Global Servers Market By Server Type, By Component, By Processor Architecture, By Form Factor, By Deployment Model, By End Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Servers Market encompasses the design, manufacture, and commercial supply of rack-mount, tower, blade, high-density, and edge server systems incorporating central processing units, graphics processing units, memory, storage, and networking hardware, deployed for enterprise data processing, cloud computing infrastructure, artificial intelligence workloads, high-performance computing, telecommunications network virtualization, and edge computing applications across commercial enterprises, hyperscale cloud operators, government agencies, financial institutions, telecommunications providers, and research organizations worldwide.

Market Insights

The global servers market is experiencing one of the most significant structural demand expansions in its history, driven by the convergence of hyperscale cloud capacity investment at unprecedented scale, the explosive emergence of artificial intelligence infrastructure as a primary server procurement category, the accelerating migration of enterprise workloads to hybrid and multi-cloud architectures, and the progressive virtualization of telecommunications network functions creating entirely new server demand channels that did not exist in previous market cycles. The market was valued at approximately USD 132.8 billion in 2025 and is projected to advance at a compound annual growth rate of 10.7% through 2034, as the relentless growth of cloud-native application deployment, large language model training infrastructure, generative AI inference serving, and distributed edge computing collectively sustain server procurement volumes and average unit values substantially above the historical market trajectory established prior to the artificial intelligence infrastructure investment cycle.

The artificial intelligence server segment, anchored by graphics processing unit-dense systems deployed for large language model training, computer vision model development, and at-scale generative AI inference serving, has emerged as the fastest-growing and highest average unit value category within the global server market, fundamentally restructuring the revenue and margin profile of server original equipment manufacturers and component suppliers whose product portfolios are most heavily weighted toward AI-optimized configurations. The capital expenditure commitments of hyperscale cloud providers for AI training cluster infrastructure are sustaining graphics processing unit server procurement backlogs that are compressing delivery lead times, driving premium pricing for AI-optimized server configurations, and incentivizing new entrants including custom silicon developers, accelerated computing platform vendors, and direct liquid cooling infrastructure specialists to compete for the growing addressable market created by AI workload infrastructure requirements that conventional server architectures were not optimized to address.

Enterprise server demand is simultaneously undergoing a technology refresh cycle as organizations accelerate the modernization of on-premises and colocation data center infrastructure to support AI-augmented enterprise applications, containerized microservice architectures, and real-time data analytics workloads that require server configurations with substantially higher memory bandwidth, storage performance, and network throughput than the legacy infrastructure they replace. The adoption of ARM-based server processors from custom silicon programs developed by hyperscale operators and specialist semiconductor vendors is disrupting the historical dominance of x86 processor architecture in server deployments, introducing price-performance competition that is reshaping processor procurement strategies among cloud operators optimizing total cost of ownership across multi-billion-dollar server fleet investments. Liquid cooling infrastructure, encompassing both rear-door heat exchangers and direct liquid cooling systems that remove heat through liquid-cooled cold plates attached to processors and memory modules, is transitioning from a niche specialty into a mainstream data center investment as the thermal density of AI server configurations exceeds the capacity limits of conventional air cooling architectures in high-density deployment environments.

North America is the largest regional server market by revenue, anchored by the concentration of global hyperscale cloud operators, the world’s highest density of enterprise data center capacity, and the most substantial artificial intelligence infrastructure investment programs among both cloud service providers and technology enterprises. Asia-Pacific represents the fastest-growing regional market, driven by the scale of cloud infrastructure expansion across China, Japan, South Korea, India, and Southeast Asia, combined with government-sponsored AI compute infrastructure programs and the growing domestic technology sector server procurement base across the region. Europe is the third major regional market, shaped by stringent data sovereignty regulations, significant enterprise digital transformation investment, expanding colocation capacity, and growing AI infrastructure procurement among European technology companies and financial institutions.

Key Drivers

Artificial Intelligence Infrastructure Investment Surge Driving Unprecedented Demand for GPU-Dense Server Configurations and Fundamentally Reshaping the Global Server Market Revenue and Margin Structure

The commercial emergence of generative artificial intelligence, large language model development, and at-scale AI inference serving is generating the most transformative capital expenditure cycle in the history of the server industry, as hyperscale cloud providers, technology corporations, and sovereign AI programs commit multi-billion-dollar annual investment to GPU-accelerated computing infrastructure required for AI model training and inference at commercially and strategically significant scale. The escalating compute intensity of frontier AI model development, driven by the empirical relationship between model scale, training compute, and capability, is sustaining a rapid expansion in AI server cluster size, GPU count per system, and data center power density that is driving server market revenue growth at a rate substantially exceeding historical compute demand expansion patterns and creating durable procurement demand that extends well beyond the current investment cycle.

Hyperscale Cloud Capacity Expansion and Enterprise Hybrid Cloud Adoption Sustaining Structurally Elevated Server Procurement Volumes Across Public Cloud and On-Premises Infrastructure

Global hyperscale cloud service providers are maintaining elevated capital expenditure programs for data center capacity expansion driven by the continued migration of enterprise workloads from on-premises infrastructure to public cloud platforms, the growth of cloud-native application development generating incremental server capacity demand independent of workload migration activity, and the infrastructure requirements of AI cloud services that are expanding the total addressable workload hosted on hyperscale server fleets at a pace that consistently exceeds capacity planning projections. Enterprise hybrid cloud architecture adoption is simultaneously generating incremental server procurement for on-premises and colocation infrastructure that must interoperate with public cloud environments, sustaining enterprise server demand even as cloud migration redirects some workloads away from customer-owned infrastructure.

Telecommunications Network Function Virtualization and Open RAN Deployment Converting Proprietary Network Hardware Spend into Commodity Server Procurement Across Global Carrier Infrastructure

The global telecommunications industry transition from purpose-built proprietary network hardware to software-defined network functions running on commodity server platforms is creating a structurally new and growing server procurement channel as mobile network operators, fixed-line carriers, and cable operators deploy virtual network functions, cloud-native core network elements, and Open Radio Access Network baseband processing workloads on standard server infrastructure that replaces dedicated network hardware appliances with general-purpose compute platforms. This network function virtualization transition is converting telecommunications capital expenditure historically directed to specialized network equipment vendors into commodity server procurement benefiting standard server manufacturers, expanding the global server total addressable market by incorporating telecommunications infrastructure replacement as an incremental demand category alongside traditional enterprise and hyperscale server procurement channels.

Key Challenges

Data Center Power Consumption Escalation and Electricity Infrastructure Capacity Constraints Creating Site Availability Bottlenecks That Limit Hyperscale and AI Server Deployment Pace

The power consumption intensity of GPU-dense artificial intelligence server deployments is driving data center power density requirements to levels that are outpacing the capacity of existing electrical grid infrastructure in major data center markets including Northern Virginia, Dublin, Singapore, and Amsterdam, where utility power allocation constraints and grid interconnection queue backlogs are creating multi-year delays in data center capacity commissioning that limit the pace at which hyperscale operators can deploy procured server hardware awaiting suitable power-enabled data center facilities. The scale of projected AI infrastructure power demand growth is simultaneously straining national grid planning frameworks and renewable energy procurement pipelines that cannot expand generation capacity at the speed required to serve data center load growth while meeting corporate power purchase agreement and sustainability commitment requirements.

Advanced Semiconductor Supply Chain Concentration and GPU Allocation Constraints Creating Server Delivery Lead Time Uncertainty and Procurement Cost Volatility for AI Infrastructure Programs

The concentration of advanced semiconductor fabrication for high-performance server processors and AI accelerators at a small number of leading-edge foundry facilities, combined with the extraordinary demand for graphics processing units from hyperscale AI infrastructure programs, telecommunications network virtualization, and enterprise AI adoption simultaneously, is creating persistent allocation constraints, extended procurement lead times, and price volatility that complicate capital expenditure planning for organizations managing large-scale server deployment programs with defined go-live timelines. Export control regulations restricting the supply of advanced AI chips to certain markets are adding geopolitical supply chain risk dimensions that affect server procurement strategies for multinational enterprises operating across jurisdictions subject to semiconductor export licensing requirements.

Escalating Data Center Total Cost of Ownership and Energy Efficiency Pressure Driving Architectural Complexity in Server Thermal Management, Power Delivery, and Sustainable Infrastructure Design

The escalating power consumption and heat generation density of AI-optimized server configurations is compelling data center operators and enterprise technology teams to invest in advanced thermal management infrastructure including direct liquid cooling, immersion cooling, and rear-door heat exchanger systems that introduce significant additional capital expenditure, operational complexity, and maintenance requirements relative to conventional air-cooled data center architectures, while simultaneously requiring server hardware designed for liquid cooling compatibility that is not fully interoperable with the large installed base of air-cooled data center infrastructure. Corporate sustainability commitments and energy efficiency regulatory requirements in the European Union and other jurisdictions are adding compliance obligations around power usage effectiveness, renewable energy procurement, and server hardware lifecycle management that further elevate the total cost of ownership of large-scale server infrastructure programs.

Market Segmentation

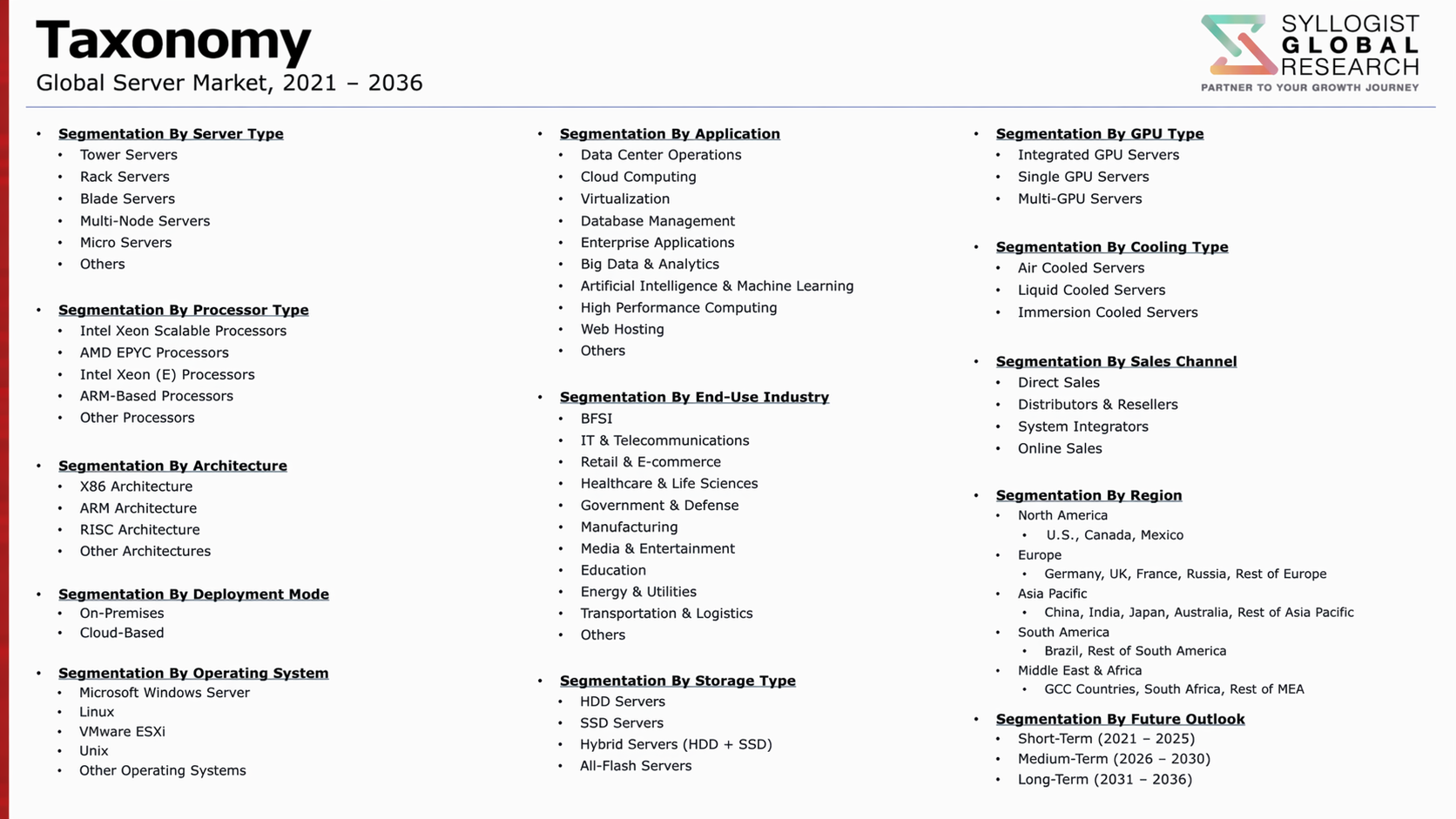

- Segmentation By Server Type

- Tower Servers

- Rack-Mount Servers

- Blade Servers

- High-Density and Hyperscale Servers

- GPU-Accelerated AI and HPC Servers

- Edge Servers

- Others

- Segmentation By Component

- Central Processing Units and Server Processors

- Graphics Processing Units and AI Accelerators

- Server Memory and RAM

- Server Storage (SSD, HDD, NVMe)

- Networking and Interface Cards

- Power Supply and Cooling Systems

- Others

- Segmentation By Processor Architecture

- x86 Architecture Servers

- ARM Architecture Servers

- RISC and Power Architecture Servers

- Others

- Segmentation By Form Factor

- 1U and 2U Rack Servers

- 4U and Above High-Density Rack Servers

- Blade Server Chassis and Modules

- Tower and Pedestal Form Factors

- Micro and Ultra-Dense Form Factors

- Segmentation By Deployment Model

- On-Premises Enterprise Data Centers

- Colocation and Third-Party Data Centers

- Hyperscale Public Cloud Data Centers

- Edge and Distributed Computing Deployments

- Government and Sovereign Cloud Infrastructure

- Segmentation By End Use Industry

- Banking, Financial Services, and Insurance

- Information Technology and Cloud Services

- Telecommunications and Network Operators

- Government and Defense

- Healthcare and Life Sciences

- Retail and E-Commerce

- Manufacturing and Industrial

- Education and Research

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global servers market valuation in 2025, projected through 2034, segmented by server type, component, and end use industry, enabling server manufacturers, cloud infrastructure investors, and enterprise technology planners to identify the highest-growth hardware categories and most durable procurement opportunities across the global server infrastructure landscape?

- How is the artificial intelligence infrastructure investment surge reshaping the composition, average unit value, and margin structure of global server procurement, and which GPU-accelerated server configurations, direct liquid cooling architectures, and AI-optimized networking technologies are defining next-generation hyperscale AI cluster design standards and driving the most significant incremental revenue growth in the server market through 2034?

- How are hyperscale cloud provider capital expenditure programs, enterprise hybrid cloud adoption trajectories, and telecommunications network function virtualization deployments collectively shaping global server demand volumes, deployment model mix, and procurement timing patterns, and what workload growth drivers and cloud service expansion trends are sustaining elevated server procurement beyond the current AI infrastructure investment cycle?

- How is the competitive landscape structured among global server original equipment manufacturers, custom silicon hyperscale hardware developers, and accelerated computing platform vendors, and what product portfolio differentiation, direct liquid cooling capability, AI-optimized architecture development, and hyperscale customer co-design partnership strategies are enabling leading competitors to capture share in the highest-value AI and cloud server segments?

- What data center power capacity constraints, grid infrastructure limitations, advanced semiconductor supply chain concentration risks, and GPU allocation bottlenecks are most significantly affecting the pace and economics of large-scale server infrastructure deployment, and how are hyperscale operators, enterprise data center developers, and server procurement teams adapting their strategies to manage these structural supply and infrastructure constraints?

- How are ARM-based server processor architectures, custom hyperscale silicon programs, and open compute hardware designs disrupting the historical x86 processor dominance in server deployments, and what price-performance economics, workload compatibility improvements, and ecosystem maturity developments are determining the pace and extent of alternative processor architecture adoption across cloud and enterprise server procurement through 2034?

- Which regional server markets, specifically Asia-Pacific, the Middle East, and Latin America, are expected to generate the highest incremental growth through 2034, and what combinations of cloud infrastructure expansion, AI compute program investment, digital transformation acceleration, and data sovereignty regulatory frameworks are driving server procurement growth and shaping supplier market positioning in each region?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Semiconductor Supply Chain Disruption, Advanced Processor Shortage & Component Lead Time Risk

- Geopolitical Trade Restrictions, Export Controls & Server Hardware Supply Chain Concentration Risk

- Cybersecurity, Firmware Vulnerability & Hardware-Level Server Security Risk

- Data Centre Power Availability, Energy Cost Escalation & Cooling Infrastructure Constraint Risk

- Technology Transition, AI Accelerator Obsolescence & Rapid Refresh Cycle Risk

- Regulatory Framework & Standards

- Energy Efficiency Standards for Servers: ENERGY STAR, EU Code of Conduct for Data Centres & MEPS Frameworks

- Data Centre Regulatory Frameworks: EU Data Act, GDPR Data Localisation & National Sovereignty Requirements

- Server Hardware Security Standards: NIST SP 800-193 Platform Firmware Resilience & TCG Trusted Platform Module (TPM)

- Export Control Regulations: EAR, Wassenaar Arrangement & Advanced Server Chip Export Restriction Frameworks

- RoHS, WEEE, REACH & Hazardous Substance Compliance Standards for Server Hardware Manufacturing

- Government Procurement, National Security Review & Strategic Technology Standards for Critical IT Infrastructure

- Global Server Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped)

- Market Size & Forecast by Server Type

- Rack Servers

- Tower Servers

- Blade Servers

- High-Density & Micro Servers

- Modular & Composable Infrastructure Servers

- GPU Servers & AI Accelerated Computing Platforms

- Edge Servers & Ruggedised Edge Computing Platforms

- High-Performance Computing (HPC) & Supercomputer Nodes

- Arm-Based & Alternative Architecture Servers

- Market Size & Forecast by Processor Architecture

- x86 (Intel Xeon & AMD EPYC) Processor-Based Servers

- Arm-Based (Ampere, AWS Graviton & Nvidia Grace) Processor Servers

- RISC-V & Open-Source Instruction Set Architecture (ISA) Servers

- GPU-Accelerated (Nvidia H-Series, AMD Instinct & Intel Gaudi) Server Platforms

- FPGA-Accelerated & SmartNIC-Integrated Server Platforms

- Custom ASIC & Domain-Specific Accelerator Server Platforms

- Market Size & Forecast by Memory & Storage Configuration

- DDR4 DRAM Memory-Based Servers

- DDR5 & HBM (High Bandwidth Memory) Servers

- NVMe SSD & All-Flash Storage Servers

- CXL (Compute Express Link) Memory-Pooling & Composable Memory Servers

- Persistent Memory (PMem) & Storage-Class Memory Integrated Servers

- Market Size & Forecast by Deployment Model

- On-Premises Enterprise & Corporate Data Centre Servers

- Hyperscale & Cloud Service Provider (CSP) Data Centre Servers

- Colocation & Third-Party Data Centre Hosted Servers

- Edge & Near-Edge Deployment Servers

- Telecom & Central Office (CO) Servers

- Market Size & Forecast by Application

- AI Training & Inference Workloads

- Cloud Computing, Virtualisation & Software-Defined Infrastructure

- Enterprise Applications (ERP, CRM, Databases & Business Intelligence)

- High-Performance Computing (HPC), Simulation & Scientific Research

- Big Data Analytics, Data Warehousing & Data Lakehouse Workloads

- Content Delivery, Streaming & Web-Scale Application Hosting

- Telecom Network Function Virtualisation (NFV) & 5G Core Infrastructure

- Edge Computing, IoT Data Processing & Real-Time Analytics

- Storage & Backup Infrastructure

- Market Size & Forecast by End-User

- Hyperscale Cloud Service Providers (CSPs) & Internet Giants

- Enterprise Businesses (BFSI, Manufacturing, Retail & Media)

- Government, Defence & Public Sector

- Telecommunications & Network Operators

- Healthcare & Life Sciences Organisations

- Education, Research & National Laboratories

- Colocation & Managed Service Providers (MSPs)

- Small & Medium-Sized Enterprises (SMEs)

- Market Size & Forecast by Sales Channel

- Direct OEM & Server Manufacturer Sales

- Value-Added Reseller (VAR) & IT Distributor Channel

- Systems Integrator & Managed Service Provider Channel

- ODM & White-Box Server Channel (for Hyperscalers)

- Online & E-Commerce Channel

- Government & Public Procurement Tender Channel

- North America Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Server Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Server Type

- By Processor Architecture

- By Memory & Storage Configuration

- By Deployment Model

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Sweden, Ireland, China, Japan, South Korea, India, Australia, Singapore, Taiwan, Brazil, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- AI Server Platform Technology Deep-Dive: GPU Clusters, NVLink, Infiniband & Ethernet Scale-Out Fabric Architecture

- Next-Generation Processor Technology: Intel Xeon 6, AMD EPYC Turin, Arm Neoverse & Custom Silicon Roadmaps

- CXL (Compute Express Link) Technology: Memory Pooling, Disaggregation & Composable Infrastructure Architecture

- Liquid Cooling & Direct Liquid Cooling (DLC) Technology for High-Density AI & HPC Server Deployments

- Open Compute Project (OCP) & Open Rack Standards: Hyperscale ODM Server Design & Disaggregated Hardware

- Software-Defined Infrastructure, Composable Disaggregated Architecture & Rack-Scale Design Technology

- Silicon Photonics, Co-Packaged Optics & High-Speed Interconnect Technology for Next-Generation Server Networking

- Patent & IP Landscape in Server Hardware Technologies

- Value Chain & Supply Chain Analysis

- Advanced Processor, GPU & Accelerator Chip Design & Foundry Supply Chain

- DRAM, HBM & NAND Flash Memory Component Supply Chain

- PCB, Motherboard & Server Board Manufacturing Supply Chain

- Power Supply Unit (PSU), VRM & Power Delivery Component Supply Chain

- Chassis, Rack, Thermal Management & Cooling Hardware Supply Chain

- NIC, HBA, Storage Controller & Networking Component Supply Chain

- OEM System Integration, Testing, Validation & Logistics Supply Chain

- VAR, Systems Integrator, MSP & ODM Channel

- Pricing Analysis

- Average Selling Price (ASP) Analysis by Server Type & Processor Architecture

- AI GPU Server & HPC Node Capital Cost & Total Cost of Ownership (TCO) Analysis

- On-Premises Server Capex vs. Cloud Infrastructure Equivalent Cost Comparison

- Edge Server & Ruggedised Platform Pricing Analysis

- Server Refresh Cycle Economics: Depreciation, Residual Value & Replacement Cost Analysis

- Price Trend Analysis: Impact of Processor Generation, Memory Pricing & AI Accelerator Demand on Server ASP

- Sustainability & Environmental Analysis

- Server Energy Efficiency Benchmarking: Performance per Watt, Power Usage Effectiveness (PUE) & SPECpower Analysis

- Carbon Footprint of Server Manufacturing: Processor Fabrication, Assembly & Global Logistics Impact

- Data Centre Water Consumption: Liquid Cooling Water Use & Water Usage Effectiveness (WUE) Standards

- Circular Economy for Servers: Refurbishment, Remanufacturing, Asset Recovery & WEEE Compliance

- Renewable Energy Procurement, PPA Frameworks & Net Zero Commitments for Data Centre Server Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Server Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Server Type, Application & Geography

- Player Classification

- Global Brand OEM Server Manufacturers (Full-Line & Enterprise)

- ODM & White-Box Server Manufacturers Serving Hyperscalers

- AI & GPU Server Specialist Manufacturers

- Edge Server & Ruggedised Computing Platform Providers

- HPC & Supercomputer System Integrators

- Arm & Alternative Architecture Server Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Server Type, Processor Architecture & Region

- Company Profile

- Company Overview & Headquarters

- Server Products & Technology Portfolio

- Key Customer Relationships & Reference Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Server Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Contract Wins, Capacity Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Server Type, Processor Architecture, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output