Market Definition

The Europe e-Forecourts Market encompasses the development, ownership, operation, and commercial management of dedicated electric vehicle charging hubs that are purpose-built or comprehensively retrofitted to replicate the convenience, throughput capacity, and multi-service retail experience of conventional petrol forecourts within a fully electrified refuelling infrastructure context, serving battery electric vehicle and plug-in hybrid electric vehicle drivers requiring high-power public charging across motorway corridors, urban arterial routes, retail and leisure destination catchments, and logistics and fleet operator depot environments across European markets. An e-forecourt is distinguished from conventional public charging installations by its integration of multiple simultaneous high-power charging bays, typically deploying direct current fast charging infrastructure operating at output capacities of 150 kilowatts to 400 kilowatts per charger and capable of accommodating six or more vehicles concurrently, within a purpose-designed site that combines charging infrastructure with complementary amenity and retail services including convenience retail, food and beverage, restrooms, Wi-Fi connectivity, and vehicle services that generate ancillary revenue streams and extend customer dwell time beyond the duration of the charging session itself. The market encompasses the full value chain of e-forecourt development and operation including site identification and land acquisition, grid connection and electrical infrastructure engineering, charging equipment procurement and installation, canopy and forecourt civil construction, retail and amenity fit-out, digital payment and energy management platform deployment, ongoing operations and maintenance, and the multi-party commercial structures linking charging network operators, energy retailers, site developers, fuel retail incumbents transitioning their forecourt estates, and independent e-forecourt specialist developers who are collectively defining the emerging commercial architecture of electrified public refuelling infrastructure across Europe. Key participants include dedicated e-forecourt developers and operators, incumbent fuel retail networks transitioning existing forecourt sites, charging equipment manufacturers, energy utilities and renewable power suppliers, retail and food service brands seeking forecourt concession opportunities, and national and European regulatory bodies whose alternative fuels infrastructure regulation frameworks govern minimum charging infrastructure deployment obligations across member state road networks.

Market Insights

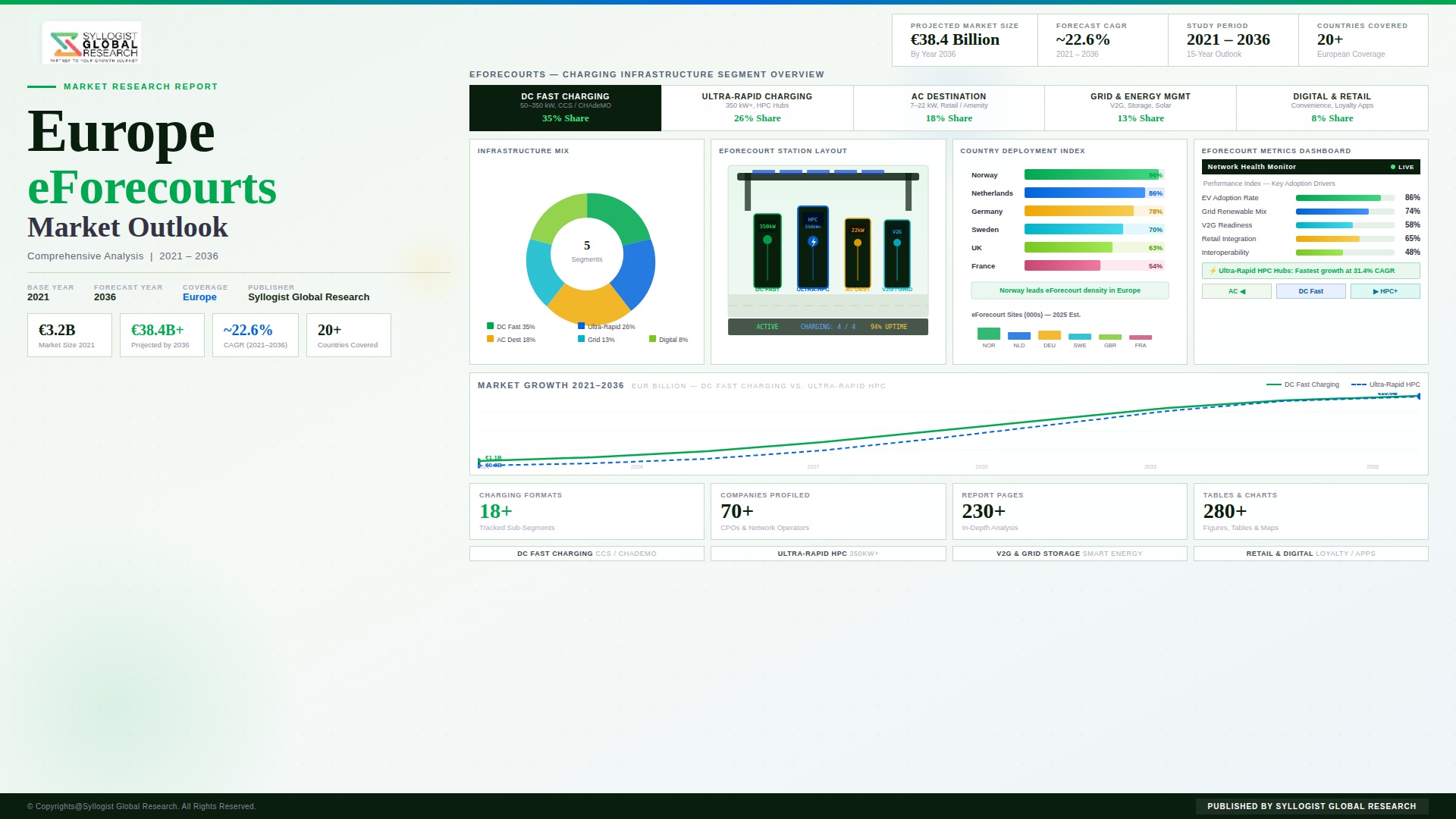

The Europe e-forecourts market is emerging as a structurally distinct and commercially critical segment of the broader European electric vehicle charging infrastructure landscape, defined by its ambition to resolve the two most persistent barriers to mainstream battery electric vehicle adoption across European consumer and fleet operator segments, namely charging speed anxiety arising from the limited power output of legacy public charging installations that require hours rather than minutes to meaningfully restore vehicle range, and the inferior site experience of early-generation charging deployments that offered isolated charging posts in car parks or motorway service areas without the amenity, convenience retail, and predictable service quality standards that petrol forecourt customers have been conditioned to expect over decades of conventional refuelling. The Europe e-forecourts market was valued at approximately USD 1.4 billion in 2025 and is projected to reach USD 9.8 billion by 2034, advancing at a compound annual growth rate of 24.1% over the forecast period from 2027 to 2034, driven by the accelerating battery electric vehicle fleet expansion across European markets, the European Union Alternative Fuels Infrastructure Regulation mandatory charging infrastructure deployment obligations along TEN-T core and comprehensive network corridors, and the growing commercial validation of the multi-service e-forecourt business model by first-mover operators whose operational sites are demonstrating revenue generation per square metre competitive with conventional petrol forecourt economics.

The commercial architecture of the e-forecourt model is proving substantially more complex and capital-intensive than conventional public charging deployment, as the combination of high-power multi-bay charging infrastructure, grid connection upgrades capable of sustaining simultaneous megawatt-scale power draw across multiple active charging bays, on-site battery energy storage systems mitigating peak demand grid charges and providing resilience against grid supply interruptions, solar photovoltaic canopy installations generating partial on-site renewable electricity supply, and the full retail amenity fit-out required to justify consumer dwell time and generate ancillary non-charging revenue streams creates a total site development capital requirement of approximately USD 3.2 million to USD 8.5 million per e-forecourt location depending on charging bay count, grid connection cost, land value, and retail amenity specification, a capital commitment that demands rigorous site selection, traffic volume validation, and commercial partnership structuring that distinguishes e-forecourt development from simpler public charging deployment programmes. The revenue model of a mature e-forecourt operation combines charging session revenue, whose profitability is determined by the spread between wholesale electricity procurement cost and retail charging tariff per kilowatt-hour at the utilisation rate achieved across the charging bay array, with retail concession income from food and beverage and convenience operators, advertising and media revenue from digital forecourt signage, fleet subscription and corporate account charging revenue from commercial vehicle operators, and in some advanced operational models, grid services revenue from vehicle-to-grid and battery storage arbitrage programmes that monetise the forecourt energy infrastructure asset base beyond its primary EV charging function.

The competitive landscape of the European e-forecourts market is characterised by a convergence of participant categories from previously distinct industry sectors, as incumbent fuel retail networks including BP, Shell, TotalEnergies, and Esso are repurposing and upgrading existing high-traffic forecourt estates with multi-bay high-power charging infrastructure to defend their refuelling destination relevance and customer relationship continuity into the electric vehicle era, while dedicated EV charging network operators including Ionity, Osprey, Gridserve, Fastned, and Allego are developing purpose-built e-forecourt sites from greenfield positions on motorway junctions, retail park peripheries, and transport interchange locations where their site selection capabilities and charging-first operational expertise provide competitive differentiation relative to fuel retail incumbents whose estate transition programmes are constrained by existing site layouts, lease structures, and grid connection limitations that predate the power infrastructure requirements of high-power multi-bay charging operations. The United Kingdom has emerged as the most commercially advanced European e-forecourt market, with Gridserve’s Electric Forecourt network and BP Pulse’s high-power hub programme establishing operational benchmarks for multi-service e-forecourt design, customer experience standards, and commercial performance metrics that are informing e-forecourt development strategies across Continental European markets where equivalent dedicated hub programmes are at earlier stages of commercial deployment but are accelerating rapidly as battery electric vehicle fleet penetration crosses the threshold levels that validate high-power hub site utilisation economics.

From a country-level perspective, the United Kingdom, Germany, the Netherlands, Norway, and France collectively account for approximately 68.4% of total European e-forecourt market revenue in 2025, reflecting the concentration of advanced battery electric vehicle fleet penetration, mature public charging infrastructure investment ecosystems, and enabling policy environments in these five markets that have created the demand density and commercial confidence required for first-generation e-forecourt network investment at scale. Norway, despite its smaller total vehicle market, represents the most structurally mature e-forecourt market in Europe in per-capita terms, with battery electric vehicle new vehicle market share exceeding 88% in 2025 generating a total BEV fleet of approximately 780,000 vehicles whose charging infrastructure requirements have driven e-forecourt development along national route corridors and in urban centres to a density that provides a preview of the infrastructure deployment patterns that larger Continental European markets will replicate as their own BEV fleet penetration rates converge toward Norwegian benchmarks over the forecast period. Germany, as Europe’s largest vehicle market with approximately 3.2 million battery electric vehicles in service by end-2025, represents the largest single-country revenue opportunity for e-forecourt development and is experiencing accelerating private investment in high-power charging hub infrastructure following the German government’s publicly funded high-power charging network tender programme, which established minimum charging hub specifications and density requirements along federal motorway corridors that are directly informing commercial e-forecourt site development decisions by private operators deploying capital alongside and beyond the publicly tendered network.

Key Drivers

European Union Alternative Fuels Infrastructure Regulation Mandating High-Power Charging Hub Deployment Along TEN-T Corridors and Creating Regulatory-Backed Investment Demand Across Member States

The European Union Alternative Fuels Infrastructure Regulation, which entered into force in 2023 and replaces the previous Alternative Fuels Infrastructure Directive with directly applicable binding member state obligations, establishes mandatory minimum charging infrastructure deployment requirements along the Trans-European Transport Network core and comprehensive road corridors that create a time-bound and legally enforceable demand signal for high-power charging hub development precisely on the motorway and primary arterial route catchments where e-forecourt sites generate the traffic volumes and dwell time characteristics required for commercially viable hub operation. The regulation requires member states to deploy at minimum one charging pool with a combined output of at least 600 kilowatts including at least one 150-kilowatt individual charger every 60 kilometres along TEN-T core network motorways by the end of 2025, scaling to 1,400-kilowatt combined capacity pools every 60 kilometres by 2030, obligations whose technical specifications and power output requirements align precisely with the multi-bay high-power charging hub format that defines the e-forecourt infrastructure model. The regulatory deployment timeline is generating a committed investment pipeline in high-power charging hub infrastructure across all 27 European Union member states simultaneously, supplemented by national government co-funding programmes in Germany, France, Italy, Spain, and the Netherlands that are providing capital grants and grid connection subsidies reducing e-forecourt development economics risk during the early utilisation ramp period when charging session revenue alone cannot fully cover site capital and operating cost recovery, creating a hybrid public-private investment environment that is accelerating commercial e-forecourt network development beyond the pace achievable through purely market-driven investment.

Rapidly Expanding Battery Electric Vehicle Fleet Across Europe Generating Sustainable High-Power Public Charging Demand Density That Validates E-Forecourt Site Economics

The sustained acceleration of battery electric vehicle new vehicle sales across European markets is expanding the addressable charging demand base for e-forecourt operators at a pace that is progressively validating hub site utilisation economics across an expanding geography of viable site locations, as each successive year of BEV fleet growth adds vehicles to the pool of potential charging customers within each e-forecourt catchment area and incrementally increases the average daily charging session throughput achievable at established hub sites. Battery electric vehicle new vehicle registrations in Europe reached approximately 2.4 million units in 2025 across the EU-27 and United Kingdom combined, bringing the total European BEV fleet to approximately 9.8 million vehicles, and are projected to grow to over 6.1 million annual registrations by 2030 as the 2035 internal combustion engine new vehicle sale prohibition deadline creates an accelerating fleet electrification trajectory across all major European markets that continuously expands the structural demand base for high-power public charging infrastructure. E-forecourt operators in established markets report that hub sites in high-traffic motorway and urban arterial locations achieving BEV fleet catchment densities above 15,000 electric vehicles within a 20-kilometre radius are generating charging bay utilisation rates above 28% on an annualised basis, a utilisation threshold that operators characterise as approaching breakeven on charging revenue alone before ancillary retail and fleet account revenues are incorporated, validating the core commercial thesis of the e-forecourt model in markets where BEV fleet density has reached the critical mass required to sustain hub site economics.

Fuel Retail Incumbent Network Transformation Programmes Deploying Capital at Scale to Convert High-Traffic Forecourt Estates Into Multi-Service E-Forecourt Hubs

The strategic transformation programmes of major European fuel retail networks represent the largest single source of committed capital deployment into the e-forecourt market, as BP, Shell, TotalEnergies, Esso, and national fuel retail operators across Germany, France, the Netherlands, and Scandinavia are allocating multi-billion-dollar capital expenditure programmes to the conversion and upgrade of their highest-traffic forecourt locations into multi-service electric vehicle charging hubs that leverage existing site assets, grid connections, retail infrastructure, and customer relationships to accelerate e-forecourt network deployment at a pace and geographic density that pure-play e-forecourt developers building from greenfield positions cannot match within equivalent timeframes or capital envelopes. BP has committed USD 1 billion to its BP Pulse EV charging network expansion through 2030, with a significant proportion allocated to high-power hub development at premium BP forecourt locations across the United Kingdom and Continental Europe; Shell Recharge is developing high-power charging hubs across its European forecourt network targeting 50,000 public charge points by 2025; and TotalEnergies is deploying high-power charging infrastructure across its network of over 16,000 European service stations through its TotalEnergies Charge network programme. The competitive urgency driving fuel retail incumbent e-forecourt investment is amplified by the recognition that forecourt sites generating the highest fuel volume revenues today are precisely the high-traffic motorway and arterial route locations that will generate the highest EV charging session volumes as fleet electrification advances, creating a strategic asset defence rationale for e-forecourt conversion investment that extends beyond near-term revenue optimisation to long-term site relevance preservation.

Key Challenges

Grid Connection Constraints and Long Lead Times for High-Power Electrical Infrastructure Upgrades Limiting E-Forecourt Deployment Velocity Across Priority Locations

The most operationally constraining and commercially damaging challenge confronting e-forecourt developers across European markets is the severe mismatch between the electrical grid connection capacity required to power multi-bay high-power charging hubs, whose simultaneous peak demand can exceed one to three megawatts at sites with six to twelve 150-kilowatt to 350-kilowatt chargers operating concurrently, and the available grid infrastructure at the prime high-traffic roadside and forecourt locations where e-forecourt site economics are most viable, with grid reinforcement and new connection projects at the required power levels carrying lead times of 18 to 48 months from application submission to energisation in the United Kingdom, Germany, France, and the Netherlands due to the combination of distribution network operator engineering resource constraints, civil works required for cable trenching and substation installation, and regulatory approval processes that have not been streamlined to reflect the urgency of electric vehicle infrastructure deployment. A 2024 survey of e-forecourt developers operating across European markets identified grid connection delays as the primary cause of project timeline extension in over 60% of sites under development, with an average delay of 14 months between planning permission approval and site energisation attributable to grid connection processes alone, translating directly into deferred revenue generation, extended capital carrying cost periods, and in some cases site abandonment when landowner lease timelines cannot accommodate the full development period including grid connection delay. On-site battery energy storage system deployment is being deployed by leading e-forecourt operators as a partial mitigation strategy for grid connection power limitations, enabling sites to operate charging infrastructure at peak capacity from stored energy during high-demand periods while drawing from the grid at a lower contracted connection capacity during off-peak periods, but storage system capital costs of USD 350,000 to USD 900,000 per installation add materially to total site development investment requirements.

E-Forecourt Site Utilisation Rate Dependency on BEV Fleet Density Creating a Financially Vulnerable Early Deployment Phase Before Catchment EV Populations Reach Commercial Viability Thresholds

The commercial viability of individual e-forecourt sites is critically dependent on achieving minimum charging bay utilisation rates that generate sufficient charging session revenue to cover the combined capital depreciation, grid connection standing charges, electricity procurement costs, operations and maintenance expenditure, and retail site operating costs that constitute the full cost base of a multi-service e-forecourt hub, yet the utilisation rates achievable at newly opened e-forecourt sites are structurally constrained by the BEV fleet density within the site catchment area at the time of opening, which in many European markets outside Norway, the Netherlands, and the United Kingdom remains below the threshold required to generate commercially adequate charging throughput without extended loss-making ramp periods requiring sustained investor capital support. Financial modelling by e-forecourt developers consistently identifies a minimum catchment BEV fleet density of approximately 12,000 to 18,000 battery electric vehicles within a 20-kilometre radius as the viability threshold for achieving charging revenue breakeven at a standard six-bay 150-kilowatt to 350-kilowatt e-forecourt hub operating at market-average retail tariff rates, a density that as of 2025 is achieved only within the higher-penetration urban and suburban catchments of the United Kingdom, Norway, the Netherlands, and parts of Germany and Sweden, leaving the majority of European geographies requiring two to five additional years of BEV fleet growth before e-forecourt sites can approach commercial self-sufficiency on charging revenue alone. Public co-funding mechanisms including EU Innovation Fund grants, national government charging infrastructure subsidy programmes, and AFIR-linked public procurement frameworks are providing essential bridge funding during this early utilisation ramp period, but subsidy dependency creates programme execution risk if political commitment to EV infrastructure funding wavers.

Electricity Procurement Cost Volatility and Retail Tariff Compression Threatening E-Forecourt Charging Revenue Margin Across the Operating Portfolio

E-forecourt operators are structurally exposed to wholesale electricity price volatility that directly compresses the gross margin earned on charging session revenue, as the spread between the wholesale electricity procurement cost and the retail tariff per kilowatt-hour charged to EV drivers constitutes the primary revenue contribution from which all site operating costs must be recovered, and this spread is simultaneously squeezed from below by electricity price spikes driven by European energy market volatility and from above by competitive tariff pressure as the density of high-power public charging infrastructure in premium locations increases and price-sensitive EV drivers exhibit measurable tariff elasticity in their charging destination selection behaviour. European wholesale electricity prices experienced extreme volatility between 2021 and 2024, with day-ahead prices in Germany, France, and the United Kingdom at various points exceeding USD 500 per megawatt-hour compared to long-run average levels below USD 80 per megawatt-hour, creating periods in which e-forecourts procuring electricity on short-term or spot market terms generated negative gross margins on charging sessions at regulated or competitively benchmarked retail tariff levels. E-forecourt operators are responding to electricity procurement risk through long-term power purchase agreements with renewable energy generators that provide 10 to 15 year fixed price electricity supply frameworks insulating charging margin from spot market volatility, through on-site solar photovoltaic generation reducing grid electricity procurement requirements by 8% to 18% depending on site canopy area and geographic location, and through battery energy storage arbitrage programmes that shift electricity procurement toward lower-price off-peak periods, but each mitigation approach requires upfront capital investment or contractual commitment that adds complexity and counterparty risk to e-forecourt project finance structures.

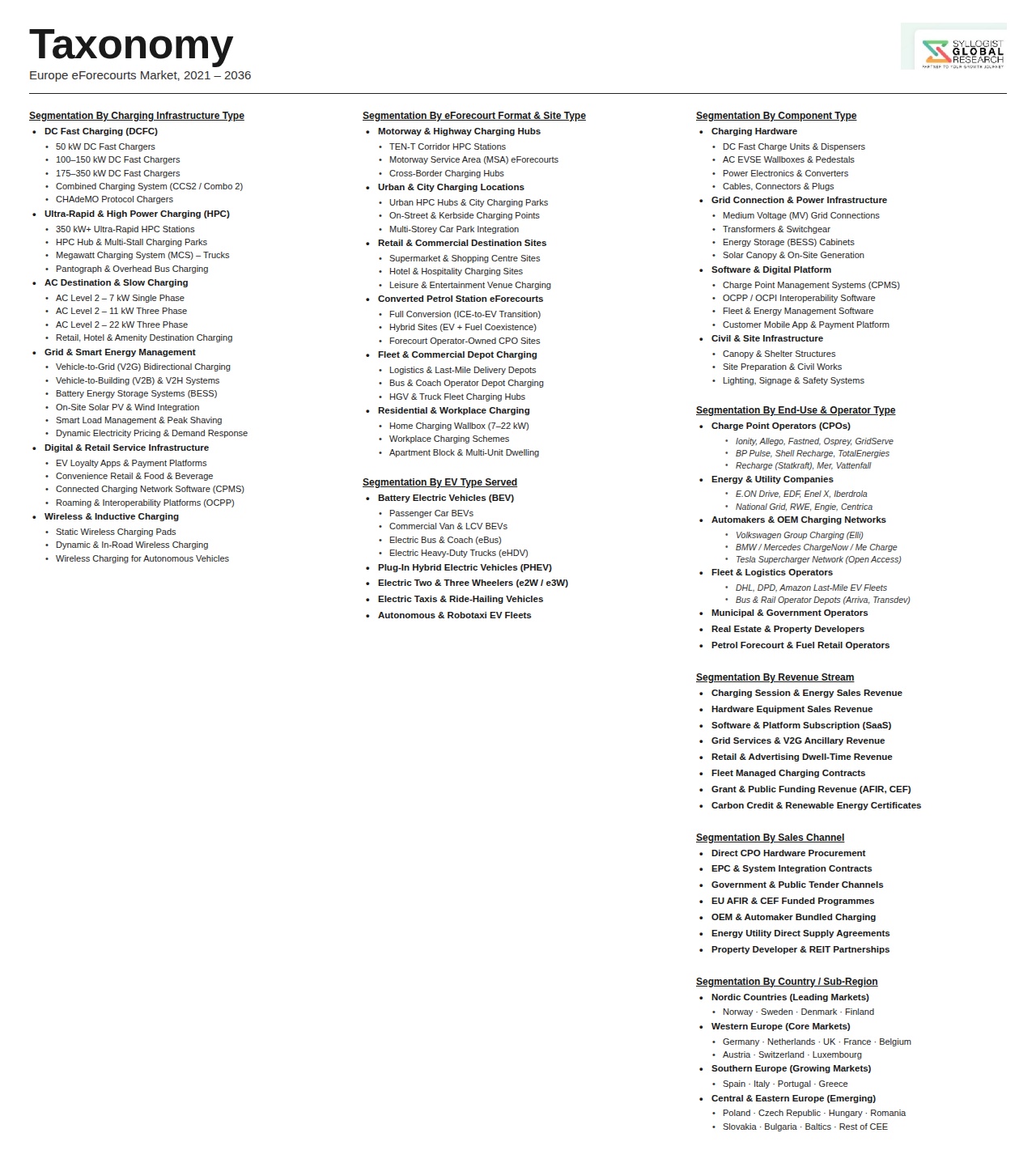

Market Segmentation

- Segmentation By Charging Power Level

- High-Power DC Fast Charging (150 kW to 249 kW)

- Ultra-High-Power DC Fast Charging (250 kW to 349 kW)

- Megawatt-Class DC Fast Charging (350 kW and Above)

- Mixed-Power Hub (Combination of AC and DC Charging Levels)

- Others

- Segmentation By Site Type

- Motorway and Highway Corridor E-Forecourt Hubs

- Urban and Suburban Arterial Route E-Forecourts

- Retail Park and Leisure Destination E-Forecourts

- Converted Incumbent Fuel Retail Forecourt Sites

- Purpose-Built Greenfield E-Forecourt Developments

- Transport Interchange and Park-and-Ride E-Forecourts

- Others

- Segmentation By Number of Charging Bays

- Small Hub Format (2 to 5 Simultaneous Charging Bays)

- Medium Hub Format (6 to 12 Simultaneous Charging Bays)

- Large Hub Format (13 to 24 Simultaneous Charging Bays)

- Mega Hub Format (25 and Above Simultaneous Charging Bays)

- Others

- Segmentation By Operator Type

- Dedicated E-Forecourt Specialist Developers and Operators

- Incumbent Fuel Retail Network Operators

- National and Pan-European EV Charging Network Operators

- Energy Utility and Power Company-Operated Hubs

- Retail and Motorway Service Area Operators

- Public Sector and Municipally Operated Charging Hubs

- Others

- Segmentation By Energy Source

- Grid-Supplied Renewable Energy Certificated Power

- On-Site Solar Photovoltaic Generation With Grid Backup

- Battery Energy Storage System Integrated Supply

- Combined Solar, Storage, and Grid Hybrid Supply

- Wind Power Purchase Agreement Backed Supply

- Others

- Segmentation By Ancillary Service Offering

- Convenience Retail and Food and Beverage

- Quick Service Restaurant and Coffee Concessions

- Vehicle Wash and Valeting Services

- Restroom and Traveller Amenity Facilities

- Wi-Fi Connectivity and Digital Lounge Amenities

- Fleet Management and Commercial Vehicle Services

- Advertising and Digital Out-of-Home Media

- Others

- Segmentation By Revenue Model

- Pay-As-You-Go Per-kWh Retail Tariff Charging

- Fleet and Corporate Subscription Account Charging

- Roaming Network Partner Charging Session Revenue

- Retail Concession and Tenancy Income

- Grid Services and Vehicle-to-Grid Revenue

- Battery Storage Energy Arbitrage Revenue

- Advertising and Sponsorship Revenue

- Others

- Segmentation By Vehicle Type Served

- Passenger Battery Electric Vehicles

- Plug-In Hybrid Electric Vehicles

- Light Commercial Electric Vans and Delivery Vehicles

- Medium and Heavy Electric Commercial Trucks

- Electric Buses and Coaches

- Others

- Segmentation By Country

- United Kingdom

- Germany

- France

- Netherlands

- Norway

- Sweden

- Belgium

- Denmark

- Austria

- Spain

- Italy

- Poland

- Rest of Europe

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total Europe e-forecourts market valuation in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by charging power level across high-power DC fast, ultra-high-power DC fast, and megawatt-class charging categories, by site type across motorway corridor hubs, urban arterial e-forecourts, retail destination sites, and converted incumbent fuel forecourts, and by country across the United Kingdom, Germany, France, Netherlands, Norway, Sweden, and the rest of Europe, to enable e-forecourt developers, charging network operators, fuel retail incumbents, energy utilities, infrastructure investors, and equipment manufacturers to identify which site formats, power configurations, and national markets will generate the highest absolute revenue growth and the most commercially validated hub economics across the forecast period as European BEV fleet penetration accelerates toward critical mass charging demand density thresholds?

- How are the binding mandatory charging infrastructure deployment obligations of the European Union Alternative Fuels Infrastructure Regulation, specifically the TEN-T core network 600-kilowatt charging pool requirements by 2025 and 1,400-kilowatt requirements by 2030 at maximum 60-kilometre intervals, translating into confirmed e-forecourt development pipeline volumes by corridor, country, and operator type across European markets, and what is the projected split of AFIR-driven infrastructure deployment between publicly tendered and co-funded charging hub programmes and commercially self-funded e-forecourt investment by private operators, at what site capital cost and charging bay count configurations, and across what deployment timeline that would enable infrastructure investors and equipment suppliers to calibrate their capital allocation and supply capacity planning to the regulatory-mandated e-forecourt development pipeline through the forecast period?

- What are the detailed unit economics of a commercially representative European e-forecourt hub at 2025 operational benchmarks and projected 2030 maturity benchmarks, including site capital development cost per charging bay by site type and power level, average charging bay utilisation rate by market and site location category, charging session revenue per kilowatt-hour delivered at market-average retail tariff levels, ancillary retail and fleet account revenue contribution as a percentage of total site revenue, operating cost structure including electricity procurement, operations and maintenance, grid standing charges, and retail concession cost, and the minimum BEV fleet catchment density within a defined radius required to achieve site-level charging revenue breakeven for each hub format category, providing a rigorous commercial viability framework for e-forecourt investment decision-making across different European market and site contexts?

- How are grid connection capacity constraints, distribution network operator resource limitations, and the 18 to 48 month lead times for high-power electrical infrastructure upgrades affecting e-forecourt development pipeline execution rates and site opening timelines across the United Kingdom, Germany, France, Netherlands, and other key European markets, and what are the technical, regulatory, and commercial mitigation strategies being deployed by leading e-forecourt operators including on-site battery energy storage integration, solar photovoltaic generation, flexible grid connection tariffs, and distribution network operator collaboration programmes that are reducing grid dependency and improving site development timeline predictability, and at what capital cost per site and what reduction in effective grid connection capacity requirement are these mitigation technologies achieving at operational e-forecourt deployments providing reference data for wider industry adoption?

- Who are the leading e-forecourt developers, dedicated EV charging hub operators, incumbent fuel retail network operators deploying high-power charging hub programmes, energy utility-backed charging infrastructure investors, and charging equipment manufacturers currently defining the competitive landscape of the European e-forecourts market, and what are their respective site portfolio sizes and development pipeline commitments by country and site format, capital investment programmes and funding structures across equity, project finance, and public co-funding mechanisms, charging equipment supplier relationships and technology platform selections, retail and food service concession partnership models generating ancillary site revenue, energy procurement and on-site generation strategies managing electricity cost and renewable supply credentialing, and strategic positioning relative to the AFIR compliance deployment obligations and commercial BEV fleet growth trajectory that together define the market development pace and competitive opportunity across European e-forecourt markets through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Country Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Grid Capacity, Power Infrastructure Upgrade Cost & Electricity Network Constraint Risk

- EV Adoption Rate Uncertainty, Charging Demand Forecasting & Utilisation Risk

- Cybersecurity, Payment System Fraud & Connected Charging Infrastructure Vulnerability Risk

- Real Estate Availability, Planning Permission, Land Cost & Site Development Risk

- Technology Obsolescence, Charging Standard Fragmentation & Stranded Asset Risk

- Regulatory Framework & Standards

- EU Alternative Fuels Infrastructure Regulation (AFIR): Mandatory Charging Deployment Targets & Highway Corridor Requirements

- EU Fit for 55, European Green Deal & National Energy and Climate Plans (NECPs) Driving e-Forecourt Investment

- OCPP, OCPI, ISO 15118 & EU Data Act: Interoperability, Roaming & Open Data Obligations for Charging Operators

- EU Building Energy Performance Directive (EPBD): EV-Ready Infrastructure Requirements for New & Renovated Buildings

- Electricity Retail Regulation, Smart Charging Directives, Demand Response & Consumer Pricing Transparency Frameworks

- Europe e-Forecourts Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Sites, Charging Points & Sessions)

- Market Size & Forecast by Infrastructure Component

- DC Fast Charging Equipment: 50 kW to 150 kW Rapid Chargers & Associated Switchgear

- Ultra-Rapid & High-Power Charging (HPC) Equipment: 150 kW to 350 kW+ Dispensers

- AC Destination Charging Infrastructure: 7 kW to 22 kW Chargers for Dwell-Time Locations

- Grid Connection & Electrical Infrastructure: Transformers, Switchboards & Cable Ducting

- Battery Energy Storage Systems (BESS) for Peak Shaving, Grid Stability & Demand Management

- On-Site Renewable Energy Generation: Solar PV Canopies, Wind Integration & Microgrid Systems

- Digital Infrastructure: Payment Terminals, CPMS Software, Network Connectivity & Back-Office Platform

- Canopy, Forecourt Civil Works, Lighting, Signage & Customer Amenity Infrastructure

- Market Size & Forecast by Technology

- Combined Charging System (CCS2) DC Fast & Ultra-Rapid Charging Technology

- AC Type 2 (Mennekes) Destination Charging Technology

- Tesla NACS & Supercharger Network Technology

- CHAdeMO Protocol Charging Technology

- ISO 15118 Plug & Charge (PnC) & Vehicle-to-Grid (V2G) Bidirectional Charging Technology

- Dynamic Load Management, Smart Charging & Demand Response Technology

- Battery Energy Storage Integration & On-Site Renewable Energy Coupling Technology

- AI-Enabled Site Optimisation, Predictive Maintenance & Customer Analytics Technology

- Market Size & Forecast by Charging Speed

- Rapid Charging (50 kW to 149 kW)

- Ultra-Rapid Charging (150 kW to 349 kW)

- High-Power Charging (350 kW and Above)

- Destination & AC Charging (Up to 22 kW)

- Market Size & Forecast by Site Format

- Purpose-Built Standalone e-Forecourt: Large-Format EV-Only Charging Hub

- Converted Petrol Forecourt: Legacy Fuel Retail Site Retrofitted with EV Charging Infrastructure

- Motorway Service Area & TEN-T Corridor Charging Hub

- Retail, Supermarket & Shopping Centre Integrated Charging Forecourt

- Hotel, Hospitality & Leisure Venue Integrated Charging Forecourt

- Fleet Depot, Logistics Hub & Commercial Vehicle Charging Forecourt

- Urban & City Centre Fast Charging Hub

- Market Size & Forecast by Application

- Passenger Car Public Charging

- Light Commercial Vehicle (LCV) & Last-Mile Delivery Fleet Charging

- Heavy Commercial Vehicle (HCV), Bus & Coach High-Power Charging

- Ride-Hailing, Taxi Fleet & Shared Mobility Operator Charging

- Hydrogen Fuel Cell Vehicle (FCEV) Dispensing at Integrated e-Forecourt Sites

- Market Size & Forecast by End-User

- Private EV Drivers & Consumer Retail Charging Customers

- Fleet Operators & Corporate Mobility Managers

- Fuel Retail & Forecourt Operators

- Motorway Service Area & TEN-T Corridor Operators

- Real Estate Developers, Retail Parks & Hospitality Groups

- Municipalities, Local Authorities & Public Infrastructure Bodies

- Market Size & Forecast by Revenue Model

- Pay-As-You-Go: Per kWh, Per Minute & Per Session Pricing

- Subscription & Membership Model: Monthly & Annual Roaming Pass

- White-Label & Franchise Network Licensing Model

- Ancillary Revenue: Retail, Food & Beverage, Advertising & Loyalty Programme

- Vehicle-to-Grid (V2G) & Grid Services Revenue: Frequency Response & Demand Turn-Down

- Market Size & Forecast by Country

- Germany

- France

- United Kingdom

- Netherlands

- Norway

- Sweden

- Spain

- Italy

- Rest of Europe

- Germany e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- France e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- United Kingdom e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Netherlands e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Norway e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Sweden e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Spain e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Italy e-Forecourts Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Sites, Charging Points & Sessions)

- By Infrastructure Component

- By Technology

- By Charging Speed

- By Site Format

- By Application

- By End-User

- By Revenue Model

- By Region

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- Ultra-Rapid & High-Power Charging (HPC) Hardware: 350 kW+ Dispenser & Liquid-Cooled Cable Technology Deep-Dive

- ISO 15118 Plug & Charge, CCS2 Adoption & Vehicle-to-Grid (V2G) Bidirectional Energy Flow Technology

- On-Site Battery Energy Storage (BESS) Integration: Peak Shaving, Grid Arbitrage & Backup Power Technology

- Solar PV Canopy, On-Site Renewable Generation & Microgrid Control Technology for e-Forecourts

- Dynamic Load Management, Smart Charging Optimisation & Demand Response Technology

- AI-Enabled Site Operations: Predictive Maintenance, Utilisation Forecasting & Customer Experience Personalisation

- Payment, Roaming & CPMS Platform Technology: OCPP 2.0.1, OCPI & Open Standards Back-Office Integration

- Patent & IP Landscape in e-Forecourt & EV Charging Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Charging Equipment OEM & Power Electronics Component Supply Chain

- Battery Energy Storage System & On-Site Renewable Energy Equipment Supply Chain

- Grid Connection, Transformer, Switchgear & Electrical Balance-of-Plant Supply Chain

- Civil Engineering, Canopy Construction & Forecourt Fitout Supply Chain

- CPMS Software, Payment Platform & Network Connectivity Supply Chain

- CPO, Site Developer, Fuel Retailer & Real Estate Partner Channel

- Operations, Maintenance, Remote Monitoring & Asset Management Service Channel

- Pricing Analysis

- DC Fast & Ultra-Rapid Charger Hardware Unit Cost & Total Site Capital Expenditure Analysis

- Grid Connection Upgrade & Electrical Infrastructure Cost Analysis by Site Scale

- BESS & On-Site Solar PV Integration Capital Cost & Payback Period Analysis

- Per kWh, Per Minute & Session-Based Consumer Pricing Benchmarking Across Key European Markets

- CPO Revenue, Operating Cost & Site-Level EBITDA Economics Analysis

- Total e-Forecourt Development Economics: CapEx, OpEx, Revenue & Return on Investment Modelling

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of e-Forecourt Infrastructure: Embodied Carbon, Operational Energy & End-of-Life

- Renewable Energy Sourcing, Green Tariff Procurement & Carbon-Neutral Charging Site Certification

- BESS Second-Life Battery Integration: Repurposed EV Battery Use & Environmental Benefit Assessment

- EV Charging vs. Petrol Forecourt: Well-to-Wheel Carbon Savings & Air Quality Improvement Contribution

- ESG Reporting, EU Taxonomy Alignment, Net Zero Commitments & Sustainable Site Design Standards for European e-Forecourt Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Site Format & Country)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Site Format, Charging Speed & Country

- Player Classification

- Pure-Play Charge Point Operators (CPOs) & e-Forecourt Network Developers

- Legacy Fuel Retail Groups Transitioning to e-Forecourt Operators

- Motorway Service Area & TEN-T Corridor Charging Network Operators

- Utility & Energy Company-Backed Charging Infrastructure Developers

- Charging Equipment OEMs with Network & CPO Capabilities

- Real Estate, Retail & Hospitality Groups Integrating e-Forecourt Infrastructure

- Technology & Software Platform Providers: CPMS, Roaming & Smart Charging Solutions

- Start-ups & New Entrants in High-Power Charging Hub Development

- Competitive Analysis Frameworks

- Market Share Analysis by Site Format, Technology & Country

- Company Profile

- Company Overview & Headquarters

- e-Forecourt Network Size, Site Portfolio & Charging Point Count

- Key Customer Relationships, Site Partnerships & Real Estate Network

- Geographic Footprint & Expansion Pipeline

- Revenue (e-Forecourt & Charging Segment) & Utilisation Rates

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Site Openings, Network Expansions, Technology Upgrades)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Network Scale vs. Charging Speed Capability)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Component, Site Format, Application, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Site Development & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output