Global Robotics-as-a-Service Business Models Market By Service Model, By Robot Type, By End Use Industry, By Application, By Enterprise Size, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Robotics-as-a-Service Business Models Market encompasses subscription-based, outcome-based, and usage-based commercial frameworks through which robotic hardware, software, maintenance, connectivity, and operational support services are delivered to enterprise customers as integrated managed service contracts rather than capital asset purchases, enabling organizations to deploy industrial robots, collaborative robots, autonomous mobile robots, service robots, and drone systems across manufacturing, logistics, healthcare, agriculture, and retail applications without direct ownership of robotic capital assets or in-house robotics engineering capability.

Market Insights

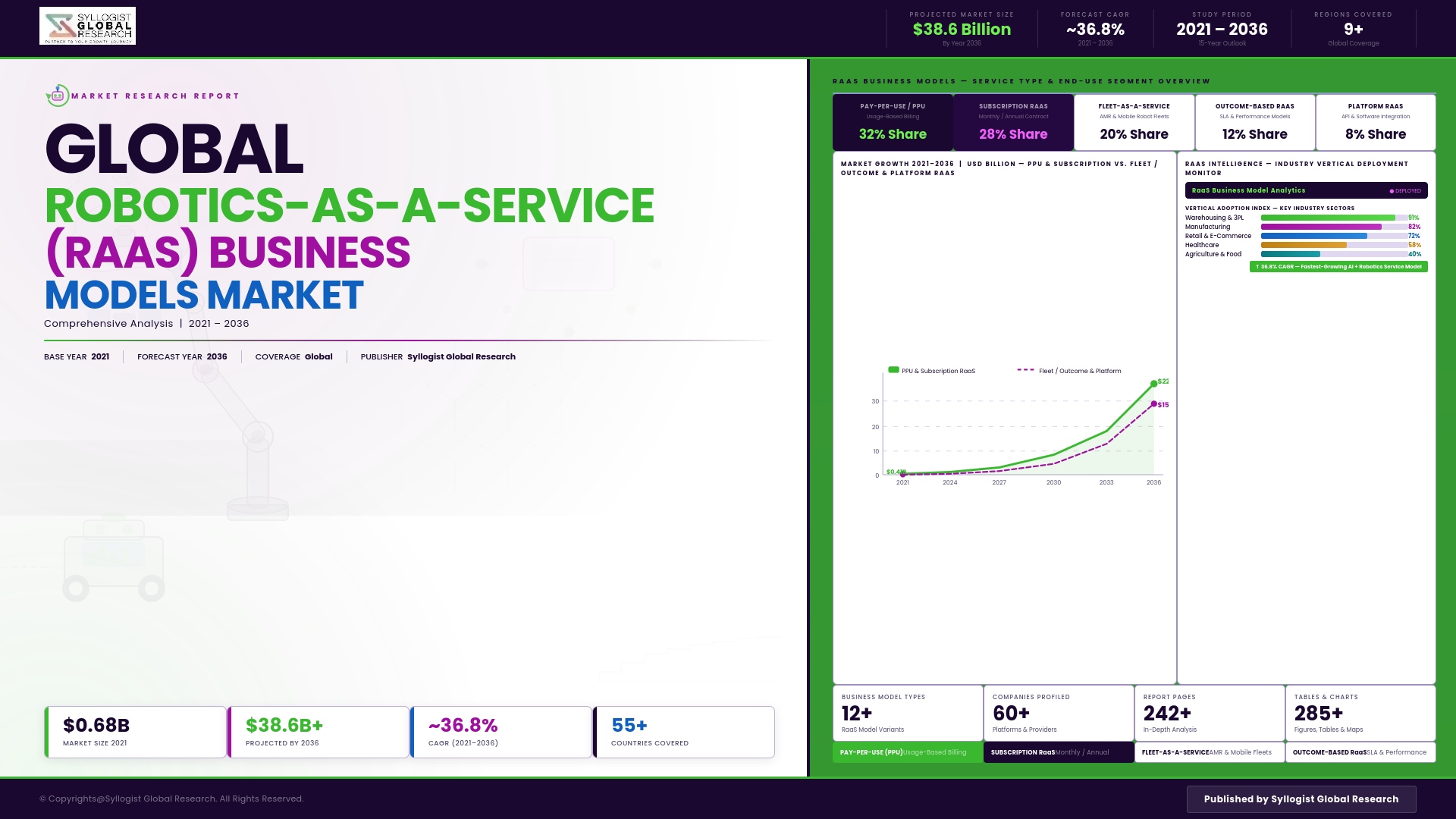

The global Robotics-as-a-Service market is advancing through a structural commercial transformation that is fundamentally altering the financial accessibility, operational risk profile, and adoption pace of automation across a dramatically broadened range of enterprise customers, as the shift from robotics capital expenditure to subscription and outcome-based service models removes the balance sheet commitment, technical integration complexity, and residual technology obsolescence risk that historically confined advanced robotics deployment to large corporations with dedicated automation engineering teams and sufficient capital budgets to absorb multi-year robot depreciation schedules. The market was valued at approximately USD 7.6 billion in 2025 and is projected to expand at a compound annual growth rate of 29.4% through 2034, as the convergence of cloud robotics platforms enabling remote fleet management, AI-powered robot software improving task adaptability without hardware replacement, and the demonstrated unit economics of subscription robot deployments across logistics, warehousing, and light manufacturing create a commercially compelling alternative to traditional robot capital ownership that is unlocking automation adoption among mid-market manufacturers, growing e-commerce fulfillment operators, and service industry organizations that represent the largest untapped robotics deployment opportunity globally.

Autonomous mobile robots deployed under subscription contracts in warehouse and fulfillment center operations represent the largest and most commercially mature segment within the global Robotics-as-a-Service market, reflecting the operational characteristics of logistics automation that are particularly well-matched to the service delivery model, including high task repeatability that enables reliable performance metric specification in service contracts, the seasonal demand variability of e-commerce fulfillment that makes flexible subscription scaling more economical than fixed capital asset ownership sized for peak capacity, and the standardized floor plan and workflow environments of modern fulfillment centers that reduce robot commissioning complexity and enable rapid deployment by service providers managing multi-site robot fleets across customer portfolios. Collaborative robot subscription programs in light manufacturing and assembly operations are the second fastest-growing application segment, as the reduction in safety guarding requirements, ease of task reprogramming, and compact form factor of collaborative robots relative to traditional industrial robots reduce the facility modification investment required for deployment, making subscription-based collaborative robot programs viable for small and medium-sized manufacturers whose floor space, production variability, and budget constraints previously excluded them from automation investment.

The software and data intelligence layer is emerging as the most strategically significant value creation component within the Robotics-as-a-Service business model, as service providers who can deploy fleets of robots across multiple customer sites develop proprietary operational performance datasets, AI task optimization algorithms, and predictive maintenance capabilities that improve robot productivity, reduce service cost, and deepen customer dependency in ways that pure hardware leasing models cannot achieve. Cloud-connected robot fleet management platforms enabling real-time operational monitoring, remote software updates, task reassignment, and performance analytics across geographically distributed customer deployments are creating the technology infrastructure that differentiates leading Robotics-as-a-Service operators from commodity hardware rental providers and establishes subscription revenue streams with high customer retention and expansion characteristics. The integration of robot-generated operational data into customer enterprise resource planning, warehouse management, and manufacturing execution systems is further deepening the value proposition and switching cost embedded in established Robotics-as-a-Service relationships, transforming robotic deployments from equipment rentals into intelligent automation infrastructure partnerships with strategic customer lock-in characteristics that support long-term contract extension and fleet expansion revenue growth.

North America is the largest regional market for Robotics-as-a-Service, anchored by the scale of United States e-commerce fulfillment infrastructure investment, the high labor cost environment incentivizing automation adoption across manufacturing and logistics, the maturity of the robotics venture investment ecosystem producing well-capitalized service model operators, and the active procurement of autonomous mobile robot subscription programs by major retail and third-party logistics operators managing large warehouse portfolios. Europe represents the second largest regional market, driven by high manufacturing labor costs across Germany, France, and the Nordic countries, growing collaborative robot subscription adoption among small and medium-sized manufacturers, and the strategic automation investment programs of European automotive and consumer goods corporations. Asia-Pacific is the fastest-growing Robotics-as-a-Service market, driven by the scale of Chinese manufacturing automation investment, growing e-commerce fulfillment automation in Japan and South Korea, and the rapid emergence of domestic Robotics-as-a-Service providers in China offering cost-competitive subscription automation programs to domestic manufacturers and logistics operators.

Key Drivers

Labor Market Tightness, Rising Wage Costs, and Workforce Availability Constraints Compelling Mid-Market Enterprises to Seek Accessible Automation Alternatives to Capital-Intensive Robot Ownership

Persistent labor shortages across manufacturing, warehousing, logistics, and service industry operations in North America, Europe, and increasingly Asia-Pacific are compelling organizations to accelerate automation investment as the only viable long-term strategy for addressing structural workforce availability constraints that recruitment, retention incentives, and wage increases alone cannot resolve at the scale of operational requirements. The Robotics-as-a-Service subscription model addresses the specific financial barrier facing mid-market enterprises where the capital budget required for outright robot purchase exceeds available investment capacity or competing capital allocation priorities, by converting automation from a capital expenditure requiring board-level approval and multi-year payback justification into an operational expenditure comparable to labor cost that can be evaluated on month-to-month cost comparison terms directly against the wages, benefits, and training costs of the human labor it supplements or replaces.

E-Commerce Growth and Omnichannel Fulfillment Complexity Driving Subscription Automation Demand Among Logistics Operators Managing Variable Throughput and Rapid Scalability Requirements

The sustained growth of e-commerce and the increasing complexity of omnichannel retail fulfillment operations that must simultaneously serve direct-to-consumer shipping, retail store replenishment, and marketplace order fulfillment from shared inventory and facility infrastructure is creating operational automation requirements characterized by high task variety, seasonal peak demand variability, and rapid throughput scaling needs that fixed-capital robot ownership poorly accommodates relative to flexible subscription models enabling fleet size adjustment without stranded asset exposure. Third-party logistics operators managing multi-tenant fulfillment facilities for diverse retail customers with varying automation requirements and contract duration horizons find the subscription robot model particularly well-aligned with their business model, as it enables rapid facility automation configuration changes between customers without the capital commitment risk of owned robot assets whose residual value depends on continued facility utilization.

Cloud Robotics Platforms, AI Task Learning Capabilities, and Remote Fleet Management Infrastructure Enabling Robotics-as-a-Service Business Models at Economically Viable Scale

The maturation of cloud robotics infrastructure enabling real-time telemetry monitoring, over-the-air software updates, remote diagnostic support, and centralized fleet performance management across geographically distributed customer deployments has fundamentally enabled the Robotics-as-a-Service operating model by allowing service providers to manage large robot fleets at customer sites with minimal on-site technical staffing, dramatically reducing the service delivery cost structure that determines subscription pricing competitiveness. AI-powered robot task learning platforms that enable robots to adapt to new product types, packaging formats, and task variations through supervised learning rather than manual reprogramming are simultaneously improving the operational versatility of subscription robot deployments, reducing customer changeover costs, and expanding the range of manufacturing and logistics tasks addressable through standard subscription robot configurations without application-specific hardware customization.

Key Challenges

Robotics-as-a-Service Unit Economics and Long-Term Contract Profitability Challenges Constraining Service Provider Financial Sustainability and Investor Return Achievement

The Robotics-as-a-Service business model requires service providers to bear the upfront capital cost of robot procurement, deployment, and commissioning while recovering investment through multi-year subscription fee amortization, creating a capital-intensive working capital requirement that has challenged the financial sustainability of several well-funded Robotics-as-a-Service operators who encountered longer-than-projected customer acquisition cycles, higher-than-anticipated service and maintenance costs, and customer contract cancellation or non-renewal rates that undermined the unit economics assumptions embedded in their original business model projections. Demonstrating sustainable contract-level profitability and achieving the customer fleet density required to spread fleet management platform fixed costs across sufficient subscription revenue is proving more challenging and time-consuming than initial market projections anticipated for operators in capital-intensive robot categories.

Customer Integration Complexity, Enterprise System Connectivity Requirements, and Site-Specific Customization Needs Extending Deployment Timelines and Elevating Service Provider Implementation Costs

The deployment of subscription robot services within customer operational environments requires integration with existing warehouse management systems, enterprise resource planning platforms, manufacturing execution systems, and facility infrastructure including charging stations, WiFi networks, floor markings, and safety barriers, creating implementation complexity and customization requirements that extend time-to-value for customers, elevate service provider deployment labor costs, and complicate the standardized service delivery model that Robotics-as-a-Service unit economics depend upon. The diversity of customer facility layouts, existing automation equipment configurations, IT system architectures, and operational workflow requirements means that each new customer site deployment requires substantial site-specific engineering and integration effort that resists the modular, reproducible deployment process that enables service providers to achieve the deployment velocity and cost efficiency required for sustainable business model scaling.

Cybersecurity Vulnerabilities in Cloud-Connected Robot Fleets and Operational Technology Security Requirements Creating Risk Management Complexity for Enterprise Customers and Service Providers

The cloud connectivity that enables Robotics-as-a-Service fleet management, remote diagnostics, and software updates simultaneously creates cybersecurity attack surfaces within customer operational technology environments that sophisticated adversaries can potentially exploit to disrupt production operations, access proprietary manufacturing process data, or compromise safety systems, generating risk management complexity for enterprise customers whose operational technology security frameworks must accommodate cloud-connected robot systems managed by external service providers with varying cybersecurity posture standards and data governance practices. The intersection of robot operational continuity requirements with enterprise cybersecurity policy creates procurement friction and extended security review timelines that slow Robotics-as-a-Service contract progression, particularly in regulated industries including pharmaceuticals, defense, and critical infrastructure where operational technology security standards are most stringent and third-party system access most tightly controlled.

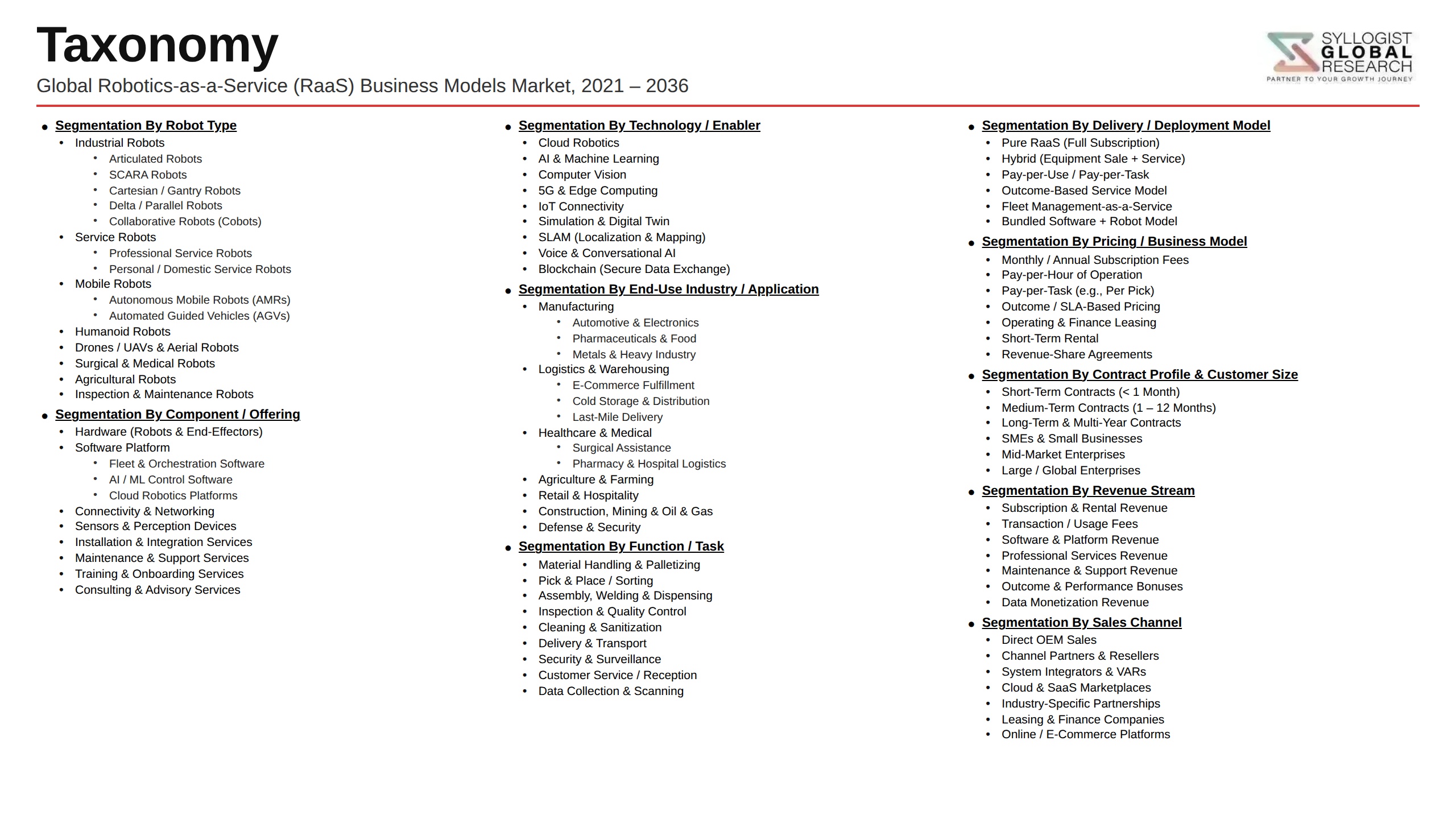

Market Segmentation

- Segmentation By Service Model

- Subscription-Based Robot Leasing (Monthly and Annual)

- Outcome-Based and Pay-Per-Task Models

- Robot-as-a-Service Managed Operations Programs

- Hybrid Ownership and Service Contract Models

- Fleet Management and Software-as-a-Service Add-Ons

- Others

- Segmentation By Robot Type

- Autonomous Mobile Robots and Automated Guided Vehicles

- Collaborative Robots (Cobots)

- Industrial Articulated Robots

- Service and Humanoid Robots

- Agricultural and Field Robots

- Drone and Aerial Robot Systems

- Others

- Segmentation By End Use Industry

- E-Commerce Fulfillment and Warehousing

- Manufacturing and Assembly

- Healthcare and Hospital Logistics

- Retail and In-Store Automation

- Agriculture and Food Production

- Construction and Infrastructure

- Hospitality and Facility Management

- Others

- Segmentation By Application

- Goods-to-Person Order Picking and Sorting

- Assembly and Parts Handling

- Inspection, Quality Control, and Monitoring

- Disinfection and Cleaning Automation

- Inventory Management and Stocktaking

- Last-Mile and Last-Yard Delivery

- Others

- Segmentation By Enterprise Size

- Large Enterprises (Above 1,000 Employees)

- Medium Enterprises (100 to 1,000 Employees)

- Small Enterprises (Below 100 Employees)

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global Robotics-as-a-Service market valuation in 2025, projected through 2034, segmented by service model, robot type, and end use industry, enabling automation service providers, robot manufacturers, logistics operators, and investors to identify the highest-growth subscription model categories and most commercially significant enterprise automation service deployment opportunities across the global market?

- How are subscription-based, outcome-based, and pay-per-task Robotics-as-a-Service models comparing in terms of customer acquisition economics, contract profitability, fleet utilization optimization, and customer retention characteristics, and what pricing architecture, service scope definition, and performance guarantee structures are proving most effective at achieving sustainable unit economics across autonomous mobile robot and collaborative robot deployment programs?

- Which Robotics-as-a-Service application categories, specifically warehouse goods-to-person picking, collaborative robot assembly, autonomous inventory scanning, and healthcare logistics automation, are demonstrating the most compelling total cost of ownership advantages relative to direct robot ownership or human labor alternatives, and what operational efficiency, labor cost reduction, and throughput improvement metrics are commercially deployed programs achieving in verified customer deployments?

- How is the competitive landscape structured among autonomous mobile robot service providers, collaborative robot subscription developers, industrial robot leasing programs, and generalist automation service operators, and what robot fleet scale, software platform differentiation, enterprise integration capability, and vertical industry specialization strategies are enabling leading Robotics-as-a-Service operators to build defensible customer bases and recurring revenue streams?

- What cloud robotics platform capabilities, AI task learning systems, remote fleet management architectures, and predictive maintenance algorithms are most critical to enabling economically viable Robotics-as-a-Service operations at scale, and how are leading service providers investing in software platform development and operational data intelligence to differentiate from commodity hardware leasing competitors and improve subscription contract profitability?

- How are mid-market manufacturers, growing e-commerce operators, and service industry organizations evaluating Robotics-as-a-Service subscription programs relative to direct capital purchase, automation system integrator deployment, and labor force alternatives, and what financial payback expectations, operational flexibility requirements, and technology upgrade provisions are most critical to enterprise procurement decision-making for subscription robot service contract commitments?

- Which regional Robotics-as-a-Service markets, specifically North America, Europe, and Asia-Pacific, are expected to generate the highest incremental subscription revenue growth through 2034, and what combinations of labor market tightness, e-commerce fulfillment automation investment, small and medium enterprise automation accessibility initiatives, and domestic robot service provider ecosystem maturity are defining market growth trajectories and competitive dynamics in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Robot Downtime, Maintenance Failure & Service Level Agreement (SLA) Liability Risk

- Cybersecurity, Data Privacy & Remote Access Vulnerability of Connected Robot Fleets Risk

- Customer Churn, Contract Cancellation & Long-Term Revenue Predictability Risk

- Hardware Obsolescence, Rapid Technology Cycle & Capital Recovery Risk

- Skilled Technician Shortage, Field Service Scalability & Cost Overrun Risk

- Liability, Worker Safety, Insurance Coverage & Regulatory Compliance Risk

- Regulatory Framework & Standards

- ISO 10218, ISO/TS 15066 & Collaborative Robot (Cobot) Safety Standards for RaaS Deployments

- EU Machinery Regulation (2023/1230), ATEX & CE Marking Standards for Robotic Equipment as a Service

- OSHA General Industry Safety Standards, ANSI/RIA R15.06 & US Robotic Safety Regulatory Frameworks

- GDPR, CCPA & Data Protection Regulatory Frameworks for Robot-Generated Operational & Facility Data

- AI Act (EU) Risk Classification, Autonomous System Accountability & Liability Frameworks for Service Robots

- UL 3100, IEC 62443 & Industrial IoT Cybersecurity Standards for Networked Robot Fleet Management

- Global Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Active RaaS Robot Units & Service Contracts)

- Market Size & Forecast by Robot Type

- Autonomous Mobile Robots (AMRs) & Automated Guided Vehicles (AGVs)

- Collaborative Robots (Cobots) & Industrial Robotic Arms

- Autonomous Cleaning, Disinfection & Facility Service Robots

- Delivery, Last-Mile & Logistics Service Robots

- Agricultural & Field Robots (Harvesting, Weeding & Inspection Robots)

- Security, Surveillance & Patrol Robots

- Inspection, Maintenance & Drone-as-a-Service Platforms

- Surgical & Medical Robotic Systems

- Social, Customer Service & Hospitality Robots

- Market Size & Forecast by Business Model

- Pure RaaS Subscription Model (Monthly/Annual Fee per Robot Unit)

- Pay-per-Use & Task-Based Pricing Model (per Pick, per km, per Hour)

- Outcome-Based & Performance-Linked Pricing Model

- Robot Leasing & Equipment Financing Model (Finance Lease & Operating Lease)

- Hybrid Model: Hardware Purchase with Software & Maintenance Subscription

- Managed Robotics Service & Fully Operated Robot Fleet Model

- Market Size & Forecast by Service Component

- Hardware Provision, Robot Unit Supply & Fleet Deployment

- Robot Operating System (ROS), Software Platform & Fleet Management Software

- Connectivity, IoT Integration & Remote Monitoring Services

- Predictive Maintenance, Repair & Field Service

- Training, Onboarding, Commissioning & Change Management Services

- AI, Analytics, Data Insights & Performance Reporting Services

- Cybersecurity, Compliance & SLA Management Services

- Market Size & Forecast by Deployment Environment

- Indoor Structured & Semi-Structured Environments (Warehouses, Factories & Retail)

- Outdoor & Unstructured Environments (Agriculture, Construction & Public Spaces)

- Hazardous & Controlled Environments (Mining, Oil & Gas & Nuclear Facilities)

- Healthcare & Clinical Environments (Hospitals, Labs & Pharmacies)

- Market Size & Forecast by Application

- Warehousing, Order Fulfilment & Intralogistics Automation

- Manufacturing Assembly, Machine Tending & Pick-and-Place Automation

- Retail Store Operations, Inventory Management & Customer Service

- Healthcare Logistics, Pharmacy Dispensing & Surgical Assistance

- Facility Management, Cleaning, Disinfection & Security

- Agriculture, Crop Monitoring, Harvesting & Precision Farming

- Infrastructure Inspection, Maintenance & Asset Monitoring

- Last-Mile Delivery, Parcel Handling & Port Logistics

- Market Size & Forecast by End-User

- E-Commerce, Retail & Omnichannel Fulfilment Operators

- Manufacturing & Industrial Companies

- Healthcare Providers, Hospitals & Pharmaceutical Companies

- Third-Party Logistics (3PL) & Supply Chain Operators

- Agriculture & Food Production Companies

- Facility Management & Property Services Companies

- Government, Defence & Public Sector Agencies

- Small & Medium-Sized Enterprises (SMEs) via Managed RaaS Models

- Market Size & Forecast by Sales Channel

- Direct RaaS Provider & Robot OEM Sales Channel

- System Integrator & Automation Consultant Channel

- Marketplace, Platform Aggregator & Broker Channel

- Distributor, Reseller & Value-Added Partner Channel

- North America Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Robotics-as-a-Service Business Models Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Active RaaS Robot Units & Service Contracts)

- By Robot Type

- By Business Model

- By Service Component

- By Deployment Environment

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, United Kingdom, Netherlands, Sweden, Denmark, Spain, Italy, Japan, China, South Korea, Australia, Singapore, India, Taiwan, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- AMR & AGV Fleet Management Technology Deep-Dive: Multi-Robot Coordination, Dynamic Routing, SLAM & Warehouse Orchestration

- Cobot & Robotic Arm Technology for RaaS: Ease-of-Programming, Plug-and-Produce & Tool-Changing Systems

- AI & Computer Vision Technology for Robot Perception, Scene Understanding & Autonomous Task Execution

- Digital Twin, Simulation & Deployment Acceleration Technology for RaaS Fleet Configuration & Rollout

- Remote Operation, Teleoperation & Human-in-the-Loop Technology for Edge Case Handling in RaaS Deployments

- Edge Computing, 5G Connectivity & Low-Latency Communication Technology for Distributed Robot Fleet Management

- Predictive Maintenance, Self-Diagnostics & Robot Health Monitoring Technology for SLA Assurance in RaaS

- Patent & IP Landscape in Robotics-as-a-Service Technologies

- Value Chain & Supply Chain Analysis

- Robot Hardware: Actuator, Sensor, Motor, Battery & Structural Component Manufacturing Supply Chain

- Compute, Edge AI Chip, Vision Sensor & Electronics Supply Chain for Autonomous Robot Systems

- Robot Operating System (ROS), AI Software & Fleet Management Platform Development Supply Chain

- System Integration, Site Survey, Infrastructure Preparation & Deployment Supply Chain

- Connectivity, IoT, Cloud Platform & Cybersecurity Infrastructure Supply Chain

- Field Service Network, Maintenance, Spare Parts & Technician Deployment Supply Chain

- Customer Success, Training & Ongoing Performance Management Channel

- Pricing Analysis

- RaaS Subscription Pricing Analysis by Robot Type: Monthly per-Unit Rate Benchmarking

- Pay-per-Use Pricing: per-Pick, per-km & per-Hour Rate Analysis by Application & Robot Type

- RaaS vs. Robot Capex Ownership Total Cost of Ownership (TCO) & Breakeven Analysis

- Managed Robotics Service Full-Scope Contract Pricing & Scope-of-Work Structure Analysis

- SLA Penalty, Uptime Guarantee & Performance KPI Pricing Implication Analysis

- Price Trend Analysis: Hardware Cost Reduction, AI Commoditisation & Impact on RaaS Pricing

- Sustainability & Environmental Analysis

- Energy Consumption, Battery Chemistry & Carbon Footprint of AMR & Autonomous Robot Fleet Operations

- RaaS Circular Economy Model: Robot Refurbishment, Component Reuse & End-of-Life Hardware Recycling

- Role of RaaS in Reducing Labour-Intensive Physical Work, Occupational Injury & Worker Safety Improvement

- Workforce Displacement, Reskilling & Social Impact of Robotic Automation: Responsible Deployment Standards

- ESG Reporting, Responsible AI & Sustainable Robotics Standards for RaaS Providers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Robot Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Robot Type, Business Model & Geography

- Player Classification

- Robot OEM Manufacturers Offering Native RaaS Models

- Dedicated RaaS Platform & Managed Robotics Service Providers

- Automation System Integrators Transitioning to RaaS Delivery

- Logistics & Warehouse Automation Specialists with RaaS Offerings

- Agricultural & Field Robot RaaS Providers

- Technology Financiers, Robot Leasing Companies & Capital Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Robot Type, Business Model & Region

- Company Profile

- Company Overview & Headquarters

- RaaS Robot Products, Service Portfolio & Business Model Structure

- Key Customer Relationships & Reference Deployments

- Active Robot Fleet Size, Deployed Units & Contract Portfolio

- Revenue (RaaS Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (New Contracts, Product Launches, Business Model Innovations)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Robot Capability vs. Service Model Maturity)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Robot Type, Business Model, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Service Portfolio, Business Model Design & Pricing Strategy

- Technology Investment, Fleet Scalability & Platform Development Strategy

- Geographic Expansion & Vertical Market Entry Strategy

- Customer Acquisition, Retention & Success Management Strategy

- Partnership, M&A & RaaS Ecosystem Strategy

- Sustainability, Workforce Transition & Responsible Automation Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output