Market Definition

The India Automotive Sensors Market encompasses the design, engineering, manufacturing, calibration, and supply of electronic and electromechanical sensing devices integrated across two-wheelers, three-wheelers, passenger vehicles, light commercial vehicles, medium and heavy commercial vehicles, tractors, and electric vehicles produced and sold within India that measure, detect, and transmit critical physical, thermal, chemical, positional, and kinetic parameters to electronic control units, engine management systems, transmission control modules, battery management systems, body control modules, and advanced driver assistance system processors for the purpose of optimising powertrain performance, enforcing Bharat Stage VI emission compliance, activating passive and active safety systems, managing battery state and thermal conditions in electrified powertrains, and enabling the growing portfolio of driver assistance and connected vehicle functions entering volume production across Indian vehicle platforms. The market includes engine management sensors such as oxygen sensors, mass air flow sensors, manifold absolute pressure sensors, crankshaft and camshaft position sensors, knock sensors, coolant temperature sensors, and throttle position sensors; safety and chassis sensors encompassing wheel speed sensors for anti-lock braking and electronic stability control systems, steering angle sensors, yaw rate sensors, and tyre pressure monitoring system sensors; exhaust aftertreatment sensors including nitrogen oxide sensors, exhaust gas temperature sensors, and differential pressure sensors mandated by Bharat Stage VI Phase 2 on-board diagnostics regulations; advanced driver assistance system sensors comprising radar modules, camera systems, and ultrasonic parking sensors; and electric vehicle-specific sensors including battery current, cell temperature, voltage, isolation resistance, and motor position sensing devices. The market covers both original equipment supply to vehicle manufacturers through Tier-1 supplier channels and aftermarket replacement sensor demand serviced through dealer networks, independent parts distributors, and e-commerce platforms. Key participants include global sensor technology companies with India presence, domestic Indian sensor manufacturers, Tier-1 automotive system integrators, vehicle OEMs, and regulatory bodies whose Bharat Stage VI, AIS, and BIS standards govern mandatory sensor performance and certification requirements in the Indian automotive market.

Market Insights

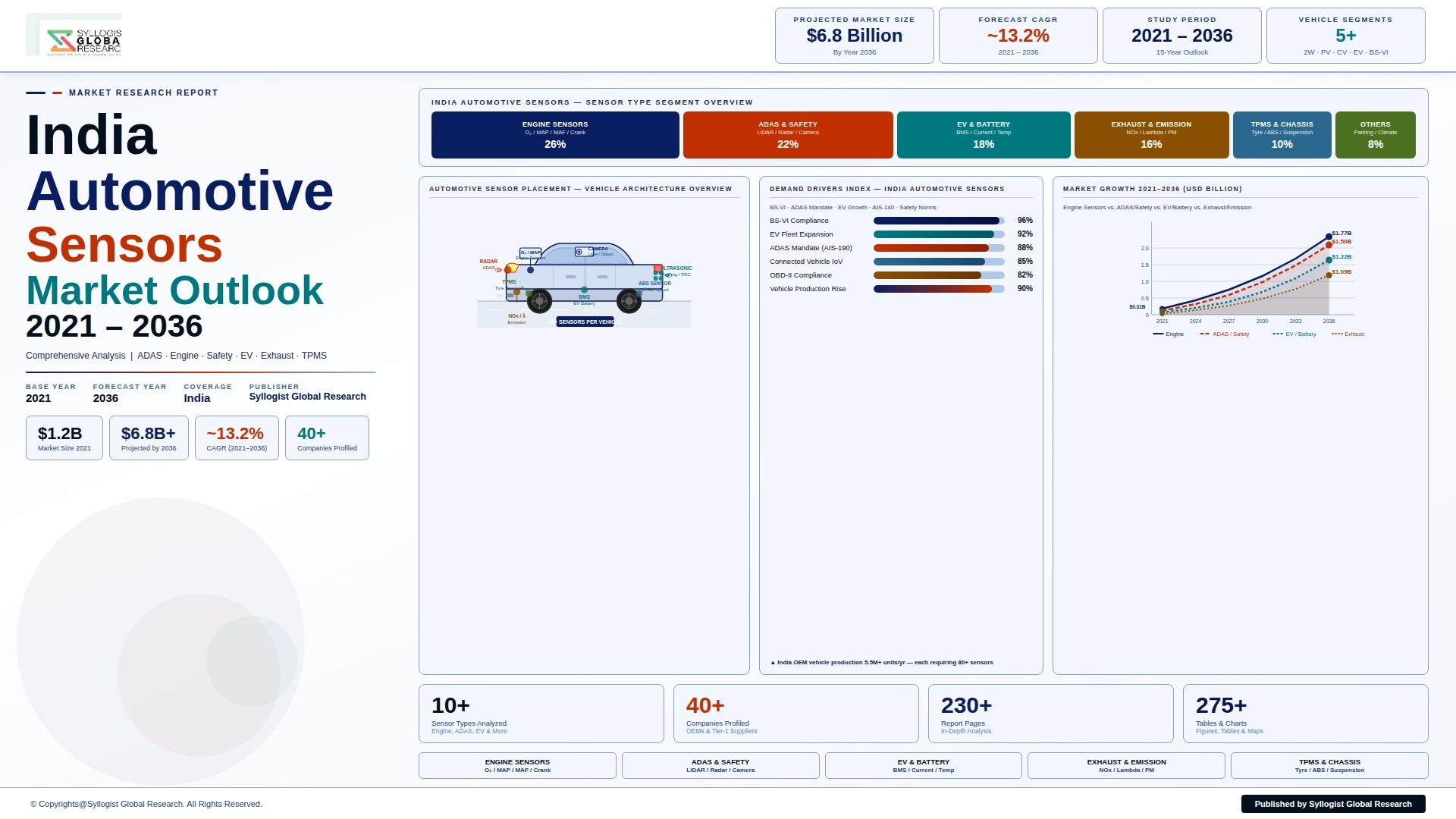

The India automotive sensors market was valued at approximately USD 1.2 billion in 2024 and is projected to reach USD 6.8 billion by 2036, advancing at a compound annual growth rate of approximately 13.2% through the forecast period, driven by the deepening enforcement of Bharat Stage VI Phase 2 on-board diagnostics regulations, the accelerating adoption of electric vehicles across two-wheeler, three-wheeler, and passenger vehicle segments, and the progressive introduction of advanced driver assistance system mandates that are structurally expanding per-vehicle sensor content across all major vehicle categories. India’s total vehicle production reached approximately 5.6 million four-wheelers and 21.4 million two-wheelers and three-wheelers in 2024, positioning India as the third-largest vehicle manufacturing nation globally and creating a high-volume domestic sensor procurement market that is attracting sustained investment from global sensor technology companies seeking to localise engineering and manufacturing capability within the Indian Tier-1 automotive supply chain to serve both domestic OEM requirements and export-oriented component programs.

The enforcement of Bharat Stage VI Phase 2 on-board diagnostics requirements from April 2023 has materially elevated the mandatory sensor content of every new four-wheeler entering Indian roads, requiring permanent monitoring systems that continuously assess catalytic converter efficiency, oxygen sensor degradation, exhaust gas recirculation valve function, and diesel particulate filter loading through a sensor network of significantly greater density and diagnostic precision than the architectures deployed under pre-BS-VI emission control frameworks. Phase 2 OBD compliance necessitates upstream and downstream oxygen sensors for catalyst efficiency monitoring, nitrogen oxide sensors for diesel vehicles equipped with selective catalytic reduction aftertreatment, exhaust gas temperature sensors at multiple aftertreatment positions, mass air flow sensors with charge air monitoring capability, and manifold pressure sensors integrated into turbocharger control logic, collectively adding an estimated USD 52 of mandatory emission monitoring sensor content per four-wheeler relative to the pre-BS-VI vehicle baseline.

The accelerating penetration of electric vehicles across India’s automotive market is introducing a distinct and high per-unit-value sensor architecture centred on battery management, motor control, thermal regulation, and isolation monitoring that generates new demand streams for battery current sensors, cell temperature sensor arrays, battery voltage sensors, isolation resistance monitors, motor position resolvers, and inverter temperature sensors that are structurally incremental to rather than substitutes for conventional powertrain sensor demand. Electric two-wheelers reached approximately 1.06 million units in fiscal year 2024 while passenger electric vehicles reached approximately 0.09 million units and electric three-wheelers constituted approximately 0.68 million units, with combined electric vehicle production introducing an estimated 28 to 35 distinct battery and motor management sensor types per vehicle and establishing the electric vehicle sensor architecture as the fastest growing individual sub-segment within the broader India automotive sensors market across the forecast horizon.

The progressive tightening of vehicle safety regulations through Automotive Industry Standard AIS-190 governing autonomous emergency braking, the mandatory fitment of six airbags in passenger vehicles from October 2023, and the Government of India’s stated policy intent to mandate front-facing camera and radar systems on new vehicles through a phased regulatory programme are collectively creating a structural demand increment for advanced driver assistance sensor hardware that is fundamentally different in technology content and unit value from conventional engine and emission sensor demand. Front-facing monocular camera modules priced at approximately USD 22 per unit at the OEM supply level, short-range ultrasonic parking sensors averaging USD 3.5 per unit, and 77-gigahertz front radar modules valued at approximately USD 78 per unit represent the primary advanced driver assistance sensor categories entering volume fitment across Indian passenger vehicle platforms, with the cumulative ADAS sensor content per vehicle projected to increase from approximately USD 38 in 2024 to USD 142 by 2036 as regulatory mandates broaden across vehicle categories.

Key Drivers

Bharat Stage VI Phase 2 On-Board Diagnostics Mandate and Escalating Emission Monitoring Sensor Content Requirements Across All New Four-Wheeler Vehicle Categories

The mandatory enforcement of Bharat Stage VI Phase 2 OBD-II requirements across all new four-wheelers sold in India from April 2023 has established a structurally higher baseline sensor content per vehicle that is irreversible within the forecast period and creates a durable, regulation-driven revenue foundation for emission and engine management sensor suppliers operating in the Indian automotive market. The BS-VI Phase 2 OBD architecture requires a minimum of two oxygen sensors per petrol vehicle, at least one nitrogen oxide sensor per diesel vehicle equipped with selective catalytic reduction, up to four exhaust gas temperature sensors per diesel vehicle monitoring catalyst light-off and protection functions, particulate matter sensors on diesel particulate filter-equipped vehicles, and expanded manifold pressure sensor arrays integrated into variable geometry turbocharger control systems, collectively representing a sensor content increase of approximately USD 52 to USD 68 per four-wheeler relative to the pre-BS-VI emission monitoring architecture. This compliance-driven sensor content floor is applicable to every new four-wheeler regardless of powertrain configuration among non-electric vehicles, establishing a guaranteed minimum sensor procurement volume per vehicle that grows in step with total four-wheeler production volumes irrespective of individual OEM technology strategy decisions, providing emission sensor suppliers with a production-volume-linked demand baseline of high structural predictability across the forecast period.

Accelerating Electric Vehicle Adoption Creating Structurally New and High-Value Battery Management, Motor Control, and Thermal Regulation Sensor Demand Across Two-Wheeler, Three-Wheeler, and Passenger Vehicle Segments

The rapid expansion of India’s electric vehicle market is generating a category of automotive sensor demand that is entirely incremental to conventional internal combustion engine sensor procurement, with each battery electric vehicle introducing a sensor architecture valued at approximately USD 95 to USD 180 per vehicle in battery management, motor control, thermal regulation, and isolation monitoring sensor content that has no equivalent in the conventional powertrain sensor bill of materials and therefore represents pure additive market expansion rather than substitutive displacement of existing sensor revenue. Battery management system sensor arrays in electric vehicles include individual cell voltage monitoring integrated circuits, NTC thermistor temperature sensor arrays monitoring thermal uniformity across battery cell groups, hall-effect current sensors measuring charge and discharge current for state-of-charge calculation, isolation resistance monitors ensuring battery pack electrical isolation from the vehicle chassis meets minimum safety thresholds, and motor position resolvers providing rotor position feedback for field-oriented motor control algorithms. The combined electric vehicle sector production in India reached approximately 1.83 million units in fiscal year 2024 across two-wheeler, three-wheeler, and passenger vehicle categories and is projected to reach 8.4 million units by 2036, establishing a structurally expanding high-value sensor demand base that is growing substantially faster than overall automotive production volumes and commanding per-vehicle sensor content values that are two to four times higher than equivalent conventional two-wheeler sensor content levels.

Progressive ADAS Safety Regulation, AIS-190 Automatic Emergency Braking Mandate, and Six-Airbag Requirement Structurally Expanding Per-Vehicle Camera, Radar, and Ultrasonic Sensor Content Across Indian Vehicle Platforms

The Government of India’s progressive tightening of vehicle safety standards through Automotive Industry Standard AIS-190 governing autonomous emergency braking and forward collision warning systems, the mandatory six-airbag requirement for passenger vehicles enforced from October 2023 that requires crash sensor, impact sensor, and accelerometer arrays of greater complexity than single or dual-airbag architectures, and the regulatory roadmap toward mandatory front-facing camera fitment on new vehicles are collectively creating a structural demand expansion for advanced driver assistance sensor hardware expected to add an estimated USD 85 to USD 145 of incremental ADAS sensor content per new passenger vehicle by 2030 relative to the average sensor content baseline of 2024-era vehicles. The 77-gigahertz front radar module required for autonomous emergency braking compliance represents the highest per-unit value ADAS sensor category entering mass fitment across Indian OEM vehicle programs, with unit pricing at approximately USD 78 per module at the Tier-1 supply level and vehicle penetration projected to expand from approximately 8% of new passenger vehicle production in 2024 to over 45% by 2030 as AIS-190 Phase 1 and Phase 2 compliance deadlines approach, creating a radar module procurement volume increment of substantial absolute scale within the Indian automotive sensor market across the forecast period.

Key Challenges

High Import Dependency on Semiconductor-Intensive Sensor Components, Limited Domestic Manufacturing Ecosystem, and Vulnerability to Supply Chain Disruptions for Advanced Automotive Sensor Technologies

The India automotive sensors market operates under a structural import dependency that exposes vehicle manufacturers, Tier-1 suppliers, and vehicle buyers to supply chain vulnerabilities and cost escalation risks that are difficult to mitigate within the contractually constrained pricing frameworks governing OEM component supply agreements. Advanced automotive sensor categories including 77-gigahertz radar modules, monocular and stereo camera system-on-chip processors, MEMS-based inertial measurement units for electronic stability control, and nitrogen oxide sensor ceramic elements are manufactured by a globally concentrated supply base in Japan, Germany, the United States, and South Korea, with virtually no domestic Indian manufacturing presence in the semiconductor and ceramic sensor element segments that constitute the majority of sensor unit cost. The semiconductor supply disruption of 2021-2022 reduced Indian passenger vehicle production by an estimated 0.8 million units due to sensor and electronic control unit shortages, demonstrating the operational vulnerability of the Indian automotive supply chain to disruptions in global sensor semiconductor supply chains over which Indian OEMs and Tier-1 suppliers exercise no meaningful control. While the Government of India’s Production Linked Incentive schemes for semiconductors and electronics are beginning to catalyse investment in domestic electronics manufacturing, the lead time required to establish a globally competitive domestic automotive sensor semiconductor manufacturing ecosystem is measured in decades rather than years, leaving the Indian automotive sensor market structurally exposed to import dependency and associated exchange rate, logistics, and geopolitical risks across the forecast period.

Intense OEM Cost-Down Pressure, Price Sensitivity Across the Two-Wheeler and Entry-Level Passenger Vehicle Segments, and Structural Margin Compression for Automotive Sensor Suppliers

The India automotive market is characterised by a uniquely intense cost optimisation culture driven by the dominance of the price-sensitive two-wheeler segment, which constitutes over 75% of total vehicle unit production and in which the average vehicle selling price ranges from approximately USD 900 to USD 2,800, creating a vehicle economics framework within which OEM procurement teams exercise relentless pressure to reduce per-sensor supply prices to the minimum level consistent with regulatory compliance and functional performance requirements. Two-wheeler OEMs operating in India impose sensor procurement cost targets that are typically 30% to 50% below the equivalent sensor supply prices accepted by passenger vehicle OEMs in European and North American markets, compressing the revenue and margin available to sensor suppliers on high-volume two-wheeler sensor programs to levels that make investment in advanced manufacturing technology, quality systems, and application engineering difficult to justify on program economics alone. The entry-level passenger vehicle segment, which accounted for approximately 42% of passenger car sales volumes in India in 2024, similarly imposes OEM sensor cost targets that restrict the ability of Tier-1 suppliers to specify technically superior sensor technologies in applications where a lower-cost alternative achieves minimum regulatory compliance, effectively limiting the penetration of advanced sensing technologies in the highest-volume vehicle categories and constraining the pace of per-vehicle sensor content escalation across the Indian automotive market relative to premium vehicle segments in developed markets.

EV Transition Disrupting Conventional Powertrain Sensor Demand While Creating Technology Transition Uncertainty and Investment Risk for Established Internal Combustion Engine Sensor Suppliers

Established automotive sensor suppliers whose India revenue is concentrated in internal combustion engine management sensor categories, specifically oxygen sensors, mass air flow sensors, crankshaft position sensors, knock sensors, and EGR valve position sensors, face a medium-to-long-term structural demand erosion as the accelerating penetration of battery electric vehicles progressively displaces conventional powertrain sensor demand from new vehicle production volumes, creating a product portfolio transition challenge that requires simultaneous management of declining conventional sensor programs and investment in electric vehicle sensor architectures requiring fundamentally different manufacturing technologies, materials, and calibration capabilities. The transition challenge is compounded by uncertainty surrounding the pace of electric vehicle adoption in the two-wheeler segment, which is the largest individual vehicle category in India by volume and which determines the aggregate conventional versus electric powertrain sensor demand split more decisively than passenger vehicle electrification trends. While electric two-wheeler penetration reached approximately 5% of total two-wheeler sales in fiscal year 2024, the pace of penetration acceleration is sensitive to battery raw material cost trajectories, government subsidy policy continuity under successive FAME programme frameworks, and charging infrastructure availability in tier-2 and tier-3 cities where the majority of two-wheeler sales occur, creating investment planning uncertainty for sensor suppliers who must calibrate their internal combustion engine sensor capacity reduction and electric vehicle sensor capacity expansion strategies against a demand transition timeline of meaningful uncertainty across the forecast period.

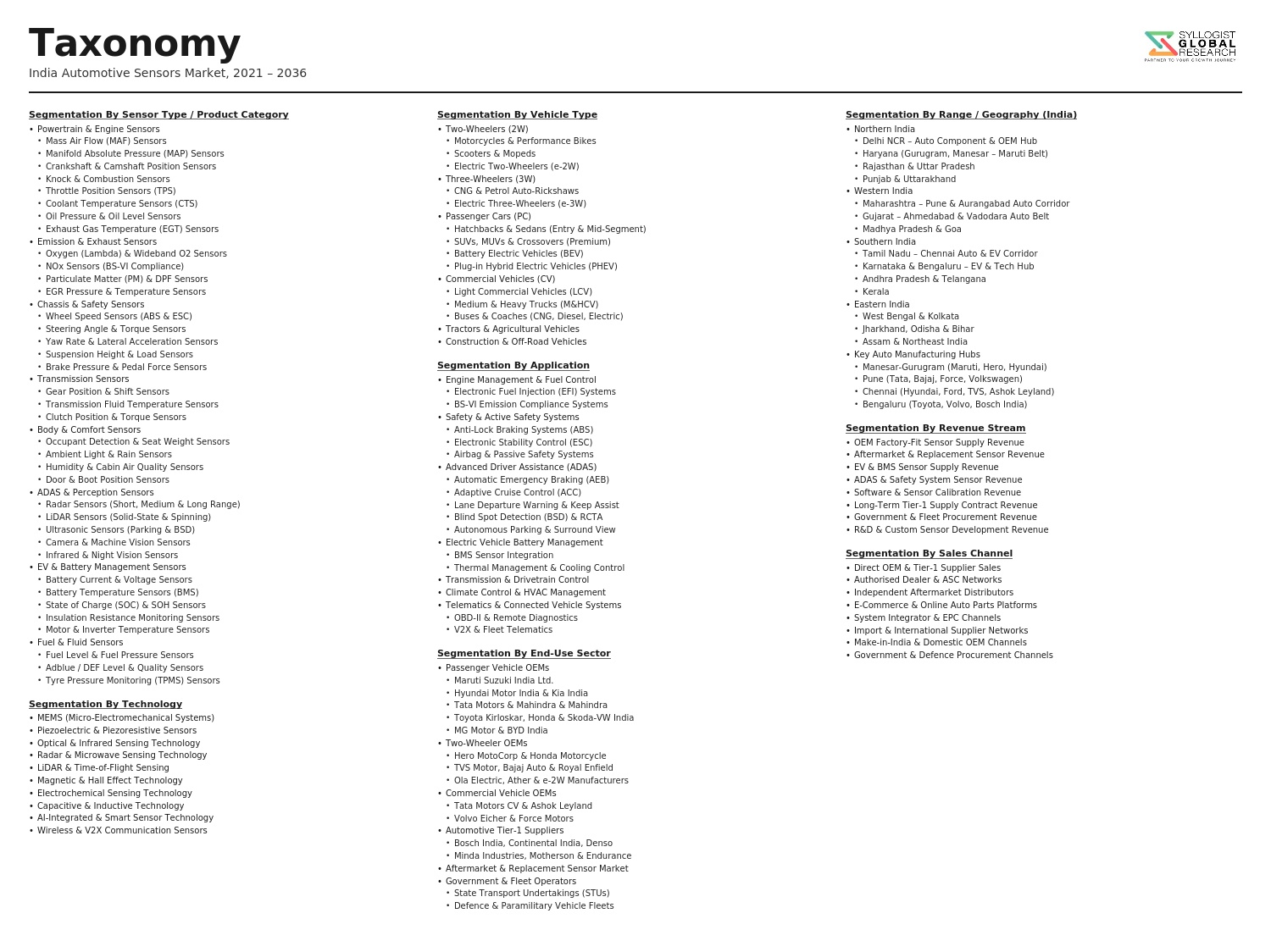

Market Segmentation

- Segmentation By Sensor Type

- Oxygen Sensors (Wideband and Narrowband)

- Mass Air Flow Sensors

- Manifold Absolute Pressure Sensors

- Crankshaft and Camshaft Position Sensors

- Knock Sensors

- Coolant Temperature Sensors

- Throttle Position Sensors

- Wheel Speed Sensors (ABS and ESC)

- Nitrogen Oxide Sensors

- Exhaust Gas Temperature Sensors

- Tyre Pressure Monitoring System (TPMS) Sensors

- Radar Sensors (Short Range, Medium Range, and Long Range)

- Camera Sensors (Monocular and Stereo)

- Ultrasonic Proximity Sensors

- Battery Current Sensors (EV)

- Battery Temperature Sensors (EV)

- Motor Position Sensors (EV)

- Others

- Segmentation By Technology

- MEMS (Micro-Electro-Mechanical Systems) Based Sensors

- Wired Sensors (Conventional Analog and Digital Output)

- Wireless and IoT-Enabled Sensors

- Smart Sensors with On-Board Processing Capability

- Others

- Segmentation By Vehicle Type

- Two-Wheelers (Motorcycles and Scooters)

- Three-Wheelers (Passenger and Cargo)

- Passenger Vehicles (Hatchback, Sedan, and SUV)

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Electric Two-Wheelers

- Electric Three-Wheelers

- Electric Passenger Vehicles

- Tractors and Off-Highway Vehicles

- Others

- Segmentation By Application

- Engine Management and Emission Control

- Exhaust Aftertreatment and OBD Monitoring

- Safety and Chassis Control (ABS, ESC, and Airbag Systems)

- Advanced Driver Assistance Systems (ADAS)

- Tyre Pressure Monitoring

- Battery Management (EV)

- Motor and Inverter Control (EV)

- Thermal Management

- Body Control and Comfort

- Others

- Segmentation By Distribution Channel

- OEM Direct Supply through Tier-1 Automotive Suppliers

- Authorised Dealer and Service Network

- Independent Aftermarket Distributors and Wholesalers

- Online and E-Commerce Platforms

- Others

- Segmentation By End-User

- Passenger Vehicle OEMs

- Two-Wheeler and Three-Wheeler OEMs

- Commercial Vehicle OEMs

- Electric Vehicle OEMs

- Aftermarket Service Providers and Independent Repair Workshops

- Fleet Operators

- Others

- Segmentation By Region

- North India

- South India

- West India

- East India

- Central India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2036

Key Questions this Study Will Answer

- What is the total India automotive sensors market valuation in the base year 2025, and what is the projected market size and compound annual growth rate through 2036, disaggregated by sensor type across oxygen sensors, mass air flow sensors, nitrogen oxide sensors, radar modules, camera systems, battery management sensors, and TPMS sensors, and by vehicle type across two-wheelers, passenger vehicles, commercial vehicles, and electric vehicles, to enable sensor manufacturers, automotive OEMs, Tier-1 system integrators, and investors to identify which sensing technology categories and vehicle segment combinations will generate the highest absolute revenue growth and the most defensible demand trajectory across the forecast period in the context of simultaneous BS-VI OBD escalation, electric vehicle penetration growth, and ADAS regulatory mandate implementation?

- How is the enforcement of Bharat Stage VI Phase 2 on-board diagnostics requirements reshaping the mandatory sensor content specification of new four-wheelers across petrol and diesel powertrain categories in India, what is the estimated per-vehicle emission monitoring sensor content increase relative to the pre-BS-VI architecture baseline, which specific sensor types including nitrogen oxide sensors, exhaust gas temperature sensors, particulate matter sensors, and upstream and downstream oxygen sensors are experiencing the greatest volume and revenue growth as a direct result of Phase 2 OBD compliance requirements, and how are domestic Tier-1 suppliers and global sensor companies repositioning their India product portfolios and manufacturing localisation strategies to capture the structurally guaranteed emission sensor demand created by BS-VI Phase 2 enforcement across the forecast period?

- What is the projected market size, compound annual growth rate, and per-vehicle sensor content valuation of the electric vehicle sensor segment in India through 2036, encompassing battery management system sensors, motor position sensors, inverter temperature sensors, and isolation resistance monitors across electric two-wheelers, electric three-wheelers, and electric passenger vehicles, and how are the simultaneous demand dynamics of declining internal combustion engine sensor volumes in conventional powertrain categories and accelerating electric vehicle sensor content growth expected to reshape the total India automotive sensor market revenue composition between 2025 and 2036 across vehicle type, sensor type, and Tier-1 supplier categories?

- How is the Government of India’s progressive ADAS safety regulation roadmap under Automotive Industry Standard AIS-190 governing autonomous emergency braking, the mandatory six-airbag requirement for passenger vehicles, and the anticipated camera and radar fitment mandates expected to expand per-vehicle ADAS sensor content across passenger vehicle platforms in India through 2036, what is the projected volume and revenue trajectory of 77-gigahertz front radar modules, monocular camera systems, and ultrasonic parking sensor arrays as regulatory mandate penetration expands from approximately 8% of new passenger vehicle production to broader market coverage, and which global radar and camera sensor technology companies are best positioned to capture dominant supply positions within the India ADAS sensor market as fitment rates scale?

- Who are the leading automotive sensor manufacturers, Tier-1 system integrators, and domestic Indian sensor companies currently defining the competitive landscape of the India automotive sensors market, and what are their respective sensor technology portfolios across engine management, emission control, safety, ADAS, and electric vehicle sensor categories, manufacturing and engineering localisation footprints in India, OEM program supply relationships with major Indian vehicle manufacturers including two-wheeler and electric vehicle OEMs, strategies for navigating the simultaneous challenge of BS-VI compliance sensor demand growth and electric vehicle sensor architecture investment requirements, and competitive positioning relative to both global MNC sensor companies and emerging domestic Indian sensor manufacturing initiatives supported through Production Linked Incentive schemes and the Atmanirbhar Bharat automotive component localisation programme?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- EV Transition, ADAS Technology Disruption & ICE Sensor Obsolescence Risk

- Semiconductor & Sensor Chip Import Dependency, Supply Shortage & Geopolitical Risk

- Localisation, PLI Scheme Execution & Domestic Sensor Manufacturing Scale-Up Risk

- BS-VI, Upcoming Emission Norms & Rapidly Changing Regulatory Compliance Risk

- Cybersecurity, Data Privacy & Connected Vehicle Vulnerability Risk

- Regulatory Framework & Standards

- BS-VI Emission Norms, OBD Compliance & Mandatory Engine and Exhaust Sensor Fitment Standards

- AIS-190 ADAS Mandate, AIS-140 Fleet Telematics & Compulsory Sensor Fitment Regulations for New Vehicles

- PLI Scheme for Automotive Components & Sensor Localisation Policy Framework

- EV Policy (FAME II, PM E-Drive), Battery Safety Standards (AIS-048, AIS-156) & BMS Sensor Requirements

- Automotive Data Security, Cybersecurity Standards & CERT-In Framework for Connected Vehicle Sensors

- India Automotive Sensors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Sensor Type

- Engine Management Sensors (O2, MAP, MAF, Crankshaft Position, Knock & Camshaft Sensors)

- ADAS & Safety Sensors (Radar, Camera, LiDAR, Ultrasonic & IMU Sensors)

- EV & Battery Management Sensors (Current, Voltage, Temperature & Cell Monitoring Sensors)

- Exhaust & Emission Sensors (NOx, Lambda, Particulate Matter & EGR Sensors)

- Tyre Pressure Monitoring System (TPMS) Sensors

- Chassis & Suspension Sensors (ABS Wheel Speed, Ride Height & Steering Angle Sensors)

- Parking & Proximity Sensors (Ultrasonic Parking, Blind Spot & Reversing Camera Sensors)

- HVAC & Comfort Sensors (Cabin Temperature, Humidity, Sunlight & Air Quality Sensors)

- Fuel & Fluid Level Sensors (Fuel Level, Oil Pressure, Coolant Temperature & Brake Fluid Sensors)

- Market Size & Forecast by Technology

- MEMS-Based Sensors (Micro-Electro-Mechanical Systems)

- Radar Sensors (Short, Medium & Long Range)

- Camera & Machine Vision Sensors (Monocular, Stereo & Surround View)

- Ultrasonic Sensors

- LiDAR Sensors (Mechanical & Solid-State)

- Electrochemical & Optical Sensors (Lambda, NOx & PM)

- Hall Effect & Magnetic Sensors

- Other Technologies (Piezoelectric, Capacitive & Resistive)

- Market Size & Forecast by Vehicle Type

- Two-Wheeler (Motorcycles & Scooters)

- Three-Wheeler (Auto-Rickshaw & Cargo Three-Wheeler)

- Passenger Vehicle (Hatchback, Sedan, SUV & MPV)

- Light Commercial Vehicle (LCV)

- Medium & Heavy Commercial Vehicle (M&HCV)

- Electric Vehicle (2W EV, 3W EV, 4W EV & Commercial EV)

- Market Size & Forecast by Application

- Engine Management & Powertrain Control

- Advanced Driver Assistance Systems (ADAS) & Active Safety

- Emission Control & Exhaust Aftertreatment

- Battery Management & EV Powertrain Monitoring

- Tyre Pressure & Chassis Dynamics Monitoring

- Parking Assistance, Surround View & Reversing Aids

- Cabin Comfort, HVAC & Air Quality Monitoring

- Market Size & Forecast by Sales Channel

- OEM Direct Supply (Tier-1 Supplier to Vehicle Manufacturer)

- Aftermarket Replacement & Service Channel

- Online Retail & E-Commerce Platforms

- Market Size & Forecast by End-User

- OEM Vehicle Manufacturers (Passenger & Commercial Vehicle OEMs)

- Tier-1 Automotive System Integrators & Module Suppliers

- EV Manufacturers & Electric Mobility Startups

- Aftermarket Service Centers & Multi-Brand Workshop Networks

- Fleet Operators & Telematics Service Providers

- North India Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- By State

- Market Size & Forecast

- South India Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- By State

- Market Size & Forecast

- West India Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- By State

- Market Size & Forecast

- East India Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- By State

- Market Size & Forecast

- Central India Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- By State

- Market Size & Forecast

- State-Wise* Automotive Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Sensor Type

- By Technology

- By Vehicle Type

- By Application

- By Sales Channel

- By End-User

- Market Size & Forecast

*States Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Haryana, Karnataka, Tamil Nadu, Gujarat, Rajasthan, Uttar Pradesh, Telangana, West Bengal, Delhi NCR, Madhya Pradesh, Kerala, Punjab, Andhra Pradesh, Uttarakhand

- Technology Landscape & Innovation Analysis

- MEMS Sensor Technology Deep-Dive (Pressure, Inertial, Gyroscope & Accelerometer)

- Radar Sensor Technology for ADAS, Blind Spot Detection & Adaptive Cruise Control

- Camera & Machine Vision Sensor Technology for Lane Departure, Object & Pedestrian Detection

- LiDAR Technology for Autonomous Driving & Advanced Driver Assistance Applications

- Ultrasonic Sensor Technology for Parking Assistance, Proximity & Level Sensing

- Electrochemical & Optical Sensor Technology for Exhaust Emission & Lambda Monitoring

- Battery Management System (BMS) Sensor & EV-Specific Sensing Technology

- AI-Based Sensor Fusion, ECU Integration & Connected Vehicle Data Platform Technology

- Patent & IP Landscape in Automotive Sensor Technologies

- Value Chain & Supply Chain Analysis

- Semiconductor Wafer Fabrication, MEMS Manufacturing & Sensor Die Supply Chain

- Sensor Chip Packaging, Module Assembly & Electronic Control Unit (ECU) Integration Supply Chain

- Tier-1 Automotive Sensor System Supplier & OEM Direct Supply Channel

- Tier-2 & Tier-3 Component, Housing, Connector & PCB Manufacturing Supply Chain

- Aftermarket Sensor Replacement, Distributor & Retail Supply Channel

- Testing, Calibration, Certification & Quality Assurance Service Chain

- R&D, Software, Sensor Fusion Algorithm & Embedded Systems Ecosystem

- Pricing Analysis

- OEM-Grade vs. Aftermarket Sensor Price Differential Analysis by Sensor Type

- Price Analysis by Vehicle Type & Application Segment

- Imported vs. Domestically Manufactured Sensor Cost Competitiveness Analysis

- PLI Incentive & Localisation Impact on Automotive Sensor Pricing

- Volume Pricing Dynamics & OEM Long-Term Contract vs. Spot Market Pricing

- EV Sensor Cost Trajectory & BMS Sensor Price Trend Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment of Automotive Sensors: Carbon Footprint, E-Waste & Material Recovery

- MEMS & Semiconductor Waste Management, RoHS Compliance & Hazardous Substance Control

- Sensor-Enabled Vehicle Efficiency Improvement, Emission Reduction & Fuel Economy Contribution

- ADAS & EV Sensor Role in Road Safety, Accident Prevention & Sustainable Mobility

- Responsible Sourcing, Conflict Minerals & ESG Compliance in Sensor Supply Chains

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Global vs. Domestic Players by Sensor Type & Application)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sensor Type, Technology & Vehicle Segment

- Player Classification

- Global Tier-1 OEM Sensor Manufacturers with India Operations

- Domestic Automotive Sensor & Instrument Cluster Manufacturers

- Semiconductor & MEMS Chip Suppliers Serving India Automotive OEMs

- ADAS, Radar, Camera & LiDAR Sensor Specialists

- EV Battery Management & Power Electronics Sensor Suppliers

- Aftermarket Sensor Suppliers & Replacement Parts Distributors

- Automotive ECU, Software & Sensor Fusion Platform Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Sensor Type, Technology & Vehicle Segment

- Company Profile

- Company Overview & Headquarters

- Automotive Sensor Product & Technology Portfolio

- Key OEM Customer Relationships & Vehicle Platform Fitment

- Manufacturing Footprint, R&D Centres & Production Capacity in India

- Revenue (Automotive Sensor Segment) & Volume

- Technology Differentiators, IP & AIS or IATF Certifications

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Sensor Launches, Design Wins, Capacity Additions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Sensor Type, Technology, Vehicle Segment, Application & Region

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output