Market Definition

The Global Irrigation Systems Market encompasses the design, manufacture, supply, installation, and operation of infrastructure and equipment used to artificially deliver water to agricultural land, including drip and micro-irrigation systems, sprinkler and center pivot systems, surface and flood irrigation infrastructure, subsurface irrigation networks, and associated pumping, filtration, fertigation, automation, and soil moisture monitoring components, procured by commercial farmers, agribusinesses, government irrigation agencies, horticultural operators, and landscape management organizations for field crops, orchards, vegetables, turf, and greenhouse production worldwide.

Market Insights

The global irrigation systems market is entering a period of sustained structural growth, driven by the simultaneous pressures of accelerating freshwater scarcity, expanding agricultural production requirements from growing global food demand, and the progressive tightening of water use efficiency regulations that are compelling farmers and irrigation authorities worldwide to transition from inefficient surface and flood irrigation practices toward precision water delivery technologies that maximize crop output per unit of water consumed. The market was valued at approximately USD 17.8 billion in 2025 and is projected to advance at a compound annual growth rate of 7.3% through 2034, as the combination of climate-driven water stress intensification, government subsidy programs supporting drip and micro-irrigation adoption in water-scarce agricultural regions, and the integration of digital automation and soil sensing technology into modern irrigation management systems drives a broad-based upgrade cycle from conventional gravity-fed surface irrigation toward sensor-guided precision irrigation infrastructure across major agricultural production regions in Asia, the Middle East, Africa, and Latin America.

Drip and micro-irrigation systems represent the fastest-growing technology segment within the global irrigation market, reflecting their demonstrated ability to reduce agricultural water consumption by forty to sixty percent relative to conventional surface irrigation methods while simultaneously improving crop yield, quality, and fertilizer use efficiency through precise application of water and nutrients directly to the root zone at controlled rates calibrated to crop water demand and soil moisture status. The adoption of subsurface drip irrigation, which installs emitter lines below the soil surface to deliver water directly at root depth while eliminating surface evaporation losses and enabling uninterrupted mechanized field operations over installed drip lines, is registering growing procurement activity in high-value vegetable, fruit, and cash crop production systems where the capital investment in subsurface installation is justified by the operational and yield efficiency advantages achievable over the multi-year productive life of properly installed subsurface drip networks. Center pivot and linear move sprinkler systems maintain a dominant position in large-scale grain and forage crop irrigation across the North American Great Plains, South American Cerrado, and Eastern European steppe regions, where the operational efficiency of large-radius pivot systems covering several hundred hectares per installation provides irrigation water delivery economics that no alternative system type can match at comparable field scale.

The integration of digital precision irrigation management technology is fundamentally transforming the operational sophistication and water use efficiency performance of modern irrigation systems, as soil moisture sensor networks, evapotranspiration-based irrigation scheduling algorithms, variable rate irrigation prescriptions linked to spatial soil variability mapping, and remote monitoring and control platforms enable irrigation managers to replace fixed schedule or crop appearance-based water application decisions with real-time data-driven irrigation management that consistently delivers water precisely when, where, and in the quantities that crop water stress thresholds and soil moisture depletion levels require. Smart irrigation controllers incorporating weather forecast data, satellite-derived crop coefficient estimates, and AI-powered predictive irrigation scheduling are gaining adoption among commercial horticultural and specialty crop producers where the premium value of irrigated output justifies investment in advanced automation systems delivering measurable reductions in water consumption and energy costs relative to conventional timer-based irrigation scheduling.

Asia-Pacific dominates the global irrigation systems market by installed infrastructure scale and annual procurement volume, driven by the massive agricultural water consumption of rice, wheat, sugarcane, and vegetable production across China, India, Indonesia, and Vietnam, the large ongoing government investment in irrigation infrastructure modernization programs, and the growing adoption of drip and micro-irrigation in water-stressed Indian agricultural states supported by national government subsidy programs making precision irrigation systems economically accessible to smallholder farmers. The Middle East and Africa represents the fastest-growing regional market, propelled by severe water scarcity conditions in the Arabian Peninsula and North Africa, large-scale horticultural export production requiring efficient irrigation across water-constrained growing regions, and development bank-funded irrigation modernization programs across sub-Saharan Africa targeting food security improvement through expanded irrigated area and improved water use efficiency. North America maintains a large and technologically advanced irrigation market anchored by center pivot systems in the Great Plains and Pacific Coast specialty crop drip irrigation investment.

Key Drivers

Accelerating Freshwater Scarcity and Agricultural Water Use Efficiency Mandates Compelling Transition from Surface Flood Irrigation to Precision Drip and Micro-Irrigation Systems Globally

Progressive depletion of groundwater aquifers supporting irrigated agriculture in major food-producing regions including the Indo-Gangetic Plain, North China Plain, California Central Valley, and Middle Eastern agricultural zones is creating an existential water availability constraint that is compelling governments and farmers to mandate or incentivize the transition from highly inefficient surface flood irrigation practices, which apply water with field-level efficiencies below fifty percent, toward precision drip and micro-irrigation systems achieving application efficiencies above ninety percent that sustain equivalent or superior crop production on substantially reduced water volumes. Freshwater abstraction caps, tradeable water entitlement frameworks, and tiered agricultural water pricing structures are simultaneously creating economic incentives for irrigation efficiency investment that reinforce regulatory compliance drivers across water-stressed agricultural production regions.

Government Subsidy Programs, Irrigation Infrastructure Development Finance, and Smallholder Precision Irrigation Access Initiatives Accelerating Market Penetration in Developing Economy Agricultural Regions

Large-scale government subsidy programs supporting drip and micro-irrigation adoption among smallholder and commercial farmers in India, Morocco, Ethiopia, Egypt, Brazil, and Mexico are significantly accelerating the market penetration of precision irrigation technologies by reducing the effective capital cost to farmers below the threshold that unsubsidized market economics would support, enabling adoption in farming communities where farm income levels and credit access would otherwise constrain investment in efficient irrigation infrastructure. Multilateral development bank agricultural water management programs, international climate adaptation funds, and bilateral development finance institution agricultural productivity projects are simultaneously channeling substantial investment into irrigation modernization across developing economy agricultural landscapes, expanding the addressable market for precision irrigation systems into previously underserved smallholder and government-managed irrigation scheme segments.

Digital Precision Irrigation, Smart Soil Moisture Management, and AI-Powered Scheduling Technology Driving Irrigation System Upgrade and Technology Add-On Investment Among Commercially Oriented Farm Operators

Commercial farm operators managing high-value horticultural, vegetable, and specialty crop production systems are investing in digital irrigation management technology upgrades that integrate soil moisture sensor networks, satellite-derived evapotranspiration data, weather forecast-based scheduling algorithms, and variable rate application capability into existing drip and sprinkler infrastructure, enabling real-time precision water management that reduces irrigation water consumption, lowers pumping energy costs, improves crop yield and quality outcomes, and generates documented sustainability performance data satisfying retailer and food processor supply chain water stewardship reporting requirements. The growing connectivity of irrigation control systems through cloud-based management platforms and mobile application interfaces is enabling farm operators to monitor and adjust irrigation programs remotely across multiple field locations, reducing the labor requirements of irrigation management while improving the timeliness and precision of water application decisions.

Key Challenges

High Capital Investment Requirements for Drip and Micro-Irrigation System Installation Creating Adoption Barriers Among Smallholder Farmers in Developing Country Agricultural Markets

The capital cost of installing drip or micro-irrigation infrastructure encompasses emitter lines, filtration systems, pressure regulators, manifolds, mainlines, fertigation equipment, and pump sets that collectively represent per-hectare investment substantially exceeding the annual net income of smallholder farmers in developing country agricultural markets, creating a fundamental affordability barrier that limits precision irrigation adoption to commercially oriented producers with access to formal agricultural credit, government subsidy support, or sufficient cash income from high-value crops to service the capital investment on commercially viable payback periods. The fragmentation of smallholder landholdings across multiple non-contiguous parcels further elevates effective installation costs and operational management complexity relative to the large consolidated fields for which most commercially designed drip and sprinkler systems are optimally engineered.

Inadequate Agricultural Water Pricing Frameworks and Subsidized Flood Irrigation Perpetuating Inefficient Water Use Practices That Undermine the Economic Case for Precision Irrigation Investment

In many developing and middle-income country agricultural markets, irrigation water is supplied to farmers at heavily subsidized tariff rates or provided free of charge through government-managed canal and gravity flow irrigation schemes, eliminating the water cost savings benefit that represents the primary economic return on precision irrigation investment and fundamentally undermining the financial justification for farmers to upgrade from surface flood irrigation to more capital-intensive drip and sprinkler systems whose investment payback depends on monetizable water savings that zero or near-zero water pricing frameworks render commercially invisible. Agricultural water pricing reform, which economists consistently identify as the most effective policy instrument for driving efficient irrigation technology adoption, faces strong political resistance from farm lobby groups and rural constituencies with electoral significance that complicates the implementation of water tariff structures reflecting true water scarcity costs.

Irrigation System Maintenance Complexity, Emitter Clogging, and Technical Support Availability Constraints Reducing Operational Reliability and Long-Term Performance of Drip Infrastructure in Remote Agricultural Areas

Drip and micro-irrigation systems require systematic maintenance programs encompassing filtration system cleaning and media replacement, emitter clogging inspection and flushing, lateral line pressure testing, fertigation equipment calibration, and periodic chemical treatment to prevent biological and mineral scale accumulation that progressively reduces emitter discharge uniformity and system performance over the operational life of installed infrastructure. In remote agricultural areas with limited access to technically qualified irrigation maintenance services, replacement components, and specialist repair expertise, system performance degradation from inadequate maintenance is a pervasive problem that reduces irrigation application uniformity, reduces crop yield outcomes, and accelerates system replacement requirements in ways that undermine the long-term return on investment and user satisfaction with precision irrigation system installations.

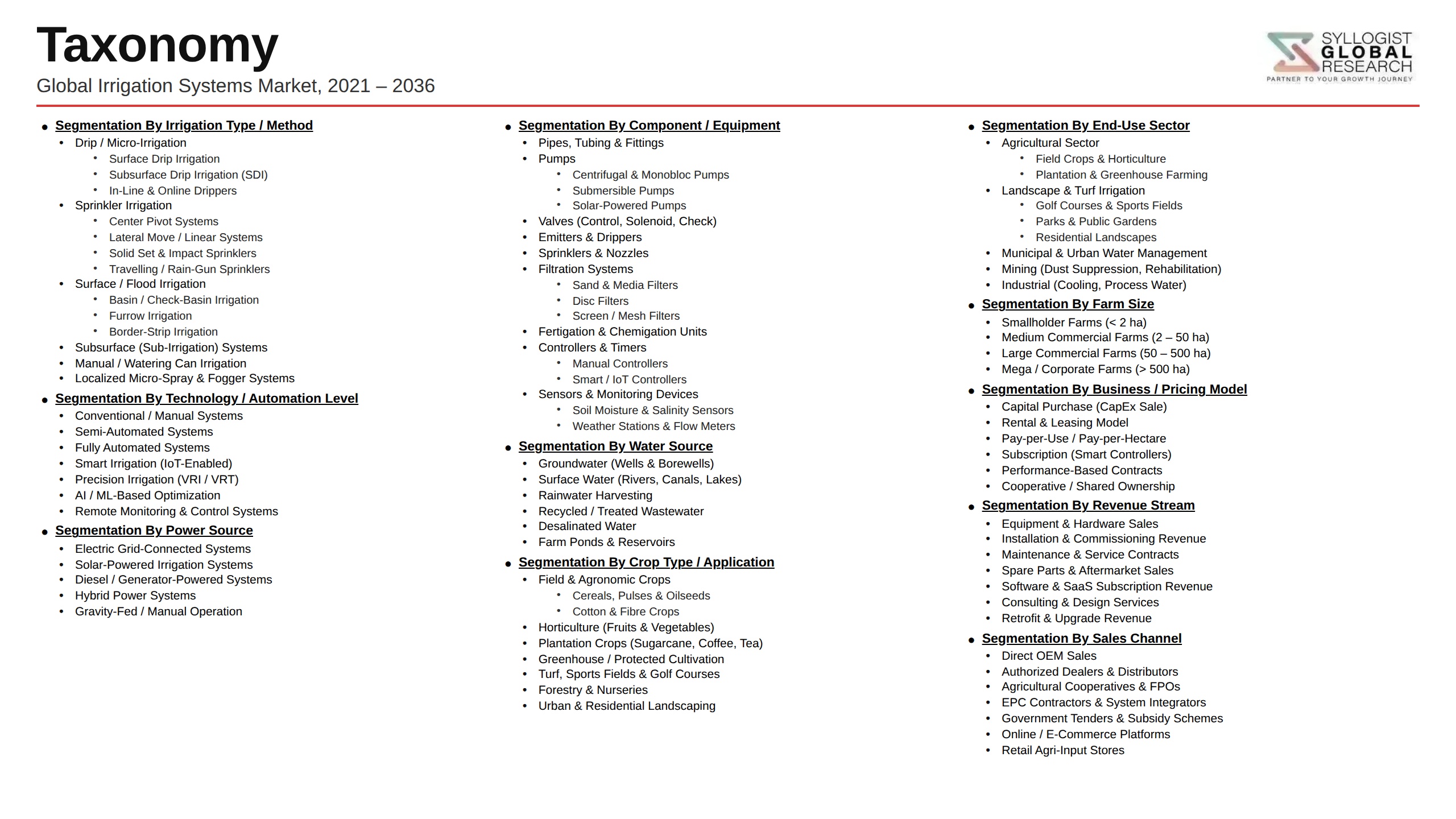

Market Segmentation

- Segmentation By System Type

- Drip and Micro-Irrigation Systems

- Sprinkler Irrigation Systems

- Center Pivot and Linear Move Systems

- Surface and Furrow Irrigation Infrastructure

- Subsurface Drip Irrigation Systems

- Flood and Basin Irrigation Systems

- Others

- Segmentation By Irrigation Method

- Micro-Drip and Point Source Emitter Systems

- Overhead and Under-Canopy Sprinkler Systems

- Subsurface Root-Zone Water Delivery

- Gravity-Fed Surface Flow Irrigation

- Automated Variable Rate Irrigation

- Others

- Segmentation By Crop Type

- Field Crops (Wheat, Maize, Rice, Soybean)

- Vegetables and Root Crops

- Fruits and Orchards

- Sugarcane and Energy Crops

- Cotton and Fiber Crops

- Turf, Landscape, and Golf Course

- Greenhouse and Protected Cultivation

- Others

- Segmentation By Component

- Emitters, Drippers, and Micro-Sprinklers

- Pipes, Tubes, and Lateral Lines

- Pumps and Pumping Stations

- Filtration and Water Treatment Systems

- Fertigation and Chemical Injection Equipment

- Controllers, Valves, and Automation Systems

- Soil Moisture Sensors and Monitoring Devices

- Others

- Segmentation By Power Source

- Electric Grid-Powered Irrigation Systems

- Solar-Powered Irrigation Pumps and Systems

- Diesel and Engine-Powered Pumping

- Gravity-Fed and Pressurized Canal Systems

- Others

- Segmentation By End User

- Commercial and Large-Scale Farm Operators

- Smallholder and Subsistence Farmers

- Government Irrigation Schemes and Agencies

- Horticultural and Specialty Crop Producers

- Greenhouse and Protected Cultivation Operators

- Golf Courses and Landscape Managers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global irrigation systems market valuation in 2025, projected through 2034, segmented by system type, crop type, and end user, enabling irrigation equipment manufacturers, agricultural technology investors, and government irrigation program planners to identify the highest-growth technology categories and most commercially significant precision irrigation adoption opportunities across the global agricultural water management landscape?

- How are government subsidy programs supporting drip and micro-irrigation adoption in India, Morocco, Ethiopia, Brazil, and Mexico reshaping market penetration rates among smallholder and commercial farm segments, and what subsidy design structures, credit facilitation mechanisms, and technical extension support models are proving most effective at translating program funding into sustained precision irrigation system adoption and operational performance outcomes?

- Which irrigation technology segments, specifically subsurface drip, AI-powered variable rate irrigation, solar-powered drip systems for off-grid smallholder applications, and smart fertigation platforms, are registering the highest commercial adoption momentum through 2034, and what crop value economics, water cost savings, yield improvement evidence, and digital connectivity requirements are driving technology selection among different farm scale and geographic market segments?

- How is the competitive landscape structured among global irrigation equipment manufacturers, regional drip irrigation specialists, digital precision irrigation platform developers, and solar pump suppliers, and what product portfolio expansion, geographic market entry, dealer and distributor network development, digital services integration, and smallholder-specific product design strategies are enabling leading companies to capture share across high-growth emerging market segments?

- What agricultural water pricing policy reforms, groundwater extraction regulation frameworks, tradeable water entitlement structures, and irrigation efficiency performance standards are governments in water-stressed agricultural regions implementing to drive economic incentives for precision irrigation adoption, and how are these evolving water governance frameworks shaping the investment economics and market demand for efficient irrigation system procurement across different country regulatory environments?

- How are digital soil moisture monitoring, satellite evapotranspiration estimation, weather forecast integration, and remote irrigation control platforms combining to improve water application efficiency and crop yield outcomes in commercial irrigation operations, and what return on investment evidence and operational performance data from precision irrigation technology deployments are persuading commercially oriented farm operators to invest in digital irrigation management upgrades?

- Which regional irrigation markets, specifically Asia-Pacific, the Middle East and Africa, and Latin America, are projected to generate the highest incremental system procurement growth through 2034, and what combinations of freshwater scarcity severity, irrigated area expansion programs, precision irrigation subsidy frameworks, solar pump economics, and food security investment priorities are defining irrigation technology adoption trajectories and market growth rates in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Water Scarcity, Groundwater Depletion & Freshwater Availability Risk

- Raw Material Price Volatility: Plastic, Steel & Polymer Input Cost Fluctuation Risk

- Climate Variability, Drought & Extreme Weather Impact on Irrigation Demand Risk

- Government Subsidy Policy Uncertainty & Agricultural Support Programme Withdrawal Risk

- Counterfeit Product Competition, Low-Quality Imports & Brand Erosion Risk

- Clogging, Maintenance Neglect & System Performance Degradation Risk

- Regulatory Framework & Standards

- National Water Rights, Irrigation Water Allocation, Abstraction Licensing & Water Use Efficiency Regulatory Frameworks

- ISO 9261, ISO 11545 & ASABE Standards for Drip Emitters, Sprinklers & Irrigation Equipment Performance

- EU Water Framework Directive, Common Agricultural Policy (CAP) & Irrigation Water Use Efficiency Standards

- Fertiliser & Nutrient Application through Fertigation: Regulatory Standards & Groundwater Protection Requirements

- Government Subsidy Schemes, Pradhan Mantri Krishi Sinchayee Yojana (PMKSY) & National Irrigation Programme Frameworks

- Recycled Water, Treated Wastewater Reuse & Greywater Irrigation Regulatory Frameworks by Jurisdiction

- Global Irrigation Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped & Irrigated Area, Million Hectares)

- Market Size & Forecast by System Type

- Drip Irrigation Systems (Surface Drip & Subsurface Drip Irrigation)

- Micro-Sprinkler & Micro-Jet Irrigation Systems

- Sprinkler Irrigation Systems (Centre Pivot, Lateral Move & Solid Set)

- Flood & Surface Irrigation Systems (Furrow, Border & Basin)

- Subsurface Drip Irrigation (SDI) Systems

- Boom & Reel Traveller Irrigation Systems

- Low-Volume & Bubbler Irrigation Systems

- Market Size & Forecast by Component

- Drip Emitters, Drippers & Pressure-Compensating Emitters

- Sprinkler Heads, Rotors & Impact Sprinklers

- Laterals, Mainlines & Distribution Pipes (HDPE, PVC & PE)

- Pumps, Pump Stations & Booster Sets

- Filters: Screen, Disc, Sand Media & Centrifugal Filters

- Fertigation Systems, Injectors & Nutrient Dosing Units

- Valves: Solenoid, Pressure Regulating, Air Release & Check Valves

- Controllers, Timers & Irrigation Automation Systems

- Soil Moisture Sensors, Weather Stations & Smart Irrigation Monitoring Systems

- Market Size & Forecast by Water Source

- Surface Water Irrigation (Rivers, Canals, Reservoirs & Ponds)

- Groundwater Irrigation (Boreholes, Tubewells & Aquifer Abstraction)

- Treated Wastewater & Recycled Water Irrigation

- Rainwater Harvesting-Fed Irrigation Systems

- Desalination-Sourced Irrigation Water

- Market Size & Forecast by Field of Application

- Row Crops & Cereal Grain Irrigation (Maize, Wheat, Rice & Soybean)

- Vegetable & Horticulture Crop Irrigation

- Orchard, Vineyard & Permanent Crop Irrigation

- Greenhouse & Controlled Environment Agriculture Irrigation

- Turf, Golf Course & Sports Field Irrigation

- Landscape, Public Green Space & Urban Irrigation

- Forestry, Afforestation & Nursery Irrigation

- Market Size & Forecast by Farm Size

- Smallholder & Subsistence Farms (Below 2 Hectares)

- Small & Family Farms (2 to 20 Hectares)

- Medium Commercial Farms (20 to 200 Hectares)

- Large-Scale & Corporate Farms (Above 200 Hectares)

- Market Size & Forecast by End-User

- Commercial & Corporate Farmers

- Smallholder & Subsistence Farmers

- Government Irrigation Authorities & Canal Command Projects

- Greenhouse, Nursery & Controlled Environment Agriculture Operators

- Landscape, Golf Course & Sports Turf Managers

- Municipal Authorities & Urban Green Infrastructure Managers

- Market Size & Forecast by Sales Channel

- Direct Manufacturer & OEM Sales

- Agri-Input Dealer, Distributor & Cooperative Network

- Irrigation Installer, Contractor & System Integrator Channel

- Government Subsidy, Tender & Public Scheme Procurement Channel

- Online & E-Commerce Channel

- North America Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Irrigation Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped & Irrigated Area, Million Hectares)

- By System Type

- By Component

- By Water Source

- By Field of Application

- By Farm Size

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, Spain, Italy, Netherlands, Israel, Turkey, China, India, Australia, Japan, South Korea, Indonesia, Pakistan, Brazil, Argentina, Chile, Colombia, Saudi Arabia, UAE, Egypt, South Africa, Morocco, Ethiopia

- Technology Landscape & Innovation Analysis

- Pressure-Compensating & Self-Cleaning Drip Emitter Technology Deep-Dive: Design Innovations, Anti-Drain & Root Intrusion Resistance

- Centre Pivot & Linear Move Precision Irrigation Technology: Variable Rate Irrigation (VRI), GPS Guidance & Telemetry Advances

- Smart Irrigation Controller & IoT-Based Scheduling Technology: ET-Based, Soil Moisture-Driven & Weather-Responsive Automation

- Precision Fertigation Technology: Real-Time EC/pH Monitoring, Proportional Dosing & Nutrient Optimisation Systems

- AI & Machine Learning for Irrigation Scheduling, Yield Prediction & Water Use Optimisation

- Subsurface Drip Irrigation (SDI) Technology: Tape Design, Installation Depth, Soil Wetting Pattern & Long-Term Performance

- Solar-Powered Irrigation System Technology: PV Pump Drives, Battery Storage & Off-Grid Rural Irrigation Design

- Patent & IP Landscape in Irrigation System Technologies

- Value Chain & Supply Chain Analysis

- Polyethylene, PVC, Polypropylene & Specialty Polymer Raw Material Supply Chain

- Pipe Extrusion, Emitter Moulding & Component Fabrication Supply Chain

- Pump, Filter, Valve & Control Equipment Manufacturing Supply Chain

- Sensor, Controller, Electronics & Smart Irrigation Hardware Supply Chain

- Packaged System Assembly, Kitting & Quality Testing Supply Chain

- Agri-Input Dealer, Distributor & Regional Stockist Channel

- Irrigation Installer, Contractor & Agronomic Advisory Service Channel

- Aftermarket Maintenance, Spare Parts & System Upgrade Channel

- Pricing Analysis

- Irrigation System Capital Cost Analysis by System Type & Scale (USD per Hectare)

- Drip vs. Sprinkler vs. Flood Irrigation Total Cost of Ownership (TCO) & Water Saving Payback Analysis

- Component Price Analysis by Product Type: Emitters, Pipes, Pumps, Filters & Controllers

- Smart & Precision Irrigation System Premium vs. Conventional System Pricing Comparison

- Impact of Government Subsidy Schemes on Net Farmer Investment & System Affordability Analysis

- Price Trend Analysis: Impact of Polymer Costs, Labour & Technology on Irrigation Equipment Pricing

- Sustainability & Environmental Analysis

- Water Use Efficiency: Comparative Water Saving Analysis Across Drip, Sprinkler, Micro & Surface Irrigation Methods

- Lifecycle Assessment (LCA) of Irrigation Systems: Embodied Energy, Plastic Use & End-of-Life Pipe & Tape Recycling

- Groundwater Depletion, Soil Salinisation & Waterlogging Risk from Over-Irrigation: Impact & Mitigation

- Role of Precision Irrigation in Reducing Agricultural Water Footprint & Supporting SDG 6 (Clean Water & Sanitation)

- Fertigation & Precision Nutrient Management: Reducing Nitrate Leaching, Nutrient Runoff & Fertiliser Carbon Footprint

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Application & Geography

- Player Classification

- Global Diversified Irrigation System Companies (Full Portfolio)

- Specialist Drip & Micro-Irrigation Manufacturers

- Specialist Centre Pivot, Lateral Move & Sprinkler Manufacturers

- Irrigation Pump, Filter & Valve Specialists

- Smart Irrigation Controller, Software & Precision Water Management Providers

- Regional & Local Irrigation Equipment Manufacturers

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Irrigation Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Irrigation Systems Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Contract Wins, Capacity Expansion)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Component, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Water Stewardship Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)