Market Definition

The Global Power Semiconductor Market encompasses the design, fabrication, packaging, testing, and commercial supply of semiconductor devices engineered to control, convert, and condition electrical power across a defined range of voltage, current, frequency, and thermal operating parameters in applications spanning consumer electronics, industrial automation, automotive electrification, renewable energy power conversion, rail traction, telecommunications infrastructure, data center power management, and defense electronics. Power semiconductors are distinguished from logic and memory semiconductors by their primary function of managing energy flow rather than processing information, operating at voltage ratings from below 10 volts for low-dropout regulators in portable devices to above 6,500 volts for insulated-gate bipolar transistors and integrated gate-commutated thyristors in high-voltage direct current transmission and rail traction applications, and handling current ratings from milliamperes to kiloamperes depending on device type and application context. The market encompasses the complete power semiconductor device portfolio including power diodes, bipolar junction transistors, power metal-oxide-semiconductor field-effect transistors, insulated-gate bipolar transistors, silicon carbide metal-oxide-semiconductor field-effect transistors, silicon carbide Schottky barrier diodes, gallium nitride high-electron-mobility transistors, thyristors, triacs, gate turn-off thyristors, integrated gate-commutated thyristors, intelligent power modules, and power integrated circuits that combine multiple switching, gate driver, and protection functions within single package architectures. The market additionally encompasses the substrate materials, epitaxial wafer supply chains, and advanced packaging technologies including direct bonded copper substrates, sintered die attach, double-sided cooling modules, and chip-scale packages that are integral to the performance and reliability of finished power semiconductor devices across their end-use operating environments. Key participants include integrated device manufacturers, fabless design companies, contract foundries, epitaxial wafer suppliers, substrate and packaging material producers, module assemblers, and the automotive, industrial, energy, and consumer electronics end users whose electrification and power conversion investment drives structural market demand.

Market Insights

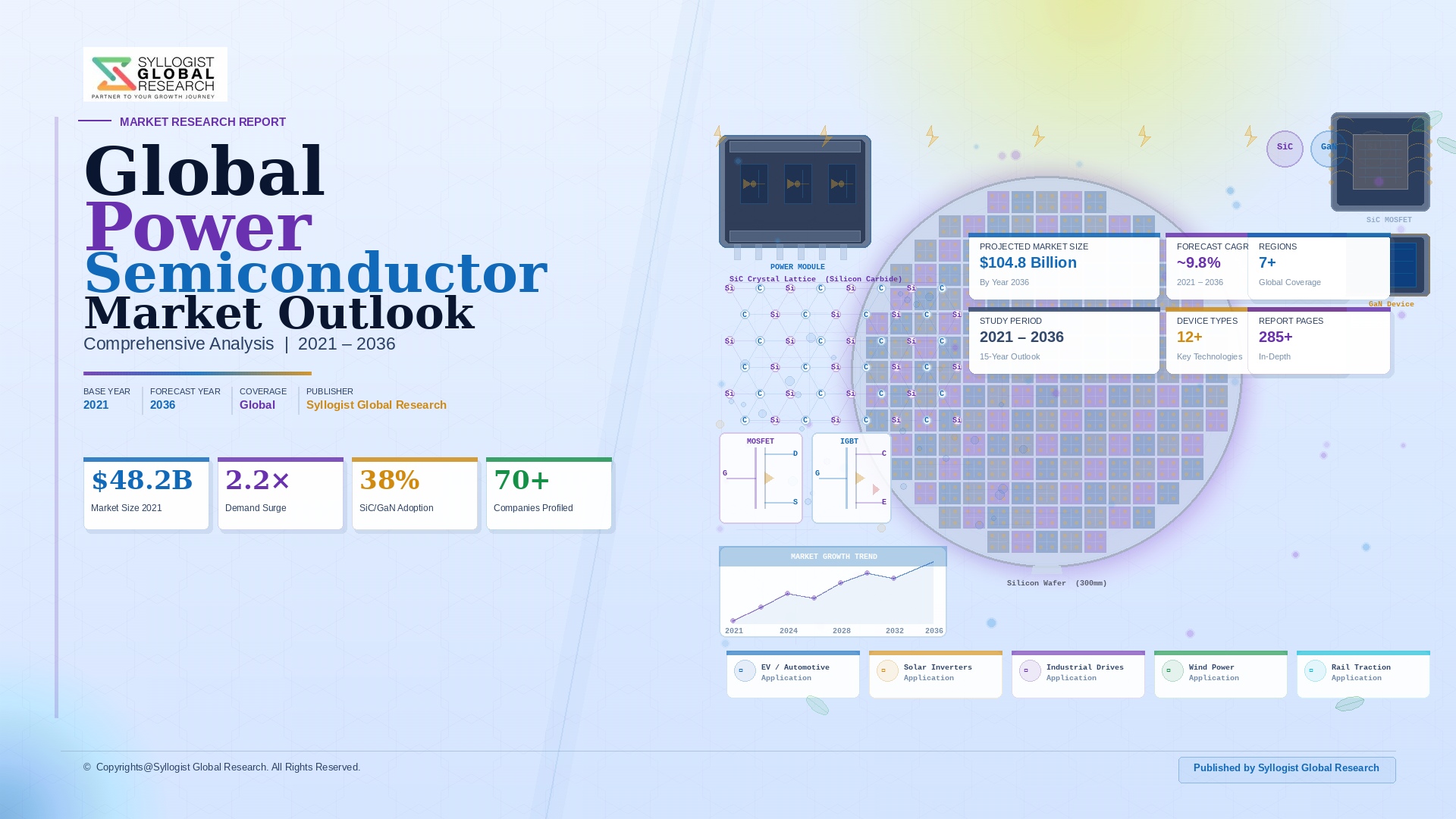

The global power semiconductor market was valued at approximately USD 52.4 billion in 2025 and is projected to reach USD 112.8 billion by 2034, advancing at a compound annual growth rate of 8.9% over the forecast period from 2027 to 2034, propelled by the electrification of transportation, the rapid scaling of renewable energy power conversion infrastructure, the intensifying power density and efficiency requirements of data center power management, and the progressive substitution of silicon insulated-gate bipolar transistors and metal-oxide-semiconductor field-effect transistors by silicon carbide and gallium nitride wide-bandgap semiconductor devices that command substantially higher per-unit average selling prices while delivering superior switching frequency, thermal performance, and conversion efficiency across automotive inverters, electric vehicle charging, solar and wind power converters, and industrial motor drives. Global electric vehicle production reached approximately 17.4 million units in 2025, with each battery electric vehicle incorporating power semiconductor content of approximately USD 430 to USD 680 per vehicle for the traction inverter, onboard charger, DC-DC converter, and battery management power stage, compared to approximately USD 55 to USD 80 of power semiconductor content in a conventional internal combustion engine vehicle, representing a content multiplier of approximately seven to nine times that is the single most powerful structural demand driver in the power semiconductor market and is expected to sustain above-market-average revenue growth in the automotive segment through the forecast period as global electric vehicle production volumes scale toward an estimated 38 million units annually by 2034. The silicon carbide device segment reached approximately USD 3.8 billion in revenue in 2025 and is projected to reach USD 14.6 billion by 2034 at a compound annual growth rate of 16.1%, driven predominantly by automotive traction inverter adoption where silicon carbide metal-oxide-semiconductor field-effect transistors enable inverter efficiency improvements of approximately two to three percentage points relative to silicon insulated-gate bipolar transistors, extending electric vehicle driving range by approximately 5% to 10% on equivalent battery capacity.

The automotive segment constitutes the dominant and fastest-growing end-use market for power semiconductors, accounting for approximately 34% of total market revenue in 2025 and growing at approximately 12.6% annually, driven not only by the electric vehicle powertrain transition but by the proliferation of 48-volt mild hybrid systems, advanced driver assistance system power supply requirements, electrified chassis actuators including electric power steering and active suspension, and the progressive electrification of thermal management, braking, and accessory systems that collectively increase the total power semiconductor content per vehicle across the full spectrum of conventional, hybrid, and battery electric vehicle platforms. Tesla’s transition to silicon carbide power modules in its Model 3 traction inverter in 2018 established silicon carbide as the performance-preferred technology for electric vehicle main drive inverters, with subsequent adoption by Toyota in its bZ4X platform, BYD in its premium Han and Tang models, Volkswagen Group across its PPE and MEB electric vehicle platforms, and effectively all major automotive original equipment manufacturers now specifying silicon carbide traction inverters for their battery electric vehicle programs, creating a structural silicon carbide demand commitment from the automotive sector that is the primary driver of the massive capacity expansion investments being undertaken by silicon carbide device manufacturers including Wolfspeed, Onsemi, STMicroelectronics, Infineon, and ROHM across their silicon carbide substrate, epitaxy, and device fabrication facilities globally. The onboard charger and DC-DC converter segments within electric vehicles are progressively adopting gallium nitride high-electron-mobility transistors from technology providers including GaN Systems, Navitas Semiconductor, Infineon, and Texas Instruments, leveraging gallium nitride’s superior high-frequency switching capability to reduce magnetic component size and enable higher power density charger designs that reduce vehicle weight and packaging volume while improving charging efficiency across the expanding range of AC and DC charging power levels deployed globally.

The industrial and energy segment, encompassing motor drives for industrial automation and HVAC, renewable energy inverters for solar photovoltaic and wind power generation, energy storage system power conditioning, and grid infrastructure including flexible alternating current transmission systems, static synchronous compensators, and high-voltage direct current converter stations, represents the second-largest application category at approximately 38% of total market revenue in 2025, sustained by the global renewable energy capacity expansion that added approximately 295 gigawatts of solar photovoltaic and approximately 115 gigawatts of wind capacity in 2025 alone, each gigawatt of installed capacity requiring approximately USD 4 to USD 8 million of power semiconductor content for inverters, power optimizers, and grid interface converters depending on technology configuration and voltage level. The transition of industrial motor drives toward silicon carbide-based architectures from conventional silicon insulated-gate bipolar transistor platforms is gaining commercial momentum, driven by silicon carbide’s ability to enable higher switching frequencies that reduce motor winding losses through reduced voltage harmonic distortion, decrease motor drive heat sink volume and cooling requirements through reduced switching losses, and enable more compact variable frequency drive designs at equivalent power ratings, with total addressable market for silicon carbide in industrial motor drives estimated at approximately USD 2.4 billion by 2030 as cost reduction through manufacturing scale-up makes silicon carbide increasingly cost-competitive with high-performance silicon insulated-gate bipolar transistors at voltage ratings of 650 to 1,200 volts. The data center power management segment is experiencing the fastest growth within the industrial category at approximately 18.4% annually, driven by the extraordinary power density and energy efficiency requirements of artificial intelligence accelerator infrastructure whose GPU and custom accelerator chips draw several hundred watts per chip, creating power delivery architecture requirements that are pushing power management semiconductor performance beyond the capability of conventional silicon-based solutions toward gallium nitride integrated circuits that achieve superior transient response, switching frequency, and power density in voltage regulator module and bus converter applications.

The competitive and geopolitical landscape of the global power semiconductor market is undergoing a fundamental restructuring driven by the strategic designation of semiconductor manufacturing, including power semiconductor fabrication, as critical national and economic security infrastructure by the United States, European Union, Japan, South Korea, India, and China, leading to unprecedented levels of government-supported investment in domestic power semiconductor manufacturing capacity that is simultaneously expanding global supply and reshaping the geographic distribution of fabrication capacity away from its historically concentrated Asian footprint toward a more geographically diversified but substantially higher-cost multi-regional production landscape. The United States CHIPS and Science Act’s USD 52.7 billion in semiconductor manufacturing and research incentives, the European Union Chips Act’s EUR 43 billion framework to double Europe’s global semiconductor market share to 20% by 2030, Japan’s government-sponsored Rapidus advanced semiconductor program, and India’s USD 10 billion semiconductor incentive scheme are collectively mobilizing a wave of capacity investment in geographies where construction and operating costs substantially exceed those of established Asian manufacturing clusters, creating upward pressure on power semiconductor production cost structures that will influence device pricing, customer qualification strategies, and supply chain diversification decisions across all major end-use markets through the forecast period. Wolfspeed’s USD 6.6 billion Mohawk Valley silicon carbide fabrication facility in New York, Infineon’s USD 5.0 billion silicon carbide expansion at its Villach Austria campus, STMicroelectronics and Sanan Optoelectronics’ joint silicon carbide manufacturing venture in Chengdu, and ROHM’s USD 3.8 billion silicon carbide investment program in Japan collectively illustrate the geographic diversification and absolute capital scale of silicon carbide manufacturing expansion that is simultaneously addressing structural supply shortfalls relative to automotive and industrial demand growth and establishing national and regional supply security positions for the most strategically important next-generation power semiconductor technology.

Key Drivers

Accelerating Global Electric Vehicle Adoption Generating a Structural Seven-to-Nine Times Power Semiconductor Content Multiplier Per Vehicle Relative to Conventional Internal Combustion Platforms

The global transition from internal combustion engine vehicles to battery electric vehicles represents the most structurally impactful single demand driver in the history of the power semiconductor industry, as the replacement of a mechanical drivetrain consuming approximately USD 55 to USD 80 of power semiconductor content with a battery electric powertrain incorporating traction inverters, onboard chargers, DC-DC converters, battery management power electronics, and electrified chassis subsystems consuming approximately USD 430 to USD 680 of power semiconductor content per vehicle creates a revenue multiplier of approximately seven to nine times per vehicle produced that is transforming the automotive segment from a moderate growth market into the dominant structural growth engine of the power semiconductor industry through the forecast period. The transition to silicon carbide traction inverters from silicon insulated-gate bipolar transistors is amplifying the content per vehicle revenue impact further, as silicon carbide device average selling prices carry a premium of approximately three to five times over equivalent silicon devices at comparable power ratings, with the automotive silicon carbide market valued at approximately USD 2.1 billion in 2025 and projected to reach approximately USD 8.4 billion by 2034 as silicon carbide traction inverter adoption rates across new battery electric vehicle programs increase from approximately 45% in 2025 toward above 85% by 2030 across global automotive original equipment manufacturer platforms. The 48-volt mild hybrid system proliferation across conventional vehicle platforms in Europe, China, and North America is creating an additional power semiconductor demand layer independent of full battery electric vehicle adoption, with each 48-volt mild hybrid system incorporating approximately USD 60 to USD 120 of incremental power semiconductor content for the belt-integrated starter-generator converter, DC-DC bidirectional converter, and lithium-ion battery management power stage, collectively adding a USD 1.0 billion to USD 1.5 billion annual addressable market increment to automotive power semiconductor demand by 2030.

Massive Renewable Energy Capacity Expansion and Grid Modernization Investment Creating Sustained Demand for High-Efficiency Power Conversion Semiconductors Across Solar, Wind, and Energy Storage Applications

The global renewable energy capacity expansion required to meet national net-zero commitments and clean energy transition targets is generating a sustained and growing structural demand stream for power semiconductors used in photovoltaic inverters, wind turbine converters, energy storage system power conditioning, and grid infrastructure power electronics, with global renewable energy investment reaching approximately USD 1.8 trillion in 2025 and projected to sustain investment at or above this level through the forecast period, creating reliable multi-year forward demand visibility for power semiconductor manufacturers servicing the energy sector that supports the long-term capacity investment decisions required to expand silicon carbide and advanced silicon device fabrication infrastructure. Each gigawatt of installed solar photovoltaic capacity requires approximately USD 4 to USD 6 million of power semiconductor content in string inverters, central inverters, microinverters, and power optimizers, translating the approximately 295 gigawatts of solar photovoltaic installations completed globally in 2025 into approximately USD 1.2 to USD 1.8 billion of annual solar inverter power semiconductor demand, with the transition toward higher power density and higher efficiency silicon carbide-based inverter designs progressively increasing per-watt semiconductor content value as device average selling prices premium more than offsets the reduced device count enabled by silicon carbide’s superior performance. Grid modernization programs including high-voltage direct current interconnectors, flexible alternating current transmission systems, and grid-scale battery energy storage inverters are deploying insulated-gate bipolar transistor modules and increasingly silicon carbide modules at voltage ratings of 1,700 to 6,500 volts whose per-unit value can range from USD 5,000 to over USD 50,000 for high-power integrated modules, representing a high-unit-value market segment whose growth is directly correlated with renewable energy grid integration investment scaling through 2034.

Wide-Bandgap Semiconductor Material Transition from Silicon to Silicon Carbide and Gallium Nitride Driving Structural Average Selling Price Expansion and Content Value Uplift Across All Major Application Segments

The technology transition from silicon-based power semiconductor devices to wide-bandgap silicon carbide and gallium nitride devices across automotive, industrial, energy, and data center applications is generating a structural average selling price expansion and total addressable market enlargement for the power semiconductor industry that is independent of volume growth, as silicon carbide and gallium nitride devices command per-unit pricing premiums of three to ten times over equivalent silicon devices based on their superior electrical and thermal properties including higher breakdown voltage, higher thermal conductivity, and higher electron saturation velocity that collectively enable higher switching frequencies, lower conduction and switching losses, higher operating temperatures, and smaller system form factors that deliver quantifiable system-level cost and performance benefits to end users justifying the device premium. Silicon carbide’s bandgap of 3.26 electron volts and critical electric field of 3.0 megavolts per centimeter compared to silicon’s 1.12 electron volt bandgap and 0.3 megavolts per centimeter critical field enable silicon carbide devices to achieve on-resistance figures at a given blocking voltage that are approximately 100 times lower than silicon, translating directly into lower conduction losses in traction inverters, solar converters, and industrial drives that improve system efficiency, reduce cooling requirements, and decrease system total cost of ownership in ways that create commercially self-justifying demand for silicon carbide despite its higher upfront device cost. Gallium nitride’s superior high-frequency switching performance enabling operating frequencies above 1 megahertz, compared to typical silicon metal-oxide-semiconductor field-effect transistor switching frequencies below 100 kilohertz and silicon carbide operating at 100 to 500 kilohertz, is driving adoption in fast chargers, data center voltage regulator modules, and wireless power transfer applications where frequency-dependent passive component miniaturization delivers transformative system size and weight reductions that make gallium nitride the enabling technology rather than a cost-driven premium substitution.

Key Challenges

Silicon Carbide Substrate Supply Constraints, Crystal Growth Yield Limitations, and Wafer Cost Premiums Creating Persistent Supply Chain Bottlenecks for Automotive and Industrial Demand Scaling

The global silicon carbide power semiconductor supply chain faces a structural bottleneck at the substrate and epitaxial wafer level whose resolution requires capital-intensive and technically demanding manufacturing capacity expansion programs spanning three to five years from investment commitment to qualified production output, creating a persistent supply-demand imbalance that is constraining the pace of silicon carbide adoption in automotive traction inverters, industrial motor drives, and renewable energy inverters and maintaining a silicon carbide substrate price premium that limits the addressable market breadth of silicon carbide applications to those where the performance benefit creates sufficient system-level value to absorb the device cost premium relative to silicon alternatives. Silicon carbide crystal growth using the physical vapor transport method requires sublimation growth of silicon carbide source powder at temperatures approaching 2,400 degrees Celsius within closely controlled thermal gradient environments over growth periods of one to two weeks to produce boules of 150 to 200 millimeter diameter, with crystal defect density, micropipe count, and polytype purity requirements for automotive-grade substrates imposing severe yield constraints that result in substrate yield rates of 40% to 60% per boule, substantially below the near-100% yield achievable in silicon crystal growth, driving silicon carbide substrate costs to approximately USD 800 to USD 1,500 per 150-millimeter wafer compared to below USD 10 per equivalent silicon wafer and making substrate cost the dominant component in silicon carbide device manufacturing economics. The transition from 150-millimeter to 200-millimeter silicon carbide substrates, which would increase die area per wafer by approximately 78% and dramatically reduce per-die substrate cost, is progressing more slowly than originally projected by silicon carbide device manufacturers due to epitaxial layer uniformity challenges on larger diameter silicon carbide substrates and the need for complete re-qualification of automotive customer supply chains when transitioning wafer diameter generations, maintaining cost pressure on silicon carbide device manufacturers and constraining the pace of average selling price reduction that would accelerate broader market adoption.

Automotive Quality and Reliability Qualification Requirements, Long Customer Qualification Timelines, and Supply Chain Concentration Risks Creating Execution Barriers for Silicon Carbide Market Penetration

The automotive sector’s extraordinarily demanding quality, reliability, and supply chain qualification requirements create execution barriers for power semiconductor manufacturers seeking to penetrate the electric vehicle traction inverter market with silicon carbide devices, as automotive original equipment manufacturers and tier-one inverter suppliers impose qualification processes including AEC-Q101 device qualification, PPAP production part approval, extended burn-in and accelerated lifetime testing at high temperature and high voltage stress conditions, and multi-year field reliability validation programs that require silicon carbide device manufacturers to commit substantial engineering resources and testing infrastructure investment over qualification timelines of eighteen to thirty-six months before commercial production orders are placed, delaying revenue recognition from the substantial silicon carbide manufacturing capacity investments being executed by device manufacturers ahead of confirmed customer awards. The geographic concentration of silicon carbide substrate supply in a small number of manufacturers, with Wolfspeed accounting for approximately 60% to 65% of global 150-millimeter silicon carbide substrate output in 2025 and II-VI Coherent, SiCrystal, and a small number of Japanese and Chinese producers collectively supplying the remainder, creates supply security vulnerability for silicon carbide device manufacturers whose production capacity investments depend on reliable substrate supply from a concentrated supplier base whose own manufacturing yields, capacity expansions, and business continuity represent critical dependencies that automotive customers are increasingly factoring into supply chain risk assessments and dual-sourcing requirements. The simultaneous execution of multiple multi-billion-dollar silicon carbide manufacturing capacity expansion programs across Wolfspeed, Infineon, STMicroelectronics, Onsemi, and ROHM within a compressed three-to-five year window creates execution risk of coordinated oversupply in the medium term if electric vehicle adoption rates in key markets including China and Europe diverge downward from the growth trajectories that underpinned original capacity investment decisions.

Geopolitical Supply Chain Risks, Export Control Restrictions on Advanced Semiconductor Manufacturing Equipment and Materials, and Technology Decoupling Pressures Fragmenting the Global Power Semiconductor Industry

The progressive tightening of export controls by the United States, Netherlands, and Japan on advanced semiconductor manufacturing equipment including lithography systems, etch tools, and deposition equipment, combined with the escalating United States restrictions on the supply of advanced semiconductor chips and manufacturing technology to Chinese entities, is creating technology access barriers, supply chain fragmentation, and customer-supplier relationship disruption across the global power semiconductor industry that increases development costs, extends product commercialization timelines, and creates regional supply security vulnerabilities that are forcing both manufacturers and end users to undertake costly supply chain restructuring programs. While most power semiconductor devices are manufactured on legacy silicon process nodes below the cutting-edge logic technology boundaries targeted by current export controls, silicon carbide epitaxial growth equipment, advanced ion implantation systems for silicon carbide and gallium nitride device fabrication, and high-temperature annealing equipment have exposure to export restriction frameworks that could constrain Chinese silicon carbide and gallium nitride device manufacturers from accessing the most advanced equipment generations required to close the performance and yield gap with leading Western and Japanese silicon carbide producers. The Chinese government’s response to technology access restrictions, manifested through the National Integrated Circuit Industry Investment Fund’s continued capital deployment, MIIT subsidies for domestic wide-bandgap semiconductor development programs, and state-directed wafer foundry and device manufacturer capacity investments targeting silicon carbide and gallium nitride device self-sufficiency for the domestic automotive and industrial markets, is simultaneously creating potential medium-term oversupply risk in standard silicon power semiconductor categories and accelerating the development of a separate domestic Chinese silicon carbide supply chain that will increasingly serve the domestic electric vehicle and renewable energy markets at competitive price points that could displace incumbent Western and Japanese device manufacturers from one of the highest-growth regional power semiconductor markets globally.

Market Segmentation

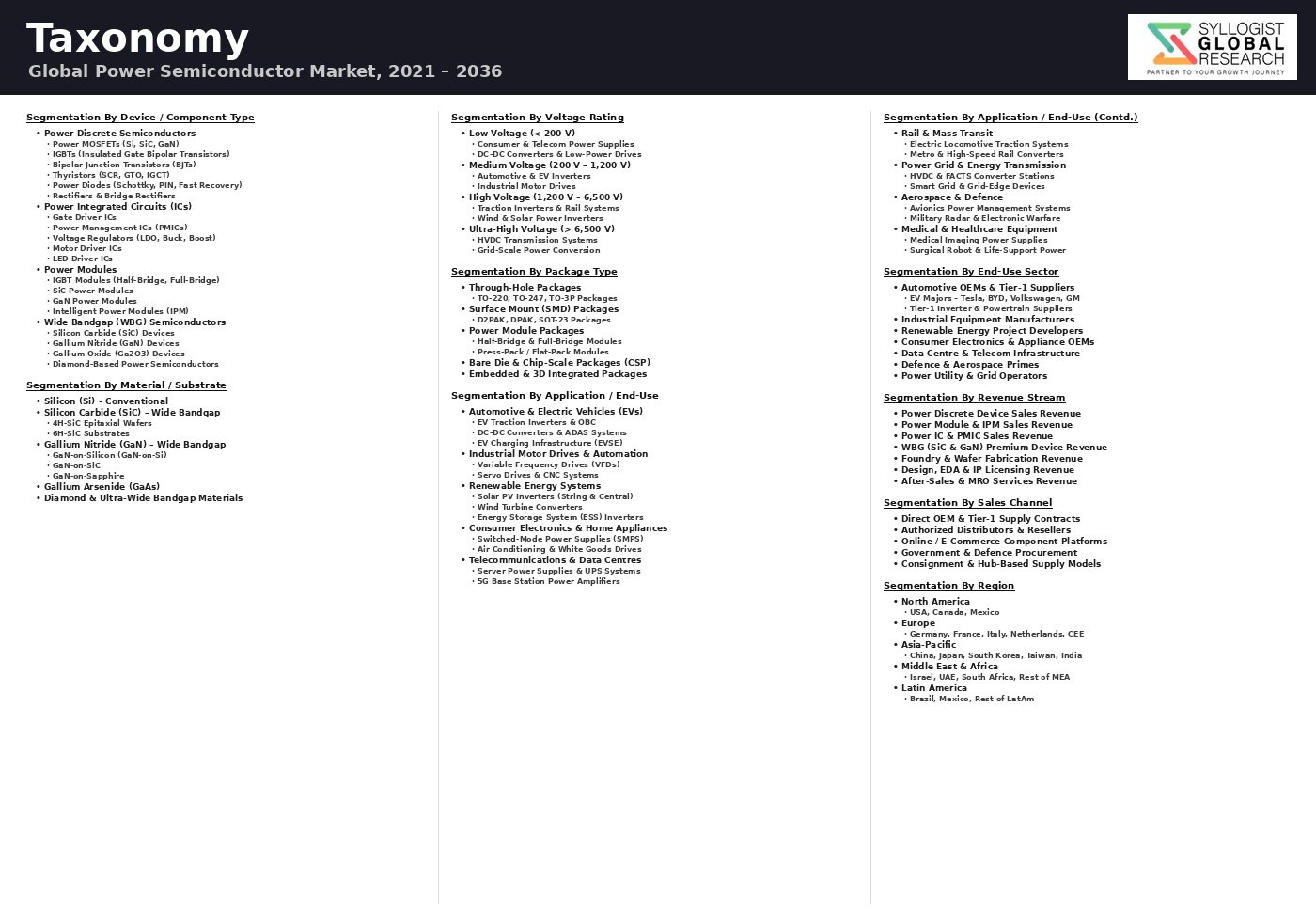

- Segmentation By Device Type

- Power Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs)

- Insulated-Gate Bipolar Transistors (IGBTs) and IGBT Modules

- Silicon Carbide MOSFETs and Schottky Barrier Diodes

- Gallium Nitride High-Electron-Mobility Transistors (GaN HEMTs) and GaN ICs

- Power Diodes (Schottky, Fast Recovery, and Ultrafast)

- Thyristors, Gate Turn-Off Thyristors (GTOs), and Integrated Gate-Commutated Thyristors (IGCTs)

- Intelligent Power Modules (IPMs) and Power Integrated Circuits

- Others

- Segmentation By Material

- Silicon (Si)

- Silicon Carbide (SiC)

- Gallium Nitride (GaN)

- Gallium Oxide (Ga2O3) and Emerging Wide-Bandgap Materials

- Diamond Semiconductor (Research and Early Development Stage)

- Segmentation By Voltage Rating

- Low Voltage (Below 250 Volts)

- Medium Voltage (250 to 900 Volts)

- High Voltage (900 to 3,300 Volts)

- Very High Voltage (Above 3,300 Volts)

- Segmentation By End-Use Application

- Automotive and Electric Vehicles (Traction Inverters, OBC, DC-DC Converters, and ADAS)

- Industrial Motor Drives and Variable Frequency Drives

- Renewable Energy (Solar Photovoltaic Inverters, Wind Turbine Converters, and Energy Storage)

- Grid Infrastructure (HVDC, FACTS, and Static Synchronous Compensators)

- Data Centers and Server Power Supplies

- Consumer Electronics and White Goods

- Telecommunications and 5G Base Station Power

- Rail Traction and Transportation

- Medical Equipment and Healthcare Devices

- Defense and Aerospace

- Others

- Segmentation By Package Type

- Discrete Devices (TO-247, TO-220, D2PAK, and Others)

- Standard Modules (Half-Bridge, Full-Bridge, and Three-Phase Modules)

- Intelligent Power Modules (IPMs) with Integrated Gate Drivers and Protection

- Chip-Scale and Wafer-Level Packages

- Custom and Application-Specific Power Modules

- Others

- Segmentation By Supply Chain Model

- Integrated Device Manufacturers (IDMs)

- Fabless Design Companies with Foundry Manufacturing

- Contract Foundries and Pure-Play Foundries

- Module Assemblers and Packaging Specialists

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Power Semiconductor Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by device type including silicon MOSFETs and IGBTs, silicon carbide MOSFETs and diodes, gallium nitride HEMTs and ICs, intelligent power modules, and thyristors, by material including silicon, silicon carbide, and gallium nitride, and by end-use application including automotive and electric vehicles, industrial motor drives, renewable energy, grid infrastructure, data centers, and consumer electronics, to enable power semiconductor manufacturers, automotive and industrial equipment producers, renewable energy developers, data center operators, investment managers, and government semiconductor policy planners to identify the highest-growth device technology and application segment combinations generating the most commercially durable demand across the forecast period to 2034?

- What is the silicon carbide power semiconductor market revenue, production capacity, substrate and epitaxy supply chain status, wafer diameter transition timeline from 150-millimeter to 200-millimeter, device average selling price trajectory, and automotive traction inverter design win pipeline of the leading silicon carbide device manufacturers including Wolfspeed, Onsemi, STMicroelectronics, Infineon Technologies, ROHM Semiconductor, and Mitsubishi Electric, and how are these market participants managing the simultaneous execution risks of multi-billion-dollar manufacturing capacity expansion programs, automotive customer qualification processes of eighteen to thirty-six months, substrate supply concentration dependency on a small number of crystal growth specialists, and the medium-term oversupply risk arising from coordinated capacity investment across multiple manufacturers within a compressed investment timeframe?

- How is the electric vehicle power semiconductor content per vehicle evolving as automotive platforms transition from silicon insulated-gate bipolar transistor traction inverters to silicon carbide traction inverters, adopt 800-volt battery architectures requiring higher voltage-rated devices, integrate gallium nitride-based onboard chargers and DC-DC converters, and expand electrification across chassis, thermal management, and auxiliary systems, and what are the total power semiconductor content value projections per vehicle platform across battery electric, plug-in hybrid, full hybrid, and 48-volt mild hybrid configurations from the major automotive original equipment manufacturers through 2034, and at what silicon carbide device cost reduction milestones does silicon carbide traction inverter adoption achieve universal penetration across all battery electric vehicle segments including cost-sensitive entry-level platforms?

- What are the implications of the United States CHIPS and Science Act, European Union Chips Act, Japan semiconductor manufacturing revival programs, India semiconductor incentive scheme, and China’s domestic semiconductor industry development investments for the geographic distribution of power semiconductor fabrication capacity through 2034, and how are the associated government-incentivized manufacturing capacity additions outside of established Asian production clusters affecting power semiconductor manufacturing cost structures, device average selling prices, supply chain regionalization strategies of major automotive and industrial customers, and the competitive positioning of integrated device manufacturers operating both in government-incentivized Western geographies and established lower-cost Asian manufacturing locations?

- What are the technical performance benchmarks, application suitability profiles, current commercial adoption stage, key customer qualification activity, average selling price premium relative to silicon, and five-year adoption trajectory of gallium nitride power semiconductors across data center voltage regulator modules, electric vehicle onboard chargers, fast charging stations, solar microinverters, telecommunications base station power supplies, and industrial power conversion applications, and which gallium nitride technology platform including enhancement-mode gallium nitride on silicon, gallium nitride on silicon carbide, and integrated gallium nitride power ICs from leading developers including Navitas Semiconductor, GaN Systems, Infineon Technologies, Texas Instruments, and Transphorm is best positioned to achieve the cost, reliability, and integration level required for high-volume adoption in each application segment through 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Semiconductor Supply Chain, Wafer Substrate & Raw Material Concentration Risk

- Geopolitical, Export Control & Technology Decoupling Risk

- Technology Transition & Wide Bandgap Adoption Rate Risk

- Market Cyclicality, Inventory Correction & Demand Volatility Risk

- Manufacturing Yield, Reliability & Product Qualification Risk

- Regulatory Framework & Standards

- Semiconductor Export Controls, Foreign Direct Investment Restrictions & Strategic Technology Designation Frameworks (US CHIPS Act, EU Chips Act, Japan & South Korea Policy)

- Energy Efficiency Standards, Minimum Energy Performance Standards (MEPS) & Ecodesign Regulations Driving Power Semiconductor Adoption in End-Use Equipment

- EV & Charging Infrastructure Safety, EMC & Qualification Standards Applicable to Power Semiconductor Devices and Modules

- Automotive Functional Safety (ISO 26262), AEC-Q101/Q100 & IATF 16949 Qualification Standards for Automotive-Grade Power Semiconductors

- Conflict Mineral, REACH, RoHS & Environmental Compliance Regulations for Power Semiconductor Packaging & Substrate Materials

- Global Power Semiconductor Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped)

- Market Size & Forecast by Device Type

- Power MOSFET (Metal-Oxide-Semiconductor Field-Effect Transistor)

- IGBT (Insulated Gate Bipolar Transistor) Discrete & Module

- Power Diode (Rectifier, Schottky, Fast Recovery & Zener)

- Thyristor (SCR, TRIAC, GTO & IGCT)

- Power Bipolar Junction Transistor (BJT)

- Silicon Carbide (SiC) MOSFET & Schottky Barrier Diode (SBD)

- Gallium Nitride (GaN) HEMT & Power IC

- Intelligent Power Module (IPM) & Power Electronic Module

- Market Size & Forecast by Semiconductor Material

- Silicon (Si) Power Semiconductors

- Silicon Carbide (SiC) Wide Bandgap Power Semiconductors

- Gallium Nitride (GaN) Wide Bandgap Power Semiconductors

- Gallium Oxide (Ga2O3) Ultra-Wide Bandgap Power Semiconductors (Emerging)

- Diamond-Based Ultra-Wide Bandgap Power Semiconductors (Research Stage)

- Market Size & Forecast by Voltage Rating

- Low Voltage (Below 200V)

- Medium Voltage (200V to 900V)

- High Voltage (900V to 3.3 kV)

- Very High Voltage (Above 3.3 kV)

- Market Size & Forecast by Packaging Type

- Discrete Through-Hole Package (TO-247, TO-220, TO-3P)

- Discrete Surface Mount Package (D2PAK, DPAK, SOT-23, DFN)

- Standard Power Module (half-bridge, full-bridge, chopper & boost)

- Intelligent Power Module (IPM) with Gate Driver & Protection

- Custom & High-Power Press-Pack Module

- Chip-Scale Package (CSP), Wafer-Level Package (WLP) & Embedded Die Package

- Market Size & Forecast by Application

- Electric Vehicles (EV) & Hybrid Electric Vehicles (HEV): Inverter, On-Board Charger & DC-DC Converter

- EV Charging Infrastructure (AC Wallbox, DC Fast Charger & Ultra-Fast Charger)

- Industrial Motor Drives, Variable Speed Drives (VSD) & Industrial Automation

- Renewable Energy (Solar PV Inverter, Wind Turbine Converter & Energy Storage PCS)

- Consumer Electronics & Home Appliances (SMPS, PFC & Motor Control)

- Data Centre, Telecom & Server Power Supply (UPS, HVDC & POL Converter)

- Power Grid & Smart Grid (HVDC Transmission, STATCOM, Solid-State Transformer)

- Railways & Mass Transit (Traction Inverter, Auxiliary Converter & Battery Management)

- Industrial Welding, Induction Heating & Power Supply

- Aerospace, Defence & Medical Power Electronics

- Market Size & Forecast by End-User

- Automotive OEM & Tier-1 Supplier

- Industrial Equipment Manufacturer

- Consumer Electronics & Appliance OEM

- Renewable Energy System Integrator & Inverter Manufacturer

- Data Centre & Telecom Infrastructure Operator

- Railway & Mass Transit Equipment Manufacturer

- Market Size & Forecast by Sales Channel

- Direct OEM Supply (Long-Term Volume Supply Agreement)

- Authorised Distributor & Franchise Distributor Network

- Independent Distributor & Spot Market Channel

- Online B2B Electronic Component Marketplace

- North America Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Power Semiconductor Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Device Type

- By Semiconductor Material

- By Voltage Rating

- By Packaging Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Netherlands, Sweden, Switzerland, China, Japan, South Korea, Taiwan, India, Singapore, Malaysia, Thailand, Vietnam, Australia, Brazil, Israel, Saudi Arabia, UAE

- Technology Landscape & Innovation Analysis

- Silicon Carbide (SiC) Power Device Technology Deep-Dive

- Gallium Nitride (GaN) Power Device & Power IC Technology

- Silicon Power MOSFET & IGBT Technology (Superjunction, Trench & Field-Stop)

- Power Module Packaging, Substrate & Advanced Assembly Technology

- Wide Bandgap Wafer Growth, Substrate Manufacturing & Defect Reduction Technology

- Gate Driver, Protection Circuit & Intelligent Power Module Integration Technology

- Thermal Management, Heat Sink & Cooling Technology for High-Power Semiconductor Devices

- Patent & IP Landscape in Power Semiconductor Technologies

- Value Chain & Supply Chain Analysis

- Raw Material & Substrate Supply Chain (SiC Boule, GaN Epitaxy, Silicon Wafer, Copper & Substrate)

- Wafer Fabrication (Front-End) & Epitaxial Layer Equipment Supply Chain

- Back-End Assembly, Test, Packaging & Module Manufacturing Supply Chain

- Integrated Device Manufacturer (IDM), Fabless & Foundry Landscape

- Authorised Distributor, Independent Distributor & Value-Added Reseller Channel

- OEM & Systems Integration Procurement, Qualification & Design-In Process

- End-of-Life, RoHS Compliance, Returns & Counterfeit Mitigation

- Pricing Analysis

- Silicon Power MOSFET & IGBT Discrete Device Average Selling Price (ASP) Analysis

- SiC MOSFET & SiC Schottky Diode Pricing vs. Silicon Equivalent: Premium Analysis & Cost Reduction Roadmap

- GaN HEMT & GaN Power IC Pricing Analysis: Cost Parity with Silicon Trajectory

- Standard & Intelligent Power Module (IPM) Pricing Analysis by Power Rating & Application

- Distributor Mark-Up, Spot Market Premium & Long-Term Volume Contract Discount Analysis

- Total System Cost Comparison: Wide Bandgap vs. Silicon Power Stage for EV, Solar & Industrial Applications

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Silicon vs. SiC vs. GaN Power Semiconductor Manufacturing: Carbon Footprint & Energy Intensity Comparison

- System-Level Energy Efficiency Gains from Wide Bandgap Adoption: Quantifying CO2 Reduction in EV, Renewable Energy & Industrial Motor Drive Applications

- Conflict Mineral, Critical Material & ESG Supply Chain Due Diligence for Power Semiconductor Substrates & Packaging

- Semiconductor Manufacturing Water Consumption, Chemical Waste & Environmental Compliance

- Regulatory-Driven Sustainability: RoHS, REACH, EU Taxonomy & Green Electronics Procurement Policy Impact on Power Semiconductor Design & Supply Chain

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Device Type & Material)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Device Type, Semiconductor Material & Geography

- Player Classification

- Global Integrated Device Manufacturers (IDMs) with Full Device & Module Portfolio

- SiC Specialist Power Semiconductor Manufacturers

- GaN Specialist Power Semiconductor & Power IC Companies

- Fabless Power Semiconductor Design Companies

- Power Module & Intelligent Power Module Specialists

- Foundry & Contract Wafer Fabrication Service Providers for Power Semiconductors

- SiC & GaN Wafer, Substrate & Epitaxial Wafer Suppliers

- Authorised & Independent Distributor & Value-Added Reseller Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Device Type, Semiconductor Material & Region

- Company Profile

- Company Overview & Headquarters

- Power Semiconductor Products & Technology Portfolio

- Key OEM Customer Relationships & Design-Win Pipeline

- Manufacturing Footprint, Wafer Fab Capacity & Packaging Assembly

- Revenue (Power Semiconductor Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Product Launches, Customer Wins)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Device Type, Semiconductor Material, Voltage Rating, Application & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & OEM Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)