Global Neuromorphic Computing Hardware Market By Component Type, By Neuron Technology, By Application, By End Use Industry, By Deployment Mode, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Neuromorphic Computing Hardware Market encompasses the design, fabrication, and commercial deployment of brain-inspired integrated circuits, spiking neural network processors, memristive devices, and supporting hardware architectures that replicate biological neural computation principles to deliver ultra-low power artificial intelligence inference, real-time sensory data processing, and adaptive learning capabilities, serving edge computing, robotics, autonomous systems, aerospace, healthcare, and defense applications requiring energy-efficient on-device intelligence beyond the performance boundaries of conventional von Neumann computing architectures.

Market Insights

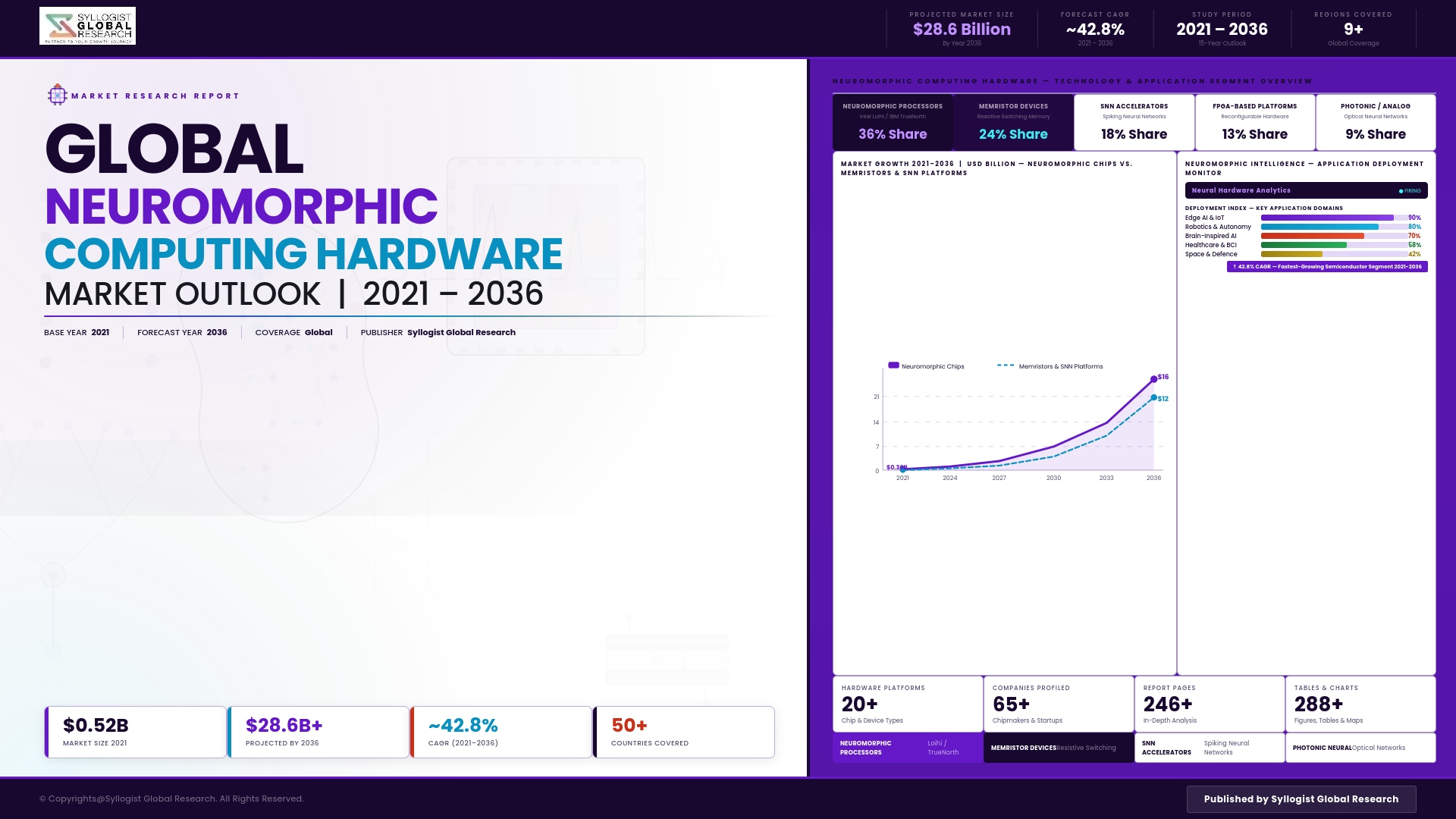

The global neuromorphic computing hardware market is transitioning from an academically driven research frontier into a commercially viable technology category, propelled by the unsustainable energy consumption trajectory of conventional artificial intelligence hardware, the explosive proliferation of edge intelligence requirements in autonomous systems and the Internet of Things, and a maturing ecosystem of neuromorphic chip architectures, spiking neural network software frameworks, and application-specific deployment use cases that are collectively advancing the technology from laboratory demonstration toward early commercial adoption. The market was valued at approximately USD 3.9 billion in 2025 and is projected to expand at a compound annual growth rate of 22.6% through 2034, as neuromorphic hardware transitions from a specialist research instrument into a production-deployable component for energy-constrained edge AI applications across robotics, autonomous vehicles, wearable health monitoring, smart sensors, and next-generation defense intelligence platforms.

The fundamental architectural distinction between neuromorphic processors and conventional graphics processing unit and tensor processing unit-based AI hardware lies in the event-driven, spike-based computation model of neuromorphic chips, which processes sensory input data only when meaningful changes occur rather than continuously, achieving orders-of-magnitude reductions in active power consumption that make neuromorphic architectures uniquely suited to battery-operated, thermally constrained, or energy-harvesting edge deployment environments where continuous always-on AI inference is required without the power delivery infrastructure supporting data center AI computation. Leading neuromorphic chip programs from major semiconductor developers and research institutions, including implementations based on phase-change memory, resistive random access memory, and complementary metal oxide semiconductor spiking neuron circuits, are demonstrating inference accuracy, latency, and energy efficiency combinations on standard sensory processing benchmarks that are increasingly competitive with conventional embedded AI processors in target application domains, advancing the technology readiness of commercial neuromorphic hardware platforms toward the specifications required by early adopter customers in robotics and autonomous perception applications.

The defense and aerospace sector is emerging as the most strategically significant near-term commercial adoption environment for neuromorphic computing hardware, driven by the operational imperatives of unmanned systems, battlefield edge intelligence, and space-based computing applications where size, weight, and power constraints are operationally decisive and the continuous power demands of conventional AI processors represent a fundamental operational limitation. Intelligence, surveillance, and reconnaissance applications requiring always-on multi-modal sensory fusion, target discrimination, and anomaly detection at the tactical edge represent a compelling performance-to-power requirement match for neuromorphic architectures that is generating active evaluation and prototype procurement investment among defense research organizations in the United States, United Kingdom, and key allied nations. Simultaneously, the consumer electronics and wearable health monitoring segments represent high-volume commercialization pathways for neuromorphic hardware in longer-horizon applications including always-on voice recognition, gesture detection, cardiac monitoring, and neurological condition tracking where millimeter-scale form factor and microwatt power consumption requirements are equally non-negotiable.

North America dominates the global neuromorphic computing hardware market, anchored by the concentration of semiconductor research and development investment, defense advanced research program funding, and technology company neuromorphic chip development programs across the United States, which hosts the largest ecosystem of neuromorphic hardware startups, academic research centers, and corporate research laboratories advancing the commercial readiness of next-generation brain-inspired computing platforms. Europe represents a significant research and early commercialization market, supported by coordinated funding through the European Union Human Brain Project and national semiconductor research programs in Germany, the Netherlands, and the United Kingdom. Asia-Pacific is the fastest-growing regional market, driven by substantial government-backed semiconductor and artificial intelligence research investment in China, Japan, and South Korea targeting neuromorphic computing as a strategic deep technology priority for long-term technology leadership.

Key Drivers

Exponential Growth in Edge AI Deployment and Unsustainable Power Consumption of Conventional AI Hardware Creating Structural Demand for Ultra-Low Power Neuromorphic Processing Architectures

The proliferation of artificial intelligence inference requirements at the network edge across autonomous vehicles, industrial robotics, smart surveillance systems, wearable devices, and Internet of Things sensor nodes is generating processing workloads that conventional embedded AI chips cannot serve efficiently within the power, thermal, and battery constraints governing edge hardware design, creating a compelling technology gap that neuromorphic computing architectures are uniquely positioned to address through their event-driven, spike-based computation model that consumes power only in proportion to input data activity rather than continuously. As edge AI deployment scales from millions to billions of connected intelligent devices requiring always-on inference capability, the cumulative energy efficiency advantage of neuromorphic hardware over conventional processor architectures represents an increasingly decisive competitive differentiator for device manufacturers optimizing system-level energy consumption and battery life.

Defense and Aerospace Sector Investment in Size, Weight, and Power-Optimized Edge Intelligence Creating High-Value Early Adoption Markets for Neuromorphic Computing Platforms

Military and aerospace applications impose the most stringent size, weight, and power requirements of any computing application domain, making neuromorphic architectures particularly compelling for unmanned aerial vehicle onboard processing, satellite-based intelligence analysis, soldier-worn sensor fusion systems, and undersea autonomous vehicle navigation, where operational mission duration, payload capacity constraints, and thermal management limitations make conventional graphics processing unit-based AI inference impractical. Defense research funding organizations in the United States and allied nations are channeling substantial investment into neuromorphic computing hardware development and evaluation, providing the market with high-value early procurement contracts that validate neuromorphic hardware platforms, generate application-specific performance benchmarking data, and establish defense qualification pathways that underpin longer-term commercial confidence in neuromorphic technology readiness.

Advances in Memristive and Phase-Change Memory Device Technology Enabling High-Density In-Memory Neuromorphic Computation That Overcomes the von Neumann Bottleneck Constraining Conventional AI Chips

Progress in resistive random access memory, phase-change memory, ferroelectric memory, and spin-transfer torque magnetic memory device technologies is enabling the construction of neuromorphic hardware architectures that store synaptic weight values directly within analog memory devices co-located with computation circuits, eliminating the energy and latency overhead of continuous data movement between separate processor and memory components that represents the fundamental inefficiency of conventional von Neumann computing architecture. These in-memory computing neuromorphic implementations are demonstrating synaptic density, weight precision, and endurance characteristics that are progressively approaching the specifications required for commercial deployment in pattern recognition, sensory classification, and temporal sequence learning applications, advancing the practical implementation feasibility of large-scale neuromorphic hardware systems beyond research prototype scale.

Key Challenges

Absence of Standardized Neuromorphic Programming Frameworks and Spiking Neural Network Training Tools Creating Software Ecosystem Fragmentation That Limits Developer Adoption and Application Deployment

The neuromorphic computing hardware ecosystem currently lacks the mature, standardized software development frameworks, spiking neural network training libraries, hardware abstraction layers, and application programming interfaces that have enabled the rapid developer ecosystem growth and widespread commercial adoption of conventional AI hardware platforms supported by well-established deep learning frameworks. Each major neuromorphic hardware platform currently requires application developers to learn proprietary programming models, specialized spiking neural network configuration tools, and hardware-specific optimization techniques that impose substantial development effort barriers, limit the portability of applications across different neuromorphic hardware implementations, and restrict the pool of developers capable of building production-ready neuromorphic applications to a small community of specialized researchers and engineers.

Difficulty Translating Conventional Deep Learning Models into Spiking Neural Network Equivalents Without Significant Accuracy Degradation Constraining the Breadth of Deployable Neuromorphic Applications

The dominant paradigm of contemporary artificial intelligence development is based on rate-coded deep neural network architectures trained through backpropagation on graphics processing unit clusters, and converting these trained conventional neural network models into temporally coded spiking neural network equivalents suitable for neuromorphic hardware execution currently involves accuracy trade-offs, temporal coding overhead, and network architecture transformation complexity that limits the performance achievable on neuromorphic hardware relative to the original conventional network benchmark across many practical application workloads. Training spiking neural networks from scratch using biologically plausible learning rules including spike-timing-dependent plasticity achieves superior neuromorphic hardware efficiency but requires specialized expertise, purpose-built training infrastructure, and substantially longer development cycles than conventional deep learning model development, restricting the range of application domains where neuromorphic hardware can currently deliver competitive inference accuracy.

Limited Fabrication Ecosystem Maturity and High Unit Cost of Advanced Neuromorphic Chip Architectures Constraining Volume Production Scalability and Commercial Deployment Economics

Neuromorphic chips incorporating analog memristive synaptic devices, three-dimensional integrated circuit stacking, and advanced spiking neuron circuit topologies require specialized semiconductor fabrication processes that are not fully supported by mainstream commercial foundry production lines optimized for conventional digital logic and memory manufacturing, resulting in limited production volume capacity, elevated per-unit manufacturing costs, and supply chain constraints that currently restrict the economic viability of neuromorphic hardware deployment to high-value defense, research, and premium edge applications where performance advantages justify premium pricing. The absence of sufficient commercial volume to drive the manufacturing learning curve cost reductions that have historically enabled semiconductor hardware transitions represents a circular constraint on neuromorphic market scaling that requires coordinated ecosystem investment to resolve.

Market Segmentation

- Segmentation By Component Type

- Neuromorphic Chips and Spiking Neural Network Processors

- Memristive and Phase-Change Memory Devices

- Neuromorphic Sensor and Transducer Interfaces

- Supporting Logic and Communication Hardware

- Development Boards and Evaluation Platforms

- Others

- Segmentation By Neuron Technology

- Complementary Metal Oxide Semiconductor Spiking Neurons

- Resistive Random Access Memory Synaptic Arrays

- Phase-Change Memory Neuromorphic Devices

- Ferroelectric and Spin-Torque Memory Synapses

- Photonic Neuromorphic Devices

- Others

- Segmentation By Application

- Image and Visual Pattern Recognition

- Acoustic and Speech Processing

- Sensory Fusion and Multi-Modal Perception

- Autonomous Navigation and Path Planning

- Anomaly Detection and Predictive Monitoring

- Natural Language and Temporal Sequence Processing

- Others

- Segmentation By End Use Industry

- Defense, Aerospace, and Intelligence

- Consumer Electronics and Wearable Devices

- Automotive and Autonomous Vehicles

- Industrial Robotics and Automation

- Healthcare and Medical Diagnostics

- Smart Infrastructure and Internet of Things

- Academic and Government Research

- Others

- Segmentation By Deployment Mode

- Edge and On-Device Deployment

- Embedded and Integrated System Deployment

- Cloud-Assisted Hybrid Neuromorphic Architectures

- Standalone Research and Development Systems

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global neuromorphic computing hardware market valuation in 2025, projected through 2034, segmented by component type, neuron technology, and end use industry, enabling semiconductor developers, defense procurement agencies, and technology investors to identify highest-growth technology categories and most strategically significant early adoption application opportunities across the neuromorphic hardware landscape?

- How do the energy efficiency, inference latency, and computational density performance characteristics of leading neuromorphic chip architectures compare against conventional embedded AI processors and graphics processing unit-based systems across target application benchmarks, and what performance thresholds must neuromorphic hardware achieve to displace incumbent solutions in autonomous vehicle, robotics, and wearable health monitoring applications?

- Which end use industry segments, specifically defense and aerospace, consumer electronics, industrial robotics, autonomous vehicles, and healthcare monitoring, represent the most commercially viable near-term adoption environments for neuromorphic computing hardware, and what application-specific performance requirements, procurement timelines, and technology qualification criteria are shaping neuromorphic hardware evaluation and adoption decisions in each segment?

- How is the competitive landscape structured among major semiconductor corporations, specialized neuromorphic chip startups, and government-funded research institutions developing commercial neuromorphic hardware platforms, and what intellectual property strategies, foundry partnerships, software ecosystem development investments, and application-specific product differentiation approaches are enabling leading competitors to establish defensible market positions?

- What software ecosystem development priorities, spiking neural network training framework standardization initiatives, hardware abstraction layer specifications, and developer toolchain investments are most critical to accelerating commercial application deployment on neuromorphic hardware platforms, and how are leading neuromorphic hardware developers and industry consortia addressing the software fragmentation challenge constraining broader developer adoption?

- How are advances in memristive device technology, three-dimensional chip integration, photonic neuromorphic architectures, and analog in-memory computing progressing toward the fabrication maturity, device endurance, and production cost levels required for volume commercial deployment, and which neuromorphic hardware technology platforms are most favorably positioned to achieve cost-competitive commercial production scale through 2034?

- Which regional markets, specifically North America, Europe, and Asia-Pacific, are generating the most significant government research funding, defense procurement investment, and commercial development activity in neuromorphic computing hardware, and how are national semiconductor strategy programs, artificial intelligence research funding priorities, and defense technology investment frameworks shaping the geographic distribution of neuromorphic hardware innovation and commercial leadership through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Immaturity, Scalability Limitation & Commercialisation Timeline Risk

- Semiconductor Fabrication Complexity, Yield Rate & Advanced Node Manufacturing Risk

- Talent Scarcity, Neuromorphic Programming Expertise & Ecosystem Readiness Risk

- Geopolitical Semiconductor Export Controls, Supply Chain Concentration & IP Security Risk

- Standards Fragmentation, Software Incompatibility & Customer Adoption Barrier Risk

- Regulatory Framework & Standards

- AI Hardware Export Control, Dual-Use Technology Classification & National Security Regulatory Frameworks

- Semiconductor Manufacturing, Advanced Node Process Control & Fab Safety Regulatory Standards

- AI Ethics, Responsible AI Hardware Design & Algorithmic Accountability Regulatory Frameworks

- Energy Efficiency Standards, Green Computing Directives & Data Centre Power Consumption Regulations

- Intellectual Property Protection, Patent Landscape & Open-Standard Initiatives for Neuromorphic Architectures

- Government-Funded Research, National AI Strategy & Neuromorphic Computing Programme Frameworks

- Global Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped & Billions of Neurons Deployed)

- Market Size & Forecast by Hardware Type

- Neuromorphic Processor Chips & Integrated Circuits

- Neuromorphic Development Boards & Evaluation Kits

- Neuromorphic Computing Systems & Server-Class Platforms

- Neuromorphic Sensor & Edge AI Modules

- Event-Driven Dynamic Vision Sensors (DVS) & Neuromorphic Cameras

- Neuromorphic Co-Processors & Accelerator Cards

- Hybrid Neuromorphic-Conventional Computing Platforms

- Market Size & Forecast by Architecture

- Spiking Neural Network (SNN) Hardware Architectures

- Memristive & Resistive RAM (ReRAM) Based Neuromorphic Architectures

- Phase-Change Memory (PCM) Based Neuromorphic Architectures

- Ferroelectric & FeFET-Based Neuromorphic Architectures

- Spintronic & Magnetic Tunnel Junction (MTJ) Based Neuromorphic Architectures

- Photonic & Optical Neuromorphic Architectures

- CMOS-Based Digital & Mixed-Signal Neuromorphic Architectures

- Market Size & Forecast by Memory Technology

- Resistive RAM (ReRAM) & Memristors

- Phase-Change Memory (PCM)

- Flash & Floating Gate Non-Volatile Memory

- SRAM & Embedded Memory for On-Chip Synaptic Storage

- Ferroelectric RAM (FeRAM) & Ferroelectric FET (FeFET)

- Market Size & Forecast by Neuron & Synapse Scale

- Small-Scale Devices (Up to 1 Million Neurons)

- Medium-Scale Devices (1 Million to 100 Million Neurons)

- Large-Scale Systems (100 Million to 1 Billion Neurons)

- Wafer-Scale & Extreme-Scale Neuromorphic Systems (Above 1 Billion Neurons)

- Market Size & Forecast by Application

- Edge AI Inference & Ultra-Low Power Embedded Intelligence

- Autonomous Robotics, Motor Control & Sensorimotor Processing

- Computer Vision, Object Recognition & Event-Based Imaging

- Natural Language Processing (NLP) & Speech Recognition at the Edge

- Brain-Machine Interface (BMI) & Neural Signal Processing

- Aerospace, Satellite & Defence Real-Time Signal Processing

- Smart Sensor Fusion, IoT & Industrial Predictive Maintenance

- Scientific Research, Brain Simulation & Computational Neuroscience

- Autonomous Vehicles & Advanced Driver Assistance Systems (ADAS)

- Market Size & Forecast by End-User

- Technology & Semiconductor Companies

- Defence, Aerospace & Government Agencies

- Healthcare, Neuroscience & Medical Device Companies

- Automotive & Autonomous Vehicle Manufacturers

- Industrial Automation & Robotics Companies

- Cloud, Data Centre & Hyperscale Computing Operators

- Research Universities & National Laboratories

- Market Size & Forecast by Sales Channel

- Direct OEM & Chip Manufacturer Sales

- Distributor & Electronic Component Channel

- Cloud-Based Neuromorphic Computing-as-a-Service (NCaaS) Channel

- Government & Defence Procurement Channel

- Academic & Research Institution Channel

- North America Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Neuromorphic Computing Hardware Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Billions of Neurons Deployed)

- By Hardware Type

- By Architecture

- By Memory Technology

- By Neuron & Synapse Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Sweden, Israel, China, Japan, South Korea, India, Australia, Singapore, Taiwan, Brazil, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Intel Loihi Architecture Deep-Dive: On-Chip Learning, Hierarchical Connectivity & Loihi 2 Advances

- IBM TrueNorth & Next-Generation IBM Neuromorphic Architecture: Design Philosophy, Scalability & Application Mapping

- SpiNNaker & SpiNNaker 2 Many-Core Neuromorphic Platform: Architecture, Real-Time Brain Simulation & Research Applications

- Memristive Crossbar Array Technology: Device Physics, Synaptic Plasticity Emulation & In-Memory Computing

- Photonic Neuromorphic Computing: Optical Spiking Neurons, Photonic Synapses & Ultra-Fast Signal Processing

- 3D Integration, Chiplet & Heterogeneous Packaging Technology for High-Density Neuromorphic Systems

- Neuromorphic Software Frameworks, Spiking Neural Network Compilers & Programming Toolchains

- Patent & IP Landscape in Neuromorphic Computing Hardware Technologies

- Value Chain & Supply Chain Analysis

- Advanced Semiconductor Wafer, Specialty Node & EUV Lithography Supply Chain

- Novel Memory Material, Memristive Device & Emerging Non-Volatile Memory Component Supply Chain

- Chip Design, EDA Tooling & IP Core Supply Chain for Neuromorphic Architectures

- Foundry, Packaging, Testing & Advanced Assembly Supply Chain

- PCB, Module Assembly, Cooling & System Integration Supply Chain

- Software, SDK, Neuromorphic OS & Application Framework Supply Chain

- OEM, System Integrator & Research Partner Channel

- Pricing Analysis

- Neuromorphic Chip & Processor Unit Price Analysis by Architecture & Scale

- Development Board, Evaluation Kit & Research Platform Pricing Analysis

- Neuromorphic System & Server-Class Platform Total Cost of Ownership (TCO) Analysis

- Cost per Synaptic Operation & Energy per Inference: Neuromorphic vs. GPU vs. CPU Cost-Performance Benchmarking

- Neuromorphic-Computing-as-a-Service (NCaaS) Cloud Pricing Model Analysis

- Price Roadmap: Impact of Volume Scale, Advanced Node Migration & Competing Memory Technologies

- Sustainability & Environmental Analysis

- Energy Efficiency Benchmarking: Neuromorphic Hardware vs. GPU, CPU & FPGA in Inference Workloads

- Carbon Footprint of Neuromorphic Chip Fabrication: Advanced Node Manufacturing, Process Gases & Water Use

- Role of Neuromorphic Computing in Reducing AI Energy Consumption & Data Centre Carbon Emissions

- Conflict Mineral Sourcing, Responsible Procurement & ESG Supply Chain Standards for Neuromorphic Hardware

- End-of-Life Electronics Recycling, WEEE Directive Compliance & Circular Economy for Neuromorphic Devices

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Hardware Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Hardware Type, Architecture & Geography

- Player Classification

- Large Semiconductor & Technology Companies with Neuromorphic Research Programmes

- Dedicated Neuromorphic Chip & Hardware Startups

- Academic Spin-Offs & University-Originated Neuromorphic Hardware Companies

- Defence & Aerospace Neuromorphic Computing Suppliers

- Edge AI & IoT Chip Companies with Neuromorphic-Inspired Architectures

- Cloud & Hyperscaler Companies Developing Proprietary Neuromorphic Silicon

- Competitive Analysis Frameworks

- Market Share Analysis by Hardware Type, Architecture & Region

- Company Profile

- Company Overview & Headquarters

- Neuromorphic Hardware Products & Technology Portfolio

- Key Customer Relationships & Reference Deployments

- Manufacturing Footprint & Foundry Partnerships

- Revenue (Neuromorphic Hardware Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Research Milestones, Contract Wins)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Hardware Type, Architecture, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output