Global Hyperlocal Delivery Platforms Market By Platform Type, By Delivery Category, By Business Model, By Technology, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Hyperlocal Delivery Platforms Market encompasses digital marketplace and logistics management platforms that connect consumers with local merchants, restaurants, grocery stores, pharmacies, and service providers to fulfill on-demand orders within a geographically constrained radius, typically two to ten kilometers, through crowdsourced or employed delivery partner networks, enabling real-time order placement, payment processing, delivery tracking, and merchant management for food delivery, quick-commerce grocery, pharmaceutical, and general merchandise categories across urban and suburban consumer markets globally.

Market Insights

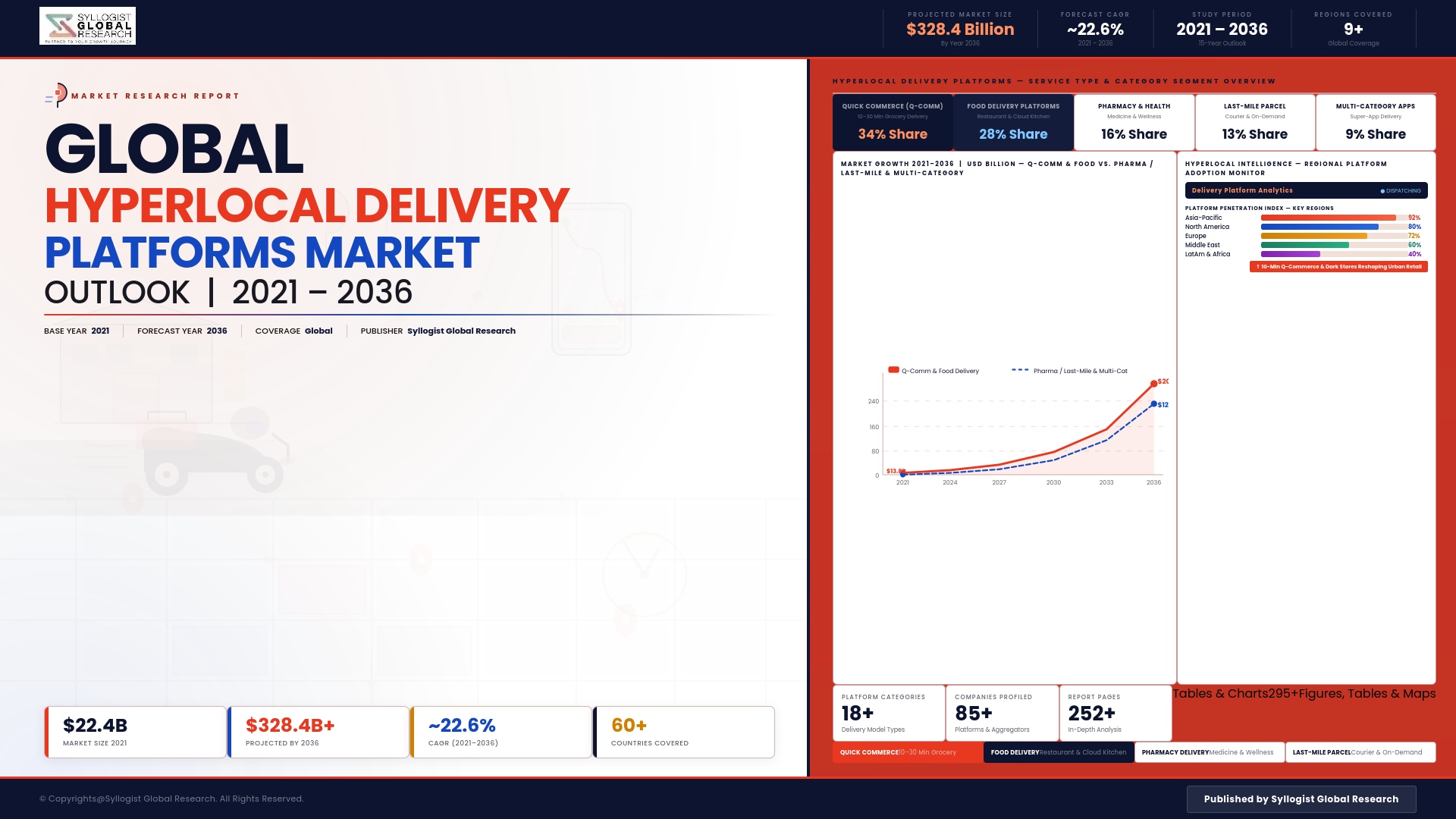

The global hyperlocal delivery platforms market is navigating a pivotal phase of business model consolidation and unit economic recalibration, as the extraordinary investment volumes deployed during the pandemic-era rapid expansion period have given way to a more disciplined operating environment characterized by investor pressure for profitability demonstration, geographic rationalization toward markets with sustainable order economics, and the strategic differentiation of surviving platforms through proprietary inventory positioning, advertising revenue diversification, and loyalty program depth that transforms on-demand delivery from a standalone logistics service into an integrated commerce and convenience ecosystem. The market was valued at approximately USD 142.8 billion in 2025 and is projected to advance at a compound annual growth rate of 12.6% through 2034, as structural growth in urban digital commerce adoption, expanding product category coverage beyond food and grocery into fashion, electronics, beauty, and home goods, and the maturing unit economics of established dense urban delivery networks create durable revenue expansion across the global hyperlocal delivery platform landscape despite the consolidation of operator count in most regional markets.

Food delivery remains the largest revenue category within the global hyperlocal delivery platform market, reflecting the combination of high order frequency, habitual re-purchase behavior, and strong consumer willingness to pay convenience premiums for restaurant meal delivery that have established food as the foundational commerce category upon which hyperlocal platform operator scale, rider network density, and technology infrastructure development have been built. However, the strategic significance of food delivery as a standalone category is evolving as leading platforms leverage their established rider networks, mobile consumer interfaces, and urban logistics infrastructure to expand into adjacent on-demand delivery categories including grocery quick-commerce, pharmaceutical delivery, alcohol and beverage delivery, and general merchandise fulfillment, creating bundled multi-category service propositions that increase consumer platform engagement frequency, improve order basket economics, and generate the cross-category data intelligence required for advanced personalization and targeted advertising capabilities. The quick-commerce grocery segment, characterized by ten-to-thirty minute grocery delivery from dark stores or local store partners, is registering the most dynamic growth trajectory within the category expansion portfolio, driven by the demonstrated consumer demand for convenient top-up grocery shopping occasions where immediate availability justifies premium delivery pricing relative to planned weekly shopping at lower-cost traditional grocery channels.

Platform monetization model evolution is a defining strategic development in the global hyperlocal delivery market, as established platforms progressively reduce their dependence on delivery fee and commission margin as primary revenue sources by developing high-margin advertising and sponsored listing revenue streams that leverage their position as high-frequency consumer commerce interfaces with valuable purchase intent data. Merchant advertising programs enabling restaurants and retailers to purchase promotional placement, targeted consumer reach, and sponsored category positioning within hyperlocal platform search and discovery interfaces are generating rapidly growing revenue contributions at margins substantially superior to delivery commission economics, transforming hyperlocal platforms from logistics service businesses into digital advertising platforms with logistics fulfillment capabilities. Subscription membership programs offering unlimited delivery, exclusive discounts, and priority service access to high-frequency users are simultaneously improving consumer retention, order frequency, and average basket value economics in ways that materially improve per-user lifetime value metrics and reduce the customer acquisition cost recovery timelines that have challenged platform unit economics in competitive multi-platform consumer markets.

Asia-Pacific dominates the global hyperlocal delivery platforms market by both gross merchandise value and platform operator diversity, anchored by the extraordinary scale and sophistication of hyperlocal delivery ecosystems in China and India, where leading platform operators have achieved multi-category super-app integrations combining food delivery, grocery, pharmaceutical, general merchandise, and financial services within unified consumer platforms that serve hundreds of millions of active users across tiered urban markets. Southeast Asia represents the fastest-growing regional sub-market within Asia-Pacific, driven by rapidly expanding smartphone internet penetration, urbanization, and the growing presence of well-capitalized regional platform operators expanding coverage across Indonesia, Vietnam, Thailand, the Philippines, and Malaysia. North America and Europe represent the second and third largest regional markets, characterized by dominant two-to-three platform competitive structures in most national markets where surviving operators have achieved sufficient urban market density to generate sustainable delivery network economics in core city markets.

Key Drivers

Structural Urbanization, Smartphone Commerce Adoption, and On-Demand Convenience Behavioral Normalization Sustaining Long-Term Consumer Demand Growth for Hyperlocal Delivery Services

The global concentration of consumer purchasing power and working-age population within increasingly dense urban agglomerations, combined with the ubiquitous smartphone internet access that makes on-demand ordering frictionless and the behavioral normalization of convenience commerce across demographic cohorts that fully embraced digital-first consumer behavior during the pandemic period, is generating durable structural growth in hyperlocal delivery demand that is not primarily dependent on continued platform promotional subsidies or below-cost delivery pricing to sustain consumer engagement. Younger urban consumer demographics who regard on-demand food and grocery delivery as a standard lifestyle infrastructure rather than an occasional premium service represent a growing share of urban household consumption, providing hyperlocal platforms with a structurally loyal user base whose lifetime platform engagement and order frequency provide the economic foundation for sustainable business model development.

Multi-Category Expansion Beyond Food Delivery Increasing Platform Engagement Frequency, Average Order Value, and Advertising Revenue Potential Across Consumer Commerce Occasions

The strategic expansion of hyperlocal delivery platforms from food-only propositions into grocery quick-commerce, pharmaceutical, alcohol, beauty, electronics, and general merchandise on-demand delivery is significantly increasing the number of consumer commerce occasions addressable through single platform relationships, elevating monthly active user engagement frequency, improving platform revenue per user metrics, and generating the multi-category purchase intent data that enables high-value targeted advertising capabilities attracting substantial merchant marketing investment. Platform operators who successfully position themselves as multi-category on-demand convenience hubs rather than single-category delivery services are achieving consumer retention, cross-selling economics, and advertising yield performance that creates fundamentally more sustainable and defensible business models than single-category food delivery competitors whose lower consumer engagement frequency limits monetization potential per active user.

Advertising Revenue Diversification and Merchant Services Expansion Creating High-Margin Revenue Streams That Improve Platform Unit Economics Beyond Delivery Commission Dependency

The development of high-margin digital advertising and merchant services revenue streams including sponsored product listings, banner advertising, loyalty program management, analytics and performance reporting, and commissioned financial services integrated within hyperlocal delivery platform interfaces is enabling established operators to achieve platform-level profitability metrics that pure delivery commission economics cannot sustain at competitive fee structures in mature multi-platform consumer markets. Merchant advertising programs leveraging the high purchase intent context and closed-loop conversion attribution capability of hyperlocal commerce interfaces are attracting growing restaurant, grocery, and consumer goods marketing budget allocation at cost-per-order and return-on-advertising-spend performance levels that outperform general digital advertising channels, creating a rapidly growing platform revenue category with structural margin advantages over logistics-dependent commission income.

Key Challenges

Delivery Partner Labor Classification Disputes, Gig Economy Regulation, and Employment Benefit Obligations Creating Structural Operating Cost Escalation Risk for Crowdsourced Delivery Models

The legal and regulatory status of crowdsourced delivery partners engaged as independent contractors rather than employees is subject to ongoing legislative challenge, court adjudication, and administrative rulemaking across the European Union, United Kingdom, United States, Australia, India, and other major hyperlocal platform markets, with regulatory determinations requiring gig delivery workers to be classified as employees carrying entitlement to minimum wage guarantees, social insurance contributions, paid leave, and other employment benefits imposing substantial per-delivery labor cost increases that directly erode the delivery cost economics upon which hyperlocal platform pricing structures and merchant commission rates have been calibrated. The geographic variability and ongoing uncertainty of gig worker classification regulatory outcomes makes structural labor cost planning particularly challenging for platform operators managing multi-market operations across jurisdictions with diverging and evolving employment law interpretations.

Hyperlocal Platform Market Saturation, Multi-Homing Consumer Behavior, and Intense Promotional Competition Constraining Average Revenue Per User Growth and Customer Acquisition Cost Recovery

In mature hyperlocal delivery markets including the United States, United Kingdom, Germany, and major Asian urban centers where two or more well-funded platform operators compete for consumer order share, multi-homing behavior enabling consumers to opportunistically switch between competing platforms based on promotional discount availability, restaurant selection, and delivery fee comparisons limits the platform loyalty and consumer lifetime value metrics that sustainable unit economics require, creating persistent pressure to maintain promotional investment at levels that delay the timeline for recovering customer acquisition costs through long-term order commission and advertising revenue streams. The high platform switching facilitation of app-store discovery and zero-friction account creation across competing hyperlocal platforms fundamentally constrains consumer retention without continuous promotional incentive maintenance.

Restaurant and Merchant Commission Rate Resistance, Platform Fee Regulation, and Disintermediation Risk Constraining Revenue Growth and Merchant Partnership Sustainability

Restaurant and retail merchant partners generating the transaction volume and product selection that make hyperlocal platforms valuable to consumers are subject to commission rates commonly ranging from fifteen to thirty percent of order value that compress merchant profitability on platform-mediated transactions and generate persistent commercial tension that is manifesting in regulatory commission cap legislation in multiple jurisdictions, organized merchant advocacy campaigns, and growing investment by restaurant chains and grocery operators in proprietary direct ordering applications and delivery capabilities that reduce platform dependency and commission cost exposure. The risk of significant merchant disintermediation from leading platforms reduces the sustainable commission rate ceiling and long-term gross merchandise value growth potential of hyperlocal delivery platform businesses in markets where merchant platform alternatives and regulatory commission caps materially constrain revenue extraction from the merchant supply side of the platform marketplace.

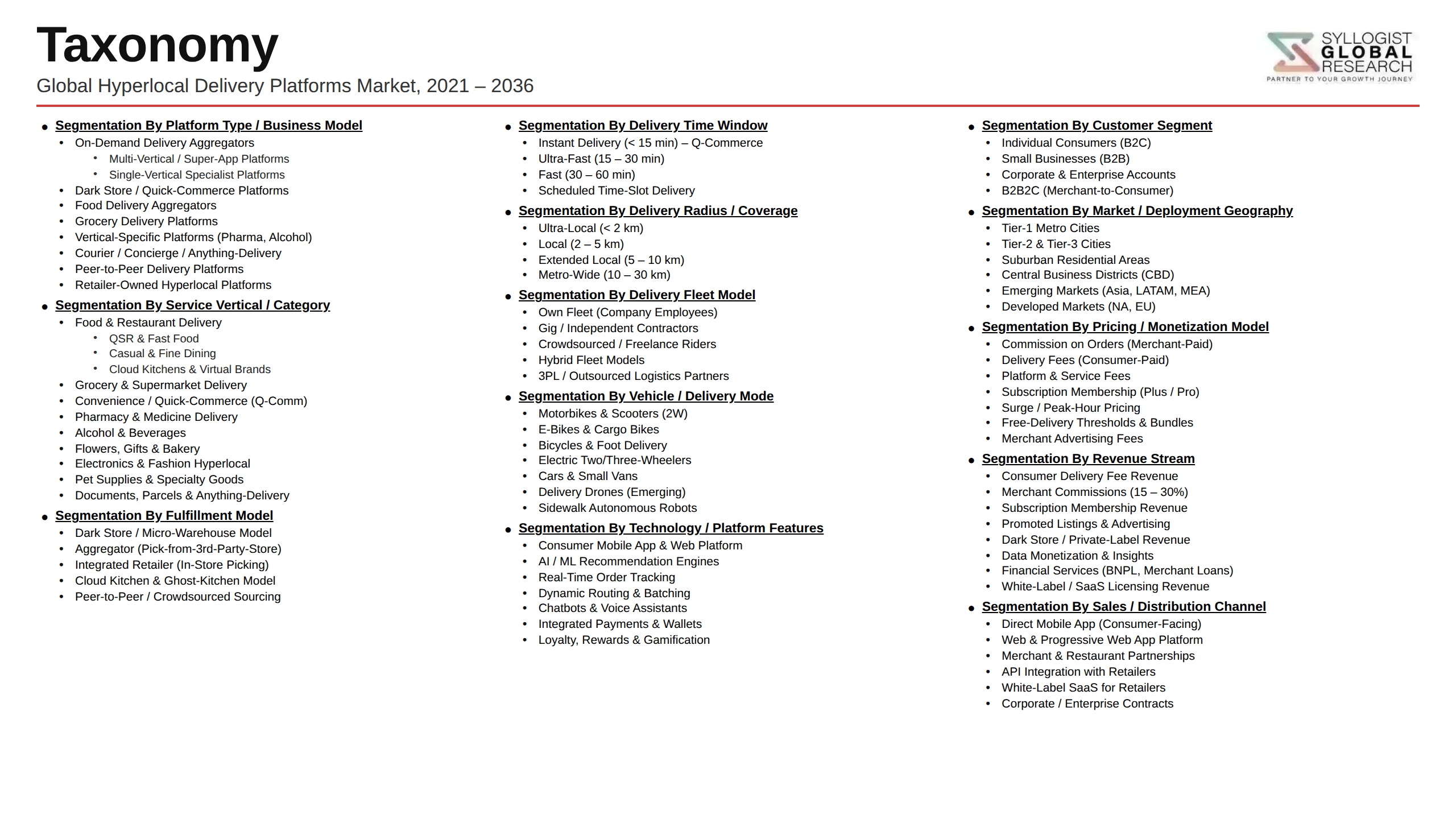

Market Segmentation

- Segmentation By Platform Type

- Food and Restaurant Delivery Platforms

- Quick-Commerce Grocery and Dark Store Platforms

- Multi-Category On-Demand Super-App Platforms

- Pharmaceutical and Healthcare Delivery Platforms

- Alcohol and Beverage Delivery Platforms

- General Merchandise On-Demand Platforms

- Others

- Segmentation By Delivery Category

- Restaurant and Prepared Food

- Grocery and Fresh Produce

- Pharmaceutical and Health Products

- Alcohol, Beverages, and Convenience Items

- Fashion, Beauty, and Personal Care

- Electronics and Consumer Goods

- Others

- Segmentation By Business Model

- Commission-Based Marketplace Models

- Subscription and Membership Revenue Models

- Advertising and Sponsored Listing Revenue Models

- First-Party Dark Store and Owned Inventory Models

- Hybrid Marketplace and Logistics Service Models

- Others

- Segmentation By Technology

- AI-Powered Demand Forecasting and Route Optimization

- Real-Time Order Tracking and Communication Systems

- Machine Learning Personalization and Recommendation

- Fraud Detection and Payment Security Platforms

- Merchant Analytics and Performance Reporting Tools

- Others

- Segmentation By End User

- Urban and Suburban Consumers

- Restaurant and Food Service Merchants

- Grocery Retailers and Supermarkets

- Pharmacies and Health Retailers

- Independent Retailers and Local Businesses

- Corporate and Enterprise Catering Clients

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global hyperlocal delivery platforms market valuation in 2025, projected through 2034, segmented by platform type, delivery category, and business model, enabling platform operators, merchant partners, investors, and technology suppliers to identify the highest-growth service categories and most commercially significant market expansion opportunities across the global hyperlocal delivery landscape?

- How are leading hyperlocal delivery platforms evolving their monetization models beyond food delivery commission dependence toward advertising, sponsored listings, subscription membership, financial services, and merchant analytics revenue streams, and what revenue mix diversification trajectories and platform-level profitability improvement milestones are commercially advanced operators demonstrating across major urban markets through 2034?

- Which multi-category expansion strategies, specifically quick-commerce grocery dark store operations, pharmaceutical on-demand delivery, alcohol delivery, and general merchandise integration, are generating the highest incremental platform revenue and consumer engagement frequency improvements among operators expanding beyond food delivery, and what supply chain, inventory positioning, and merchant partnership models are supporting category expansion viability?

- How is the competitive landscape structured among dominant global and regional hyperlocal delivery platform operators, super-app ecosystems with integrated on-demand delivery capabilities, and single-category specialist platforms, and what geographic expansion, merchant acquisition, consumer loyalty, technology differentiation, and multi-category integration strategies are enabling leading operators to consolidate market share in maturing competitive environments?

- What gig economy labor classification regulatory developments, employment status adjudications, minimum wage guarantee extensions, and social benefit obligation requirements in the European Union, United Kingdom, United States, Australia, and major Asian markets are most significantly affecting per-delivery labor cost structures, and how are hyperlocal delivery platforms adapting operating models, delivery partner engagement frameworks, and pricing structures to manage employment regulation compliance cost impacts?

- How are restaurant and retail merchant commission rate pressures, platform fee regulatory caps in New York, Berlin, and other major markets, and merchant direct-ordering app investment programs affecting the gross merchandise value growth potential, sustainable commission rate ceilings, and merchant partnership stability of leading hyperlocal delivery platforms, and what value-added merchant services are platforms developing to justify commission structures and reduce disintermediation risk?

- Which regional hyperlocal delivery markets, specifically Asia-Pacific, Latin America, and the Middle East and Africa, are expected to generate the highest incremental gross merchandise value growth through 2034, and what combinations of urbanization pace, smartphone commerce adoption, restaurant and grocery digitalization, consumer income growth, and platform operator investment and consolidation dynamics are defining market expansion trajectories and competitive positioning in each emerging regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Unit Economics Viability, High Delivery Cost & Path-to-Profitability Risk

- Gig Worker Retention, Courier Availability & Peak-Hour Capacity Constraint Risk

- Intense Platform Competition, Market Consolidation & Winner-Take-Most Dynamics Risk

- Customer Loyalty, Low Switching Cost & Multi-Homing Behaviour Risk

- Merchant Commission Resistance, Exclusivity Rejection & Disintermediation Risk

- Regulatory Action on Gig Economy, Platform Labour Classification & Pricing Restriction Risk

- Regulatory Framework & Standards

- Gig Worker & Delivery Courier Classification: AB5 (California), EU Platform Work Directive & Global Labour Law Frameworks

- Food Safety, Handling & Hygiene Standards for Restaurant & Grocery Delivery Platform Operations

- Urban Mobility Regulation: E-Bike, E-Moped, Cargo Bike & Two-Wheeler Last-Mile Delivery Access Frameworks

- Platform Antitrust, Market Dominance & Predatory Pricing Investigation Frameworks for Delivery Aggregators

- Data Privacy, GDPR, CCPA & Consumer Location Data Protection Standards for Hyperlocal Delivery Platforms

- Dynamic Pricing, Surge Fee Disclosure & Consumer Transparency Regulatory Frameworks for On-Demand Delivery

- Global Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Orders, GMV & Active Users)

- Market Size & Forecast by Platform Type

- Food & Restaurant Delivery Aggregator Platforms

- Quick Commerce (Q-Commerce) & Instant Grocery Delivery Platforms

- Hyperlocal Retail & General Merchandise Delivery Platforms

- Pharmacy & Healthcare Products Hyperlocal Delivery Platforms

- Alcohol, Beverages & Speciality Product Hyperlocal Delivery Platforms

- Flower, Gift & Occasion-Based Hyperlocal Delivery Platforms

- Multi-Category & Super-App Integrated Hyperlocal Delivery Platforms

- Market Size & Forecast by Business Model

- Platform Aggregator Model (Marketplace Connecting Merchants & Couriers)

- Vertically Integrated Model (Platform Owns Inventory, Dark Store & Courier Fleet)

- Hybrid Model (Aggregator with Own Inventory for Key Categories)

- White-Label & Logistics-as-a-Service (LaaS) Platform Model

- Social Commerce & Peer-to-Peer Hyperlocal Delivery Model

- Market Size & Forecast by Delivery Speed

- Ultra-Fast Delivery (Below 15 Minutes)

- Express Delivery (15 to 30 Minutes)

- Standard Hyperlocal Delivery (30 to 60 Minutes)

- Scheduled & Slotted Same-Day Delivery

- Market Size & Forecast by Technology

- AI & Machine Learning-Based Demand Forecasting & Dynamic Routing

- Geolocation, Mapping & Real-Time Tracking Technology

- Dark Store Operations, Robotics & Automated Picking Technology

- Dynamic Pricing, Surge Management & Revenue Optimisation Technology

- Customer App, Merchant App & Courier App Ecosystem Technology

- Conversational Commerce, Chatbot & WhatsApp-Based Ordering Technology

- Market Size & Forecast by Product Category

- Prepared Meals & Restaurant Food

- Grocery, Fresh Produce & Daily Essentials

- Pharmacy, Medicines & Health Products

- Alcohol, Beer, Wine & Beverages

- Consumer Electronics, Mobile Accessories & Small Appliances

- Fashion, Beauty, Personal Care & Lifestyle Products

- Pet Food, Supplies & Pet Care Products

- Market Size & Forecast by End-User

- Individual Consumers (B2C)

- Office, Corporate & Business Customers (B2B)

- Restaurants, Food Service & Cloud Kitchen Merchants

- Grocery Stores, Supermarkets & Convenience Retailers

- Pharmacy Chains & Healthcare Retailers

- Market Size & Forecast by Revenue Stream

- Delivery Fee & Service Charge from Consumers

- Commission from Merchant Partners & Restaurants

- Subscription & Loyalty Membership Revenue (Platform Pass & Prime Models)

- In-App Advertising, Sponsored Listings & Promotional Revenue

- Product Margin from Own Inventory & Dark Store Operations

- North America Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

- Europe Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

- Asia-Pacific Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

- Latin America Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

- Middle East & Africa Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

- Country-Wise* Hyperlocal Delivery Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Orders, GMV & Active Users)

- By Platform Type

- By Business Model

- By Delivery Speed

- By Technology

- By Product Category

- By End-User

- By Country

- By Revenue Stream

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Netherlands, Spain, Italy, Sweden, China, Japan, South Korea, India, Indonesia, Singapore, Australia, Brazil, Mexico, Colombia, Saudi Arabia, UAE, Turkey, South Africa, Nigeria

- Technology Landscape & Innovation Analysis

- Dark Store Technology Deep-Dive: Micro-Warehouse Design, Automated Picking Systems, Slotting Logic & Sub-10-Minute Fulfilment

- AI Route Optimisation & Multi-Order Batching Technology for Ultra-Fast & High-Density Urban Delivery Networks

- Conversational Commerce & Social Ordering Technology: WhatsApp, WeChat & Messaging App-Based Hyperlocal Delivery Flows

- Hyperlocal Demand Forecasting & AI-Based Real-Time Inventory Replenishment Technology for Dark Store Networks

- Dynamic Courier Pool Management, Gig Driver Allocation & Surge Prediction Technology

- Super App Integration Technology: Embedding Hyperlocal Delivery into Ride-Hailing, Fintech & Lifestyle App Ecosystems

- Loyalty, Gamification & Personalisation Technology for Customer Retention in Hyperlocal Delivery Platforms

- Patent & IP Landscape in Hyperlocal Delivery Platform Technologies

- Value Chain & Supply Chain Analysis

- Merchant & Restaurant Partner Onboarding, Catalogue Management & Integration Supply Chain

- Dark Store Inventory Procurement, Supplier Network & Replenishment Supply Chain

- Dark Store Real Estate, Fit-Out, Cold Chain Equipment & Facility Management Supply Chain

- Courier Recruitment, E-Bike/E-Moped Fleet Procurement & Maintenance Supply Chain

- Platform Technology, App Development, Cloud Infrastructure & AI Stack Supply Chain

- Packaging, Branded Bags, Cold Insulation & Delivery Material Supply Chain

- Payment Gateway, Fintech, Digital Wallet & Loyalty Infrastructure Supply Chain

- Pricing Analysis

- Delivery Fee & Service Charge Benchmarking by Platform, Market & Delivery Speed

- Merchant Commission Rate Analysis by Platform, Category & Market

- Full Cost-per-Order Analysis: Fulfilment, Courier Payout, Platform Overhead & Margin Structure

- Subscription Membership Pricing: Platform Pass, Loyalty Pass & Bundled Delivery Plan Analysis

- Customer Acquisition Cost (CAC), Lifetime Value (LTV) & LTV/CAC Ratio Analysis

- Path-to-Profitability Analysis: Order Density, AOV Threshold & Break-Even Economics for Hyperlocal Platforms

- Sustainability & Environmental Analysis

- Carbon Footprint of Hyperlocal Delivery: Emissions per Order Analysis by Delivery Mode, Distance & Urban Density

- E-Cargo Bike, E-Moped & Zero-Emission Fleet Adoption Pathway for Hyperlocal Delivery Decarbonisation

- Packaging Waste, Disposable Bag Reduction & Sustainable Packaging Initiatives in Hyperlocal Delivery

- Food Waste Reduction: Role of AI Demand Forecasting & Dark Store Inventory Management in Minimising Spoilage

- SDG 11 (Sustainable Cities), SDG 12 (Responsible Consumption) & ESG Reporting Standards for Hyperlocal Delivery Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Product Category & Geography

- Player Classification

- Global Multi-Market Food & Grocery Delivery Aggregator Platforms

- Regional & Local Hyperlocal Delivery Super Apps

- Pure-Play Q-Commerce & Ultra-Fast Grocery Delivery Platforms

- Retailer-Owned Hyperlocal Delivery Platforms

- White-Label & Logistics-as-a-Service (LaaS) Hyperlocal Technology Providers

- Social Commerce & Messaging App-Based Hyperlocal Delivery Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Product Category & Region

- Company Profile

- Company Overview & Headquarters

- Platform Products, Delivery Categories & Business Model Structure

- Key Merchant Partner Network & Restaurant Portfolio

- Active User Base, Monthly Orders & GMV

- Revenue (Hyperlocal Delivery Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Market Expansions, Product Launches, Funding Rounds)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Delivery Speed vs. Category Breadth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Business Model, Product Category, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Platform Product, Category Expansion & Business Model Strategy

- Technology Investment, AI & Dark Store Operational Excellence Strategy

- Geographic Expansion & New City Market Entry Strategy

- Merchant, Restaurant Partner & Supplier Engagement Strategy

- Partnership, M&A & Super App Ecosystem Integration Strategy

- Sustainability, Fleet Electrification & Green Delivery Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output