Global Smart Inventory Management Platforms Market By Solution Type, By Technology, By Deployment Mode, By End Use Industry, By Enterprise Size, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Smart Inventory Management Platforms Market encompasses cloud-based and on-premises software solutions that integrate AI-powered demand forecasting, real-time inventory tracking, automated replenishment, multi-location stock visibility, IoT sensor data ingestion, RFID and barcode scanning interfaces, supplier collaboration portals, and predictive analytics capabilities to optimize inventory levels, reduce carrying costs, minimize stockouts and overstock events, and synchronize supply chain replenishment across retail, manufacturing, healthcare, food and beverage, e-commerce, and distribution enterprise customers globally.

Market Insights

The global smart inventory management platforms market is experiencing a structural demand expansion driven by the growing recognition across retail, manufacturing, healthcare, and distribution industries that inventory mismanagement represents one of the largest and most recoverable sources of working capital inefficiency and customer service failure, and that the AI-powered demand sensing, real-time visibility, and automated replenishment capabilities of modern smart inventory platforms deliver measurable improvements in inventory turns, stockout rates, carrying cost reduction, and cash flow optimization that legacy ERP inventory modules and spreadsheet-based inventory management cannot replicate. The market was valued at approximately USD 4.8 billion in 2025 and is projected to expand at a compound annual growth rate of 17.3% through 2034, as the proliferation of multi-channel commerce creating omnichannel inventory complexity, the expansion of distributed fulfillment networks requiring real-time inventory visibility across dozens of nodes, and the growing deployment of IoT sensors and RFID infrastructure enabling continuous inventory position updates collectively elevate the data availability and operational urgency that justify enterprise investment in sophisticated smart inventory platforms beyond conventional periodic-cycle inventory management approaches.

AI-powered demand forecasting represents the highest commercial value capability within smart inventory management platforms, as the replacement of statistical time-series forecasting models with machine learning demand sensing algorithms that incorporate external signals including weather data, social media trend indicators, promotional calendar effects, competitive pricing intelligence, and macroeconomic variables alongside historical sales patterns delivers forecast accuracy improvements of twenty to forty percent relative to conventional methods that translate directly into proportional reductions in safety stock requirements, overstock write-down events, and lost sales from stockouts. The integration of demand forecast outputs with automated replenishment and supplier collaboration capabilities transforms demand signal improvement into operational inventory reduction outcomes by triggering purchase orders, production schedules, and distribution transfers in response to forecast changes without requiring manual buyer review of every SKU position, enabling inventory managers to focus analytical attention on exception management and strategic supplier relationships rather than routine reorder execution that automated systems can handle more consistently and responsively than human planning cycles allow.

Real-time inventory visibility across omnichannel retail networks, multi-warehouse distribution operations, and extended supply chain partner ecosystems is emerging as the most strategically significant capability differentiator in the smart inventory platform market, as the operational shift toward distributed inventory positioning across store backrooms, micro-fulfillment centers, regional distribution centers, and supplier-managed inventory locations creates a visibility challenge that only platforms with real-time IoT and RFID data integration, unified inventory ledger architecture, and multi-node allocation optimization can address at the speed and accuracy required for omnichannel order promising and dynamic inventory rebalancing decisions. Retail inventory shrinkage reduction through RFID-enabled real-time item-level visibility is generating particularly compelling return on investment evidence for smart inventory platform adoption in fashion and general merchandise retail, where the combination of shrinkage prevention, out-of-stock reduction, and receiving process accuracy improvements from RFID integration consistently deliver platform investment payback within one to two years of deployment, creating strong commercial justification for retail chain-wide smart inventory platform rollouts.

North America leads the global smart inventory management platforms market by revenue, reflecting the high technology adoption rates of United States and Canadian retail, manufacturing, and distribution enterprises, the concentration of enterprise software investment in supply chain optimization following the supply chain disruption experiences of recent years, and the mature venture and private equity investment ecosystem producing well-funded smart inventory platform developers serving mid-market and enterprise customer segments. Europe represents the second largest regional market, driven by the supply chain resilience investment agenda of European manufacturing corporations, the omnichannel retail transformation of major European grocery and general merchandise chains, and the healthcare supply chain compliance requirements generating pharmaceutical and medical device inventory management software investment. Asia-Pacific is the fastest-growing regional market, anchored by the enormous scale of Chinese e-commerce and manufacturing inventory management requirements, the rapid omnichannel retail digitalization of Indian and Southeast Asian retail sectors, and the growing demand for AI-powered inventory optimization among Japanese and South Korean manufacturers and distributors integrating smart inventory capabilities into digital supply chain transformation programs.

Key Drivers

Omnichannel Commerce Complexity and Distributed Inventory Network Expansion Creating Multi-Node Visibility and Real-Time Allocation Optimization Requirements Beyond Legacy ERP Inventory Capabilities

The transformation of retail fulfillment from centralized distribution center-to-store replenishment toward omnichannel inventory deployment across store networks, urban micro-fulfillment nodes, regional distribution centers, and direct-to-consumer shipping points is creating multi-location inventory visibility, real-time order promising, and dynamic stock rebalancing requirements that legacy ERP inventory management modules designed for single-location or two-tier distribution architectures cannot address at the location count, update frequency, and decision latency required for competitive omnichannel service delivery. Smart inventory platforms providing unified real-time inventory position across all nodes, AI-powered allocation optimization balancing fulfillment efficiency against inventory deployment cost, and automated transfer order generation to rebalance stock proactively before stockout events occur are enabling omnichannel retailers to simultaneously improve service levels, reduce total inventory investment, and optimize fulfillment cost across complex distributed networks.

Supply Chain Disruption Experience and Resilience Investment Agenda Elevating Inventory Visibility, Demand Sensing, and Supplier Collaboration Platform Adoption Across Manufacturing and Distribution Industries

The acute supply chain disruptions experienced across multiple industries during recent years exposed the catastrophic operational and financial consequences of inventory blind spots, demand signal latency, and supplier visibility gaps that conventional periodic inventory review and manual supply chain management processes generate under high-volatility conditions, creating a lasting organizational commitment among manufacturing, healthcare, and distribution enterprises to invest in smart inventory platforms providing continuous multi-tier supply chain visibility, early warning disruption detection, demand-supply scenario modeling, and automated safety stock adjustment capabilities. Chief supply chain officers and enterprise risk management programs are incorporating smart inventory platform capability investment as a core supply chain resilience strategy, generating sustained enterprise software budget allocation that is independent of the return on investment calculations governing normal discretionary technology expenditure.

IoT Sensor and RFID Infrastructure Maturation Enabling Continuous Real-Time Item-Level Inventory Tracking That Transforms Inventory Data Quality and Management Decision Speed

The progressive reduction in RFID tag and reader hardware costs, combined with the commercial availability of low-power IoT environmental sensors, smart shelf weight detection systems, and computer vision inventory scanning solutions, is enabling continuous item-level and case-level inventory position tracking across retail stores, warehouses, and distribution environments at infrastructure investment levels that generate positive return on investment through inventory accuracy improvement, shrinkage reduction, and receiving process automation. The richness and timeliness of inventory data generated by IoT and RFID infrastructure integration with smart inventory platforms fundamentally changes the operational decision-making capability available to inventory managers, enabling real-time replenishment trigger automation, exception-based management of inventory anomalies, and predictive analysis of stockout and overstock risk at the item and location level with lead times sufficient for proactive corrective action.

Key Challenges

Data Quality Deficiencies, Legacy System Integration Complexity, and Incomplete Inventory Master Data Limiting the Accuracy and Reliability of AI-Powered Forecasting and Optimization Outputs

The performance of AI-powered demand forecasting, automated replenishment, and inventory optimization capabilities within smart inventory platforms is fundamentally dependent on the quality, completeness, and timeliness of historical sales data, current inventory position data, product master data, and supplier lead time data that platform algorithms consume, and the endemic data quality problems characterizing legacy enterprise systems including incomplete transaction histories, inaccurate inventory counts from physical audit cycle gaps, inconsistent product attribute data, and unreliable supplier performance records create systematic biases and accuracy limitations in algorithmic outputs that can erode user confidence and limit the inventory reduction and service level improvements achievable relative to platform capability specifications. Addressing data quality prerequisites requires investment in data governance, cleansing, and integration programs that precede platform deployment and add timeline and cost complexity to implementation projects.

Change Management Resistance, Buyer and Planner Trust Barriers, and Organizational Adoption Challenges Limiting the Utilization of Smart Inventory Platform Automation Capabilities

The transition from experience-based manual inventory buying and planning practices to algorithm-driven automated replenishment recommendations requires inventory management professionals to develop trust in AI forecast outputs and automated purchasing decisions that initially appear counterintuitive when compared against buyer intuition and historical practice patterns, creating change management challenges that slow the organizational adoption of smart inventory platform automation capabilities and limit the inventory optimization benefits achievable when users systematically override algorithm recommendations based on personal judgment rather than exception-justified business logic. Building algorithmic transparency, providing buyers with meaningful override controls and decision explanation tools, and demonstrating forecast accuracy performance relative to human judgment consistently are critical change management investments required to achieve the full automation utilization rates that justify smart inventory platform investment economics.

Vendor Landscape Fragmentation, Platform Integration Proliferation Risk, and Enterprise Procurement Complexity in a Market with Numerous Specialized Point Solution Competitors

The smart inventory management platform market encompasses a wide range of point solution providers specializing in specific capabilities including demand forecasting, RFID-based real-time tracking, supplier collaboration portals, warehouse inventory optimization, and retail shelf inventory management, creating procurement evaluation complexity for enterprise buyers seeking comprehensive inventory management capability who must either select a broad platform accepting performance trade-offs across individual capability areas or implement a multi-vendor technology stack managing integration complexity, data synchronization overhead, and vendor relationship management across multiple contracts. The integration of multiple specialized inventory management tools with existing ERP, warehouse management, and order management systems creates technical debt and maintenance burden that adds ongoing cost and performance risk to enterprise inventory management technology architectures built on numerous point solution integrations.

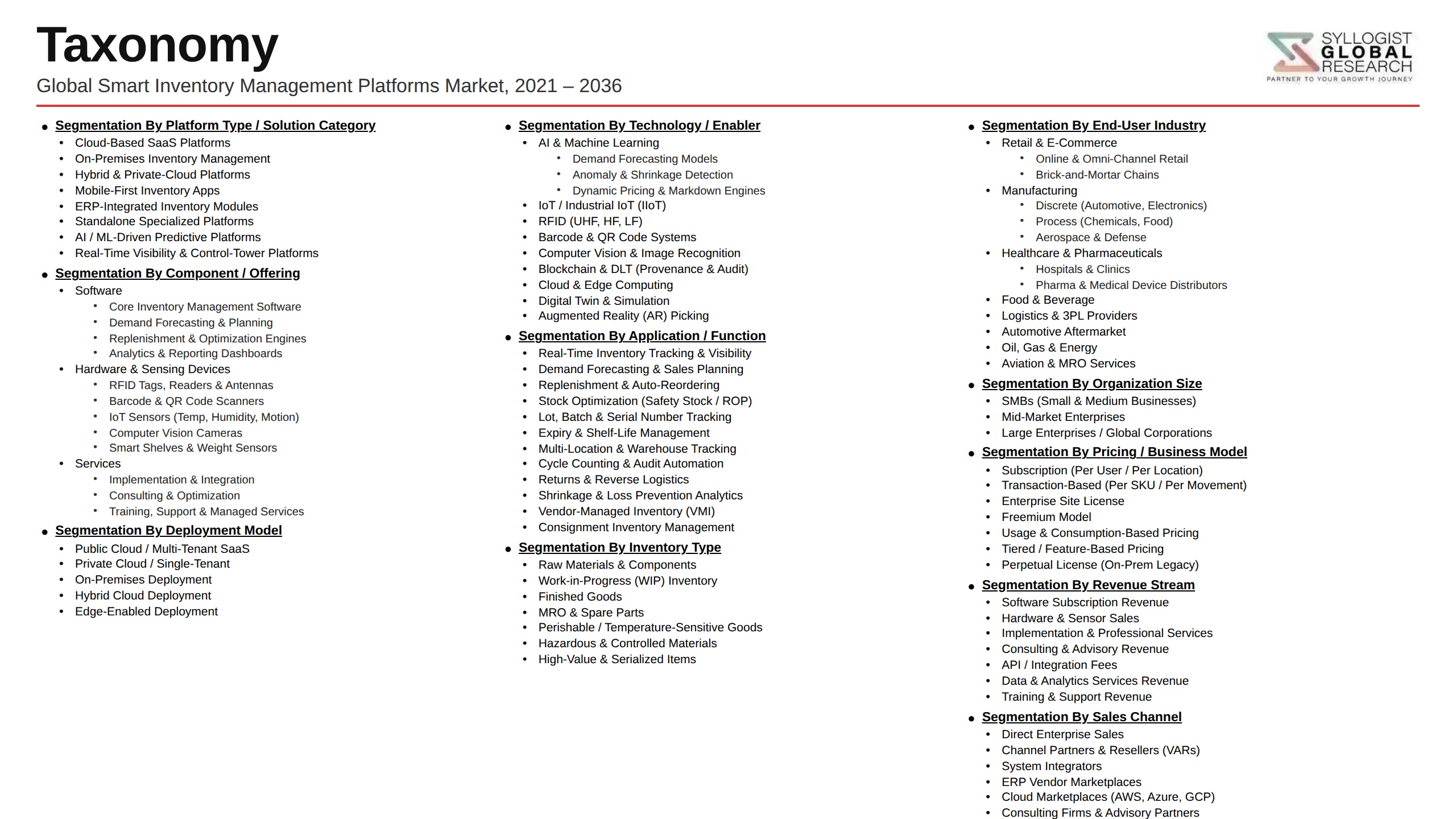

Market Segmentation

- Segmentation By Solution Type

- AI-Powered Demand Forecasting and Planning Platforms

- Real-Time Multi-Location Inventory Visibility Systems

- Automated Replenishment and Purchase Order Management

- RFID and IoT-Integrated Inventory Tracking Platforms

- Supplier Collaboration and Vendor-Managed Inventory Portals

- Inventory Analytics and Reporting Platforms

- Others

- Segmentation By Technology

- Artificial Intelligence and Machine Learning

- RFID and Near-Field Communication Tracking

- IoT Sensors and Smart Shelf Systems

- Blockchain and Distributed Ledger Traceability

- Computer Vision and Automated Scanning

- Cloud Integration and API Connectivity Platforms

- Others

- Segmentation By Deployment Mode

- Cloud-Based and SaaS Platforms

- On-Premises Enterprise Deployments

- Hybrid Cloud and On-Premises Architectures

- Mobile-First and Edge-Computing Deployments

- Segmentation By End Use Industry

- Retail and Omnichannel Commerce

- Manufacturing and Industrial Operations

- Food, Grocery, and Beverage Distribution

- Pharmaceutical and Healthcare

- E-Commerce and Third-Party Logistics

- Consumer Electronics and Technology

- Automotive and Spare Parts Distribution

- Others

- Segmentation By Enterprise Size

- Large Enterprises (Above USD 1 Billion Revenue)

- Mid-Market Enterprises (USD 100 Million to USD 1 Billion Revenue)

- Small and Medium Enterprises (Below USD 100 Million Revenue)

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global smart inventory management platforms market valuation in 2025, projected through 2034, segmented by solution type, technology, and end use industry, enabling platform vendors, enterprise software investors, and supply chain technology buyers to identify the highest-growth capability categories and most commercially significant inventory platform adoption opportunities across the global market?

- How are AI-powered demand forecasting algorithms, real-time multi-node inventory visibility architectures, and automated replenishment systems combining to deliver measurable inventory optimization outcomes, and what forecast accuracy improvements, inventory turn increases, stockout rate reductions, and working capital release are commercially deployed smart inventory platforms demonstrating in verified enterprise customer implementations across retail, manufacturing, and distribution sectors?

- Which smart inventory platform capability segments, specifically omnichannel inventory allocation optimization, RFID real-time item-level tracking, AI demand sensing with external signal integration, and supplier collaboration portals, are generating the highest enterprise procurement investment and fastest adoption growth through 2034, and what return on investment evidence and deployment scale economics are most compelling to enterprise procurement decision-makers?

- How is the competitive landscape structured among broad supply chain platform vendors with embedded inventory management modules, specialized smart inventory platform developers, RFID and IoT solution providers with inventory analytics capabilities, and ERP vendors expanding AI inventory optimization functionality, and what differentiation strategies, partner ecosystem development, and customer success program investment are enabling specialist platforms to compete against embedded ERP alternatives?

- What data quality prerequisites, inventory master data governance requirements, legacy ERP integration complexity challenges, and organizational change management investments are most critically determining the timeline and ultimate performance outcome of smart inventory platform implementations, and what implementation methodology innovations, pre-built ERP connectors, and data quality assessment frameworks are platform vendors developing to reduce deployment risk and accelerate time-to-value?

- How are IoT sensor, smart shelf, computer vision scanning, and RFID infrastructure cost reductions enabling continuous real-time item-level inventory tracking at commercially viable total investment levels across retail, pharmaceutical, and distribution warehouse environments, and what combination of shrinkage reduction, receiving process improvement, out-of-stock prevention, and safety stock reduction outcomes are justifying RFID integration investment payback in different industry deployment contexts?

- Which regional smart inventory platform markets, specifically North America, Asia-Pacific, and Europe, are expected to generate the highest incremental software investment growth through 2034, and what combinations of omnichannel retail transformation, manufacturing supply chain resilience investment, healthcare inventory compliance requirements, e-commerce distribution automation, and enterprise digital transformation program maturity are defining regional market growth trajectories and competitive dynamics?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Quality, Inventory Master Data & Integration Complexity Risk

- AI Forecast Accuracy, Demand Volatility & Predictive Model Risk

- Cybersecurity, Data Breach & Inventory Information Leakage Risk

- Customer Adoption, Change Management & User Training Risk

- Capital Investment, Subscription Churn & Unit Economics Risk

- Regulatory Framework & Standards

- Data Privacy (GDPR, CCPA) & Customer Information Protection Frameworks

- Pharmaceutical Serialisation, GDP, FDA DSCSA & EU FMD Compliance Standards

- Food Safety, Lot Traceability, FSMA & Cold Chain Recordkeeping Standards

- Hazardous Material, ITAR & Restricted Inventory Reporting Regulations

- Green Finance, ESG Disclosure & Sustainable Supply Chain Procurement Standards

- Global Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Active Deployments and SKUs Managed)

- Market Size & Forecast by Solution Type

- Inventory Tracking, Real-Time Visibility & Asset Location Modules

- AI Demand Forecasting & Automated Replenishment Modules

- Warehouse Management, Slotting & Pick Path Optimisation Modules

- Order Management, Fulfilment Orchestration & Distributed OMS Modules

- Supply Chain Visibility, Supplier Collaboration & In-Transit Tracking

- Returns Management & Reverse Logistics Modules

- Inventory Analytics, BI Dashboards & ABC/XYZ Reporting Modules

- Loss Prevention, Shrinkage Detection & Compliance Tracking Modules

- Specialty Modules (Cold Chain, Serialised, Hazmat & Consignment Inventory)

- Market Size & Forecast by Technology

- Cloud-Native SaaS & Multi-Tenant Architecture Technology

- Artificial Intelligence, Machine Learning & Predictive Analytics Technology

- IoT Sensor, RFID & Real-Time Location System (RTLS) Technology

- Computer Vision, Camera-Based Inventory & Shelf Detection Technology

- Digital Twin, Warehouse Simulation & Virtual Inventory Technology

- Blockchain, Lot/Batch Traceability & Provenance Technology

- Edge Computing, 5G & Low-Latency Inventory Network Technology

- Robotics Integration (AMR, AGV & ASRS) & Warehouse Automation Technology

- Generative AI, Demand Sensing & Operator Support Agent Technology

- Market Size & Forecast by Output Type

- Real-Time Inventory Visibility & Stock Position Output

- Demand Forecast, Replenishment Order & Safety Stock Output

- Order Fulfilment, Pick-Pack-Ship Workflow Output

- Compliance, Traceability & Audit-Ready Reporting Output

- Loss, Shrinkage & Aging Inventory Detection Output

- Market Size & Forecast by Deployment Scale

- Enterprise & Multi-Site Deployment (Above 100,000 SKUs Managed)

- Mid-Market Deployment (10,000 to 100,000 SKUs Managed)

- Small Business & Single-Site Deployment (Below 10,000 SKUs Managed)

- Market Size & Forecast by Application

- Retail, Brick-and-Mortar & Specialty Store Operations

- E-Commerce, Omnichannel & Direct-to-Consumer Operations

- Manufacturing, Production & Work-in-Progress (WIP) Inventory

- Wholesale, Distribution & B2B Trade Operations

- Logistics, Third-Party Logistics (3PL) & Fulfilment Centre Operations

- Healthcare, Pharmacy & Pharmaceutical Inventory

- Food, Beverage, Cold Chain & Quick-Service Restaurant Operations

- Market Size & Forecast by End-User

- Retailer, Specialty Brand & Department Store

- E-Commerce, Omnichannel & Direct-to-Consumer Company

- Manufacturer & Industrial Enterprise

- Wholesaler, Distributor & B2B Trader

- 3PL, Fulfilment Centre & Healthcare/Pharmacy Operator

- Market Size & Forecast by Sales Channel

- Direct Enterprise Sales & Subscription Licensing

- Channel Partner, Value-Added Reseller (VAR) & System Integrator Network

- Cloud Marketplace (AWS, Azure, GCP) & Embedded Distribution

- Consulting, Custom Implementation & Managed Service Engagement

- North America Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Smart Inventory Management Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Active Deployments and SKUs Managed)

- By Solution Type

- By Technology

- By Output Type

- By Deployment Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- AI Demand Forecasting, Predictive Analytics & Replenishment Engine Deep-Dive

- Computer Vision, Shelf Detection & Camera-Based Inventory Technology

- IoT, RFID & Real-Time Location System (RTLS) Technology

- Warehouse Robotics (AMR, AGV & ASRS) Integration & Orchestration Technology

- Digital Twin, Warehouse Simulation & Virtual Inventory Technology

- Blockchain, Lot/Batch Traceability & Provenance Verification Technology

- Generative AI, Demand Sensing & Conversational Operator Support Technology

- Patent & IP Landscape in Smart Inventory Management Platform Technologies

- Value Chain & Supply Chain Analysis

- Cloud Infrastructure, AI Compute & SaaS Hosting Supply Chain

- IoT Sensor, RFID Tag & Camera Hardware Manufacturing Supply Chain

- ERP, WMS & Supply Chain Software Integration Partner Supply Chain

- Channel Partner, Value-Added Reseller & System Integrator Network

- Retail, Manufacturing, 3PL & Distribution End-User Procurement Landscape

- Marketplace (Cloud, App Store & Industry Marketplace) Distribution Channel

- Implementation, Training, Managed Service & Support Ecosystem

- Pricing Analysis

- Per-Seat & Per-User Subscription Pricing Analysis

- Per-SKU & Inventory Volume-Based Pricing Analysis

- Module-Based & Bundled Suite Pricing Structure Analysis

- Enterprise Licensing, Custom Contract & Volume Discount Pricing Analysis

- Implementation, Customisation & Professional Services Pricing Analysis

- Total Smart Inventory Platform Cost Economics: Cost per SKU & Customer Lifetime Value Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Smart Inventory Platforms: Carbon Footprint, Energy Intensity & Compute Footprint Across Cloud Architecture Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Sustainable Inventory Operations, Reduced Stock-Outs and Circular Returns Management

- Responsible Data Use, Customer Privacy & Worker Surveillance Due Diligence

- Environmental Compliance, E-Waste Reduction & Sustainable Packaging Inventory Consideration

- Regulatory-Driven Sustainability, GDPR, SDG 9 (Industry Innovation) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Solution Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Solution Type, Technology & Geography

- Player Classification

- Integrated Enterprise Software & Supply Chain Management Vendors

- Specialist Smart Inventory & Warehouse Management Platform Providers

- AI Demand Forecasting & Replenishment Optimisation Vendors

- Computer Vision, RFID & IoT Asset Tracking Solution Providers

- Robotics, AMR & Warehouse Automation Software Vendors

- Cloud-Native SaaS & Vertical-Specific Inventory Platform Innovators

- E-Commerce, Omnichannel & Distributed Order Management Specialists

- Implementation Partner, System Integrator & Consulting Service Specialist

- Competitive Analysis Frameworks

- Market Share Analysis by Solution Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Smart Inventory Management Platform Products & Technology Portfolio

- Key Customer Relationships & Reference Enterprise Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Smart Inventory Management Platform Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Solution Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output