Global Same-Day Delivery Infrastructure Market By Infrastructure Type, By Technology, By Vehicle Type, By End Use Sector, By Business Model, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Same-Day Delivery Infrastructure Market encompasses the physical, digital, and operational assets required to fulfill consumer and enterprise orders within the same calendar day of placement, including urban micro-fulfillment centers, dark stores, last-mile sortation hubs, autonomous delivery vehicle fleets, drone delivery systems, crowdsourced driver networks, AI-powered route optimization platforms, real-time order management systems, and parcel locker and pickup point networks, procured and operated by e-commerce retailers, grocery operators, pharmaceutical distributors, logistics service providers, and on-demand delivery platform companies globally.

Market Insights

The global same-day delivery infrastructure market is experiencing a period of rapid commercial maturation, shaped by the crystallization of consumer delivery speed expectations at levels that make same-day availability a competitive necessity rather than a premium differentiator for e-commerce, grocery, pharmaceutical, and on-demand retail operators in major urban markets, and by the accelerating investment in micro-fulfillment, route optimization, and autonomous delivery technologies that are progressively improving the unit economics of same-day delivery toward commercially sustainable margins without the universal reliance on premium delivery surcharges that characterized the market’s early development phase. The market was valued at approximately USD 18.7 billion in 2025 and is projected to expand at a compound annual growth rate of 22.4% through 2034, as the combination of urban population density growth, smartphone commerce penetration, expanding product category coverage beyond apparel and electronics into grocery, pharmaceutical, beauty, and home goods, and the maturation of crowdsourced delivery network density across major metropolitan markets creates sustainable volumes and route economics that support broader geographic same-day delivery coverage without requiring the subsidized delivery unit economics that limited the initial commercial viability of same-day programs to high-value orders and premium subscriber segments.

The micro-fulfillment center and dark store network segment represents the most strategically critical infrastructure investment category within the same-day delivery ecosystem, as the geographic positioning of inventory within fifteen to thirty minutes of dense residential populations is the primary determinant of same-day delivery feasibility, cycle time performance, and unit economics viability for all subsequent last-mile delivery execution modes including delivery driver dispatch, autonomous vehicle deployment, and drone delivery. The rapid build-out of urban dark store networks by grocery delivery operators in major European, North American, and Asian cities over the past four years has demonstrated both the operational model feasibility and the intense competitive dynamics of hyperlocal inventory positioning, with leading grocery delivery platforms investing aggressively in dark store density to establish geographic coverage advantages before market consolidation reduces the number of well-capitalized operators capable of sustaining city-wide same-day network economics. Pharmaceutical and healthcare product same-day delivery is the fastest-growing product category within the infrastructure investment pipeline, as regulatory approvals for prescription medication same-day delivery expand across United States, European, and Asian markets and the demonstrated demand for convenient medication access from pharmacy and telehealth platform customers creates compelling investment cases for dedicated pharmaceutical micro-fulfillment and temperature-controlled last-mile delivery infrastructure.

Autonomous last-mile delivery technology is advancing from selective deployment in controlled suburban environments toward broader commercial scaling in urban environments, with sidewalk delivery robots, cargo bicycles, autonomous delivery vans, and drone delivery systems each establishing commercial operations across different geography types and product weight categories that are collectively expanding the range of same-day delivery scenarios where automated delivery economics can improve upon crowdsourced human delivery unit costs. Drone delivery is attracting particular infrastructure investment and regulatory attention for pharmaceutical, medical supply, and high-urgency consumer delivery applications in geographies where aerial navigation can bypass surface road network congestion and distance constraints, with commercial drone delivery programs advancing toward scale operations in Australia, the United Kingdom, the United States, and multiple Asian markets under regulatory frameworks that are progressively expanding approved operating envelopes to enable commercially relevant delivery coverage areas. AI-powered route optimization platforms integrating real-time traffic, weather, driver location, order batching, and delivery time window data are enabling same-day delivery networks to improve route efficiency, reduce delivery cost per order, and compress delivery cycle times in ways that materially improve the unit economics of human-delivered same-day programs without requiring autonomous vehicle deployment.

Asia-Pacific dominates the global same-day delivery infrastructure market by investment volume and operational scale, anchored by the extraordinary density and sophistication of same-day and instant delivery infrastructure in China where major e-commerce and grocery platforms have invested billions of dollars in micro-fulfillment, dark store, and delivery network infrastructure supporting delivery times measured in minutes across major urban centers, alongside the rapidly growing same-day delivery ecosystems of India, South Korea, Japan, and Southeast Asian urban markets. North America represents the second largest regional market, driven by the Amazon Prime same-day delivery network expansion, grocery delivery platform dark store investment, and the growing pharmaceutical same-day delivery infrastructure investment by major pharmacy chains and healthcare operators. Europe is the third major regional market, characterized by the densely populated urban geographies that favor same-day logistics economics, strong quick-commerce platform investment activity, and growing retailer same-day delivery infrastructure commitment across the United Kingdom, Germany, France, and the Netherlands.

Key Drivers

Consumer Delivery Speed Expectation Escalation and Same-Day Availability as a Competitive Necessity Compelling Retail and E-Commerce Operators to Invest in Proximity Fulfillment Infrastructure

The progressive normalization of same-day delivery availability across grocery, pharmaceutical, and consumer electronics categories by leading e-commerce and quick-commerce platforms has elevated delivery speed from a premium service differentiator to a baseline consumer expectation whose absence from a retailer or marketplace offering creates measurable cart abandonment and customer attrition rates that justify the infrastructure investment required to compete on same-day availability. Retailers, supermarket chains, pharmacy operators, and marketplace platforms that lack same-day delivery capability in major urban markets are experiencing competitive market share erosion to same-day-capable competitors, compelling infrastructure investment decisions driven by competitive defensive necessity as much as organic demand growth, and creating an accelerating industry dynamic where same-day capability investment by one major market participant generates responsive investment commitments from competitors seeking to prevent sustained competitive disadvantage.

Urban Density Growth, Smartphone Commerce Penetration, and On-Demand Economy Behavioral Shifts Expanding the Consumer Base and Order Volume Economics of Same-Day Delivery Networks

Accelerating urbanization concentrating growing proportions of consumer purchasing power within the dense residential geographies that make same-day delivery network economics most favorable, combined with smartphone commerce adoption enabling spontaneous, need-based purchasing behavior that assigns high value to rapid delivery fulfillment, is expanding the addressable consumer base and average order frequency of same-day delivery networks in ways that progressively improve route density, delivery cost per order amortization, and micro-fulfillment center inventory utilization metrics toward the commercial viability thresholds that support network expansion beyond early premium consumer segments. The behavioral normalization of on-demand commerce across age demographics, product categories, and spending levels following the pandemic-accelerated e-commerce adoption wave is creating a durable structural expansion of same-day delivery demand that is not reversing as pandemic-era usage incentives recede.

Autonomous Delivery Technology Advancement and AI Route Optimization Progress Improving Same-Day Unit Economics Toward Commercially Sustainable Levels Across Broader Geographic and Product Category Coverage

The advancing commercial readiness of sidewalk delivery robots, autonomous delivery vans, cargo drones, and AI-powered dynamic routing platforms is creating a credible cost reduction trajectory for same-day delivery unit economics that is supporting sustained infrastructure investment under business models premised on achieving delivery cost parity with standard next-day delivery economics as autonomous delivery technology scales and per-delivery hardware amortization decreases with fleet size growth. Real-time AI optimization of order batching, route planning, driver assignment, and delivery time window management is simultaneously improving the productivity of human-delivered same-day programs by reducing empty miles, minimizing average delivery radius, and maximizing orders delivered per driver hour, generating meaningful near-term cost improvements that make profitable same-day delivery economics achievable for a broader range of order values and delivery distances than previous-generation logistics management systems could support.

Key Challenges

Same-Day Delivery Unit Economics and Last-Mile Cost Structure Sustainability Creating Persistent Profitability Challenges for Operators Without Sufficient Order Density or Premium Pricing Power

The operational cost structure of same-day delivery, combining micro-fulfillment facility real estate and labor costs, delivery driver wages and platform fees, return processing overhead, and the time pressure logistics of compressed delivery windows, creates per-order cost structures that significantly exceed those of standard next-day or two-day delivery across all but the highest-density urban delivery markets with sufficient order volume to achieve route efficiency benchmarks that justify the operational cost premium relative to standard shipping alternatives. Consumer resistance to paying same-day delivery surcharges that fully reflect the operational cost premium, combined with competitive pressure from well-capitalized platforms subsidizing same-day delivery as a customer acquisition and retention investment rather than a profitable service, creates persistent unit economics tension that has driven multiple well-funded same-day delivery operators into financial restructuring or operational retreat to core profitable markets.

Urban Traffic Congestion, Delivery Access Restrictions, and Last-Mile Environmental Regulation Increasing Delivery Complexity and Cost in the Dense Urban Geographies Where Same-Day Demand Is Highest

Same-day delivery networks depend on rapid and reliable last-mile access to dense urban residential and commercial delivery points, yet the cities with the highest same-day delivery demand concentration are simultaneously implementing low-emission zone restrictions, diesel vehicle access bans, loading dock time restrictions, and urban congestion charging schemes that increase the operating cost, route planning complexity, and delivery time variability of conventional van-based delivery fleets in precisely the urban environments where same-day economics require the highest delivery productivity per driver hour. Securing adequate urban loading, staging, and micro-fulfillment real estate at commercially viable lease rates in high-demand city center and inner-suburban locations adds further cost pressure and operational planning complexity to same-day delivery network development in the most attractive urban markets.

Regulatory Uncertainty for Autonomous and Drone Delivery Operations Limiting the Scale and Geographic Coverage of Technology-Enabled Same-Day Cost Reduction Programs

The commercial scaling of autonomous sidewalk delivery robots, delivery drones, and autonomous delivery vehicles that are expected to materially improve same-day delivery unit economics is contingent on regulatory frameworks governing autonomous vehicle road access, drone beyond-visual-line-of-sight operations, airspace integration, and liability frameworks for delivery incidents involving autonomous systems, and the slow and geographically uneven development of these regulatory frameworks across national and subnational jurisdictions is constraining the pace at which autonomous delivery technology can be deployed at commercially meaningful scale in the urban environments where same-day infrastructure investment and unit economic improvement opportunities are greatest. Inconsistent and overlapping municipal, state, and federal regulatory jurisdictions governing autonomous delivery operations in the United States and similar regulatory fragmentation in European and Asian markets creates compliance complexity that extends operational launch timelines and increases the deployment cost of autonomous delivery programs.

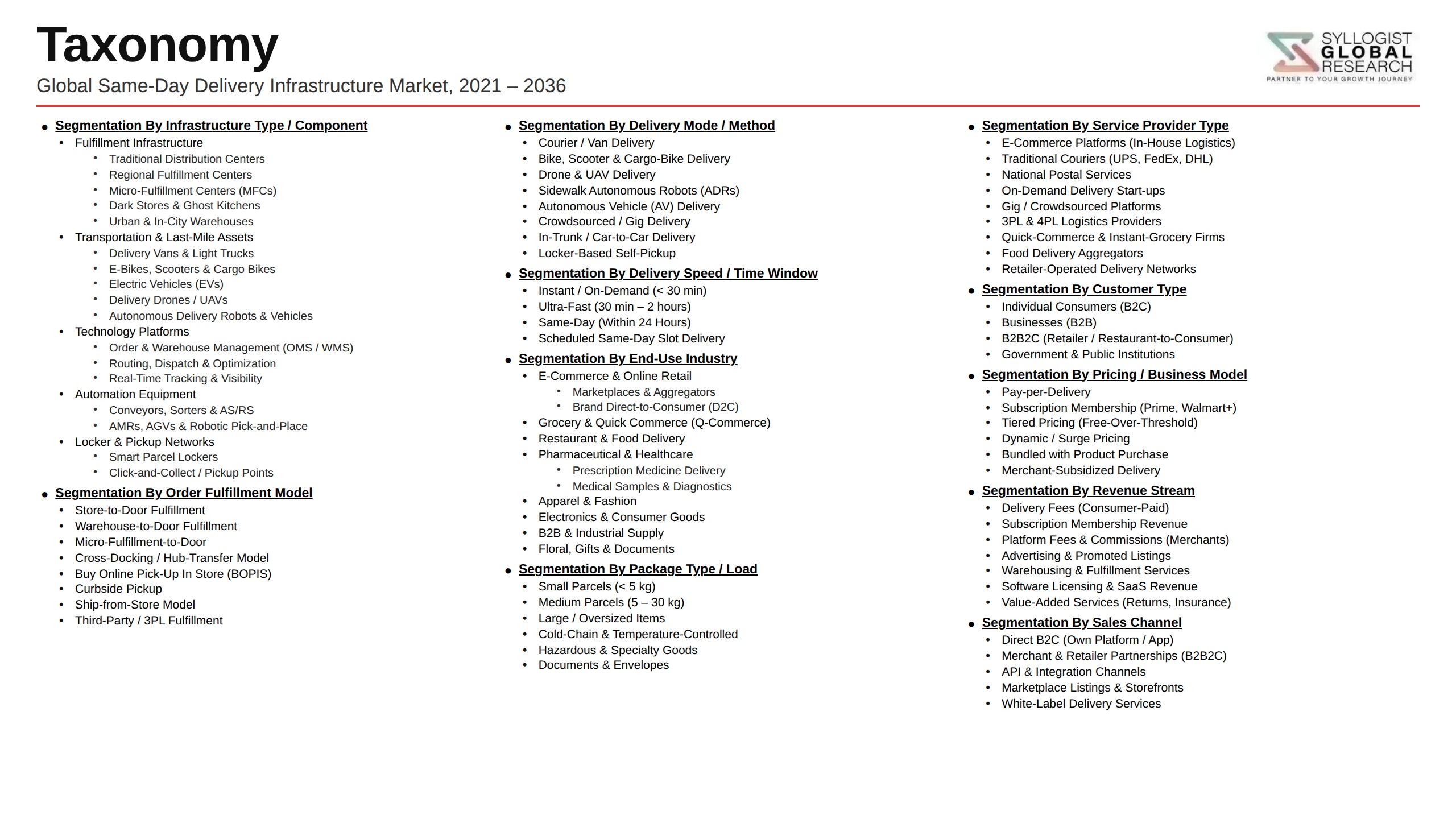

Market Segmentation

- Segmentation By Infrastructure Type

- Urban Micro-Fulfillment Centers and Dark Stores

- Last-Mile Sortation and Delivery Hubs

- Automated Parcel Lockers and Pickup Point Networks

- Drone Delivery Launch and Landing Infrastructure

- Autonomous Vehicle Fleet Depots and Charging Stations

- AI Route Optimization and Order Management Platforms

- Others

- Segmentation By Technology

- AI-Powered Route Optimization and Dispatch Platforms

- Autonomous Delivery Vehicle Systems

- Drone and Unmanned Aerial Delivery Systems

- Robotic Micro-Fulfillment and Order Picking Automation

- Real-Time Tracking and Delivery Experience Platforms

- Crowdsourced Driver Network Management Systems

- Others

- Segmentation By Vehicle Type

- Conventional Delivery Vans and Cargo Vehicles

- Electric Cargo Bikes and Micro-Mobility Vehicles

- Sidewalk and Pavement Delivery Robots

- Autonomous Last-Mile Delivery Vans

- Cargo Drones and Unmanned Aerial Vehicles

- Others

- Segmentation By End Use Sector

- E-Commerce and Online Retail

- Grocery and Fresh Food Delivery

- Pharmaceutical and Healthcare Products

- Restaurant and Food Service Delivery

- Fashion and Apparel

- Electronics and Consumer Goods

- Others

- Segmentation By Business Model

- Retailer-Owned Same-Day Delivery Networks

- Third-Party Logistics Same-Day Service Providers

- On-Demand Delivery Platform Operators

- Crowdsourced and Gig Economy Delivery Models

- Drone and Autonomous Delivery as a Service

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global same-day delivery infrastructure market valuation in 2025, projected through 2034, segmented by infrastructure type, technology, and end use sector, enabling logistics operators, e-commerce retailers, infrastructure investors, and technology developers to identify the highest-growth infrastructure investment categories and most commercially significant same-day delivery expansion opportunities across the global market?

- How are micro-fulfillment center and dark store network investment programs evolving in terms of facility size, geographic density strategy, product category coverage, and automation intensity across leading grocery, pharmacy, and e-commerce operators in North America, Europe, and Asia-Pacific, and what proximity-to-consumer location economics and inventory positioning models are proving most operationally viable at commercial scale?

- Which same-day delivery unit economic models, specifically high-density urban dark store grocery networks, pharmaceutical same-day pharmacy programs, autonomous vehicle delivery pilots, and drone delivery commercial programs, are demonstrating commercially sustainable cost-per-delivery trajectories, and what order density thresholds, delivery radius constraints, and technology deployment conditions are required to achieve margin-positive same-day operations?

- How is the competitive landscape structured among vertically integrated e-commerce platform same-day networks, specialized third-party logistics same-day providers, on-demand delivery platform operators, and autonomous delivery technology companies, and what proprietary infrastructure ownership, technology differentiation, geographic density advantages, and supply chain partnership strategies are enabling leading operators to build durable competitive positions?

- What regulatory framework developments across drone beyond-visual-line-of-sight approvals, autonomous vehicle urban road access permissions, low-emission zone delivery restrictions, and gig economy labor classification legislation in key markets are most significantly affecting same-day delivery infrastructure investment decisions, operational model design, and technology deployment timelines for major market participants through 2034?

- How are AI route optimization advances, real-time dynamic batching algorithms, electric cargo vehicle adoption, sidewalk robot commercial deployments, and cargo drone regulatory approvals combining to improve same-day delivery cost structures, and what per-delivery cost reduction milestones must be achieved to make same-day delivery commercially viable for average-value consumer orders without premium delivery surcharges or subsidized pricing?

- Which regional same-day delivery markets, specifically Asia-Pacific, North America, and Europe, are expected to generate the highest incremental infrastructure investment through 2034, and what combinations of urban population density, consumer delivery speed expectations, e-commerce penetration rates, on-demand platform investment, and autonomous delivery technology regulatory readiness are defining market growth trajectories and infrastructure investment priorities in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Last-Mile Cost Escalation, Courier Labour Shortage & Unit Economics Viability Risk

- Urban Congestion, Traffic Restriction & Delivery Time Window Compliance Risk

- Real Estate Cost, Dark Store & Micro-Fulfilment Centre Availability Risk

- Consumer Demand Fluctuation, Seasonality & Same-Day Service Profitability Risk

- Regulatory Restriction on Delivery Vehicles, Gig Worker Classification & Labour Law Risk

- Competitive Pressure, Market Saturation & Unsustainable Discounting Risk

- Regulatory Framework & Standards

- Urban Low-Emission Zone (LEZ), Zero-Emission Delivery Zone & Last-Mile Vehicle Access Restriction Regulatory Frameworks

- Gig Economy, Independent Contractor Classification & Platform Worker Rights Regulatory Frameworks by Jurisdiction

- Drone Delivery Regulation: FAA Part 135, EASA U-Space & National BVLOS Operational Approval Frameworks

- Autonomous Delivery Robot (ADR) Street Access, Pavement Use & Sidewalk Robot Regulatory Frameworks

- Food Safety, Cold Chain Compliance & Perishable Goods Transport Regulatory Standards for Same-Day Delivery

- Dark Store Zoning, Urban Logistics Hub Planning Permission & Last-Mile Facility Regulatory Frameworks

- Global Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Number of Same-Day Deliveries & Parcels per Year)

- Market Size & Forecast by Infrastructure Type

- Urban Fulfilment Centres & Dark Stores

- Micro-Fulfilment Centres (MFCs) & In-Store Fulfilment Nodes

- Urban Consolidation Centres (UCCs) & Cross-Dock Transhipment Hubs

- Parcel Lockers, Smart Kiosks & Out-of-Home (OOH) Delivery Points

- Returns Processing Centres & Reverse Logistics Hubs

- Delivery-as-a-Service (DaaS) Platform & Courier Fleet Infrastructure

- Drone Delivery Network Infrastructure

- Autonomous Delivery Robot (ADR) Network & Charging Infrastructure

- Market Size & Forecast by Delivery Mode

- Human Courier (Gig, Employed & Crowd-Sourced) Delivery

- E-Cargo Bike & Electric Two-Wheeler Delivery

- Electric Van & Light Commercial Vehicle (LCV) Delivery

- Autonomous Ground Delivery Robot (Sidewalk & Road-Going)

- Drone & UAV Last-Mile Delivery

- Hybrid Autonomous-Human Handoff Delivery Models

- Market Size & Forecast by Technology

- Route Optimisation, Dynamic Dispatch & Real-Time Traffic Intelligence Software

- Warehouse Automation & Robotic Picking for Rapid Fulfilment

- AI Demand Forecasting, Inventory Pre-Positioning & Dark Store Replenishment Technology

- Delivery Tracking, Real-Time Visibility & Customer Communication Platforms

- Drone Fleet Management, UTM (Urban Traffic Management) & BVLOS Control Systems

- Autonomous Robot Navigation, SLAM & Last-Metre Delivery Technology

- Market Size & Forecast by Product Category Delivered

- Grocery, Fresh Food & Perishable Products

- Pharmacy, Healthcare & Over-the-Counter (OTC) Products

- Fashion, Apparel & Consumer Electronics

- Restaurant Meals & Food Delivery

- Documents, Small Parcels & General Merchandise

- Flowers, Gifts & Occasion-Specific Products

- Market Size & Forecast by Geography Served

- Dense Urban Core & City Centre Delivery Zones

- Suburban & Peri-Urban Delivery Zones

- Secondary Cities & Mid-Tier Urban Markets

- Rural & Remote Same-Day Delivery (Drone-Enabled)

- Market Size & Forecast by End-User

- E-Commerce Retailers & Online Marketplaces

- Grocery & Supermarket Chains

- Quick Commerce (Q-Commerce) & Instant Grocery Platforms

- Food Delivery & Restaurant Aggregator Platforms

- Pharmacy Chains & Healthcare Product Providers

- Fashion, Apparel & Consumer Electronics Retailers

- Third-Party Logistics (3PL) & Parcel Carrier Operators

- Market Size & Forecast by Revenue Model

- Per-Delivery Fee & Consumer-Paid Delivery Charge Model

- Retailer-Subsidised Free Same-Day Delivery Subscription Model

- Platform Commission & Marketplace Merchant Fee Model

- Infrastructure-as-a-Service & Fulfilment-as-a-Service (FaaS) Model

- North America Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Europe Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Asia-Pacific Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Latin America Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Middle East & Africa Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- Country-Wise* Same-Day Delivery Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Number of Same-Day Deliveries & Parcels per Year)

- By Infrastructure Type

- By Delivery Mode

- By Technology

- By Product Category Delivered

- By Geography Served

- By End-User

- By Country

- By Revenue Model

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, United Kingdom, Germany, France, Netherlands, Spain, Italy, Sweden, China, Japan, South Korea, India, Australia, Singapore, Indonesia, Brazil, Mexico, Saudi Arabia, UAE, South Africa

- Technology Landscape & Innovation Analysis

- Dark Store & Micro-Fulfilment Technology Deep-Dive: Layout Design, Robotic Picking, Slotting Optimisation & Throughput Economics

- AI Route Optimisation & Dynamic Dispatch Technology: Multi-Courier, Multi-Stop & Real-Time Reoptimisation for Same-Day Fleets

- Drone Delivery Technology: Fixed-Wing vs. Multirotor, BVLOS Capability, Payload Range & Urban Air Traffic Management

- Autonomous Sidewalk Delivery Robot Technology: Navigation, Obstacle Avoidance, Geofencing & Multi-Unit Fleet Management

- Hyperlocal Demand Forecasting & AI-Based Pre-Positioning Technology for Same-Day Inventory Management

- Electric Cargo Bike, E-Moped & Light EV Technology for Urban Last-Mile Delivery Fleet Electrification

- Digital Twin & Simulation Technology for Urban Logistics Network Design & Same-Day Capacity Planning

- Patent & IP Landscape in Same-Day Delivery Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Retail Inventory, Demand Sensing & Pre-Positioning into Urban Fulfilment Nodes Supply Chain

- Dark Store & MFC Real Estate, Fit-Out, Automation Equipment & Facility Management Supply Chain

- Delivery Fleet: EV, E-Bike, Drone, Robot Procurement, Charging & Maintenance Supply Chain

- Route Optimisation, Dispatch & Last-Mile Technology Platform Supply Chain

- Packaging, Cold Chain, Insulated Bag & Perishable Handling Material Supply Chain

- Gig Courier, Employed Driver & Crowdsource Delivery Worker Engagement Channel

- Parcel Locker, OOH Network & Access Point Infrastructure Supply Chain

- Pricing Analysis

- Same-Day Delivery Consumer Fee Benchmarking by Market, Category & Speed Tier

- Full Cost-per-Delivery Analysis: Fulfilment, Sortation, Last-Mile Labour & Fleet Cost Structure

- Dark Store & Micro-Fulfilment Centre Capital & Operating Cost per Square Metre Analysis

- Drone vs. Human Courier Cost-per-Delivery Comparison & Break-Even Volume Analysis

- Subscription vs. Pay-per-Delivery Model Revenue & Margin Comparison Analysis

- Path-to-Profitability Analysis: Unit Economics, Density Effects & Volume Threshold for Same-Day Service Viability

- Sustainability & Environmental Analysis

- Carbon Footprint of Same-Day Delivery: Emissions per Parcel Analysis by Delivery Mode & Urban Density

- Fleet Electrification Roadmap: E-Van, E-Cargo Bike, Drone & Robot Adoption for Net Zero Last-Mile Delivery

- Packaging Waste, Single-Use Plastic & Sustainable Packaging Standards for Same-Day & Quick Commerce Delivery

- Urban Congestion Impact, Traffic Generation & City Partnership Strategies for Sustainable Last-Mile Operations

- SDG 11 (Sustainable Cities), SDG 12 (Responsible Consumption) & ESG Reporting Standards for Delivery Operators

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Delivery Mode & Geography

- Player Classification

- Integrated E-Commerce Retailer & Marketplace Own-Delivery Networks

- Quick Commerce & Instant Grocery Delivery Platform Operators

- Pure-Play Same-Day & On-Demand Delivery Platform Operators

- Traditional Parcel Carriers & Postal Operators Expanding into Same-Day

- Dark Store, MFC & Urban Fulfilment Technology & Real Estate Operators

- Drone & Autonomous Last-Mile Delivery Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Delivery Mode & Region

- Company Profile

- Company Overview & Headquarters

- Same-Day Delivery Infrastructure, Platform & Service Portfolio

- Key Customer Relationships & Retail Partner Network

- Network Footprint, Number of Dark Stores/MFCs & Delivery Zone Coverage

- Revenue (Same-Day Delivery Segment) & Funding Raised

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Market Launches, Fleet Expansion, Technology Deployments)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Delivery Speed vs. Geographic Coverage)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Delivery Mode, Product Category, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Network Infrastructure, Dark Store Expansion & Fulfilment Footprint Strategy

- Technology Investment, Automation & Route Optimisation Strategy

- Geographic Expansion & New City Market Entry Strategy

- Retail Partner, Merchant & Customer Engagement Strategy

- Partnership, M&A & Last-Mile Ecosystem Strategy

- Sustainability, Fleet Electrification & Green Delivery Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output