s dominant vehicle production volume of approximately 31.6 million vehicles annually and by the exceptionally high interior material content per vehicle that Chinese OEM programs have established as a competitive standard in their domestic market, where interior quality perceptions carry disproportionate purchase decision weight relative to powertrain or chassis performance attributes in the consumer value hierarchy that defines competitive positioning in the world’s largest automotive market. Chinese premium domestic brands including BYD, Li Auto, NIO, Xpeng, and Huawei-partnered Aito have systematically elevated interior material specifications to levels historically associated exclusively with European luxury brands, featuring genuine leather or ultra-premium synthetic leather seating across entry-level trims, ambient lighting integrated into softened instrument panel surfaces, wood veneer and metallic inlay decorative elements previously reserved for flagship models, and microfiber headliner materials substituting for the molded fabric headliners standard in equivalent European and North American vehicle segments, generating per-vehicle interior material values in the Chinese mid-market segment that exceed comparable European or North American segment equivalents by 20% to 35% and driving sustained unit value growth within the Asia-Pacific regional market that amplifies volume-driven revenue growth. Europe represents the second-largest regional market, characterized by the most stringent VOC emission and recyclability regulatory requirements globally, which continue to drive sustained material innovation investment among European chemical companies and material suppliers serving OEM programs subject to Euro 7 interior air quality and end-of-life vehicle directive recycled content compliance obligations.

Key Drivers

Battery Electric Vehicle Proliferation Driving Structural Uplift in Acoustic and Thermal Management Material Content Per Vehicle Across All Segments

The accelerating global production ramp of battery electric vehicles is generating a structurally and durably higher per-vehicle interior material content requirement relative to internal combustion engine equivalents, as the elimination of powertrain masking noise fundamentally transforms the acoustic management material specification challenge and elevates the performance threshold required from floor systems, dash insulators, door panel absorbers, wheel arch liners, and headliner assemblies to achieve the interior acoustic comfort benchmarks that OEM customer satisfaction targets and consumer expectation calibration in the battery electric vehicle segment demand. Battery electric vehicle production globally reached approximately 18.1 million units in 2025 and is projected to exceed 42 million units annually by 2034, with each incremental battery electric vehicle unit entering production carrying an acoustic and thermal material content premium of approximately USD 180 to USD 240 per vehicle relative to a comparable internal combustion engine vehicle, generating a cumulative annual material demand increment attributable exclusively to battery electric vehicle acoustic specification uplift of approximately USD 3.3 billion in 2025 growing to an estimated USD 9.2 billion by 2034 as battery electric vehicle production volumes scale across all segment categories from premium to entry-level. Thermal management material requirements in battery electric vehicles additionally generate demand for new flame-retardant insulation, battery enclosure lining, and thermal runaway protection materials within the passenger cabin boundary that have no equivalent in internal combustion engine vehicle interior material specifications, further expanding the per-vehicle material content addressable by interior materials suppliers with battery electric vehicle-specific product development capabilities.

Premiumization of Vehicle Interior Quality Standards Across Mid-Market and Entry-Level Segments Escalating Per-Vehicle Interior Material Spend Globally

The systematic elevation of interior material quality expectations across mid-market and entry-level vehicle segments, driven by the competitive dynamics of the Chinese domestic market where domestic OEMs have established premium interior specifications as a primary competitive battleground, the aspirational positioning strategies of electric vehicle-native brands whose interior cabin environments serve as the primary physical product differentiation medium in the absence of traditional powertrain performance metrics, and the progressive filtering of premium interior material applications from flagship models into mainstream trim lines by established global OEMs responding to consumer expectation escalation, is generating a sustained per-vehicle interior material value uplift that operates independently of new vehicle production volume trends and amplifies revenue growth across all material categories serving soft-touch, surface quality, and premium appearance applications. The average per-vehicle interior material spend across the global new vehicle production base increased from approximately USD 480 per vehicle in 2019 to approximately USD 564 per vehicle in 2025, a cumulative increase of approximately 17.5% in six years driven primarily by specification escalation in seat upholstery, instrument panel surface, door panel cladding, and headliner material grades rather than by raw material price inflation alone. Synthetic leather and microfiber materials, which carry per-square-meter unit values approximately 2.5 to 4 times those of conventional woven polyester seat fabrics, are experiencing the highest volume growth rates within the automotive upholstery material category as OEMs extend synthetic leather seating from premium trim levels into standard and entry configurations across global vehicle programs, directly expanding the addressable revenue per vehicle for premium surface material suppliers.

Tightening Interior Volatile Organic Compound and Air Quality Regulations Driving Systematic Material Reformulation Investment Across Global OEM Supply Chains

Regulatory escalation in automotive interior air quality standards across China, the European Union, South Korea, and Japan is compelling systematic reformulation of interior material formulations across adhesives, foams, synthetic leathers, coatings, and plastic substrates to achieve volatile organic compound emission profiles compliant with tightening regulatory limits and OEM internal specification standards, generating sustained research and development investment demand for low-VOC and zero-VOC material technologies that carries higher development cost and unit price premiums relative to conventional formulations but creates durable competitive differentiation for material suppliers achieving early regulatory compliance leadership. China GB 27630 standard governing passenger car interior air quality sets limits on benzene, toluene, xylene, ethylbenzene, styrene, formaldehyde, acetaldehyde, and acrolein concentrations that have compelled systematic reformulation of polyurethane foam blowing agents, adhesive formulations, PVC plastisol coatings, and decorative laminate adhesive systems across the supply chains serving Chinese OEM interior programs, with compliance investment costs estimated at USD 12 to USD 38 per vehicle in material reformulation premium above conventional specification equivalents depending on the breadth of material systems requiring simultaneous reformulation within a given vehicle program. The European Union anticipated revision of interior air quality requirements under the broader Euro 7 framework and end-of-life vehicle directive amendments introducing minimum recycled content mandates are generating prospective compliance investment in bio-based plasticizers, water-based coating systems, and solvent-free adhesive technologies that are progressively establishing themselves as the specification baseline for new OEM platform program material approvals across European production operations.

Key Challenges

Raw Material Price Volatility Across Petrochemical, Textile, and Natural Material Supply Chains Compressing Interior Material Supplier Margins Under Fixed OEM Contract Pricing

Automotive interior material manufacturers operate across multiple raw material supply chains whose price dynamics are governed by fundamentally different market mechanisms, including petrochemical-derived polymer resins and polyurethane precursors whose costs fluctuate with crude oil and natural gas feedstock pricing, natural textile fibers including cotton and wool whose prices respond to agricultural commodity and weather cycle dynamics, synthetic textile fibers including polyester and nylon whose costs are linked to purified terephthalic acid and caprolactam derivative pricing within the petrochemical chain, and specialty chemicals including flame retardants, plasticizers, and surface coatings whose pricing reflects specialty chemical supply concentration among a limited number of global producers. The simultaneous exposure to price volatility across these diverse raw material categories creates margin risk that is structurally difficult to hedge within the fixed annual price agreement or modest annual price reduction contractual frameworks that govern automotive Tier-1 and Tier-2 supply agreements, as OEM procurement organizations apply cost reduction targets of 2% to 4% per model year on interior material programs regardless of underlying raw material cost dynamics, compressing material supplier gross margins during raw material inflation episodes to levels that threaten program profitability and capital investment capacity simultaneously. The 2021 to 2023 period of extreme petrochemical feedstock price volatility, which saw polypropylene resin prices increase by over 60% and polyurethane precursor prices increase by over 40% relative to 2020 baseline levels, demonstrated the severity of the margin compression risk facing interior material suppliers operating under automotive contractual pricing frameworks that provide no automatic raw material cost passthrough mechanism.

Performance and Durability Validation Complexity of Sustainable Alternative Materials Extending OEM Approval Timelines and Limiting Scale Deployment of Bio-Based and Recycled-Content Substitutes

The substitution of conventional petroleum-derived interior materials with bio-based, recycled-content, and animal-free alternative materials is consistently constrained by the extended OEM material validation and approval processes required to certify that sustainable alternative materials meet the full spectrum of automotive interior durability, safety, and performance requirements across the 10 to 15 year vehicle service lifecycle, including resistance to ultraviolet light degradation, thermal aging at sustained temperatures up to 120 degrees Celsius in sun-loaded cabin environments, abrasion resistance across simulated passenger ingress and egress cycles, colorfastness under combined UV and humidity exposure, flammability compliance to Federal Motor Vehicle Safety Standard FMVSS 302 and equivalent international standards, and long-term low-VOC emission maintenance as materials age within the closed vehicle cabin environment. Bio-based polyols derived from castor oil, soybean oil, and rapeseed oil as partial replacements for petroleum-derived polyols in polyurethane foam formulations have demonstrated satisfactory initial performance in laboratory conditions but require extended real-world vehicle fleet aging validation programs spanning three to five years before OEM material approval committees authorize full-scale production deployment, delaying the commercial scale-up of bio-based foam formulations that have been technically demonstrated as viable substitutes but cannot achieve volume OEM deployment within the timeline expectations of OEM sustainability commitment reporting cycles. The absence of standardized automotive-specific sustainability performance test protocols that could provide a consistent validation framework across OEM material approval processes creates duplicative testing investment requirements for material suppliers seeking multi-OEM approvals for the same sustainable material formulation.

Consumer Perception Gaps Between Genuine Leather and Premium Synthetic Alternatives Creating Market Resistance to Material Substitution in Luxury and Premium Vehicle Segments

The premium automotive interior materials market confronts a persistent and commercially significant consumer perception challenge in the substitution of genuine leather with synthetic leather, microfiber, and bio-based alternatives in luxury and premium vehicle interior applications, as the tactile properties, aging characteristics, natural variation aesthetics, and aspirational status associations of genuine leather retain strong consumer preference among the demographically established buyer profiles of premium and luxury vehicle segments whose purchase decisions are most sensitive to material authenticity perceptions and whose willingness-to-pay for genuine leather specifications generates the highest per-vehicle revenue contribution within the automotive leather and upholstery material category. OEM consumer research conducted across European and North American premium vehicle buyer panels consistently identifies genuine leather seating as among the top three interior specification attributes influencing purchase satisfaction and brand perception scoring, with synthetic leather alternatives rated as clearly inferior substitutes in tactile quality, breathability, and long-term aging character by experienced premium vehicle buyers whose ownership history provides a direct comparison baseline against which synthetic material performance is evaluated rather than assessed in isolation. The commercial tension between OEM sustainability commitments to eliminate animal-derived materials from interior specifications and the genuine leather preference of existing premium segment customer bases is generating a strategic positioning dilemma that is driving investment in ultra-premium synthetic leather technologies including solvent-free polyurethane topcoat constructions with three-dimensional embossed grain replication and microfiber nonwoven base structures engineered to replicate the compressibility and recovery properties of genuine cowhide, but whose unit cost premiums of 15% to 35% above genuine leather at equivalent quality tiers limit their commercial deployment to OEMs willing to absorb material cost increases without proportionate retail price adjustments.

Market Segmentation

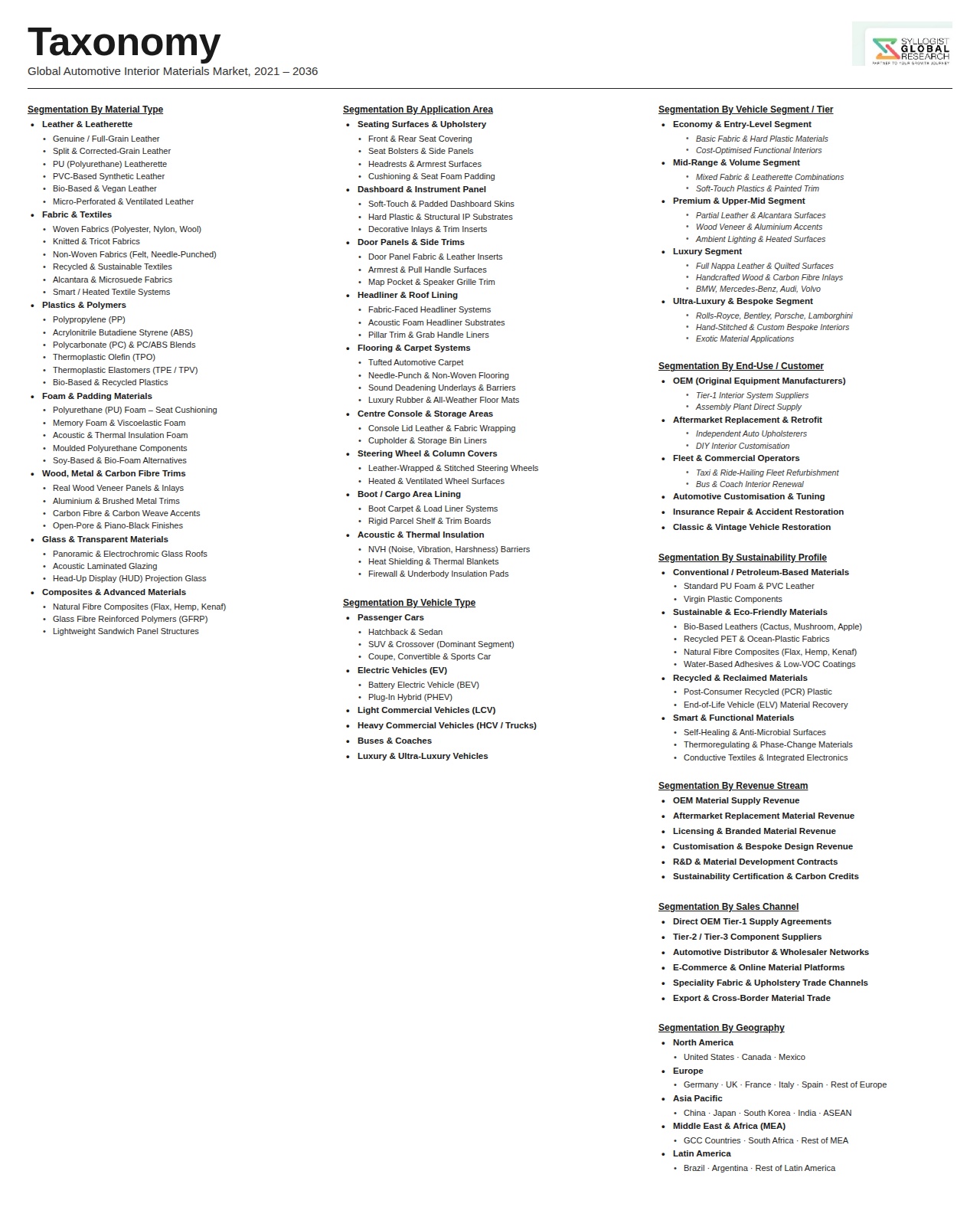

- Segmentation By Material Type

- Thermoplastic Polymers (Polypropylene, ABS, PC Blends, and TPO)

- Polyurethane Foam (Seat Cushion, Headrest, Armrest, and Soft-Touch Pad)

- Genuine Leather (Cowhide, Nappa, and Full-Grain Variants)

- Synthetic Leather (PU-Coated and PVC-Based Artificial Leather)

- Bio-Based and Animal-Free Leather Alternatives

- Woven and Knitted Textile Seat Fabrics

- Nonwoven and Needle-Punched Carpet and Liner Materials

- Microfiber and Alcantara-Type Suede Materials

- Natural Fiber Composites (Kenaf, Flax, Hemp, and Sisal Reinforced Panels)

- Acoustic Absorbers and Noise Insulation Materials

- Mass Loaded Barriers and Viscoelastic Damping Compounds

- Wood Veneer, Carbon Fiber Inlay, and Decorative Trim Materials

- Surface Coatings, Soft-Touch Paints, and Texture Films

- Thermal and Fire-Resistant Insulation Materials

- Others

- Segmentation By Application

- Seating Systems (Cushion, Backrest, Headrest, and Armrest Surfaces)

- Instrument Panel and Dashboard Surfaces

- Door Panel Cladding and Trim

- Headliner and Roof Interior

- Floor Systems and Carpet Assemblies

- Center Console and Transmission Tunnel Cladding

- Pillar Trim (A, B, and C Pillars)

- Steering Wheel Covering and Grip Materials

- Cargo Area Liners and Boot Trim

- Acoustic Underbody and Wheel Arch Insulation

- Others

- Segmentation By Vehicle Type

- Passenger Cars (Compact and Sub-Compact)

- Passenger Cars (Mid-Size and Full-Size)

- Premium and Luxury Passenger Cars

- Sport Utility Vehicles (SUVs) and Crossovers

- Light Commercial Vehicles (LCVs) and Pickup Trucks

- Medium and Heavy Commercial Trucks

- Buses and Coaches

- Two-Wheelers and Three-Wheelers

- Others

- Segmentation By Propulsion Type

- Internal Combustion Engine (ICE) Vehicles

- Full Hybrid Electric Vehicles (HEV)

- Plug-In Hybrid Electric Vehicles (PHEV)

- Battery Electric Vehicles (BEV)

- Fuel Cell Electric Vehicles (FCEV)

- Others

- Segmentation By Material Origin

- Petroleum-Derived Conventional Materials

- Bio-Based and Renewable Origin Materials

- Recycled-Content and Post-Consumer Waste Derived Materials

- Animal-Derived Natural Materials (Genuine Leather and Wool)

- Hybrid Bio-Based and Recycled Blend Materials

- Others

- Segmentation By Vehicle Trim Level

- Entry-Level and Base Trim Specifications

- Mid-Level and Standard Trim Specifications

- Premium Trim and Comfort Package Specifications

- Luxury and Flagship Trim Specifications

- Performance and Sport Edition Specifications

- Others

- Segmentation By Sales Channel

- Original Equipment Manufacturer (OEM) Direct Supply

- Tier-1 Interior System Integrator Supply

- Aftermarket Replacement and Customization

- Independent Distributors and Converters

- Others

- Segmentation By End User

- Passenger Vehicle OEMs

- Commercial Vehicle OEMs

- Bus and Coach Manufacturers

- Tier-1 Interior Module and Seat System Suppliers

- Aftermarket Upholstery and Customization Specialists

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Automotive Interior Materials Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by material type across polyurethane foam, thermoplastic polymers, genuine leather, synthetic leather, textile fabrics, natural fiber composites, acoustic insulation, and sustainable alternative materials, and by application across seating, instrument panel, door panels, headliner, floor systems, and acoustic underbody, to enable interior material manufacturers, specialty chemical companies, OEM material procurement teams, Tier-1 interior system integrators, and sustainability-focused investors to identify which material categories and application segments will generate the highest absolute revenue growth and the strongest unit value escalation trajectory across the forecast period in the context of battery electric vehicle acoustic requirement uplift, premiumization trends, and sustainable material substitution mandates?

- How is the proliferation of battery electric vehicles across all global vehicle segments expected to reshape per-vehicle interior material content specifications, mix, and value through 2034, specifically quantifying the incremental acoustic and thermal management material demand generated per battery electric vehicle relative to equivalent internal combustion engine vehicles across floor systems, dash insulators, door panel absorbers, wheel arch liners, headliner acoustic treatments, and battery enclosure thermal materials, and identifying which acoustic and thermal material technologies including fibrous absorbers, mass loaded barriers, viscoelastic damping compounds, and aerogel-based thermal insulators are best positioned to capture the battery electric vehicle-driven material content increment across mainstream and premium vehicle program specifications globally?

- What is the projected market size, growth trajectory, and competitive landscape of the sustainable automotive interior materials segment through 2034, including the revenue split between bio-based polymer and foam materials, recycled-content textile and fiber applications, animal-free synthetic leather alternatives, and natural fiber composite panel materials, the OEM program deployment timelines and volume trajectories for sustainable material mandates across major vehicle manufacturers in Europe, China, North America, and Asia-Pacific, the unit cost premium evolution of sustainable alternatives relative to conventional equivalents as production volumes scale, and the regulatory requirements including EU end-of-life vehicle directive recycled content mandates and China GB 27630 VOC emission limits that are accelerating the substitution timeline for sustainable material adoption across mainstream vehicle program material specifications?

- How are the premiumization dynamics in the Chinese domestic vehicle market, specifically the elevation of interior material quality standards by domestic electric vehicle OEMs including BYD, Li Auto, NIO, Xpeng, and their technology-partnered variants, expected to influence per-vehicle interior material value benchmarks, material specification standards, and competitive positioning requirements for global material suppliers serving Chinese OEM programs, and how are the 20% to 35% per-vehicle interior material value premiums established by leading Chinese domestic OEM programs relative to comparable European and North American segment equivalents creating competitive pressure on European and North American OEMs to escalate their own mid-market vehicle interior material specifications in response to the shifting consumer quality reference baseline that Chinese OEM programs are establishing globally?

- Who are the leading automotive interior material manufacturers across thermoplastic polymer compounding, polyurethane foam systems, genuine and synthetic leather, technical textile and carpet, acoustic management, natural fiber composite, and sustainable bio-based material categories currently defining the competitive landscape of the global automotive interior materials market, and what are their respective product portfolios and technology development roadmaps across conventional and sustainable material categories, OEM program nomination pipelines and platform coverage across major vehicle production regions, manufacturing footprint and capacity expansion strategies for bio-based and recycled-content material scaling, compliance investment programs for VOC emission and end-of-life recyclability regulatory requirements, and strategic partnership models with OEM sustainability teams, Tier-1 interior integrators, and raw material innovation partners pursuing next-generation animal-free leather and bio-circular polymer solutions for automotive interior deployment through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility: Petroleum-Derived Polymers, Natural Fibres & Specialty Chemical Input Risk

- Tightening VOC, Flame Retardancy & Hazardous Substance Regulation Compliance Risk

- Supply Chain Disruption, Single-Source Dependency & Logistics Cost Volatility Risk

- Consumer Preference Shift, Sustainability Expectations & Bio-Based Material Adoption Risk

- EV & Autonomous Vehicle Interior Design Disruption & Material Requirement Change Risk

- Regulatory Framework & Standards

- VOC Emission Limits, Indoor Air Quality Standards & Odour Testing Requirements for Automotive Interiors

- Flame Retardancy & Fire Safety Standards: FMVSS 302, ECE R118 & Material Flammability Testing

- REACH, RoHS & Restricted Hazardous Substance Standards Applicable to Automotive Interior Materials

- Recycled Content Mandates, End-of-Life Vehicle (ELV) Directive & Bio-Based Material Procurement Frameworks

- Crashworthiness, Occupant Protection & Interior Surface Safety Standards: FMVSS, ECE & NCAP Requirements

- Global Automotive Interior Materials Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes & Square Metres)

- Market Size & Forecast by Material Type

- Leather & Leather Alternatives: Genuine Leather, PU Synthetic Leather & Vegan Bio-Based Leather

- Thermoplastic Polymers: PP, ABS, PC/ABS Blends & TPO for Door Panels, Dashboards & Trims

- Polyurethane (PU) Foam: Seating Foam, Headliner Foam & Acoustic Absorption Foam

- Textiles & Woven Fabrics: Woven, Knitted, Tufted & Non-Woven Seat & Headliner Fabrics

- Natural Fibre Composites: Kenaf, Flax, Hemp, Jute & Coir-Reinforced Bio-Composite Panels

- Glass Fibre & Carbon Fibre Reinforced Composites for Structural Interior Load-Bearing Components

- Acoustic & Thermal Insulation Materials: Mineral Wool, PET Fibre, Melamine Foam & Multi-Layer Laminates

- Wood, Aluminium & Decorative Surface Trim Materials: Real Wood Veneer, Brushed Metal & Hydrographic Films

- Adhesives, Sealants & Surface Coatings: Interior Bonding, Anti-Scratch & Haptics Enhancement Coatings

- Smart & Functional Materials: Electrochromic Films, Conductive Textiles & Embedded Sensor Substrates

- Market Size & Forecast by Technology

- Injection Moulding & Multi-Shot Moulding Technology for Interior Plastic Trim

- Thermoforming, Vacuum Forming & Press Lamination Technology for Surface Panels

- Slush Moulding & Spray PU Technology for Soft-Touch Dashboard & Door Panel Skins

- Foam-in-Place, Hot Compression Moulding & Cut-and-Sew Technology for Seating

- In-Mould Decoration (IMD), In-Mould Labelling (IML) & Laser Etching for Surface Aesthetics

- 3D Knitting, Spacer Fabric & Additive Manufacturing Technology for Interior Textile Components

- Bio-Based Polymer Processing & Natural Fibre Composite Compression Moulding Technology

- Acoustic Simulation, NVH Testing & Material Performance Validation Technology

- Market Size & Forecast by Application

- Seating Systems: Seat Covers, Cushion Foam, Seat Backs & Headrests

- Dashboard & Instrument Panel Assemblies

- Door Panels, Armrests & Side Trim

- Headliner, Roof Lining & Pillar Trim

- Floor Covering, Carpet & Under-Carpet Acoustic Layers

- Centre Console, Storage & Gear Shift Surrounds

- Steering Wheel Wrapping & Column Trim

- Trunk Lining, Boot Floor & Load Compartment Trim

- Market Size & Forecast by Vehicle Type

- Passenger Cars: Economy, Mid-Range & Premium Segments

- Light Commercial Vehicles (LCVs): Vans, Pick-Ups & Small Trucks

- Heavy Commercial Vehicles (HCVs): Trucks, Buses & Coaches

- Electric Vehicles (BEV, PHEV & HEV)

- Autonomous & Shared Mobility Vehicles

- Two-Wheelers, Three-Wheelers & Recreational Vehicles

- Market Size & Forecast by End-User

- OEM First-Fit Supply: Tier 1 Interior Systems Integrators & Component Suppliers

- Aftermarket Replacement, Refurbishment & Customisation

- Fleet Operators, Rental Companies & Commercial Vehicle Converters

- Market Size & Forecast by Sales Channel

- OEM Direct Supply & Tier 1 Long-Term Supply Agreement

- Tier 2 & Tier 3 Specialty Material & Chemical Supplier Channel

- Aftermarket Distributor, Retailer & Custom Upholstery Channel

- Online & Direct-to-Workshop E-Commerce Channel

- North America Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Automotive Interior Materials Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes & Square Metres)

- By Material Type

- By Technology

- By Application

- By Vehicle Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Bio-Based & Vegan Leather Alternatives: Mushroom Leather, Cactus Leather, Pinatex & Recycled PET Textile Deep-Dive

- Natural Fibre Composite Technology: Kenaf, Flax & Hemp Reinforced Bio-Composites for Lightweight Interior Panels

- Smart Surface & Functional Material Technology: Conductive Textiles, Electrochromic Films & Touch-Sensitive Substrates

- Acoustic & NVH Material Innovations: Ultra-Thin Absorbers, Microperforated Films & Multi-Layer Damping Composites

- Sustainable Foam Technology: Bio-Based PU, Recycled-Content Foam & Water-Blown Formulation Advances

- In-Mould Decoration, Surface Haptics & Soft-Touch Coating Technology for Premium Interior Surfaces

- Additive Manufacturing & Digital Knitting for Mass-Customised Interior Textile & Trim Components

- Patent & IP Landscape in Automotive Interior Material Technologies

- Value Chain & Supply Chain Analysis

- Petrochemical Feedstock, Bio-Based Monomer & Specialty Polymer Raw Material Supply Chain

- Leather Tanning, PU Synthetic Leather Coating & Textile Weaving Supply Chain

- Foam Formulation, Moulding & Lamination Supply Chain

- Natural Fibre Harvesting, Processing & Composite Panel Manufacturing Supply Chain

- Tier 1 Interior Systems Integrator & Module Assembly Supply Chain

- OEM First-Fit Procurement, Homologation & Quality Approval Channel

- Aftermarket Distributor, Upholstery Supplier & Recycling and End-of-Life Recovery Channel

- Pricing Analysis

- Leather vs. PU Synthetic vs. Vegan Bio-Based Leather: Cost per Square Metre & Total Seating System Cost

- Thermoplastic Interior Trim Pricing: Commodity PP vs. Engineered ABS & PC/ABS Blend Cost Analysis

- Natural Fibre Composite vs. Glass Fibre Reinforced Panel: Weight, Cost & Performance Trade-Off Analysis

- Acoustic & Thermal Insulation Material Pricing: Lightweight vs. Standard Solution Cost Comparison

- Smart & Functional Material Premium Pricing: Conductive Textile, Electrochromic Film & Sensor Substrate Cost

- Total Interior Material Cost per Vehicle Analysis: Economy vs. Premium vs. EV Platform Comparison

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Automotive Interior Materials: Carbon Footprint, Energy Use & Water Consumption by Material Type

- Bio-Based, Recycled-Content & Vegan Material Adoption: OEM Sustainability Commitments & Consumer Demand Drivers

- VOC Emission Reduction, Healthy Interior Air Quality & Occupant Wellbeing Contribution of Low-Emission Materials

- End-of-Life Vehicle (ELV) Recyclability: Material Recovery Rates, Closed-Loop Recycling & Circular Economy Design

- REACH, RoHS & Restricted Substance Phase-Out: Transition to Safer, Non-Hazardous Interior Material Formulations

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Material Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Material Type, Application & Geography

- Player Classification

- Diversified Tier 1 Automotive Interior Systems Integrators

- Specialty Leather, PU Synthetic & Vegan Leather Material Suppliers

- Thermoplastic Polymer & Engineered Resin Producers for Automotive Interiors

- Polyurethane Foam & Acoustic Material Manufacturers

- Automotive Textile, Woven Fabric & Non-Woven Material Specialists

- Natural Fibre Composite & Bio-Based Material Developers

- Adhesive, Coating & Surface Treatment Specialists for Automotive Interiors

- Smart Material, Functional Textile & Embedded Electronics Material Start-ups

- Competitive Analysis Frameworks

- Market Share Analysis by Material Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Automotive Interior Materials Products & Portfolio

- Key Customer Relationships & OEM Supply Programmes

- Manufacturing Footprint & Production Capacity

- Revenue (Automotive Interior Materials Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Material Approvals, Capacity Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Sustainability Credentials vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Material Type, Technology, Application, Vehicle Type & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output