Market Definition

The Global Additive Manufacturing in Aerospace Components Market encompasses the application of layer-by-layer material deposition and fusion technologies for the design, prototyping, tooling, and serial production of structural and functional components used across commercial aviation, military aviation, space launch and satellite systems, and unmanned aerial vehicle platforms. Additive manufacturing, commercially referred to as three-dimensional printing across its various process modalities, enables the fabrication of geometrically complex aerospace components directly from digital design files without the subtractive material removal processes, specialized tooling, or multi-stage assembly operations that characterize conventional manufacturing workflows. The market spans a spectrum of process technologies, most prominently powder bed fusion methods including selective laser melting and electron beam melting for metallic aerospace structures, directed energy deposition for large-format component fabrication and repair, binder jetting for high-throughput metallic and ceramic component production, stereolithography and digital light processing for polymer tooling and cabin interior components, and continuous fiber reinforcement-based composite extrusion for structural lightweight applications. Materials processed within this market include titanium alloys, nickel-based superalloys, aluminum alloys, refractory metals, high-performance engineering polymers, ceramic matrix composites, and continuous fiber-reinforced polymer composites, each selected to satisfy the demanding mechanical, thermal, and fatigue performance requirements imposed by aerospace operating environments. Key participants include aerospace original equipment manufacturers deploying in-house additive manufacturing centers, specialized additive manufacturing service bureaus holding aerospace quality certifications, metal powder and feedstock material suppliers, additive manufacturing machine and system OEMs, and regulatory bodies including the Federal Aviation Administration, European Union Aviation Safety Agency, and defense procurement authorities responsible for certifying additively manufactured flight-critical components for operational deployment.

Market Insights

The global additive manufacturing in aerospace components market is navigating a critical transition from a technology predominantly employed for rapid prototyping and non-structural cabin interior applications toward serial production of flight-critical metallic structural components, propulsion system hardware, and space vehicle primary structures, representing a fundamental change in both the commercial scale and strategic importance of additive manufacturing within the aerospace value chain. This transition is being validated by an expanding inventory of certified additively manufactured components in active commercial and military service, with the cumulative number of FAA-approved additive manufacturing designs for flight-critical applications having surpassed 3,000 individual part qualifications by 2025, across programs spanning turbine engine fuel nozzles, heat exchangers, turbine shrouds, airframe brackets, satellite attitude control thruster bodies, and rocket engine combustion chambers. The global market valuation for additive manufacturing in aerospace components stood at approximately USD 3.8 billion in 2025 and is projected to reach USD 11.2 billion by 2034, expanding at a compound annual growth rate of 12.8% over the forecast period from 2027 to 2034, driven by accelerating certification activity, expanding material qualification libraries, the scaling of multi-laser powder bed fusion systems capable of serial production throughput rates, and a sustained reduction in per-part production costs as machine utilization, build yield, and post-processing automation levels improve across leading aerospace additive manufacturing facilities.

The propulsion system segment represents the most commercially mature and financially significant application domain for metallic additive manufacturing within aerospace, anchored by the now widely documented success of laser powder bed fusion-produced fuel nozzle tips for commercial turbofan engines, which consolidate what were previously assemblies of between 18 and 25 individually machined and brazed sub-components into a single additively manufactured part, delivering a 25% reduction in component weight, a five-fold improvement in service life, and elimination of the associated assembly labor and inspection burden. This proof of concept has catalyzed a broader program of propulsion component additive manufacturing adoption, encompassing turbine blade trailing edge inserts, low-pressure turbine airfoils with internal cooling channel geometries unachievable through conventional casting, combustor swirler assemblies, bearing housings, and full annular heat exchanger cores for next-generation engine architectures. Engine OEMs are now deploying large-format directed energy deposition systems for the near-net-shape fabrication of fan casings, compressor drum forgings, and turbine exhaust case weldments, reducing raw material input by 40% to 65% relative to conventional billet machining approaches and compressing lead times for critical path structural forgings from 52 weeks to as few as 8 weeks in optimized production environments. The total addressable market for additively manufactured propulsion components across commercial and military turbofan, turboprop, and turboshaft engine programs is estimated at USD 4.3 billion annually by 2030, representing the single largest sub-segment within the broader aerospace additive manufacturing market.

The space and defense segments are exhibiting the most rapid adoption velocity for additive manufacturing, driven by the unique economics of low-volume, high-complexity hardware that characterizes both rocket propulsion and satellite systems, where the part count reduction, lead time compression, and geometric freedom afforded by additive manufacturing deliver disproportionate value relative to the corresponding benefits achievable in high-volume commercial aviation production environments. Commercial space launch providers have adopted additive manufacturing as a foundational manufacturing strategy, with leading new-entrant launch vehicle developers producing rocket engine combustion chambers, regeneratively cooled nozzle assemblies, turbopump housings, and propellant manifolds through laser powder bed fusion and directed energy deposition processes, achieving engine assembly part counts that are 80% to 95% lower than equivalent conventionally manufactured designs. Satellite manufacturers are deploying binder jetting and laser powder bed fusion to produce aluminum and titanium structural panels, antenna support brackets, propulsion subsystem components, and thermal management hardware with mass fractions and structural efficiency levels that are enabling meaningful increases in payload-to-bus mass ratios across geostationary and low-Earth-orbit satellite programs. On the defense side, the United States Department of Defense and its allied counterparts have designated additive manufacturing as a strategic industrial capability for sustainment of legacy aircraft and naval vessel fleets, with the potential to produce obsolete or sole-sourced spare parts on demand at forward operating locations using portable additive manufacturing systems, fundamentally transforming the logistics architecture and supply chain resilience characteristics of military platform sustainment in contested and austere operating environments.

From a regional standpoint, North America maintains the most advanced and largest-volume aerospace additive manufacturing ecosystem, anchored by the United States, where the concentration of commercial airframe OEMs, major defense prime contractors, and government-funded research programs through agencies including the Air Force Research Laboratory, the Manufacturing USA institutes, and the Department of Energy’s national laboratory network has created a uniquely dense innovation and commercialization infrastructure for aerospace additive manufacturing. The United States aerospace additive manufacturing market generated approximately USD 1.6 billion in revenue in 2025, representing 42% of global market share, supported by federal investment in additive manufacturing research exceeding USD 320 million annually across defense and civilian agency programs. Europe represents the second-largest regional market, where Airbus, Safran, Rolls-Royce, and MTU Aero Engines have collectively established among the world’s most sophisticated industrial aerospace additive manufacturing capabilities, supported by the European Union’s Clean Aviation Joint Undertaking and Horizon Europe funding frameworks that are co-investing in additive manufacturing for next-generation low-emission aircraft structures and propulsion hardware. Asia-Pacific is the fastest-growing regional market, with China’s government-directed investment in additive manufacturing for aerospace applications, channeled through its national civil-military fusion industrial policy, having produced a domestic ecosystem of titanium powder bed fusion capability that is now supplying structural components for the COMAC C919 and C929 commercial aircraft programs, while Japan, South Korea, and India are independently building sovereign aerospace additive manufacturing capacity as elements of broader defense and advanced manufacturing industrial policy strategies.

Key Drivers

Part Count Consolidation, Topology Optimization, and the Structural Weight Reduction Imperative Across Next-Generation Aerospace Programs

The most commercially compelling and structurally durable driver of additive manufacturing adoption across aerospace components is the technology’s unique capability to consolidate multi-part assemblies into single integrated structures while simultaneously enabling topology-optimized geometries that distribute material precisely where structural loads demand it, delivering component weight reductions that are directly translatable into aircraft fuel burn improvements, payload capacity increases, or range extensions that carry quantifiable economic and competitive value for airframe OEMs and airlines operating under intensifying fuel cost and carbon emission reduction pressures. In commercial aviation, where every kilogram of structural weight reduction across a high-cycle narrow-body aircraft program translates into a present-value fuel saving of approximately USD 3,000 over a 20-year operational life, the ability of additive manufacturing to deliver weight reductions of 20% to 55% relative to conventionally manufactured bracket, duct, fitting, and heat exchanger designs represents a financially compelling justification for the qualification investment required to certify additively manufactured alternatives. The development of large-format metal additive manufacturing systems capable of producing near-net-shape structural components with envelope dimensions exceeding one meter in all axes, including directed energy deposition and wire arc additive manufacturing platforms, is extending the weight reduction opportunity beyond small and medium bracket applications toward primary structural elements including wing ribs, fuselage frames, and landing gear trunnion components that represent individually higher-value certification investments with correspondingly larger unit weight saving payoffs for program-level fuel efficiency targets.

Accelerating Commercial Space Activity and the Economics of On-Demand Low-Volume Complex Hardware Production

The sustained and structurally transformative expansion of commercial space launch activity, driven by the scaling of satellite broadband constellation deployment programs, the emergence of a competitive commercial launch services market, and increasing governmental investment in lunar exploration and cislunar infrastructure programs, is creating a qualitatively distinct demand environment for additive manufacturing that differs fundamentally from the high-volume serial production economics of commercial aviation. Rocket propulsion components, spacecraft structures, and in-space propulsion hardware are produced in quantities ranging from tens to low hundreds of units annually per program, at geometric and material complexity levels that render conventional tooling-dependent manufacturing economically prohibitive and schedular unsustainable for the rapid iteration cycles characteristic of new space program development methodologies. Additive manufacturing eliminates the tooling lead time and capital investment barrier that would otherwise constrain the pace of design iteration in rocket engine development, enabling combustion chamber, injector plate, and nozzle designs to be redesigned, printed, and hot-fire tested within development cycles measured in weeks rather than the months or years required for conventionally tooled equivalent components. The projected growth of the global space economy to approximately USD 1.1 trillion by 2040, with aerospace additive manufacturing playing an enabling role across launch vehicle production, satellite manufacturing, orbital servicing hardware, and eventually in-situ resource utilization for lunar and Martian surface infrastructure, establishes a durable long-cycle demand trajectory for aerospace additive manufacturing that extends well beyond the current commercial aviation and defense program pipeline.

Military Sustainment Imperatives, Supply Chain Resilience Priorities, and the Strategic Value of Distributed On-Demand Parts Production

Defense establishments across North America, Europe, and the Asia-Pacific are increasingly recognizing additive manufacturing as a critical enabler of military platform sustainment resilience, specifically its potential to eliminate the strategic and operational vulnerability created by dependence on single-source conventional suppliers for obsolete or low-demand spare parts whose production tooling has been retired and whose commercial supply chains have been discontinued, a challenge that is acutely affecting the sustainment of legacy military aircraft, naval vessels, and ground vehicle fleets whose designed service lives substantially exceed the economic viability windows of their original equipment supply chains. The United States Department of Defense has formally designated additive manufacturing as a priority industrial capability for supply chain risk mitigation, with the Army, Navy, Air Force, and Marine Corps each operating dedicated additive manufacturing roadmap programs that collectively committed over USD 950 million in additive manufacturing investment across fiscal years 2023 through 2025. The strategic dimension of distributed manufacturing, in which certified additive manufacturing production capacity is deployed to forward operating bases, naval vessels, or maintenance depots in geographically dispersed or logistically contested environments, enabling the on-demand production of critical spare parts without dependence on intercontinental supply chains, is attracting significant investment from defense procurement authorities who recognize that the concentration of manufacturing capacity in a small number of geographically specific industrial facilities constitutes a strategic vulnerability in peer-competitor conflict scenarios that additive manufacturing is uniquely positioned to mitigate through production capability distribution.

Key Challenges

Certification Complexity, Qualification Cost, and the Extended Timeline for Flight-Critical Additive Manufacturing Part Approval

The most consequential barrier constraining the pace of additive manufacturing adoption across flight-critical aerospace component applications is the exceptional complexity, cost, and duration of the regulatory qualification and certification process required to demonstrate that additively manufactured parts meet the airworthiness, structural integrity, fatigue life, and material property consistency standards mandated by the FAA, EASA, and military airworthiness authorities for components whose failure could compromise the safety of the aircraft or the success of the mission they support. Unlike conventionally manufactured components produced through well-characterized casting, forging, or machining processes whose material property databases span decades of production and service experience, additively manufactured metallic components exhibit mechanical properties that are highly sensitive to process parameter selection, feedstock powder quality, machine calibration state, build orientation, thermal history, and post-processing treatment sequences, any of which can introduce property variability that qualification test campaigns must exhaustively characterize before certification authorities will approve the part for flight. The qualification cost for a single additively manufactured flight-critical metallic component, encompassing material characterization testing, process parameter development and locking, non-destructive inspection method development and validation, fatigue and fracture mechanics test coupon programs, full-scale component structural demonstration testing, and documentation package preparation, typically ranges from USD 2 million to USD 12 million depending on the structural criticality, load complexity, and regulatory jurisdiction of the application, creating a per-part qualification investment threshold that economically restricts the business case for additive manufacturing to components of sufficiently high individual unit value, sufficient production volume, or sufficiently compelling weight or lead time advantage to justify the qualification expenditure.

Feedstock Material Quality Consistency, Powder Supply Chain Concentration, and In-Process Defect Detection Limitations

The performance and certification integrity of metallic aerospace additive manufacturing is fundamentally dependent on the chemical composition, particle size distribution, morphology, flowability, and inter-batch consistency of the metal powder feedstocks consumed by laser and electron beam powder bed fusion and directed energy deposition systems, yet the global supply chain for aerospace-grade titanium, nickel superalloy, and aluminum alloy additive manufacturing powders remains highly concentrated among a limited number of atomization facilities with certified aerospace production capability, creating supply security vulnerabilities and inter-supplier quality variability challenges that impose material qualification costs and supply planning constraints on aerospace additive manufacturing programs that were not anticipated in their initial business case analyses. Powder reuse management, specifically the controlled reuse of unfused powder recovered from completed builds through sieving, blending, and oxygen content monitoring protocols, introduces a cumulative material degradation risk that requires rigorous process control and documentation to maintain within the bounds of the material qualification envelope, adding operational overhead to production workflows and creating potential certification exposure if powder handling procedures deviate from qualified process specifications. In-process defect detection within powder bed fusion build chambers, where the formation of porosity, lack-of-fusion defects, hot cracking, and residual stress-induced distortion can occur within individual build layers at length scales below the resolution capability of currently deployed in-situ monitoring systems, remains an insufficiently resolved quality assurance challenge that prevents the replacement of destructive and non-destructive post-build inspection with real-time process monitoring-based quality certification in the manner that would be required to fully achieve the lead time and cost benefits that additive manufacturing theoretically offers relative to conventional manufacturing process chains.

Post-Processing Burden, Surface Finish Limitations, and the Total Cost of Ownership Gap Relative to Conventional Manufacturing at Scale

A persistent and commercially significant challenge affecting the economic competitiveness of additive manufacturing for aerospace component production is the substantial post-processing burden imposed by the as-built surface finish quality, residual stress state, and dimensional accuracy limitations of current additive manufacturing process technologies, which in most flight-critical metallic applications necessitate a sequence of stress relief heat treatment, hot isostatic pressing, CNC machining of critical dimensional features and mating surfaces, electrochemical or abrasive surface finishing for fatigue-critical areas, and non-destructive inspection using computed tomography and fluorescent penetrant or magnetic particle inspection methods, collectively adding processing time, equipment investment, labor cost, and yield risk that can account for 40% to 70% of the total part manufacturing cost and substantially erode the cost competitiveness of additive manufacturing relative to established conventional manufacturing alternatives at production volumes above several hundred units per year. The surface roughness of as-built laser powder bed fusion components, which typically ranges from 6 to 20 micrometers Ra on downward-facing and unsupported surfaces, is incompatible with the fatigue performance requirements of rotating engine components, pressure vessel interfaces, and aerodynamic external surfaces without substantial material removal through CNC machining or electrochemical polishing operations that partially negate the buy-to-fly ratio advantages that additive manufacturing achieves in raw material input efficiency. The total cost of ownership comparison between additive manufacturing and conventional manufacturing for aerospace components therefore requires rigorous and application-specific analysis encompassing raw material cost, machine time, post-processing operations, qualification amortization, scrap rates, and inventory carrying cost savings, an analysis that frequently reveals additive manufacturing to be cost-competitive only within a specific window of geometric complexity, production volume, and lead time value that narrows considerably as production volumes scale.

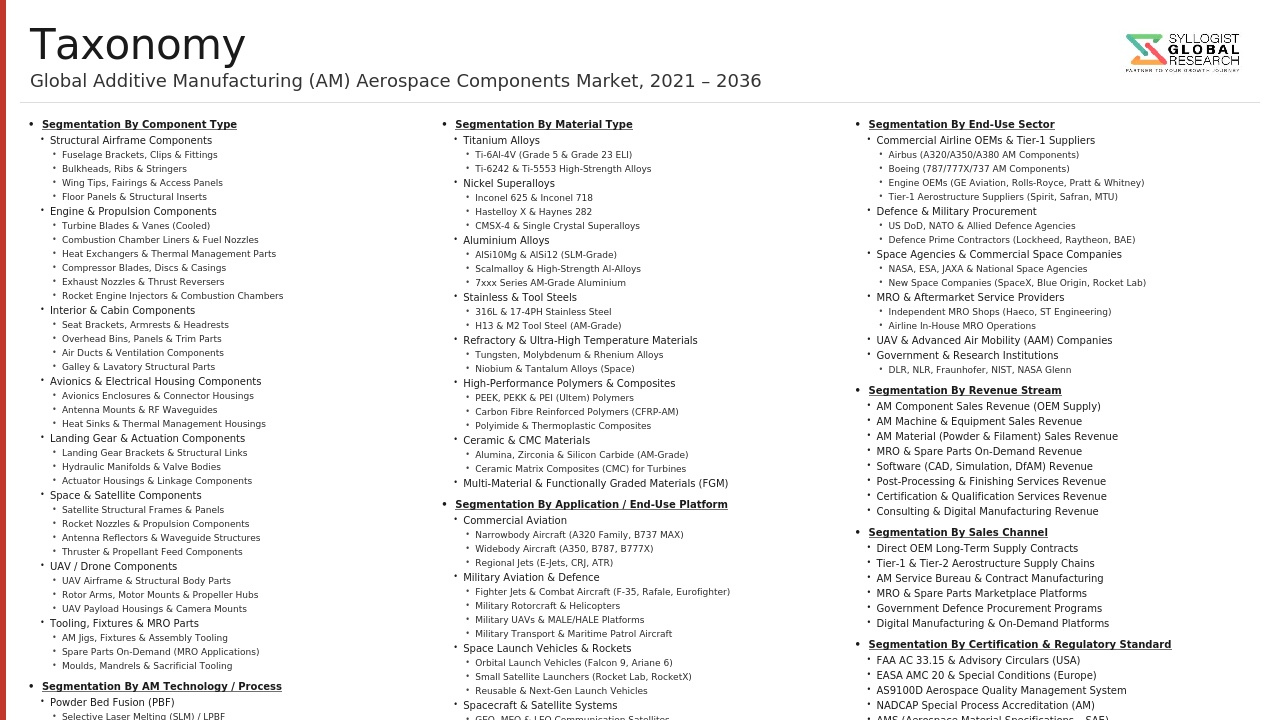

Market Segmentation

- Segmentation By Process Technology

- Powder Bed Fusion, Selective Laser Melting (SLM) / Laser Powder Bed Fusion (LPBF)

- Powder Bed Fusion, Electron Beam Melting (EBM)

- Directed Energy Deposition (DED), Laser-Based

- Directed Energy Deposition, Wire Arc Additive Manufacturing (WAAM)

- Binder Jetting

- Stereolithography (SLA) and Digital Light Processing (DLP)

- Fused Deposition Modeling (FDM) and Continuous Fiber Extrusion

- Cold Spray Additive Manufacturing

- Others

- Segmentation By Material Type

- Titanium Alloys (Ti-6Al-4V and Variants)

- Nickel-Based Superalloys (Inconel 625, Inconel 718, Haynes 282)

- Aluminum Alloys (AlSi10Mg, Scalmalloy)

- Stainless Steel and Tool Steel

- Refractory Metals (Tungsten, Molybdenum, Rhenium)

- High-Performance Engineering Polymers (PEEK, PEKK, Ultem)

- Ceramic Matrix Composites (CMC)

- Continuous Fiber-Reinforced Polymer Composites

- Others

- Segmentation By Component Type

- Propulsion System Components (Fuel Nozzles, Turbine Blades, Combustor Hardware)

- Airframe Structural Components (Brackets, Ribs, Frames, Fittings)

- Heat Exchangers and Thermal Management Hardware

- Cabin Interior and Non-Structural Components

- Tooling, Jigs, and Manufacturing Fixtures

- Rocket Engine and Spacecraft Propulsion Components

- Satellite Structures and Subsystem Hardware

- Landing Gear Components

- Hydraulic and Fluid System Components

- Others

- Segmentation By Aviation Platform

- Commercial Aviation (Narrow-Body Aircraft)

- Commercial Aviation (Wide-Body Aircraft)

- Military Fixed-Wing Aircraft

- Military Rotary-Wing Aircraft (Helicopters)

- Business and General Aviation

- Unmanned Aerial Vehicles (UAVs) and Unmanned Combat Aerial Vehicles (UCAVs)

- Launch Vehicles and Rockets

- Satellites and Spacecraft

- Others

- Segmentation By Application

- Prototyping and Concept Validation

- Tooling and Manufacturing Aid Production

- Serial Production of Flight-Critical Metallic Components

- Serial Production of Non-Structural and Cabin Interior Components

- Maintenance, Repair, and Overhaul (MRO) Spare Parts Production

- Repair and Restoration of Worn or Damaged Components

- On-Demand Defense Sustainment Parts Manufacturing

- Others

- Segmentation By Production Type

- In-House OEM Additive Manufacturing Centers

- Third-Party Additive Manufacturing Service Bureaus

- Collaborative Joint Venture and Consortium Production

- Government and Defense Laboratory Additive Manufacturing Facilities

- Others

- Segmentation By Machine Build Volume

- Small Format (Build Envelope Below 250 x 250 x 250 mm)

- Medium Format (Build Envelope 250 mm to 500 mm)

- Large Format (Build Envelope Above 500 mm)

- Segmentation By End User

- Commercial Airframe OEMs and Tier-One Aerostructure Suppliers

- Aero-Engine and Propulsion System OEMs

- Defense Prime Contractors and Military Aviation Programs

- Commercial Space Launch Vehicle Developers

- Satellite and Spacecraft Manufacturers

- MRO Service Providers and Airline Maintenance Organizations

- Defense Sustainment and Depot Maintenance Organizations

- General and Business Aviation Manufacturers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Additive Manufacturing in Aerospace Components Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by process technology, laser powder bed fusion, electron beam melting, directed energy deposition, binder jetting, and polymer-based processes, and by application domain spanning commercial aviation, military aviation, space launch vehicles, and satellite systems, to enable aerospace OEMs, machine suppliers, material producers, and investors to identify which technology and application combinations offer the strongest near-term revenue capture and long-term growth positioning?

- How is the certification and airworthiness qualification landscape for additively manufactured flight-critical metallic components evolving across the FAA, EASA, and key national military airworthiness authority jurisdictions through 2034, and what are the projected qualification cost trajectories, timeline reductions, and process standardization developments, including the adoption of material and process qualification frameworks, in-situ monitoring-based quality assurance, and digital thread traceability standards, that will determine the pace at which additive manufacturing achieves broad adoption in primary structural and propulsion applications?

- What is the current competitive positioning and projected market share evolution of the leading aerospace additive manufacturing machine OEMs, metal powder and feedstock material suppliers, and certified additive manufacturing service bureaus, and how are their respective technology roadmaps, material portfolio expansions, machine scale-up investments, strategic aerospace OEM partnerships, and geographic capacity additions expected to reshape the competitive landscape across both capital equipment and production services segments through the forecast period?

- How is the adoption of additive manufacturing for military platform sustainment, on-demand spare parts production, and forward-deployed distributed manufacturing evolving within the defense programs of the United States, United Kingdom, France, Germany, Australia, and key Asia-Pacific nations, and what is the projected addressable market value of additively manufactured defense sustainment components by 2034, segmented by service branch, platform category, and geographic deployment region?

- What role is additive manufacturing expected to play in the production of next-generation commercial turbofan engine components, including advanced cooling channel turbine blades, ceramic matrix composite hot-section structures, additively manufactured heat exchanger cores, and integrated combustor assemblies, within the engine programs of leading propulsion OEMs, and what volume of additively manufactured components per engine shipset, at what per-component value, is projected to be achieved across narrow-body and wide-body aircraft propulsion programs by 2030 and 2034 respectively?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Readiness & Process Maturity Risk

- Qualification & Certification Risk

- Supply Chain & Feedstock Risk

- Intellectual Property & Cybersecurity Risk

- Scaling & Production Risk

- Geopolitical & Export Control Risk

- Regulatory Framework & Standards

- Civil Aviation Airworthiness Regulations for AM Parts

- Space & Launch Vehicle AM Standards

- Military & Defence AM Standards

- Material & Process Standards for Aerospace AM

- Quality Management & NDT Standards for Aerospace AM

- Global Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Parts Produced)

- Market Size & Forecast by AM Process / Technology Type

- Powder Bed Fusion (PBF)

- Laser Powder Bed Fusion (LPBF / SLM / DMLS)

- Electron Beam Powder Bed Fusion (EB-PBF / EBM)

- Multi-Laser LPBF Systems

- Directed Energy Deposition (DED)

- Laser DED / Laser Metal Deposition (LMD)

- Electron Beam DED (EB-DED)

- Wire Arc Additive Manufacturing (WAAM)

- Cold Spray / Supersonic Particle Deposition

- Binder Jetting (BJ)

- Metal Binder Jetting for Aerospace Brackets & Fittings

- Ceramic Binder Jetting for Investment Casting Cores

- Material Extrusion (MEX)

- Fused Filament Fabrication (FFF) – High-Performance Polymer

- Bound Metal Deposition (BMD)

- Continuous Fibre Reinforcement (CFR-FFF) for Composite Structures

- Vat Photopolymerisation

- Stereolithography (SLA) for Tooling, Jigs & Fixtures

- Digital Light Processing (DLP) for Precision Casting Patterns

- Material Jetting

- PolyJet / MultiJet Fusion for Cabin Interior Prototyping

- Drop-On-Demand Metal Jetting for High-Resolution Metal Parts

- Sheet Lamination

- Ultrasonic Additive Manufacturing (UAM) for Multi-Material Structures

- Market Size & Forecast by Material Type

- Metal AM Materials

- Polymer AM Materials

- Composite AM Materials

- Ceramic AM Materials

- Specialty & Novel AM Materials

- Market Size & Forecast by Aerospace Component Type

- Engine & Propulsion Components

- Combustion Chamber Liners & Injectors

- Turbine Blades, Vanes & Nozzle Guide Vanes (NGV)

- Turbine Blade Internal Cooling Channels & Complex Internal Features

- Fuel Nozzles & Swirlers (GE LEAP Fuel Nozzle Benchmark)

- Compressor Stages & Impellers

- Engine Brackets, Bosses & Manifolds

- Exhaust Components & Thrust Reverser Parts

- Heat Exchangers & Oil Coolers

- Rocket Engine Combustion Chambers & Nozzles

- Turbopump Components for Launch Vehicles

- Structural & Airframe Components

- Titanium Primary Structural Parts (Ribs, Spars, Frames, Brackets)

- Topology-Optimised Hinges, Brackets & Lugs

- Door Surround Fittings & Window Frames

- Leading Edge Structural Components

- Landing Gear Components & Structural Fittings

- Bulkheads & Pressure Vessel Fittings

- Wing Tips & Winglets

- Fuselage Structural Inserts & Printed Frames

- Avionics & Electrical System Components

- Avionics Housings, Brackets & Mounting Structures

- Waveguides, Antenna Structures & RF Components

- Heat Sinks & Thermal Management Components for Avionics

- Electrical Connector & Junction Box Housings

- Interior & Cabin Components

- Cabin Overhead Bin Components & Partitions

- Seat Structural Brackets, Headrests & Armrests

- Air Ducts, Grilles & Ventilation Components

- Galley & Lavatory Structural & Functional Parts

- In-Flight Entertainment (IFE) System Housings & Mounts

- Cabin Lighting Fixtures & Architectural Elements

- Floor Panels & Interior Trim Components

- Fluid System & Hydraulic Components

- Hydraulic Manifolds & Valve Bodies

- Fuel System Brackets, Clamps & Feed Lines

- Pneumatic Ducting & Bleed Air Components

- Oxygen System Components

- Heat Exchanger Cores & Fluid Cooling Plates

- Space & Launch Vehicle Components

- Rocket Engine Thrust Chambers & Nozzle Extensions

- Satellite Structural Bus Panels & Brackets

- Propellant Tank Fittings & Propulsion System Manifolds

- Antenna Reflectors & Waveguide Structures

- Solar Panel Substrates & Honeycomb Core Structures

- Payload Adapters & Separation Systems

- Satellite Thermal Control Panels & Heat Pipes

- Tooling, Jigs, Fixtures & Moulds

- Composite Layup Mandrels & Autoclave Tooling

- Assembly Jigs, Fixtures & Check Gauges

- Drilling & Fastener Installation Templates

- Investment Casting Patterns & Wax Moulds

- Wind Tunnel Model AM Components

- MRO & Repair Components

- Obsolete Spare Part Reproduction via AM

- DED Repair of Worn Engine & Structural Components

- Cold Spray Repair of Corrosion-Damaged Aerospace Parts

- AM-Produced Interim Replacements for Long-Lead Spare Parts

- Market Size & Forecast by Aircraft / Platform Type

- Commercial Aviation

- Narrow-Body Commercial Aircraft (A320 Family, Boeing 737 MAX)

- Wide-Body Commercial Aircraft (A350, A380, Boeing 787, 777X)

- Regional Jets & Turboprops

- Business Jets & Corporate Aviation

- Military Aviation

- 5th & 6th-Generation Combat Aircraft (F-35, FCAS, GCAP, KF-21)

- Military Transport Aircraft (C-17, A400M, KC-46)

- Military Helicopters (Attack, Transport, Maritime)

- Trainer Aircraft

- Unmanned Aerial Vehicles (UAV) & UCAV

- Rotorcraft

- Civil & Commercial Helicopters

- Military Helicopters

- Advanced Air Mobility (AAM) / eVTOL Aircraft

- Space & Launch Vehicles

- Orbital Launch Vehicles (Falcon 9, Ariane 6, Vulcan, New Glenn)

- Small Satellite Launch Vehicles (Rocket Lab, ABL Space, Orbex)

- Commercial Satellites (GEO, MEO, LEO Constellations)

- Human Spaceflight Vehicles (Orion, Starliner, Dragon)

- Reusable Launch Vehicles

- Unmanned Aerial Vehicles (UAV) & Drones

- Fixed-Wing ISR / MALE UAVs

- Multi-Rotor Commercial Drones

- Loitering Munitions & Combat UAVs

- General Aviation & Training Aircraft

- Commercial Aviation

- Market Size & Forecast by End-Use Application

- Prototyping & Rapid Product Development

- Series Production (Flight Hardware)

- Spare Parts & MRO Production

- Tooling, Jigs & Fixtures Production

- Research & Development (Wind Tunnel, Test Articles)

- Defence Sustainment & Obsolescence Management

- Market Size & Forecast by Sales Channel

- Direct OEM In-House AM Facility

- Tier-1 Aerospace Supplier AM Production

- Independent AM Service Bureau for Aerospace

- Defence Depot & Military Base AM Facilities

- Spare Parts Distributor & Digital Inventory Platform

- Engine & Propulsion Components

- Powder Bed Fusion (PBF)

- North America Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

- Europe Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

- Latin America Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Additive Manufacturing in Aerospace Components Market Outlook

- Market Size & Forecast

- By Value

- By AM Process / Technology Type

- By Material Type

- By Aerospace Component Type

- By Aircraft / Platform Type

- By End-Use Application

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, United Kingdom, France, Italy, Spain, Netherlands, Sweden, Switzerland, Russia, China, Japan, India, South Korea, Australia, Singapore, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Metal Additive Manufacturing Technology Landscape for Aerospace

- In-Process Quality Assurance & Monitoring Technology

- Design for Additive Manufacturing (DfAM) Technology

- Post-Processing Technology for Aerospace AM Components

- Digital Thread & Industry 4.0 in Aerospace AM

- Simulation & Process Modelling for Aerospace AM

- Patent & IP Landscape in Aerospace AM

- Value Chain & Supply Chain Analysis

- Raw Material & Feedstock Supply Chain

- Metal Powder Production & Supply Chain

- AM Machine / System Manufacturers

- Software & Digital Tools Supply Chain

- Post-Processing Equipment Supply Chain

- Aerospace AM Service Bureau & Contract Manufacturers

- End-Use Aerospace Customers

- MRO & Aftermarket AM Applications

- Pricing Analysis

- AM System & Equipment Pricing Analysis

- Metal AM Powder Pricing Analysis

- Aerospace AM Part Production Cost Analysis

- Certification & Qualification Cost Analysis

- Total Cost of Ownership (TCO) Analysis

- Sustainability & Energy Efficiency

- Environmental Benefits of Aerospace AM vs. Conventional Manufacturing

- Metal Powder Circular Economy & Recycling

- Aircraft Lifecycle Sustainability Impact of AM Components

- Additive Manufacturing Energy Efficiency

- ESG & Sustainability Reporting for Aerospace AM

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Segment)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by AM Process Type & Aerospace Component Category

- Player Classification

- Tier-1 AM System OEMs with Dominant Aerospace Market Position

- Aerospace Prime & Tier-1 Supplier In-House AM Operations

- Aerospace-Dedicated AM Service Bureaux & Contract Manufacturers

- Metal AM Powder Specialists for Aerospace

- DfAM, Simulation & AM Software Specialists

- Post-Processing & NDT Equipment Specialists for Aerospace AM

- Emerging & Disruptive AM Startups with Aerospace Focus

- Competitive Analysis Frameworks

- Market Share Analysis by AM Process, Material & Aerospace Segment

- Company Profile

- Company Overview & Headquarters

- AM Products, Systems & Services Portfolio for Aerospace

- Key Aerospace Customer Relationships & Approved Supplier Status

- Qualified Material-Process-Part Combinations

- Revenue (Aerospace AM Segment) & Backlog

- R&D Investment & Technology Roadmap

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Certifications, Product Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map (Technology Leadership vs. Aerospace Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix – By AM Process, Material, Component Type & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Investment & R&D Prioritisation Strategy

- Qualification & Certification Strategy

- Design & Engineering Strategy

- Supply Chain & Feedstock Strategy

- Partnership, M&A & Ecosystem Development Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)