Market Definition

The Global Next-Generation Military Radar and Electronic Warfare Systems Market encompasses the research, development, manufacturing, integration, and operational deployment of advanced sensing, detection, tracking, and electromagnetic spectrum dominance technologies serving the defense and national security requirements of armed forces, government intelligence agencies, and allied military coalitions worldwide. Military radar systems within this market include active electronically scanned array (AESA) radars, passive electronically scanned array (PESA) radars, ground-based air defense radars, naval multifunction surveillance radars, airborne fire-control and early warning radars, over-the-horizon radars, counter-drone detection systems, and man-portable battlefield surveillance radars, each engineered to detect, classify, and track aerial, surface, subsonic, supersonic, and hypersonic threats across contested electromagnetic environments. The electronic warfare segment encompasses electronic attack systems designed to deny, degrade, and deceive adversary sensors and communications; electronic protection systems that safeguard friendly platforms and networks from hostile jamming and interception; and electronic support systems that conduct passive signals intelligence gathering, emitter location, and threat library construction. The convergence of radar and electronic warfare into integrated radio frequency systems is a defining architectural trend, with modern platforms increasingly combining sensing and jamming functions within unified apertures governed by software-defined waveform management. Key participants include prime defense contractors, government-owned defense research establishments, specialized radio frequency and semiconductor component suppliers, and defense ministries operating procurement programs across North America, Europe, Asia-Pacific, and the Middle East. The market is governed by classified and export-controlled technology frameworks, including International Traffic in Arms Regulations and Wassenaar Arrangement controls, which shape both competitive dynamics and international collaboration structures within the global defense electronics ecosystem.

Market Insights

The global next-generation military radar and electronic warfare systems market is undergoing the most consequential technological and structural transformation in its post-Cold War history, driven simultaneously by the resurgence of great-power competition, the proliferation of advanced anti-access and area-denial capabilities among peer and near-peer adversaries, and the maturation of disruptive enabling technologies, including gallium nitride semiconductors, artificial intelligence-enabled signal processing, and software-defined radio frequency architectures, that are fundamentally redefining what is achievable in radar sensitivity, waveform agility, and electronic attack precision. As of 2026, global defense spending has reached its highest sustained level since the early 1990s, with NATO member aggregate defense budgets exceeding USD 1.4 trillion and Asia-Pacific defense expenditures growing at approximately 6.1% annually, creating a demand environment of exceptional depth and durability for advanced radar and electronic warfare systems. The global market valuation for next-generation military radar and electronic warfare systems stood at approximately USD 31.4 billion in 2025 and is projected to reach USD 58.7 billion by 2034, expanding at a compound annual growth rate of 7.2% over the forecast period from 2027 to 2034, underpinned by parallel investment streams in platform-embedded systems, ground-based infrastructure, and rapidly growing expenditure on software upgrades and cognitive electronic warfare capabilities that extend the operational utility of deployed hardware across evolving threat environments.

A defining inflection point shaping the competitive and technological landscape of this market is the transition from mechanically scanned and first-generation electronically scanned array radar architectures to fully digital AESA systems built on gallium nitride transmit-receive module technology, which delivers order-of-magnitude improvements in power efficiency, bandwidth, and reliability relative to preceding gallium arsenide-based designs. Gallium nitride-based AESA radars now form the programmatic foundation of the most consequential current-generation fighter aircraft radar programs globally, including the AN/APG-82 and AN/APG-85 systems in the United States, the Captor-E ECRS Mk2 in Europe, and the J/APG-2 and KLJ-7A systems in the Asia-Pacific region, as well as a new generation of ship-based multifunction radars and ground-based long-range air defense sensors. Simultaneously, the integration of machine learning algorithms into radar signal processing chains is enabling real-time adaptive waveform selection, clutter suppression in highly contested spectral environments, and autonomous target classification at processing speeds and accuracy levels that exceed human operator performance by significant margins. The cognitive radar concept, in which the system continuously learns from its electromagnetic environment and autonomously reconfigures its transmission parameters to maximize information extraction while minimizing exploitable emission signatures, is transitioning from laboratory demonstration to operational program integration, with funded development efforts underway in the United States, United Kingdom, France, Israel, and China.

The electronic warfare segment is experiencing a particularly acute period of investment intensification, driven by the demonstrated effectiveness of adversary jamming, deception, and anti-radiation missile systems in recent and ongoing conflicts, which have exposed critical vulnerabilities in legacy platform self-protection suites and ground-based radar networks that were not designed to operate within the dense, dynamic electromagnetic threat environments now characterizing near-peer contested battlespaces. Airborne electronic attack capabilities, including next-generation standoff and escort jamming systems, are receiving substantial funded development attention from the United States, which awarded the Next Generation Jammer program at a contracted value exceeding USD 2.9 billion for full-rate production, and from European NATO members who are collectively investing in a new generation of pod-based and internally carried electronic attack systems compatible with Eurofighter Typhoon, Rafale, and F-35 platform integration. Ship-based electronic warfare systems, particularly those designed for simultaneous multi-threat engagement across the full radio frequency spectrum from high frequency through Ka-band, are being developed as sovereign capability programs by naval powers including the United States, United Kingdom, France, Japan, and India, driven by the threat posed by advanced anti-ship missile seekers employing frequency-hopping and multi-mode terminal guidance that defeat narrowband legacy jamming systems. The escalating sophistication of adversary integrated air defense systems, particularly the S-400, S-500, and HQ-9 family of ground-based air defense networks, is compelling offensive electronic warfare investment as a necessary precondition for credible air campaign planning across all major alliance structures.

From a regional demand standpoint, North America commands the largest single market share, with the United States Department of Defense allocating approximately USD 12.6 billion in fiscal year 2025 toward radar modernization, electronic warfare system development, and spectrum management capabilities across all military services and the intelligence community, reflecting the primacy of electromagnetic spectrum superiority in American military doctrine. Europe has transitioned from a decade of defense budget austerity to a period of accelerating investment, with Germany’s Zeitenwende defense spending commitment of 2% of GDP, Poland’s emergence as the largest European per-capita defense investor, and the United Kingdom’s additional USD 3.1 billion in defense electronics funding collectively generating a demand environment for advanced radar and electronic warfare systems that has not been witnessed on the continent since the Cold War’s closing decade. Asia-Pacific represents the fastest-growing regional market, with China’s defense electronics industrial base having achieved near-parity with Western capabilities in several radar and electronic warfare technology domains, India’s USD 1.8 billion investment in indigenous AESA radar development programs for its air and naval platforms, and Japan’s decision to double its defense budget as a share of GDP by 2027 creating a substantial new procurement market for advanced sensing and electronic warfare capabilities. The Middle East remains a strategically significant high-value market, with Saudi Arabia, the UAE, and Israel driving demand for advanced air defense radar systems, airborne electronic warfare suites, and counter-drone detection and defeat capabilities that reflect the region’s acute threat environment from ballistic missiles, cruise missiles, and low-observable unmanned systems.

Key Drivers

Escalating Great-Power Competition and the Proliferation of Advanced Anti-Access and Area-Denial Threat Systems

The primary structural driver of demand across the global military radar and electronic warfare market is the rapid and well-documented advancement of peer and near-peer adversary capabilities in contested electromagnetic environments, which has created an urgent and sustained modernization imperative for legacy sensing and self-protection systems fielded by Western and allied armed forces. The deployment of fifth-generation stealth aircraft, hypersonic glide vehicles, low-observable cruise missiles, and sophisticated integrated air defense networks by China and Russia has rendered a significant proportion of existing long-range surveillance radar infrastructure and airborne self-protection suites operationally inadequate against the threat sets they are now required to address. The United States National Defense Strategy, the NATO Defence Investment Pledge, and successive European national defense reviews have each identified electromagnetic spectrum dominance as a tier-one operational priority, translating policy designation into funded program commitments across fighter aircraft radar upgrades, shipborne multifunction radar replacements, ground-based long-range surveillance sensor modernization, and next-generation electronic attack capability development. The proliferation of advanced Russian-origin and Chinese-origin air defense systems to third-party states and non-state actors further amplifies and geographically extends the demand signal for electronic warfare capabilities that can credibly suppress or defeat these exported threat systems across a widening range of operational theaters and alliance commitment scenarios.

Gallium Nitride Semiconductor Maturation and the Software-Defined Radio Frequency Architecture Revolution

The commercial and defense-grade maturation of gallium nitride wide-bandgap semiconductor technology has delivered a foundational enabling capability that is driving a generational replacement cycle across virtually every category of military radar and electronic warfare transmitter hardware, with cascading effects on system range, sensitivity, bandwidth, power efficiency, and operational reliability that collectively justify platform-level recapitalization programs even where legacy systems retain residual operational utility. Gallium nitride transmit-receive modules achieve output power densities approximately five times greater than equivalent gallium arsenide designs at comparable junction temperatures, enabling radar apertures of equivalent physical size to deliver substantially greater effective radiated power, longer detection ranges against low-observable targets, and improved resistance to adversary jamming through higher instantaneous bandwidth availability. Simultaneously, the maturation of software-defined radio frequency architectures, in which previously hardware-fixed functions including waveform generation, frequency selection, modulation, and signal processing are implemented in reprogrammable field-programmable gate array and digital signal processing hardware governed by uploadable software, is transforming the upgrade economics and threat-response agility of deployed radar and electronic warfare systems in ways that were structurally impossible with analog hardware architectures. This software-defined paradigm enables deployed systems to receive capability upgrades addressing newly identified threats through software uploads rather than hardware replacement, dramatically improving the lifecycle cost economics of advanced radar and electronic warfare platforms and reducing the interval between threat emergence and fielded countermeasure availability from years to weeks in optimized acquisition and software development pipeline environments.

Surging Counter-Unmanned Aerial System Requirements and the Expansion of Multi-Domain Electromagnetic Threat Environments

The demonstrated operational impact of unmanned aerial systems, ranging from commercially derived quadrotors carrying improvised munitions to sophisticated long-range strike drones and autonomous loitering munitions, across multiple recent and ongoing conflicts has created a rapidly growing and structurally new demand category for radar sensing, identification, and defeat capabilities that were not contemplated within the acquisition planning frameworks of most national defense establishments as recently as five years prior. The detection, tracking, and engagement of small, slow, low-altitude unmanned aerial vehicles represents a radar and signal processing challenge that is fundamentally distinct from the high-altitude, high-speed threats that existing air defense radar networks were optimized to address, requiring new sensor modalities, lower frequency bands, higher revisit rates, and artificial intelligence-enabled target discrimination algorithms capable of separating hostile unmanned systems from birds, weather returns, and civilian drone traffic in complex urban and littoral electromagnetic environments. Expenditure on counter-unmanned aerial system radar and electronic warfare defeat capabilities is growing at approximately 23.4% annually across NATO member states alone, with program investments spanning vehicle-mounted short-range detection systems, fixed-site perimeter protection sensors for critical infrastructure, ship-based close-in threat detection radars, and airborne self-protection systems capable of detecting and responding to drone swarm threats. The expansion of electromagnetic competition into the space domain, cyber-electromagnetic interface, and undersea acoustic-electromagnetic domains is further broadening the addressable market for next-generation sensing and electronic warfare investment beyond the traditional air, land, and sea platform categories that have historically defined the scope of radar and electronic warfare procurement.

Key Challenges

Electromagnetic Spectrum Congestion, Frequency Allocation Conflicts, and the Shrinking Operational Bandwidth Available to Military Systems

One of the most structurally consequential and least publicly visible challenges confronting the military radar and electronic warfare market is the progressive compression of available radio frequency spectrum for military operational use, driven by the explosive commercial demand for spectrum allocation from cellular telecommunications operators deploying 5G and 6G networks, satellite broadband constellation operators requiring large contiguous spectrum bands in L, S, and Ka-band frequencies that overlap with established military radar allocations, and the proliferation of unlicensed commercial wireless devices that collectively raise the ambient electromagnetic noise floor across contested and even non-contested operational environments. Spectrum reallocation decisions by national telecommunications regulators in the United States, European Union, and Asia-Pacific have in multiple instances reassigned frequency bands previously reserved for military radar operations to commercial broadband applications, compelling military radar developers to redesign systems for compressed or relocated frequency allocations at substantial cost and schedule impact. The challenge is compounded in multinational coalition operations, where spectrum deconfliction among allied forces operating diverse radar and electronic warfare systems across geographically overlapping coverage areas requires sophisticated dynamic spectrum management architectures and real-time frequency coordination that impose significant command-and-control overhead and restrict tactical flexibility. The increasing density of commercial satellite communications downlink signals in frequencies adjacent to military radar operating bands is further degrading radar receiver sensitivity in some operational geometries, requiring costly interference mitigation hardware and software adaptations that add weight, power consumption, and development cost to new system designs.

Export Control Complexity, Technology Transfer Restrictions, and the Challenge of Building Allied Interoperability Without Compromising Sensitive Technology

The global military radar and electronic warfare market operates within one of the most restrictive and operationally consequential export control regimes in international trade, with the International Traffic in Arms Regulations, Export Administration Regulations, Wassenaar Arrangement multilateral controls, and bilateral defense cooperation agreement frameworks collectively governing which technology, at what level of capability, can be transferred between which nations and under what end-use certification and monitoring conditions. These restrictions create significant market access barriers for prime contractors seeking to offer advanced radar and electronic warfare capabilities to allied partner nations, frequently compelling the development of downgraded export variants that lack the most sensitive waveform characteristics, signal processing algorithms, and frequency management capabilities of the domestic configuration, a design bifurcation that adds development cost, complicates production planning, and reduces the operational interoperability value of the exported system within coalition military architectures. The challenge has intensified as the technology gap between domestic and export-permissible capability levels has widened with successive generations of advanced radar and electronic warfare hardware, and as allied partner nations, particularly in the Asia-Pacific and Middle East, have grown increasingly resistant to accepting downgraded systems that they perceive as inadequate against the threat environments they face. Managing the tension between protecting sensitive technology from potential adversary exploitation through third-party technology transfer or system reverse-engineering and providing allies with genuinely capable systems that strengthen deterrence and coalition war-fighting effectiveness represents an enduring policy and commercial challenge with no straightforward resolution.

Artificial Intelligence Integration Complexity, Algorithm Validation for Safety-Critical Applications, and Adversarial Machine Learning Vulnerabilities

The integration of artificial intelligence and machine learning algorithms into the signal processing, target classification, threat identification, and autonomous response decision chains of military radar and electronic warfare systems represents both the most promising technological frontier and one of the most complex engineering, safety assurance, and ethical governance challenges confronting the defense electronics industry in the current development cycle. Radar signal processing algorithms based on deep neural network architectures can achieve target detection and classification performance that substantially exceeds rule-based signal processing in high-clutter environments, yet their behavior in out-of-distribution electromagnetic scenarios, signal environments that differ significantly from training data, can be unpredictable in ways that are difficult to characterize exhaustively through pre-deployment test and evaluation campaigns. Military airworthiness and operational certification authorities have not yet established standardized frameworks for validating the safety and reliability of AI-enabled radar and electronic warfare systems in safety-critical engagement decision applications, creating qualification uncertainty that extends development timelines and increases program cost for developers incorporating machine learning into operational decision chains. Adversarial machine learning attacks, in which hostile actors deliberately craft radio frequency emissions specifically designed to deceive or corrupt the inference behavior of AI-enabled radar classification systems, represent an emergent and operationally significant vulnerability that requires defensive counter-measures to be developed, tested, and validated in parallel with the AI capability itself, adding a recursive development complexity that conventional hardware-defined system engineering processes are not adequately structured to accommodate.

Market Segmentation

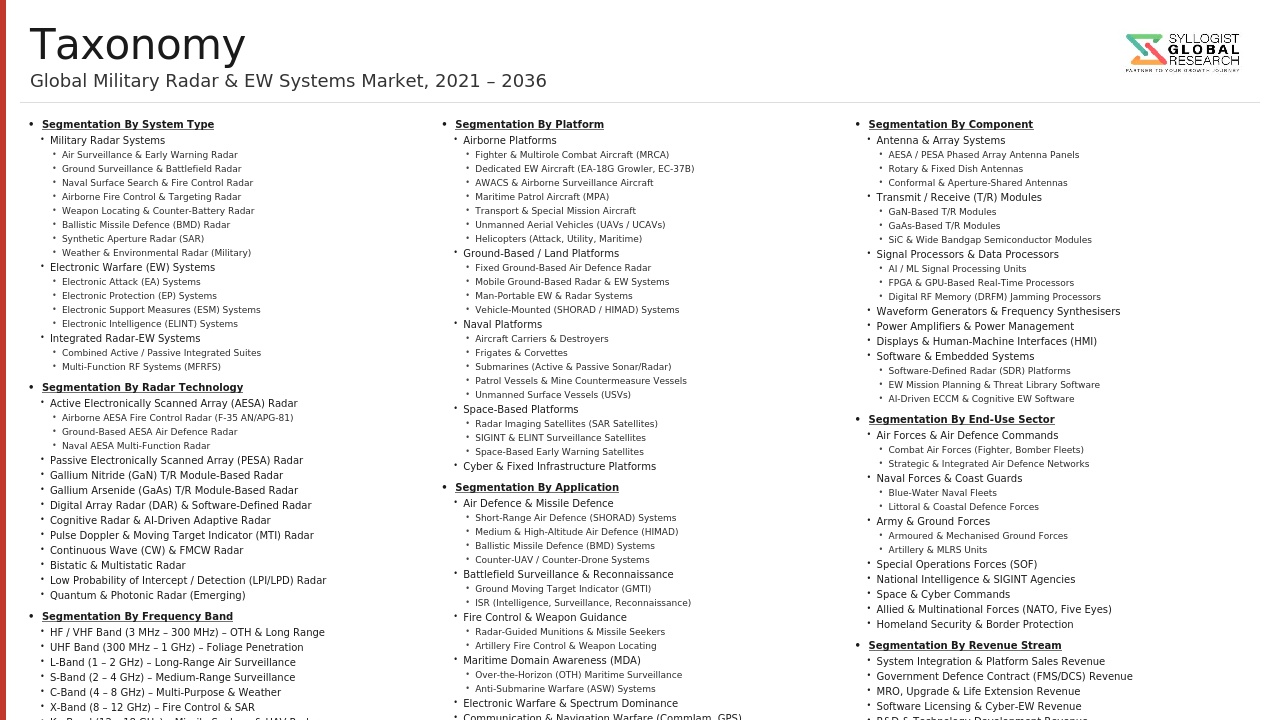

- Segmentation By System Type

- Military Radar Systems

- Electronic Attack (EA) Systems

- Electronic Protection (EP) Systems

- Electronic Support Measures (ESM) and Signals Intelligence (SIGINT) Systems

- Integrated Radio Frequency Systems (Combined Radar and EW)

- Counter-Unmanned Aerial System (C-UAS) Radar and EW Systems

- Others

- Segmentation By Radar Technology

- Active Electronically Scanned Array (AESA) Radar

- Passive Electronically Scanned Array (PESA) Radar

- Mechanically Scanned Array (MSA) Radar

- Cognitive and Adaptive Radar

- Over-the-Horizon (OTH) Radar

- Synthetic Aperture Radar (SAR)

- Inverse Synthetic Aperture Radar (ISAR)

- Quantum Radar (Developmental Stage)

- Others

- Segmentation By Frequency Band

- HF and VHF Band

- UHF Band

- L-Band

- S-Band

- C-Band

- X-Band

- Ku-Band and Ka-Band

- Multi-Band and Wideband Systems

- Others

- Segmentation By Platform

- Airborne Platforms (Fixed-Wing Fighter and Strike Aircraft)

- Airborne Platforms (Airborne Early Warning and Control Aircraft)

- Airborne Platforms (Maritime Patrol and ISR Aircraft)

- Airborne Platforms (Helicopters and Rotary-Wing)

- Naval Platforms (Surface Combatants)

- Naval Platforms (Submarines)

- Ground-Based Fixed Installations

- Ground-Based Mobile and Transportable Systems

- Space-Based Radar and EW Payloads

- Unmanned Aerial Vehicles (UAVs)

- Others

- Segmentation By Application

- Air Defense and Missile Defense

- Airborne Fire Control and Targeting

- Maritime Surface Search and Surveillance

- Ground Surveillance and Battlefield Awareness

- Signals Intelligence (SIGINT) and Electronic Intelligence (ELINT)

- Communications Intelligence (COMINT) and Cyber-Electromagnetic Operations

- Counter-Drone Detection and Defeat

- Electronic Attack and Suppression of Enemy Air Defenses (SEAD)

- Force Protection and Directed Energy Integration

- Others

- Segmentation By Component

- Transmit-Receive (T/R) Modules (GaN and GaAs)

- Antenna Arrays and Aperture Assemblies

- Signal and Data Processors

- Waveform Generators and Exciter Systems

- Electronic Warfare Jamming Transmitters

- Radar Warning Receivers (RWR) and Missile Approach Warning Systems (MAWS)

- Software-Defined Radio Frequency Processing Hardware

- Power Amplifiers and High-Power Microwave Components

- Others

- Segmentation By Technology

- Gallium Nitride (GaN) Wide-Bandgap Semiconductor Technology

- Software-Defined Radar and EW Architectures

- Artificial Intelligence and Machine Learning-Enabled Signal Processing

- Cognitive Electronic Warfare

- Directed Energy Weapons Integration (High-Power Microwave)

- Low Probability of Intercept / Low Probability of Detection (LPI/LPD) Waveforms

- Multi-Function RF Systems

- Others

- Segmentation By Sales Channel

- Direct Government-to-Government (G2G) Defense Procurement

- Foreign Military Sales (FMS) Programs

- Direct Commercial Sales (DCS)

- Prime Contractor Integration and Subcontracting

- Cooperative Development and Co-Production Programs

- Others

- Segmentation By End User

- Air Force and Tactical Aviation Commands

- Naval and Maritime Forces

- Army and Ground Forces

- Special Operations Forces

- Defense Intelligence and SIGINT Agencies

- Missile Defense Agencies

- Homeland Security and Border Protection Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Next-Generation Military Radar and Electronic Warfare Systems Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by system type, military radar, electronic attack, electronic protection, electronic support measures, and integrated radio frequency systems, to enable prime contractors, component suppliers, and defense investors to identify which technology and program categories are expected to generate the highest incremental revenue and investment returns over the forecast period?

- How is the transition from legacy gallium arsenide-based electronically scanned array radar architectures to gallium nitride-based AESA systems reshaping the competitive dynamics among established prime defense contractors and specialized component suppliers, and which airborne, naval, and ground-based radar platform programs are expected to account for the largest share of transmit-receive module procurement volumes and system integration revenue through 2034?

- What is the projected revenue contribution and compound annual growth rate of the electronic attack and cognitive electronic warfare segment relative to the broader electronic warfare market, and how are software-defined and AI-enabled electronic warfare system architectures transforming the development cost structures, upgrade economics, program timelines, and long-term competitive positioning of leading electronic warfare system developers across North America, Europe, and Asia-Pacific?

- How is the rapidly escalating global demand for counter-unmanned aerial system radar and electronic warfare defeat capabilities expected to evolve in terms of market size, technology requirements, platform integration approaches, and geographic procurement distribution through 2034, and which detection radar technologies, jamming modalities, and directed energy defeat systems are expected to achieve the broadest operational adoption across land, naval, and fixed-site defense applications?

- Who are the leading prime defense contractors, specialized electronic warfare system developers, gallium nitride component manufacturers, and artificial intelligence signal processing technology providers currently defining the competitive landscape of the global next-generation military radar and electronic warfare systems market, and what are their respective program portfolios, research and development investment trajectories, export market strategies, international co-development partnerships, and sovereign capability program engagements through the forecast horizon?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Integration Trends

- Investment & Funding Activity

- Risk Assessment Framework

- Technology Readiness & Obsolescence Risk

- Programme & Procurement Risk

- Supply Chain & Critical Material Risk

- Export Control & Geopolitical Risk

- Cyber & Electronic Security Risk

- Environmental & Spectrum Risk

- Regulatory Framework & Standards

- International Arms Control & Export Regulations

- NATO Standardisation & Interoperability

- Military Radar & EW Standards

- European & Allied Military Standards

- Spectrum Management & ITU Regulations

- Global Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by System Type

- Next-Generation Military Radar Systems

- Ground-Based Radar Systems

- Airborne Radar Systems

- Naval / Shipborne Radar Systems

- Space-Based Radar Systems

- Submarine & Underwater Radar / Sonar Radar Systems

- Electronic Warfare (EW) Systems

- Electronic Attack (EA) Systems

- Electronic Protection (EP) Systems

- Electronic Support / Electronic Intelligence (ES / ELINT) Systems

- Integrated Electronic Warfare Suites

- Multi-Function RF (MFRF) & Integrated RF Systems

- Counter-UAS / Counter-Drone Radar & EW Systems

- Directed Energy Electronic Warfare (High-Power Microwave / HPM) Systems

- Next-Generation Military Radar Systems

- Market Size & Forecast by Radar Technology Type

- Active Electronically Scanned Array (AESA) Radar

- GaN-Based AESA Radar (Gallium Nitride T/R Modules)

- GaAs-Based AESA Radar (Legacy & Transitioning)

- Silicon Photonic AESA Radar

- Digital Array Radar (DAR)

- Passive Electronically Scanned Array (PESA) Radar

- Mechanically Scanned Array (MSA) Radar (Legacy & Upgrade)

- Cognitive / Adaptive Radar

- AI/ML-Enabled Adaptive Waveform Radar

- Environment-Aware Cognitive Radar

- Over-the-Horizon (OTH) Radar

- Surface Wave OTH Radar

- Sky Wave OTH Radar

- Low Probability of Intercept / Low Probability of Detection (LPI/LPD) Radar

- Bistatic & Multistatic Radar Systems

- Passive Radar (Exploiting Non-Cooperative Illuminators)

- Quantum Radar (Research & Pre-Development Stage)

- Terahertz (THz) Radar (R&D Stage)

- Active Electronically Scanned Array (AESA) Radar

- Market Size & Forecast by Electronic Warfare System Type

- Electronic Attack (EA) Systems

- Airborne Self-Protection Jamming (ASPJ) Pods

- Standoff Electronic Attack (SOJ) / Escort Jamming Systems

- Ship-Based Active Jamming & Deception Systems

- Ground-Based Electronic Attack Systems

- High-Power Microwave (HPM) Directed Energy Weapons

- DRFM (Digital Radio Frequency Memory) Jamming Systems

- Cyber-Electronic Attack Systems

- Electronic Protection (EP) Systems

- Radar Electronic Counter-Countermeasures (ECCM) Systems

- Low Observable (Stealth) Waveform & LPI Radar Protection

- Missile Approach Warning Systems (MAWS)

- Electronic Warfare Countermeasure Dispensing Systems (Chaff / Flares)

- Ship Self-Defence Suite Electronic Protection

- Electronic Support / ELINT Systems

- Airborne Electronic Intelligence (ELINT) Collection Systems

- Ground-Based Signal Intelligence (SIGINT) / ELINT Systems

- Naval ELINT & Electronic Support Measures (ESM)

- Space-Based ELINT & Signals Intelligence Payloads

- Radar Warning Receivers (RWR)

- Passive Direction Finding (DF) & Emitter Geolocation Systems

- Integrated Electronic Warfare Suites

- Airborne Integrated EW Suites (Fixed-Wing & Rotary-Wing)

- Ship-Based Integrated EW Suites

- Ground Vehicle Integrated EW Systems

- Man-Portable Electronic Warfare Systems (MANPADS-EW)

- Market Size & Forecast by Platform

- Airborne Platforms

- Fighter / Combat Aircraft (5th & 6th Generation)

- Airborne Early Warning & Control (AEW&C) Aircraft

- Electronic Attack & Electronic Warfare Aircraft (Dedicated EA Platform)

- Maritime Patrol Aircraft (MPA)

- ISR / Surveillance Aircraft

- Unmanned Aerial Vehicles (UAV) & UCAV (Medium & High Altitude Long Endurance)

- Helicopters (Attack, Maritime, ASW)

- Transport & Tanker Aircraft (Self-Protection EW)

- Ground-Based Platforms

- Ground-Based Air Defence (GBAD) Radar Systems

- Counter-UAS Ground Radar & EW Systems

- Artillery & Mortar Locating Radar

- Battlefield Surveillance Radar

- Air Traffic Control Military Radar

- Ground Vehicle-Mounted Radar & EW Systems

- Man-Portable Radar & EW Systems

- Naval / Maritime Platforms

- Aircraft Carriers (Integrated Mast, Air Surveillance, Fire Control Radar)

- Destroyers & Frigates (Multi-Function Naval Radar & EW Suite)

- Corvettes & Patrol Vessels

- Submarines (Periscope Mast Radar, ESM & EW Systems)

- Mine Countermeasures Vessels (Sonar-Radar Integration)

- Unmanned Surface Vessels (USV) & Unmanned Underwater Vehicles (UUV)

- Space-Based Platforms

- Reconnaissance & ELINT Satellites

- Space-Based Radar (SBR) & GMTI (Ground Moving Target Indicator) Satellites

- Space Domain Awareness (SDA) Radar Constellations

- Space-Based EW (Anti-Satellite Jamming & SIGINT)

- Market Size & Forecast by Frequency Band

- HF / VHF / UHF Band (Over-the-Horizon & Long-Range Surveillance)

- L-Band (1–2 GHz – Long-Range Air Surveillance & Ballistic Missile Defence)

- S-Band (2–4 GHz – Medium-Range Surveillance & Weather)

- C-Band (4–8 GHz – Tracking & Fire Control)

- X-Band (8–12 GHz – Fire Control, SAR, Maritime Surveillance)

- Ku-Band (12–18 GHz – Airborne SAR, Fire Control)

- Ka-Band (27–40 GHz – High-Resolution SAR, Fire Control)

- Millimetre Wave / W-Band (75–110 GHz – Counter-UAS, Imaging)

- Wideband / Multi-Band & Ultra-Wideband (UWB) EW Systems

- Market Size & Forecast by Application

- Air Surveillance & Air Defence

- Long-Range Air Surveillance Radar

- Tactical Air Defence Radar

- Ballistic Missile Defence (BMD) Radar

- Hypersonic Missile Detection Radar

- Fire Control & Weapon Guidance

- Airborne Fire Control Radar (Fighter Aircraft)

- Ground-Based Fire Control Radar (SAM, AAA)

- Naval Fire Control Radar

- Artillery & Rocket Fire Control Radar

- Intelligence, Surveillance & Reconnaissance (ISR)

- Synthetic Aperture Radar (SAR) for Ground & Maritime Imaging

- Ground Moving Target Indicator (GMTI) Radar

- Inverse SAR (ISAR) for Ship & Air Target Classification

- Airborne ELINT & SIGINT Collection

- Electronic Attack & Jamming

- Airborne Electronic Attack (Self-Protection & Escort Jamming)

- Ground-Based Electronic Attack & GPS Jamming

- Ship-Based Electronic Attack & Deception

- Counter-UAS & Drone Defence

- Detect, Track & Identify (DTI) Radar for Small UAS

- Electronic Counter-UAS (Soft-Kill Jamming & Spoofing)

- Kinetic-Electronic Hybrid Counter-UAS Systems

- Electronic Protection & Self-Defence

- Airborne Self-Protection Countermeasures

- Ship Self-Defence EW Suite

- Radar ECCM & Low-Observable Waveform Protection

- Border Security, Coastal Surveillance & Force Protection

- Persistent Ground Surveillance Radar (Fixed & Relocatable)

- Coastal / Maritime Domain Awareness Radar

- Force Protection / Base Defence Radar

- Space Domain Awareness & Missile Defence

- Space Surveillance Radar for Object Tracking & Cataloguing

- Anti-Satellite (ASAT) EW & Directed Energy Systems

- Ballistic Missile Early Warning Radar

- Market Size & Forecast by End-Use Sector

- Air Force

- Army / Land Forces

- Navy / Maritime Forces

- Space Force / Space Commands

- Homeland Security & Border Forces

- Intelligence & Special Operations Forces

- Others (Joint Commands, Allied Forces, Paramilitary)

- Market Size & Forecast by Component

- Transmit / Receive (T/R) Modules & AESA Antenna Arrays

- GaN T/R Modules

- GaAs T/R Modules

- Silicon Photonic T/R Modules (Emerging)

- Radar Signal Processors & Data Processors

- COTS-Based Signal Processing Boards

- FPGA-Based Real-Time Radar Signal Processors

- GPU-Accelerated Radar Processing Platforms

- AI / ML Inference Engines for Radar Target Classification

- Electronic Warfare Jamming Systems & Transmitters

- Travelling Wave Tube Amplifiers (TWTA) for EW

- Solid-State Power Amplifiers (SSPA) for EW

- DRFM Jamming Modules

- High-Power Microwave (HPM) Transmitters

- Receivers & Electronic Support Measure (ESM) Front-Ends

- Broadband Wideband EW Receiver Sub-Systems

- Radar Warning Receiver (RWR) Front-End Modules

- Direction Finding (DF) Arrays & Receivers

- Antenna Systems

- Phased Array Antenna Assemblies

- Conformal Antennas for Airborne & Shipborne Applications

- Multi-Band Multi-Function Antenna Arrays

- Low-Observable (Stealth-Optimised) Antenna Designs

- Radar Displays, Human-Machine Interface (HMI) & Operator Consoles

- Power Generation & Power Conditioning Systems

- Software: Radar & EW Mission Software, Waveform Libraries & AI Models

- Cooling & Thermal Management Systems

- Transmit / Receive (T/R) Modules & AESA Antenna Arrays

- Air Surveillance & Air Defence

- Airborne Platforms

- Electronic Attack (EA) Systems

- North America Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

- Europe Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

- Asia-Pacific Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

- Middle East & Africa Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

- Latin America Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

- Country-Wise* Next-Generation Military Radar & Electronic Warfare Systems Market Outlook

- Market Size & Forecast

- By Value

- By System Type

- By Radar Technology Type

- By Electronic Warfare System Type

- By Platform

- By Frequency Band

- By Application

- By End-Use Sector

- By Component

- Market Size & Forecast

*Countries Analyzed: United States, Canada, United Kingdom, Germany, France, Italy, Sweden, Norway, Poland, Israel, Russia, China, Japan, South Korea, India, Australia, Singapore, Saudi Arabia, UAE, Turkey, South Africa, Brazil

- Technology Landscape & Innovation Analysis

- AESA & Phased Array Radar Technology Landscape

- Cognitive & AI-Enabled Radar Technology

- Software-Defined Radar & Open Architecture Technology

- Electronic Attack & Jamming Technology

- Electronic Support & Intelligence Technology

- Counter-UAS Radar & EW Technology

- Space-Based Radar & EW Technology

- Advanced Materials & Semiconductor Technology

- Quantum & Photonic Technology in Radar & EW

- Patent & IP Landscape

- Value Chain & Supply Chain Analysis

- Raw Materials & Advanced Semiconductor Substrates

- Semiconductor Fabrication & MMIC Manufacturing

- Radar & EW Sub-System Component Manufacturing

- Radar & EW System Integration

- Software Development & Mission Data

- Testing, Verification & Validation (V&V)

- Defence Procurement & Customer Base

- MRO, Sustainment & Mid-Life Upgrade

- Pricing Analysis

- Next-Generation Radar System Pricing Analysis

- Electronic Warfare System Pricing Analysis

- Component & Sub-System Pricing

- Total Programme Cost Analysis

- Defence Budget & Procurement Programme Analysis

- Global Defence Budget Trends & Radar / EW Spending Allocation

- Key Active Procurement Programmes – Radar

- Key Active Procurement Programmes – Electronic Warfare

- Upcoming Procurement Pipeline & RFP Watch

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Sub-Segment)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type & Geography

- Player Classification

- Tier-1 Global Defence Prime Contractors (Full-Spectrum Radar & EW Capability)

- Tier-2 Specialist Radar System OEMs

- Tier-2 Specialist Electronic Warfare System OEMs

- Component & Sub-System Specialists (GaN, DRFM, T/R Modules, EW Receivers)

- Software & AI / Cognitive EW Technology Providers

- Emerging & Disruptive Technology Companies

- State-Owned Defence Enterprises (Russia, China, India)

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Platform & Geography

- Company Profile

- Company Overview & Headquarters

- Radar & Electronic Warfare Products & Systems Portfolio

- Key Programs, Contracts & Delivery Status

- Technology Differentiators & IP

- Revenue (Defence Electronics Segment) & Backlog

- Export Markets & FMS Activity

- Key Strategic Partnerships, Teaming Agreements & JVs

- Recent Developments (Contract Wins, Technology Demos, M&A, Partnerships)

- SWOT Analysis

- Strategic Focus Areas & Investment Roadmap

- Competitive Positioning Map (Technology Leadership vs. Programme Capture)

- Key Company Profiles

- Raytheon Technologies (RTX) – Raytheon Intelligence & Space

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix – By System Type, Platform & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Investment & R&D Prioritisation Strategy

- Programme Capture & Business Development Strategy

- Open Architecture & Software Strategy

- Supply Chain Resilience & Critical Material Strategy

- Partnership, M&A & Internationalisation Strategy

- Sustainability & ESG Strategy for Defence Electronics

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)