Market Definition

The North America Predictive Maintenance for Logistics Fleets Market encompasses the development, deployment, and managed operation of data-driven maintenance intelligence systems that continuously monitor the mechanical, electrical, and operational condition of commercial trucking fleets, last-mile delivery vehicles, intermodal rail assets, warehouse material handling equipment, and associated logistics infrastructure to anticipate component failure events before they occur, enabling fleet operators and maintenance organizations to schedule proactive interventions that prevent unplanned downtime, reduce total maintenance expenditure, extend asset service life, and improve the safety and regulatory compliance of logistics fleet operations across the United States, Canada, and Mexico. Predictive maintenance for logistics fleets applies a spectrum of sensing, data acquisition, machine learning, and decision-support technologies to transform the traditional reactive and schedule-based preventive maintenance paradigms that have historically governed commercial fleet upkeep into condition-based, data-driven maintenance workflows whose intervention timing is determined by the actual measured deterioration state of each individual asset rather than by fixed mileage, time, or calendar intervals that are inevitably either too frequent, generating unnecessary cost, or too infrequent, missing developing failure conditions.

The market encompasses onboard telematics and electronic logging device platforms generating continuous vehicle operational data streams; engine and drivetrain condition monitoring systems using vibration analysis, oil quality sensing, and thermal imaging; tire pressure and wear monitoring systems; brake system health monitors; battery state-of-health monitoring for electric and hybrid logistics vehicles; predictive analytics software platforms applying machine learning algorithms to multi-source sensor data streams to generate failure probability scores, remaining useful life estimates, and maintenance work order recommendations; fleet management information system integrations enabling predictive maintenance alerts to be translated into workshop scheduling, parts procurement, and driver notification workflows; and professional services including system integration, data science consulting, and managed analytics services supporting fleet operator adoption and continuous improvement of predictive maintenance programs. Key participants include commercial vehicle OEMs embedding predictive maintenance capabilities within connected vehicle platforms, telematics and fleet management software providers, independent predictive analytics software developers, aftermarket sensor and diagnostic hardware suppliers, fleet management outsourcing companies, and the trucking, parcel delivery, e-commerce fulfillment, and intermodal logistics operators whose maintenance cost reduction imperatives and safety compliance obligations define the commercial demand structure of this market.

Market Insights

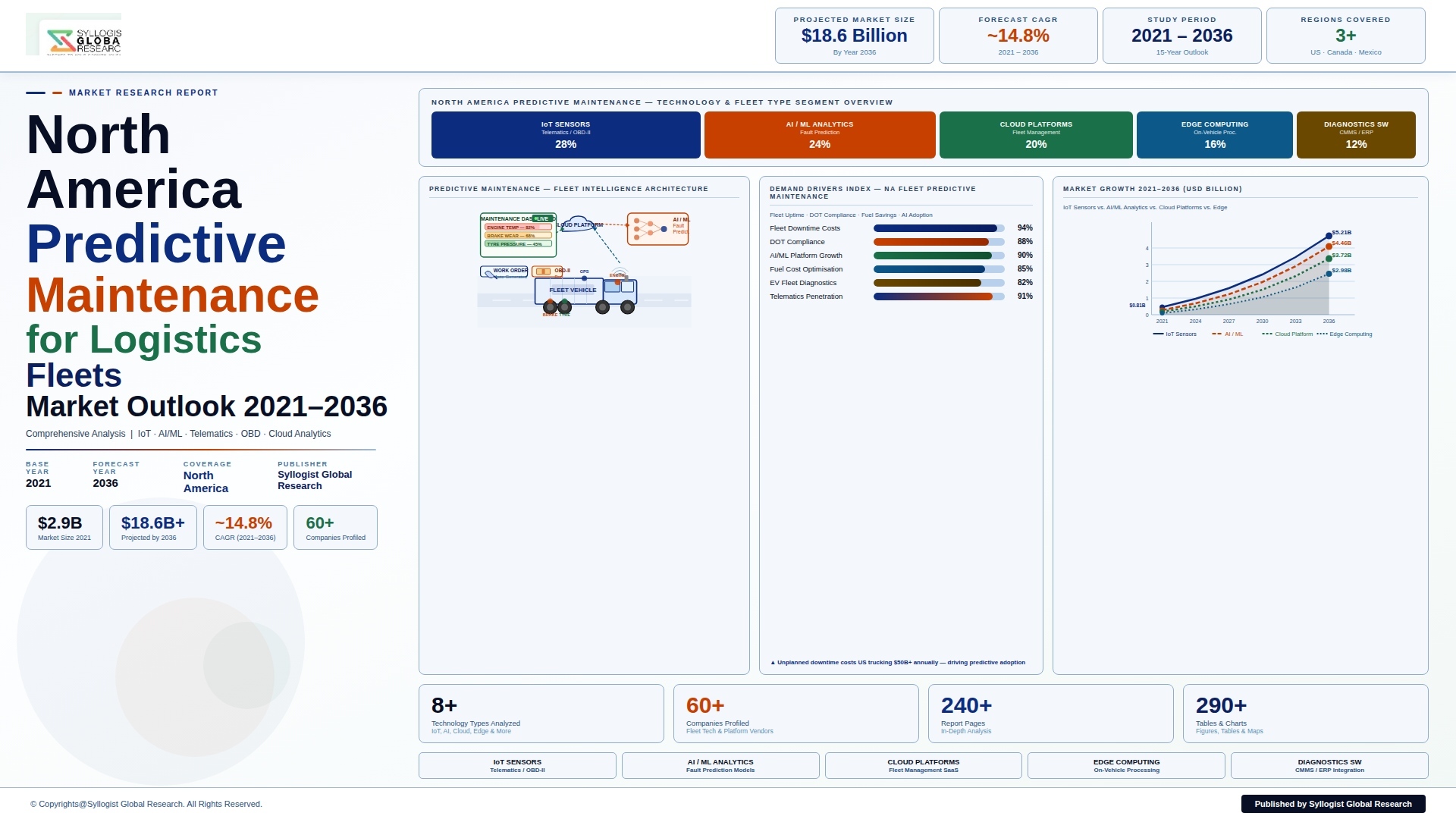

The North America predictive maintenance for logistics fleets market is experiencing a structural demand acceleration rooted in the simultaneous pressure of driver shortage economics that make each unplanned breakdown event disproportionately costly in terms of service disruption, customer penalty exposure, and recovery logistics complexity, the progressive connectivity maturation of the North American commercial vehicle fleet through mandated electronic logging device adoption creating a ubiquitous data infrastructure foundation for predictive analytics, and the entry of AI-native software platform providers whose machine learning model sophistication and cloud computing cost efficiency are delivering actionable failure prediction capabilities at price points accessible to mid-market fleet operators who were historically unable to justify the enterprise software investment required by first-generation predictive maintenance platforms. The North America predictive maintenance for logistics fleets market was valued at approximately USD 1.8 billion in 2025 and is projected to reach USD 4.6 billion by 2034, advancing at a compound annual growth rate of 10.9% over the forecast period from 2027 to 2034, driven by the expanding deployment of connected vehicle telematics across the region’s 3.6 million registered commercial trucks, the growing integration of predictive maintenance analytics within fleet management platforms adopted by parcel delivery, less-than-truckload, full truckload, and dedicated contract carriage operators, and the accelerating adoption of electric commercial vehicles whose battery and powertrain health monitoring requirements create new and technically demanding predictive maintenance application categories.

The commercial trucking segment constitutes the largest and most commercially mature application within the North American predictive maintenance for logistics fleets market, accounting for approximately 54% of total market revenue in 2025, driven by the extraordinary financial consequences of unplanned Class 8 truck breakdowns whose average per-incident cost, including roadside repair, towing, driver downtime, load rerouting, customer penalty exposure, and fleet utilization loss, has been documented at USD 3,000 to USD 17,000 per event depending on breakdown location, component failure type, and cargo criticality, creating a commercially compelling return on investment case for predictive maintenance technology deployment whose prevention of even a small number of breakdown events per truck per year generates payback periods of six to eighteen months on typical system investment levels. Daimler Trucks North America’s Detroit Connect platform, Volvo Trucks’ Uptime Services connected maintenance program, Navistar’s OnCommand Connection telematics suite, and Paccar’s PACCARConnect system each deliver predictive fault detection capabilities to their respective installed commercial vehicle fleet bases, leveraging the proprietary engine and powertrain sensor data architectures embedded in their connected vehicle platforms to generate failure predictions whose specificity and lead time exceed what aftermarket telematics systems can deliver from external OBD-II and J1939 data streams alone. The less-than-truckload segment, operating high-density multi-stop daily delivery cycles with rigid linehaul departure schedules whose adherence is critically dependent on vehicle availability, has demonstrated particularly strong predictive maintenance adoption rates among national LTL carriers including FedEx Freight, Old Dominion Freight Line, and XPO Logistics, whose terminal-based maintenance operations benefit directly from the advance scheduling visibility that failure predictions with 24-to-72-hour lead times provide over the reactive breakdown management paradigm that previously dominated LTL fleet maintenance.

The last-mile delivery fleet segment, encompassing the hundreds of thousands of step vans, cargo vans, and medium-duty delivery trucks operated by UPS, FedEx, Amazon Logistics, DHL Supply Chain, and regional parcel carriers across North American urban and suburban delivery networks, represents the most rapidly expanding adoption category within the predictive maintenance for logistics fleets market, driven by the extraordinary operational pressure on last-mile delivery assets that must complete 100 to 200 delivery stops per day in stop-and-go urban driving conditions generating accelerated brake, transmission, and engine wear rates that make condition-based maintenance timing substantially more economical than fixed-interval servicing. Amazon’s investment in predictive maintenance technology for its Amazon Delivery Service Partner program, whose 100,000-plus delivery van fleet represents one of the largest single commercial vehicle fleets in North America, has generated substantial market momentum through the development of proprietary telematics and predictive analytics capabilities that are simultaneously improving fleet reliability and reducing per-vehicle maintenance cost at a scale that demonstrates predictive maintenance ROI with a statistical robustness unavailable from smaller fleet implementations. The accelerating electrification of last-mile delivery fleets, with Amazon having deployed over 20,000 Rivian electric delivery vans and UPS operating a growing fleet of electric vehicles from BrightDrop and other manufacturers, is creating a structurally new and technically demanding predictive maintenance application category centered on battery state-of-health monitoring, thermal management system performance prediction, regenerative braking system condition assessment, and charging infrastructure optimization that requires purpose-built predictive analytics models trained on electric vehicle operational data whose accumulation is still in early stages relative to the mature failure prediction model libraries available for diesel powertrain applications.

The integration of predictive maintenance capabilities within broader fleet management platform ecosystems is defining the competitive architecture of the North American market, as fleet operators increasingly prefer consolidated technology platforms that deliver predictive maintenance alerts, driver behavior monitoring, route optimization, fuel efficiency management, regulatory compliance documentation, and maintenance workflow management within a unified operational interface rather than deploying separate point solutions for each fleet management function. Samsara, Motive, Verizon Connect, Geotab, and Trimble Fleet Management have each developed predictive maintenance modules within their comprehensive fleet management platforms that leverage the continuous telematics data streams their systems generate to apply machine learning failure prediction models without requiring additional hardware investment beyond the telematics devices fleet operators have already deployed for ELD compliance and fleet visibility purposes, creating a commercially compelling upgrade pathway that is driving predictive maintenance adoption among the large installed base of telematics platform subscribers. The warehouse and distribution center material handling equipment segment, encompassing forklifts, automated guided vehicles, conveyor systems, and sortation equipment at the approximately 23,000 fulfillment and distribution centers operating across North America, is emerging as a significant adjacent market for predictive maintenance technology whose application to high-utilization warehouse assets operating in tightly orchestrated automated workflows generates downtime cost consequences comparable to or exceeding those of over-the-road truck breakdowns, and whose sensor-rich operational environments provide ideal predictive maintenance data collection conditions.

Key Drivers

Mandatory Electronic Logging Device Adoption Creating Ubiquitous Vehicle Data Infrastructure Enabling Fleet-Wide Predictive Analytics Deployment

The Federal Motor Carrier Safety Administration’s Electronic Logging Device mandate, which required the adoption of FMCSA-registered ELD devices by virtually all commercial motor carriers operating in the United States by December 2019 and has been progressively enforced through roadside inspection and carrier audit programs since, created a foundational connected vehicle data infrastructure across the North American commercial trucking fleet that simultaneously satisfies hours of service regulatory compliance requirements and generates continuous vehicle operational data streams whose analytical value extends substantially beyond regulatory compliance into predictive maintenance, fuel efficiency optimization, and driver performance management applications. The universal ELD deployment baseline means that North American fleet operators who have not yet adopted predictive maintenance analytics are already generating the vehicle sensor data streams required by most commercial predictive maintenance platforms through their existing ELD infrastructure, eliminating the hardware deployment cost and organizational change management barrier that historically limited predictive maintenance adoption to large fleets with the capital resources to invest in dedicated telematics hardware programs. The progressive upgrade of ELD hardware generations toward higher-bandwidth, multi-sensor telematics gateway devices capable of capturing J1939 CAN bus data at higher polling frequencies, integrating with additional body electronics and auxiliary sensor channels, and transmitting real-time data streams to cloud analytics platforms is continuously improving the predictive maintenance signal quality available from ELD-based data infrastructure, enabling more precise failure prediction models with longer advance notice windows that directly translate into improved maintenance scheduling efficiency and reduced breakdown incidence for fleet operators who have deployed predictive analytics on their ELD data streams.

Escalating Commercial Vehicle Driver Shortage and Fleet Utilization Pressure Making Unplanned Downtime Economically Intolerable for North American Trucking Operators

The structural commercial truck driver shortage in North America, with the American Trucking Associations estimating a deficit of approximately 64,000 drivers in 2025 that is projected to grow to over 82,000 by 2030 as driver demographic aging accelerates retirements faster than new driver licensing programs can replace them, has fundamentally elevated the commercial cost of unplanned vehicle breakdowns by eliminating the driver slack that previously allowed fleet operators to reassign available drivers to cover breakdown-affected loads without significant service disruption or customer penalty exposure, making each vehicle unavailability event directly chargeable against customer service commitments and carrier financial performance at a cost magnitude that substantially exceeds the vehicle repair cost alone. The freight rate volatility and carrier margin compression experienced across North American truckload and LTL markets since 2022, arising from the post-pandemic demand normalization that reduced spot market freight rates while carrier operating costs including fuel, insurance, equipment, and labor continued to escalate, has intensified fleet operator focus on controllable cost reduction programs of which predictive maintenance represents one of the highest-return investment opportunities given that maintenance and repair costs typically constitute 8% to 12% of total carrier operating cost and that predictive maintenance programs have documented total maintenance cost reductions of 15% to 25% across verified implementation case studies at North American fleet operators of various scales. The Hours of Service regulatory framework governing commercial driver working time limits amplifies the downtime cost of breakdowns occurring during active linehaul operations by consuming driver HOS availability during roadside wait and repair time that cannot be recovered, directly reducing driver productivity and revenue generation capacity for the affected trip and potentially subsequent trips within the 70-hour weekly HOS window.

Electric Commercial Vehicle Fleet Expansion Creating New Battery Health Monitoring and Powertrain Predictive Maintenance Requirements With Premium Technology Demand

The accelerating electrification of North American commercial vehicle fleets, driven by California’s Advanced Clean Trucks regulation mandating zero-emission vehicle sales percentages for commercial vehicle manufacturers beginning in 2024 and progressively extending to 18 additional states adopting California emissions standards, combined with fleet operator sustainability commitments and the total cost of ownership improvements achievable through electric vehicle operating cost advantages in high-utilization urban and suburban delivery cycle applications, is creating a structurally new and premium-value predictive maintenance application category whose battery state-of-health monitoring, thermal management system prediction, and electric drivetrain condition assessment requirements cannot be satisfied by the diesel powertrain-optimized predictive maintenance models and sensor architectures that characterize the current generation of commercial fleet predictive maintenance platforms. The battery pack represents the highest-value and most operationally critical component of an electric commercial vehicle, with Class 6 and Class 7 electric truck battery systems valued at USD 80,000 to USD 180,000 per vehicle, whose remaining useful life, capacity degradation trajectory, thermal management performance, and cell-level health status directly determine vehicle range capability, charging cycle efficiency, and the financial timing of battery replacement obligations that represent the largest single maintenance cost event in the electric vehicle lifecycle. Purpose-built electric vehicle predictive maintenance platforms from technology developers including SparkCognition, Flux Power, and Xos Trucks, alongside OEM-integrated battery management systems from Daimler’s eCascadia and Freightliner eCanter platforms and PACCAR’s Kenworth T680E and Peterbilt 579EV electric trucks, are establishing the commercial and technical foundations of an electric fleet predictive maintenance segment whose per-vehicle system value and technical sophistication substantially exceed the equivalent diesel fleet predictive maintenance market, driving above-average revenue growth in the electrification-linked segment of the broader market.

Key Challenges

Data Integration Complexity Across Heterogeneous Multi-OEM Fleet Compositions and Legacy Telematics Infrastructure Limiting Predictive Model Accuracy

The majority of North American commercial logistics fleet operators manage heterogeneous vehicle populations comprising multiple OEM brands, engine generations, body configurations, and telematics hardware generations whose data protocols, sensor channel availability, diagnostic trouble code vocabularies, and connectivity architectures vary materially across vehicle makes and model years, creating a data integration complexity challenge that requires predictive maintenance platform providers to maintain extensive multi-OEM data normalization, diagnostic code mapping, and sensor calibration libraries whose development and ongoing maintenance represents a significant ongoing engineering investment that constrains the speed of new vehicle platform onboarding and limits the failure prediction model accuracy achievable from multi-OEM fleet data streams relative to single-OEM fleet environments. The coexistence within large fleet operator environments of vehicles connected through legacy serial telematics devices generating low-frequency J1939 data snapshots, modern gateway telematics platforms delivering high-frequency multi-channel CAN bus data, OEM connected vehicle platforms transmitting proprietary telemetry through manufacturer cloud backends, and unconnected older vehicles requiring manual odometer and fault code data entry creates a data quality stratification within the same fleet that forces predictive maintenance platforms to operate with inconsistent signal availability, timing resolution, and feature set coverage across individual fleet assets, generating prediction model accuracy disparities between well-connected and poorly connected vehicle populations that create uneven value delivery and user experience inconsistency for fleet operators seeking uniform maintenance intelligence coverage across their entire asset base. The ELD mandate’s minimum data transmission standards, designed for hours of service regulatory compliance rather than predictive maintenance analytics, do not require the high-frequency multi-parameter vehicle health data streams that deliver the most actionable predictive maintenance signals, meaning that carriers who have deployed minimum-specification ELD devices to achieve regulatory compliance generate data of insufficient richness for high-accuracy failure prediction without additional hardware investment.

Change Management Resistance and Maintenance Technician Workforce Adoption Barriers Limiting Operational Value Realization From Predictive Maintenance Platform Investments

The operational value of predictive maintenance technology deployment in logistics fleet environments is critically dependent on the adoption and workflow integration of predictive maintenance alerts and recommendations by fleet maintenance managers, shop foremen, and technician workforces whose established reactive and schedule-based maintenance cultures, tool and system familiarity preferences, and professional identity as hands-on diagnostic experts rather than data analytics consumers create substantial organizational change management challenges that technology deployment alone cannot resolve and that represent the primary cause of the performance gap between the theoretical maintenance cost savings demonstrated in vendor case studies and the actual savings realized in typical fleet operator deployments. The commercial truck technician shortage, which mirrors the driver shortage in severity with industry estimates suggesting a deficit of over 28,000 qualified diesel technicians across North America, means that fleet maintenance organizations are already operating under significant workforce capacity constraints that limit their ability to dedicate maintenance planning time and scheduling flexibility to the condition-based work order management that predictive maintenance systems require, potentially reducing the operational benefit of failure advance warnings if the workshop capacity to act on those warnings within the recommended intervention timeframe is insufficient due to technician unavailability. The trust calibration challenge, arising from the false positive failure predictions that inevitably occur in early-stage predictive model deployments before sufficient fleet-specific operational data has accumulated to refine model accuracy, generates maintenance manager skepticism that can undermine program adoption if initial prediction accuracy levels are insufficient to demonstrate clear differentiation from the existing maintenance scheduling intuition that experienced fleet managers have developed through years of hands-on fleet operational experience.

Cybersecurity Vulnerabilities in Connected Fleet Telematics Infrastructure Creating Data Privacy and Operational Security Risks for Logistics Operators

The extensive connectivity of predictive maintenance-enabled logistics fleet telematics systems, which continuously transmit sensitive vehicle operational data, location information, cargo status, driver behavioral data, and maintenance condition information through cellular networks to cloud analytics platforms operated by third-party technology vendors, creates a cybersecurity attack surface whose exploitation by malicious actors could compromise fleet operator competitive intelligence, expose shipper cargo routing and inventory data to unauthorized access, enable vehicle remote system interference through compromised telematics gateways, or disrupt fleet management operations through ransomware attacks targeting fleet management information systems that integrate predictive maintenance platforms. The National Motor Freight Traffic Association’s cybersecurity guidance for motor carriers and the Commercial Vehicle Safety Alliance’s connected vehicle security recommendations have raised industry awareness of telematics cybersecurity risk, but the implementation of comprehensive cybersecurity measures including end-to-end encryption of vehicle data transmissions, multi-factor authentication for fleet management platform access, penetration testing of telematics hardware and software interfaces, and incident response planning for connected vehicle cybersecurity events remains inconsistent across North American fleet operators, with smaller carriers in particular lacking the IT security expertise and budget to implement cybersecurity programs commensurate with their connected vehicle data exposure. The third-party data sharing arrangements embedded in many predictive maintenance platform commercial agreements, which grant technology vendors broad rights to aggregate and analyze fleet operator vehicle data for model training, benchmark reporting, and product development purposes, create data governance concerns for fleet operators who view their operational data as a competitive asset and who are increasingly evaluating vendor data handling practices as a procurement criterion alongside predictive accuracy and platform functionality in their technology selection decisions.

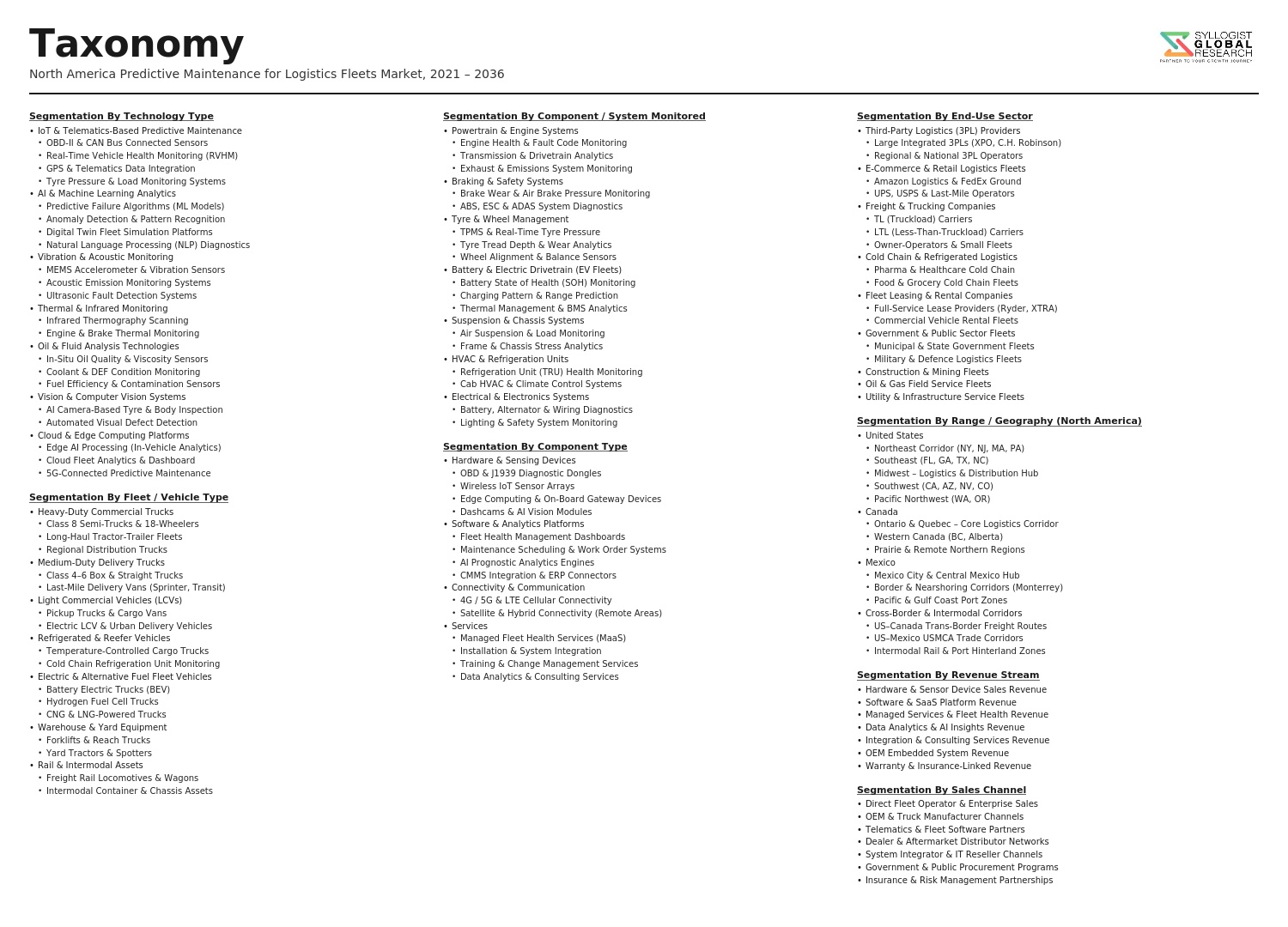

Market Segmentation

- Segmentation By Fleet Type

- Class 8 Long-Haul Trucking Fleets

- Less-Than-Truckload (LTL) and Regional Trucking Fleets

- Last-Mile and Parcel Delivery Fleets

- Dedicated Contract Carriage Fleets

- Refrigerated and Specialty Cargo Fleets

- Intermodal and Rail Logistics Fleets

- Warehouse and Distribution Center Material Handling Equipment

- Electric and Hybrid Commercial Vehicle Fleets

- Others

- Segmentation By Component

- Onboard Telematics Hardware and ELD Platforms

- Engine and Powertrain Condition Monitoring Systems

- Tire Pressure and Wear Monitoring Systems

- Brake System Health Monitoring

- Battery State-of-Health Monitoring (EV and Hybrid)

- Transmission and Drivetrain Sensors

- Predictive Analytics and AI Software Platforms

- Fleet Management System Integration Middleware

- Professional Services (Integration, Consulting, Managed Analytics)

- Others

- Segmentation By Technology

- Machine Learning and AI-Based Failure Prediction Models

- IoT Sensor Networks and Remote Condition Monitoring

- Digital Twin and Asset Simulation Platforms

- Natural Language Processing for Maintenance Record Analysis

- Edge Computing for Real-Time Onboard Diagnostics

- Computer Vision for Visual Inspection Automation

- Others

- Segmentation By Deployment Model

- Cloud-Based SaaS Predictive Maintenance Platforms

- On-Premise Fleet Management System Integration

- OEM-Integrated Connected Vehicle Maintenance Programs

- Managed Service and Outsourced Analytics Models

- Others

- Segmentation By Fleet Size

- Small Fleets (Below 50 Vehicles)

- Mid-Size Fleets (50 to 500 Vehicles)

- Large Fleets (500 to 5,000 Vehicles)

- Enterprise Mega-Fleets (Above 5,000 Vehicles)

- Others

- Segmentation By End User

- Truckload and LTL Carriers

- Parcel and Express Delivery Companies

- E-Commerce Fulfillment and Last-Mile Operators

- Third-Party Logistics (3PL) Providers

- Private Fleet Operators (Retail, Food and Beverage, Manufacturing)

- Fleet Leasing and Fleet Management Outsourcing Companies

- Intermodal and Rail Freight Operators

- Others

- Segmentation By Country

- United States

- Canada

- Mexico

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the North America Predictive Maintenance for Logistics Fleets Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by fleet type, component, technology, deployment model, fleet size, end user, and country, to enable telematics providers, predictive analytics software developers, commercial vehicle OEMs, fleet management service companies, and investors to identify which technology categories and fleet operator segments will generate the highest absolute revenue and the most commercially defensible demand growth across the forecast period?

- What is the documented and projected financial return on investment from predictive maintenance program deployment across Class 8 long-haul, LTL, and last-mile delivery fleet categories in North America, including quantified reductions in unplanned breakdown frequency, total maintenance cost per mile, tire and brake component replacement cost, vehicle downtime days per year, and roadside service call incidence, and how do these ROI outcomes vary by fleet size, vehicle age, operating cycle intensity, and predictive maintenance platform sophistication level?

- How is the electrification of commercial delivery and logistics fleets across North America, driven by California Advanced Clean Trucks regulation adoption, Amazon and UPS electric vehicle deployment programs, and PACCAR and Daimler electric truck commercial launches, creating new battery state-of-health monitoring, thermal management prediction, and electric drivetrain condition assessment requirements that differ fundamentally from diesel fleet predictive maintenance needs, and which technology providers are best positioned to capture the premium predictive maintenance segment associated with electric commercial vehicle fleet growth through 2034?

- How are the leading telematics and fleet management platform providers including Samsara, Motive, Geotab, Verizon Connect, and Trimble incorporating predictive maintenance capabilities within their consolidated fleet management platform offerings, what is the competitive differentiation between OEM-integrated predictive maintenance programs from Daimler, Volvo, Navistar, and PACCAR versus independent telematics platform-based predictive analytics, and how is the market share balance between OEM-captive and independent predictive maintenance solutions expected to evolve through 2034 as electric vehicle OEM connectivity platforms deliver richer proprietary sensor data than aftermarket telematics can access?

- Who are the leading predictive maintenance technology providers, commercial vehicle telematics companies, fleet management software platforms, AI analytics specialists, and managed maintenance service operators currently defining the competitive landscape of the North America predictive maintenance for logistics fleets market, and what are their respective technology platform capabilities, fleet type coverage breadth, AI model accuracy benchmarks and failure prediction lead time performance, data integration coverage across multi-OEM fleet compositions, pricing and deployment models, customer base scale and retention, and strategic investment priorities in electric vehicle predictive maintenance, digital twin development, and edge computing deployment through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Integration Complexity, Legacy Telematics Incompatibility & Fleet Management System Migration Risk

- Cybersecurity, Connected Vehicle Data Privacy & OBD / CAN Bus Vulnerability Risk for Fleet Operators

- AI Model Accuracy, False Positive Alert Fatigue & Technician Trust Deficit Risk in Predictive Maintenance Adoption

- High Upfront Investment, ROI Demonstration Gap & SME Fleet Operator Affordability Risk

- EV Fleet Transition, Powertrain Complexity Shift & Predictive Maintenance Model Retraining Risk for Logistics Fleets

- Regulatory Framework & Standards

- FMCSA Hours-of-Service, ELD Mandate & Commercial Vehicle Safety Regulations Creating Predictive Maintenance Data Infrastructure in North America

- US DOT & Transport Canada Vehicle Inspection, Out-of-Service Criteria & Fleet Safety Compliance Frameworks

- NHTSA & Transport Canada Connected Vehicle, OBD-II & Telematics Data Standards Applicable to Predictive Maintenance Systems

- California CARB Fleet Emission Compliance, Clean Truck Rules & Predictive Maintenance Role in Emission Control Verification

- CCPA, US State-Level Data Privacy Laws & Cross-Border Data Handling Regulations for Fleet Telematics & Predictive Maintenance Platforms

- North America Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Fleet Size (Number of Vehicles Monitored)

- Market Size & Forecast by Solution Type

- Predictive Maintenance Software & AI Analytics Platform

- Condition Monitoring & IoT Sensor Hardware

- Telematics & Connected Vehicle Data Integration Platform

- Prognostics & Health Management (PHM) System

- Remote Diagnostics & Over-the-Air (OTA) Vehicle Health Monitoring System

- Integrated Fleet Management & Predictive Maintenance Suite

- Managed Service & Predictive Maintenance-as-a-Service (PdMaaS)

- Market Size & Forecast by Component

- Hardware (OBD Dongles, IoT Sensors, Edge Computing Devices & Gateway Units)

- Software (AI & ML Analytics Engine, Dashboard, Alerting & Workflow Management)

- Connectivity & Communication Infrastructure (Cellular, 5G, Wi-Fi & Satellite)

- Professional Services (Implementation, Integration, Training & Consulting)

- Managed & Subscription Services (Ongoing Monitoring, Model Updates & Support)

- Market Size & Forecast by Technology

- Artificial Intelligence & Machine Learning-Based Fault Prediction

- IoT & Wireless Sensor Network-Based Condition Monitoring

- Digital Twin & Vehicle Simulation-Based Prognostics

- Telematics, GPS & CAN Bus Data Analytics

- Computer Vision & Thermal Imaging-Based Inspection Technology

- Vibration, Acoustic Emission & Oil Analysis-Based Diagnostics

- Market Size & Forecast by Fleet Type

- Heavy-Duty Long-Haul Trucking Fleets (Class 7 & 8 Trucks)

- Medium-Duty Regional & Distribution Delivery Fleets (Class 4 to 6 Trucks)

- Last-Mile Light Commercial Vehicle Fleets (Class 1 to 3 Vans & Pickups)

- Refrigerated & Temperature-Controlled (Reefer) Cargo Fleets

- Electric & Alternative Fuel Logistics Vehicle Fleets

- Intermodal, Drayage & Port Logistics Fleets

- Rail Freight & Intermodal Container Fleets

- Market Size & Forecast by Monitored Component

- Engine & Powertrain Health Monitoring

- Transmission & Drivetrain Monitoring

- Tyre Pressure & Wear Monitoring (TPMS & Predictive Tyre Health)

- Brake System & Foundation Brake Monitoring

- Battery & Electric Powertrain Health Monitoring (for EV Fleets)

- Suspension, Axle & Steering System Monitoring

- Refrigeration Unit & Temperature Control System Monitoring

- Market Size & Forecast by Deployment Mode

- Cloud-Based Predictive Maintenance Platform

- On-Premise & Edge-Deployed Predictive Maintenance System

- Hybrid Cloud & Edge Deployment

- Market Size & Forecast by End-User

- Third-Party Logistics (3PL) & Contract Logistics Providers

- Truckload (TL) & Less-Than-Truckload (LTL) Carriers

- Private Fleet Operators (Retail, FMCG & Manufacturing)

- Last-Mile Delivery & E-Commerce Fulfilment Operators

- Refrigerated & Cold Chain Logistics Operators

- Government & Public Sector Fleet Operators

- Fleet Leasing & Fleet Management Companies

- Market Size & Forecast by Sales Channel

- Direct Sales to Fleet Operators & Logistics Companies

- OEM & Vehicle Manufacturer Embedded Integration

- Fleet Management Software & Telematics Platform Partner Channel

- Value-Added Reseller (VAR) & System Integrator Channel

- Subscription & SaaS Marketplace Platform

- United States Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Canada Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Mexico Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Northeast & Mid-Atlantic United States Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Midwest & Great Lakes United States Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- State & Province-Wise* Predictive Maintenance for Logistics Fleets Market Outlook

- Market Size & Forecast

- By Value

- By Fleet Size (Number of Vehicles Monitored)

- By Solution Type

- By Component

- By Fleet Type

- By Deployment Mode

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Market Size & Forecast

- *Key States & Provinces Analyzed in the Syllogist Global Research Portfolio: California, Texas, Florida, New York, Illinois, Ohio, Pennsylvania, Georgia, Michigan, Tennessee, North Carolina, New Jersey, Arizona, Washington, Colorado, Ontario, Quebec, British Columbia, Alberta, Nuevo Leon, Jalisco, Mexico City

- Technology Landscape & Innovation Analysis

- AI & Machine Learning Fault Prediction Technology Deep-Dive: Supervised, Unsupervised & Reinforcement Learning Models for Fleet Diagnostics

- Digital Twin Technology for Logistics Vehicle Prognostics: Virtual Vehicle Model, Real-Time Synchronisation & Remaining Useful Life (RUL) Prediction

- Edge AI & On-Board Processing Technology: Real-Time Anomaly Detection, Reduced Latency & Bandwidth Optimisation for Fleet Predictive Maintenance

- 5G-Connected Fleet & V2X Communication Technology: High-Bandwidth Telematics, Remote Diagnostics & OTA Software Update Capability

- EV Fleet Predictive Maintenance Technology: Battery State-of-Health (SoH), Thermal Management & Electric Drivetrain Prognostics

- Computer Vision & Automated Vehicle Inspection Technology: Camera-Based Undercarriage, Tyre & Body Damage Detection

- Generative AI & Large Language Model (LLM) Technology for Fleet Maintenance Knowledge Management & Technician Decision Support

- Patent & IP Landscape in Predictive Maintenance Technologies for Logistics Fleets

- Value Chain & Supply Chain Analysis

- IoT Sensor, OBD Hardware & Edge Computing Device Manufacturing Supply Chain

- AI & ML Software Development, Model Training & Cloud Analytics Platform Supply Chain

- Telematics Module, Cellular Modem & Connectivity Infrastructure Supply Chain

- System Integration, Fleet Onboarding & Data Pipeline Development Supply Chain

- OEM & Vehicle Manufacturer Embedded Technology Partnership Channel

- Fleet Operator, 3PL & Logistics Company Direct Sales & Subscription Channel

- Aftermarket Service, Repair Shop Integration & Parts Procurement Optimisation Channel

- Pricing Analysis

- Predictive Maintenance SaaS Platform Per-Vehicle Per-Month Subscription Pricing Benchmarking Across North American Vendors

- IoT Hardware & OBD Sensor Kit Capital Cost & Total Cost of Ownership (TCO) Analysis

- Managed Predictive Maintenance Service Fee & Outcome-Based Pricing Model Analysis

- ROI Analysis: Downtime Reduction, Unplanned Repair Cost Saving & Fuel Efficiency Gain vs. Predictive Maintenance Investment

- EV Fleet Predictive Maintenance Premium Pricing vs. ICE Fleet Equivalent Cost Analysis

- Total Cost of Predictive Maintenance per Vehicle per Year Across Fleet Types & Deployment Models

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Predictive Maintenance Systems: Hardware Carbon Footprint, Data Centre Energy Use & Net Environmental Benefit

- Predictive Maintenance Contribution to Fleet Fuel Efficiency, Emission Reduction & CARB Clean Truck Compliance in North America

- EV Fleet Battery Longevity, State-of-Health Optimisation & Second-Life Battery Management Through Predictive Maintenance

- Predictive Maintenance Role in Reducing Fleet Parts Waste, Premature Component Replacement & Circular Logistics Economy

- Regulatory-Driven Sustainability, SDG 9 (Industry & Innovation), SDG 11 (Sustainable Cities) & SDG 13 (Climate Action) Alignment & ESG Fleet Reporting

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Solution Type & End-User)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Solution Type, Fleet Type & Country

- Player Classification

- Integrated Fleet Management & Telematics Platform Providers with Predictive Maintenance Modules

- Dedicated AI & Machine Learning Predictive Maintenance Software Vendors

- Commercial Vehicle OEMs with Embedded Predictive Maintenance & Remote Diagnostics Capability

- IoT Hardware, Sensor & Connected Vehicle Technology Providers

- Digital Twin & Simulation-Based Fleet Prognostics Specialists

- Managed Predictive Maintenance Service & PdMaaS Providers

- EV Fleet Health Monitoring & Battery Analytics Specialists

- Start-Ups & AI-Native Logistics Fleet Predictive Maintenance Ventures

- Competitive Analysis Frameworks

- Market Share Analysis by Solution Type, Fleet Type & Country

- Company Profile

- Company Overview & Headquarters

- Predictive Maintenance Products, Platform & Service Portfolio

- Key Customer Relationships & Reference Fleet Deployments in North America

- Fleet Vehicles Monitored, Geographic Footprint & Data Network Scale

- Revenue (Predictive Maintenance Segment) & Annual Recurring Revenue (ARR)

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Product Launches, Fleet Wins, Platform Updates)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (AI Capability vs. Fleet Coverage Scale)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Solution Type, Technology, Fleet Type, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output