Market Definition

The India Automotive Aftermarket Parts Market encompasses the manufacturing, distribution, wholesale trade, and retail supply of replacement components, maintenance consumables, performance enhancement products, accessories, and repair materials used to service, repair, restore, and upgrade the in-use vehicle fleet operating across India’s road transport network, covering passenger cars, two-wheelers, three-wheelers, light commercial vehicles, medium and heavy commercial vehicles, tractors, and off-highway equipment across their operational service lives following initial vehicle purchase from original equipment manufacturer dealership channels. The automotive aftermarket encompasses all replacement part categories including engine components, transmission parts, brake systems, suspension and steering components, electrical and electronic systems, body panels, filters, lubricants, tyres and batteries, cooling system components, exhaust systems, and the full range of vehicle consumables and maintenance materials consumed during routine servicing and unplanned repair events throughout the vehicle ownership lifecycle.

The market is structured across three principal supply channels: the organized genuine parts channel distributing OEM-branded and authorized supplier replacement parts through franchised dealership service networks and authorized multi-brand service chains; the organized branded aftermarket channel supplying independent workshops and retail outlets with branded replacement parts from established domestic and international Tier-1 component manufacturers whose quality and fitment credentials are recognized by professional mechanics and vehicle owners; and the unorganized bazaar channel distributing low-cost, frequently non-branded or counterfeit replacement parts through traditional automotive spare parts markets concentrated in urban commercial districts and semi-urban roadside retail clusters. The market further encompasses automotive lubricants and fluids distributed through vehicle service centers and retail outlets; tyres sold through replacement channels independent of new vehicle purchases; batteries replaced through organized and unorganized retail networks; and the growing digital aftermarket encompassing e-commerce platforms including Amazon, Flipkart, and specialist automotive e-tailers whose online spare parts retail is progressively formalizing a previously fragmented and predominantly offline market. Key participants include OEM parts divisions of Maruti Suzuki, Tata Motors, Mahindra, Hyundai, Hero MotoCorp, and Honda, independent Indian and multinational component manufacturers, lubricant and consumable companies, tyre manufacturers, battery producers, and the diverse distribution and retail infrastructure spanning dealer service networks, independent workshops, spare parts wholesalers, and e-commerce platforms.

Market Insights

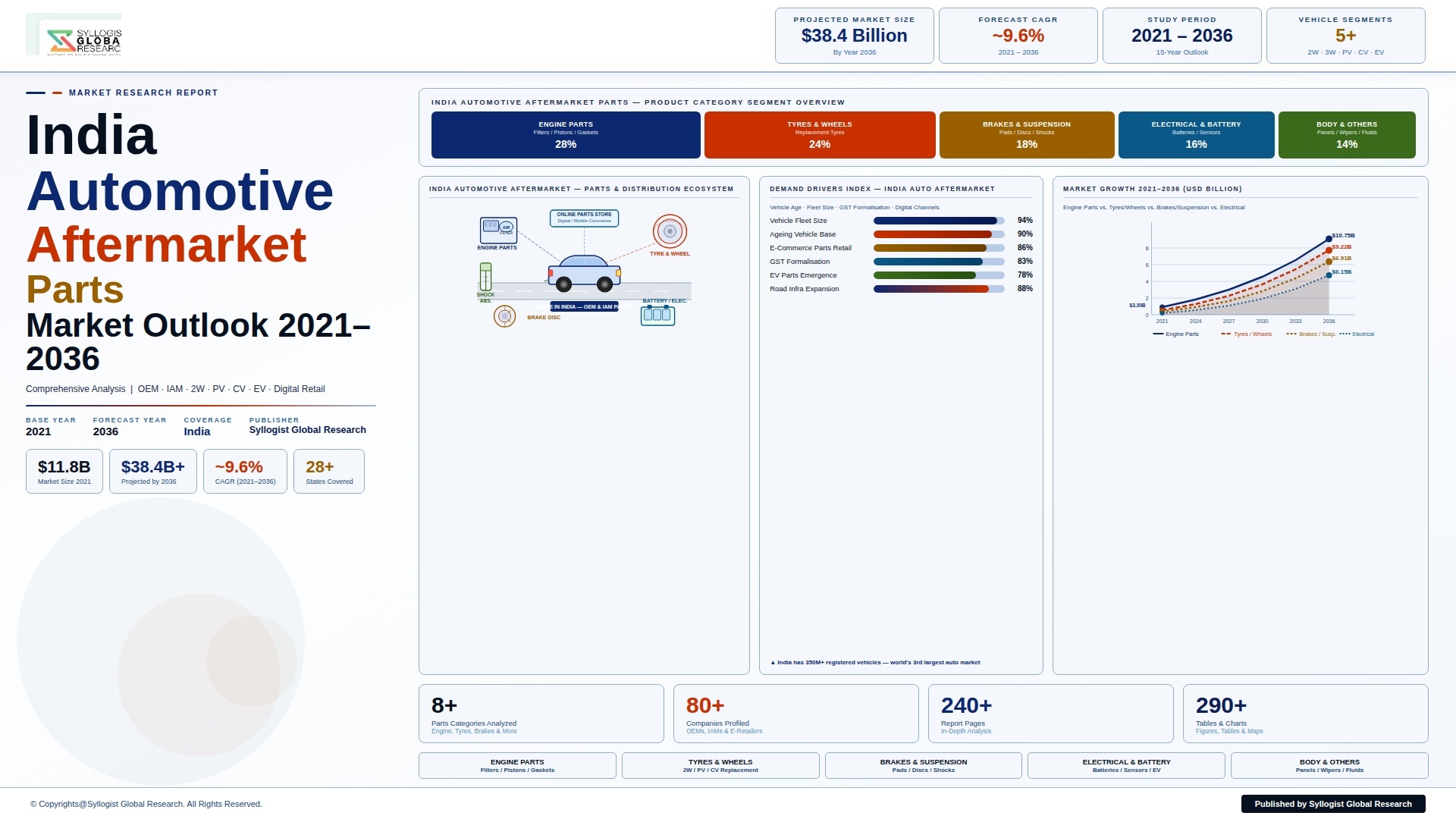

The India automotive aftermarket parts market is entering a structurally favorable demand expansion phase driven by the rapid accumulation of the Indian vehicle parc to the scale where aftermarket service demand generates a self-sustaining commercial engine independent of new vehicle sales cycles, the progressive aging of the in-use vehicle fleet as the large new vehicle sales volumes of the 2015 to 2023 period create a growing cohort of vehicles transitioning from dealership warranty service into independent aftermarket maintenance, and the formalization trend across automotive retail and service channels that is progressively shifting repair and maintenance expenditure from the unorganized bazaar toward branded organized aftermarket channels with higher revenue capture per service event. The India automotive aftermarket parts market was valued at approximately USD 14.8 billion in 2025 and is projected to reach USD 26.3 billion by 2034, advancing at a compound annual growth rate of 6.6% over the forecast period from 2027 to 2034, driven by the expanding total vehicle parc whose registered population exceeded 340 million units in 2025 and continues growing at 20 to 22 million new registrations annually, the increasing average vehicle age that correlates directly with higher per-vehicle annual maintenance and repair expenditure, and the rising labor and parts revenue capture of organized multi-brand service chains and OEM extended dealership networks that are progressively formalizing aftermarket service delivery across India’s metropolitan and tier-2 city markets.

The two-wheeler aftermarket segment constitutes the largest revenue category within the India automotive aftermarket market, accounting for approximately 38% of total aftermarket parts revenue in 2025, reflecting the sheer scale of India’s two-wheeler fleet which exceeded 200 million registered units in 2025, making it the world’s largest two-wheeler fleet by a substantial margin, and whose intensive daily utilization in urban commuting, rural mobility, and last-mile delivery applications generates among the highest annual parts consumption per vehicle of any vehicle category globally. Two-wheeler maintenance expenditure is concentrated in high-frequency consumable replacement categories including engine oil changes at intervals of 1,500 to 3,000 kilometers, chain and sprocket sets, brake pads and shoes, spark plugs, air filters, tyres, and batteries whose combined annual consumption across 200 million vehicles generates enormous absolute replacement volumes that anchor the commercial viability of India’s spare parts distribution infrastructure across urban, semi-urban, and rural market geographies. The growing premium two-wheeler segment, led by the rapid sales expansion of Royal Enfield, Bajaj’s KTM and Triumph-licensed platforms, Honda’s CB series, and Yamaha’s MT and R series, is creating a higher-value parts replacement market within the two-wheeler category whose brand-specific performance part and accessory consumption generates above-average revenue per maintenance event compared to commuter segment vehicles, and whose owner demographics exhibit higher brand loyalty, authorized service channel preference, and willingness to pay premium prices for OEM-branded parts that benefit organized aftermarket channel operators.

The commercial vehicle aftermarket segment represents the highest parts revenue per vehicle category within the India aftermarket market, driven by the intensive operational utilization, high annual mileage accumulation, and critical safety implications of medium and heavy commercial vehicle fleet maintenance that generate parts replacement frequencies, consumable consumption volumes, and repair labor hours substantially exceeding those of passenger vehicle maintenance programs. Indian commercial vehicle operators, managing fleets of trucks, buses, and tipper vehicles under the economic pressure of freight rate competition and fuel cost volatility, prioritize the minimization of vehicle downtime over parts brand preference in their maintenance procurement decisions, creating a commercially large and price-sensitive demand market for replacement parts spanning engine overhaul components, clutch assemblies, brake system components, suspension bushes and leaf springs, electrical systems, and body repair panels that is served by both organized branded aftermarket suppliers and the lower-cost unorganized supply chain. The growth of organized fleet operators including Blue Dart, Delhivery, Mahindra Logistics, and corporate captive fleets managing large vehicle populations through systematic preventive maintenance programs is progressively shifting commercial vehicle aftermarket procurement from the transactional spot purchase model of owner-operator truck mechanics toward structured fleet maintenance supply agreements with organized parts suppliers, creating commercial opportunities for branded aftermarket suppliers whose quality assurance, supply chain reliability, and fleet program management capabilities differentiate them from the unorganized supply chain alternatives.

The digitalization of India’s automotive aftermarket distribution and retail ecosystem represents the most structurally transformative trend reshaping the competitive architecture of the market over the forecast period, as e-commerce platforms, digital auto parts marketplaces, and tech-enabled multi-brand service chain aggregators collectively challenge the historical dominance of the unorganized physical bazaar channel by providing price transparency, counterfeit product risk reduction through platform authentication programs, doorstep delivery convenience, and expanded SKU availability that address the principal commercial disadvantages of the organized branded aftermarket channel relative to low-cost bazaar alternatives. Amazon India’s automotive category, Flipkart’s spare parts marketplace, and specialist automotive e-commerce platforms have collectively reached approximately USD 1.2 billion in annual automotive parts and accessories gross merchandise value in 2025, growing at approximately 22% annually, with product categories including filters, lubricants, batteries, tyres, and accessory items representing the highest online purchase frequency, as consumer comfort with online automotive parts purchase grows with improving delivery reliability, return policy clarity, and product authenticity guarantee mechanisms on major platforms. The multi-brand automotive service chain segment, represented by GoMechanic before its restructuring, MyTVS, 3S Speedwings, Bosch Car Service authorized workshops, and Midas Auto service network, is creating a formalized organized service infrastructure that captures branded parts revenue from the independent workshop channel by providing training, tooling, quality assurance, and brand marketing support to participating workshops in exchange for sourcing commitments that direct replacement parts procurement through organized channel suppliers rather than bazaar alternatives.

Key Drivers

Expanding Indian Vehicle Parc and Progressive Fleet Aging Creating Structurally Growing Per-Vehicle Maintenance and Parts Replacement Demand

The accumulated scale of the Indian vehicle fleet, whose total registered population of over 340 million units in 2025 represents the product of two decades of accelerating new vehicle sales combined with a relatively low vehicle scrappage and retirement rate compared to developed country automotive markets, is creating a structurally expanding aftermarket demand base whose commercial growth trajectory is driven more by the aging and accumulated mileage of the existing fleet than by incremental new vehicle additions. Vehicles aged three to eight years represent the peak aftermarket spending segment, generating per-vehicle annual maintenance expenditure of USD 120 to USD 350 for passenger cars and USD 80 to USD 180 for two-wheelers as warranty coverage expires and unplanned repair events begin supplementing routine maintenance in overall service expenditure, and the large cohort of vehicles sold during the 2018 to 2023 high-volume new vehicle sales period is progressively entering this peak aftermarket spending age band throughout the forecast period, creating a demographically driven aftermarket demand acceleration that is structurally independent of new vehicle market cycle performance. The government’s vehicle scrappage policy, which provides financial incentives for retiring vehicles older than 15 years through green tax waivers and scrapping certificate discounts on new vehicle purchases, is expected to accelerate the retirement of approximately 5 to 7 million end-of-life vehicles annually from fiscal year 2025-26, simultaneously creating new vehicle sales demand and reducing the oldest and highest-maintenance-cost segment of the parc while sustaining the commercially productive 3 to 12-year vehicle age bracket that generates the highest aftermarket parts revenue intensity.

Increasing Vehicle Complexity, BS VI Technology Content, and Advanced Driver Assistance System Adoption Elevating Per-Event Repair Value Across Organized Service Channels

The nationwide transition to Bharat Stage VI emission standards implemented in April 2020, which required the adoption of direct fuel injection, exhaust gas recirculation, selective catalytic reduction for diesel vehicles, and advanced engine management electronic control systems across the entire new vehicle portfolio, has materially increased the technical complexity and parts replacement cost profile of India’s in-use vehicle fleet, as the sophisticated emission control components installed on BS VI vehicles require specialized diagnostic equipment, trained technicians, and OEM or high-quality branded aftermarket replacement parts whose technical fitment requirements are incompatible with the lower-quality unorganized bazaar supply chain. The growing penetration of advanced driver assistance systems, automated transmission variants, turbocharging across petrol and diesel powertrains, and electric vehicle powertrain technology in India’s premium passenger car and SUV segments is creating a technically demanding aftermarket servicing environment whose diagnostic and repair complexity concentrates revenue in organized dealership and multi-brand service chains equipped with the specialized tools, software, and trained technician workforces required to service these advanced vehicle systems. The expansion of India’s SUV and premium hatchback segments, which now account for over 55% of total passenger vehicle sales, has elevated the average vehicle value and associated owner expectation for authorized service quality, brand-genuine parts usage, and service documentation that together drive replacement parts procurement through organized channels at average order values and gross margins substantially above the economy vehicle segment serviced predominantly through the unorganized workshop and bazaar channel.

Organized Multi-Brand Service Chain Expansion and Digital Automotive Retail Growth Formalizing Aftermarket Distribution and Capturing Bazaar Market Share

The organized automotive aftermarket service and parts distribution ecosystem is experiencing structural expansion through the simultaneous growth of OEM-authorized extended dealership service networks reaching tier-2 and tier-3 cities, the proliferation of tech-enabled multi-brand service chains deploying standardized service quality, digital jobcard management, and organized parts procurement across franchised workshop networks, and the rapid scaling of e-commerce automotive parts and accessories retail whose price transparency, authenticity assurance, and delivery convenience are progressively attracting parts purchases from the 40 to 45-year-old and younger vehicle owner demographic toward online procurement channels. The organized aftermarket penetration of India’s passenger car parts replacement market has grown from approximately 35% in 2018 to approximately 47% in 2025, driven by the increasing complexity of vehicle systems requiring authorized service tooling and software, the growing owner preference for service documentation supporting used vehicle resale value, and the government’s Motor Vehicles Amendment Act provisions strengthening consumer protection rights in automotive service transactions that favor organized service channel operators with documented service records and genuine parts supply chain accountability. The entry of Reliance Retail’s AutoZone concept, Tata group’s Tata Motors service extension programs, and Mahindra’s digital service ecosystem into organized multi-brand aftermarket parts retail and service is bringing the capital scale, brand trust, supply chain management expertise, and technology investment capacity of India’s largest conglomerates into a market historically fragmented among thousands of small independent parts distributors and workshop operators, creating a competitive dynamic that is accelerating the consolidation and formalization of India’s automotive aftermarket distribution structure through the forecast period.

Key Challenges

Counterfeit and Substandard Parts Proliferation Undermining Market Quality Integrity and Organized Channel Competitiveness

The India automotive aftermarket is severely impacted by the widespread availability of counterfeit, substandard, and misrepresented replacement parts circulating through the unorganized bazaar distribution network, with the Automotive Component Manufacturers Association of India estimating that counterfeit parts constitute approximately 25% to 35% of the total aftermarket parts volume in certain high-demand categories including filters, brake pads, spark plugs, bearings, and electricals, generating an annual revenue loss to legitimate branded parts manufacturers of approximately USD 1.2 billion while simultaneously creating significant vehicle safety, reliability, and warranty dispute implications for vehicle owners unknowingly installing non-compliant parts during maintenance events. The challenge of counterfeit part identification at the point of sale is acute for the vehicle owner and independent workshop mechanic community whose parts procurement decisions are primarily driven by price and physical appearance rather than quality verification through technical testing, chemical analysis, or supply chain authentication, allowing sophisticated counterfeit operations to produce visually convincing copies of branded parts at prices enabling significant discount to legitimate branded alternatives while maintaining adequate retail profit margins for participating bazaar traders. The enforcement capacity of India’s Intellectual Property Office, regional trade enforcement authorities, and the anti-counterfeiting teams operated by major parts manufacturers and OEM parts divisions is insufficient to systematically disrupt the scale and geographic distribution of counterfeit parts operations across India’s tens of thousands of spare parts retail clusters, requiring supplementary market-based approaches including QR code authentication, holographic packaging security features, and e-commerce platform seller authentication programs to progressively improve parts quality assurance at the retail point of purchase.

Highly Fragmented and Unorganized Distribution Infrastructure Limiting Supply Chain Efficiency and Organized Channel Reach in Tier-3 and Rural Markets

The India automotive aftermarket distribution infrastructure, while commercially extensive in its geographic reach through a network of approximately 4,200 automotive spare parts wholesale markets, over 500,000 retail parts outlets, and approximately 800,000 independent repair workshops, is characterized by extreme fragmentation and low organizational sophistication across the majority of its participating commercial entities, generating systemic inefficiencies in inventory management, credit financing, logistics, and parts authentication that elevate total distribution costs, extend supply lead times, and create quality inconsistency at retail that organized branded aftermarket suppliers cannot resolve through product quality investment alone without simultaneously transforming the distribution channel structure through which their parts reach end customers. The working capital constraints of the multi-tier distribution chain, in which parts travel through national distributor, regional distributor, sub-distributor, and retail outlet levels before reaching the mechanic or vehicle owner end customer, with each intermediary level applying markup and extending credit terms that collectively add 25% to 40% to the manufacturer’s ex-factory price before the product reaches the counter, create a price escalation dynamic that simultaneously reduces the price competitiveness of branded organized channel parts against bazaar alternatives and constrains the investment capacity of channel participants in inventory depth, storage quality, and business formalization. The geographic challenge of servicing tier-3, tier-4, and rural automotive markets, where India’s approximately 75 million rural two-wheelers and 12 million agricultural tractors generate substantial parts replacement demand but where the low purchase frequency per outlet, extended logistics timelines, and absence of cold chain and climate-controlled storage infrastructure for sensitive parts categories create commercially challenging supply conditions for organized channel operators accustomed to metro and tier-1 city distribution economics.

Electric Vehicle Transition and Changing Powertrain Technology Disrupting Traditional Parts Replacement Demand Structure and Distribution Channel Positioning

The accelerating penetration of electric vehicles in India’s two-wheeler and three-wheeler segments, with electric two-wheeler sales reaching approximately 1.05 million units in fiscal year 2024-25 representing approximately 5.2% of total two-wheeler sales and growing rapidly under FAME-II subsidy support and state government EV promotion schemes, is creating a structural disruption to the traditional aftermarket parts demand profile of the segments where EV adoption is advancing fastest, as electric powertrains eliminate the engine oil, spark plug, air filter, clutch, and fuel system maintenance requirements that collectively constitute a significant proportion of routine two-wheeler aftermarket service revenue at existing repair workshop and parts retail businesses. The limited repair serviceability of electric vehicle powertrain systems, whose battery packs, motor controllers, and integrated power electronics modules are designed as sealed replaceable units rather than field-repairable component assemblies, concentrates EV maintenance revenue in a small number of high-value battery health service and battery replacement events rather than the high-frequency low-value consumable replacement pattern of internal combustion engine maintenance, fundamentally altering the business model viability of independent workshops and spare parts retailers whose economic model depends on high-frequency small-transaction maintenance revenue from large vehicle population service volumes. The absence of adequate EV servicing training, battery testing and repair tooling, and EV parts supply chain infrastructure within the existing independent aftermarket workshop ecosystem, whose technical capability and tooling investment remains oriented toward internal combustion engine vehicle servicing, creates a service quality gap in the EV aftermarket that is concentrating early EV owner service revenue within OEM dealership networks and authorized service centers rather than distributing it across the broader independent workshop base that has historically captured a substantial share of routine vehicle maintenance expenditure.

Market Segmentation

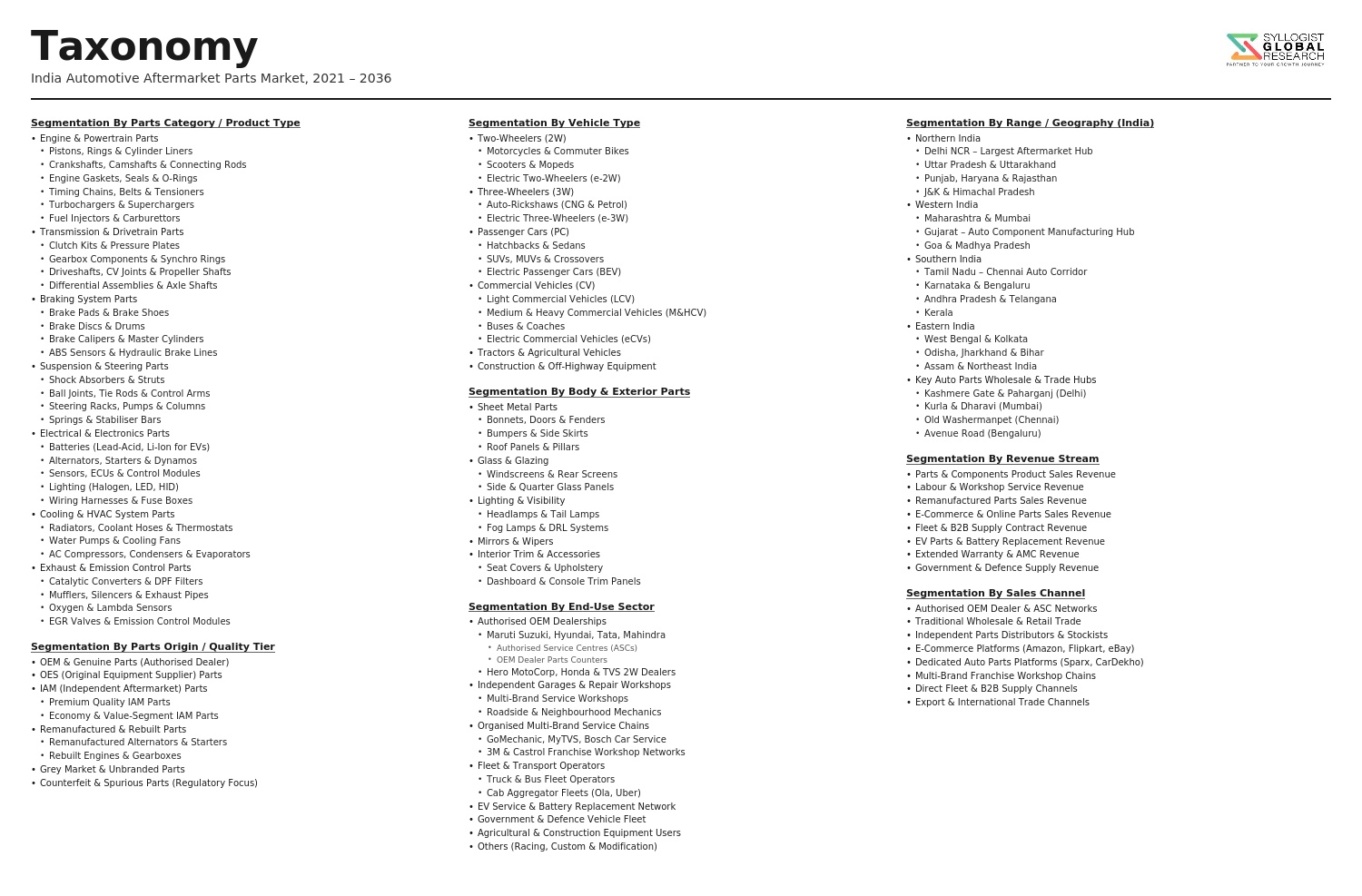

- Segmentation By Product Type

- Engine and Powertrain Components (Pistons, Valves, Bearings, Gaskets)

- Transmission and Drivetrain Parts (Clutch, Gearbox, Axle Components)

- Brake System Components (Pads, Shoes, Discs, Drums, Cylinders)

- Suspension and Steering Parts (Shock Absorbers, Bushes, Tie Rods)

- Electrical and Electronic Components (Alternators, Starters, Sensors, ECUs)

- Filters (Oil, Air, Fuel, Cabin Air)

- Tyres (Replacement and Retreaded)

- Batteries (Lead-Acid and Lithium-Ion)

- Lubricants, Oils, and Fluids

- Cooling System Components (Radiators, Thermostats, Water Pumps)

- Exhaust System Components

- Body Parts and Panels

- Accessories and Appearance Products

- Others

- Segmentation By Vehicle Type

- Two-Wheelers (Motorcycles and Scooters)

- Three-Wheelers (Passenger and Cargo)

- Passenger Cars

- Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles

- Light Commercial Vehicles (LCVs)

- Medium and Heavy Commercial Vehicles (Trucks and Buses)

- Tractors and Agricultural Equipment

- Electric Vehicles (Two-Wheeler and Four-Wheeler)

- Others

- Segmentation By Parts Origin

- OEM Genuine Parts (Dealer and Authorized Channel)

- Organized Branded Aftermarket Parts (IAM)

- Unbranded and Unorganized Bazaar Parts

- Remanufactured and Reconditioned Parts

- Imported Aftermarket Parts

- Others

- Segmentation By Distribution Channel

- OEM Authorized Dealership Service Networks

- Organized Multi-Brand Service Chains

- Independent Workshops and Roadside Mechanics

- Automotive Spare Parts Wholesale Markets and Bazaars

- E-Commerce and Online Automotive Retail Platforms

- Fleet Operator Direct Procurement

- Tyre and Battery Specialty Retail Chains

- Others

- Segmentation By Vehicle Age

- Under Warranty (0 to 3 Years)

- Post-Warranty Mid-Life (3 to 8 Years)

- Aging Fleet (8 to 15 Years)

- End-of-Life Vehicles (Above 15 Years)

- Others

- Segmentation By End User

- Individual Vehicle Owners

- Independent Repair Workshops and Garages

- Organized Fleet Operators and Logistics Companies

- Government and Defense Fleet Maintenance

- OEM and Authorized Dealership Service Departments

- Others

- Segmentation By Region

- Northern India (Delhi NCR, Uttar Pradesh, Punjab, Rajasthan)

- Western India (Maharashtra, Gujarat)

- Southern India (Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala)

- Eastern India (West Bengal, Odisha, Bihar)

- Central India (Madhya Pradesh, Chhattisgarh)

- Northeastern India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Automotive Aftermarket Parts Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by product type, vehicle type, parts origin, distribution channel, vehicle age category, and region, to enable component manufacturers, OEM parts divisions, multi-brand service chains, e-commerce platform operators, and aftermarket investors to identify which product categories, vehicle segments, and channel formats will generate the highest absolute revenue growth and most commercially defensible market positions across the forecast period?

- What is the current market share split between the organized genuine parts channel, organized branded independent aftermarket, unorganized bazaar parts supply, and e-commerce online retail across the major vehicle type and product category segments of the Indian aftermarket, and what is the projected channel share evolution through 2034 as digitalization, vehicle complexity increase, organized service chain expansion, and government anti-counterfeiting enforcement collectively shift demand from unorganized toward organized distribution channels?

- How is the accelerating penetration of electric two-wheelers and three-wheelers in India restructuring the maintenance and parts replacement demand profile of the two-wheeler and three-wheeler aftermarket segments, what is the projected net impact of EV penetration on total aftermarket parts revenue per vehicle across these segments through 2034, and what new aftermarket product categories, service capabilities, and distribution infrastructure investments are required from organized channel operators to capture EV-specific maintenance revenue as the electric fleet grows?

- How are India’s BS VI emission standard requirements, the adoption of direct injection and turbocharged petrol engines, growing ADAS feature content, and the shift toward automatic and CVT transmission platforms in the passenger car segment collectively raising the technical complexity and average repair order value of passenger car aftermarket service events, and how are organized dealership service networks, multi-brand service chains, and independent workshops differentiating their technical capability investment and parts procurement strategies to capture the premium maintenance expenditure of India’s increasingly complex and higher-value vehicle population?

- Who are the leading Indian and multinational automotive component manufacturers supplying the organized aftermarket including Bosch India, Minda Industries, Motherson Group, Varroc Engineering, Endurance Technologies, and specialty parts manufacturers, the OEM parts distribution arms of Maruti Suzuki, Tata Motors, Mahindra, Hero MotoCorp, and Bajaj Auto, the multi-brand service chain operators, and the major e-commerce automotive retail platforms currently defining the competitive landscape of the India automotive aftermarket parts market, and what are their respective product portfolios, distribution network reach, channel investment strategies, digital platform development programs, EV aftermarket positioning, and competitive responses to the ongoing formalization and digitalization of India’s automotive aftermarket distribution infrastructure through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Counterfeit Parts, Unorganised Sector & GST Evasion Risk

- EV Transition, Declining ICE Vehicle Base & Obsolescence Risk

- Supply Chain Disruption, Import Dependency & Logistics Risk

- Digital Disruption, E-Commerce Price Erosion & Margin Compression Risk

- Regulatory, BIS Certification & Quality Standard Enforcement Risk

- Regulatory Framework & Standards

- Motor Vehicles Act, AIS Standards & Compulsory Type Approval Framework for Automotive Parts

- BIS Certification, IS Standards & Mandatory Quality Marking Requirements for Aftermarket Components

- GST Framework, Harmonised System (HS) Codes & Tax Structure Applicable to Automotive Parts Distribution

- End-of-Life Vehicle (ELV) Policy, Scrappage Programme & Remanufacturing Regulatory Framework

- Consumer Protection, Warranty Obligations, IPR & Anti-Counterfeiting Enforcement Standards

- India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Product Type

- Engine Parts (Filters, Pistons, Gaskets, Timing Belts & Engine Management)

- Tyres & Wheels (Replacement Tyres, Tubes, Alloy Wheels & Accessories)

- Brakes & Suspension (Pads, Discs, Drums, Shock Absorbers & Struts)

- Electrical & Battery (Batteries, Alternators, Starters & Wiring Harnesses)

- Transmission & Drivetrain (Clutch, Gearbox, Driveshaft & CV Joints)

- Body & Exterior Parts (Bumpers, Mirrors, Lamps, Wipers & Panels)

- HVAC & Comfort Parts (AC Compressors, Blowers, Filters & Thermostats)

- Lubricants, Fluids & Chemicals (Engine Oil, Brake Fluid, Coolant & Additives)

- EV-Specific Parts (Battery Modules, Charging Components, BMS & Inverters)

- Market Size & Forecast by Vehicle Type

- Two-Wheeler (Motorcycles & Scooters)

- Three-Wheeler (Auto-Rickshaw, Cargo Three-Wheeler)

- Passenger Vehicle (Hatchback, Sedan, SUV & MPV)

- Light Commercial Vehicle (LCV)

- Medium & Heavy Commercial Vehicle (M&HCV)

- Electric Vehicle (2W EV, 3W EV, 4W EV & Commercial EV)

- Market Size & Forecast by Parts Origin

- OEM Genuine Parts

- Independent Aftermarket (IAM) Parts

- Remanufactured & Rebuilt Parts

- Second-Hand & Salvage Parts

- Market Size & Forecast by Distribution Channel

- Authorised OEM Dealer & Service Network

- Independent Auto Parts Retailers & Distributors

- Online Retail & E-Commerce Platforms

- Multi-Brand Service Chains & Franchise Networks

- Roadside Mechanics & Unorganised Workshops

- Market Size & Forecast by End-User

- Individual Vehicle Owners (DIY & Do-It-For-Me)

- Independent Workshops & Roadside Service Centres

- Fleet Operators (Taxi, Logistics, Bus & Commercial Fleets)

- Insurance Repair & Accidental Parts Replacement

- Government & Institutional Fleets

- Market Size & Forecast by Sales Channel

- Offline Traditional Trade (Wholesale Distributors & Retail Stockists)

- Online Direct-to-Consumer (D2C) & Platform-Based E-Commerce

- B2B Fleet & Institutional Procurement

- Subscription-Based Maintenance & AMC (Annual Maintenance Contract) Channel

- North India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- By State

- Market Size & Forecast

- South India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- By State

- Market Size & Forecast

- West India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- By State

- Market Size & Forecast

- East India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- By State

- Market Size & Forecast

- Central India Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- By State

- Market Size & Forecast

- State-Wise* Automotive Aftermarket Parts Market Outlook

- Market Size & Forecast

- By Value

- By Product Type

- By Vehicle Type

- By Parts Origin

- By Distribution Channel

- By End-User

- By Sales Channel

- Market Size & Forecast

*States Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Delhi, Karnataka, Tamil Nadu, Gujarat, Rajasthan, Uttar Pradesh, Telangana, West Bengal, Haryana, Madhya Pradesh, Kerala, Punjab, Andhra Pradesh, Bihar

- Technology Landscape & Innovation Analysis

- Digital Aftermarket Platforms, E-Commerce & Online Parts Retail Technology Deep-Dive

- Telematics, Predictive Maintenance & Connected Vehicle Aftermarket Technology

- Remanufacturing, Refurbishment & Circular Economy Technologies for Auto Parts

- 3D Printing & Additive Manufacturing for On-Demand Parts Production

- Diagnostics, OBD-II Tools & AI-Based Vehicle Health Monitoring Platforms

- EV Battery Servicing, Second-Life Battery Technology & Charging Component Innovation

- Blockchain, Track & Trace & Anti-Counterfeiting Technology in Auto Parts Supply Chain

- Patent & IP Landscape in Automotive Aftermarket Parts Technologies

- Value Chain & Supply Chain Analysis

- OEM Parts Manufacturing, In-House Captive Supply & Authorized Dealer Network

- Independent Aftermarket (IAM) Manufacturer, Tier-1 & Tier-2 Supplier Chain

- Wholesale Distributor, Regional Stockist & Tier Distribution Network

- Independent Workshops, Multi-Brand Service Centers & Roadside Mechanic Channel

- Online Retail Platforms, Aggregators & Digital Aftermarket Marketplace Channel

- Fleet Operators, Insurance Companies & Institutional B2B Procurement Channel

- Remanufacturer, Recycler & End-of-Life Vehicle (ELV) Parts Recovery Channel

- Pricing Analysis

- OEM Genuine vs. IAM Parts Price Differential Analysis by Product Category

- Price Analysis by Vehicle Type (2W, PV, CV & EV Parts Pricing Trends)

- Distribution Margin, Channel Mark-Up & Trade Pricing Structure Analysis

- Online vs. Offline Pricing Dynamics & E-Commerce Price Competitiveness

- Remanufactured, Rebuilt vs. New Parts Price Competitiveness Analysis

- GST Impact, Landed Cost & Import Duty Effect on Aftermarket Parts Pricing

- Sustainability & Environmental Analysis

- Remanufacturing, Refurbishment & Circular Economy Contribution of the Aftermarket Parts Industry

- ELV Scrappage Policy Impact on Aftermarket Parts Availability & Recycled Content

- EV Battery Second-Life, Recycling & Sustainable Parts Ecosystem Development

- Carbon Footprint of Aftermarket Parts Production vs. OEM Original Parts Manufacturing

- Green Workshop Standards, Hazardous Waste Management & Environmental Compliance in Servicing

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Organised vs. Unorganised Sector by Product & Channel)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Product Type, Channel & Region

- Player Classification

- OEM Authorized Parts Suppliers & Captive Dealer Networks

- Independent Aftermarket (IAM) Manufacturers & Branded Parts Suppliers

- Tyre Manufacturers & Replacement Tyre Specialists

- Battery & Electrical Parts Manufacturers

- Online Aftermarket Platforms, E-Commerce Aggregators & Digital Retailers

- Remanufacturers, Rebuilders & Circular Economy Parts Specialists

- Multi-Brand Service Chain Operators & Franchise Workshop Networks

- Competitive Analysis Frameworks

- Market Share Analysis by Product Type, Channel & Region

- Company Profile

- Company Overview & Headquarters

- Aftermarket Parts Product & Brand Portfolio

- Key Customer Relationships & Distribution Partnerships

- Manufacturing Footprint & Production Capacity

- Revenue (Aftermarket Segment) & Sales Volume

- Technology Differentiators & Quality Certifications (BIS, OEM Approved)

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Capacity Expansion, E-Commerce Entry)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Quality vs. Price Competitiveness)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Product Type, Vehicle Type, Parts Origin, Channel & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output