Market Definition

The Global Smart Leakage Detection Technologies Market encompasses the design, development, manufacturing, deployment, and operational service of advanced sensor systems, acoustic monitoring platforms, pressure and flow analytics solutions, artificial intelligence-powered data processing software, and integrated network management platforms used to identify, localize, quantify, and predict fluid and gas leakage events within water distribution networks, natural gas transmission and distribution pipelines, oil and petroleum product pipelines, industrial process pipelines, district heating and cooling networks, and building plumbing infrastructure. Smart leakage detection is distinguished from conventional passive leak inspection methods by its continuous real-time or near-real-time monitoring capability, its ability to pinpoint leak location with precision sufficient to guide targeted excavation or intervention without widespread infrastructure disruption, its integration of multi-source sensor data through cloud-based analytics platforms and machine learning algorithms that reduce false alarm rates and improve detection sensitivity for small and incipient leaks, and its connectivity to supervisory control and data acquisition systems and network digital twin models that enable predictive and condition-based maintenance responses. The technology portfolio within this market spans acoustic correlators and noise loggers that detect the characteristic sound signature of leaking fluid escaping under pressure, transient flow monitoring systems that identify pressure wave anomalies caused by pipe bursts or significant leakage events, smart metering infrastructure with district metered area flow balance analysis capabilities, fiber optic distributed sensing systems that detect ground temperature and vibration anomalies along pipeline routes, satellite and airborne remote sensing platforms using infrared and multispectral imaging to detect ground moisture and vegetation stress patterns associated with subsurface water leakage, and drone-based inspection systems carrying gas sensors for natural gas distribution network leak surveys. Key participants include smart sensor manufacturers, pipeline monitoring technology developers, water utility technology providers, industrial automation companies, data analytics software developers, system integrators, and municipal and industrial asset owners deploying smart leakage detection infrastructure.

Market Insights

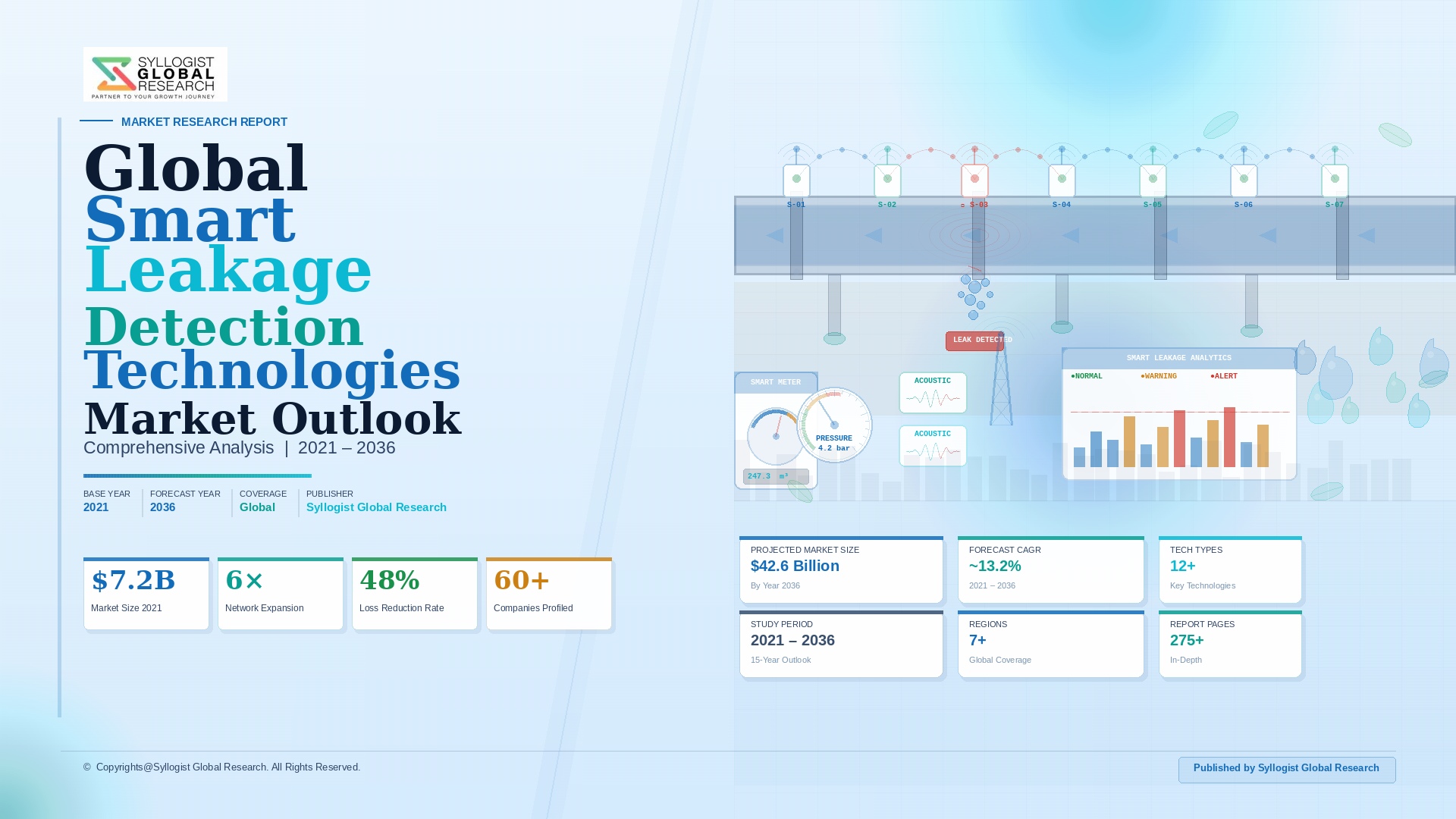

The global smart leakage detection technologies market was valued at approximately USD 4.8 billion in 2025 and is projected to reach USD 12.6 billion by 2034, advancing at a compound annual growth rate of 11.2% over the forecast period from 2027 to 2034, driven by the escalating global water scarcity crisis that makes non-revenue water losses from leaking distribution infrastructure a financially and operationally unacceptable drain on utility resources, the accelerating digitalization of utility asset management through smart infrastructure investment programs, the regulatory tightening of leakage performance obligations imposed on water and gas utilities across Europe, North America, and Asia-Pacific, and the rapidly declining cost of acoustic sensor hardware, wireless communication modules, and cloud-based analytics platforms that is democratizing smart leakage detection deployment beyond the largest metropolitan water utilities toward mid-sized and smaller distribution network operators. Global non-revenue water losses from urban water distribution systems are estimated at approximately 126 billion cubic meters annually, representing approximately 30% of total water injected into distribution networks worldwide and carrying an economic value of approximately USD 39 billion per year in treated water production cost that is wholly unrecovered by water utilities, with the highest non-revenue water rates concentrated in aging distribution network infrastructure in Eastern Europe, the Middle East, Latin America, and South and Southeast Asia where pipe asset replacement backlogs, limited pressure management investment, and inadequate leakage monitoring capabilities combine to sustain chronically high real losses that are increasingly unsustainable in the context of water resource stress and utility financial viability pressures. The global natural gas distribution network leakage segment is growing at approximately 13.4% annually within the broader smart leakage detection market, driven by methane emission reduction regulatory obligations, net-zero infrastructure commitments of gas network operators, and the high global warming potential of methane that makes even small fugitive gas losses a disproportionate contributor to the climate impact of gas network infrastructure relative to the energy value of gas lost.

The water utility segment constitutes the largest application category within the global smart leakage detection technologies market, accounting for approximately 47% of total market revenue in 2025, anchored by the extensive smart leakage detection deployment programs undertaken by water utilities across the United Kingdom, Germany, Netherlands, Australia, Japan, Singapore, and the United States that are progressively transitioning from periodic manual acoustic survey methods toward permanent wireless acoustic noise logger networks providing continuous monitoring coverage of entire distribution zones. United Kingdom water utilities operate under a legally binding regulatory framework administered by the Water Services Regulation Authority that sets company-specific economic level of leakage targets updated at each five-year price review cycle, with the 2020 to 2025 regulatory period requiring sustained leakage reduction investment across all regulated companies, and the 2025 to 2030 price review introducing more stringent sustainability-based leakage targets that have allocated approximately USD 3.8 billion in regulatory capital expenditure allowances specifically for leakage reduction and smart network monitoring investment across the sector. The district metered area approach, which divides water distribution networks into discrete hydraulic zones monitored by flow meters at zone entry and exit points enabling continuous minimum night flow analysis to identify and quantify leakage, is being augmented by permanent acoustic noise logger installations at hydrant and fitting locations throughout each district metered area, creating a multi-layer monitoring architecture that reduces the average leak run time from detection to repair from over 180 days in networks relying solely on manual survey to below 30 days in fully instrumented smart networks, delivering proportional reductions in real loss volumes and associated water production and pumping energy costs that typically yield payback periods of three to five years on smart monitoring infrastructure investment.

Artificial intelligence and machine learning integration is fundamentally transforming the commercial value proposition of smart leakage detection technologies by enabling pattern recognition across multi-dimensional sensor data streams that substantially reduces false positive alarm rates, improves leak location accuracy to within meters rather than tens of meters, and enables predictive leakage risk modeling that identifies pipe segments with elevated probability of imminent failure based on historical break records, material age, soil conditions, pressure cycling history, and hydraulic stress indicators, allowing utilities to prioritize proactive intervention programs before detectable leakage occurs rather than reacting to reported bursts and service disruptions. Machine learning-based acoustic analysis platforms deployed by leading technology providers including Echologics, Primayer, Gutermann, and Mueller Water Products are achieving leak localization accuracies of within five meters for pressurized water mains using correlator algorithms that analyze the cross-correlation of acoustic signals recorded at multiple sensor nodes simultaneously, enabling confident excavation targeting without the extensive exploratory digging that inflated repair costs and customer disruption impact under conventional survey methods. The integration of smart leakage detection sensor data with geographic information system pipeline asset registers, hydraulic network models, and maintenance management systems within unified digital water network management platforms is creating a new category of intelligent network operations capability that extends beyond reactive leak detection toward predictive infrastructure management, with leading water utility technology platform providers including Xylem Vue, Itron, Sensus, and Suez Advanced Solutions offering integrated leakage intelligence platforms that combine sensor data acquisition, cloud analytics, asset risk scoring, and maintenance workflow management within single subscription software environments accessible to network operations teams without requiring specialist data science capabilities.

The oil and gas pipeline leakage detection segment represents a high-value and technically demanding application category within the smart leakage detection market, accounting for approximately 28% of total market revenue in 2025 and growing at approximately 12.8% annually, driven by increasingly stringent pipeline integrity management regulations following high-profile pipeline failure incidents, the commercial imperative of minimizing hydrocarbon product loss from gathering, transmission, and distribution networks, and the environmental liability exposure of undetected pipeline releases that can result in regulatory penalties, remediation costs, and reputational damage disproportionate to the volume of fluid released when leaks go undetected for extended periods. Regulatory frameworks including the United States Pipeline and Hazardous Materials Safety Administration integrity management program requirements, the European Union’s Gas and Hydrogen Infrastructure Regulation provisions for leak detection obligations, and methane emission reporting and reduction obligations under the United States Securities and Exchange Commission climate disclosure rules and the European Union’s Methane Regulation create a multi-layered compliance environment that mandates continuous or periodic leak detection capability across different pipeline categories, distance classes, and proximity to high-consequence areas that collectively encompass the majority of commercially significant oil and gas transmission and distribution infrastructure globally. Fiber optic distributed acoustic sensing technology, which transforms the entire length of an optical fiber cable installed alongside a pipeline into a continuously interrogated distributed sensor capable of detecting acoustic emissions from leaks, unauthorized third-party interference, pig passage, and ground movement events with precise location identification to within meters over cable lengths of up to 100 kilometers per interrogator unit, is experiencing the fastest adoption growth within the oil and gas pipeline monitoring segment as its combination of continuous coverage, precise localization, and multi-hazard detection capability addresses the comprehensive integrity monitoring requirements of high-consequence pipeline routes at per-kilometer costs that are declining rapidly as fiber optic interrogator hardware scales in production volume.

Key Drivers

Escalating Global Water Scarcity, Non-Revenue Water Financial Losses, and Regulatory Leakage Performance Obligations Compelling Smart Monitoring Investment by Water Utilities Worldwide

The convergence of accelerating global water scarcity driven by climate change-induced precipitation variability and groundwater depletion, the staggering financial scale of non-revenue water losses estimated at USD 39 billion per year globally representing approximately 30% of total water injected into distribution networks, and the tightening of legally binding leakage reduction targets imposed on water utilities by economic regulators in the United Kingdom, Australia, Netherlands, Singapore, and increasingly across the United States and Asia-Pacific is creating a compelling and commercially durable investment case for smart leakage detection technology deployment that simultaneously addresses financial sustainability, environmental stewardship, and regulatory compliance objectives for water network operators. Water utilities operating aging distribution infrastructure face a particularly acute leakage challenge, with network pipe materials including cast iron, asbestos cement, and unlined ductile iron installed between 1930 and 1970 experiencing accelerating deterioration and increasing burst frequency that drives both visible service disruptions and significant background leakage through micro-fissures and joint deterioration that is only detectable through sensitive continuous acoustic monitoring, creating a structural demand for smart leakage detection as an essential component of aging infrastructure management programs that must simultaneously identify the highest-loss network zones for priority rehabilitation while minimizing leakage from pipes not yet scheduled for replacement. The economic return on smart leakage detection investment for water utilities is directly quantifiable through the reduction in water production, treatment, and pumping energy costs achieved by reducing leakage volumes, with a utility reducing annual leakage by 10 million cubic meters through smart detection-enabled faster repair generating annual cost savings of approximately USD 2 to USD 4 million depending on local water production cost, typically yielding payback periods well within the operational lifetime of deployed monitoring infrastructure.

Accelerating Utility Digitalization, Smart Infrastructure Investment Programs, and Internet of Things Sensor Cost Reduction Enabling Mass Deployment of Continuous Leakage Monitoring Networks

The accelerating digitalization of utility infrastructure management through smart water network investment programs, advanced metering infrastructure rollouts, and the integration of operational technology with information technology platforms is creating a favorable institutional and technological environment for mass deployment of smart leakage detection sensor networks that leverage shared communication infrastructure, cloud analytics platforms, and digital twin network models originally deployed for metering, pressure management, and network optimization purposes, reducing the incremental cost and operational complexity of adding permanent leakage monitoring capability to utility digital infrastructure portfolios. The dramatic reduction in unit cost of wireless acoustic noise loggers from approximately USD 800 to USD 1,200 per device in 2015 to approximately USD 180 to USD 380 per device in 2025 driven by electronics miniaturization, low-power microcontroller advancement, and LPWAN communication module commoditization through NB-IoT and LoRaWAN standards, has fundamentally changed the economics of dense noise logger deployment across entire distribution networks rather than the selective deployment of smaller numbers of high-cost devices at predicted high-leakage zones that characterized earlier smart leakage monitoring practice. Government infrastructure investment programs including the United States Infrastructure Investment and Jobs Act’s USD 55 billion water infrastructure allocation, the European Union’s cohesion and structural funds supporting water network modernization across member states, and national smart water initiative funding programs in Singapore, Japan, Australia, and South Korea are providing substantial grant co-financing for smart leakage detection deployment that accelerates adoption by reducing the net capital cost burden on utility balance sheets and enabling technology deployment programs at scales that would not be commercially self-justifiable on utility investment returns alone within regulatory pricing constraint frameworks.

Stringent Methane Emission Reduction Regulations and Net-Zero Commitments by Gas Network Operators Driving Mandatory Fugitive Gas Leakage Detection Program Investment

The regulatory and corporate commitment imperative to reduce methane emissions from gas distribution and transmission infrastructure is generating a structurally new and rapidly growing demand stream for smart gas leakage detection technologies, driven by the extraordinarily high global warming potential of methane at approximately 84 times that of carbon dioxide over a 20-year horizon, the magnitude of estimated annual methane losses from global gas distribution networks at approximately 2.5 million metric tons per year, and the progressive tightening of methane emission reporting and reduction obligations under the United States Environmental Protection Agency methane regulations, the European Union Methane Regulation applicable to the energy sector from 2024, and the Global Methane Pledge commitment by over 150 countries to reduce global methane emissions by 30% below 2020 levels by 2030 across all sectors including the energy sector. Gas network operators in the United States, European Union, United Kingdom, and Japan are investing in advanced mobile and fixed leakage detection platforms including laser absorption spectroscopy instruments, cavity ring-down spectroscopy sensors, tunable diode laser analyzers, and drone-mounted methane imaging cameras that enable rapid and quantitative survey of large distribution network footprints at sensitivity levels capable of detecting leaks of less than 0.1 standard cubic feet per hour, substantially more sensitive than legacy flame ionization detector survey methods that have historically missed a significant proportion of small but continuous background leakage events that collectively represent a large share of total network methane loss. Regulatory methane loss measurement, reporting, and verification obligations are also creating demand for automated continuous emission monitoring systems at compressor stations, metering and regulation facilities, and urban distribution network assets that generate auditable emissions data required for regulatory compliance submissions and sustainability disclosure reporting.

Key Challenges

High False Positive Alarm Rates, Acoustic Signal Interference in Complex Urban Pipeline Environments, and Operator Alert Fatigue Undermining the Operational Value of Smart Leakage Detection Systems

The operational effectiveness of smart leakage detection systems deployed in real-world distribution network environments is systematically challenged by the prevalence of acoustic noise sources unrelated to pipe leakage that generate signals closely resembling leak signatures within the frequency ranges monitored by noise loggers and acoustic correlators, including traffic vibration, soil settlement, valve operation, pump cycling, air valve discharge, animal intrusion, and third-party excavation activity, creating false positive alert generation rates that can exceed genuine leak detections by factors of five to ten in densely urbanized network environments where background acoustic noise levels are elevated and variable throughout the day and week. High false positive rates impose significant operational costs on water utility network operations teams who must dispatch field crews to investigate each alert, with investigation costs of approximately USD 250 to USD 800 per site visit and a false alarm investigation rate that can consume a substantial proportion of network operations labor capacity at utilities deploying large noise logger networks without sufficiently sophisticated signal processing algorithms to filter spurious alerts before escalation to operational workflows. While artificial intelligence signal classification algorithms have substantially improved false positive rejection performance at leading technology providers, the diversity of pipe material, diameter, soil type, burial depth, water pressure, and urban noise environment combinations encountered across real distribution networks means that algorithm training and calibration requirements are highly site-specific, requiring sustained investment in local signal library development and model refinement before detection systems achieve operationally reliable performance levels, creating a significant commissioning and optimization overhead that adds time and cost to smart leakage detection deployments and can delay realization of the asset management benefits that justified initial technology investment.

Fragmented Legacy Pipeline Asset Data, Incomplete Geographic Information System Records, and Poor Network Hydraulic Model Accuracy Limiting the Effectiveness of Data-Driven Leakage Analytics

The effectiveness of smart leakage detection analytics platforms that integrate sensor data with pipeline asset registers, hydraulic network models, and geographic information system databases to produce leak risk scores, network loss quantification, and targeted maintenance recommendations is fundamentally dependent on the quality, completeness, and accuracy of underlying asset information that in many utility organizations reflects decades of incomplete record-keeping, inconsistent data entry standards, missing pipe material and installation date records, inaccurate network topology representations, and hydraulic model calibration deficiencies that substantially degrade the performance of data-driven leakage management applications relative to their theoretical capability under ideal data quality conditions. Water utility asset records in many developing and emerging market network operators, and in a significant proportion of smaller utilities in developed markets, contain material gaps including unregistered service connections, undocumented historic pipe modifications, absent fitting and valve location data, and pressure zone boundary uncertainties that prevent reliable minimum night flow analysis, accurate acoustic correlation distance calculation, and meaningful leak risk prioritization using asset condition indicators, limiting these organizations to the most basic reactive alert response functionality from their smart leakage detection deployments rather than the predictive and optimization-oriented applications that generate the highest return on investment. The capital and operational investment required to develop, verify, and maintain the comprehensive and accurate pipeline asset information foundation necessary to unlock full smart leakage detection platform value, including ground-penetrating radar surveys to locate unregistered infrastructure, physical network audits to verify geographic information system accuracy, hydraulic model recalibration programs, and ongoing data governance processes, represents a substantial pre-requisite cost that many utilities do not adequately account for in smart leakage detection technology business cases and that delays or limits the achievement of projected performance and return on investment outcomes.

Cybersecurity Vulnerabilities in Internet-Connected Leakage Detection Infrastructure and Data Privacy Challenges Associated with Continuous High-Resolution Network Monitoring

The integration of smart leakage detection sensor networks with cloud analytics platforms, supervisory control and data acquisition systems, and advanced metering infrastructure through wireless and internet-connected communication pathways introduces significant cybersecurity attack surface expansion into water and gas utility operational technology environments that have historically operated as isolated closed-loop control systems with limited external network connectivity, creating new categories of cyber risk including unauthorized remote access to leak detection sensor networks enabling false alarm generation or alarm suppression to conceal deliberate infrastructure damage, interception of network hydraulic performance data revealing sensitive operational patterns exploitable for malicious interference planning, and potential lateral movement from compromised leakage detection communication infrastructure into connected operational technology systems controlling pumping stations, pressure management facilities, and chemical dosing systems. Water and gas utility cybersecurity programs must navigate the inherent tension between the cloud connectivity and remote access capabilities that are essential features of smart leakage detection platforms delivering the data aggregation, analytics processing, and remote configuration functions that differentiate smart monitoring from conventional survey approaches, and the operational technology security principle of network segmentation and restricted external connectivity that represents the fundamental defense against cyber intrusion into control systems governing critical national infrastructure. Regulatory requirements for critical infrastructure cybersecurity including the United States Environmental Protection Agency cybersecurity assessment obligations under the Safe Drinking Water Act, the European Union’s Network and Information Security Directive 2 requirements applicable to water and gas utilities, and sector-specific cybersecurity frameworks in the United Kingdom, Australia, and Singapore are increasing the compliance cost and technical complexity of deploying internet-connected smart leakage detection systems in a manner consistent with regulatory security obligations, adding cybersecurity architecture design, penetration testing, incident response planning, and ongoing security monitoring requirements to the total cost of smart leakage detection program ownership.

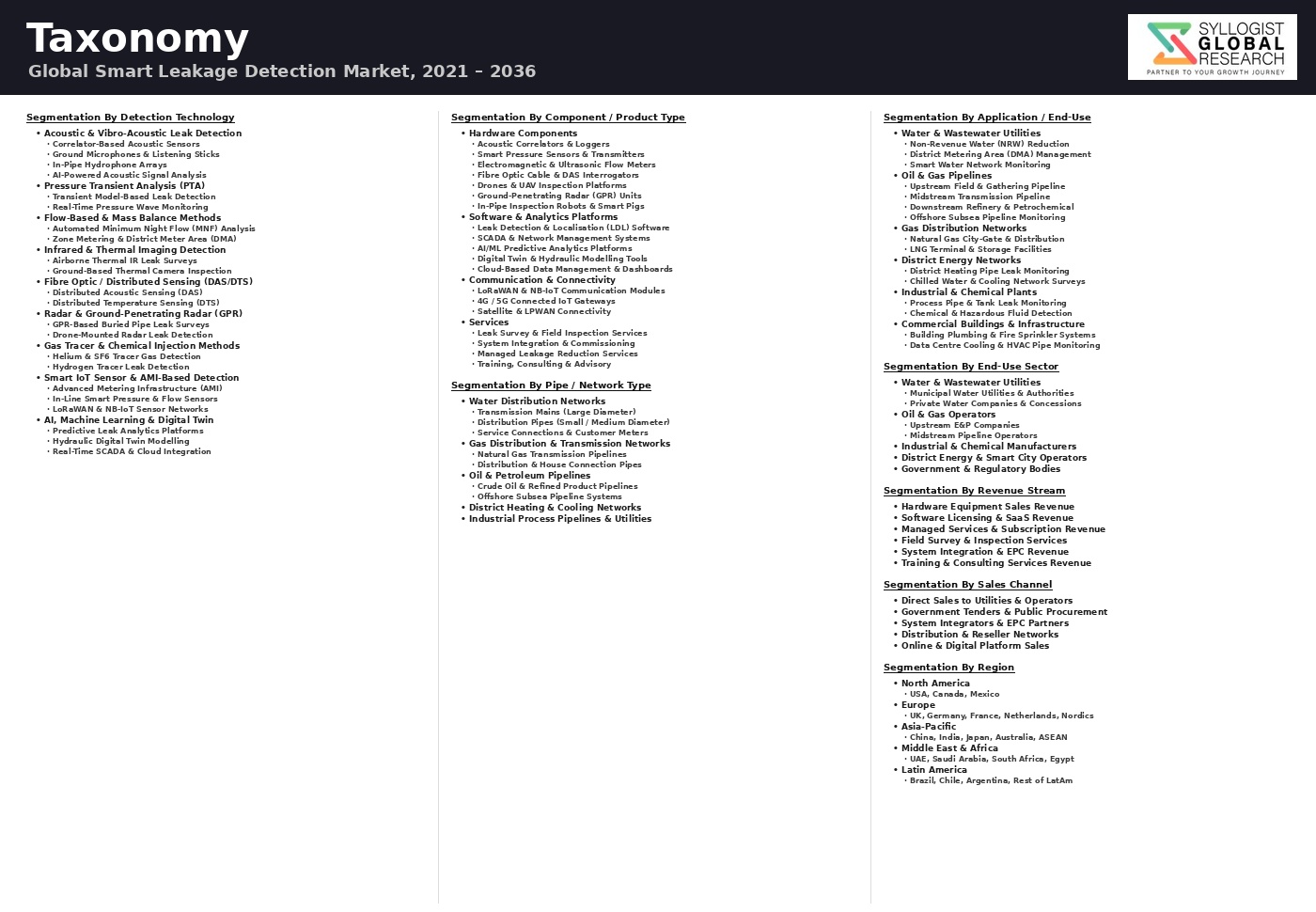

Market Segmentation

- Segmentation By Technology Type

- Acoustic Noise Loggers and Correlators

- Pressure Transient and Wave Analysis Systems

- Smart Flow Meters and District Metered Area Monitoring Systems

- Fiber Optic Distributed Acoustic and Temperature Sensing

- Satellite and Airborne Remote Sensing (Infrared and Multispectral Imaging)

- Drone-Based Gas and Leak Detection Systems

- Laser Absorption Spectroscopy and Cavity Ring-Down Spectroscopy Gas Sensors

- Artificial Intelligence and Machine Learning Analytics Platforms

- Digital Twin and Hydraulic Network Modeling Integration Platforms

- Others

- Segmentation By Application

- Water Distribution Network Leakage Detection

- Natural Gas Distribution and Transmission Pipeline Monitoring

- Oil and Petroleum Product Pipeline Integrity Monitoring

- District Heating and Cooling Network Leakage Detection

- Industrial Process Pipeline and Facility Monitoring

- Building and Commercial Plumbing Leakage Detection

- Wastewater and Sewer Network Infiltration Detection

- Others

- Segmentation By Component

- Hardware (Sensors, Loggers, Meters, and Communication Modules)

- Software (Analytics Platforms, Digital Twin Models, and Network Management Systems)

- Services (Installation, Commissioning, Managed Monitoring, and Maintenance)

- Segmentation By Communication Technology

- Narrowband Internet of Things (NB-IoT)

- LoRaWAN and Low Power Wide Area Network

- Cellular (4G LTE and 5G)

- Fixed-Line and Fiber Optic Communication

- Satellite Communication (Remote and Rural Pipeline Applications)

- Others

- Segmentation By End User

- Municipal and Public Water Utilities

- Private Water Service Providers and Concessionaires

- Natural Gas Distribution and Transmission Network Operators

- Oil and Gas Pipeline Operators

- District Energy Network Operators

- Industrial Facilities and Process Plant Operators

- Building Owners, Facility Managers, and Real Estate Operators

- Government and Regulatory Bodies (Compliance and Performance Monitoring)

- Others

- Segmentation By Deployment Model

- Permanent Fixed Network Monitoring Infrastructure

- Mobile and Periodic Survey-Based Detection

- Cloud-Based Managed Detection as a Service

- Hybrid Fixed and Mobile Detection Programs

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Smart Leakage Detection Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type including acoustic noise loggers, pressure transient analysis, fiber optic distributed sensing, satellite and drone-based remote sensing, and artificial intelligence analytics platforms, and by application including water distribution, natural gas distribution and transmission, oil and petroleum product pipelines, district heating networks, and industrial process pipelines, to enable technology developers, water and gas utilities, pipeline operators, infrastructure investors, and regulatory bodies to identify which technology categories and application segments will generate the highest absolute revenue growth and the most commercially durable demand trajectory across the forecast period to 2034?

- How are evolving regulatory leakage performance obligations, including the United Kingdom Water Services Regulation Authority sustainability-based leakage reduction targets within the 2025 to 2030 price review cycle, the European Union Methane Regulation emission reduction obligations applicable to gas network operators from 2024, the United States Pipeline and Hazardous Materials Safety Administration pipeline integrity management requirements, and comparable regulatory frameworks across Australia, Japan, Singapore, and emerging markets, creating compliance-driven investment mandates for smart leakage detection deployment, and what are the estimated aggregate compliance capital expenditure requirements generated by these regulatory frameworks across water and gas utility sectors in each major regulated market through 2034?

- How are artificial intelligence and machine learning algorithm advances reducing false positive alarm rates, improving leak localization accuracy, enabling predictive pipe failure risk scoring, and extending smart leakage detection platform value from reactive leak response toward proactive infrastructure management, and which technology providers including Echologics, Primayer, Gutermann, Mueller Water Products, Xylem, Itron, Sensus, and Pure Technologies are leading the integration of sensor data acquisition, cloud analytics, asset risk scoring, digital twin network modeling, and maintenance workflow management within unified intelligent leakage management platforms, and what are the differentiated technical capabilities and commercial positioning strategies of these market participants across water utility, gas network, and oil pipeline application segments?

- What are the non-revenue water volumes, leakage rates expressed as percentage of system input volume, economic value of water losses, and smart leakage detection technology adoption status across the major water utility markets in the United Kingdom, Germany, Netherlands, United States, Australia, Japan, Singapore, India, China, Brazil, and the Middle East, and which market segments combining high non-revenue water economic loss, regulatory leakage reduction pressure, utility digital infrastructure maturity, and available capital investment capacity represent the most commercially attractive near-term growth opportunities for smart leakage detection technology providers seeking to prioritize geographic market expansion and customer acquisition investment through 2034?

- What are the cybersecurity architecture requirements, operational technology network segmentation approaches, regulatory compliance obligations under the European Union Network and Information Security Directive 2 and equivalent critical infrastructure cybersecurity frameworks in the United States, United Kingdom, and Australia, and the data privacy considerations associated with continuous high-resolution hydraulic performance monitoring that smart leakage detection system deployers and water and gas utility technology procurement managers must address to ensure that internet-connected smart monitoring infrastructure can be deployed in a manner consistent with critical national infrastructure security obligations, and how are leading technology providers incorporating cybersecurity by design principles, secure communication protocols, and remote access management capabilities into their smart leakage detection product architectures to meet the evolving security requirements of utility customers operating under mandatory critical infrastructure protection frameworks?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Integration & Interoperability Risk

- Data Security, Cybersecurity & Privacy Risk

- Regulatory & Compliance Risk

- Market & Demand Risk

- Environmental & Operational Liability Risk

- Regulatory Framework & Standards

- Water Network Leakage Reduction Mandates, Non-Revenue Water (NRW) Targets & Utility Regulatory Frameworks

- Oil & Gas Pipeline Integrity Management, Leak Detection Regulations & SCADA Safety Standards

- Industrial Hazardous Fluid, Chemical Plant & Pressure Vessel Leak Detection Safety Standards

- Building & Infrastructure Plumbing, Gas Detection Safety & Fire Code Compliance Standards

- IoT Device Security, Data Communication Protocol Standards & Environmental Monitoring Regulations

- Global Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Deployed & Sensors Installed)

- Market Size & Forecast by Technology Type

- Acoustic & Vibro-Acoustic Leak Detection (Correlators, Loggers & Ground Microphones)

- Fibre Optic Distributed Sensing (DAS / DTS / DSS) Leak Detection Systems

- Pressure & Flow Transient Analysis (PTA / TFALDA) Systems

- IoT-Based Smart Sensor Networks (Wireless Pressure, Flow & Moisture Sensor Arrays)

- Infrared (IR) & Thermal Imaging Leak Detection Systems

- Ground-Penetrating Radar (GPR) & Electromagnetic Leak Survey Systems

- Gas Chromatography, Chemical Tracer & Odorant-Based Leak Detection

- AI & Machine Learning-Based Leak Detection & Analytics Platforms

- Drone, UAV & Robotic Pipeline Inspection & Leak Detection Systems

- Satellite & Remote Sensing-Based Leak Detection (Hyperspectral & SAR Imaging)

- Market Size & Forecast by Component

- Hardware (Sensors, Transmitters, Loggers, Correlators & Detection Probes)

- Software & Analytics Platforms (SCADA Integration, Digital Twin, AI/ML & Cloud SaaS)

- Communication & Connectivity Infrastructure (LoRaWAN, NB-IoT, 4G/5G & Satellite)

- Services (Installation, Commissioning, Maintenance, Calibration & Managed Services)

- Market Size & Forecast by Deployment Mode

- Fixed / Permanently Installed Continuous Monitoring Systems

- Portable & Handheld Survey Equipment

- Mobile & Vehicle-Mounted Survey Systems

- Drone / UAV-Deployed Aerial Survey Systems

- Cloud-Based & Software-as-a-Service (SaaS) Remote Monitoring Platforms

- Market Size & Forecast by End-Use Application / Industry

- Water & Wastewater Utilities (Distribution Network, Transmission Main & Sewer Leak Detection)

- Oil & Gas Pipelines (Crude Oil, Natural Gas, LNG, LPG & Refined Product Transmission & Distribution)

- Industrial & Chemical Process Plants (Hazardous Fluid, Cryogenic & Chemical Tank & Pipe Leak Detection)

- Building & Commercial Real Estate (Plumbing, HVAC, Data Centre & Underfloor Leak Detection)

- Power Generation & Nuclear Facilities (Cooling Water, Steam & Fuel Leak Detection)

- Mining & Minerals Processing (Tailings Dam, Process Water & Acid Leak Detection)

- Agriculture & Irrigation Infrastructure (Irrigation Network, Canal & Reservoir Leak Detection)

- Market Size & Forecast by Pipeline / Network Type

- Water Distribution Pipes (Cast Iron, Ductile Iron, PVC, HDPE & Asbestos Cement)

- Oil & Gas Transmission & Distribution Pipelines (Steel, HDPE & Composite)

- District Heating & Cooling Network Pipes

- Industrial Process Piping & Chemical Plant Pipework

- Building Internal Plumbing, Gas Supply & Sprinkler Systems

- Market Size & Forecast by End-User

- Water & Wastewater Utility Operators

- Oil & Gas Pipeline Operators (Midstream & Downstream)

- Industrial & Chemical Plant Operators

- Building Owners, Facilities Managers & Real Estate Developers

- Government, Municipalities & Smart City Programme Operators

- Engineering, Procurement & Construction (EPC) Contractors

- Market Size & Forecast by Sales Channel

- Direct OEM Supply to Utility & Industrial Operators

- System Integrator, EPC & EPCM Contractor Channel

- Distributor, Reseller & Specialist Instrumentation Dealer Network

- Managed Service, Leakage-as-a-Service & Performance Contract Channel

- North America Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Smart Leakage Detection Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed & Sensors Installed)

- By Technology Type

- By Component

- By Deployment Mode

- By End-Use Application / Industry

- By Pipeline / Network Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Italy, Spain, Netherlands, Sweden, China, Japan, South Korea, India, Australia, Singapore, UAE, Saudi Arabia, Israel, South Africa, Brazil, Argentina, Chile

- Technology Landscape & Innovation Analysis

- Acoustic & Vibro-Acoustic Leak Detection Technology Deep-Dive

- Noise Correlator Technology: Cross-Correlation Algorithm Design, Multi-Pipe Material Velocity Calibration & Frequency Band Selection for Water, Gas & Oil Network Applications

- Acoustic Leak Logger Network Design: Wireless Logger Placement Optimisation, Overnight Survey Protocol, Data Aggregation & Central Noise Analysis for Large Distribution Networks

- Step Test & Zone Isolation Methodology: District Metered Area (DMA) Boundary Valve Operation, Minimum Night Flow (MNF) Analysis & Leak Run-Time Modelling

- Ground Microphone & Listening Rod Technology: Contact Microphone Sensitivity, Digital Signal Processing (DSP) Amplification & Real-Time Audio Spectrum Leak Signature Identification

- Advanced Correlation Software Platforms: AI-Enhanced Cross-Correlation, Pipe Material Database Integration, GPS Location Mapping & Cloud-Based Leak Position Reporting

- Fibre Optic Distributed Sensing (DAS / DTS / DSS) Leak Detection Technology

- IoT Smart Sensor Network & Wireless Communication Technology for Leakage Monitoring

- AI, Machine Learning & Digital Twin Analytics Technology for Leak Detection & Prediction

- Infrared Thermal Imaging, GPR & Ground Survey Technology for Buried Infrastructure Leak Detection

- Drone, UAV, Robotic & Satellite Remote Sensing Leak Detection Technology

- Pressure & Flow Transient Analysis (TFALDA) & Hydraulic Modelling Technology

- Patent & IP Landscape in Smart Leakage Detection Technologies

- Acoustic & Vibro-Acoustic Leak Detection Technology Deep-Dive

- Value Chain & Supply Chain Analysis

- Sensor, Transducer, Acoustic Component & Electronic Hardware Supply Chain

- Communication Module, IoT Connectivity & Network Infrastructure Supply Chain

- Software Platform, AI Analytics, Cloud & Digital Twin Technology Supply Chain

- Leak Detection OEM, System Integrator & Solution Provider Landscape

- Utility Operator, Industrial End-User & EPC Contractor Procurement Channel

- Aftermarket Service, Calibration, Maintenance & Managed Service Channel

- End-of-Life Equipment Management, Sensor Recycling & Circular Economy

- Pricing Analysis

- Acoustic Correlator & Leak Logger System Pricing Analysis

- Fibre Optic Distributed Sensing (DAS / DTS) System Pricing Analysis

- IoT Smart Sensor Network & Wireless Monitoring Platform Pricing Analysis

- AI & Software Analytics Platform Pricing Analysis (Licence, SaaS & Per-Sensor Models)

- Drone, UAV & Robotic Pipeline Inspection System Pricing Analysis

- Total System & Managed Service Contract Pricing Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Smart Leakage Detection Technology Hardware & Systems

- Water Loss Reduction, Non-Revenue Water (NRW) Impact & Water Scarcity Sustainability Contribution

- Greenhouse Gas Emission Reduction from Methane & Hydrocarbon Leak Detection in Oil & Gas Infrastructure

- Environmental Contamination Prevention, Soil & Groundwater Protection from Industrial Leak Detection

- Regulatory-Driven Sustainability, Smart Water Network Policy & Climate Adaptation Investment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology Type & End-Use Segment)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Application & Geography

- Player Classification

- Global Integrated Smart Leakage Detection Solution Providers

- Specialist Acoustic Leak Detection Equipment Manufacturers

- Fibre Optic Distributed Sensing System Providers

- IoT Smart Water & Pipeline Monitoring Platform Companies

- AI, Analytics & Digital Twin Software Specialists for Leak Management

- Drone, UAV & Robotic Pipeline Inspection Technology Companies

- Satellite & Remote Sensing Leak Detection Service Providers

- Managed Leakage Service, Water Loss Consultancy & NRW Reduction Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Smart Leakage Detection Products & Technology Portfolio

- Key Customer Relationships & Reference Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Leakage Detection Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Component, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2037)