Market Definition

The Global Military Robotics and Unmanned Combat Vehicles Market encompasses the design, engineering, development, integration, testing, and procurement of ground-based unmanned ground vehicles, unmanned aerial vehicles, unmanned maritime surface vessels, unmanned underwater vehicles, and modular robotic platform systems developed and deployed by defense ministries, armed forces, and national security agencies for combat, intelligence, surveillance and reconnaissance, explosive ordnance disposal, logistics resupply, force protection, border security, and lethal precision strike missions across all operational environments and warfare domains. A military robotic or unmanned combat vehicle is a remotely operated, semi-autonomous, or fully autonomous platform engineered to perform defined tactical and operational missions in contested environments without requiring the continuous physical presence of a human operator within the vehicle or system, integrating propulsion and mobility systems, mission-specific payload modules, communications and datalink architectures, sensor suites incorporating electro-optical, infrared, synthetic aperture radar, and signals intelligence capabilities, and varying levels of machine autonomy enabled by embedded artificial intelligence and computer vision algorithms. The market encompasses the complete system value chain, including the primary unmanned platform vehicle or airframe, propulsion and power management systems, mission payload integration including weapons systems and sensor packages, ground control stations and operator interface hardware, communications relay and network integration infrastructure, battle management system software, and logistics and sustainment services that constitute the operational lifecycle cost of a deployed unmanned combat system. Key participants include defense prime contractors, specialist robotics and autonomous systems developers, defense electronics and sensor system suppliers, software and artificial intelligence platform developers, national defense procurement agencies, and allied nation interoperability standardization bodies whose operational requirements and certification standards define the fundamental engineering and performance parameters governing unmanned combat vehicle design globally.

Market Insights

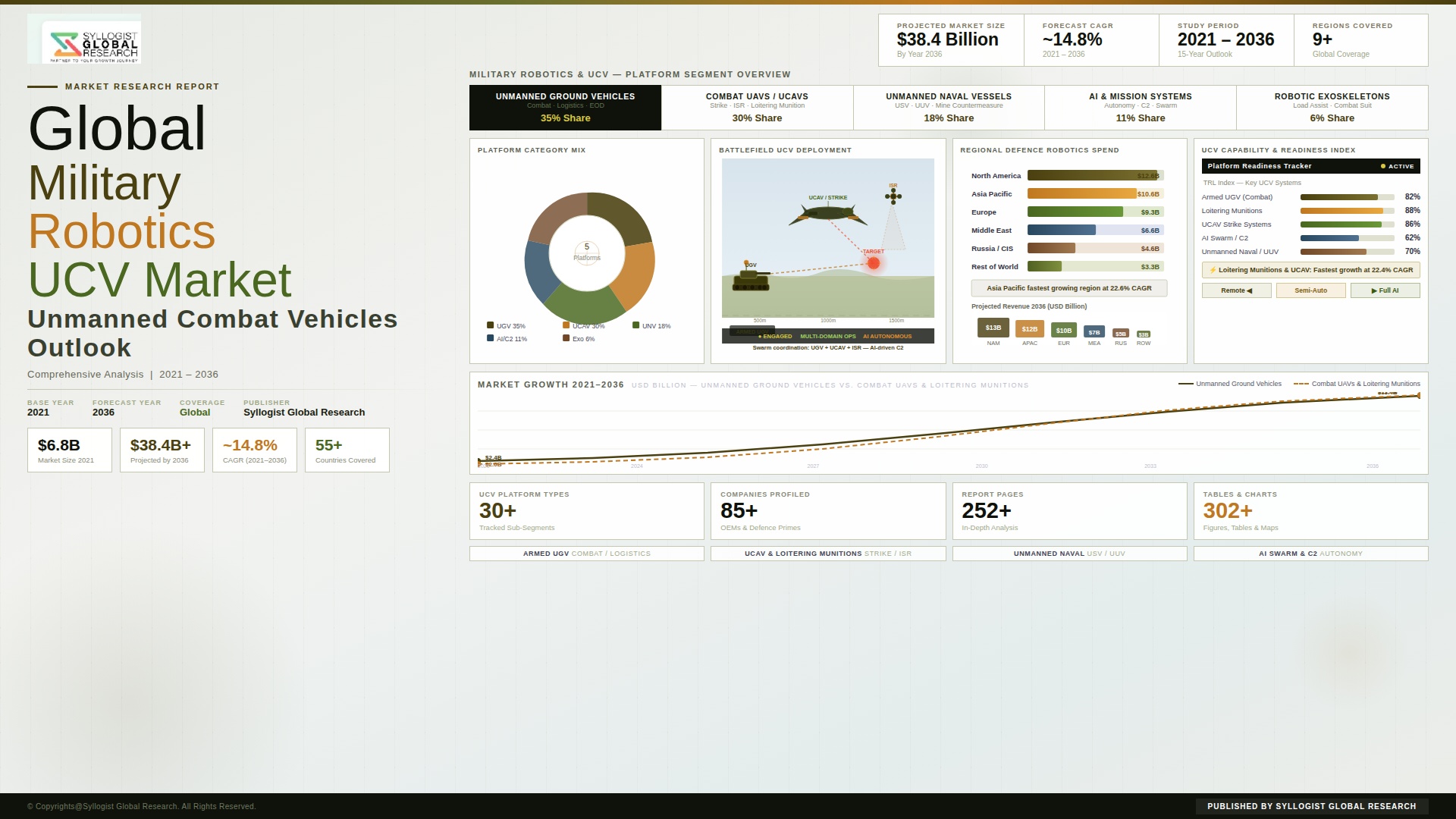

The global military robotics and unmanned combat vehicles market is experiencing a period of accelerated structural expansion driven by the convergence of escalating geopolitical tensions across multiple theaters, the demonstrated operational effectiveness of unmanned systems in recent high-intensity conflict environments, and a broad-based shift in defense procurement doctrine toward force multiplication through autonomous and remotely operated platforms that reduce soldier exposure to lethal threat environments while simultaneously expanding the persistent surveillance and precision strike capacity available to operational commanders. The global military robotics and unmanned combat vehicles market was valued at approximately USD 21.7 billion in 2025 and is projected to reach USD 45.3 billion by 2034, advancing at a compound annual growth rate of 8.6% over the forecast period from 2027 to 2034, as major defense powers accelerate autonomous systems investment in response to the strategic lessons of recent conflicts and as commercially derived artificial intelligence and sensor miniaturization technologies dramatically reduce the unit cost and development timeline of operationally capable unmanned platforms across all mobility domains. The depth and breadth of procurement programs across NATO member states, Indo-Pacific treaty allies, and major non-aligned defense spenders collectively underpin a demand trajectory whose durability is structurally anchored in multi-year defense budget commitments and long-cycle platform acquisition programs rather than in volatile year-to-year discretionary spending patterns.

The technology landscape of military robotics is undergoing a fundamental transition from remote-controlled platforms dependent on continuous human operator input toward increasingly autonomous systems capable of executing defined mission sets with minimal real-time human intervention, enabled by the integration of advanced machine learning algorithms, computer vision, sensor fusion architectures, and onboard edge computing capabilities that allow unmanned platforms to perceive, interpret, and respond to dynamic battlefield environments with reaction speeds and operational persistence that exceed human physiological limits. Unmanned aerial vehicles continue to represent the largest platform segment by both unit volume and revenue, accounting for approximately 54% of total market revenue in 2025, with tactical reconnaissance and strike-enabled loitering munition systems experiencing the most rapid procurement growth as their demonstrated cost-effectiveness relative to manned strike aircraft platforms has generated substantial reallocation of tactical aviation budgets toward unmanned strike capacity across multiple national defense establishments. Unmanned ground vehicles are the fastest-growing mobility segment at a projected compound annual growth rate of 11.2% through 2034, driven by increasing procurement of wheeled and tracked logistics carrier, explosive ordnance disposal, and direct-fire-capable robotic combat vehicle platforms as defense establishments pursue the doctrinal transition toward optionally manned or fully autonomous ground combat formations that reduce infantry casualty exposure in high-intensity urban and contested terrain environments.

From a regional standpoint, North America constitutes the largest and most technologically advanced regional market for military robotics and unmanned combat vehicles, driven by sustained United States Department of Defense investment in autonomous systems across all service branches, with the Army Robotic Combat Vehicle program, the Navy and Marine Corps unmanned surface and underwater vehicle acquisition strategies, and the Air Force collaborative combat aircraft initiative collectively representing a generational transformation of United States military force structure toward human-machine teaming architectures that embed autonomous platforms as integral components of combined arms formations rather than as supplementary reconnaissance or support tools. Asia-Pacific represents the fastest-growing regional procurement market, driven by the acceleration of Chinese People Liberation Army unmanned systems capability development as a central pillar of military modernization, substantial Indian defense autonomous systems procurement expansion under indigenization mandates, South Korean and Japanese unmanned platform investment in response to regional security environment deterioration, and the broader Indo-Pacific arms dynamics generating increased unmanned systems procurement across Southeast Asian defense establishments. Europe has experienced a step-change acceleration in military robotics investment following the geopolitical recalibration of continental defense priorities, with multiple European Union member states and United Kingdom defense programs accelerating unmanned ground vehicle, loitering munition, and maritime drone procurement to levels substantially above pre-2022 planning baselines.

The integration of artificial intelligence and machine autonomy into military unmanned platforms is generating both the most transformative capability advancements and the most complex operational, legal, and ethical governance challenges in the history of defense systems acquisition, as defense establishments navigate the tension between the operational imperative to deploy AI-enabled autonomous weapons systems capable of engaging time-critical targets without human confirmation and the international humanitarian law obligations, strategic stability considerations, and domestic political constraints that continue to require meaningful human control over lethal force application decisions, producing a complex and jurisdiction-specific regulatory environment in which the permissible autonomy level of deployed systems varies materially across national defense establishments and alliance frameworks. The emergence of swarm-capable unmanned systems, in which large numbers of individually simple autonomous platforms coordinate collective behavior through distributed artificial intelligence algorithms to overwhelm adversary air defense, electronic warfare, and counter-drone systems, represents the most disruptive near-term capability trajectory in the market, with both the United States and Chinese defense establishments having demonstrated operational swarm capability with platforms numbering in the hundreds, and several allied and partner nation programs targeting deployable swarm systems exceeding 1,000 coordinated platforms within the forecast period, creating a structurally new demand category for swarm-specific platform design, communication mesh networking, and human supervision interface technology.

Key Drivers

Escalating Geopolitical Tensions and Defense Budget Expansion Across Major Military Powers Accelerating Autonomous Systems Procurement

The sustained deterioration of the global strategic security environment across multiple geographic theaters, including the prolonged high-intensity conflict in Eastern Europe, the intensifying military competition in the Indo-Pacific, persistent instability across the Middle East and sub-Saharan Africa, and the accelerating strategic rivalry between established and revisionist major powers, is generating a durable and structurally reinforced expansion in defense expenditure across NATO member states, Indo-Pacific allies, and non-aligned defense spenders that is disproportionately directed toward unmanned and autonomous systems as the capability investment category offering the most asymmetric improvement in operational effectiveness per unit of procurement expenditure. Global defense spending exceeded USD 2.4 trillion in 2025, with the majority of major defense powers operating under multi-year budget growth commitments that provide defense contractors and autonomous systems developers with the long-duration procurement visibility needed to justify the capital-intensive engineering development investment required to bring advanced unmanned combat platform programs to production maturity. The operational experience derived from recent conflicts has provided defense establishments with unprecedented real-world validation data demonstrating the tactical utility, cost-effectiveness relative to manned platforms, and force multiplication effects of deployed unmanned systems across reconnaissance, strike, logistics, and electronic warfare mission categories, generating a procurement urgency that is compressing traditional multi-decade defense acquisition cycles and accelerating fielding timelines for autonomous systems across both established and emerging defense market customers.

Advances in Artificial Intelligence, Edge Computing, and Sensor Miniaturization Enabling Operational Capability Breakthroughs in Autonomous Military Platforms

The rapid maturation and cost reduction of commercially derived artificial intelligence inference hardware, computer vision algorithms, inertial navigation and simultaneous localization and mapping technology, solid-state lidar and radar sensor systems, and high-bandwidth low-latency communications technologies are enabling the development of military unmanned platforms with operational autonomous capability that was technically infeasible or prohibitively expensive within defense-exclusive research and development budgets a decade ago, allowing defense programs to leverage the enormous commercial investment in autonomous vehicle, robotics, and AI infrastructure to achieve military-grade autonomous navigation, target recognition, and mission execution capability at unit platform costs that are increasingly accessible to mid-tier defense budgets as well as to leading military powers. The transition from cloud-dependent artificial intelligence architectures toward embedded edge computing solutions capable of executing complex inference workloads onboard unmanned platforms without reliance on continuous high-bandwidth communications links is particularly operationally significant, as edge-capable autonomous systems can maintain mission execution capacity in communications-degraded or electronically contested environments where adversary jamming and electronic warfare systems are specifically designed to deny the communications connectivity on which remotely operated platforms depend. Military-specific artificial intelligence capability development is additionally being accelerated by the formation of dedicated defense AI development organizations within major military establishments, with United States, United Kingdom, Australian, and other allied defense establishments institutionalizing AI development pipeline infrastructure that systematically converts commercial foundation model and computer vision research output into deployable military autonomous systems capability within compressed integration timelines.

Operational Imperative to Reduce Military Personnel Casualty Exposure in High-Intensity Conflict Environments Driving Doctrine Transformation Toward Human-Machine Teaming

The fundamental strategic driver underlying sustained global investment in military robotics and unmanned combat vehicles is the enduring imperative of national defense establishments to accomplish operational objectives while minimizing the politically, socially, and operationally costly exposure of military personnel to lethal threat environments, with unmanned and autonomous systems offering the capability to conduct the highest-risk mission categories, including close reconnaissance of fortified adversary positions, explosive ordnance clearance operations, direct assault in urban terrain, and penetration of heavily defended airspace, without placing human operators within the lethal engagement envelope, thereby preserving human life while maintaining or expanding operational capability in threat environments where the casualty cost of manned operations would be strategically unsustainable. The doctrinal evolution toward human-machine teaming frameworks, in which autonomous unmanned platforms are integrated as organic elements of infantry, armor, aviation, and maritime formations rather than deployed as standalone specialist assets, is generating a structural and recurring demand for unmanned platform procurement that is embedded in force structure planning rather than dependent on discretionary program funding, providing defense contractors with durable demand visibility extending across full platform generation lifecycles of 15 to 25 years. The operational experience of integrating unmanned platforms into combined arms formations is additionally demonstrating cognitive load reduction benefits for human commanders, as autonomous systems absorb surveillance, perimeter security, and logistics resupply mission burdens that previously required human crew assignment, allowing military manpower to be concentrated on the higher-order decision-making, tactical judgment, and kinetic engagement functions that continue to require human judgment and authorization within current rules of engagement frameworks.

Key Challenges

Regulatory, Legal, and Ethical Governance Frameworks for Lethal Autonomous Weapons Systems Creating Compliance Uncertainty and Procurement Complexity

The deployment and operational use of military autonomous systems with the capability to select and engage targets without human confirmation occupies an increasingly contested legal, ethical, and international governance space in which the absence of binding international legal consensus on the permissible autonomy level of deployed lethal weapons systems creates fundamental programmatic uncertainty for defense developers and procurement agencies attempting to define the human control requirements, autonomous engagement authorization boundaries, and accountability frameworks that their systems must satisfy across current and future legal and operational environments. The Convention on Certain Conventional Weapons discussions on lethal autonomous weapons systems have failed to produce binding multilateral agreement on prohibition or restriction frameworks, leaving national defense establishments to develop their own autonomy governance policies in the absence of internationally harmonized standards, resulting in heterogeneous and potentially incompatible autonomy authorization frameworks across allied defense establishments that complicate interoperability, multinational operational deployment, and joint certification of autonomous systems operating under coalition rules of engagement. The risk that future international legal developments, domestic legislative constraints, or coalition operational policy changes could require costly retrofitting of autonomy restriction hardware and software into deployed platforms, or could restrict the operational employment of autonomous systems in ways that substantially reduce their tactical utility, represents a procurement risk factor that defense acquisition authorities must account for in platform design requirements, creating pressure toward architecturally flexible human-on-the-loop or human-in-the-loop system designs that preserve operational utility while accommodating potential future autonomy restriction requirements.

Cybersecurity Vulnerabilities, Electronic Warfare Susceptibility, and Adversarial AI Countermeasures Threatening the Operational Reliability of Deployed Autonomous Platforms

Military unmanned and autonomous systems represent high-value targets for adversary cyber intrusion, electronic warfare attack, and artificial intelligence countermeasure operations, with the communications links, navigation systems, sensor processing pipelines, and autonomous decision-making algorithms that constitute the operational capability of unmanned platforms presenting attack surfaces that sophisticated state-level adversaries are actively developing the technical capability to exploit through signal jamming, GPS denial, communications hijacking, sensor spoofing, and adversarial machine learning attacks that cause autonomous systems to misclassify targets, navigate to unintended locations, or execute unsafe behaviors that could result in fratricide, mission failure, or operational exploitation by opposing forces. The vulnerability of satellite-dependent global navigation satellite system positioning to electronic denial and spoofing in contested operational environments has been extensively demonstrated in recent conflict theaters, directly undermining the autonomous navigation capability of GPS-dependent unmanned platforms and creating a critical operational dependency that adversaries can exploit to deny or degrade unmanned system effectiveness precisely in the high-intensity conflict environments where their tactical utility is most needed. Securing autonomous military platforms against the full spectrum of cyber and electronic warfare attack vectors across their operational lifecycle requires sustained investment in cyber-resilient communications architectures, anti-jamming and anti-spoofing navigation technology, hardened autonomous decision-making systems resilient to adversarial input perturbation, and security certification frameworks capable of validating the cyber integrity of complex artificial intelligence systems, generating development cost and timeline pressures that are particularly acute for smaller defense contractors and partner nation procurement programs with constrained cybersecurity engineering resources.

High Development and Unit Procurement Costs, Long Certification Timelines, and Technology Obsolescence Cycles Constraining Scalable Deployment Across Defense Establishments

The development, qualification, and production of operationally capable military unmanned combat vehicles and robotic systems requires sustained engineering investment across multiple complex technology domains simultaneously, including platform structural design and materials engineering, propulsion system development, embedded autonomy software architecture, sensor and payload integration, communications system design, and military environmental qualification and safety certification, generating total program development costs that frequently exceed USD 500 million for advanced combat-capable unmanned ground vehicle or large unmanned aerial vehicle programs before production units are delivered to operational users, creating substantial financial barriers to entry for new defense program participants and compressing the number of defense contractors capable of competing at the prime system integration level for major autonomous systems acquisition programs. The rapid pace of artificial intelligence and sensor technology advancement is simultaneously creating platform obsolescence dynamics that are substantially faster than the traditional 20-to-30-year defense platform lifecycle, with autonomous systems fielded as recently as five years ago potentially lacking the computational architecture required to host current-generation artificial intelligence inference workloads, creating a technology refresh and upgrade investment requirement that defense acquisition budgets were not historically structured to accommodate at the frequency demanded by the current pace of commercial AI development. The unit procurement cost of advanced unmanned combat platforms, including combat-capable unmanned ground vehicles with direct-fire weapon integration priced at approximately USD 3.2 million per unit and large unmanned aerial vehicles with persistent intelligence, surveillance, and reconnaissance payload capacity priced at approximately USD 8.5 million per platform, while substantially lower than equivalent manned platform procurement costs, remains sufficiently high to limit the fleet size that mid-tier defense budgets can sustain at operational readiness levels, constraining the force multiplication benefits that large-scale unmanned platform deployment is theoretically capable of generating.

Market Segmentation

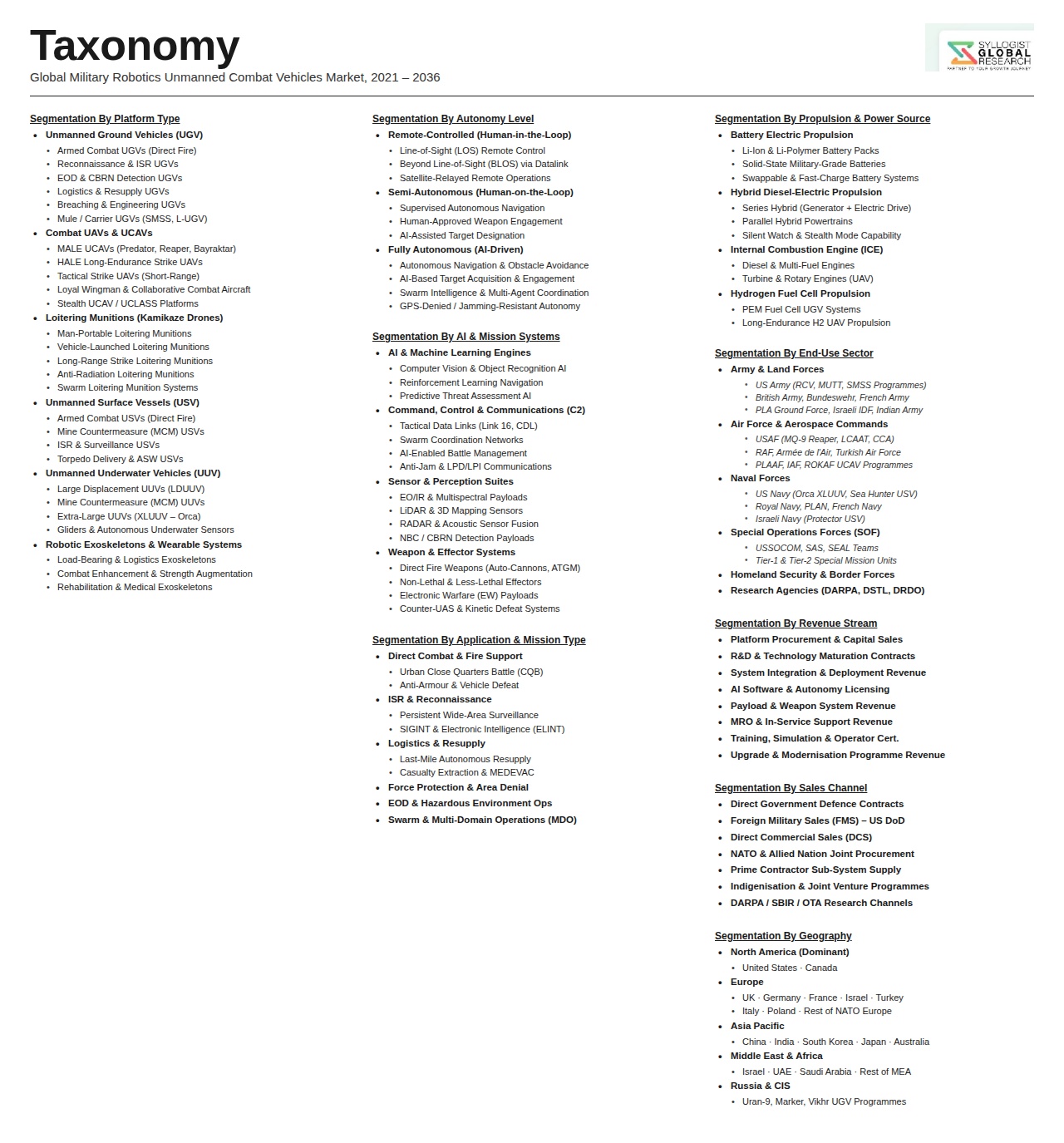

- Segmentation By Platform Type

- Unmanned Ground Vehicles (UGV)

- Unmanned Aerial Vehicles (UAV) and Loitering Munitions

- Unmanned Maritime Surface Vehicles (USV)

- Unmanned Underwater Vehicles (UUV)

- Unmanned Space and Orbital Platforms

- Others

- Segmentation By Mission Application

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Combat and Precision Strike

- Explosive Ordnance Disposal (EOD) and Mine Clearance

- Logistics and Resupply

- Electronic Warfare and Signals Intelligence

- Border Security and Perimeter Protection

- Search and Rescue in Hostile Environments

- Others

- Segmentation By Level of Autonomy

- Remote Controlled (Human-on-the-Loop)

- Semi-Autonomous (Human-in-the-Loop)

- Supervised Autonomous

- Fully Autonomous

- Swarm and Collaborative Multi-Agent Systems

- Segmentation By Propulsion Type

- Electric Battery-Powered Systems

- Diesel and Hybrid Propulsion Systems

- Turbine and Jet Engine-Powered Systems

- Fuel Cell and Hydrogen-Powered Systems

- Solar and Renewable Energy Hybrid Systems

- Others

- Segmentation By Operational Range

- Short Range (Below 50 km)

- Medium Range (50 km to 300 km)

- Long Range (300 km to 1,000 km)

- Extended Range and Persistent (Above 1,000 km)

- Segmentation By Payload and Weapon System

- Unarmed Sensor and Reconnaissance Payloads

- Directed Energy Weapons

- Anti-Tank Guided Missiles and Rocket Systems

- Machine Guns and Cannon-Armed Turrets

- Loitering Munition Warheads

- Electronic Warfare and Jamming Payloads

- Others

- Segmentation By End User

- Army and Land Forces

- Navy and Marine Corps

- Air Force and Aerospace Defense

- Special Operations Forces

- Homeland Security and Border Agencies

- Others

- Segmentation By Component

- Unmanned Platform Vehicle or Airframe

- Propulsion and Power Management Systems

- Ground Control Stations and Operator Interfaces

- Communication and Datalink Systems

- Sensor Suites (Electro-Optical, Infrared, Radar)

- Autonomy and AI Software

- Mission Payload and Weapons Integration

- Battle Management and C2 Software

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Military Robotics and Unmanned Combat Vehicles Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by platform type, unmanned ground vehicles, unmanned aerial vehicles, unmanned surface vessels, and unmanned underwater vehicles, and by mission application, including intelligence surveillance and reconnaissance, precision strike, explosive ordnance disposal, and logistics, to enable defense contractors, autonomous systems developers, defense procurement agencies, and strategic investors to identify which platform segment and mission application category will generate the highest absolute revenue and the most durable procurement growth trajectory across the forecast period?

- How is the integration of artificial intelligence, edge computing, and machine learning-enabled autonomy reshaping the technical requirements, operational capability thresholds, and per-unit system value of military unmanned platforms across all mobility domains, and which specific autonomy capability tiers, from supervised autonomous to swarm-coordinated multi-agent systems, are expected to account for the largest share of defense procurement expenditure and generate the most significant tactical and operational capability step-changes for the major military powers investing most heavily in autonomous systems programs through 2034?

- What is the projected market size, compound annual growth rate, and competitive landscape of the unmanned ground vehicle segment, encompassing logistics carrier, explosive ordnance disposal, direct-fire robotic combat vehicle, and autonomous reconnaissance platform sub-categories, through 2034, and which national defense programs, operational requirements frameworks, and technology development roadmaps are expected to generate the largest procurement volumes, at what per-platform system values, as land force establishments transition toward human-machine teaming force structure architectures across North America, Europe, and Asia-Pacific?

- How are evolving international governance discussions on lethal autonomous weapons systems, national autonomy authorization policies of leading military powers, and coalition interoperability requirements reshaping the human control architecture, autonomous engagement authorization boundaries, and operational employment constraints of military unmanned combat platforms, and what is the estimated programmatic cost and operational capability impact that compliance with anticipated future autonomy governance requirements will impose on defense developers and procurement agencies acquiring advanced autonomous systems across the forecast period?

- Who are the leading prime defense contractors, specialist autonomous systems developers, artificial intelligence platform integrators, and unmanned platform component suppliers currently defining the competitive landscape of the global military robotics and unmanned combat vehicles market, and what are their respective program portfolios across ground, air, maritime, and underwater domains, manufacturing and systems integration capacity expansion strategies, regional procurement positioning, technology development roadmaps for next-generation AI-enabled autonomous capability, and strategic responses to the accelerating pace of commercial AI technology translation into military autonomous systems applications?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Geopolitical Instability, Arms Control & Export Regulation Risk

- Cybersecurity, Electronic Warfare & Counter-UAS Vulnerability Risk

- Technology Maturity, System Integration & Interoperability Risk

- Ethical, Legal & International Humanitarian Law Compliance Risk

- Budget Volatility, Procurement Delays & Programme Cancellation Risk

- Regulatory Framework & Standards

- National Defence Procurement Frameworks & Unmanned Systems Acquisition Policy

- Export Control Regulations: ITAR, EAR & Wassenaar Arrangement Applicability to Military Robotics

- Rules of Engagement, Autonomous Weapons Policy & Lethal Autonomous Systems (LAWS) Governance

- Military Airspace Deconfliction, UAS Flight Standards & Certification Frameworks

- Cybersecurity, Data Security & Communications Encryption Standards for Unmanned Military Platforms

- Global Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Deployed & Orders Placed)

- Market Size & Forecast by Platform Type

- Unmanned Ground Vehicles (UGV): Combat, Logistics & Explosive Ordnance Disposal (EOD)

- Unmanned Aerial Vehicles (UAV): Tactical, MALE, HALE & Loitering Munitions

- Unmanned Underwater Vehicles (UUV): AUV & ROV for Mine Countermeasures & ISR

- Unmanned Surface Vessels (USV): Combat Patrol, Mine Warfare & Force Protection

- Unmanned Combat Aerial Vehicles (UCAV): Strike, Stealth & Wingman Platforms

- Multi-Domain Autonomous Systems & Collaborative Robotics Platforms

- Market Size & Forecast by Technology

- Artificial Intelligence (AI) & Machine Learning for Autonomous Decision-Making & Target Recognition

- Swarm Robotics & Collaborative Multi-Agent Control Technology

- Navigation, Positioning & GNSS-Denied Operation Technology

- Sensor Fusion: EO/IR, SAR, LiDAR, Radar & Acoustic Sensing Integration

- Communications, Datalink, Spectrum Management & Secure C2 Technology

- Propulsion: Electric, Hybrid & Fuel Cell Systems for Unmanned Platforms

- Stealth, Signature Management & Counter-Detection Technology

- Human-Machine Interface (HMI), Tele-Operation & Supervised Autonomy Technology

- Cyber Resilience, Electronic Warfare Protection & Anti-Jamming Technology

- Market Size & Forecast by Autonomy Level

- Remote-Controlled (RC) & Tele-Operated Systems

- Semi-Autonomous Systems with Human-on-the-Loop Control

- Fully Autonomous & AI-Governed Engagement Systems

- Market Size & Forecast by Application

- Intelligence, Surveillance, Reconnaissance & Target Acquisition (ISTAR)

- Direct Combat, Precision Strike & Fire Support

- Explosive Ordnance Disposal (EOD) & Counter-IED Operations

- Logistics, Resupply & Casualty Evacuation Support

- Border Security, Perimeter Defence & Force Protection

- Mine Countermeasures (MCM) & Underwater Domain Awareness

- Electronic Warfare, Cyber Operations & Signal Intelligence (SIGINT)

- Urban Warfare, Building Clearance & Close Combat Support

- Market Size & Forecast by End-User

- Army & Land Forces

- Air Force & Air Defence Commands

- Navy & Maritime Forces

- Special Operations Forces (SOF)

- National Security, Border & Homeland Defence Agencies

- Market Size & Forecast by Sales Channel

- Direct Government-to-Government (G2G) & Foreign Military Sales (FMS)

- Prime Defence Contractor & OEM Direct Supply

- System Integration, Technology Licensing & Co-Development Partnership

- Maintenance, Repair, Overhaul (MRO) & Through-Life Support Contract

- North America Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Military Robotics & Unmanned Combat Vehicles Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Orders Placed)

- By Platform Type

- By Technology

- By Autonomy Level

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Israel, Russia, China, Japan, India, South Korea, Australia, Turkey, Saudi Arabia, UAE, Brazil, Poland, Sweden, Italy, Norway

- Technology Landscape & Innovation Analysis

- Artificial Intelligence, Machine Learning & Autonomous Navigation Technology Deep-Dive

- Swarm Robotics, Multi-Agent Coordination & Collaborative Autonomy Platforms

- GNSS-Denied Navigation, LiDAR & Sensor Fusion Technology

- Directed Energy, Loitering Munitions & Precision Strike Payload Integration

- Propulsion: Electric, Hybrid & Fuel Cell Technology for Unmanned Military Platforms

- Human-Machine Teaming, Tele-Operation & Supervised Autonomy Interface Technology

- Cyber Resilience, Anti-Jamming, Spectrum Agility & Counter-UAS Technology

- Patent & IP Landscape in Military Robotics & Unmanned Combat Vehicle Technologies

- Value Chain & Supply Chain Analysis

- Airframe, Hull & Structural Component Manufacturing Supply Chain

- Propulsion, Power & Energy Storage Systems Supply Chain

- Sensors, EO/IR, Radar & Payload Systems Supply Chain

- AI Software, Autonomy Stack & Mission Management Systems Supply Chain

- Communications, Datalink & C2 Systems Supply Chain

- Prime Defence Contractor, System Integrator & OEM Landscape

- MRO, Upgrades & Through-Life Support Channel

- Pricing Analysis

- Tactical UGV (EOD & Combat) Unit Cost & Life-Cycle Cost Analysis

- Tactical & MALE UAV Platform Procurement & Operating Cost Analysis

- UCAV Strike Platform Development, Unit & Programme Cost Analysis

- UUV & USV Platform Unit Pricing & Mission Cost Analysis

- AI Autonomy Software, Licensing & Integration Cost Structure Analysis

- Total Programme Economics: Development, Procurement, Operations & Upgrade Cost Modelling

- Sustainability & Environmental Analysis

- Lifecycle Environmental Impact Assessment of Military Robotic Platforms: Energy, Emissions & Materials

- Transition to Electric & Hybrid Propulsion: Carbon Footprint Reduction in Unmanned Military Systems

- Conflict Zone Environmental Impact, Explosive Remnants of War & Post-Conflict Remediation Considerations

- Ethical Frameworks, International Humanitarian Law & Autonomous Weapons Environmental Considerations

- Defence Industry ESG Commitments, Sustainability Reporting & Green Procurement Policy Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Technology & Geography

- Player Classification

- Prime Defence Contractors with Integrated Robotics & UAS Divisions

- Specialist UGV & Ground Robotics Manufacturers

- UAV & UCAV Platform Developers

- UUV & USV Maritime Unmanned Systems Providers

- AI, Autonomy Software & Mission Management Platform Providers

- Sensor, Payload & EO/IR Systems Specialists

- Communications, C2 & Datalink Technology Providers

- Defence Technology Start-ups & Dual-Use Robotics Companies

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Military Robotics Products & Platform Portfolio

- Key Customer Relationships & Reference Programme Deliveries

- Manufacturing Footprint & Production Capacity

- Revenue (Military Robotics & UAS Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Programme Milestones, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Responsible Innovation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)