Market Definition

The Global Digital Marketplace Platforms Market encompasses the development, operation, monetization, and continuous evolution of technology-mediated online platforms that facilitate multi-sided commercial exchanges between buyers and sellers of physical goods, digital products, services, labor, financial instruments, and creative content across internet-connected devices globally, generating platform revenue through transaction commissions, subscription fees, advertising, value-added services, and data monetization models that scale with the volume, variety, and velocity of transactions conducted through the platform ecosystem. Digital marketplace platforms are distinguished from conventional single-vendor e-commerce websites by their multi-sided network architecture, in which the platform operator does not own the inventory or service capacity being transacted but rather provides the discovery, trust, payment processing, logistics coordination, and dispute resolution infrastructure that enables independent buyers and sellers to transact at lower search, verification, and execution costs than would be possible through offline or fragmented digital channels.

The market encompasses business-to-consumer e-commerce marketplaces connecting retail brands, third-party sellers, and direct-to-consumer manufacturers with individual shoppers across general merchandise, fashion, electronics, home goods, grocery, and specialty retail categories; business-to-business procurement and supply chain marketplaces connecting industrial buyers with component suppliers, raw material traders, and MRO product distributors; peer-to-peer and consumer-to-consumer marketplaces facilitating secondhand, rental, and resale transactions; service and gig economy marketplaces connecting freelance professionals, tradespeople, and on-demand labor with individual and business service buyers; accommodation and travel experience marketplaces; digital content and software marketplaces; financial services and lending marketplaces; and vertical industry-specific marketplace platforms serving healthcare, agriculture, education, real estate, and legal services. The market further encompasses the enabling technology infrastructure including marketplace software platforms, payment gateway integration, logistics and fulfillment technology, seller onboarding and compliance tools, AI-powered search and recommendation engines, fraud detection systems, and analytics and advertising technology stacks that collectively constitute the commercial and technical architecture of modern digital marketplace operations. Key participants include global technology conglomerates operating dominant marketplace ecosystems, vertical-specialist marketplace platform companies, marketplace software-as-a-service providers enabling enterprise marketplace deployment, and the seller, brand, and service provider communities whose participation generates the supply-side network effects that determine marketplace commercial viability.

Market Insights

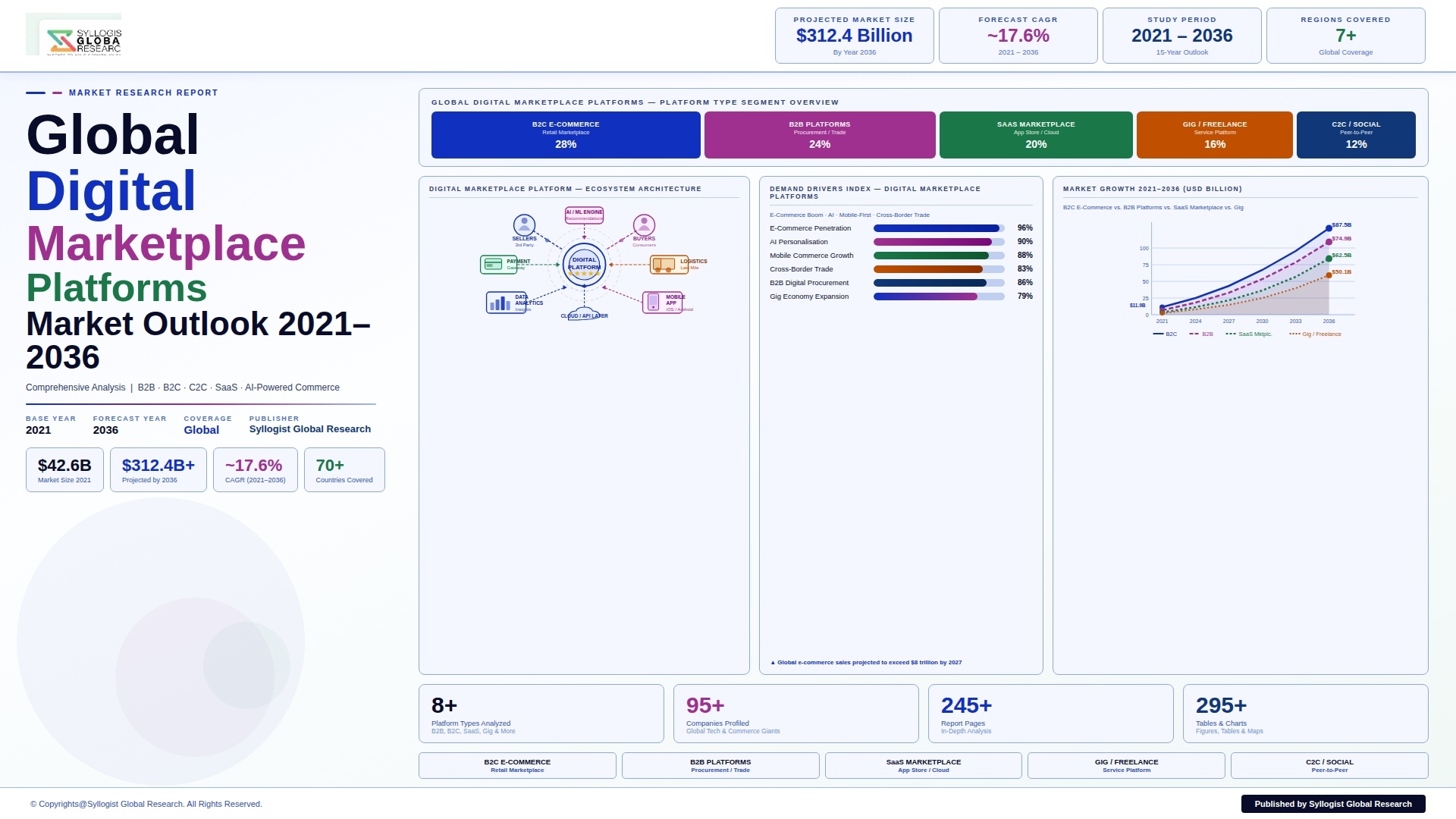

The global digital marketplace platforms market is entering a phase of structural maturation in developed markets combined with explosive growth momentum in emerging economies, driven by the progressive digitalization of consumer and business purchasing behavior across all transaction categories, the compounding network effects that concentrate transaction volume on leading marketplace platforms at the expense of standalone retailer and service provider digital presences, and the accelerating integration of artificial intelligence, embedded finance, and social commerce capabilities into marketplace architectures that are expanding the value capture potential and user engagement depth of leading platform operators beyond their original transactional intermediary roles. The global digital marketplace platforms market was valued at approximately USD 680 billion in 2025 and is projected to reach USD 1.42 trillion by 2034, advancing at a compound annual growth rate of 8.5% over the forecast period from 2027 to 2034, underpinned by the continued shift of retail, services, and B2B procurement spending from offline and direct-channel digital formats toward marketplace platforms whose discovery, convenience, price transparency, and social proof advantages are progressively compelling buyers across all demographic and geographic segments to conduct an increasing proportion of their purchasing through marketplace interfaces on mobile and desktop devices.

The e-commerce marketplace segment, encompassing general merchandise and category-specialist online retail platforms, constitutes the largest revenue-generating component of the global digital marketplace market, with total global marketplace gross merchandise value reaching approximately USD 3.8 trillion in 2025 across all platform types, of which the top five marketplace platforms by GMV, including Amazon, Alibaba’s Taobao and Tmall, JD.com, Pinduoduo, and Shopee, account for approximately 62% of total global marketplace transaction volume, reflecting the winner-takes-most dynamics of marketplace competition where supply-side seller liquidity and demand-side buyer traffic concentration create self-reinforcing competitive moats that are extraordinarily difficult for newer entrants to overcome without sustained capital investment and differentiated positioning in underserved categories or geographies. Amazon’s third-party marketplace, which now accounts for approximately 60% of total items sold on the platform and generates an estimated USD 140 billion in annual service revenue from seller fees, fulfillment services, and advertising, has fundamentally transformed from a retailer into a marketplace operator and logistics services business whose seller services revenue growth substantially outpaces its first-party retail revenue growth, illustrating the financial model evolution of digital marketplace platforms toward higher-margin service revenue streams that leverage the platform’s established buyer and seller network without requiring the inventory capital deployment of conventional retail. The social commerce marketplace segment, integrating shoppable content, influencer commerce, and live streaming sales formats within social media platform environments on TikTok Shop, Instagram Shopping, and Pinterest, is growing at approximately 28.4% annually and is fundamentally blurring the boundary between content discovery and transactional commerce in ways that are creating both competitive pressure on standalone marketplace platforms and strategic integration imperative for established players seeking to capture the impulse purchase and community-driven commerce behaviors that social commerce formats uniquely enable.

The B2B digital marketplace segment represents the most commercially underexplored and highest-growth-potential territory within the global digital marketplace platforms landscape, as the digitalization of business procurement, supply chain sourcing, and inter-enterprise commercial transactions has proceeded substantially more slowly than consumer e-commerce but is now experiencing structural acceleration driven by the demonstrated cost efficiency, sourcing optionality, and supply chain transparency benefits of marketplace-mediated procurement over traditional direct sales and distributor-intermediated B2B purchasing models. Global B2B e-commerce marketplace transaction volumes reached approximately USD 7.9 trillion in 2025, substantially exceeding consumer marketplace volumes, yet the proportion of B2B transactions conducted through digital marketplace platforms rather than traditional procurement channels remains well below the equivalent consumer penetration rate, implying a large and commercially significant digitalization opportunity whose capture will drive above-average marketplace platform revenue growth in industrial supplies, chemicals, agricultural inputs, construction materials, manufacturing components, and professional services procurement categories through the forecast period. Alibaba’s 1688.com and Alibaba International, Amazon Business which achieved USD 35 billion in annual sales in 2024, Faire in the wholesale and independent retail B2B segment, and sector-specific B2B marketplaces including Thomasnet for industrial components, Chemours for specialty chemicals, and Agora for construction materials are collectively demonstrating the commercial viability of B2B marketplace models across diverse industrial procurement categories, with payment terms integration, bulk pricing structures, RFQ workflows, and ERP system connectivity emerging as the critical B2B-specific platform functionality requirements that differentiate commercially successful B2B marketplaces from consumer marketplace platforms that have attempted to extend into business procurement without addressing the structural complexity of enterprise purchasing processes.

The gig economy and services marketplace segment, encompassing labor marketplaces including Upwork, Fiverr, and Toptal for professional freelance services, Uber and Lyft for transportation, DoorDash and Deliveroo for food delivery, Angi and TaskRabbit for home services, and Airbnb and Vrbo for accommodation, constitutes a structurally transformative component of the global digital marketplace market whose growth trajectory is driven by the increasing organizational preference for flexible workforce models, the expanding population of skilled professionals seeking location-independent income generation, and the growing consumer acceptance of marketplace-mediated service procurement over traditional service provider engagement channels. The global gig economy platforms generated an estimated USD 455 billion in gross service value in 2025, with the professional services marketplace sub-segment led by Upwork and Fiverr growing at approximately 12.1% annually as the remote work normalization accelerated by the COVID-19 pandemic has permanently expanded the addressable market for global professional services marketplace platforms by eliminating the geographic proximity constraint that historically limited the buyer-seller matching radius in professional services procurement. Emerging market digital marketplace ecosystems in India, Southeast Asia, Latin America, and Sub-Saharan Africa represent the highest absolute growth opportunity territories for the global marketplace platforms market, with India’s digital marketplace sector generating approximately USD 72 billion in GMV in 2025 and growing at approximately 19.3% annually as smartphone penetration, UPI payment infrastructure, and logistics network expansion collectively enable marketplace commerce to reach India’s 500-million-strong internet user base at commercially viable unit economics across an expanding range of retail and service categories.

Key Drivers

Accelerating Global Smartphone Penetration and Mobile Commerce Adoption Expanding the Accessible Buyer Population Across Emerging and Developed Markets

The continuing expansion of smartphone ownership and mobile internet access across emerging economies in South Asia, Southeast Asia, Sub-Saharan Africa, and Latin America is structurally enlarging the addressable buyer population for global and regional digital marketplace platforms by bringing first-time digital commerce participants into marketplace ecosystems through mobile-first platform interfaces and digital payment solutions that lower the access and trust barriers historically associated with online commerce adoption in low-income and first-generation internet user demographics. Global smartphone users reached approximately 6.9 billion in 2025, with the incremental user addition concentrated in emerging markets where first-internet-device adoption via smartphones rather than desktop computers creates a mobile-native user behavior profile that is inherently more compatible with marketplace app commerce than desktop web browsing shopping patterns, structurally advantaging mobile-optimized marketplace platforms whose user experience, notification-driven engagement, and one-tap checkout capabilities align with the consumption behavior of mobile-first digital commerce participants. The proliferation of mobile payment infrastructure including India’s UPI, Brazil’s Pix, Southeast Asia’s regional payment networks, and mobile money systems across Sub-Saharan Africa has resolved the payment friction barrier that historically constrained marketplace adoption among unbanked and underbanked consumer populations, enabling marketplace platforms to access a commercially significant buyer base in markets where formal banking infrastructure penetration remains low but mobile phone ownership and digital wallet adoption is high. The integration of buy-now-pay-later and embedded credit products directly within marketplace checkout flows is further expanding the accessible buyer population by extending purchasing power to consumer segments whose purchasing frequency and basket value were previously constrained by limited formal credit access, generating both incremental GMV growth and higher-margin embedded financial services revenue for marketplace platform operators who offer integrated lending alongside transactional intermediation.

Artificial Intelligence Integration Transforming Marketplace Discovery, Personalization, Fraud Prevention, and Seller Performance Management Capabilities

The deployment of large language models, computer vision, recommendation algorithm advancement, and real-time behavioral analytics within digital marketplace platform architectures is fundamentally transforming the buyer discovery experience, seller performance management capability, fraud and counterfeiting detection effectiveness, and dynamic pricing optimization sophistication of leading marketplace platforms in ways that are widening the competitive moat between AI-native and AI-laggard marketplace operators and creating measurable commercial value for both buyers and sellers that reinforces platform loyalty and reduces switching incentive to alternative commerce channels. Amazon’s AI-powered product recommendation engine, which is estimated to contribute approximately 35% of total platform purchases through personalized discovery surfaces, and Alibaba’s Alix virtual shopping assistant that generated RMB 50 billion in sales during the 2024 Singles Day shopping event, represent leading examples of AI commercial value creation within established marketplace ecosystems whose competitive advantages from accumulated behavioral data and recommendation model training depth are structurally difficult for smaller or newer marketplace operators to replicate without comparable data scale and AI infrastructure investment. The application of computer vision and multimodal AI models to marketplace product listing quality improvement, visual search functionality enabling buyers to find products through image rather than text queries, and automated counterfeit product detection through image and metadata analysis is improving marketplace trust and buyer conversion rates while reducing seller compliance burden and platform liability exposure from fraudulent and infringing listings, creating mutual value creation for buyers, sellers, and platform operators that reinforces AI investment priority across leading marketplace organizations. Generative AI-powered seller tools automating product description creation, SEO-optimized listing generation, customer service response drafting, and advertising copy production are further deepening the marketplace platform value proposition for seller communities by reducing the operational cost and marketing expertise barrier to effective marketplace participation, expanding the seller base and supply-side diversity that generates the buyer value proposition of breadth, selection, and competitive pricing.

Platform Economy Regulatory Evolution and Cross-Border Trade Infrastructure Development Enabling Marketplace Expansion Into Previously Inaccessible Markets and Transaction Categories

The progressive development of cross-border e-commerce regulatory frameworks, digital trade agreement provisions, streamlined customs clearance for low-value parcel shipments, and harmonized marketplace seller compliance standards across major trading blocs including the European Union, ASEAN Economic Community, and the African Continental Free Trade Area is materially improving the commercial viability of cross-border marketplace transactions and enabling platform operators to extend their geographic seller and buyer reach beyond single-country marketplace operations into genuinely pan-regional and global commerce networks. The European Union’s e-commerce VAT reform and Import One Stop Shop mechanism, which simplified the VAT compliance burden for non-EU marketplace sellers serving European buyers and shifted VAT collection liability to marketplace platforms rather than individual sellers, has created a more transparent and enforceable cross-border e-commerce compliance environment that is expanding legitimate marketplace seller participation from Asian, Middle Eastern, and American origin suppliers in European marketplace ecosystems. The development of bonded warehouse, free trade zone, and seller fulfillment infrastructure networks by marketplace platform operators including Amazon FBA, Alibaba’s Cainiao logistics, and Shopee’s logistics network across Southeast Asia is resolving the last-mile delivery reliability and return logistics complexity that constrained cross-border marketplace adoption in markets where consumer trust in delivery performance was insufficient to support sustained marketplace purchasing behavior, creating a virtuous cycle of logistics infrastructure investment, buyer trust improvement, transaction volume growth, and further logistics investment that is progressively integrating previously fragmented national marketplace ecosystems into regionally connected commerce networks.

Key Challenges

Intensifying Global Regulatory Scrutiny of Dominant Marketplace Platform Market Power, Data Practices, and Competitive Conduct

Digital marketplace platforms that have achieved dominant market positions in their respective categories face an intensifying and geographically expanding regulatory scrutiny of their competitive practices, data collection and monetization activities, treatment of third-party sellers operating on their platforms, and the structural conflicts of interest arising from the dual role of marketplace operators who simultaneously sell their own first-party products in competition with third-party sellers while controlling the algorithmic ranking, advertising, and fulfillment systems that determine seller visibility and commercial success on the platform. The European Union’s Digital Markets Act, which designated Amazon, Apple, Google, Meta, Microsoft, and ByteDance as digital gatekeepers subject to a prescriptive set of interoperability, data sharing, and self-preferencing prohibitions, represents the most comprehensive regulatory intervention in digital marketplace competitive conduct to date, with the Act’s provisions requiring Amazon to provide third-party sellers with access to the same data the platform collects about their transactions, prohibiting Amazon from using seller data to inform its own private label product decisions, and mandating interoperability with competing services in ways that structurally limit the self-reinforcing competitive advantages that marketplace scale confers. Antitrust investigations and consent decrees targeting Amazon in the United States, European Union, Germany, Italy, and India, Google Shopping in the European Union, and Alibaba and Meituan in China collectively represent a global regulatory enforcement trend whose cumulative compliance cost, operational constraint, and business model modification implications are progressively increasing the regulatory risk discount applied to dominant digital marketplace platform valuations and creating competitive uncertainty that complicates long-term platform architecture and monetization strategy investment decisions.

Counterfeit Product Proliferation, Seller Fraud, and Consumer Trust Integrity Challenges Undermining Marketplace Platform Reliability and Brand Value

The open seller participation architecture that enables digital marketplace platforms to achieve the supply-side breadth and competitive pricing that constitutes their primary buyer value proposition simultaneously creates structural vulnerability to counterfeit product listings, fraudulent seller practices, review manipulation, and misleading product representation that erode consumer trust, generate brand owner intellectual property enforcement obligations, create product liability exposure for platform operators, and impose regulatory compliance costs under consumer protection, product safety, and intellectual property enforcement frameworks that are progressively assigning marketplace operator responsibility for the quality and authenticity of products sold through their platforms. The scale of counterfeit product proliferation on major e-commerce marketplaces is commercially significant, with brand owners across luxury goods, consumer electronics, pharmaceuticals, and consumer health categories reporting that counterfeit versions of their products are routinely listed and sold through major marketplace platforms despite notice-and-takedown procedures, AI-based detection systems, and seller verification programs whose effectiveness is systematically circumvented by organized counterfeit supply networks that adapt their listing tactics to evade platform detection algorithms faster than platform enforcement systems can evolve. The European Union Product Liability Directive revision and the proposed Liability of Online Platforms for Products regulation, alongside the US INFORM Consumers Act seller identity verification requirements, are progressively shifting marketplace operator legal liability from passive hosting toward active product safety responsibility for goods sold through their platforms, creating compliance investment requirements and litigation exposure that disproportionately affect smaller marketplace operators lacking the legal, technical, and operational resources of dominant platform companies to implement comprehensive seller vetting, product testing, and supply chain authenticity verification programs.

Last-Mile Logistics Cost Inflation, Delivery Expectation Escalation, and Returns Management Complexity Compressing Marketplace Unit Economics

The structural escalation of consumer delivery expectation toward same-day and next-day fulfillment windows, driven by Amazon Prime’s standard-setting delivery speed commitments that have progressively reset the baseline consumer delivery expectation across all marketplace platforms globally, is imposing substantial logistics infrastructure investment requirements and per-order fulfillment cost burdens on marketplace operators and their third-party seller communities that are compressing marketplace unit economics, raising seller participation cost barriers, and creating sustainability concerns around the carbon intensity and packaging waste generation of rapid delivery fulfillment networks whose environmental footprint is attracting increasing regulatory and consumer advocacy attention. The last-mile delivery cost component of e-commerce fulfillment, which accounts for approximately 41% to 53% of total supply chain cost in densely populated urban markets and a substantially higher proportion in low-density suburban and rural delivery environments, has increased by an estimated 18% to 25% in real terms across North American and European markets between 2019 and 2025 due to the combined effects of labor cost inflation in warehousing and delivery operations, fuel cost volatility, vehicle fleet electrification capital investment requirements, and the operational inefficiency of delivering to an increasingly fragmented set of residential addresses with low parcel density per delivery route. The growing volume of marketplace product returns, which average 15% to 30% of total orders across apparel, electronics, and general merchandise categories and reach 40% to 50% in fashion categories where size and fit uncertainty drives high return rates, generates reverse logistics costs, product refurbishment and restocking expenses, and inventory write-down losses that collectively represent a significant and poorly controlled cost center for marketplace operators and sellers whose financial models are disproportionately stressed by the return rate escalation accompanying rapid GMV growth in discretionary product categories.

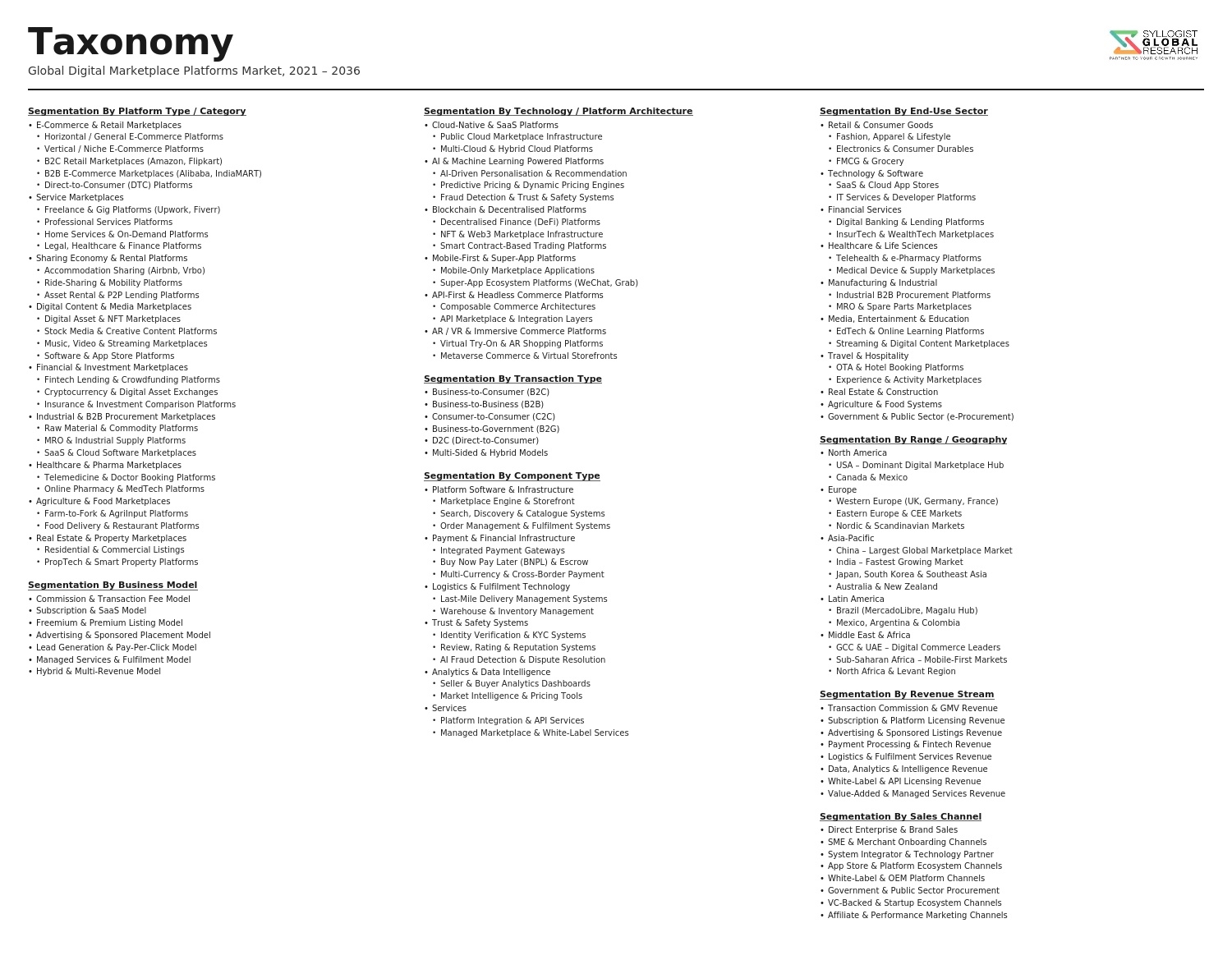

Market Segmentation

- Segmentation By Marketplace Type

- Business-to-Consumer (B2C) E-Commerce Marketplaces

- Business-to-Business (B2B) Procurement and Supply Marketplaces

- Consumer-to-Consumer (C2C) and Peer-to-Peer Marketplaces

- Gig Economy and On-Demand Services Marketplaces

- Digital Content and Software Marketplaces

- Financial Services and Lending Marketplaces

- Social Commerce and Live Streaming Marketplaces

- Others

- Segmentation By Product and Service Category

- General Merchandise and Multi-Category Retail

- Fashion, Apparel, and Accessories

- Consumer Electronics and Technology Products

- Home, Garden, and Furniture

- Grocery, Food, and Health Products

- Industrial and B2B Supplies (MRO, Components, Raw Materials)

- Travel, Accommodation, and Experiences

- Professional and Freelance Services

- Second-Hand, Refurbished, and Recommerce

- Others

- Segmentation By Revenue Model

- Transaction Commission and Take Rate Model

- Subscription and Membership Fee Model

- Marketplace Advertising and Sponsored Listing Revenue

- Fulfillment and Logistics Service Revenue (3PL)

- Embedded Financial Services (BNPL, Payments, Insurance)

- Data and Analytics Monetization

- SaaS Marketplace Enablement Platform Licensing

- Others

- Segmentation By Deployment Model

- Centralized Platform Operator Model

- Decentralized and Blockchain-Based Marketplace Platforms

- White-Label and Enterprise Marketplace Software (SaaS)

- Headless Commerce and API-First Marketplace Architecture

- Others

- Segmentation By End User

- Individual Consumers (B2C Buyers)

- Small and Medium Enterprise Sellers and Buyers

- Large Enterprise and Corporate Procurement Users

- Independent Professionals and Freelancers

- Brand Owners and Direct-to-Consumer Manufacturers

- Financial Institutions and Fintech Service Providers

- Others

- Segmentation By Technology Enabler

- AI and Machine Learning Recommendation and Personalization

- Mobile Commerce and Super-App Integration

- Augmented Reality and Virtual Try-On Capabilities

- Blockchain and Smart Contract-Based Trust Mechanisms

- Embedded Payment and Digital Wallet Infrastructure

- Voice Commerce and Conversational AI Interfaces

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Digital Marketplace Platforms Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by marketplace type, product and service category, revenue model, and region, to enable platform operators, technology investors, enterprise software providers, and strategic acquirers to identify which marketplace categories and geographic markets will generate the highest absolute revenue and the most commercially defensible growth trajectories across the forecast period?

- How is the competitive balance between dominant global marketplace platforms including Amazon, Alibaba, JD.com, and Shopee and emerging regional and vertical-specialist marketplace challengers evolving across B2C, B2B, services, and social commerce segments, what specific competitive strategies including vertical focus, social commerce integration, embedded finance, and geographic expansion are proving most effective in challenging incumbent platform network effect advantages, and what is the projected market share distribution among top global and regional marketplace platform operators through 2034?

- What is the current and projected revenue contribution of non-transactional platform monetization streams including marketplace advertising, fulfillment and logistics services, embedded financial products, and seller SaaS tools relative to traditional take-rate commission revenue across leading marketplace platforms, how are platform operators optimizing their monetization architecture to maximize revenue per GMV dollar as gross merchandise value growth decelerates in maturing markets, and what new revenue stream categories are expected to emerge as commercially significant contributors to marketplace platform revenue by 2034?

- How are the European Union Digital Markets Act gatekeeper obligations, the US Federal Trade Commission marketplace competition enforcement actions, and equivalent digital market regulation frameworks in India, South Korea, Japan, and Australia reshaping the operational practices, data governance frameworks, competitive conduct constraints, and business model architecture of dominant digital marketplace platform operators, and what is the projected compliance cost and competitive repositioning investment required by designated gatekeeper platforms to achieve and maintain regulatory compliance through the forecast period?

- Who are the leading global marketplace platform operators, vertical-specialist marketplace disruptors, marketplace enablement software providers, and logistics and payments infrastructure companies whose capabilities define the competitive architecture of the global digital marketplace platforms market, and what are their respective GMV scale and growth trajectories, take rate and monetization model evolution, technology investment priorities in AI personalization and embedded finance, geographic expansion strategies across emerging market opportunities, regulatory compliance positioning, and strategic partnership and acquisition approaches in response to the structural competitive and regulatory dynamics reshaping global digital marketplace platform competition through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Platform Regulatory Risk: Antitrust Scrutiny, Digital Markets Act Enforcement & Gatekeeper Designation Risk

- Trust & Safety Risk: Fraud, Counterfeit Listings, Fake Reviews & Seller Misconduct Management Risk

- Data Privacy, GDPR, CCPA & Cross-Border Data Transfer Compliance Risk for Global Marketplace Operators

- Disintermediation, Seller Bypass & Direct-to-Consumer Channel Conflict Risk

- Cybersecurity, Platform Downtime, Payment System Breach & Business Continuity Risk

- Regulatory Framework & Standards

- EU Digital Markets Act (DMA) & Digital Services Act (DSA): Gatekeeper Obligations, Interoperability & Platform Accountability Frameworks

- US Antitrust & Platform Competition Regulation: FTC, DOJ Oversight & Proposed Platform Monopolisation Legislation

- Consumer Protection, E-Commerce Regulations & Seller Liability Frameworks Across Key Jurisdictions

- Payment Services Regulation: PSD2, Open Banking, Digital Payments Licensing & Know Your Customer (KYC) Compliance for Marketplace Transactions

- Taxation of Digital Marketplace Platforms: VAT/GST Marketplace Facilitator Laws, Digital Services Tax & OECD Pillar One Framework

- Global Digital Marketplace Platforms Market Outlook

- Market Size & Forecast by Value (Gross Merchandise Value & Platform Revenue)

- Market Size & Forecast by Platform Type

- Business-to-Consumer (B2C) E-Commerce Marketplace Platforms

- Business-to-Business (B2B) Digital Procurement & Trade Marketplace Platforms

- Consumer-to-Consumer (C2C) & Peer-to-Peer (P2P) Marketplace Platforms

- Direct-to-Consumer (D2C) Platform & Brand Storefront Marketplace

- Service Marketplace Platforms (Freelance, Professional & On-Demand Services)

- Sharing Economy & Asset Rental Marketplace Platforms

- Multi-Sided & Super-App Integrated Marketplace Platforms

- Industry-Vertical & Niche Marketplace Platforms

- Market Size & Forecast by Marketplace Model

- Managed Marketplace (Platform Controls Inventory, Fulfilment & Quality)

- Pure Marketplace (Third-Party Seller Managed with Platform as Intermediary)

- Hybrid Marketplace (Mix of First-Party & Third-Party Seller Models)

- Aggregator Marketplace (Demand Aggregation & Price Comparison)

- Decentralised & Blockchain-Enabled Marketplace

- Market Size & Forecast by Product & Service Category

- Physical Goods: Electronics, Apparel, Home & Lifestyle

- Grocery, Food & Fresh Produce

- Automotive Parts, Vehicles & Mobility Services

- Industrial, B2B Procurement & MRO Supplies

- Freelance, Professional & Knowledge-Based Services

- Travel, Accommodation & Experiences

- Financial Services, Insurance & Lending

- Healthcare, Wellness & Pharmaceutical Products

- Digital Goods, Software & Subscription Services

- Real Estate & Property

- Market Size & Forecast by Deployment Mode

- Web-Based Platform

- Mobile App-First Platform (iOS & Android)

- Social Commerce Integrated Platform

- Voice Commerce & Conversational AI Platform

- Headless & API-First Marketplace Infrastructure

- Market Size & Forecast by Monetisation Model

- Commission & Transaction Fee Model

- Subscription & Seller Membership Fee Model

- Listing & Featured Placement Fee Model

- Advertising, Sponsored Product & Performance Marketing Revenue

- Value-Added Services (Fulfilment, Payments, Financing & Logistics)

- Freemium & Tiered Access Model

- Market Size & Forecast by End-User

- Individual Consumers & Households

- Small & Medium Enterprises (SMEs) & Independent Sellers

- Large Enterprises & Global Brands

- Gig Economy Workers & Independent Service Providers

- Government & Public Sector Procurement Bodies

- Institutional & B2B Buyers

- Market Size & Forecast by Technology Enabler

- AI-Powered Recommendation, Personalisation & Search Engines

- Cloud Infrastructure, Microservices & Platform-as-a-Service (PaaS)

- Blockchain & Distributed Ledger Technology for Trust & Provenance

- AR & VR Product Visualisation & Immersive Commerce

- Digital Payments, Embedded Finance & Buy-Now-Pay-Later (BNPL) Integration

- North America Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- Europe Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- Asia-Pacific Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- Latin America Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- Middle East & Africa Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- Country-Wise* Digital Marketplace Platforms Market Outlook

- Market Size & Forecast

- By Value (Gross Merchandise Value & Platform Revenue)

- By Platform Type

- By Marketplace Model

- By Product & Service Category

- By Deployment Mode

- By End-User

- By Country

- By Monetisation Model

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- AI & Machine Learning in Marketplace Platforms: Personalised Recommendation Engines, Dynamic Pricing & Demand Forecasting Technology Deep-Dive

- Generative AI & Conversational Commerce Technology: AI Shopping Assistants, Chatbot Integration & Natural Language Product Discovery

- Blockchain & Web3 Marketplace Technology: Decentralised Platforms, Smart Contracts, NFT Marketplaces & Tokenised Loyalty

- Augmented Reality (AR) & Immersive Commerce Technology: Virtual Try-On, 3D Product Visualisation & Metaverse Commerce

- Embedded Finance & Marketplace Fintech Technology: BNPL, Marketplace Lending, Digital Wallets & Insurance Integration

- Headless Commerce, API-First Architecture & Composable Marketplace Platform Technology

- Marketplace Trust & Safety Technology: AI-Powered Fraud Detection, Fake Review Identification & Seller Verification Systems

- Patent & IP Landscape in Digital Marketplace Platform Technologies

- Value Chain & Supply Chain Analysis

- Platform Technology Infrastructure: Cloud Hosting, CDN, Search Engine & Data Analytics Stack Supply Chain

- Seller Onboarding, Catalogue Management & Product Listing Technology Supply Chain

- Payment Gateway, Fraud Prevention & Embedded Finance Integration Supply Chain

- Logistics, Last-Mile Delivery, Fulfilment Centre & Returns Management Supply Chain

- Digital Marketing, Affiliate Network & Performance Advertising Channel

- Customer Service, Trust & Safety & Dispute Resolution Operations

- Data Monetisation, Insights & Third-Party API & Partnership Ecosystem

- Pricing Analysis

- Commission Rate Benchmarking by Product Category & Marketplace Type Across Global Platforms

- Seller Subscription & Membership Fee Structure Analysis: Free vs. Premium Tier Comparison

- Advertising & Sponsored Placement CPM, CPC & ROAS Benchmarking on Leading Marketplace Platforms

- Fulfilment, Logistics & Value-Added Service Fee Structure Analysis for Marketplace Operators

- Platform Technology Licensing & White-Label Marketplace Software Pricing Analysis

- Total Seller Cost of Participation per Marketplace Channel: Effective Commission & Service Fee Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Digital Marketplace Operations: Carbon Footprint of Data Centres, Logistics Networks & Packaging

- Circular Economy Marketplace Models: Secondhand, Rental, Refurbished & Product-as-a-Service Platform Sustainability Contribution

- Sustainable Logistics, Carbon-Neutral Delivery & Green Last-Mile Innovation Across Global Marketplace Platforms

- ESG Reporting, Responsible Sourcing & Ethical Seller Standards Enforcement on Digital Marketplace Platforms

- Regulatory-Driven Sustainability, SDG 8 (Decent Work), SDG 9 (Industry & Innovation) & SDG 12 (Responsible Consumption) Alignment & ESG Disclosure Requirements

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Product Category & Region

- Player Classification

- Global Integrated E-Commerce & Super-App Marketplace Giants

- Regional B2C E-Commerce Marketplace Leaders

- B2B Digital Procurement & Industrial Marketplace Platforms

- Vertical-Specific Niche Marketplace Platforms

- Service & Gig Economy Marketplace Platforms

- Sharing Economy, Rental & Secondhand Marketplace Platforms

- Social Commerce & Influencer-Driven Marketplace Platforms

- White-Label & SaaS Marketplace Platform Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Product Category & Region

- Company Profile

- Company Overview & Headquarters

- Digital Marketplace Platform Products, Services & Technology Portfolio

- Key Seller, Brand & Buyer Relationships & Reference Markets

- Platform GMV, Active Sellers, Active Buyers & Geographic Footprint

- Revenue (Digital Marketplace Segment) & Growth Trajectory

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Platform Launches, Feature Releases, Market Expansions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Platform Scale vs. Category Specialisation)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Marketplace Model, Product Category, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output