Global Data Lake and Data Platform Market By Platform Type, By Deployment Mode, By Component, By Data Type, By End Use Industry, By Enterprise Size, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Data Lake and Data Platform Market encompasses the design, deployment, and commercial licensing of centralized and distributed data storage, ingestion, cataloging, governance, and analytics infrastructure that enables enterprises to collect, retain, and analyze structured, semi-structured, and unstructured data at scale, including cloud-based data lakes, data lakehouses, data meshes, data warehouses, real-time streaming data platforms, data catalog and lineage management tools, and unified analytics environments, procured by technology companies, financial institutions, healthcare systems, retailers, manufacturers, and government agencies globally.

Market Insights

The global data lake and data platform market is undergoing a fundamental architectural evolution that is simultaneously expanding its addressable enterprise application scope, compressing time-to-insight for data consumers across the organization, and reshaping the competitive landscape between established cloud hyperscaler data platforms and specialized data lakehouse, data mesh, and real-time streaming architecture providers. The market was valued at approximately USD 18.2 billion in 2025 and is projected to expand at a compound annual growth rate of 19.6% through 2034, as the exponential growth of enterprise data volumes from IoT sensors, digital customer interactions, operational systems, and external data sources creates storage, processing, and governance infrastructure requirements that traditional data warehousing and on-premises analytics environments cannot cost-effectively scale to address, compelling broad-based enterprise migration to cloud-native data platform architectures that offer virtually unlimited storage elasticity, serverless compute scalability, and integrated machine learning and AI analytics capabilities.

The data lakehouse architecture, which combines the cost-effective storage scalability and multi-format data ingestion flexibility of data lakes with the ACID transaction support, schema enforcement, and query performance optimization capabilities previously exclusive to structured data warehouses, is emerging as the dominant architectural framework for enterprise data platform modernization, displacing the historically common two-tier architecture of separate data lake and data warehouse systems with a unified platform layer that eliminates data duplication, reduces ETL pipeline complexity, and enables a broader range of analytical workloads including business intelligence, machine learning, and real-time operational analytics from a single integrated data storage and compute environment. Major cloud hyperscalers have each converged on proprietary data lakehouse implementations that serve as the foundational data platform offering within their cloud ecosystems, creating a competitive landscape where platform architecture preference is increasingly intertwined with broader cloud provider strategy decisions and where switching costs between competing data lakehouse implementations are non-trivial for organizations with established data pipelines, transformation logic, and analytical workload configurations developed against specific platform APIs and query engines.

Generative AI and large language model application development is creating a qualitatively new category of data platform demand, as enterprises building internal AI applications, retrieval-augmented generation systems, and AI agent workflows require unified data platform infrastructure that can simultaneously serve vector database retrieval for semantic search, structured data querying for factual grounding, and real-time event streaming for situational awareness in ways that conventional data lake architectures were not designed to support in integrated fashion. The governance, lineage, and security requirements of AI training data management, model versioning, and responsible AI deployment are simultaneously driving investment in data catalog, data quality, and active metadata management capabilities that were previously treated as supplementary features but are becoming core platform requirements for enterprises managing AI development and deployment workflows at scale. The growing strategic importance of data sharing and monetization is driving enterprise investment in data marketplace and data clean room infrastructure that enables controlled sharing of proprietary datasets with partners, advertisers, and research collaborators under privacy-preserving protocols, creating commercially valuable data products from previously siloed enterprise data assets.

North America dominates the global data lake and data platform market, anchored by the concentration of technology-intensive enterprises, the maturity of cloud computing adoption, the density of data engineering and analytics talent, and the scale of AI and machine learning application development investment among United States and Canadian financial services, technology, retail, and healthcare enterprises that collectively represent the world’s most sophisticated and highest-spending enterprise data infrastructure market. Europe represents the second largest regional market, shaped by the dual forces of expanding data platform investment for analytics and AI applications and the stringent data sovereignty, residency, and processing governance requirements of the General Data Protection Regulation and national data protection frameworks that influence platform architecture selection, cloud provider regional deployment decisions, and data governance tool investment. Asia-Pacific is the fastest-growing regional market, driven by the extraordinary scale of data generation from Chinese internet and manufacturing ecosystems, the rapidly expanding data platform investment of Japanese, South Korean, and Australian enterprises, and the accelerating cloud adoption and AI application development investment across Southeast Asian digital economy companies.

Key Drivers

Exponential Enterprise Data Volume Growth and Multi-Source Data Integration Requirements Compelling Migration from Legacy Data Warehouses to Scalable Cloud-Native Data Lake and Lakehouse Platforms

The accelerating accumulation of enterprise data from IoT device telemetry, digital customer interaction logs, machine-generated operational events, social media feeds, and third-party data provider streams is generating data volumes and ingestion velocity requirements that on-premises data warehouse and ETL infrastructure cannot cost-effectively scale to accommodate, compelling enterprises to migrate to cloud-native data lake and lakehouse architectures that provide petabyte-scale storage at dramatically lower cost per gigabyte, elastic compute provisioning for variable analytical workload demands, and native support for unstructured data formats including text, images, video, and binary files that conventional relational warehouse architectures cannot store and query efficiently. The transition from periodic batch data processing to continuous stream ingestion and real-time analytical query capabilities is simultaneously driving adoption of streaming data platform components that extend cloud data lake investments with low-latency event processing infrastructure.

Enterprise AI and Machine Learning Application Development Creating New Data Platform Infrastructure Requirements for Training Data Management, Feature Stores, and Vector Database Integration

The broad-based enterprise commitment to AI and machine learning application development across customer service, fraud detection, demand forecasting, predictive maintenance, and generative AI use cases is creating data platform infrastructure requirements that extend well beyond the business intelligence and reporting workloads that traditional data warehouse architectures were designed to serve, driving investment in unified data lakehouse environments capable of supporting ML training data versioning, feature store management, model experiment tracking, and vector embedding storage for retrieval-augmented generation applications within a single integrated data fabric. The governance, quality, and lineage management requirements of AI training data curation are simultaneously elevating investment in active data catalog, data quality monitoring, and metadata management platforms that provide the data observability and AI model traceability capabilities that responsible AI governance frameworks require.

Data Democratization Initiatives and Self-Service Analytics Adoption Driving Investment in Data Mesh, Data Catalog, and Governed Data Sharing Infrastructure Across Large Enterprise Organizations

The growing recognition that centralized data engineering teams cannot scale to meet the analytical data preparation and delivery requirements of every business domain within large enterprises is driving adoption of data mesh architectures that distribute data ownership, production, and governance responsibilities to domain-aligned product teams while providing central platform infrastructure for interoperability, security enforcement, and cross-domain data discovery through shared data catalogs. Enterprise investment in self-service analytics enablement, including semantic layer development, natural language query interfaces, automated data preparation tools, and governed data product marketplaces that make trusted data assets discoverable and accessible to business analysts and data scientists without requiring central data engineering intervention, is expanding the active user base and organizational value delivered by enterprise data platform investments beyond the specialist data engineering and analytics teams that historically constituted the primary platform user population.

Key Challenges

Data Governance Complexity, Data Quality Degradation, and Ungoverned Data Lake Proliferation Creating Analytical Unreliability and Regulatory Compliance Risk in Enterprise Data Environments

The scalability and low ingestion friction of data lake architectures that make them attractive for broad enterprise data consolidation simultaneously create governance challenges when inadequate data cataloging, quality monitoring, ownership definition, and access control enforcement allow data lakes to evolve into ungoverned repositories where undocumented, duplicated, stale, and poorly understood datasets reduce analytical reliability and erode user confidence in platform-derived insights, a failure mode sometimes characterized as data swamp formation. Enterprise data governance programs establishing data domain ownership, implementing automated data quality scoring, enforcing data classification and access policy frameworks, and maintaining active metadata catalogs that provide business-readable dataset documentation are critical investments required to maintain data lake analytical value at scale, yet their implementation requires sustained organizational discipline and technical investment that competes with data ingestion and analytical application development priorities for data engineering resource allocation.

Cloud Data Platform Cost Management Complexity and Unpredictable Compute Spend Creating Budget Overrun Risk for Organizations Without Rigorous FinOps Disciplines

The consumption-based pricing models of cloud data lakehouse and analytics platforms, where compute costs are incurred per query, per data processing job, and per storage gigabyte at rates that scale with data volume growth and query complexity increases, create enterprise technology budget management challenges when data platform usage scales faster than anticipated, inefficient queries consume disproportionate compute resources, or data retention policies allow storage accumulation without corresponding analytical value justification. Organizations that adopt cloud data platforms without implementing query cost governance, resource allocation quotas, automated query optimization, and data lifecycle management policies frequently encounter data platform cost overruns that generate CFO and budget holder dissatisfaction, constrain platform expansion plans, and create pressure to optimize platform usage in ways that limit the exploratory analytics and AI development workloads that generate the highest long-term business value from data platform investments.

Data Engineering Talent Scarcity, Rapidly Evolving Platform Technology Landscape, and Skills Gap Between Platform Capability and Enterprise Utilization Creating Implementation and Value Realization Constraints

The rapidly evolving data platform technology landscape, encompassing data lakehouse architectures, real-time streaming frameworks, data mesh organizational patterns, vector database integration, and AI-native data platform capabilities, is demanding continuous skills development from data engineering teams whose proficiency with established tools must be supplemented with expertise in new architectural patterns, platform APIs, and data product development methodologies at a pace that available hiring, training, and capability development programs struggle to match. The competitive market for data engineers, data architects, and analytics engineers with current data lakehouse and cloud platform expertise creates talent acquisition cost pressures and retention challenges that limit the organizational capacity available to execute complex data platform migration, consolidation, and capability expansion programs that deliver the analytical and AI application development productivity improvements that justify platform investment decisions.

Market Segmentation

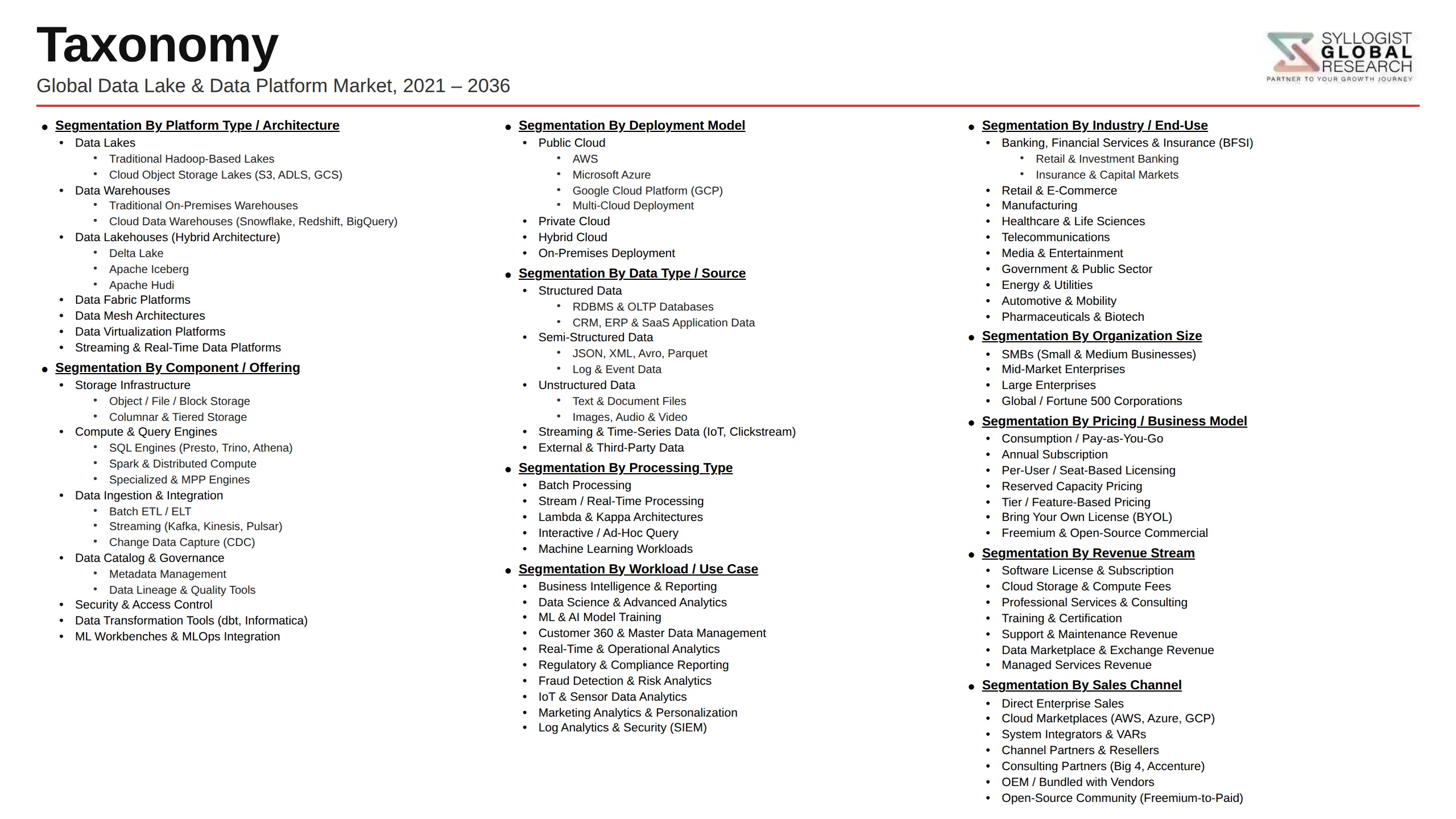

- Segmentation By Platform Type

- Cloud Data Lakes and Object Storage Platforms

- Data Lakehouse Unified Analytics Platforms

- Cloud Data Warehouses and OLAP Engines

- Real-Time Streaming and Event Processing Platforms

- Data Mesh and Domain-Oriented Data Platform Architectures

- Vector Databases and AI-Native Data Platforms

- Others

- Segmentation By Deployment Mode

- Public Cloud Deployment

- Private Cloud and On-Premises Deployment

- Hybrid Multi-Cloud Architectures

- Managed Service and Fully Serverless Platforms

- Segmentation By Component

- Data Ingestion and Pipeline Infrastructure

- Data Storage and File Format Management

- Data Processing and Query Engines

- Data Catalog and Metadata Management

- Data Governance and Quality Monitoring

- Data Visualization and Business Intelligence Layer

- Others

- Segmentation By Data Type

- Structured and Relational Data

- Semi-Structured Data (JSON, XML, Parquet)

- Unstructured Text and Document Data

- Time-Series and IoT Sensor Data

- Image, Video, and Multimedia Data

- Vector and Embedding Data for AI Applications

- Others

- Segmentation By End Use Industry

- Financial Services and Banking

- Technology and Internet Companies

- Retail and E-Commerce

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Telecommunications and Media

- Government and Public Sector

- Others

- Segmentation By Enterprise Size

- Large Enterprises (Above USD 1 Billion Revenue)

- Mid-Market Enterprises (USD 50 Million to USD 1 Billion Revenue)

- Small and Growth-Stage Enterprises (Below USD 50 Million Revenue)

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global data lake and data platform market valuation in 2025, projected through 2034, segmented by platform type, deployment mode, and end use industry, enabling data infrastructure vendors, cloud providers, and enterprise technology buyers to identify the highest-growth platform categories and most commercially significant data platform investment opportunities across the global market?

- How is the data lakehouse architectural convergence reshaping the competitive dynamics between cloud hyperscaler integrated data platform offerings and specialized independent data lakehouse, data catalog, and real-time streaming vendors, and what platform capability differentiation, open table format support, multi-cloud portability, and ecosystem partner strategy are enabling specialist vendors to compete and grow alongside dominant hyperscaler data platforms?

- How are generative AI application development, retrieval-augmented generation system requirements, AI training data management needs, and vector database integration demands creating new categories of data platform infrastructure investment, and what unified data platform architecture capabilities combining structured query, vector retrieval, streaming ingestion, and ML feature management are emerging as enterprise AI development infrastructure standards?

- What data mesh organizational architecture adoption patterns, self-service data product development frameworks, and federated data governance models are proving most effective at scaling enterprise data platform value delivery beyond centralized data engineering team capacity, and what platform capabilities in data domain ownership, data product publishing, and cross-domain discovery are most critical to successful data mesh implementation?

- How are cloud data platform cost management complexity, unpredictable query compute spend, storage cost accumulation, and FinOps discipline maturity gaps affecting enterprise data platform budget management and expansion planning, and what query cost governance frameworks, resource quota management tools, automated optimization capabilities, and data lifecycle management policies are enterprises implementing to achieve sustainable cloud data platform total cost of ownership?

- What data governance, data quality monitoring, metadata management, and data observability platform capabilities are enterprises prioritizing to prevent data lake degradation into ungoverned data swamp environments, and how are active data catalog solutions, automated data quality scoring systems, and AI-powered metadata enrichment tools improving the reliability, discoverability, and trust of enterprise data lake assets for business intelligence and AI application development?

- Which regional data lake and data platform markets, specifically North America, Europe, and Asia-Pacific, are expected to generate the highest incremental investment growth through 2034, and what combinations of AI application development investment, cloud migration program scale, data sovereignty regulatory requirements, data engineering talent ecosystem maturity, and digital industry vertical expansion are defining platform investment trajectories and competitive positioning in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Governance Failure, Data Quality Degradation & Data Swamp Risk

- Cloud Vendor Lock-In, Multi-Cloud Complexity & Portability Risk

- Security Breach, Unauthorised Data Access & Compliance Violation Risk

- Runaway Cloud Storage & Compute Cost Escalation Risk

- Talent Shortage, Data Engineering Skills Gap & Platform Adoption Barrier Risk

- Rapidly Evolving Architecture Standards & Technology Obsolescence Risk

- Regulatory Framework & Standards

- GDPR, CCPA, PDPA & Global Data Privacy Regulations Governing Data Lake Storage, Processing & Residency

- EU Data Act, Data Governance Act & Data Spaces Interoperability Regulatory Frameworks

- HIPAA, PCI-DSS & Sector-Specific Data Handling, Retention & Security Compliance Standards

- AI Act (EU), Executive Order on AI & Algorithmic Accountability Frameworks Affecting Data Platform AI Workloads

- Data Sovereignty, Cloud Localisation & Cross-Border Data Transfer Restriction Frameworks

- Open Data, FAIR Principles & Government Data Sharing Standards for Public Sector Data Platform Deployments

- Global Data Lake and Data Platform Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Petabytes of Data Under Management & Number of Deployments)

- Market Size & Forecast by Platform Type

- Data Lake Platforms (Raw, Semi-Structured & Unstructured Storage)

- Data Warehouse Platforms (Structured, SQL-Optimised & OLAP)

- Data Lakehouse Platforms (Unified Lake & Warehouse Architecture)

- Data Mesh Platforms (Decentralised Domain-Oriented Data Products)

- Data Fabric Platforms (Unified Metadata, Governance & Integration Layer)

- Cloud-Native Analytical Data Platform Suites

- Streaming & Real-Time Data Platform Infrastructure

- Operational Data Platform & Unified Transactional-Analytical Systems

- Market Size & Forecast by Component

- Data Ingestion & Integration Tools (ETL, ELT, CDC & Streaming Ingestion)

- Data Storage Infrastructure (Object Storage, Columnar & Table Formats)

- Data Processing & Compute Engines (Spark, Flink, Presto & Trino)

- Data Governance, Cataloguing, Lineage & Metadata Management Tools

- Data Quality, Observability & Data Reliability Engineering Tools

- Query, SQL Analytics & Business Intelligence Layers

- Data Virtualisation & Federated Query Engines

- AI/ML Feature Store, Model Registry & MLOps Integration Layer

- Data Security, Encryption, Access Control & Masking Tools

- Market Size & Forecast by Deployment Mode

- Public Cloud-Native Data Platform Deployment

- Hybrid Cloud Data Platform Deployment

- On-Premises & Private Cloud Data Platform Deployment

- Multi-Cloud & Cloud-Agnostic Data Platform Deployment

- Market Size & Forecast by Data Type Managed

- Structured Data (Relational, Transactional & ERP Data)

- Semi-Structured Data (JSON, XML, Parquet & Avro)

- Unstructured Data (Text, Images, Video, Audio & Documents)

- Streaming & Time-Series Data (IoT, Event, Log & Sensor Data)

- Geospatial & Location Data

- Market Size & Forecast by Application

- Advanced Analytics, Business Intelligence & Self-Service Reporting

- AI & Machine Learning Model Training, Feature Engineering & MLOps

- Real-Time Streaming Analytics & Event-Driven Decision Making

- Data Science, Experimentation & Statistical Modelling Workloads

- Customer 360, Personalisation & Marketing Analytics

- Financial Analytics, Risk Modelling & Regulatory Reporting

- IoT Data Management, Operational Analytics & Predictive Maintenance

- Data Sharing, Data Marketplace & Inter-Organisational Data Exchange

- Market Size & Forecast by End-User

- Banking, Financial Services & Insurance (BFSI)

- Retail, E-Commerce & Consumer Goods

- Healthcare, Life Sciences & Pharmaceutical

- Telecommunications & Media

- Manufacturing, Industrial & Supply Chain

- Government, Public Sector & Smart City

- Energy, Utilities & Oil and Gas

- Technology, Software & Internet Companies

- Market Size & Forecast by Revenue Model

- SaaS Platform Subscription & Per-Seat Licence Model

- Consumption-Based, Pay-per-Query & Storage-Based Pricing Model

- Perpetual Licence & On-Premises Deployment Model

- Managed Service & Professional Services Model

- North America Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Europe Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Asia-Pacific Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Latin America Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Middle East & Africa Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Country-Wise* Data Lake and Data Platform Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Petabytes Under Management & Number of Deployments)

- By Platform Type

- By Component

- By Deployment Mode

- By Data Type Managed

- By Application

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Sweden, Denmark, Australia, Japan, China, South Korea, India, Singapore, Brazil, Mexico, Saudi Arabia, UAE, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Data Lakehouse Architecture Deep-Dive: Delta Lake, Apache Iceberg & Apache Hudi Open Table Format Comparison & Ecosystem

- Data Mesh Architecture Technology: Domain Data Ownership, Data Product Thinking, Federated Governance & Self-Serve Platform Design

- AI-Augmented Data Platform Technology: LLM-Powered Data Discovery, NL-to-SQL, Automated Data Quality & Intelligent Cataloguing

- Streaming Data Platform Technology: Apache Kafka, Apache Flink, Real-Time Lakehouse & Lambda vs. Kappa Architecture

- Data Virtualisation & Zero-Copy Data Sharing Technology: Apache Arrow Flight, Databricks Delta Sharing & Snowflake Data Sharing

- Unified Analytics & AI Platform Convergence: Lakehouse-plus-MLOps Integration, Feature Store & Model Serving Technology

- Data Observability, DataOps & Automated Data Reliability Engineering Technology for Data Platform Quality Assurance

- Patent & IP Landscape in Data Lake and Data Platform Technologies

- Value Chain & Supply Chain Analysis

- Cloud Infrastructure, Object Storage & Managed Compute Service Supply Chain (AWS S3, Azure ADLS, GCS)

- Open-Source Project Ecosystem, Apache Foundation & Community Contribution Supply Chain

- Data Integration, ETL/ELT & Ingestion Tool Vendor Supply Chain

- Data Governance, Cataloguing & Metadata Platform Supply Chain

- Network Connectivity, Security & Data Transfer Infrastructure Supply Chain

- System Integrator, Data Engineering Consultancy & Implementation Partner Channel

- Hyperscaler Marketplace, SaaS Vendor & Customer Procurement Channel

- Pricing Analysis

- Cloud Data Platform Pricing Comparison: Snowflake, Databricks, BigQuery, Redshift & Azure Synapse Credit-Based Models

- Storage Pricing Analysis: Object Storage Cost per Petabyte & Hot/Cold/Archive Tier Economics

- Compute Pricing: Virtual Warehouse, Cluster Auto-Scaling & Serverless Query Pricing Model Analysis

- Total Cost of Ownership (TCO): Data Platform Build vs. Buy vs. Managed Service Cost Comparison

- Data Governance, Cataloguing & Data Quality Tool Annual Licence & Subscription Pricing Analysis

- Price Trend Analysis: Commoditisation of Storage, Compute Efficiency Gains & Open-Source Disruption Impact on Platform Pricing

- Sustainability & Environmental Analysis

- Carbon Footprint of Data Lake & Data Platform Infrastructure: Cloud Data Centre Energy Consumption, PUE & GHG Intensity

- Green Cloud Procurement, Renewable Energy PPA & Sustainable Data Centre Standards for Data Platform Deployments

- Data Minimisation, Retention Policy & Dark Data Reduction as Energy & Carbon Optimisation Strategies

- Role of Data Platforms in Enabling ESG Analytics, Sustainability Reporting & Corporate Carbon Accounting

- Responsible AI Data Practice: Bias Detection, Data Provenance & Ethical Data Governance Standards

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Application & Geography

- Player Classification

- Hyperscale Cloud Providers with Integrated Data Lake & Platform Services

- Independent Cloud Data Platform & Lakehouse Vendors

- Data Integration, ETL/ELT & Pipeline Platform Specialists

- Data Governance, Cataloguing & Metadata Management Platform Providers

- Data Observability, Quality & DataOps Platform Providers

- On-Premises & Hybrid Data Platform Vendors

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Deployment Mode & Region

- Company Profile

- Company Overview & Headquarters

- Data Lake & Platform Products, Architecture & Technology Portfolio

- Key Customer Relationships & Reference Enterprise Deployments

- Cloud Infrastructure & Partner Ecosystem

- Revenue (Data Platform Segment) & Annual Recurring Revenue (ARR)

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Integrations, Funding Rounds)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Platform Openness vs. Managed Service Completeness)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Component, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio, Architecture & Technology Investment Strategy

- Open-Source, Community & Ecosystem Development Strategy

- Geographic Expansion & Vertical Market Entry Strategy

- Enterprise Customer, ISV & System Integrator Engagement Strategy

- Partnership, Hyperscaler Alliance, M&A & Ecosystem Strategy

- Sustainability, Responsible Data & ESG Analytics Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output