Market Definition

The Global Defense AI and Autonomous Battlefield Systems Market encompasses the development, integration, procurement, and operational deployment of artificial intelligence software platforms, machine learning inference engines, autonomous unmanned ground, aerial, and maritime vehicles, intelligent surveillance and reconnaissance systems, AI-powered command and control decision-support architectures, and autonomous weapons systems across land, air, maritime, space, and cyber operational domains. The market includes embedded AI processors, edge computing hardware, secure communications infrastructure, and associated sustainment services procured by national defense ministries, military commands, intelligence agencies, and allied defense organizations globally.

Market Insights

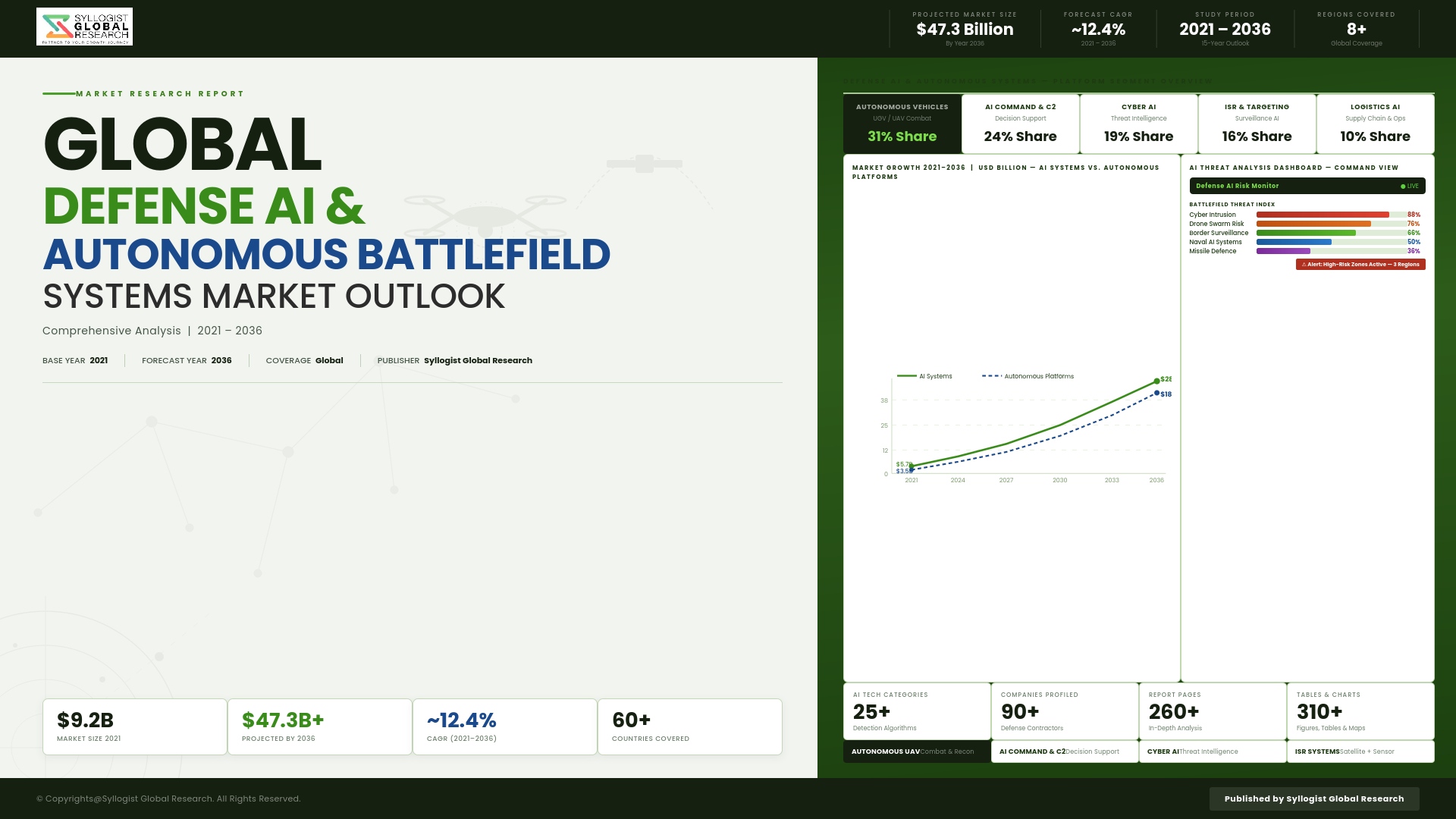

The global defense AI and autonomous battlefield systems market is approaching a fundamental inflection point, shaped by the convergence of transformative machine learning advancements, proliferating edge computing capabilities, and a deteriorating global security environment compelling major military powers and allied defense establishments to accelerate procurement of AI-enabled operational capabilities across all warfighting domains. The market was valued at approximately USD 22.4 billion in 2025 and is projected to reach USD 89.3 billion by 2034, advancing at a compound annual growth rate of 16.7% through the forecast period, as defense organizations transition artificial intelligence from experimental demonstration programs into production-scale deployment encompassing unmanned systems, intelligence, surveillance and reconnaissance platforms, cybersecurity applications, autonomous logistics, and AI-enabled command and control decision-support architectures.

The strategic imperatives driving this acceleration are reinforced by direct operational evidence from recent conflict environments, where AI-augmented military capabilities demonstrated measurable performance advantages over conventional systems at operationally significant scale, creating procurement urgency among defense establishments that witnessed these capability differentials and recognize the strategic risk of delayed modernization. The United States Department of Defense has institutionalized artificial intelligence as a cross-cutting investment priority across all military branches, with autonomous systems and AI programs receiving growing allocations within research, development, test, and evaluation budgets. China is simultaneously pursuing a nationally coordinated civil-military fusion strategy that channels commercial AI ecosystem capabilities directly into defense applications, reshaping global benchmarks for autonomous platform performance, AI-driven intelligence fusion, and algorithmic decision support.

The autonomous unmanned systems segment, which encompasses unmanned aerial vehicles, loitering munitions, unmanned ground vehicles, and unmanned maritime surface and undersea platforms, is the fastest-growing category within the broader defense AI market, driven by proven operational advantages of persistent surveillance endurance, reduced crew risk, and multi-domain swarming capabilities that autonomous platforms deliver in contested operational environments. Edge AI processors enabling onboard inference without dependence on communications links represent among the most commercially dynamic hardware categories within the market, generating strong investment from established defense prime contractors, specialized semiconductor developers, and dual-use technology companies seeking to establish positions in defense AI hardware supply chains.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, underpinned by substantial autonomous systems and defense AI investment programs in China, India, South Korea, Japan, and Australia, each driven by evolving regional threat environments and strategic modernization imperatives. North America maintains its position as the largest absolute revenue market by defense AI spending, with the United States Department of Defense providing unmatched program scale, research funding, and systems integration procurement volume. Europe represents the third major regional market, with NATO commitments and threat reassessments following the conflict in Ukraine driving materially accelerated defense AI and autonomous systems procurement across member states.

Key Drivers

Escalating Geopolitical Competition and Sustained Defense Budget Growth Establishing Durable Procurement Mandates for AI and Autonomous Systems Across Major Military Powers

The intensification of strategic competition among major military powers, combined with regionalized conflict environments demonstrating the operational effectiveness of AI-enabled surveillance and autonomous strike capabilities, is generating durable multi-year procurement mandates for defense AI and autonomous systems that are substantially resistant to near-term fiscal constraints. Global defense expenditure reached approximately USD 2.4 trillion in 2025, with AI, autonomous systems, and advanced technology modernization programs representing a growing priority allocation within national defense budgets as governments respond to operational lessons observed in recent conflicts by compressing the traditionally extended procurement timelines governing advanced military technology acquisition. NATO member expansion of defense spending targets and Indo-Pacific alliance partners accelerating autonomous systems investment are further broadening the addressable market for defense AI system developers and prime contractors.

Unmanned Autonomous Systems Proliferation and Multi-Domain Swarm Capability Development Generating Durable Procurement Growth Across Land, Air, and Maritime Operational Domains

The demonstrated operational effectiveness of unmanned aerial systems, autonomous ground platforms, and maritime unmanned surface and undersea vessels in intelligence, surveillance, reconnaissance, and direct engagement roles in recent conflict environments has triggered an unprecedented acceleration in autonomous platform procurement programs across both major military powers and emerging defense modernizers, creating durable demand for AI navigation systems, autonomous mission management software, swarm coordination algorithms, and edge computing hardware enabling platform operation in communications-contested environments. The loitering munition segment, in which AI-enabled target discrimination and terminal guidance deliver precision engagement capability at a fraction of conventional precision munition costs, has emerged as a high-volume procurement priority across multiple defense establishments simultaneously, with production programs scaling rapidly to meet demand.

AI-Enabled Intelligence, Surveillance, and Reconnaissance Integration and Multi-Source Data Fusion Delivering Decision Superiority Across the Operational Command Architecture

The transformation of battlefield command and control through AI-powered intelligence fusion, predictive threat modeling, automated sensor cueing, and machine-speed operational planning support is generating sustained investment in defense AI software platforms that process multi-source intelligence streams from satellite imagery, signals intelligence, open-source data, and autonomous sensor networks into operationally actionable assessments within decision timelines that human analytical teams cannot replicate. Defense programs in the United States, United Kingdom, Australia, and key NATO allies are investing in enterprise-scale AI-enabled command and control platforms integrating across joint force elements, providing commanders with persistent situational awareness and AI-generated course-of-action recommendations that compress the observe-orient-decide-act decision cycle to operationally decisive timelines.

Key Challenges

Evolving International Legal Frameworks and Ethical Governance Constraints Governing Lethal Autonomous Weapons Systems and Meaningful Human Control Requirements

The operational deployment of lethal autonomous weapons systems capable of selecting and engaging targets without direct human authorization is subject to intensifying international legal scrutiny, domestic legislative challenge, and sustained advocacy for binding treaty-level prohibitions, creating a regulatory risk environment that complicates defense AI program planning, acquisition strategy, and export licensing for advanced autonomous engagement systems. International humanitarian law requirements for proportionality assessment, distinction between combatants and protected persons, and command responsibility attribution in autonomous weapons engagements remain unresolved at the treaty level, while national-level policies governing meaningful human control over lethal autonomous decision-making vary materially across military powers, creating compliance complexity for multinational defense programs and allied interoperability architectures requiring cross-national system integration.

Adversarial Machine Learning Vulnerabilities, Cybersecurity Attack Surface Expansion, and Algorithmic Integrity Risks in Networked Defense AI Deployment

Artificial intelligence algorithms deployed in defense-critical applications including target recognition, autonomous navigation, threat classification, and command decision support are susceptible to adversarial machine learning attacks, data poisoning during training pipeline infiltration, and sensor spoofing techniques that can cause AI systems to produce systematically incorrect outputs under adversarially manipulated conditions, creating mission-critical failure risks qualitatively distinct from conventional software vulnerabilities and requiring dedicated adversarial robustness certification architectures that current defense AI acquisition frameworks are not consistently equipped to mandate. The expanding network connectivity of autonomous battlefield platforms simultaneously increases the cybersecurity attack surface available to sophisticated state-level adversaries seeking to compromise defense AI system integrity through communications link exploitation, onboard processor infiltration, and supply chain interdiction of AI hardware and software components.

Structural Talent Scarcity in Defense-Grade AI Engineering, Security-Cleared Machine Learning Expertise, and Dual-Use Technology Export Control Compliance Complexity

The defense AI industry confronts a structural talent constraint at the intersection of advanced machine learning engineering proficiency, security clearance eligibility, and military operational domain knowledge, where the addressable talent pool is substantially smaller than aggregate demand generated by rapidly scaling defense AI programs across the United States, European allied nations, and Asia-Pacific partner countries simultaneously, extending program timelines, elevating development costs, and limiting technical depth of defense AI architectures relative to their commercial counterparts. Dual-use technology export control regulations governing AI hardware, software algorithms, and autonomous systems components impose additional compliance complexity on multinational defense programs, cross-border technology transfer within allied coalitions, and commercial AI firms seeking to participate in international defense procurement without triggering technology transfer restrictions.

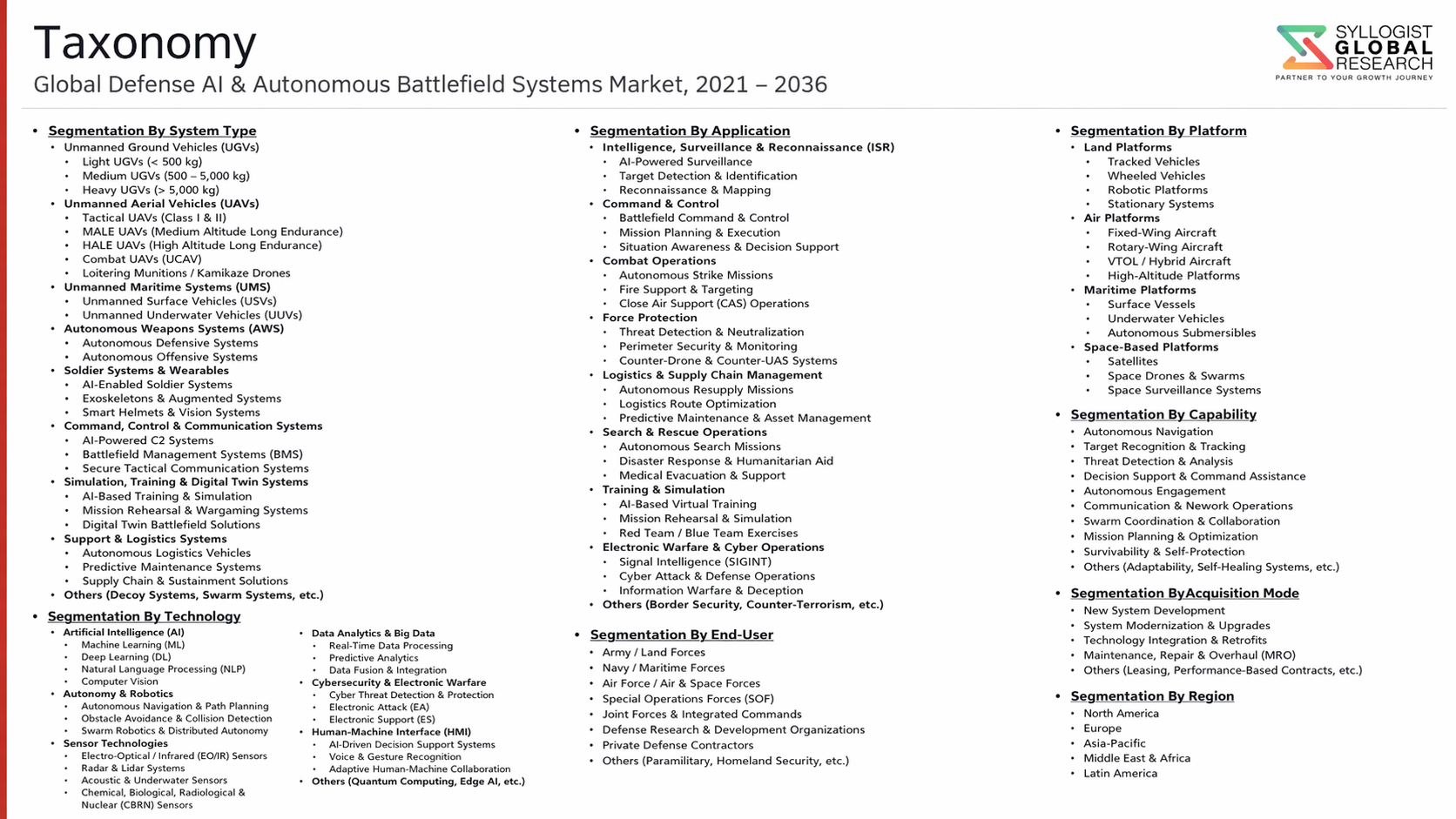

Market Segmentation

- Segmentation By Technology Type

- Computer Vision and Image Recognition Systems

- Natural Language Processing and Multi-Modal AI

- Autonomous Navigation and Path Planning Algorithms

- Predictive Analytics and Threat Intelligence Platforms

- Swarm Intelligence and Multi-Agent Coordination Systems

- Generative AI and Synthetic Training Data Platforms

- Others

- Segmentation By System Type

- Unmanned Aerial Vehicles (UAV) and Loitering Munitions

- Unmanned Ground Vehicles (UGV) and Robotic Combat Platforms

- Unmanned Maritime Surface Vehicles (USV)

- Unmanned Underwater Vehicles (UUV)

- AI-Enabled Command, Control, Communications, Computers, Intelligence, Surveillance and Reconnaissance (C4ISR) Systems

- Autonomous Cyber Defense and Electronic Warfare Systems

- Others

- Segmentation By Platform

- Airborne Platforms

- Land-Based Platforms

- Naval and Undersea Platforms

- Space-Based Platforms

- Cyber and Electronic Warfare Platforms

- Multi-Domain and Cross-Domain Systems

- Others

- Segmentation By Application

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Target Acquisition and Fire Control

- Autonomous Logistics and Resupply

- Cybersecurity and Electronic Warfare

- Training, Simulation, and Mission Rehearsal

- Predictive Maintenance and Fleet Management

- Command and Control Decision Support

- Others

- Segmentation By Component

- AI Software Platforms and Algorithm Suites

- Edge AI Processors and Onboard Computing Hardware

- Sensors and Sensor Fusion Systems

- Secure Communications and Data Link Systems

- Autonomous Navigation and Guidance Systems

- Human-Machine Interface and Operator Control Stations

- Others

- Segmentation By Autonomy Level

- Human-Operated with AI Decision Support (Level 1)

- Human-on-the-Loop Semi-Autonomous Systems (Level 2)

- Human-Supervised Autonomous Systems (Level 3)

- Fully Autonomous Systems with Optional Human Override (Level 4)

- Fully Autonomous Systems without Human Intervention (Level 5)

- Segmentation By End User

- Army and Land Forces

- Air Force and Aerospace Commands

- Naval and Maritime Forces

- Intelligence Agencies and Special Operations Commands

- Homeland Security and Border Defense Organizations

- Defense Research and Development Institutions

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Defense AI and Autonomous Battlefield Systems Market in 2025, projected through 2034, disaggregated by technology type and platform, enabling defense contractors, investors, and procurement planners to identify highest-growth segments and most durable revenue opportunities across the AI-enabled military capability landscape?

- How are the United States, China, and key NATO and Indo-Pacific allies allocating defense AI investment across autonomous unmanned systems, C4ISR platforms, and cyber defense applications, and which national programs are defining the technical and procurement benchmarks shaping global defense AI market architecture through 2034?

- What operational, regulatory, and ethical constraints on lethal autonomous weapons systems are shaping procurement boundaries, and how are leading defense contractors architecting human-machine teaming frameworks to balance operational autonomy requirements with meaningful human control obligations under evolving international humanitarian law frameworks?

- Which autonomous platform segments, including unmanned aerial vehicles, loitering munitions, unmanned ground vehicles, and unmanned undersea vessels, are generating the highest growth rates through 2034, and what sensor fusion, edge AI, and swarm coordination technologies are most critical to operational performance leadership in each category?

- How is the competitive landscape structured among prime defense contractors, specialist AI software firms, and dual-use technology companies pursuing defense AI contracts, and what partnership, acquisition, and teaming strategies are enabling new entrants to compete against established prime contractors in next-generation autonomous systems programs?

- What are the most significant cybersecurity and adversarial AI vulnerabilities affecting defense AI systems in operational deployment, and how are defense procurement agencies and system developers addressing algorithmic robustness, secure training pipeline integrity, and anti-spoofing capability requirements within formal acquisition and certification frameworks?

- Which regional defense markets, specifically Asia-Pacific, Europe, and the Middle East, are expected to generate the most substantial incremental defense AI procurement through 2034, and what geopolitical, budgetary, and industrial base factors are driving capability investment priorities and supplier selection decisions in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- AI Ethics, Algorithmic Bias & Autonomous Decision-Making Risk

- Export Controls, ITAR & International Technology Transfer Risk

- Cybersecurity, Electronic Warfare Vulnerability & System Integrity Risk

- Regulatory, Legal & International Humanitarian Law Compliance Risk

- Technology Reliability, Operational Failure & Mission-Critical Performance Risk

- Regulatory Framework & Standards

- Defense Procurement Regulations, Acquisition Frameworks & National Security Policy

- NATO STANAG Standards, Allied Interoperability Frameworks & Joint Operations Technology Policy

- Export Control Regimes: ITAR, EAR & Wassenaar Arrangement AI and Autonomous Systems Provisions

- Autonomous Weapons Systems (AWS) International Humanitarian Law, UN CCW & Lethal Autonomous Weapons Policy

- AI Ethics in Defense: DoD AI Ethics Principles, EU AI Act Defense Exemptions & National AI Strategy Frameworks

- Global Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units, Systems & Platforms Deployed)

- Market Size & Forecast by System Type

- Autonomous Unmanned Aerial Vehicles (UAVs) & Unmanned Combat Aerial Vehicles (UCAVs)

- Autonomous Unmanned Ground Vehicles (UGVs) & Robotic Combat Platforms

- Autonomous Unmanned Maritime Systems: Unmanned Surface Vessels (USVs) & Unmanned Underwater Vehicles (UUVs)

- AI-Powered Command, Control, Communications, Computers & Intelligence (C4I) Systems

- AI-Enabled Intelligence, Surveillance & Reconnaissance (ISR) Platforms

- Autonomous Loitering Munitions & Precision Guided Weapon Systems

- AI-Driven Electronic Warfare (EW), Cyber & Directed Energy Weapon Systems

- Autonomous Logistics, Resupply & Combat Support Robotics

- Swarm Intelligence & Multi-Agent Autonomous System Platforms

- Market Size & Forecast by Technology

- Machine Learning (ML) & Deep Learning Algorithms for Target Recognition & Situational Awareness

- Computer Vision & Synthetic Aperture Radar (SAR) AI Processing for Defense Applications

- Natural Language Processing (NLP) & AI-Powered Decision Support Systems

- Edge AI, Embedded Computing & Real-Time Inference Processors for Autonomous Platforms

- AI-Enabled Sensor Fusion: Multi-Domain Data Integration & Battlespace Awareness

- Reinforcement Learning for Autonomous Mission Planning & Tactical Decision-Making

- Secure AI Communication Protocols & Blockchain for Defense Networks

- Digital Twin & Simulation AI for Mission Rehearsal & Predictive Maintenance

- Market Size & Forecast by Platform

- Air Platforms

- Ground Platforms

- Naval Platforms

- Space Platforms

- Cyber & Electronic Domain Platforms

- Market Size & Forecast by Application

- Intelligence, Surveillance & Reconnaissance (ISR)

- Target Acquisition & Precision Strike

- Border Security, Perimeter Defense & Force Protection

- Logistics, Autonomous Resupply & Combat Support

- Electronic Warfare & Cyber Operations

- Command & Control Decision Support

- Search, Rescue & Casualty Evacuation (CASEVAC) Support

- Market Size & Forecast by End-User

- Army & Land Forces

- Air Force & Aerospace Commands

- Naval Forces & Maritime Commands

- Special Operations Forces (SOF)

- Intelligence Agencies & Government Security Bodies

- Homeland Security & Border Patrol Agencies

- Market Size & Forecast by Sales Channel

- Direct Government-to-Government (G2G) Defense Procurement

- Prime Defense Contractor-Led Systems Integration & Delivery

- Foreign Military Sales (FMS) & Security Assistance Programs

- Research & Development (R&D) Contracts, SBIR/STTR & Defense Innovation Programs

- North America Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Defense AI & Autonomous Battlefield Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units, Systems & Platforms Deployed)

- By System Type

- By Technology

- By Platform

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- AI Algorithms, Machine Learning & Deep Learning Technology Deep-Dive

- Autonomous UAV, UCAV & UGV Propulsion, Navigation & Payload Technology

- Edge AI, Embedded Computing & Inference Processor Technology for Battlefield Platforms

- Swarm Intelligence, Multi-Agent Systems & Cooperative Autonomy Technology

- AI-Powered Sensor Fusion, ISR Platform & Target Acquisition Technology

- Electronic Warfare AI, Cyber Defense Automation & Directed Energy Technology

- Digital Twin, Simulation AI & Autonomous Mission Rehearsal Platform Technology

- Patent & IP Landscape in Defense AI & Autonomous Systems Technologies

- Value Chain & Supply Chain Analysis

- AI Software, Algorithm Development & Defense-Grade AI Platform Supply Chain

- Autonomous Platform Airframe, Hull & Chassis Manufacturing Supply Chain

- Sensor, Payload, Electro-Optical & Electronic Warfare Component Supply Chain

- Propulsion, Power Systems & Energy Storage Supply Chain for Autonomous Platforms

- Systems Integration, Prime Defense Contractor & OEM Procurement Landscape

- Defense Ministry, Government Procurement Agency & Military End-User Channel

- Maintenance, Repair, Overhaul (MRO) & Lifecycle Support

- Pricing Analysis

- Autonomous UAV, UCAV & UGV Platform Unit Cost & Life Cycle Cost Analysis

- AI Software, Algorithm Licensing & Defense-Grade AI Platform Pricing Analysis

- Sensor Suite, Payload & ISR System Capital and Integration Cost Analysis

- Electronic Warfare & Cyber Autonomous System Program Cost Analysis

- Defense AI Program Total Cost of Ownership (TCO) & Return on Investment (ROI) Analysis

- Autonomous System Procurement Contract, R&D Funding & Cost-Plus vs. Fixed-Price Structure Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Defense Autonomous Platforms: Carbon Footprint, Energy Consumption & Material Intensity

- AI Ethics, Responsible Autonomy & Human-Machine Teaming Sustainability Framework

- Environmental Impact of Defense Operations: Noise, Emissions & Battlefield Contamination from Autonomous Systems

- Circular Economy, Platform Refurbishment & End-of-Life Disposal for Defense AI Systems

- Regulatory-Driven Sustainability, SDG 16 (Peace & Justice) Alignment & Defense ESG Disclosure Frameworks

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Technology & Geography

- Player Classification

- Prime Defense Contractors & Full-Spectrum Autonomous Systems Integrators

- Specialist AI Software, Algorithm & Defense AI Platform Providers

- Autonomous UAV, UGV & Unmanned Maritime System Manufacturers

- Sensor, Electro-Optical, Payload & Electronic Warfare Component Suppliers

- Edge AI, Embedded Computing & Defense-Grade Processor Manufacturers

- Digital Twin, Simulation AI & Mission Planning Platform Providers

- Defense-Focused Technology Startups & Non-Traditional Defense Entrants

- Government-Owned Defense Research Institutes & National Laboratories

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Defense AI & Autonomous Systems Products & Technology Portfolio

- Key Customer Relationships & Reference Program Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Defense AI & Autonomous Systems Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Market Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)