Market Definition

The Global Electronic Connectors Market encompasses the design, manufacturing, distribution, and after-sale support of electromechanical interface components that create separable or permanent electrical connections between electronic circuits, printed circuit boards, cable assemblies, subassemblies, and systems, enabling the transmission of power, signal, and data across the complete spectrum of electronic and electrical equipment deployed in consumer electronics, automotive and transportation, industrial automation, telecommunications infrastructure, aerospace and defence, medical devices, and data centre applications. Electronic connectors provide mated interface connections that allow electronic assemblies to be connected, disconnected, and reconnected during manufacturing, testing, installation, maintenance, and field service operations, with each connector consisting of a plug or header mating half carrying pin or blade contacts and a socket or receptacle mating half carrying socket or spring-loaded contacts, housed in insulating bodies manufactured from engineering thermoplastics, thermoset resins, or metallic shells whose material selection is governed by mechanical retention, environmental sealing, temperature rating, and electromagnetic compatibility requirements of the intended application. The market encompasses circular and rectangular multi-pin connectors, board-to-board and board-to-cable connectors, coaxial radio frequency connectors, fibre optic connectors, high-speed differential pair connectors for digital data transmission, power connectors for battery, motor drive, and power distribution applications, input-output interface connectors for consumer and industrial devices, military-specification connectors, medical device connectors, and the connector components including contacts, housings, backshells, jackposts, and seals whose design and material performance determine connector reliability across the environmental conditions of each application. The complete value chain encompasses precision contact stamping and plating operations, housing moulding and assembly, wire harness and cable assembly integration, distribution through catalogue and specialty connector distributors, and the electronic equipment manufacturers and contract manufacturers whose design-in qualification processes and production procurement volumes govern connector technology development and commercial supply dynamics globally.

Market Insights

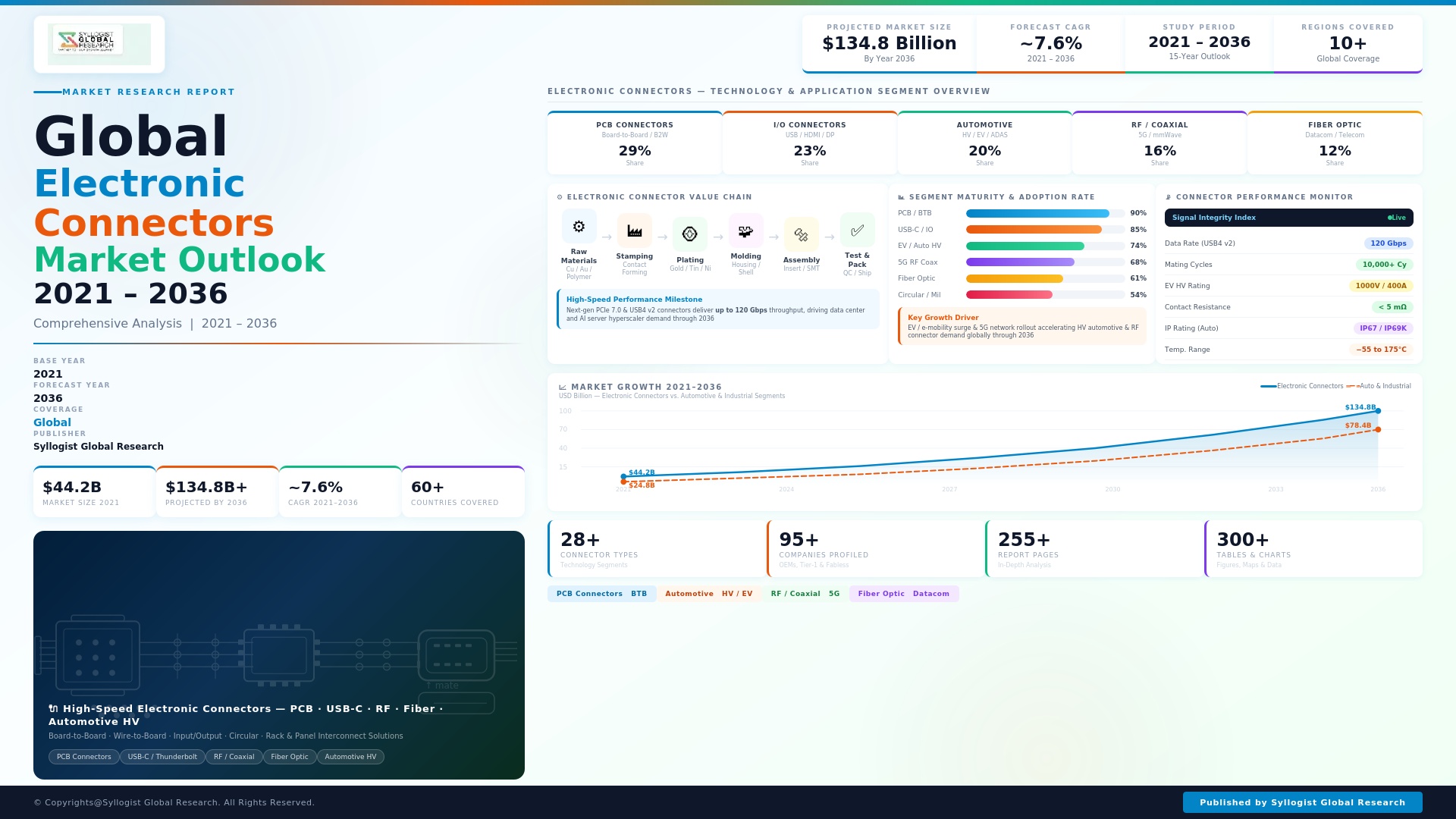

The global electronic connectors market was valued at approximately USD 82.4 billion in 2025 and is projected to reach USD 138.7 billion by 2034, advancing at a compound annual growth rate of 5.9% over the forecast period from 2027 to 2034, driven by the sustained growth of electronics content per vehicle in the automotive electrification transition, the rapid expansion of data centre and telecommunications infrastructure investment, the proliferation of industrial automation and robotics, and the growing connector content of consumer electronics devices whose increasing functional complexity, miniaturisation requirements, and data transmission bandwidth demands are continuously elevating the technical and commercial value of connector components per finished electronic assembly. The market is experiencing a structural technology transition toward higher-speed, higher-density, and more environmentally robust connector platforms as the data rates, power densities, and environmental exposure conditions of next-generation electronic systems exceed the performance envelopes of the connector technologies qualified in previous equipment generations, creating a recurring design-in and qualification cycle for upgraded connector technologies whose commercial value per unit substantially exceeds that of the products they replace.

The automotive connector segment is the largest single end-use market within the global electronic connectors industry, accounting for approximately 27% of total market revenue in 2025 and advancing at approximately 8.4% annually, driven by the explosive growth of connector content per vehicle associated with the electrification of powertrains, the proliferation of advanced driver assistance system sensor and compute architectures, the expansion of in-vehicle Ethernet network topologies replacing legacy controller area network bus wiring, and the increasing content of high-voltage connector systems interconnecting battery packs, power electronics modules, electric motors, and on-board charging units in battery electric and plug-in hybrid vehicle platforms. The average connector content per battery electric vehicle has reached approximately USD 650 to USD 950 per vehicle in 2025, compared to USD 280 to USD 380 per vehicle for equivalent internal combustion engine models, reflecting the substantially higher connector count, more demanding performance specifications, and greater unit values of the high-voltage sealed connectors, battery management system board-to-board connectors, FAKRA and Mini-FAKRA coaxial connectors for camera and radar sensor interfaces, and multi-gigabit Ethernet connectors for vehicle backbone network architecture that characterise the electrical architecture of electrified and connected vehicle platforms relative to their conventionally powered predecessors. The data centre and telecommunications infrastructure segment represents the fastest-growing major end-use market for electronic connectors, advancing at approximately 11.2% annually, driven by the hyperscale data centre construction boom associated with artificial intelligence workload expansion, where each server rack contains hundreds of high-speed backplane, cable assembly, and board-to-board connector interfaces operating at data rates of 112 gigabits per second per lane and above whose connector performance requirements are pushing the boundaries of signal integrity, crosstalk, and insertion loss achievable with conventional connector materials and geometries.

Asia-Pacific dominates the global electronic connectors market, accounting for approximately 52% of total market revenue in 2025, driven by the concentration of global electronics contract manufacturing, consumer device assembly, automotive parts production, and telecommunications equipment manufacturing in China, Japan, South Korea, Taiwan, Vietnam, and Malaysia, where the combined electronic equipment output of the region generates the world’s largest installed demand for connector components across every product category from miniature board connectors in mobile devices to high-voltage sealed connectors in electric vehicle powertrains assembled at Chinese and Japanese automotive manufacturing facilities. China is simultaneously the world’s largest connector consumption market and the country whose domestic connector manufacturing industry has undergone the most significant quality and technology capability upgrade in the past decade, with Chinese connector manufacturers having progressed from commodity low-frequency connector production toward increasingly sophisticated automotive-grade, high-speed data, and industrial connector manufacturing capability that is capturing domestic market share from international connector suppliers in mid-tier technology segments while international specialists retain leadership in the highest-performance and most reliability-critical connector categories. North America and Europe together account for approximately 36% of global connector market revenue, with revenue concentration in high-value connector segments including aerospace and defence military-specification circular connectors, medical device connectors meeting IEC 60601 biocompatibility and ingress protection requirements, high-speed data centre interconnect connectors operating at 224 gigabits per lane, and automotive connector programs at the flagship electric vehicle assembly plants of North American and European original equipment manufacturers whose supply qualification programs set the performance benchmark for the global automotive connector industry.

The miniaturisation imperative across consumer electronics, wearable devices, hearing instruments, and implantable medical devices is driving connector pitch reduction and form factor innovation at a pace that is continuously compressing the physical dimensions of connector interfaces while simultaneously increasing the current carrying capacity, contact normal force, and cycle life specifications that miniature connectors must satisfy to remain commercially viable in battery charging, data synchronisation, and sensor interface applications within space-constrained device architectures. High-speed differential pair connectors for server, storage, and networking applications operating at 112 gigabits per second per lane and advancing toward 224 gigabits per lane specifications are requiring fundamental redesign of contact geometry, housing dielectric material, and impedance control methodology to achieve the signal integrity performance needed for next-generation data centre fabric architectures, with leading connector developers investing significant electromagnetic simulation, material characterisation, and production process development effort in connector platforms whose per-unit values of USD 8 to USD 85 depending on port count and performance level represent the highest average selling price category within the electronic connectors market. The transition toward USB Type-C as the universal interface standard for consumer electronics power delivery and data transfer, mandated by the European Union for mobile devices and adopted voluntarily across the global consumer electronics industry, is generating substantial connector procurement consolidation opportunities for USB Type-C connector manufacturers whose standardised interface specification enables scale economics not achievable with the fragmented proprietary interface connector landscape of the preceding decade, while simultaneously creating an engineering challenge to deliver USB Type-C connector performance at the power delivery currents of up to 5 amperes and 240 watts that the USB Power Delivery 3.1 specification requires within connector bodies whose dimensions are constrained by the USB Type-C mechanical specification.

Key Drivers

Electric Vehicle Electrification and Connected Vehicle Architecture Growth Generating Structurally Elevated Automotive Connector Content Per Vehicle Across Global Production

The global automotive industry’s transition from internal combustion engine to battery electric and hybrid electric vehicle platforms is generating a structural and permanent increase in the connector content per vehicle that is creating one of the most commercially significant demand growth catalysts in the history of the electronic connectors industry, with the high-voltage connector systems, battery management electronics interfaces, power electronics module interconnects, and advanced driver assistance system sensor and compute network connectors of electric vehicle platforms collectively requiring two to three times the connector count and three to four times the connector value of equivalent conventional vehicle architectures. High-voltage sealed connector systems for battery electric vehicle applications, including the battery pack inter-cell and module connectors, high-voltage distribution unit connectors, and motor and inverter power connectors operating at voltages between 400 and 800 volts direct current with current ratings of 100 to 650 amperes, command unit values of USD 15 to USD 280 per connector assembly depending on current rating, sealing class, and locking system complexity, creating a high-value connector procurement category whose global market volume is expanding in direct proportion to battery electric vehicle production ramp at major automotive original equipment manufacturers worldwide. Global battery electric vehicle production reached approximately 14.8 million units in 2025 and is projected to reach approximately 41 million units annually by 2034, with each unit requiring approximately 35 to 65 high-voltage and signal connector assemblies beyond the conventional low-voltage body and powertrain connector content, generating an incremental annual connector procurement demand of approximately USD 9.6 billion by 2034 attributable solely to the high-voltage and advanced driver assistance system connector content differential between electric and internal combustion engine vehicle platforms.

Data Centre Artificial Intelligence Infrastructure Expansion and High-Speed Interconnect Bandwidth Escalation Creating Premium Connector Demand at Unprecedented Scale

The hyperscale data centre construction and upgrade programs being executed by major cloud service operators to support artificial intelligence training and inference workloads are generating connector procurement at port counts, data rate specifications, and aggregate procurement values that are transforming the scale and technology requirements of the data centre interconnect connector segment, with each artificial intelligence server cluster comprising tens of thousands of server nodes interconnected through switch fabric architectures requiring hundreds of millions of high-speed connector interfaces operating at 112 to 224 gigabits per second per lane at the board-to-board, cable assembly, and backplane interconnect levels. The transition of artificial intelligence server architectures toward copper direct-attach cable and active electrical cable assemblies for rack-level connectivity, and toward 800-gigabit and 1.6-terabit optical transceiver pluggable interfaces for inter-rack and inter-pod connectivity, is driving demand for high-density OSFP and QSFP-DD socket connectors at switch and network interface card ports whose per-socket values of USD 4 to USD 18 and annual procurement volumes at a single hyperscale campus construction program of several billion connector units collectively represent a connector market segment growing at rates that are reshaping the revenue mix and technology investment priorities of the leading electronic connector manufacturers globally. The artificial intelligence compute cluster connectivity requirements are simultaneously pulling the development of next-generation connector platforms including 224-gigabit-per-second-capable board connectors, co-packaged optics connector interfaces, and liquid-cooled connector systems compatible with direct liquid cooling architectures whose thermal management requirements are creating entirely new categories of connector engineering challenge that established connector platforms were not designed to address.

Industrial Automation Expansion, Collaborative Robotics Proliferation, and Industry 4.0 Infrastructure Investment Sustaining Broad-Based Industrial Connector Demand Growth

The global manufacturing industry’s sustained transition toward higher automation density, flexible production systems, collaborative robot integration, and Industry 4.0 digital infrastructure is generating broad-based and structurally growing demand for industrial connectors across servo drive interfaces, robot junction box connections, safety interlock systems, field bus network connections, industrial Ethernet switch infrastructure, sensor and actuator wiring, and the cable management systems that interconnect the complete automation architecture of modern manufacturing cells and production lines. Industrial connector installations in automated manufacturing facilities are growing at approximately 7.6% annually in unit volume terms, with each collaborative robot installation requiring 8 to 14 industrial connector assemblies for power, signal, Ethernet, and end-of-arm tool interface connections, and with each programmable logic controller expansion rack, distributed input-output module, and human-machine interface terminal requiring standardised industrial connector interfaces whose growing adoption of push-in terminal blocks, M8 and M12 circular connectors, and Ethernet RJ45 and industrial Ethernet connectors is replacing previous-generation terminal block and custom wiring approaches. The expanding deployment of industrial wireless sensor networks, edge computing infrastructure, and machine vision systems within manufacturing facilities is generating incremental connector demand for small-form-factor board connectors, coaxial antenna connectors, and sealed M5 and M8 sensor connectors whose cumulative unit volumes across the global manufacturing installed base represent a structurally growing connector demand stream that is less susceptible to individual industry cycle fluctuations than the automotive or consumer electronics connector markets whose concentration in specific end-use sectors creates more pronounced demand cyclicality.

Key Challenges

Contact Material Cost Volatility, Gold and Palladium Plating Thickness Optimisation, and Precious Metal Supply Chain Management Constraining Connector Manufacturing Economics

Electronic connector manufacturing economics are significantly exposed to the price volatility of gold, palladium, silver, and tin used in contact plating operations whose material cost contribution to connector manufacturing cost ranges from 15% to 45% depending on plating specifications, contact geometry, and finished connector price tier, creating raw material cost management challenges that require continuous optimisation of plating thickness and specification to maintain competitive pricing while satisfying the contact resistance, corrosion protection, and fretting wear resistance performance requirements of connector application specifications that define minimum acceptable plating parameters. Gold plating prices, which averaged approximately USD 62,000 per kilogram in 2025, create significant manufacturing cost sensitivity for high-reliability connector products whose contact performance specifications require selective gold flash or thick gold plating at critical contact engagement zones, with a one-standard-deviation upward move in gold prices adding 8% to 14% to the manufacturing cost of gold-plated signal connectors whose selling price competitiveness is determined by the highly price-aware procurement practices of electronics contract manufacturers sourcing commodity-grade connector products. Palladium, which is used as a substitute for gold in certain contact plating applications and whose supply is dominated by Russian and South African mining operations, has experienced price volatility ranging from USD 20,000 to USD 95,000 per kilogram over the decade preceding 2025, creating supply chain risk whose management requires connector manufacturers to maintain dual plating material qualification programs, strategic raw material inventory buffers, and contractual price adjustment mechanisms with customers that can accommodate precious metal market fluctuations within connector supply agreement pricing frameworks.

Signal Integrity and Electromagnetic Compatibility Challenges at High-Speed Data Rates and the Increasing Simulation and Testing Investment Required for Connector Design Validation

The escalating data rate requirements of next-generation electronic systems, with server and networking connector interfaces advancing from 56 gigabits per second to 112 gigabits per second and toward 224 gigabits per second per differential pair lane, are creating signal integrity and electromagnetic compatibility engineering challenges whose resolution requires three-dimensional electromagnetic field simulation, advanced material characterisation, and comprehensive channel compliance testing at frequencies extending to 60 gigahertz and beyond, imposing product development investment and validation timelines that substantially exceed those required for previous connector generations and are challenging the development resource capacity of all but the largest and most technologically capable connector manufacturers. Achieving the insertion loss, return loss, near-end and far-end crosstalk, and mode conversion performance required for IEEE 802.3 and OIF CEI high-speed channel specifications at 112 gigabits per second requires connector designers to precisely control contact geometry at tolerances below 50 micrometres, housing dielectric constant and dissipation factor across the full operating frequency bandwidth, contact-to-contact spacing to manage differential-to-common mode energy conversion, and shield aperture dimensions to prevent electromagnetic emission and susceptibility at millimetre-wave frequencies, creating a multi-parameter optimisation problem whose solution demands computational electromagnetic simulation infrastructure and measurement equipment investment of USD 3 million to USD 8 million per connector development program at the leading edge of high-speed connector technology. Customer qualification testing for high-speed data centre connector programs at hyperscale operators requires channel compliance testing with calibrated measurement uncertainty across multiple connector specimens and cable assembly configurations, extending validation timelines to 12 to 18 months per connector program and creating technical barriers that limit the number of suppliers capable of addressing the highest-performance data centre connector segments.

Automotive Connector Quality and Reliability Qualification Timelines, PPAP Requirements, and Warranty Liability Exposure Creating High Market Entry Barriers and Supply Concentration

The automotive connector market is characterised by qualification processes of exceptional rigor and duration relative to other electronic connector end markets, with automotive original equipment manufacturer and tier-one supplier qualification programs for new connector designs requiring completion of production part approval process documentation, dimensional measurement system analysis, process failure mode and effects analysis, control plans, and comprehensive environmental and mechanical reliability testing to automotive industry specifications including LV214, USCAR-2, ISO 16750, and supplier-specific requirements, generating qualification program durations of 18 to 36 months and investment of USD 800,000 to USD 3.5 million per connector family before first production delivery revenue is generated. The automotive industry’s zero-defect quality expectation, expressed through supplier quality management requirements including IATF 16949 third-party certification, customer-specific requirements from major original equipment manufacturers, and parts per million defect rate targets below 10 parts per million for critical connector applications, requires connector manufacturers serving automotive markets to invest substantially in manufacturing process capability, statistical process control infrastructure, automated optical inspection, and supplier quality management systems whose cumulative capital and operating cost creates a structural quality infrastructure premium relative to connector manufacturing for less quality-demanding markets. Automotive connector warranty liability exposure, where field failures of safety-relevant connectors in braking, steering, airbag, or high-voltage battery management systems can generate recall campaigns whose warranty cost per recalled vehicle ranges from USD 150 to USD 2,500 depending on repair complexity and dealer labour rates, creates contractual risk that automotive original equipment manufacturers allocate to component suppliers through warranty cost sharing agreements that impose financial liability beyond the connector component value and require robust design verification, manufacturing process control, and field failure analysis capability as prerequisites for automotive connector supply program participation.

Market Segmentation

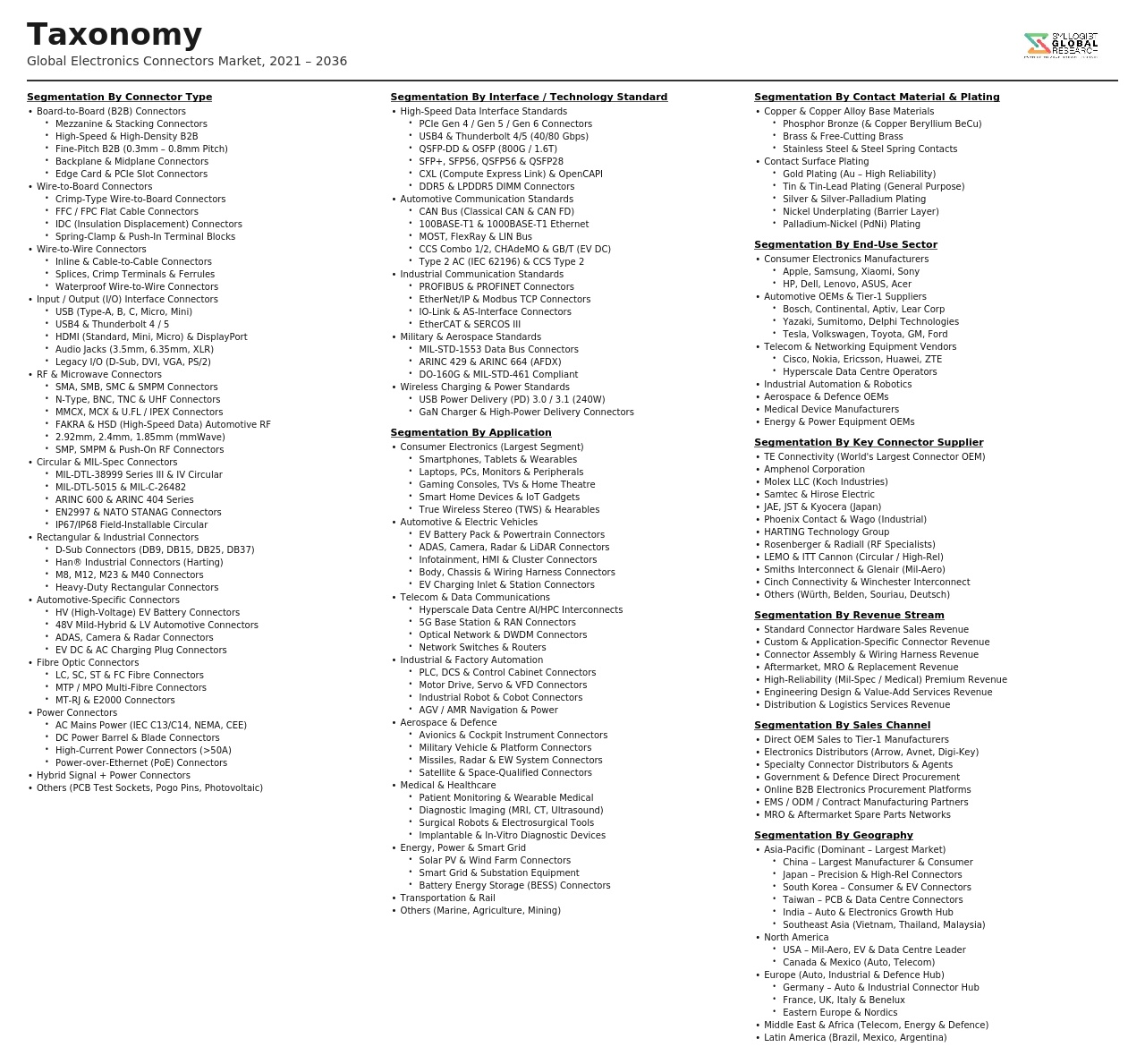

- Segmentation By Connector Type

- Board-to-Board Connectors (Mezzanine, Stacking, and Edge Card)

- Input-Output (I-O) and Interface Connectors (USB, HDMI, and DisplayPort)

- Wire-to-Board and Wire-to-Wire Connectors

- Circular and Rectangular Multi-Pin Connectors

- Coaxial and Radio Frequency (RF) Connectors

- Power Connectors and High-Voltage EV Connectors

- High-Speed Backplane and Cable Assembly Connectors

- Fibre Optic and Hybrid Electrical-Optical Connectors

- FPC and FFC Flexible Circuit Connectors

- M8 and M12 Industrial Circular Connectors

- Others

- Segmentation By End-Use Industry

- Automotive (ICE, HEV, PHEV, and BEV)

- Data Centre and Cloud Computing Infrastructure

- Telecommunications and Networking Equipment

- Industrial Automation and Robotics

- Consumer Electronics and Mobile Devices

- Aerospace and Defence

- Medical Devices and Healthcare

- Energy (Renewables, Power Distribution, and EV Charging)

- Others

- Segmentation By Signal Type

- Power Connectors (Low Voltage and High Voltage)

- Low-Frequency Signal Connectors

- High-Speed Digital Signal Connectors (Above 10 Gbps)

- Radio Frequency and Microwave Coaxial Connectors

- Fibre Optic Signal Connectors

- Mixed Signal (Power and Data Combined) Connectors

- Segmentation By Data Rate

- Standard Speed (Below 10 Gbps)

- High Speed (10 Gbps to 56 Gbps)

- Ultra High Speed (56 Gbps to 112 Gbps)

- Next-Generation (Above 112 Gbps per Lane)

- Segmentation By Termination and Housing Material

- Gold and Gold-Flashed Plated Contacts

- Palladium-Nickel Plated Contacts

- Tin and Tin-Lead Plated Contacts

- Silver and Silver-Alloy Plated Contacts

- Engineering Thermoplastic Housings (PA, PBT, and LCP)

- Metal Shell and Zinc Die-Cast Housings

- Thermoset and High-Temperature Resin Housings

- Segmentation By Sealing and Environmental Rating

- Standard Unsealed Connectors

- IP67 and IP68 Sealed Waterproof Connectors

- Military-Specification (MIL-DTL-38999, MIL-DTL-5015) Connectors

- ATEX and IECEx Hazardous Area Certified Connectors

- Medical Grade Biocompatibility-Certified Connectors

- High-Temperature and Extreme Environment Connectors

- Segmentation By Sales Channel

- Direct Sales to OEMs and Contract Manufacturers

- Authorised Electronic Component Distributors

- E-Commerce and Digital Procurement Platforms

- Specialty Connector Distributors

- Value-Added Resellers and Cable Assembly Integrators

- Segmentation By Region

- Asia-Pacific (China, Japan, South Korea, Taiwan, and Others)

- North America (United States and Canada)

- Europe (Germany, France, United Kingdom, and Others)

- Middle East and Africa

- Latin America (Brazil, Mexico, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Electronic Connectors Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by connector type, board-to-board, input-output, circular and rectangular, coaxial, power, and fibre optic, by end-use industry, automotive, data centre, telecommunications, industrial, consumer electronics, aerospace and defence, and medical, and by geography, to enable connector manufacturers, distributors, electronic equipment designers, and investors to identify which product categories and end-use markets will generate the highest absolute revenue and most commercially significant growth momentum across the forecast period?

- How is the global transition to battery electric vehicles, high-voltage power architectures operating at 400 to 800 volts, and in-vehicle Ethernet network topologies expected to reshape the automotive connector technology specifications, qualification requirements, and competitive supply landscape through 2034, what are the per-vehicle connector content value differentials between battery electric, plug-in hybrid, and internal combustion engine vehicle platforms across high-voltage power, advanced driver assistance system sensor network, and in-vehicle Ethernet connector categories, and which connector manufacturers are best positioned to capture the incremental automotive connector content growth associated with electric vehicle production ramp at major global automotive manufacturing programs?

- What is the projected commercial trajectory of high-speed data centre interconnect connectors operating at 112 to 224 gigabits per second per lane through 2034, how are the artificial intelligence infrastructure build-out programs of hyperscale cloud operators reshaping connector port count requirements, data rate upgrade cycles, and total procurement volumes at server, switch, and network interface card levels, and what are the signal integrity performance thresholds and production qualification requirements that differentiate leading connector suppliers from challenger competitors in the 224-gigabit-per-lane and co-packaged optics connector interface segments?

- How are miniaturisation requirements in consumer electronics, wearable devices, hearing instruments, and implantable medical devices driving connector pitch reduction and form factor innovation, what are the current state-of-the-art connector pitch dimensions, contact density, and current-carrying capacity benchmarks across board-to-board and flexible circuit connector categories, how is the USB Type-C universal interface standardisation mandate reshaping the consumer electronics connector supply landscape and creating scale economy opportunities for compliant connector manufacturers, and what emerging connector technologies are addressing the simultaneous requirements for smaller dimensions, higher bandwidth, and greater mechanical durability in next-generation portable and wearable device designs?

- Who are the leading electronic connector manufacturers, high-speed interconnect specialists, automotive connector suppliers, aerospace and defence connector producers, and medical connector developers currently defining the competitive landscape of the global electronic connectors market, and what are their respective product portfolio breadth across connector types and end-use markets, manufacturing and precision contact plating capabilities, automotive qualification program status and production supply positions at major electric vehicle programs, high-speed data centre connector development roadmaps, precious metal cost management strategies, and competitive positioning responses to the signal integrity engineering, automotive qualification burden, and contact material cost volatility challenges reshaping global electronic connector market dynamics through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Raw Material Price Volatility, Copper & Precious Metal Supply Disruption Risk

- Geopolitical Risk, Trade Restrictions & Concentration of PCB & Connector Manufacturing in Asia

- Technology Disruption, Wireless Connectivity Substitution & Connector Obsolescence Risk

- Counterfeit Components, Quality Fraud & Supply Chain Integrity Risk

- Miniaturisation Limits, Signal Integrity Challenges & High-Speed Performance Compliance Risk

- Regulatory Framework & Standards

- IEC, UL, MIL-SPEC & Industry Connector Performance, Safety & Qualification Standards

- Automotive Connector Standards: LV214, USCAR, ISO 20653 & AEC-Q Series Reliability Requirements

- High-Speed Data Connector Standards: USB4, PCIe 6.0, SFF & IEEE 802.3 Ethernet Standards

- Environmental & Hazardous Substance Regulations: RoHS, REACH & Conflict Mineral Compliance

- Defence, Aerospace & Medical Connector Certification: MIL-DTL, DO-160 & IEC 60601 Standards

- Global Electronic Connectors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Connector Type

- Board-to-Board Connectors

- Wire-to-Board Connectors

- Wire-to-Wire Connectors

- Input/Output (I/O) & Peripheral Connectors

- RF & Coaxial Connectors

- Circular & MIL-Spec Connectors

- Rectangular & Industrial Connectors

- Power Connectors & High-Voltage Connectors

- Fibre Optic Connectors

- Automotive Connectors

- Backplane & Mezzanine Connectors

- FPC & FFC (Flexible Printed Circuit) Connectors

- Market Size & Forecast by Technology

- High-Speed & High-Frequency Connector Technology (USB4, PCIe 6.0, CXL)

- Miniaturised & Micro/Nano Connector Technology

- Sealed & Waterproof Connector Technology (IP67, IP68 & IP69K Rated)

- Press-Fit & Surface Mount Technology (SMT) Connector Technology

- Magnetic & Pogo Pin Connector Technology

- High-Voltage & High-Power Connector Technology for EV & Energy Storage

- Fibre Optic & Optical Interconnect Technology

- Smart & Condition-Monitoring Embedded Connector Technology

- Market Size & Forecast by Contact Material

- Copper & Copper Alloy

- Gold-Plated Contacts

- Silver-Plated Contacts

- Tin-Plated Contacts

- Palladium-Nickel & Specialty Alloy Contacts

- Market Size & Forecast by Pitch Size

- Standard Pitch (Above 2.00 mm)

- Fine Pitch (0.50 mm to 2.00 mm)

- Ultra-Fine Pitch (Below 0.50 mm)

- Market Size & Forecast by End-Use Industry

- Consumer Electronics (Smartphones, Tablets, Laptops & Wearables)

- Automotive & Electric Vehicles

- Telecommunications & Data Centre Infrastructure

- Industrial Automation & Factory Equipment

- Aerospace & Defence

- Healthcare & Medical Devices

- Energy & Power (Renewable Energy, EV Charging & Smart Grid)

- Transportation & Rail

- Market Size & Forecast by Application

- Signal Transmission & Data Communication

- Power Distribution & High-Voltage Connections

- RF & Antenna Connectivity

- Sensor & Actuator Interconnection

- Board-Level & Backplane Interconnection

- External Peripheral & I/O Connectivity

- Market Size & Forecast by Sales Channel

- Direct OEM & Tier-1 Supply Agreements

- Authorised Distributor & Catalogue Distribution Channel

- E-Commerce & Online Component Procurement Channel

- Contract Electronics Manufacturer (CEM) & EMS Provider Channel

- North America Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Electronic Connectors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Connector Type

- By Technology

- By Contact Material

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- High-Speed Connector Technology Deep-Dive: USB4, PCIe 6.0, CXL & Co-Packaged Optical Interconnect Transition

- Automotive Connector Technology: HV/HV Shielded, HSD, Ethernet-over-Copper & 800V EV Architecture Connector Innovation

- Miniaturisation & Ultra-Fine Pitch Connector Technology: Sub-0.3 mm Pitch, FPC/FFC & Micro Board-to-Board Connectors

- High-Power & High-Voltage Connector Technology for EV Charging, Energy Storage & Renewable Energy Systems

- Sealed, Ruggedised & Harsh Environment Connector Technology for Automotive, Industrial & Defence Applications

- Fibre Optic & Active Optical Cable Connector Technology for Data Centre & Telecom High-Density Applications

- Smart Connector Technology: Embedded Sensing, Signal Integrity Monitoring & Predictive Contact Wear Detection

- Patent & IP Landscape in Electronic Connector Technologies

- Value Chain & Supply Chain Analysis

- Copper Strip, Alloy & Precious Metal Plating Material Supply Chain

- Plastic Housing, Thermoplastic Resin & Overmoulding Material Supply Chain

- Stamping, Plating, Moulding & Precision Contact Manufacturing Supply Chain

- Assembly, Quality Testing, Crimping & Cable Assembly Manufacturing Supply Chain

- Connector OEM Design, Brand Ownership & Product Development Channel

- Authorised Distributor, Catalogue Distributor & Value-Added Reseller Channel

- OEM, EMS, CEM & End-User Procurement & Qualification Channel

- Pricing Analysis

- Electronic Connector Unit Price Analysis by Connector Type, Technology & Performance Tier

- Contact Material & Plating Specification Impact on Connector Pricing Analysis

- High-Speed & High-Voltage Connector Premium Pricing vs. Standard Connector Benchmarking

- Miniaturised & Fine-Pitch Connector Pricing Trend & Cost Reduction Roadmap Analysis

- OEM Direct vs. Distribution Channel Pricing Structure, Discount & Margin Analysis

- Total Cost of Ownership Analysis: Connector Qualification, Tooling, Testing & Field Replacement Cost

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Electronic Connectors: Carbon Footprint, Copper Consumption, Precious Metal Use & End-of-Life Recyclability

- RoHS, REACH & Halogen-Free Compliance: Transition to Lead-Free, Cadmium-Free & Low-Toxicity Connector Materials

- Conflict Mineral Sourcing, Responsible Cobalt & Tin Supply Chain Compliance in Connector Manufacturing

- Connector Durability, Reliability & Lifecycle Extension Contribution to Electronic Waste Reduction

- Regulatory-Driven Sustainability, Net Zero Manufacturing & ESG Reporting in the Electronic Connector Industry

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Connector Type, Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Connector Type, End-Use Industry & Geography

- Player Classification

- Diversified Electronic Component & Connector Conglomerates

- Specialist Automotive Connector Manufacturers

- High-Speed & High-Frequency Connector Specialists

- Industrial, Circular & MIL-Spec Connector Manufacturers

- Miniaturised & Fine-Pitch Board-to-Board Connector Specialists

- Fibre Optic & Active Optical Cable Connector Providers

- High-Power & EV Charging Connector Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Connector Type, End-Use Industry & Region

- Company Profile

- Company Overview & Headquarters

- Electronic Connector Products & Technology Portfolio

- Key Customer Relationships & Reference OEM Design Wins

- Manufacturing Footprint & Production Capacity

- Revenue (Electronic Connector Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Capacity Expansion, Acquisitions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Connector Type, Technology, Contact Material, End-Use Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output