Market Definition

The India Industrial Sensors Market encompasses the design, manufacturing, import, distribution, and integration of electronic sensing devices that detect, measure, and transmit physical, chemical, and environmental parameters including pressure, temperature, flow, level, position, proximity, vibration, humidity, gas concentration, force, torque, and optical properties within industrial process plants, manufacturing facilities, energy generation infrastructure, oil and gas installations, mining operations, water and wastewater treatment systems, transportation networks, and building automation environments across India’s rapidly industrializing economy. Industrial sensors convert measurable physical and chemical phenomena into standardized electrical or digital output signals that interface with programmable logic controllers, distributed control systems, supervisory control and data acquisition platforms, industrial IoT gateways, and edge computing infrastructure to enable automated process control, condition monitoring, quality assurance, safety system actuation, and energy management across the full spectrum of Indian industrial operations.

The market encompasses contact and non-contact temperature sensors including thermocouples, resistance temperature detectors, infrared pyrometers, and fiber optic temperature sensors; pressure sensors and transmitters covering gauge, absolute, and differential pressure measurement; flow meters and flow sensors including electromagnetic, vortex, ultrasonic, Coriolis, and differential pressure flow measurement technologies; level sensors including ultrasonic, radar, guided wave radar, capacitance, and pressure-based level measurement; proximity and position sensors including inductive, capacitive, photoelectric, and magnetic proximity switches alongside encoders, resolvers, and linear position transducers; vibration and condition monitoring sensors; gas detection and analysis sensors; and force, load, and torque sensing systems. The market further encompasses the smart sensor segment deploying onboard microprocessors, wireless communication capabilities, self-diagnostic functions, and digital communication protocols including HART, Foundation Fieldbus, PROFIBUS, IO-Link, and industrial Ethernet that enable sensor intelligence at the device edge. Key participants include global automation technology leaders operating Indian subsidiaries and distribution networks, domestic Indian sensor manufacturers addressing cost-sensitive industrial segments, system integrators deploying sensor-based automation solutions, engineering procurement and construction companies specifying sensors in industrial capital projects, and the diverse industrial end-user base spanning oil and gas, pharmaceuticals, chemicals, food and beverage, automotive, steel, cement, power, and water treatment sectors.

Market Insights

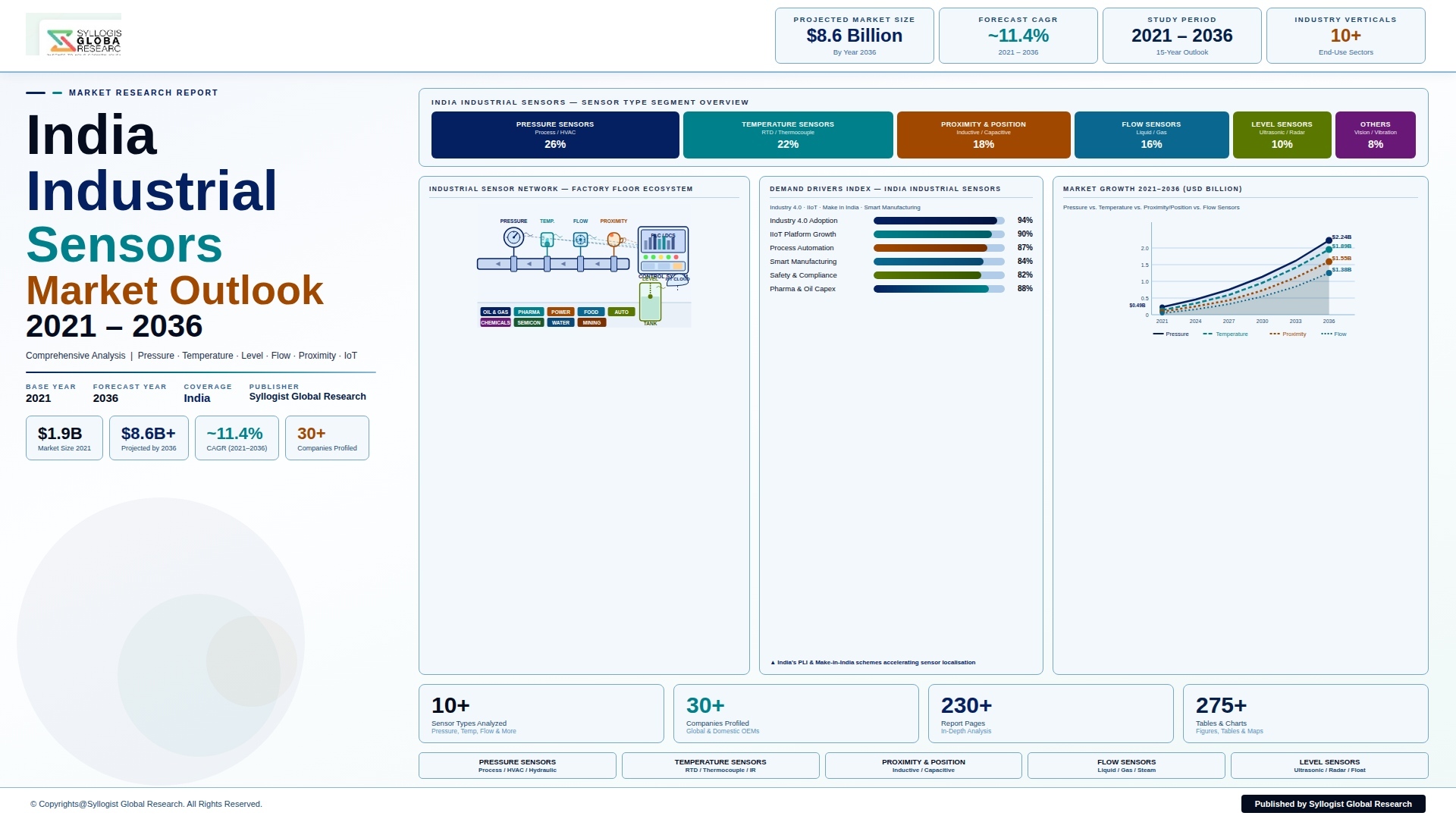

The India industrial sensors market is experiencing a structural demand acceleration driven by the simultaneous advancement of three transformative forces: the Indian government’s Make in India and PLI scheme initiatives compelling manufacturing capacity expansion across pharmaceuticals, electronics, chemicals, automotive, and food processing sectors that generate new industrial sensor installation requirements; the accelerating adoption of Industrial IoT and Industry 4.0 automation technologies by Indian manufacturers seeking to improve operational efficiency, product quality, and energy productivity in the face of global competitiveness pressure; and the progressive digitalization of India’s energy, water, and infrastructure sectors under National Infrastructure Pipeline programs that require extensive sensor-based monitoring and control systems. The India industrial sensors market was valued at approximately USD 1.9 billion in 2025 and is projected to reach USD 3.8 billion by 2034, advancing at a compound annual growth rate of 8.0% over the forecast period from 2027 to 2034, supported by the expanding greenfield and brownfield industrial capital expenditure programs across PLI scheme-supported manufacturing sectors, the growing retrofit automation investment of Indian manufacturers upgrading legacy plant control systems to digital and smart sensor architectures, and the substantial sensor procurement requirements of India’s oil and gas upstream and downstream expansion programs, renewable energy infrastructure buildout, and the water supply and sewage treatment infrastructure investments under Jal Jeevan Mission and AMRUT 2.0 schemes.

The process industry segment, encompassing oil and gas, petrochemicals, pharmaceuticals, specialty chemicals, fertilizers, and food and beverage processing, constitutes the largest and most technically sophisticated application category within the India industrial sensors market, accounting for approximately 42% of total market revenue in 2025 and characterized by the highest per-plant sensor investment density of any industrial segment due to the safety-critical, regulatory-compliance-driven, and process optimization requirements of continuous process manufacturing whose operational performance is fundamentally dependent on the accuracy, reliability, and diagnostic integrity of the measurement and control sensor infrastructure deployed throughout process plant instrumentation systems. India’s pharmaceutical sector, which has attracted over USD 33 billion in foreign direct investment and operates over 3,000 FDA-approved manufacturing facilities making it the world’s largest generic medicine producer by volume, represents one of the highest sensor specification environments in Indian industry due to the US FDA, European EMA, and WHO Good Manufacturing Practice regulatory requirements for validated measurement systems, electronic records of process parameters, and continuous in-process quality monitoring that mandate high-accuracy, calibration-traceable sensors with comprehensive audit trail documentation capabilities whose procurement and maintenance costs are justified by the regulatory market access value they protect. ONGC’s upstream oil field instrumentation modernization programs, the Petrochemicals Investment Promotion and Development Scheme driving new chemical complex development, and the continuous operational improvement programs of Reliance Industries, BPCL, HPCL, and IOC at their refinery and petrochemical assets collectively represent multi-hundred-crore rupee annual sensor procurement programs that anchor the commercial demand structure of India’s process industry sensor segment.

The manufacturing automation segment, encompassing automotive, electronics, machinery, metal fabrication, textiles, and general manufacturing facilities deploying discrete automation sensor technologies, is experiencing the most dynamic growth within the India industrial sensors market, driven by the PLI scheme’s success in attracting large-scale manufacturing investment in smartphones and electronics components, automotive components and EVs, specialty chemicals, and medical devices that has created a new wave of greenfield manufacturing facilities incorporating contemporary sensor-dense automation architectures from initial plant commissioning rather than requiring the gradual sensor retrofit programs that characterize older Indian manufacturing facilities whose automation was historically implemented incrementally against capital expenditure constraints. The automotive manufacturing sector’s transition toward electric vehicle production is creating materially different sensor requirement profiles compared to internal combustion engine vehicle manufacturing, with EV battery pack production requiring precision temperature sensors for cell formation cycling monitoring, electrochemical process parameter measurement, and thermal management system control; electric motor manufacturing demanding precision torque, vibration, and position sensing; and vehicle assembly line quality inspection generating demand for vision sensors, laser displacement sensors, and coordinate measuring machine integration that collectively represent a higher-value and technically more sophisticated sensor procurement profile than the conventional automotive assembly sensor market. The electronics manufacturing expansion centered on the Oragadam, Purana Qila, and Noida electronics clusters, anchored by Samsung, Apple supplier Foxconn’s Sriperumbudur operations, and the growing domestic electronics manufacturing ecosystem under the PLI for large-scale electronics manufacturing, is generating growing demand for precision vision sensors, force and torque sensors, and cleanroom-compatible environmental monitoring sensors whose technical specifications reflect the stringent quality control requirements of electronics manufacturing processes.

The energy and utilities segment, encompassing power generation, renewable energy infrastructure, water and wastewater treatment, and oil and gas pipeline and terminal operations, represents the most rapidly expanding sensor procurement category in India by investment value, driven by the National Infrastructure Pipeline’s USD 1.4 trillion infrastructure investment target that includes substantial allocations to power sector modernization, renewable energy capacity addition, and water infrastructure development whose instrumentation and sensor requirements are being specified and procured at a scale and pace that is creating large multi-year procurement programs for sensor suppliers and system integrators serving the energy and utilities vertical. India’s renewable energy capacity expansion program, targeting 500 gigawatts of non-fossil fuel power by 2030, is generating growing demand for condition monitoring sensors on wind turbine drivetrains and nacelle components, solar irradiance and temperature sensors for PV plant performance monitoring, vibration and temperature sensors for inverter and transformer health monitoring, and meteorological station sensors for wind and solar resource assessment that collectively represent a structurally new and rapidly growing sensor application category whose technical and commercial characteristics differ substantially from conventional power plant instrumentation. The smart grid and smart meter infrastructure investment under the Revamped Distribution Sector Scheme, which has committed INR 3,03,758 crore for distribution network upgradation and smart metering deployment, is creating demand for feeder automation sensors, fault detection equipment, power quality measurement devices, and environmental monitoring systems that collectively represent a large and multi-year sensor procurement opportunity for suppliers capable of meeting the technical and regulatory requirements of Indian power distribution infrastructure projects.

Key Drivers

Make in India and PLI Scheme Manufacturing Expansion Generating Large-Scale Greenfield Industrial Sensor Procurement Across Priority Sectors

The Indian government’s Production Linked Incentive scheme, which has committed over INR 1.97 lakh crore in manufacturing investment incentives across fourteen sectors and has successfully attracted committed investments exceeding INR 4 lakh crore in electronics, pharmaceuticals, automobiles, advanced chemistry cells, textiles, and specialty chemicals, is creating an unprecedented wave of new manufacturing facility construction whose instrumentation and automation sensor requirements represent a structurally new demand layer for the India industrial sensors market that is additive to the replacement and upgrade demand generated by India’s existing industrial plant base. Each greenfield pharmaceutical manufacturing facility constructed under PLI scheme incentives requires instrumentation investment of approximately USD 2 million to USD 8 million depending on facility scale and automation specification level, encompassing temperature, pressure, flow, and level sensors for process control, environmental monitoring sensors for cleanroom qualification, and analytical sensors for in-process quality control, while a new automotive assembly plant of 200,000 to 400,000 vehicles per year annual capacity requires automation sensor investment of approximately USD 15 million to USD 40 million across body shop, paint shop, general assembly, and quality inspection applications. The semiconductor and display manufacturing investment being attracted under the India Semiconductor Mission, whose incentive program has approved India’s first semiconductor fab investment of USD 8.9 billion by Tata Electronics in collaboration with Powerchip Semiconductor Manufacturing Corporation, will generate sensor procurement requirements of extraordinary technical sophistication and per-facility investment density, as semiconductor fabrication facilities require the most stringent process parameter control, contamination monitoring, and environmental measurement capabilities of any manufacturing application, representing a premium sensor market segment whose development will further elevate the average technical specification of India’s industrial sensor procurement as the semiconductor ecosystem develops through the forecast period.

Industrial IoT and Industry 4.0 Digital Transformation Driving Retrofit Smart Sensor Adoption Across India’s Existing Manufacturing and Process Plant Base

The accelerating adoption of Industrial IoT architectures, digital twin platforms, predictive maintenance programs, and manufacturing execution system modernization by Indian manufacturing and process industry operators who are investing in operational technology digitalization to improve production efficiency, reduce unplanned downtime, lower energy consumption, and enhance product quality consistency is generating a large and commercially significant retrofit sensor market as legacy plants replace conventional analog and discrete sensors with smart sensor devices capable of delivering the rich, continuous, multi-parameter digital data streams required by modern industrial analytics and AI-powered process optimization platforms. Indian manufacturing companies are investing in Industry 4.0 adoption programs across automotive, pharmaceuticals, chemicals, and steel sectors, with government initiatives including the Smart Advanced Manufacturing and Rapid Transformation Hub program and the National Manufacturing Competitiveness Program providing technical and financial support for digitalization investment that includes sensor network upgrades as a foundational infrastructure requirement. The predictive maintenance value proposition, which enables manufacturers to avoid the USD 3,000 to USD 40,000 per-hour cost of unplanned production line downtime through condition-based intervention enabled by vibration, temperature, and acoustic emission sensors deployed on critical rotating and reciprocating equipment, is generating compelling return on investment evidence across Indian manufacturing early adopters whose documented downtime reduction and maintenance cost savings are accelerating investment decision timelines for the broader Indian manufacturing community considering smart sensor and IIoT platform adoption. The energy cost management imperative, with Indian industrial electricity tariffs averaging INR 7 to INR 12 per kilowatt-hour and energy typically constituting 15% to 30% of total manufacturing operating cost in energy-intensive sectors, is driving investment in energy monitoring sensors, power quality measurement systems, and process efficiency optimization sensor networks whose deployment generates measurable energy cost savings that deliver payback periods of 12 to 36 months on sensor system investment.

India’s National Infrastructure Pipeline and Energy Transition Investment Generating Large-Scale Sensor Procurement in Power, Water, and Oil and Gas Sectors

The National Infrastructure Pipeline’s committed investment of USD 1.4 trillion across the 2019 to 2025 program period, subsequently extended through the National Master Plan for Infrastructure, is generating an unprecedented scale of sensor procurement demand across power generation and transmission, renewable energy, water supply and treatment, urban development, and transportation infrastructure sectors whose instrument and automation requirements are being specified and procured through central and state government agencies, public sector undertakings, and infrastructure development corporations that collectively represent the largest single institutional buyer segment in the India industrial sensors market. The Jal Jeevan Mission’s target of providing functional household tap connections to all 192 million rural households by 2024 and the AMRUT 2.0 scheme’s urban water supply and sewage treatment investment of INR 2.87 lakh crore are generating large procurement programs for flow meters, pressure transmitters, level sensors, water quality analyzers, and pump station monitoring systems across the water utilities that are implementing these programs, with each water supply scheme requiring hundreds of measurement points and each wastewater treatment plant requiring dozens of process monitoring sensors whose cumulative procurement across thousands of scheme implementations nationwide represents a structurally large sensor demand stream. The oil and gas sector’s capital expenditure expansion, driven by ONGC’s five-year USD 33 billion capital program, the development of deepwater gas fields in the KG basin, the expansion of city gas distribution networks under the National Gas Grid program, and the petroleum product pipeline network expansion by IOC, BPCL, and HPCL, is generating multiyear sensor procurement programs for pressure, flow, temperature, level, gas detection, and corrosion monitoring sensor systems whose safety-critical application requirements and SIL certification specifications represent the highest technical specification and unit value sensor categories within the India industrial sensors market.

Key Challenges

Dominance of Imported Sensor Products and Limited Domestic Manufacturing Capability Creating Supply Chain Vulnerability and Import Cost Burden

The India industrial sensors market is characterized by a pronounced structural dependence on imported sensor products from multinational automation technology leaders including Siemens, Honeywell, ABB, Emerson, Endress and Hauser, Yokogawa, and Vega Systems, whose proprietary measurement technologies, global application engineering expertise, established installed base in Indian process plants, and long-term maintenance and calibration service relationships create a deep-rooted competitive position that domestic Indian sensor manufacturers have been unable to challenge across the majority of process measurement and precision industrial sensor categories. The import duty and logistics cost burden associated with sensor procurement from international suppliers, with basic customs duty rates of 7.5% to 15% applicable to most industrial sensor categories alongside IGST, adds 20% to 35% to the landed cost of imported sensors relative to ex-factory prices, creating a commercially significant premium that narrows project economics on sensor-intensive automation contracts and constrains the affordability of sensor-dense IIoT deployment programs for cost-sensitive Indian manufacturers whose capital allocation frameworks require minimum return on investment thresholds that imported sensor pricing makes difficult to achieve relative to the equivalent cost structures in countries with domestic sensor manufacturing industries. The limited domestic manufacturing capability for precision industrial sensors in India, confined to basic flow meters, pressure gauges, level switches, and temperature assemblies produced by companies including Azbil India, Radix Instruments, and few others, leaves the majority of high-specification process instrumentation, smart sensor, and advanced measurement technology categories entirely dependent on import supply, creating strategic supply chain vulnerability during periods of global logistics disruption and creating ongoing forex expenditure that the Atmanirbhar Bharat initiative seeks to reduce but has not yet achieved at meaningful scale in the sensor manufacturing domain.

Price Sensitivity of Indian Industrial Buyers and Extended Project Decision Timelines Constraining Premium Smart Sensor Adoption

The procurement decision frameworks of Indian industrial buyers across public sector undertakings, private manufacturing companies, and infrastructure project implementing agencies are dominated by capital cost minimization objectives that systematically favor lowest-cost technically compliant sensor products over technologically superior alternatives whose higher upfront cost is justified by lifecycle cost advantages including reduced maintenance, improved diagnostic capability, and extended service life that are not adequately weighted in the L1-based tender evaluation processes that govern the majority of large-scale sensor procurement in Indian industrial capital projects. The total cost of ownership analysis framework, which provides the commercial justification for premium smart sensor investment through the quantification of avoided maintenance cost, improved process efficiency, and reduced unplanned downtime over a sensor’s 15 to 25-year operational life, is not systematically applied in Indian industrial procurement decision-making at the level of rigor required to consistently override the upfront cost differential between premium smart sensors and conventional basic sensors in competitive tender evaluations, resulting in sensor specifications that underinvest in measurement capability relative to the process optimization value the plant could extract from higher-specification instrumentation. The extended project approval, funding release, and procurement execution timelines characteristic of Indian public sector infrastructure projects, which frequently involve 12 to 36-month delays between project sanction and equipment procurement order placement due to land acquisition, environmental clearance, statutory approval, and government financial approval process timelines, create commercial uncertainty and working capital pressure for sensor suppliers and distributors who maintain inventory and application engineering resource commitments in anticipation of project procurement that materializes on unpredictable schedules.

Skilled Workforce Scarcity for Industrial Sensor Installation, Calibration, and Digital Platform Integration Limiting Technology Adoption Depth

The effective deployment and ongoing operational benefit realization from advanced industrial sensors, smart measurement systems, and IIoT-integrated sensor networks requires specialized technical competencies in instrumentation engineering, digital communication protocol configuration, sensor calibration and verification, and data analytics platform integration that are in critically short supply relative to the pace of sensor technology adoption across India’s expanding industrial base, creating a human capital constraint that limits the operational effectiveness of sensor investments and generates persistent underutilization of the intelligence capabilities for which premium sensor products are purchased. The instrumentation and control engineering workforce in India, while numerically significant through the output of engineering colleges offering electronics and instrumentation engineering programs, exhibits a substantial practical skills gap between the theoretical academic curriculum and the hands-on commissioning, calibration, troubleshooting, and digital integration competencies required for effective deployment of modern smart sensor systems, particularly in the HART digital communication configuration, Foundation Fieldbus segment commissioning, and IO-Link master integration capabilities that are prerequisites for unlocking the diagnostic and predictive maintenance value of smart transmitters and intelligent field devices. The Industry 4.0 sensor integration challenge, requiring competency in OPC-UA data modeling, MQTT message broker configuration, cloud IoT platform connectivity, and time-series database management for sensor data historian implementation, represents a skills domain at the intersection of operational technology and information technology whose practitioners are extremely scarce in the Indian industrial workforce and whose development through industry training programs, university curriculum update, and technology provider certification programs is proceeding substantially more slowly than the pace of industrial IoT platform commercial deployment creates demand for.

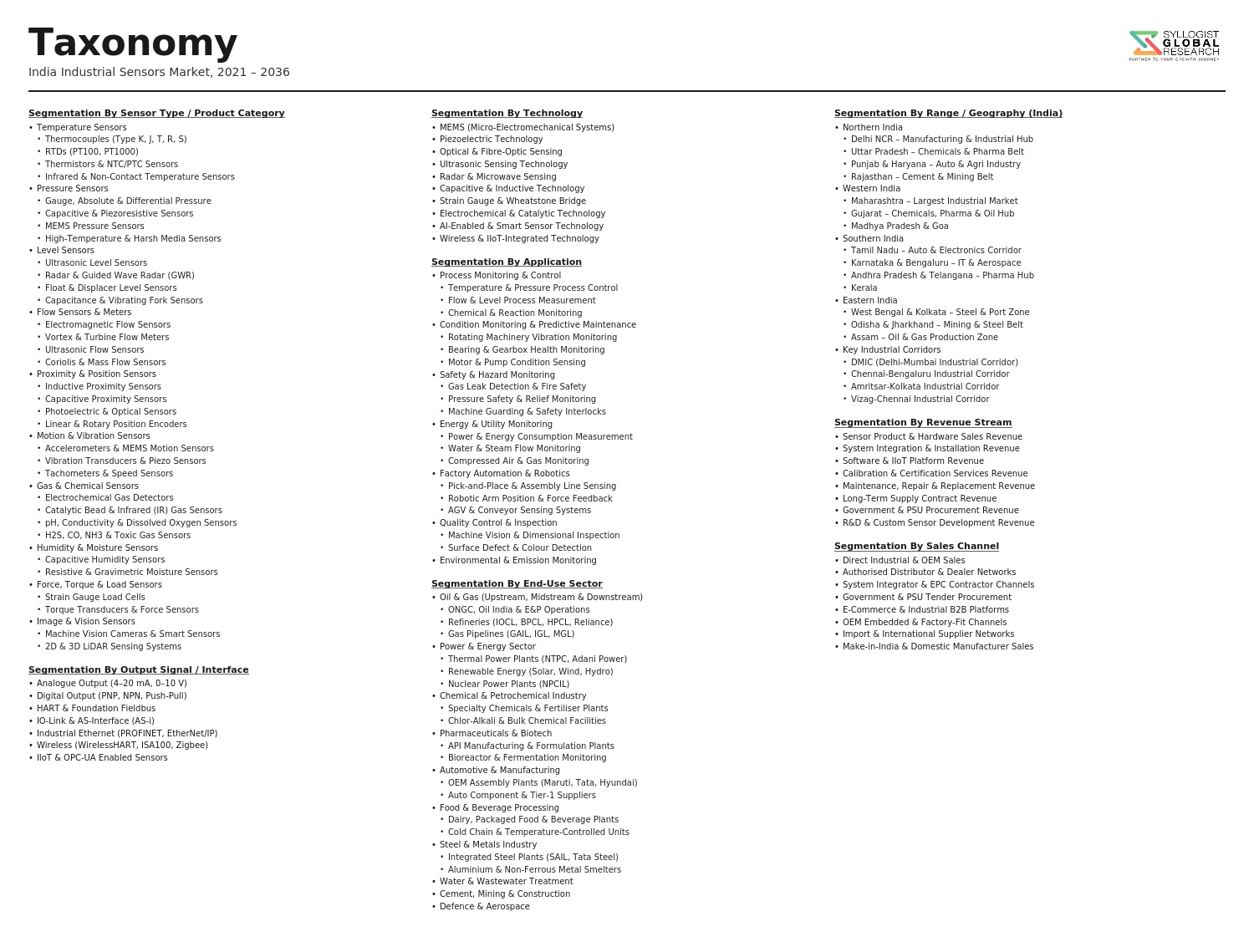

Market Segmentation

- Segmentation By Sensor Type

- Pressure Sensors and Transmitters

- Temperature Sensors (Thermocouples, RTDs, Infrared Pyrometers)

- Flow Sensors and Flow Meters (Electromagnetic, Ultrasonic, Coriolis, Vortex)

- Level Sensors (Ultrasonic, Radar, Guided Wave Radar, Capacitance)

- Proximity and Position Sensors (Inductive, Capacitive, Photoelectric, Encoders)

- Vibration and Condition Monitoring Sensors

- Gas Detection and Analytical Sensors

- Humidity and Environmental Sensors

- Force, Load, and Torque Sensors

- Vision and Optical Sensors

- Others

- Segmentation By Technology

- Conventional Analog and Discrete Sensors

- Smart and Intelligent Sensors (HART, Foundation Fieldbus, PROFIBUS)

- Wireless and IIoT-Connected Sensors (WirelessHART, ISA100.11a)

- MEMS-Based Miniaturized Sensors

- Fiber Optic Sensors

- Edge AI-Enabled Sensors

- Others

- Segmentation By End-Use Industry

- Oil and Gas (Upstream, Midstream, Downstream)

- Pharmaceuticals and Life Sciences

- Chemicals and Petrochemicals

- Automotive and Electric Vehicles

- Power Generation and Utilities (Thermal, Renewable, Nuclear)

- Food and Beverage Processing

- Water and Wastewater Treatment

- Metals, Mining, and Cement

- Electronics and Semiconductor Manufacturing

- Textiles and Apparel Manufacturing

- Paper and Pulp

- Others

- Segmentation By Application

- Process Control and Automation

- Predictive and Condition-Based Maintenance

- Safety and Hazard Monitoring

- Energy Monitoring and Management

- Environmental and Emissions Monitoring

- Quality Control and Inspection

- Industrial IoT and Digital Twin Integration

- Others

- Segmentation By Supply Source

- Multinational OEM Direct Supply and Authorized Distribution

- Domestic Indian Sensor Manufacturers

- Third-Party Importers and Trading Companies

- System Integrators and Value-Added Resellers

- Others

- Segmentation By Region

- Western India (Gujarat, Maharashtra, Rajasthan)

- Southern India (Tamil Nadu, Karnataka, Andhra Pradesh, Telangana)

- Northern India (Delhi NCR, Uttar Pradesh, Punjab, Haryana)

- Eastern India (West Bengal, Odisha, Jharkhand)

- Central India (Madhya Pradesh, Chhattisgarh)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Industrial Sensors Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by sensor type, technology, end-use industry, application, supply source, and region, to enable global and domestic sensor manufacturers, automation system integrators, industrial end users, and investors to identify which sensor categories and industrial sectors will generate the highest absolute procurement volumes and the most commercially attractive demand growth across the forecast period?

- How are the PLI scheme manufacturing investment commitments across pharmaceuticals, electronics, automotive, specialty chemicals, and advanced chemistry cells translating into greenfield plant instrumentation procurement timelines and sensor specification requirements by sector, and which sensor technology categories, communication protocols, and hazardous area certification standards are being specified in PLI scheme-supported manufacturing facilities that will define the technical procurement baseline of India’s new industrial sensor installed base through 2034?

- What is the current adoption rate of smart sensors with digital communication capabilities, IIoT connectivity, and predictive maintenance functionality across Indian process industries, discrete manufacturing, and energy sector applications, and what are the documented operational and financial benefits including downtime reduction, maintenance cost savings, energy efficiency improvement, and product quality enhancement that early IIoT sensor adopters in India are achieving, and how are these benefits accelerating investment decision timelines among the broader Indian industrial community considering smart sensor and Industry 4.0 platform adoption?

- How is India’s renewable energy capacity expansion program, comprising 500 gigawatts of non-fossil fuel power by 2030, combined with the Revamped Distribution Sector Scheme smart metering and grid automation investment, translating into sensor procurement volumes by type and application across wind energy condition monitoring, solar PV performance monitoring, smart grid feeder automation, and power quality measurement applications, and which sensor technology providers are best positioned to capture the growing energy sector sensor procurement opportunity?

- Who are the leading multinational industrial sensor manufacturers including Siemens, Honeywell, ABB, Emerson, Endress and Hauser, Yokogawa, and Vega Systems operating through Indian subsidiaries and distribution networks, the domestic Indian sensor manufacturers, the major system integrators deploying sensor-based automation solutions, and the key end-user industry procurement organizations currently defining the competitive and commercial landscape of the India industrial sensors market, and what are their respective product portfolios, Indian manufacturing and localization strategies, distribution network depth, technical service infrastructure, digital platform integration capabilities, government and PSU project track records, and strategic positioning in response to the Atmanirbhar Bharat initiative creating pressure for import substitution across industrial automation and sensor categories through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Import Dependency, China Concentration & Supply Chain Disruption Risk

- Counterfeit, Sub-Standard Sensor Products & Product Quality Risk

- Technology Obsolescence, IIoT Transition & Digital Disruption Risk

- Price Sensitivity, Cost Pressure & Market Commoditisation Risk

- Skilled Workforce Shortage, Installation Complexity & Maintenance Capability Risk

- Regulatory Framework & Standards

- BIS Standards, IS Specifications & Mandatory Certification for Industrial Instruments & Sensors

- PESO (Petroleum & Explosives Safety Organisation) Approval Framework for Hazardous Area & Intrinsically Safe Sensors

- Electrical Equipment Safety, IE Standards & Installation Norms Applicable to Industrial Sensors & Transmitters

- RoHS-Equivalent, Hazardous Substance Restriction & WEEE-Equivalent E-Waste Regulations for Sensor Products

- Calibration, Metrology & NABL Accreditation Standards for Industrial Measurement & Sensing Instruments

- India Industrial Sensors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Sensor Type

- Pressure Sensors (Gauge, Absolute, Differential & Vacuum)

- Temperature Sensors (RTD, Thermocouple, Thermistor & Infrared)

- Level Sensors (Ultrasonic, Radar, Capacitive, Float & Hydrostatic)

- Flow Sensors (Electromagnetic, Coriolis, Vortex, Ultrasonic & Differential Pressure)

- Proximity & Position Sensors (Inductive, Capacitive, Photoelectric & Ultrasonic)

- Humidity & Moisture Sensors

- Force, Load & Torque Sensors

- Gas & Chemical Detection Sensors (Fixed Gas Detectors & Electrochemical Sensors)

- Vision & Image Sensors (Industrial Cameras, Machine Vision & CMOS Sensors)

- Vibration, Acceleration & Condition Monitoring Sensors

- Market Size & Forecast by Technology

- Wired Sensors (4-20 mA, HART, Modbus & Fieldbus-Based)

- Wireless & IIoT-Enabled Sensors (WirelessHART, ISA100, Zigbee & LoRaWAN)

- MEMS-Based Sensors (Micro-Electro-Mechanical Systems)

- Smart & Intelligent Sensors with Edge Computing & On-Board Processing

- Fibre Optic Sensors (Distributed Temperature Sensing & Structural Monitoring)

- Market Size & Forecast by End-Use Industry

- Oil, Gas & Petroleum Refining

- Chemicals & Petrochemicals

- Pharmaceuticals & Biotechnology

- Food & Beverages

- Power Generation & Energy (Thermal, Hydro, Nuclear & Renewable)

- Automotive & Transportation Manufacturing

- Water & Wastewater Treatment

- Metals, Mining & Cement

- Semiconductors & Electronics Manufacturing

- Pulp, Paper & Textiles

- Market Size & Forecast by Output Signal Type

- Analog Output (4-20 mA, 0-10 V)

- Digital Output (IO-Link, Fieldbus & Industrial Ethernet)

- Wireless Output (WirelessHART, Zigbee, LoRa & Wi-Fi)

- Market Size & Forecast by Application

- Process Monitoring & Control

- Safety, Alarm & Emergency Shutdown Systems

- Predictive Maintenance & Condition Monitoring

- Quality Control & Inspection

- Energy Management & Efficiency Optimisation

- Market Size & Forecast by End-User Type

- Large Enterprises & Public Sector Undertakings (PSUs)

- Small & Medium Enterprises (SMEs)

- Engineering, Procurement & Construction (EPC) Contractors

- System Integrators & Panel Builders

- Market Size & Forecast by Sales Channel

- Direct OEM & End-User Supply (Factory Direct)

- Authorised Distributor & Dealer Network

- System Integrator & Value-Added Reseller (VAR) Channel

- Online & E-Commerce Distribution Channel

- North India Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- By State

- Market Size & Forecast

- South India Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- By State

- Market Size & Forecast

- West India Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- By State

- Market Size & Forecast

- East India Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- By State

- Market Size & Forecast

- Central India Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- By State

- Market Size & Forecast

- State-Wise* Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By End-Use Industry

- By Application

- By End-User Type

- By Sales Channel

- Market Size & Forecast

- *States Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Gujarat, Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Rajasthan, Uttar Pradesh, Delhi NCR, Haryana, Madhya Pradesh, West Bengal, Odisha, Jharkhand, Punjab

- Technology Landscape & Innovation Analysis

- MEMS Sensor Technology Deep-Dive: Miniaturisation, Multi-Parameter Integration & Cost Reduction Trends

- IIoT-Enabled Wireless Sensor Networks, Smart Sensor Architecture & Edge Intelligence Technology

- Vision & Image Sensor Technology for Industrial Machine Vision & Automated Quality Inspection

- Gas & Chemical Detection Sensor Technology: Electrochemical, Catalytic & Optical Sensing Platforms

- Fibre Optic & Distributed Sensing Technology for Process & Structural Health Monitoring

- AI & Machine Learning Integration with Industrial Sensor Data Analytics & Predictive Maintenance Platforms

- Functional Safety, SIL-Rated & Intrinsically Safe Sensor Technology for Hazardous Area Applications

- Patent & IP Landscape in Industrial Sensor Technologies

- Value Chain & Supply Chain Analysis

- Sensor Chip, Transducer Element & MEMS Component Manufacturing Supply Chain

- Sensor Module Assembly, Signal Conditioning Electronics & Transmitter Manufacturing

- OEM Integration of Sensors into Instruments, Controllers, PLCs & Field Devices

- Authorised Distributor, Agent & Dealer Network Channel

- System Integrator, Panel Builder & Value-Added Reseller (VAR) Channel

- End-User Industry Direct Procurement, MRO Buying & Institutional Supply Channel

- Calibration, Repair, Spare Parts & Aftermarket Service Channel

- Pricing Analysis

- Price Analysis by Sensor Type: Pressure, Temperature, Level, Flow & Proximity Sensors

- Price Benchmarking: Domestic Indian Manufactured vs. Imported MNC Sensor Products

- Distribution Margin, Dealer Mark-Up & Channel Pricing Structure Analysis

- OEM Project Supply vs. MRO Replacement Pricing Dynamics

- Smart & IIoT Sensor Price Premium vs. Conventional Wired Sensor Price Benchmarking

- Price Trend & Outlook: Impact of Component Costs, Import Duties & INR Exchange Rate Volatility

- Sustainability & Environmental Analysis

- Industrial Sensor-Enabled Energy Efficiency, Process Optimisation & Carbon Footprint Reduction Contribution

- RoHS, REACH-Equivalent Compliance & Hazardous Substance Reduction in Sensor Manufacturing & Packaging

- Predictive Maintenance & Sensor-Driven Reduction of Industrial Waste, Unplanned Downtime & Material Loss

- Gas Sensor Applications for Emissions Monitoring, Leak Detection & Industrial Environmental Compliance

- Lifecycle Assessment of Industrial Sensors: Durability, Repairability, End-of-Life Management & Recycling

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (MNC Dominated vs. Domestic Player Segment by Sensor Type & Industry)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sensor Type, Technology & End-Use Industry

- Player Classification

- Global MNC Sensor Manufacturers with India Presence & Local Manufacturing

- Process Instrumentation & Transmitter OEMs with Integrated Sensor Solutions

- Specialised Industrial Sensor Manufacturers (Pressure, Temperature, Level & Flow)

- Proximity, Position & Safety Sensor Specialists

- IIoT Platform & Smart Sensor Technology Providers

- Domestic Indian Sensor Manufacturers & Component Suppliers

- Distributors, System Integrators & Value-Added Resellers (VARs)

- Competitive Analysis Frameworks

- Market Share Analysis by Sensor Type, Technology & End-Use Industry

- Company Profile

- Company Overview & Headquarters

- Industrial Sensor Product & Technology Portfolio

- Key Customer Relationships & Reference Installations by Industry

- Manufacturing Footprint & Production Capacity (India & Global)

- Revenue (Industrial Sensor Segment) & Order Backlog

- Technology Differentiators, IP Portfolio & Certifications (ATEX, IECEx, PESO, BIS)

- Key Strategic Partnerships, JVs, Acquisitions & M&A Activity

- Recent Developments (Product Launches, Capacity Expansion, India Market Initiatives)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Sensor Type, Technology, End-Use Industry, Application & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output