Market Definition

The Global Industrial Sensors Market encompasses the design, manufacturing, calibration, integration, and after-sale support of electronic sensing devices that measure, monitor, and convert physical, chemical, biological, and mechanical parameters of industrial processes and environments into electrical or digital signals used for process control, equipment monitoring, safety assurance, quality inspection, energy management, and operational data acquisition across the manufacturing, energy, oil and gas, chemicals, food and beverage, pharmaceuticals, automotive, aerospace, mining, water and wastewater, and building automation industries. Industrial sensors measure a comprehensive range of physical and chemical quantities including temperature, pressure, flow, level, proximity, displacement, position, speed and rotation, force and torque, vibration and acceleration, humidity and moisture, gas composition and concentration, pH and electrochemical parameters, optical properties, and electrical quantities, converting these measurements into standardised analogue or digital output signals compatible with industrial control system architectures including programmable logic controllers, distributed control systems, supervisory control and data acquisition platforms, and industrial Internet of Things data acquisition networks. The market encompasses contact and non-contact sensing modalities, wired and wireless communication interfaces including HART, Foundation Fieldbus, Profibus, IO-Link, WirelessHART, ISA100.11a, and industrial Ethernet protocols, intrinsically safe and explosion-proof sensor variants certified for hazardous area installation, and the emerging category of smart sensors incorporating onboard microprocessors, edge computing capability, digital communication interfaces, and self-diagnostic functions that transform sensor outputs from simple measured values into pre-processed data streams with embedded calibration, condition monitoring, and predictive maintenance intelligence. The market value chain extends from sensing element and transducer component manufacturers, through sensor device assembly and calibration operations, to the system integrators, distributors, and end-user industries whose process performance, safety, regulatory compliance, and energy efficiency requirements define the sensor specification and adoption dynamics across global industrial markets.

Market Insights

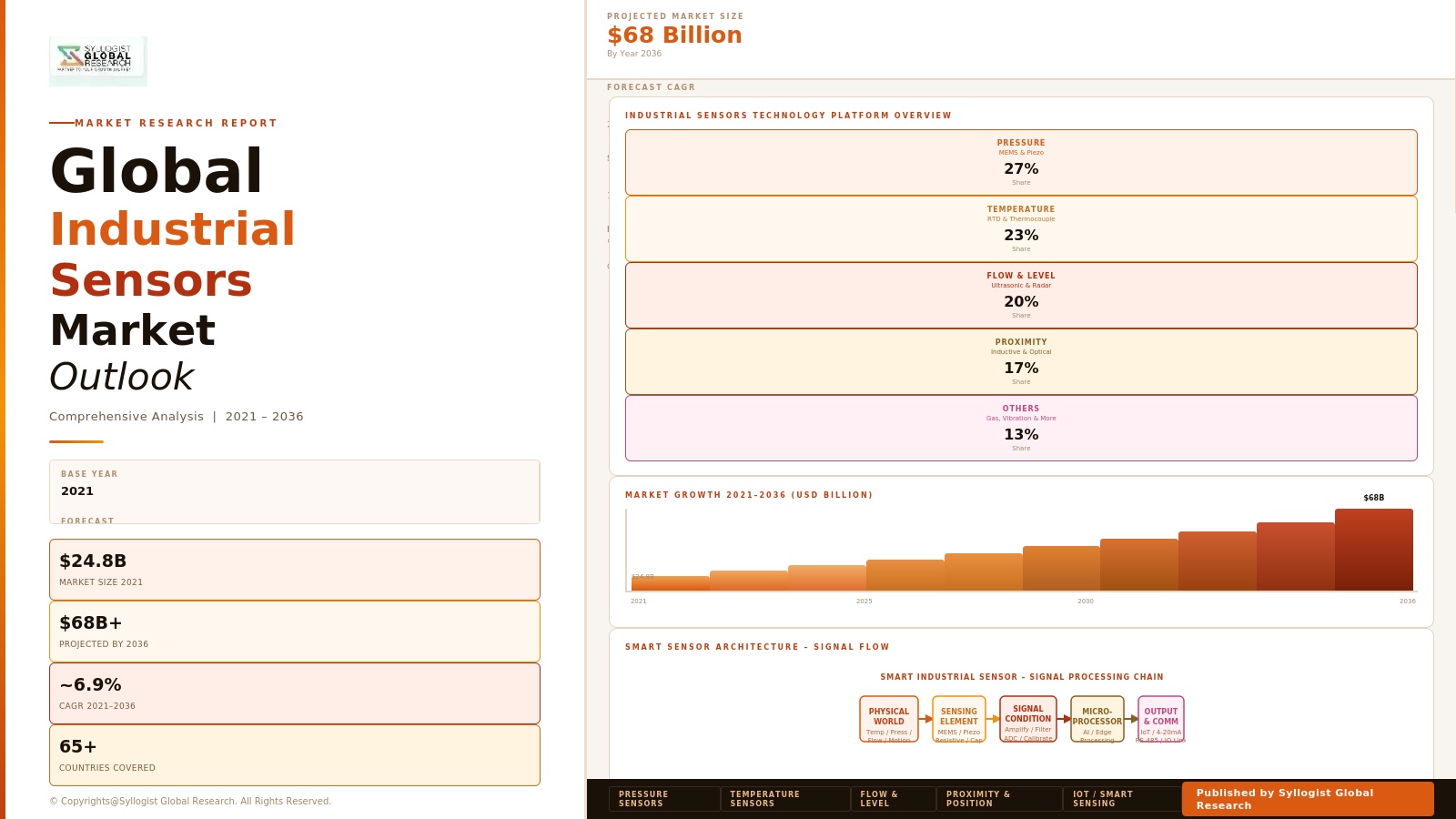

The global industrial sensors market was valued at approximately USD 24.6 billion in 2025 and is projected to reach USD 48.3 billion by 2034, advancing at a compound annual growth rate of 7.8% over the forecast period from 2027 to 2034, driven by the accelerating deployment of industrial Internet of Things architectures across manufacturing and process industries, the expanding regulatory requirements for process safety and environmental monitoring across major industrial jurisdictions, the growing adoption of predictive maintenance programs that require high-density sensor instrumentation of rotating and static equipment, and the structural expansion of industrial automation investment in emerging economies whose manufacturing sector development is generating new sensor demand across industries at an earlier stage of instrumentation maturity than equivalent sectors in developed markets. The market is experiencing a technology transition from conventional analogue transmitters and field instruments toward smart sensor platforms with digital communication capabilities, embedded diagnostics, and edge processing functions that deliver substantially greater operational intelligence per sensing point and are enabling new condition monitoring and process optimisation applications that conventional sensor architectures cannot support.

Temperature and pressure sensors collectively represent the largest product segments within the global industrial sensors market, accounting for approximately 38% of total market revenue in 2025 across thermocouple, resistance temperature detector, infrared, and thermal imaging temperature sensing technologies and differential, gauge, absolute, and multivariable pressure transmitter platforms, with these measurement parameters being universally required across virtually every industrial process application and generating the broadest installed base, highest replacement cycle volume, and most established distribution and service infrastructure of any sensor category in the industrial instrumentation market. Flow measurement sensors, encompassing electromagnetic, Coriolis, vortex, ultrasonic, thermal mass, and differential pressure flow metering technologies, represent the highest average selling price sensor category within the process industries segment, with custody transfer flow meters for hydrocarbon pipeline and liquefied natural gas applications commanding prices of USD 15,000 to USD 85,000 per instrument depending on line size and measurement accuracy class, generating a disproportionate revenue contribution from a relatively modest unit volume and sustaining the commercial importance of high-accuracy flow metrology to the total industrial sensor market revenue composition. Proximity and position sensors, encompassing inductive, capacitive, photoelectric, ultrasonic, and magnetic sensing technologies, are the highest-volume product category within the discrete manufacturing and factory automation segment, with unit shipments exceeding 800 million units annually in 2025 across machine tool, packaging, assembly automation, and material handling applications, and growing at approximately 9.2% annually as automated manufacturing line density and robot-to-sensor integration ratios increase with each successive generation of flexible manufacturing system deployment.

Asia-Pacific dominates the global industrial sensors market, accounting for approximately 44% of total market revenue in 2025, driven by the concentration of global electronics, automotive, semiconductor, chemical, and heavy manufacturing production capacity in China, Japan, South Korea, India, and Southeast Asia, whose combined industrial output generates the world’s largest installed base of automated production systems requiring continuous sensor instrumentation for process control, quality assurance, and equipment monitoring. China’s industrial sensor market reached approximately USD 5.8 billion in 2025 and is the world’s largest national market, growing at approximately 9.4% annually as Chinese manufacturers intensify automation investment in response to rising labour costs, quality improvement imperatives for export market competitiveness, and government Made in China 2025 industrial upgrading program incentives that support sensor and instrumentation procurement across targeted manufacturing sectors. The oil and gas, chemical, and petrochemical industries in the Middle East represent a growing and technically demanding regional market for process sensors, with Saudi Arabia, the United Arab Emirates, Kuwait, and Qatar collectively operating large hydrocarbon processing and downstream chemical manufacturing assets that require instrumentation to the most stringent process safety and hazardous area certification standards, and with ongoing capacity expansion programs at integrated refinery and petrochemical complexes generating greenfield sensor procurement at values estimated at approximately USD 420 million annually across the Gulf Cooperation Council states in the 2025 to 2030 capital expenditure cycle.

The proliferation of industrial Internet of Things platforms and the adoption of predictive maintenance, digital twin, and asset performance management programs across asset-intensive industries are fundamentally reshaping the sensor market by increasing the density of sensing points per facility, elevating the data communication and processing capability requirements of individual sensor devices, and creating demand for sensor networks whose aggregate data output volume and quality must satisfy the training and inference requirements of machine learning-based condition monitoring algorithms that generate actionable maintenance intelligence from sensor time series data. Smart sensors incorporating IO-Link digital communication, WirelessHART or ISA100 wireless transmission, and onboard fast Fourier transform vibration analysis or partial discharge detection algorithms are growing at approximately 16.3% annually, substantially outpacing the overall market growth rate, as industrial operators invest in sensor upgrades that simultaneously increase measurement capability, enable remote configuration and diagnostics, and provide the digital data connectivity required to integrate sensing points into enterprise asset management and industrial analytics platforms. Environmental and gas detection sensors are experiencing accelerating demand growth driven by the tightening of occupational health and safety regulations for toxic and combustible gas monitoring in confined spaces and hazardous process environments, the expansion of continuous emission monitoring requirements for industrial air quality compliance, the growing deployment of methane leak detection sensors along natural gas transmission and distribution infrastructure under regulatory frameworks enacted in the United States, European Union, and increasingly across major emerging market gas-producing nations, and the emerging market for indoor air quality monitoring in commercial and institutional buildings whose post-pandemic occupant health awareness has elevated the commercial priority of air quality sensing infrastructure investment.

Key Drivers

Industrial Automation Expansion, Smart Factory Investment, and Robot Density Growth Creating Structural High-Volume Sensor Demand Across Global Manufacturing

The global manufacturing industry’s sustained investment in industrial automation, collaborative robotics, flexible assembly systems, and smart factory digital infrastructure is generating structural and growing demand for industrial sensors across every automation technology category, with each incremental robot installation, automated guided vehicle, computer vision inspection station, and conveyor automation system requiring multiple sensors for position detection, collision avoidance, part presence verification, force feedback, and environmental perception whose aggregate demand scales in direct proportion to the expanding global installed base of automated manufacturing equipment. Global industrial robot installations reached approximately 590,000 units in 2025 and are projected to exceed 950,000 annual installations by 2034, with each industrial robot requiring an average of 12 to 18 sensors for joint position and torque sensing, end-of-arm tooling force and proximity detection, workspace safety monitoring, and machine vision guidance, generating a direct sensor demand stream of approximately 7 to 11 million sensor units annually from robot installations alone that complements the broader process sensor instrumentation demand of the manufacturing plant environments in which robots operate. The transition toward mass customisation and flexible manufacturing architectures, where production systems must be reconfigured rapidly to accommodate changing product mix and smaller batch sizes, is increasing the sensor density per production line relative to dedicated high-volume transfer line configurations, as flexible systems require more comprehensive object detection, dimensional measurement, and process parameter monitoring instrumentation to maintain quality and process consistency across a wider range of part types and production sequences than the single-product lines they replace.

Process Safety Regulation Intensification, Functional Safety Standard Compliance, and Hazardous Area Monitoring Requirements Driving Safety Sensor and Transmitter Adoption

The progressive tightening of process safety regulations and functional safety standard requirements across the oil and gas, chemical, pharmaceutical, food and beverage, and power generation industries is creating a non-discretionary compliance investment driver for safety-rated sensors, pressure transmitters, level gauges, and gas detection systems whose procurement is mandated by safety instrumented system design standards including IEC 61511 for process industries and IEC 62061 for machinery safety, with safety instrumented system sensor reliability performance requirements defined by safety integrity level classifications that specify probability of failure on demand limits achievable only through the use of certified safety sensors meeting IEC 61508 hardware safety integrity requirements. The European Union Seveso III Directive, United States OSHA Process Safety Management standard, and equivalent major hazard regulations in the United Kingdom, Australia, Canada, India, and China require systematic process hazard analysis and safety instrumented system implementation at covered facilities whose periodic revalidation and technology upgrade cycles generate recurring sensor replacement investment that grows with the expanding geographic scope of major hazard regulation coverage and the increasing stringency of safety performance requirements at each regulatory review cycle. Methane and volatile organic compound fugitive emission detection and monitoring obligations under United States Environmental Protection Agency regulations and equivalent frameworks in Canada, the European Union, and Norway are generating a rapidly expanding market for optical gas imaging cameras, laser-based open path gas detectors, and distributed sensor networks for continuous methane leak detection across oil and gas production, processing, and distribution infrastructure, with compliance-driven sensor procurement estimated at approximately USD 680 million annually in the United States alone following the implementation of the Inflation Reduction Act methane emissions reduction provisions.

Predictive Maintenance Program Adoption and Industrial IoT Platform Deployment Driving Vibration, Acoustic, and Condition Monitoring Sensor Investment Across Asset-Intensive Industries

The widespread adoption of predictive maintenance strategies across power generation, oil and gas, mining, pulp and paper, food processing, and heavy manufacturing industries, enabled by the commercial availability of industrial Internet of Things platforms, cloud-based machine learning analytics, and digital asset performance management systems, is generating sustained and growing investment in vibration sensors, acoustic emission sensors, ultrasonic thickness gauges, and multiparameter condition monitoring transmitters whose deployment density per facility is substantially greater than the instrumentation levels required for basic process control alone. Condition monitoring vibration sensor installations grew at approximately 11.4% annually in 2025 as industrial operators implemented route-based and permanently mounted online vibration monitoring programs at rotating equipment including pumps, compressors, fans, and motors whose unplanned failure consequences include production downtime costs ranging from USD 50,000 to USD 500,000 per hour at continuous process plants, making the total cost of ownership of predictive maintenance sensor programs highly favourable relative to run-to-failure or calendar-based preventive maintenance alternatives at most asset-intensive industrial facilities. The transition from route-based periodic vibration measurement, where technicians with handheld instruments collect data at scheduled intervals, toward permanently installed wireless sensor networks that continuously monitor equipment condition and transmit data to cloud analytics platforms for automated anomaly detection and remaining useful life prediction, is driving replacement of lower-cost handheld measurement programs with higher-value permanently installed sensor infrastructure whose per-asset investment of USD 800 to USD 3,500 per monitoring point generates documented maintenance cost reductions of 20% to 35% and unplanned downtime reduction of 30% to 50% at facilities with mature predictive maintenance program implementation.

Key Challenges

Cybersecurity Vulnerability of Industrial Sensor Networks, Operational Technology Attack Surface Expansion, and Secure Connectivity Implementation Complexity

The integration of industrial sensors into Internet of Things networks, cloud data platforms, and enterprise information systems is creating expanded cybersecurity attack surfaces whose exploitation at industrial facilities controlling physical processes could result in production disruption, equipment damage, safety system compromise, or environmental incidents, compelling industrial operators to implement comprehensive operational technology cybersecurity programs whose cost, complexity, and skilled workforce requirements represent a significant barrier to the pace of connected sensor deployment across facilities whose security infrastructure and personnel capability have not kept pace with the connectivity aspirations of digital transformation programs. Industrial sensor networks communicating over wireless protocols including WirelessHART, ISA100.11a, and industrial Wi-Fi are exposed to radio frequency jamming, man-in-the-middle attack, and rogue access point vulnerabilities that require cryptographic authentication, encrypted data transmission, and network intrusion detection capabilities whose implementation on resource-constrained sensor devices with limited processing power and battery energy budgets presents genuine technical challenges that sensor developers are progressively addressing through dedicated security microcontrollers and lightweight cryptographic protocol implementations. The diversity of industrial communication protocols and sensor device firmware architectures across the installed base of industrial instrumentation means that cybersecurity patch management, firmware update distribution, and vulnerability remediation programs cannot be implemented with the centralised automation available for enterprise information technology systems, requiring manual update procedures at individual field devices that impose significant operational technology cybersecurity maintenance burden on industrial facility instrumentation and control engineering teams whose staffing levels were not resourced for the ongoing cybersecurity management obligations that connected sensor deployment creates.

Harsh Environment Reliability Requirements, Extreme Temperature and Pressure Certification Costs, and Long Qualification Timelines Limiting Sensor Innovation Deployment Pace

Industrial sensors deployed in oil and gas wellhead, downhole, and subsea environments, high-temperature furnace and kiln applications, cryogenic liquefied natural gas processing, and corrosive chemical process streams must satisfy environmental performance specifications including temperature ratings from minus 200 to plus 1,800 degrees Celsius, pressure ratings to 1,000 bar, explosion-proof and intrinsically safe electrical certifications to IECEx, ATEX, and NEC standards, and material compatibility requirements for aggressive chemicals including hydrofluoric acid, chlorine, and high-concentration caustics whose cumulative specification burden creates product development and certification programs of 18 to 48 months duration and USD 500,000 to USD 3 million cost per new sensor platform that are feasible only for established sensor manufacturers with the balance sheet, regulatory affairs expertise, and testing infrastructure to sustain multi-year certification investment before generating product revenue. The fragmentation of hazardous area electrical equipment certification requirements across IECEx international, European ATEX, North American NEC and CEC, Brazilian INMETRO, Russian GOST, Chinese NEPSI, and other national frameworks requires separate certification submissions and testing at approved test laboratories in each jurisdiction, with the aggregate cost of global market certifications for a single intrinsically safe sensor transmitter commonly exceeding USD 1.5 million and requiring three to five years from initial design freeze to completion of all major market certifications, creating a structural barrier to rapid sensor technology innovation deployment in the oil and gas, chemical, and mining segments where hazardous area certification coverage is a basic market access requirement.

Sensor Drift, Calibration Management Burden, and Total Cost of Ownership Escalation in High-Density Industrial Internet of Things Sensor Deployments

The deployment of high-density industrial sensor networks containing hundreds or thousands of sensing points per facility creates calibration management challenges whose operational cost and scheduling complexity scale non-linearly with sensor count, as each instrument must be periodically removed from service, physically transported to calibration infrastructure, calibrated against traceable reference standards, and returned to service within the documentation and record management requirements of quality management systems including ISO 9001, pharmaceutical GMP, and food safety HACCP frameworks, creating calibration program management burdens that can consume significant instrumentation technician labour and process downtime whose aggregate annual cost at large continuously operating process plants with thousands of instrumented measurement points reaches USD 1.5 million to USD 4 million per facility. Sensor drift in process measurement applications, arising from sensing element degradation, fouling of process-wetted surfaces, reference junction ageing in thermocouples, and diaphragm fatigue in pressure sensors, is a persistent source of measurement inaccuracy that degrades process control performance and product quality when drift accumulation between calibration intervals exceeds process tolerance limits, requiring either high-frequency calibration programs that increase maintenance cost or acceptance of measurement uncertainty that limits process optimisation capability. The increasing deployment of wireless battery-powered sensors in Internet of Things condition monitoring applications creates battery management obligations including periodic replacement of non-rechargeable primary batteries with service lives of one to five years depending on transmission frequency and sensor type, whose aggregate battery procurement, replacement labour, and hazardous waste disposal costs at facilities deploying thousands of wireless sensor nodes represent a total cost of ownership component frequently underestimated in wireless sensor network deployment business case assessments.

Market Segmentation

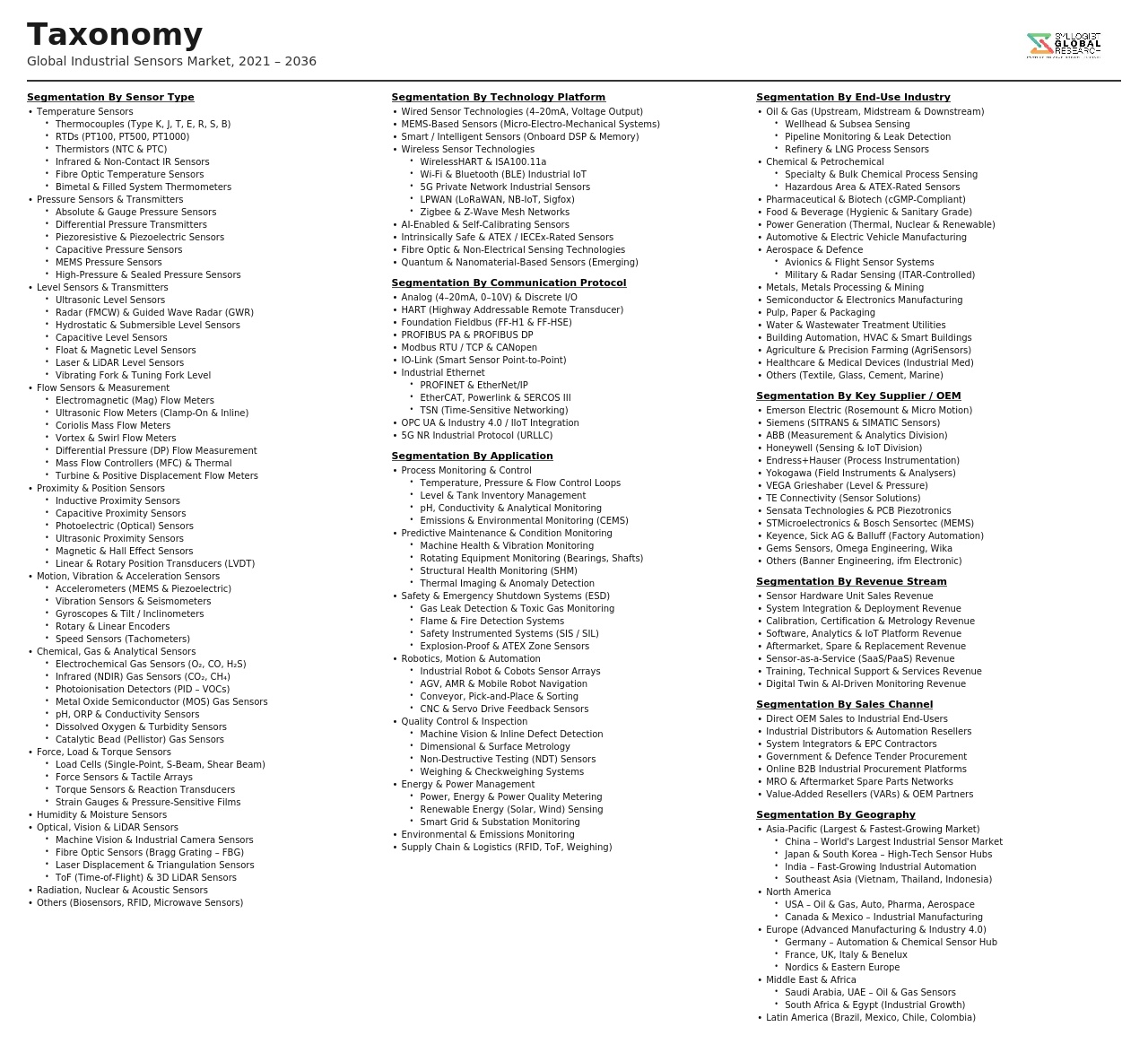

- Segmentation By Sensor Type

- Temperature Sensors (Thermocouples, RTDs, and Infrared)

- Pressure Sensors and Transmitters

- Flow Sensors and Meters (Electromagnetic, Coriolis, Vortex, and Ultrasonic)

- Level Sensors and Gauges (Radar, Ultrasonic, and Guided Wave)

- Proximity and Position Sensors (Inductive, Capacitive, and Photoelectric)

- Vibration and Acoustic Emission Sensors

- Force, Torque, and Load Sensors

- Gas and Chemical Sensors (Electrochemical, Catalytic, and Optical)

- Humidity and Moisture Sensors

- Speed and Rotation Sensors (Encoders and Tachometers)

- Image and Vision Sensors

- Others

- Segmentation By End-Use Industry

- Oil and Gas (Upstream, Midstream, and Downstream)

- Chemical and Petrochemical Manufacturing

- Food and Beverage Processing

- Pharmaceutical and Life Sciences

- Automotive Manufacturing and Assembly

- Semiconductor and Electronics Manufacturing

- Power Generation (Thermal, Nuclear, and Renewable)

- Water and Wastewater Treatment

- Mining and Mineral Processing

- Pulp, Paper, and Packaging

- Building Automation and HVAC

- Others

- Segmentation By Output and Communication Interface

- Analogue Output (4-20 mA and 0-10 V)

- HART Protocol Digital Communication

- Foundation Fieldbus and Profibus

- IO-Link Smart Sensor Interface

- Industrial Ethernet (Profinet, EtherNet/IP, and Modbus TCP)

- WirelessHART and ISA100.11a Wireless

- Industrial Wi-Fi and Bluetooth Low Energy

- Others

- Segmentation By Certification and Safety Rating

- Standard Industrial Grade Sensors

- Intrinsically Safe (ATEX and IECEx Certified)

- Explosion-Proof and Flameproof Certified Sensors

- Safety Integrity Level (SIL) Rated Sensors (SIL 1, 2, and 3)

- Hygienic and Sanitary Grade Sensors (3-A and EHEDG Certified)

- Automotive Grade Sensors (AEC-Q100 and IATF 16949)

- Segmentation By Technology

- MEMS-Based Sensors

- Optical and Fibre Optic Sensors

- Ultrasonic Sensors

- Radar and Microwave Sensors

- Electrochemical and Solid-State Gas Sensors

- Piezoelectric and Piezoresistive Sensors

- Capacitive and Inductive Sensing Technology

- Thermal and Infrared Sensing Technology

- Others

- Segmentation By Intelligence Level

- Conventional Analogue Transmitters

- Smart Sensors with Digital Communication

- Smart Sensors with Onboard Edge Processing and Diagnostics

- Wireless IoT Sensor Nodes with Cloud Connectivity

- AI-Integrated Predictive Sensor Platforms

- Segmentation By Sales Channel

- Direct Sales to End-User Industries

- Industrial Distributors and Wholesalers

- System Integrators and Engineering Contractors

- Original Equipment Manufacturer (OEM) Supply

- E-Commerce and Digital Industrial Procurement Platforms

- Segmentation By Region

- Asia-Pacific (China, Japan, South Korea, India, and Others)

- North America (United States and Canada)

- Europe (Germany, United Kingdom, France, and Others)

- Middle East and Africa

- Latin America (Brazil, Mexico, and Others)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Industrial Sensors Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by sensor type, temperature, pressure, flow, level, proximity and position, vibration, and gas and chemical sensors, by end-use industry, oil and gas, chemical and petrochemical, food and beverage, automotive, semiconductor, and power generation, and by geography, to enable sensor manufacturers, system integrators, distributors, and end-user procurement functions to identify which sensor categories and industrial markets will generate the highest absolute revenue and most commercially significant demand growth across the forecast period?

- How is the adoption of industrial Internet of Things platforms, predictive maintenance analytics, and smart factory digital infrastructure expected to reshape industrial sensor technology specifications, connectivity requirements, data output volume, and competitive differentiation criteria through 2034, what are the documented operational performance improvements in equipment uptime, energy efficiency, and maintenance cost reduction being achieved at facilities implementing high-density smart sensor deployments connected to cloud analytics platforms, and which sensor types and industrial application segments are generating the most commercially significant transition from conventional analogue instrumentation toward IO-Link, WirelessHART, and industrial Ethernet connected smart sensor architectures?

- What is the projected growth trajectory of safety-rated sensors and safety instrumented system transmitters through 2034, encompassing SIL-rated pressure, temperature, level, and gas detection sensors across oil and gas, chemical, pharmaceutical, and power generation industries, how are the IEC 61511 safety instrumented system lifecycle standard requirements, OSHA Process Safety Management regulatory framework, and equivalent national major hazard regulations across the European Union, United Kingdom, India, and Australia driving safety sensor specification and procurement decisions, and which industrial sectors and geographic markets are generating the most commercially significant near-term safety sensor demand from regulatory compliance upgrade programs?

- How are emerging sensor technologies including distributed fibre optic sensing, MEMS-based inertial and environmental sensors, optical gas imaging, laser-based open path gas detection, and quantum sensing platforms expected to displace or complement conventional electrochemical, piezoelectric, and thermometric sensing technologies in high-value industrial applications through 2034, which application segments offer the clearest technology substitution opportunity for emerging sensing platforms, and what are the performance, cost, and reliability certification barriers that must be overcome for these technologies to achieve broad deployment across process industry and discrete manufacturing sensing applications?

- Who are the leading industrial sensor and transmitter manufacturers, smart sensor platform developers, gas detection system specialists, condition monitoring sensor companies, and industrial IoT connectivity solution providers currently defining the competitive landscape of the global industrial sensors market, and what are their respective product portfolio breadth across sensor measurement parameters and industrial application segments, manufacturing and calibration facility footprints, hazardous area certification coverage across major global regulatory frameworks, research and development investment in smart sensor edge processing and wireless connectivity technology, and competitive positioning responses to the cybersecurity, calibration management, and harsh environment certification challenges reshaping industrial sensor market dynamics through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Semiconductor Component Shortage, Supply Chain Disruption & Single-Source Dependency Risk

- Cybersecurity, IIoT Connectivity Vulnerability & Operational Technology (OT) Network Risk

- Harsh Environment Reliability, Calibration Drift & Field Performance Failure Risk

- Rapid Technology Obsolescence, Platform Migration & Backward Compatibility Risk

- Geopolitical, Export Control & Critical Raw Material Supply Concentration Risk

- Regulatory Framework & Standards

- IEC, ISO & ANSI Industrial Sensor Performance, Safety & Calibration Standards

- Functional Safety Standards (IEC 61508, IEC 61511 & ISO 13849) Applicable to Safety-Rated Industrial Sensors

- Hazardous Area & Explosion-Proof Sensor Certification: ATEX, IECEx & NEC Standards

- Industrial IoT, Wireless Sensor Network & Protocol Standards (IO-Link, OPC UA, HART & WirelessHART)

- Environmental, RoHS, REACH & Conflict Mineral Compliance Standards for Industrial Sensor Manufacturing

- Global Industrial Sensors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units)

- Market Size & Forecast by Sensor Type

- Pressure Sensors

- Temperature Sensors

- Level Sensors

- Flow Sensors & Flowmeters

- Position & Displacement Sensors

- Proximity Sensors

- Force, Load & Torque Sensors

- Vibration & Acceleration Sensors (Accelerometers & IMUs)

- Gas & Chemical Sensors

- Humidity & Moisture Sensors

- Optical & Vision Sensors

- Ultrasonic Sensors

- Magnetic & Inductive Sensors

- Current & Voltage Sensors

- Market Size & Forecast by Technology

- MEMS (Micro-Electro-Mechanical Systems) Technology

- Piezoelectric Technology

- Capacitive Technology

- Resistive & Strain Gauge Technology

- Inductive & Eddy Current Technology

- Optical Fibre & Photonic Sensing Technology

- Ultrasonic & Acoustic Technology

- Infrared & Thermal Imaging Technology

- Wireless & IoT-Enabled Smart Sensor Technology

- Market Size & Forecast by Output Type

- Analog Output (4-20 mA, 0-10 V)

- Digital Output (IO-Link, RS-485 & Modbus)

- Wireless Output (Bluetooth, Wi-Fi, Zigbee & WirelessHART)

- HART & Fieldbus Output (PROFIBUS, Foundation Fieldbus & PROFINET)

- Market Size & Forecast by Form Factor

- Discrete & Point Sensors

- Smart & Intelligent Sensors with Onboard Processing

- Sensor Arrays & Multi-Parameter Modules

- Wireless Sensor Nodes & Edge Sensing Devices

- Market Size & Forecast by End-Use Industry

- Oil & Gas & Energy

- Chemical & Petrochemical Processing

- Automotive & Electric Vehicles

- Semiconductor & Electronics Manufacturing

- Food & Beverage Processing

- Pharmaceuticals & Life Sciences

- Metals, Mining & Materials Processing

- Water & Wastewater Treatment

- Aerospace & Defence

- Power Generation & Utilities

- Pulp, Paper & Packaging

- Factory Automation & Discrete Manufacturing

- Market Size & Forecast by Application

- Process Monitoring & Control

- Predictive Maintenance & Condition Monitoring

- Safety & Emergency Shutdown Systems

- Quality Inspection & In-Line Measurement

- Energy Monitoring & Efficiency Optimisation

- Environmental Monitoring & Emissions Measurement

- Robotics, Motion Control & Machine Automation

- Market Size & Forecast by Sales Channel

- Direct OEM & System Integrator Supply

- Authorised Distributor & Value-Added Reseller (VAR) Channel

- E-Commerce & Online Industrial Procurement Channel

- Engineering, Procurement & Construction (EPC) Project Supply Channel

- North America Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Europe Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Asia-Pacific Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Latin America Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Middle East & Africa Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

- Country-Wise* Industrial Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units)

- By Sensor Type

- By Technology

- By Output Type

- By End-Use Industry

- By Application

- By Sales Channel

- By Country

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- MEMS Sensor Technology Deep-Dive: Fabrication Advances, Miniaturisation & Multi-Axis Integration

- Smart & Intelligent Sensor Technology: Onboard Signal Processing, Edge AI & Self-Calibration Capabilities

- Wireless Industrial Sensor Technology: WirelessHART, ISA100, Bluetooth 5 & Ultra-Wideband (UWB) for IIoT

- Optical Fibre Sensing Technology: Distributed Temperature, Strain & Acoustic Sensing for Industrial Applications

- IO-Link & Industrial Ethernet Sensor Integration Technology: Digital Communication, Parameterisation & Diagnostics

- AI-Enabled Sensor Fusion, Predictive Analytics & Anomaly Detection Technology for Industrial Environments

- Harsh Environment & Intrinsically Safe Sensor Technology: High-Temperature, High-Pressure & Explosion-Proof Designs

- Patent & IP Landscape in Industrial Sensor Technologies

- Value Chain & Supply Chain Analysis

- MEMS Wafer Fabrication, Sensing Element & Transducer Manufacturing Supply Chain

- ASIC, Signal Conditioning IC & Microcontroller Component Supply Chain

- Housing, Enclosure, Connector & Mechanical Assembly Manufacturing Supply Chain

- Calibration, Testing & Certification Service Supply Chain

- Sensor OEM Design, Brand Ownership & Product Development Channel

- Distributor, VAR, System Integrator & MRO Supply Channel

- Industrial End-User Procurement, Maintenance & Replacement Channel

- Pricing Analysis

- Industrial Sensor Unit Price Analysis by Sensor Type, Technology & Performance Tier

- Smart Sensor Premium Pricing vs. Conventional Sensor: Feature Differentiation & Value Analysis

- Wireless Sensor Node Pricing: Hardware, Connectivity Module & Gateway Cost Analysis

- Annual Maintenance, Calibration Service & Replacement Cycle Cost Analysis

- Total Cost of Ownership (TCO) Analysis: Smart vs. Conventional Industrial Sensor Deployments

- OEM Direct vs. Distribution Channel Pricing Structure & Margin Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Industrial Sensors: Carbon Footprint, Energy Consumption, Material Use & End-of-Life Disposal

- Energy Efficiency Gains in Industrial Processes Enabled by Precision Sensing & Real-Time Monitoring

- Emissions Reduction, Leak Detection & Environmental Compliance Contribution of Industrial Gas & Chemical Sensors

- Predictive Maintenance, Asset Life Extension & Resource Efficiency Benefits of Condition Monitoring Sensors

- Regulatory-Driven Sustainability, RoHS/REACH Compliance & ESG Reporting in Industrial Sensor Manufacturing

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Sensor Type, Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sensor Type, End-Use Industry & Geography

- Player Classification

- Diversified Industrial Automation & Instrumentation Conglomerates

- Specialist Sensor Manufacturers by Type (Pressure, Temperature, Flow & Level)

- MEMS & Semiconductor Sensor Companies

- Smart Sensor, IIoT & Edge Computing Platform Providers

- Wireless Sensor Network & Industrial IoT Hardware Specialists

- Niche & Application-Specific Sensor Manufacturers (Gas, Vision & Force)

- Competitive Analysis Frameworks

- Market Share Analysis by Sensor Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Industrial Sensor Products & Technology Portfolio

- Key Customer Relationships & Reference Industrial Deployments

- Manufacturing Footprint & Production Capacity

- Revenue (Industrial Sensor Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Capacity Expansion, Acquisitions)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Sensor Type, Technology, Output Type, End-Use Industry & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output