Global Urban Metro Rail Systems Market By System Type, By Rolling Stock, By Signalling and Train Control, By Component, By Alignment, By Automation Level, By Service Type, By Procurement Model, By End User, By Region, Competition, Forecast & Opportunities, 2021-2034F

Market Definition

The Global Urban Metro Rail Systems Market covers the planning, design, manufacturing, deployment, and operation of mass-transit metropolitan rail networks operating across underground, elevated, and at-grade alignments within urban and metropolitan agglomerations. The scope includes rolling stock such as electric multiple units, light metro vehicles, monorail and rubber-tired metro coaches, and driverless automated trainsets, alongside signalling and train control systems including Communications-Based Train Control, Automatic Train Operation and Protection, train management systems, and centralized operations control centers. The market also covers traction power and electrification infrastructure across third-rail and overhead-catenary configurations, permanent way and trackwork including ballastless track and high-speed switches, tunnelling and civil works delivered through TBM-driven boring and cut-and-cover stations, and viaduct construction for elevated corridors. Station systems including platform screen doors, automated fare collection, passenger information systems, escalators, elevators, and station HVAC are core components, along with integrated depot and maintenance facilities supporting fleet availability. The urban metro rail systems market further encompasses operations and maintenance contracts, lifecycle services, system integration, and turnkey EPC services delivered by rolling stock OEMs, signalling integrators, civil contractors, and dedicated metro operating consortia. End buyers include national rail ministries, metropolitan transport authorities, special-purpose vehicles created for individual corridors, public-private partnership concessionaires, public-sector operators, and multilateral development banks financing urban transit projects. Revenue streams cover capital equipment sales, civil and electromechanical EPC contracts, signalling and rolling stock contracts, farebox and non-farebox operating revenue, long-term maintenance contracts, and digital service revenue from smart ticketing and operations modernization across North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa.

Market Insights

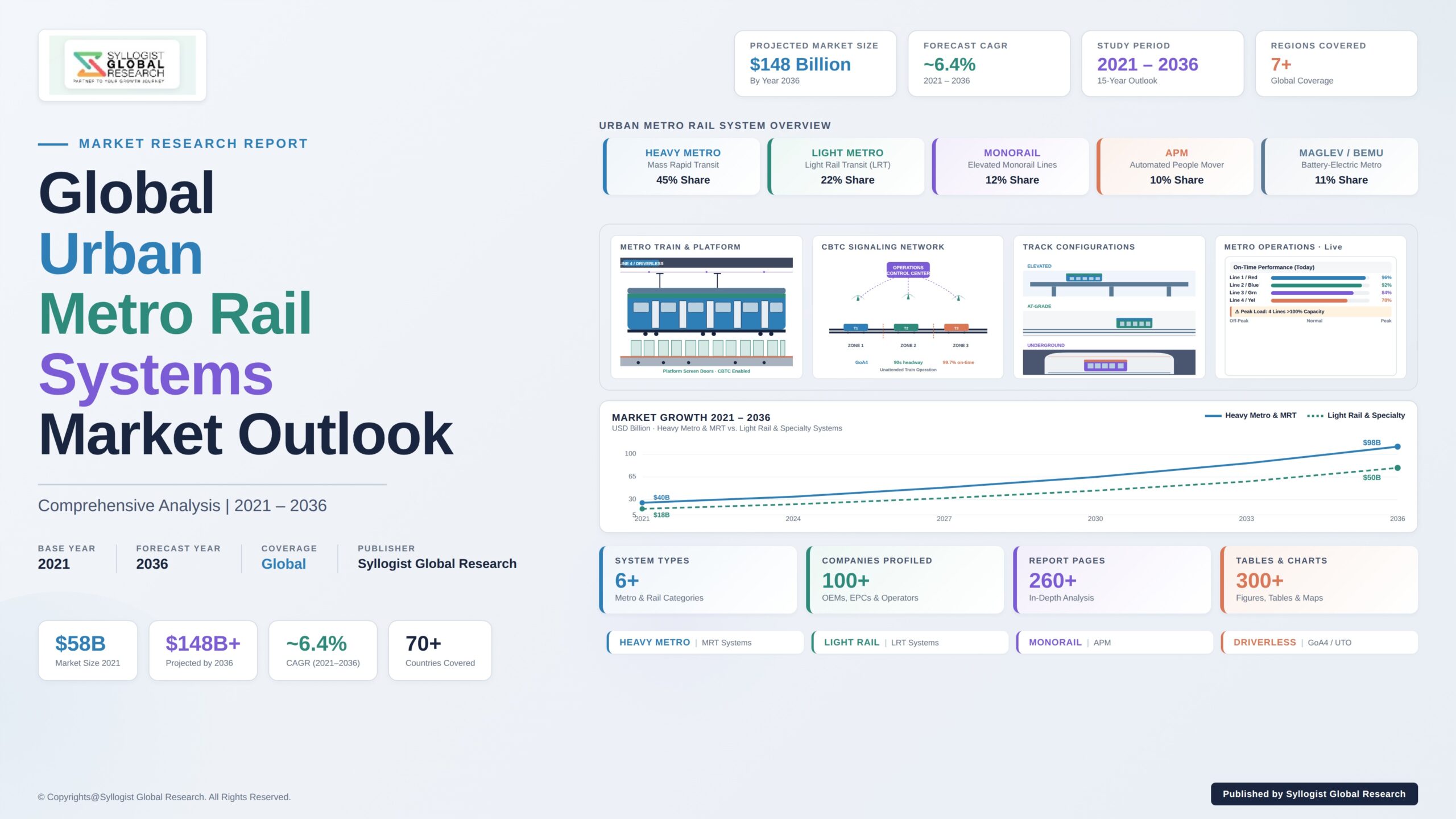

The global urban metro rail systems market is moving into a structural growth phase, shaped by accelerating urbanization in emerging economies, ambitious climate-linked transport decarbonization targets in mature markets, and an exceptionally deep pipeline of metro corridor sanctions across Asia-Pacific, Middle East, and Latin America. The market was valued at approximately USD 67.4 billion in 2025 and is projected to reach USD 142.8 billion by 2034, advancing at a compound annual growth rate of 8.7% through the forecast period, as new line extensions, fleet expansions, signalling modernization programs, and station retrofits move from sanction into procurement and execution across more than 220 active metro corridors globally.

National-level investment is reinforcing this acceleration. India’s Metro Rail Policy 2017, the PM Gati Shakti national master plan, and city-level corridor expansions across Delhi, Mumbai, Bengaluru, Hyderabad, Chennai, Pune, Ahmedabad, Surat, Kanpur, Indore, Patna, Bhopal, and Kochi are channeling sustained capital into rolling stock, signalling, and civil EPC programs. China’s continued metro buildout across more than 50 cities, Saudi Arabia’s NEOM and Riyadh Metro programs, the United Arab Emirates’ Etihad Rail and Dubai Metro extensions, Egypt’s Cairo Metro Line 4 and Line 5, Brazil’s São Paulo and Rio expansions, and the European Union’s Connecting Europe Facility allocations are creating one of the deepest infrastructure pipelines on record. Rolling stock OEMs and signalling integrators are localizing manufacturing, technology transfer, and consortium delivery to capture the global urban metro rail systems market opportunity, with India’s Make-in-India and Saudi Arabia’s local-content mandates reshaping supplier participation rules.

The signalling and train control segment, spanning Communications-Based Train Control, Automatic Train Operation, train management systems, and operations control center upgrades, is the fastest-growing category within the urban metro rail systems market, supported by sustained demand for capacity densification on existing corridors and Grade-of-Automation 3 and 4 driverless deployments on new lines. Driverless metro operations now span more than 1,100 km of revenue service globally, with major fleets in Paris, Copenhagen, Dubai, Singapore, Sydney, Honolulu, and several Chinese cities. The segment is also recording rapid adoption of platform screen doors, predictive maintenance, regenerative braking with energy recovery, and account-based smart fare collection. Rolling stock is shifting toward lightweight aluminum and stainless-steel car bodies, modular interiors, and onboard condition monitoring that enables availability-linked maintenance contracting with measurable performance penalties.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, supported by sustained urban metro rail systems market investment across India, China, Indonesia, Vietnam, the Philippines, and Bangladesh, each driven by congestion costs, urbanization, and climate-linked modal-shift priorities. China remains the world’s largest absolute revenue market by operating route length, with over 11,300 km of metro and light rail in revenue service and an active pipeline of expansion in second-tier cities. Europe represents the second major regional market, with EU Green Deal mobility funding driving metro upgrades, brownfield re-signalling, and station modernization across France, Germany, Italy, Spain, Poland, and the United Kingdom. Middle East and Africa is the fastest-rising new fleet market, anchored by Saudi Arabia’s Riyadh Metro, the UAE’s Dubai Metro extensions, Egypt’s Cairo lines, and Morocco’s Casablanca tramway, while Latin America, led by Brazil, Mexico, Colombia, and Chile, continues to sanction new corridors and rolling stock orders across the global metro rail landscape.

Key Drivers

Accelerating Urbanization, Congestion Costs, and Modal-Shift Mandates Anchoring Long-Cycle Metro Procurement Pipelines

Rising urban population concentrations, worsening road congestion, and the growing economic cost of vehicular delays are driving sustained metropolitan-authority commitments to mass-transit metro rail networks across emerging and mature economies. Metro corridors deliver measurable congestion relief, lower per-passenger energy intensity, and durable productivity gains, locking in multi-decade procurement pipelines for rolling stock, signalling, and civil EPC across the urban metro rail systems market.

Climate Targets, Transport Decarbonization, and Multilateral Climate-Finance Channels Funding Metro Capital Programs

National net-zero commitments and city-level emissions targets are channeling transport decarbonization budgets and multilateral climate-finance instruments toward electrified urban rail. The World Bank, Asian Development Bank, AIIB, JICA, and European Investment Bank have collectively committed sustained metro-linked lending across India, Indonesia, Vietnam, Egypt, and Latin America, anchoring durable demand within the global urban metro rail systems market and lowering sovereign borrowing costs for metro special-purpose vehicles and concession authorities.

Driverless Operations, CBTC Adoption, and Digital Signalling Modernization Driving Re-investment in Existing Metro Corridors

Capacity densification needs on legacy corridors, combined with operating cost pressure and labor productivity goals, are accelerating adoption of Communications-Based Train Control, Grade-of-Automation 3 and 4 driverless operations, and platform screen doors across mature networks. Brownfield signalling upgrades have emerged as a distinct multi-billion-dollar sub-segment within the urban metro rail systems market, with re-signalling cycles every 20 to 30 years generating reliable replacement demand for incumbents.

Key Challenges

Capital Intensity, Project Financing Delays, and Sovereign Debt Constraints Slowing Sanction-to-Execution Conversion

Metro projects routinely cost USD 80 million to USD 250 million per kilometer for elevated and underground alignments respectively, requiring sovereign or multilateral debt financing that competes with healthcare, education, and other infrastructure priorities. Sanction-to-execution conversion regularly stretches beyond 7 to 10 years, with land acquisition, environmental clearances, and PPP structuring absorbing significant calendar time across the urban metro rail systems market and weighing on supplier order-book conversion.

Tunneling Complexity, Land Acquisition, and Heritage-Zone Permitting Risk in Dense Urban Cores

Metro construction in dense urban cores requires complex tunneling beneath active commercial zones, heritage precincts, and overlapping utility corridors, with TBM advance rates often constrained by mixed-face ground conditions, water ingress, and adjacent-building settlement risk. Land acquisition disputes, court interventions, and heritage-conservation litigation regularly delay sanctioned corridors by years, lifting cost overruns and limiting metro contractor and signalling integrator throughput across the urban metro rail systems market.

Rolling Stock Tendering Complexity, Local-Content Mandates, and Standards Fragmentation Across National Metro Networks

Rolling stock procurement is shaped by elaborate technical tendering, evolving local-content mandates in India, Saudi Arabia, Egypt, and Indonesia, and persistent standards fragmentation across signalling, traction voltage, loading gauge, and platform interface specifications. OEMs face significant non-recurring engineering costs to localize platforms for each market, while operators face long supplier-qualification cycles and limited interoperability across networks within the global urban metro rail systems market.

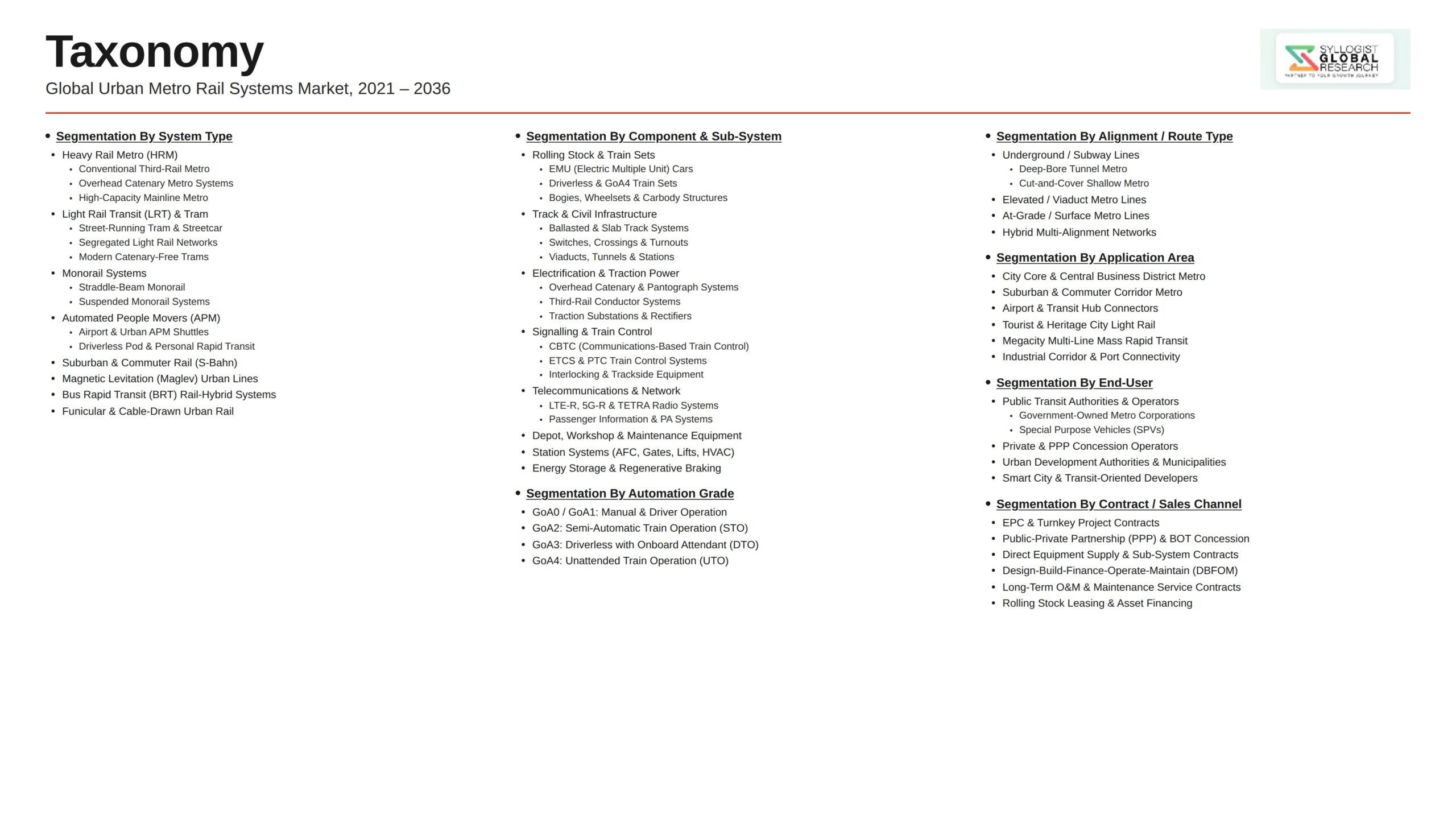

Market Segmentation

- Segmentation By System Type

- Heavy Metro / Conventional Metro

- Light Metro and Light Rail Transit (LRT)

- Monorail Systems

- Driverless Automated Metro

- Rubber-Tired Metro

- Suburban and Regional Rail

- Others

- Segmentation By Rolling Stock

- Electric Multiple Units (EMU)

- Light Metro Vehicles

- Monorail Coaches

- Driverless Automated Trainsets

- Rubber-Tired Metro Coaches

- Others

- Segmentation By Signalling and Train Control

- Communications-Based Train Control (CBTC)

- Automatic Train Operation (ATO)

- Automatic Train Protection (ATP)

- Centralized Traffic Control and OCC

- Train Management Systems

- Others

- Segmentation By Component

- Rolling Stock

- Signalling and Train Control

- Traction Power and Electrification

- Permanent Way and Trackwork

- Tunneling and Civil Works

- Station Systems and Platform Screen Doors

- Automated Fare Collection and Smart Ticketing

- Operations Control Centers

- Depot and Maintenance Facilities

- Others

- Segmentation By Alignment

- Underground Metro

- Elevated Metro

- At-Grade Metro

- Mixed Alignment Networks

- Segmentation By Automation Level (Grade of Automation)

- GoA 1 (Manual Operation)

- GoA 2 (Semi-Automatic with Driver)

- GoA 3 (Driverless with Attendant)

- GoA 4 (Unattended Train Operation)

- Segmentation By Service Type

- New Build and Greenfield Metro Projects

- Brownfield Upgrades and Re-signalling

- Operations and Maintenance Services

- Lifecycle and Modernization Services

- Segmentation By Procurement Model

- Direct Public Procurement

- Public-Private Partnership and Concession Models

- Engineering, Procurement, and Construction (EPC)

- Design-Build-Operate-Maintain (DBOM)

- Others

- Segmentation By End User

- National Rail Ministries and Metro Authorities

- Metropolitan Transport Authorities

- Special-Purpose Vehicles (Metro SPVs)

- PPP Concessionaires and Operating Consortia

- Public-Sector Operators

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global valuation of the urban metro rail systems market in 2025, projected through 2034 and disaggregated by system type, component, and region, enabling rolling stock OEMs, signalling integrators, civil contractors, multilateral lenders, and metropolitan transport authorities to identify the highest-growth segments and most durable revenue opportunities across the global mass-transit landscape?

- How are India, China, Saudi Arabia, the United Arab Emirates, Indonesia, Egypt, and the European Union allocating urban metro rail investment across rolling stock procurement, signalling modernization, civil EPC, and PPP concessions, and which national programs are setting the technical and procurement benchmarks shaping the urban metro rail systems market through 2034?

- What multilateral and sovereign-finance mechanisms, including World Bank, Asian Development Bank, AIIB, JICA, and European Investment Bank metro lending, are shaping project bankability and sanction-to-execution conversion timelines, and how are concession structures, availability-payment frameworks, and value-capture financing reshaping the financing landscape of the urban metro rail systems market?

- Which technology categories, including CBTC, Grade-of-Automation 3 and 4 driverless operations, platform screen doors, predictive maintenance, and regenerative braking with energy recovery, are generating the highest growth rates through 2034, and which suppliers are most critical to capacity densification, energy efficiency, and operational safety across mature and emerging metro networks?

- How is the competitive landscape structured among integrated rolling stock OEMs, signalling specialists, civil contractors, and turnkey consortia pursuing metro rail systems market revenue, and which partnership, technology-transfer, local-content, and acquisition strategies are enabling new entrants to compete against established incumbents across regional markets?

- What are the most material tunneling, land acquisition, heritage-zone permitting, and environmental-clearance risks affecting metro projects in dense urban cores, and how are metro authorities, EPC contractors, and finance providers responding through tunneling innovation, transit-oriented development frameworks, and risk-sharing concession structures?

- Which regional markets, specifically Asia-Pacific, Middle East and Africa, and Latin America, are expected to generate the most substantial incremental urban metro rail revenue through 2034, and what urbanization, climate, governance, and industrial-base factors are driving project priorities and supplier selection decisions in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Project Financing, Public-Private Partnership Bankability & Construction Cost Overrun Risk

- Geotechnical, Tunnelling, Right-of-Way Acquisition & Land Compensation Risk

- Ridership Forecasting, Farebox Revenue & Operating Subsidy Sustainability Risk

- Signalling Cybersecurity, Operational Safety & Driverless System Reliability Risk

- Rolling Stock Supply Chain, Component Sourcing & Long-Term Aftermarket Service Risk

- Regulatory Framework & Standards

- National Urban Transport Policy, Metro Rail Policy & Public Transit Funding Frameworks

- Rolling Stock & Infrastructure Safety Certification Standards (CENELEC EN 50126, EN 50128, EN 50129, IEC 62278, FRA)

- Signalling, CBTC & Automated Train Operation Interoperability Standards (ETCS, IEEE 1474, GoA Classifications)

- Accessibility, Universal Design & Passenger Safety Compliance Standards

- Environmental, Noise, Vibration & Cross-Disciplinary Approval Frameworks for Metro Construction

- Global Urban Metro Rail Systems Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Route Kilometres Operational and Fleet Cars in Service)

- Market Size & Forecast by System Type

- Heavy Metro & Mass Rapid Transit (MRT) Systems

- Light Metro & Light Rail Transit (LRT) Systems

- Monorail Systems

- Automated People Mover (APM) Systems

- Suburban Rail & Regional Metro Systems

- Magnetic Levitation (Maglev) Systems

- Battery-Electric & Hybrid Metro Systems

- Market Size & Forecast by Component

- Rolling Stock (Metro Cars, Coaches, Driver Cabs)

- Civil Infrastructure (Tunnels, Viaducts, Tracks, Stations)

- Signalling & Train Control Systems

- Electrification & Traction Power Systems

- Platform Screen Doors & Station Equipment

- Automatic Fare Collection (AFC) Systems

- Communication & Passenger Information Systems

- SCADA, Depot & Maintenance Equipment

- Market Size & Forecast by Automation Level

- GoA1 – Manual Train Operation with Automatic Train Protection

- GoA2 – Semi-Automated Train Operation (STO)

- GoA3 – Driverless Train Operation (DTO)

- GoA4 – Unattended Train Operation (UTO)

- Market Size & Forecast by Track Configuration

- Underground / Subway Configuration

- Elevated / Viaduct Configuration

- At-Grade / Surface Configuration

- Mixed Track Configuration

- Market Size & Forecast by Power Source

- Overhead Catenary Electrification

- Third Rail Electrification

- Battery-Electric Propulsion

- Hybrid Power Systems

- Market Size & Forecast by Application

- New Greenfield Metro Lines & Network Buildout

- Brownfield Extensions & Network Expansion

- Rolling Stock Procurement & Replacement

- Signalling & Electrification Upgrade Programs

- Station Modernisation & Capacity Enhancement

- Operations, Maintenance & Aftermarket Services

- Market Size & Forecast by End-User

- Government & Municipal Transit Authorities

- State-Owned Metro Corporations

- Private Concessionaires & PPP Operators

- Urban Development Authorities

- Joint Venture Public-Private Operators

- Market Size & Forecast by Sales Channel

- Engineering, Procurement & Construction (EPC) Turnkey Contracts

- Public-Private Partnership (PPP), BOT & Concession Contracts

- Design-Build-Finance-Operate-Maintain (DBFOM) Contracts

- Direct Equipment & Component Supply with System Integration

- Operations & Maintenance (O&M) Service Contracts

- North America Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Urban Metro Rail Systems Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Route Kilometres Operational and Fleet Cars in Service)

- By System Type

- By Component

- By Automation Level

- By Track Configuration

- By Power Source

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analysed in the Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Communications-Based Train Control (CBTC), ETCS & Automated Train Operation Technology Deep-Dive

- Driverless Metro, GoA3 / GoA4 Unattended Train Operation & Fully Automatic Operation Technology

- Battery-Electric Metro Trains, Hybrid Propulsion & Onboard Energy Storage Technology

- Tunnel Boring Machine (TBM), Microtunneling & Underground Civil Construction Technology

- Platform Screen Doors, Smart Station & Passenger Experience Enhancement Technology

- Automatic Fare Collection, Account-Based Ticketing & Mobility-as-a-Service (MaaS) Integration

- Digital Twin, AI-Based Predictive Maintenance & Asset Management Technology

- Patent & IP Landscape in Urban Metro Rail Systems Technologies

- Value Chain & Supply Chain Analysis

- Rolling Stock Manufacturing Supply Chain (Carbodies, Bogies, Traction Equipment, Interiors)

- Civil Construction, Tunnelling & Track Infrastructure Manufacturing Supply Chain

- Signalling System, CBTC & Train Control Equipment Supply Chain

- Electrification, Traction Substation & Overhead Catenary Equipment Supply Chain

- Platform Screen Door, Automatic Fare Collection & Station Equipment Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- Metro Authority, Concessionaire, Operator Channel & Long-Term O&M Service

- Pricing Analysis

- Heavy Metro Rolling Stock & Car Pricing Analysis (per Car & per Train Set)

- Light Rail, Light Metro & Monorail Vehicle Pricing Analysis

- Civil Construction Cost Analysis (Underground, Elevated, At-Grade per Kilometre)

- Signalling, CBTC & Automated Train Control System Pricing Analysis

- Electrification, Traction Power & Substation Equipment Pricing Analysis

- Station Modernisation, Platform Screen Door & Automatic Fare Collection System Pricing Analysis

- Total Metro Project Economics: Capital Cost per Route Kilometre & Operating Cost per Passenger-Kilometre

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Urban Metro Rail Systems vs Private Vehicle, Bus & Alternative Mobility Modes

- Carbon Reduction Contribution: Modal Shift from Private Vehicles, Avoided Emissions & Net Climate Impact

- Urban Air Quality, Congestion Relief & Public Health Co-Benefits of Metro Network Expansion

- Renewable Energy Integration with Metro Traction Power & Net-Zero Operating Pathway

- Regulatory-Driven Sustainability, SDG 11 (Sustainable Cities) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by System Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by System Type, Component & Geography

- Player Classification

- Integrated Rolling Stock Original Equipment Manufacturers (OEMs)

- Specialist Signalling System & CBTC Technology Providers

- Electrification, Traction Power & Substation Equipment Producers

- Tunnel Boring Machine Manufacturers & Civil Construction Specialists

- Platform Screen Door & Station Equipment OEMs

- Automatic Fare Collection & Smart Ticketing System Providers

- EPC Contractors & Project Developers Specialising in Metro Rail

- Digital Twin, Predictive Maintenance & Smart Transit Technology Providers

- Competitive Analysis Frameworks

- Market Share Analysis by System Type, Component & Region

- Company Profile

- Company Overview & Headquarters

- Urban Metro Rail Products & Technology Portfolio

- Key Customer Relationships & Reference Metro Network Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Urban Metro Rail Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By System Type, Component, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)