Market Definition

The Global Vertical Farming Market encompasses the design, construction, and operation of controlled-environment agricultural facilities utilizing stacked growing layers, artificial lighting, hydroponic, aeroponic, or aquaponic cultivation systems, and precision climate management technology to produce leafy greens, herbs, fruits, vegetables, and specialty crops in indoor urban and peri-urban environments, including purpose-built vertical farm facilities, repurposed warehouse and industrial space conversions, container farms, and building-integrated growing systems, serving retail, food service, pharmaceutical, and direct-to-consumer fresh produce markets globally.

Market Insights

The global vertical farming market is navigating a complex maturation phase that is simultaneously characterized by compelling long-term structural demand drivers, accelerating technology improvement across lighting efficiency and automation, and the sobering operational realities of high energy costs and capital intensity that have driven several high-profile vertical farming operators into financial restructuring or insolvency, prompting a fundamental industry recalibration toward business models with more disciplined unit economics, energy cost management strategies, and crop selection focused on high-value produce categories where premium pricing justifies the elevated production cost structure of controlled-environment agriculture. The market was valued at approximately USD 7.2 billion in 2025 and is projected to expand at a compound annual growth rate of 23.1% through 2034, as the industry works through its consolidation phase and emerges with a more commercially sustainable operating model built on lower-cost LED lighting, renewable energy integration, advanced automation reducing labor intensity, and strategically located proximity to urban consumer markets where supply chain freshness advantages and food safety differentiation can support premium price positioning.

Leafy greens and fresh herbs represent the dominant crop category within the global vertical farming market, reflecting the combination of high crop turnover cycles that maximize facility utilization and revenue generation per square meter, strong consumer willingness to pay a freshness and food safety premium for locally produced salad greens and culinary herbs, and the well-established cultivation protocols and yield predictability that make leafy green production the most operationally mature application for vertical farming technology. The expansion of vertical farming into higher-value specialty crops including microgreens, edible flowers, medicinal and pharmaceutical herbs, and premium soft fruit varieties is creating new revenue diversification opportunities for operators capable of developing the cultivation expertise and premium market channel relationships that specialty crop economics require. Strawberry vertical farming is attracting significant research and early commercial investment as a high-value crop category whose year-round availability premium, extended shelf life relative to field-grown product, and reduced pesticide requirements align favorably with the controlled-environment production advantages of indoor vertical cultivation systems.

The economics of vertical farming are being structurally improved by the rapid advancement of LED lighting technology, where the progression from broad-spectrum white LEDs to precisely tuned multi-channel light recipes delivering optimal photosynthetic efficiency per watt of electricity consumed is reducing lighting energy costs per kilogram of produce harvested by substantial margins relative to the first-generation full-spectrum LED systems deployed in early vertical farming facilities. Renewable energy integration through dedicated solar photovoltaic and wind power procurement agreements, combined with intelligent load scheduling that shifts energy-intensive lighting and climate control demand toward periods of low electricity tariff or renewable energy surplus, is enabling progressive vertical farm operators to materially reduce the electricity cost exposure that has been the primary driver of operating losses at many earlier-generation vertical farm businesses. Robotics, computer vision-guided harvesting systems, autonomous transplanting and seeding equipment, and AI-powered crop health monitoring platforms are advancing the labor productivity and operational consistency of vertical farm operations toward economic parameters that make high-volume leafy green production commercially viable without the premium pricing premiums that early market entrants required to cover elevated operating cost structures.

Asia-Pacific dominates the global vertical farming market by facility count and investment volume, anchored by Japan’s mature plant factory industry with its deep technical expertise in controlled-environment agriculture, the rapid expansion of vertical farming in China driven by food security policy imperatives and urban population density, South Korea’s technology-forward indoor farming ecosystem, and Singapore’s strategic vertical farming investment as a core component of its thirty-by-thirty food security plan targeting domestic production of thirty percent of national nutritional needs by 2030. North America represents the largest market by revenue, supported by the concentration of venture-backed large-scale vertical farming operators, strong consumer demand for locally grown premium produce in major metropolitan markets, and extensive retail and food service chain partnerships providing offtake scale and supply chain integration. Europe represents the third major regional market, driven by consumer sustainability preferences, stringent food safety and pesticide residue regulations, and the growing commercial viability of vertical farming in high-electricity-cost environments through accelerating renewable energy integration and LED efficiency advancement.

Key Drivers

Food Security Imperatives, Arable Land Scarcity, and Climate Change Impact on Traditional Agriculture Compelling Investment in Controlled-Environment Farming Infrastructure Independent of Weather and Geography

The convergence of global population growth, accelerating loss of arable land to urbanization, soil degradation, and desertification, and the growing disruption of traditional outdoor agricultural production systems by climate change-driven weather extremes, drought intensification, and shifting growing season patterns is compelling governments, food corporations, and institutional investors to direct capital toward controlled-environment agriculture infrastructure that decouples food production from land availability, climate variability, and supply chain geography constraints. Vertical farming facilities producing leafy greens, herbs, and specialty vegetables within urban population centers eliminate the cold chain distance, post-harvest degradation, and climate vulnerability that characterize field agriculture supply chains, delivering measurable advantages in produce freshness, shelf life, food safety, and supply consistency that increasingly resonate with urban consumers, food retail buyers, and food service operators.

Rapid LED Lighting Efficiency Advancement and Renewable Energy Cost Reduction Progressively Improving Vertical Farm Operating Economics Toward Commercially Sustainable Unit Cost Structures

Continuous advances in LED lighting efficiency, spectral tuning precision, and fixture photon delivery optimization are reducing the electricity consumption required per unit of crop biomass produced in vertical farm facilities at a pace that is materially improving the operating cost economics of indoor farming relative to the first commercial generation of vertical farm businesses whose operating losses were primarily attributable to electricity costs representing fifty to seventy percent of total cash operating expenditure. The parallel reduction in solar photovoltaic and wind power generation costs and the growing availability of favorable direct renewable power purchase agreement structures are enabling vertical farm operators in markets with sufficient renewable capacity to substantially reduce their exposure to grid electricity price volatility, improving operating cost predictability and reducing the hedging premium that energy uncertainty previously imposed on vertical farm business plan assumptions.

Urban Population Growth and Proximity-to-Consumer Demand for Locally Grown Fresh Produce Establishing a Durable Premium Market Channel for Vertically Farmed Crops in Major Metropolitan Markets

The concentration of global population in large urban agglomerations increasingly distant from productive agricultural land is driving consumer and institutional food buyer demand for locally grown fresh produce that offers verifiable provenance, reduced transportation food miles, minimal pesticide and herbicide residue content, and superior freshness characteristics relative to long-distance supply chain alternatives. Major food retail chains, premium restaurant groups, hotel operators, and corporate catering organizations in North American, European, and Asian metropolitan markets are actively seeking reliable local produce supply partnerships with vertical farm operators capable of delivering consistent year-round supply of certified pesticide-free leafy greens, herbs, and specialty vegetables at volumes and quality specifications that conventional regional agriculture cannot reliably maintain across all seasons.

Key Challenges

High Capital Expenditure and Operating Cost Structure of Vertical Farm Facilities Creating Challenging Unit Economics That Have Driven Multiple High-Profile Operator Insolvencies and Industry Consolidation

The capital intensity of constructing purpose-built or retrofitted vertical farm facilities encompassing multilevel growing infrastructure, LED lighting systems, hydroponic or aeroponic cultivation equipment, climate control systems, automation and robotics hardware, and building mechanical systems creates per-square-meter construction costs substantially exceeding conventional greenhouse or field agriculture infrastructure, requiring either premium crop pricing, very high facility utilization rates, or both to achieve positive operating cash flow and eventual return on invested capital. The concurrent challenges of high electricity costs, significant labor requirements per unit of production at most current automation levels, and the difficulty of scaling operations while maintaining crop quality consistency have created persistent unit economics pressure that has proven too severe for several well-funded vertical farming operators whose operating losses exceeded available investor capital reserves.

Electricity Cost Exposure and Grid Energy Reliability Dependence Creating Fundamental Operating Vulnerability for Energy-Intensive Vertical Farm Operations Without Renewable Power Integration

Vertical farm facilities operating with conventional grid electricity supply face electricity cost exposure representing the largest single operating expenditure category, creating structural operating loss risk during periods of elevated electricity tariff levels that erodes margins on produce sales and reduces the financial buffer available to absorb other operating challenges including crop failures, equipment breakdowns, and market pricing volatility. The dependence of vertical farm crop production on continuous artificial lighting and climate control systems means that grid power outages or supply interruptions can cause significant crop losses that compound the financial impact of electricity cost volatility with direct production asset value destruction, making grid reliability and backup power infrastructure critical operational requirements that add further capital and operating cost burden to vertical farm facility investment and operating economics.

Consumer Price Sensitivity and Limited Willingness to Pay Sustained Produce Premiums Constraining Revenue Generation Potential and Market Scaling Pace for Vertically Farmed Crop Producers

The premium pricing required to cover the elevated operating cost structure of vertical farm produce relative to field-grown and conventional greenhouse alternatives creates a consumer price sensitivity constraint that limits the addressable market for vertically farmed products to premium consumer segments, high-end food service channels, and institutional buyers with specific food safety or sustainability procurement mandates willing to pay the price differential required for vertical farm supply. Economic softening, consumer trade-down behavior during inflationary periods, and the expansion of competitive premium produce alternatives including certified organic field-grown and conventional greenhouse hydroponic products are exerting downward pressure on the price premiums achievable for vertically farmed leafy greens and herbs in established markets, compressing the margin contribution available to service the high fixed cost base of large-scale vertical farm facility operations.

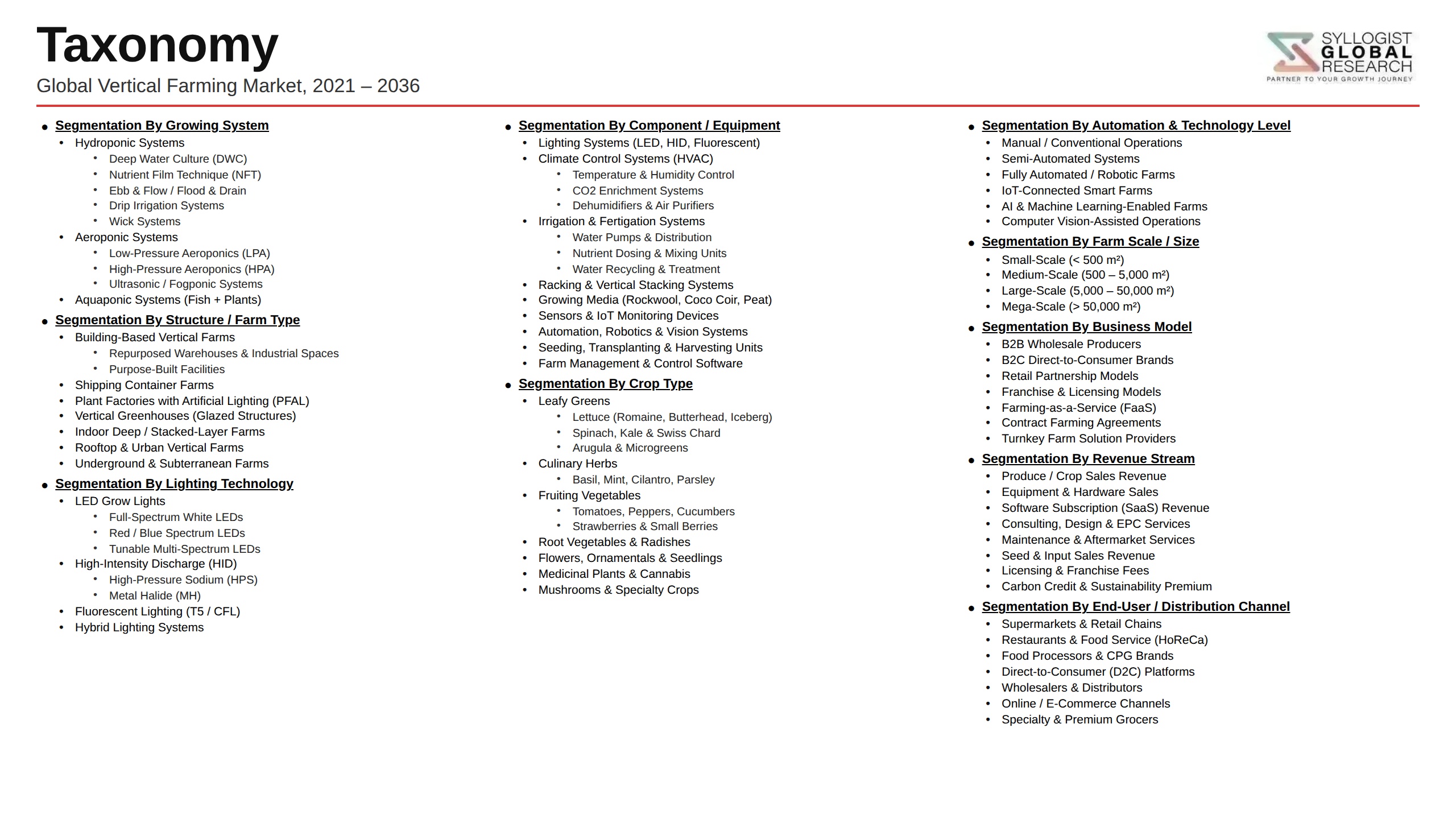

Market Segmentation

- Segmentation By Growing System

- Hydroponic Vertical Farming Systems

- Aeroponic Vertical Farming Systems

- Aquaponic Integrated Systems

- Soil-Based Vertical Growing Systems

- Others

- Segmentation By Crop Type

- Leafy Greens and Salad Crops

- Herbs and Culinary Plants

- Microgreens and Sprouts

- Soft Fruits (Strawberries, Tomatoes, Peppers)

- Pharmaceutical and Nutraceutical Crops

- Flowers and Ornamental Plants

- Others

- Segmentation By Lighting Type

- LED Lighting Systems

- Fluorescent and High-Intensity Discharge Lighting

- Hybrid Natural and Artificial Lighting

- Others

- Segmentation By Structure Type

- Purpose-Built Vertical Farm Facilities

- Repurposed Warehouse and Industrial Building Conversions

- Container and Modular Vertical Farms

- Building-Integrated and Rooftop Farming Systems

- Shipping Container Farms

- Others

- Segmentation By Component

- LED Lighting and Lighting Control Systems

- Hydroponic and Nutrient Delivery Systems

- Climate Control and HVAC Systems

- Sensors, Monitoring, and AI Management Platforms

- Robotics and Automated Harvesting Equipment

- Growing Trays, Racks, and Structural Systems

- Others

- Segmentation By End User

- Commercial Vertical Farm Operators

- Food Retail Chains and Supermarkets

- Food Service and Restaurant Groups

- Healthcare and Institutional Catering

- Pharmaceutical and Nutraceutical Companies

- Research Institutions and Universities

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global vertical farming market valuation in 2025, projected through 2034, segmented by growing system, crop type, and structure type, enabling facility operators, technology suppliers, food retail buyers, and infrastructure investors to identify the highest-growth crop and technology categories and most commercially viable market entry opportunities across the global vertical farming landscape?

- How are LED lighting efficiency advances, spectral tuning optimization, renewable energy procurement strategies, and facility energy management system improvements collectively reducing the electricity cost per kilogram of produce harvested in modern vertical farm operations, and what cost reduction milestones must be achieved for leafy green vertical farm production economics to become commercially viable without sustained premium price positioning?

- Which crop categories beyond leafy greens and herbs, specifically strawberries, tomatoes, pharmaceutical botanical crops, and microgreens, offer the most compelling unit economics for vertical farm expansion, and what cultivation protocol maturity, yield consistency, consumer market development, and price premium sustainability factors are determining the commercial viability of higher-value crop diversification strategies for vertical farm operators?

- How is the competitive landscape evolving following the insolvency and consolidation of several high-profile vertical farming operators, and what business model characteristics, facility scale decisions, crop portfolio strategies, retail and food service channel partnerships, and energy cost management approaches are distinguishing commercially sustainable vertical farm operators from those that failed to achieve viable unit economics?

- What role are government food security policies, urban agriculture investment programs, and agricultural innovation funding frameworks in Japan, Singapore, South Korea, the United Arab Emirates, and European Union member states playing in accelerating vertical farming technology development, facility construction investment, and market demand creation through public procurement, research funding, and regulatory frameworks supporting controlled-environment agriculture expansion?

- How are robotics, computer vision harvesting systems, AI-powered crop health monitoring, and autonomous transplanting and seeding equipment advancing labor productivity in vertical farm operations, and what automation investment levels and productivity improvement milestones are required to reduce the labor cost component of vertical farm operating expenditure to levels that support commercially viable production economics without premium crop pricing dependency?

- Which regional vertical farming markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the highest incremental facility investment and technology procurement growth through 2034, and what combinations of food security policy urgency, urban consumer premium produce demand, renewable energy cost competitiveness, and controlled-environment agriculture technology ecosystem maturity are defining regional market growth trajectories and investment attractiveness?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- High Energy Consumption, Electricity Cost Escalation & Profitability Risk

- Capital Intensity, Project Finance Availability & Investor Return Uncertainty Risk

- Crop Disease, Pest Outbreak & Contamination Risk in Controlled Environment

- Competition from Conventional Agriculture, Greenhouse & Field-Grown Produce on Price Risk

- Skilled Labour Scarcity, Automation Integration & Operational Complexity Risk

- Technology Obsolescence, Rapid Innovation Cycle & Platform Switching Cost Risk

- Regulatory Framework & Standards

- Food Safety Standards for Controlled Environment Agriculture (CEA): FDA FSMA, GFSI, GLOBALG.A.P. & Retailer Certification

- Organic Certification, Hydroponic & Soilless Produce Labelling Standards: USDA NOP, EU Organic Regulation & National Frameworks

- Building Code, Structural Safety, Fire Suppression & Electrical Standards for Indoor & Vertical Farm Facilities

- Water Use, Nutrient Discharge & Effluent Treatment Regulations for Vertical Farm Operations

- LED Lighting Energy Efficiency, Phytosanitary & Plant Health Import/Export Regulatory Standards

- Government Subsidy, Grant Programmes & Urban Agriculture Policy Frameworks Supporting Vertical Farming

- Global Vertical Farming Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Tonnes of Produce & Square Metres of Growing Area)

- Market Size & Forecast by Growing System

- Hydroponics (Nutrient Film Technique, Deep Water Culture & Drip Systems)

- Aeroponics

- Aquaponics

- Substrate-Based & Growing Media Systems

- Hybrid & Multi-System Growing Platforms

- Market Size & Forecast by Structure Type

- Building-Based Vertical Farms (Warehouses, Converted Industrial & Dedicated High-Rise)

- Shipping Container & Modular Vertical Farms

- Rooftop & Building-Integrated Vertical Farms

- Underground & Basement Vertical Farms

- Greenhouse-Integrated Vertical Farming Systems

- Market Size & Forecast by Component & Technology

- LED Grow Lighting Systems

- Climate Control, HVAC & Environmental Control Systems

- Hydroponic Growing Racks, Towers & Vertical Growing Structures

- Nutrient Delivery, Fertigation & Water Management Systems

- Sensors, IoT & Environmental Monitoring Systems

- Farm Management Software, AI Analytics & Automation Platforms

- Harvesting, Packaging & Post-Harvest Handling Equipment

- Renewable Energy Integration & Energy Management Systems

- Market Size & Forecast by Crop Type

- Leafy Greens & Salad Crops (Lettuce, Spinach, Kale & Arugula)

- Herbs & Microgreens (Basil, Coriander, Mint & Specialty Herbs)

- Fruits & Fruiting Vegetables (Tomatoes, Strawberries, Peppers & Cucumbers)

- Root Vegetables & Tubers

- Cannabis & Medicinal Plants

- Flowers, Ornamentals & Non-Food Crops

- Algae, Microalgae & Novel Protein Crops

- Market Size & Forecast by Farm Scale

- Small-Scale & Micro Vertical Farms (Below 1,000 m2 Growing Area)

- Medium-Scale Commercial Vertical Farms (1,000 to 10,000 m2)

- Large-Scale & Industrial Vertical Farms (Above 10,000 m2)

- Market Size & Forecast by Application

- Fresh Produce Supply for Retail & Grocery Chains

- Food Service, Restaurant & Hospitality Supply

- Pharmaceutical, Nutraceutical & Functional Food Ingredient Production

- Research, Seed Development & Plant Science Applications

- Military, Space & Remote Location Food Security Applications

- Market Size & Forecast by End-User

- Commercial Vertical Farm Operators & Agri-Tech Companies

- Retail Grocery Chains & Food Retailers

- Food Service & Restaurant Groups

- Pharmaceutical & Life Sciences Companies

- Government, Defence & Space Agencies

- Research Institutions & Universities

- Market Size & Forecast by Sales Channel

- Direct Technology & Equipment OEM Sales

- Turnkey Farm System Integrator & EPC Channel

- Farming-as-a-Service (FaaS) & Managed Operations Channel

- Direct-to-Consumer & Subscription Box Channel

- Retail & Wholesale Produce Distribution Channel

- North America Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Vertical Farming Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Tonnes of Produce & Square Metres of Growing Area)

- By Growing System

- By Structure Type

- By Component & Technology

- By Crop Type

- By Farm Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Sweden, Denmark, Norway, Japan, China, South Korea, Singapore, Australia, India, UAE, Saudi Arabia, Qatar, Israel, Brazil, Chile, South Africa, Kenya

- Technology Landscape & Innovation Analysis

- LED Grow Lighting Technology Deep-Dive: Spectral Tuning, Far-Red Photoperiod, PPFD Optimisation & Energy Efficiency Advances

- AI, Machine Learning & Computer Vision Technology for Crop Monitoring, Growth Prediction & Yield Optimisation

- Robotics & Automation Technology: Seeding, Transplanting, Harvesting & Packaging Automation in Vertical Farms

- Aeroponic & High-Pressure Nutrient Mist Technology: Root Zone Oxygenation, Water Use Efficiency & Crop Performance

- Renewable Energy Integration: Solar PV, Waste Heat Recovery & Battery Storage for Energy-Neutral Vertical Farm Operations

- Microbiome, Biostimulant & Plant Bioscience Technology for Yield Enhancement in Controlled Environment Agriculture

- Digital Twin & Predictive Analytics Technology for Virtual Farm Modelling, Scenario Testing & Resource Optimisation

- Patent & IP Landscape in Vertical Farming Technologies

- Value Chain & Supply Chain Analysis

- LED Chip, Driver, Fixture & Grow Light Manufacturing Supply Chain

- Growing Rack, Tower, Tray & Hydroponic Structure Manufacturing Supply Chain

- Nutrient Solution, Fertiliser, Growing Media & Substrate Supply Chain

- HVAC, Climate Control, CO2 Enrichment & Dehumidification Equipment Supply Chain

- Seed, Propagation Material & Germplasm Supply Chain for Vertical Farm Crops

- Farm Management Software, IoT Platform & Automation System Supply Chain

- Turnkey System Integrator, Farm Designer & EPC Channel

- Cold Chain Logistics, Retail Distribution & Direct-to-Consumer Delivery Channel

- Pricing Analysis

- Vertical Farm Capital Cost (Capex) Analysis by Structure Type, Growing System & Farm Scale

- Vertical Farm Operating Cost (Opex) Analysis: Energy, Labour, Nutrients, Seeds & Maintenance Cost Structure

- Cost per kg of Produce Analysis: Vertical Farm vs. Greenhouse vs. Conventional Agriculture Comparison

- LED Grow Light System Price Trend Analysis: Impact of Efficacy Advances & Volume Scale on Lighting Cost

- Vertical Farm Produce Retail Price Premium Analysis: Positioning vs. Conventional & Organic Competitors

- Farming-as-a-Service (FaaS) & Managed Operations Pricing Model & Unit Economics Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Vertical Farming: Carbon Footprint, Water Use, Land Use & Energy Intensity vs. Conventional Farming

- Water Efficiency: Closed-Loop Hydroponic Recirculation, Water Savings vs. Field Agriculture & Nutrient Runoff Elimination

- Pesticide-Free Production, Food Safety & Reduction of Chemical Inputs in Vertical Farm Operations

- Food Miles Reduction, Urban Food Security & Local Supply Chain Resilience Contribution of Vertical Farming

- SDG 2 (Zero Hunger), SDG 12 (Responsible Consumption) & SDG 15 (Life on Land) Alignment & Impact Reporting

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Growing System & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Growing System, Crop Type & Geography

- Player Classification

- Large-Scale Commercial Vertical Farm Operators & Produce Companies

- Vertical Farming Technology Platform & Turnkey System Providers

- Specialist LED Grow Lighting Manufacturers for Vertical Farming

- Hydroponic & Aeroponic Equipment & Component Suppliers

- Farm Management Software, AI Analytics & Automation Platform Providers

- Container & Modular Vertical Farm System Suppliers

- Competitive Analysis Frameworks

- Market Share Analysis by Growing System, Crop Type & Region

- Company Profile

- Company Overview & Headquarters

- Vertical Farming Products, Technology & Crop Portfolio

- Key Customer Relationships & Reference Farm Installations

- Farm Footprint, Growing Area & Production Capacity

- Revenue (Vertical Farming Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Farm Openings, Contract Wins, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Growing System, Crop Type, Farm Scale, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Farm Expansion, Operational Efficiency & Unit Economics Improvement Strategy

- Geographic Expansion & Urban Market Entry Strategy

- Customer, Retail Partner & End-User Engagement Strategy

- Partnership, M&A & Agri-Tech Ecosystem Strategy

- Sustainability, Energy Reduction & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)