Market Definition

The Floating LNG (FLNG) market refers to the specialized industrial sector dedicated to the development, deployment, and operation of mobile, offshore vessels designed to process and liquefy natural gas directly at sea. These facilities, typically ship-shaped or barge-like units, integrate the entire liquefied natural gas value chain onto a single floating asset, including gas reception from subsea wells, impurity treatment (pre-treatment), cryogenic liquefaction, storage in the vessel’s hull, and ship-to-ship offloading to LNG carriers. Historically, the market emerged as a strategic solution to monetize stranded or remote offshore gas fields that were previously considered economically unfeasible due to the high cost of laying long-distance subsea pipelines or constructing massive onshore liquefaction terminals.

By 2026, the market has matured significantly, moving beyond massive mega-projects like Shell’s Prelude toward more flexible, modular, and cost-effective mid-to-small-scale designs. The primary drivers of the modern FLNG market are its significantly reduced environmental footprint, eliminating the need for extensive coastal dredging and onshore land use, and its rapid speed-to-market, with conversion-based projects often reaching first production twice as fast as greenfield onshore plants. Furthermore, the market’s plug-and-play nature allows these assets to be redeployed to new fields once a reservoir is exhausted, providing operators with a hedge against geological and geopolitical risks. As global energy dynamics shift, the FLNG market is increasingly seen as a critical component of energy security for regions like Europe and emerging Asian economies, offering a scalable bridge for the transition from coal to cleaner-burning natural gas.

Market Insights

As of early 2026, the global automotive market is undergoing a period of structural realignment driven by shifting trade policies and a recalibration of powertrain strategies. While 2025 saw a pull-forward in demand, 2026 production is expected to edge lower as new tariffs and the rollback of various incentives impact consumer behavior. A notable trend is the hybrid moment, where consumers are increasingly gravitating toward hybrid electric vehicles (HEVs) and range-extended models as a pragmatic bridge between internal combustion engines and fully electric platforms. This shift is prompted by lingering affordability concerns and infrastructure gaps, forcing original equipment manufacturers (OEMs) to optimize their portfolios to balance high-stakes electrification goals with immediate market demand for versatile and cost-effective mobility.

In the energy sector, 2026 stands as a pivotal transition year characterized by an abundance wave of liquefied natural gas (LNG) capacity. Significant supply increases, primarily from North America and Qatar, are beginning to improve market liquidity and interconnectedness, potentially putting downward pressure on spot prices. However, this supply surge coincides with a leapfrog trajectory in emerging economies, where solar and battery storage are increasingly competitive against fossil fuel infrastructure. This dynamic creates a structural surplus risk, where a significant portion of newly committed LNG capital may face stranded asset risks if utilization rates fall below breakeven points. Consequently, strategic emphasis is shifting toward energy security and the flexibility provided by floating LNG (FLNG) solutions, which offer a hedge against geopolitical volatility.

Industrial manufacturing has reached an inflection point in 2026, transitioning from a focus on basic automation to the agentic AI era. Smart factories are no longer defined simply by sensors and connectivity but by intelligent systems capable of real-time, autonomous decision-making. Frontier companies are deploying AI agents that collaborate across design, production, and maintenance modules to optimize inventory dynamically and predict equipment failures with unprecedented precision. This digital thread has evolved from a static archive of data into a living system that powers closed-loop manufacturing, significantly reducing waste and energy consumption. As manufacturers align with global sustainability benchmarks, the integration of AI-driven digital twins and computer vision is becoming a prerequisite for maintaining operational competitiveness and meeting net-zero mandates.

Global supply chains are currently being reshaped by a trend toward radical localization and the emergence of new regional bright spots. Ongoing trade tensions and the implementation of significant tariffs have prompted a massive pivot toward on-shoring and the expansion of domestic production ecosystems, particularly in the Middle East and South Asia. While North America and China face adjustments due to maturing policies and fading incentives, regions like the GCC and South America are experiencing growth fueled by sovereign wealth investments in local manufacturing and supportive industrial policies. These regional hubs are focusing on specialized supply chains, such as extreme-heat optimized EV components or localized chemical processing, to minimize exposure to global logistics shocks and secure a larger share of the evolving high-tech manufacturing landscape.

Key Drivers

Monetization of Stranded and Deepwater Gas Reserves: The primary catalyst for the FLNG market is its unique ability to unlock stranded gas fields, offshore reservoirs that are too small, remote, or deep to justify the massive capital expenditure of subsea pipelines and onshore liquefaction terminals. By integrating the entire treatment and liquefaction process onto a single mobile hull, operators can bypass the logistical and environmental hurdles of land-based infrastructure. As of early 2026, this has proven particularly transformative for emerging producers in Africa and Southeast Asia, where modular FLNG units have significantly lowered the economic threshold for field development, allowing national oil companies to commercialize domestic resources with a much smaller physical and regulatory footprint.

Strategic Mobility and Rapid Energy Security Solutions: The inherent flexibility and speed-to-market of floating assets have become critical drivers in the current global energy landscape. Unlike permanent onshore facilities that require nearly five years to construct, modern FLNG units, especially those utilizing converted Moss-type tankers, can be deployed and operational in under three years. This agility allows energy companies and governments to respond rapidly to geopolitical supply shocks or seasonal demand peaks. Furthermore, the ability to relocate these assets once a reservoir is depleted significantly de-risks the investment, as the vessel remains a versatile capital asset that can be moved to a new site, thereby mitigating the long-term stranded asset risks associated with traditional coastal infrastructure.

Key Challenges

Extreme Capital Intensity and Financing Constraints: Despite advancements in modular design, FLNG projects remain among the most capital-intensive ventures in the energy sector, often requiring multi-billion dollar upfront investments. This high entry barrier largely limits participation to global supermajors and well-capitalized joint ventures, leaving smaller independent operators struggling to secure the necessary project financing. In the current 2026 economic environment of fluctuating natural gas prices and tightening credit markets, investors often demand higher equity cushions or complex political-risk insurance, particularly for projects in emerging markets. This financial sensitivity means that even minor price-cycle volatility can lead to the delay or cancellation of Final Investment Decisions (FIDs) for marginal offshore projects.

Technical Complexity and Harsh Operational Environments: Maintaining a cryogenic liquefaction plant, which requires precise temperature controls and high-pressure processing, on a floating platform in the middle of the ocean presents extraordinary engineering challenges. FLNG vessels must be designed to withstand extreme weather conditions, including typhoons and heavy swells, while maintaining the stability required for ship-to-ship LNG offloading. Technical vulnerabilities, such as heat exchanger reliability and mooring system integrity, remain persistent risks that can lead to costly unscheduled shutdowns or safety incidents. Furthermore, as global methane-slip regulations tighten in 2026, operators face increasing pressure to integrate expensive carbon-capture and emission-control technologies into the cramped footprint of a ship’s deck, further complicating the design and maintenance of these sophisticated offshore assets.

Market Segmentation

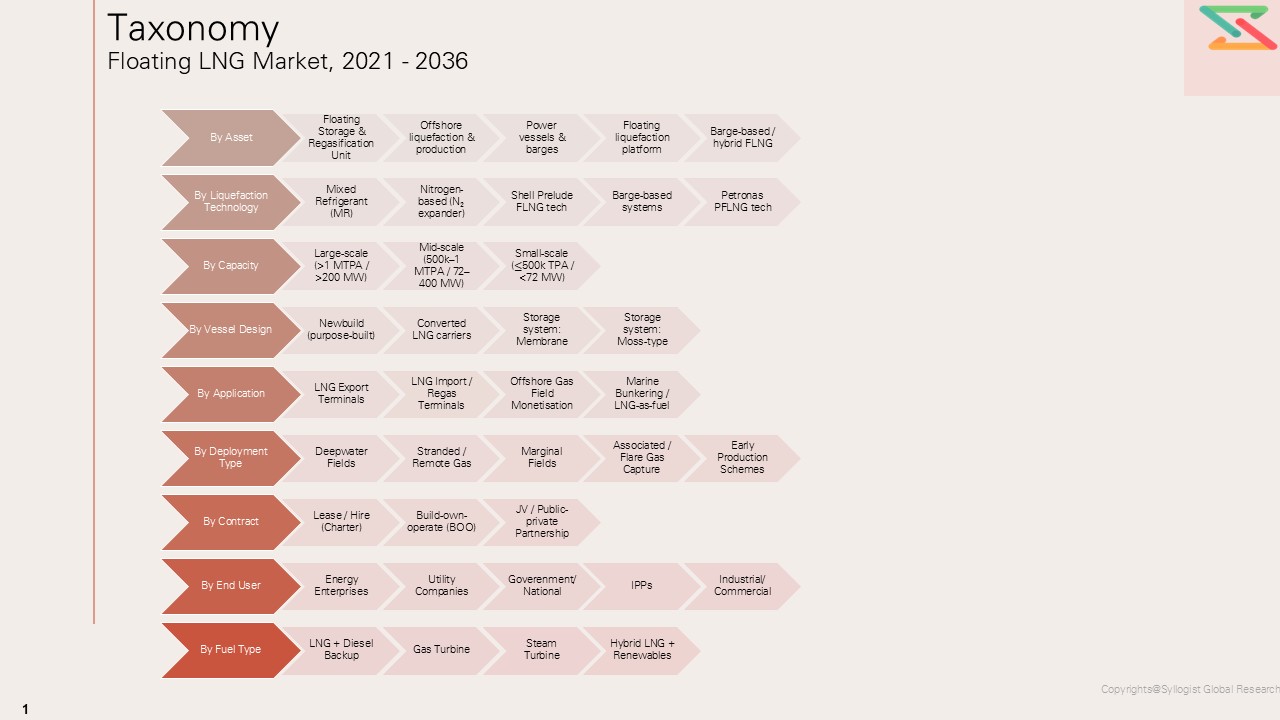

- Segmentation By Asset

- Floating Storage & Regasification Unit

- Offshore Liquefaction & Production

- Power Vessels & Barges

- Floating Liquefaction Platform

- Barge-Based / Hybrid FLNG

- Segmentation By Liquefaction Technology

- Mixed Refrigerant (MR)

- Nitrogen-Based (N₂ Expander)

- Shell Prelude FLNG Tech

- Barge-Based Systems

- Petronas PFLNG Tech

- Segmentation By Capacity

- Small-scale (≤500k TPA / <72 MW)

- Mid-scale (500k–1 MTPA / 72–400 MW)

- Large-Scale (>1 MTPA / >200 MW)

- Segmentation By Vessel Design

- New-Build (Purpose-Built)

- Converted LNG Carriers

- Storage System

- Storage System

- Segmentation By Application

- LNG Export Terminal

- LNG Import / Regas Terminal

- Offshore Gas Field Monetisation

- Marine Bunkering / LNG-As-Fuel

- Segmentation By Deployment Type

- Deep water Fields

- Remote Gas

- Marginal Fields

- Associated / Flare Gas Capture

- Early Production Schemes

- Segmentation By Contract

- Lease / Hire

- Build-Own-Operate (BOO)

- JV / Public-Private Partnership

- Segmentation By End Use Industry

- LNG + Diesel Backup

- Gas Turbine

- Steam Turbine

- Hybrid LNG + Renewables

All market revenues are presented in USD and volume in units

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2036

Key Questions this Study Will Answer

- What are the critical market metrics and forward-looking projections for the Global Floating LNG Market, including revenue size, liquefaction/regasification capacity, unit count, and average pricing by facility type (FLNG, FSRU, FSU), capacity band (Below 1 MTPA, 1–3 MTPA, 3–5 MTPA, Above 5 MTPA), deployment model (Nearshore, Offshore, Onshore-Adjacent), propulsion/mooring configuration (Turret-Moored, Spread-Moored, Ship-Shaped, Barge-Based), application (Liquefaction, Regasification, Storage, Import Terminal, Export Terminal, Peak Shaving), end-use industry (Utilities, Power Generation, Industrial, Marine Bunkering, Fertilizer, Petrochemicals), and contract structure (Owned, Leased, Tolling, Build-Own-Operate, Build-Own-Transfer)?

- How do supply–demand fundamentals vary across key regions and major consuming industries, and what role do natural gas production growth, LNG trade flows, import dependency, gas-to-power expansion, seasonal demand swings, energy security policies, decarbonization targets, and terminal infrastructure gaps play in shaping regional market competitiveness, alongside local capability in shipyard construction, topside liquefaction module fabrication, cryogenic containment system integration, mooring system installation, offshore engineering, and downstream pipeline connectivity, as well as procurement structures across direct asset ownership, long-term charter contracts, EPC consortia, and leasing arrangements?

- In what ways are raw material, equipment, and module price volatility, along with engineering and construction lead-time constraints, covering cryogenic heat exchangers, compressors, gas turbines, storage tanks, loading arms, high-spec steel, nickel alloys, valves, instrumentation, automation systems, subsea infrastructure, and marine systems, influencing project CAPEX, charter rates, developer margins, commissioning timelines, and lifecycle economics, especially for projects requiring complex pretreatment units, carbon reduction features, boil-off gas management systems, and harsh-environment offshore specifications?

- Who are the leading global and regional Floating LNG developers, FSRU/FLNG operators, shipyards, EPC contractors, liquefaction technology licensors, and marine engineering companies, and how do they benchmark across key performance dimensions including nameplate capacity (MTPA / bcm), storage volume, uptime and availability, boil-off gas handling efficiency, send-out/regasification rate, turnaround time, mooring flexibility, relocation capability, safety performance, emissions profile, digital monitoring capability, project execution track record, portfolio breadth across floating gas infrastructure solutions, and value-added offerings such as integrated gas-to-power solutions, modular deployment, and flexible chartering structures?

- What strategic insights emerge from primary discussions with FLNG developers, FSRU operators, LNG buyers, utilities, upstream gas producers, shipyards, EPC contractors, and energy infrastructure investors regarding demand shifts toward flexible and faster-to-deploy LNG infrastructure, specification changes driven by smaller-scale monetization opportunities, gas-to-power demand, stranded gas commercialization, decarbonization expectations, and energy security concerns, as well as regional sourcing strategies for critical cryogenic and offshore components, preferences between owned versus leased floating assets, and key investment and procurement criteria such as project economics, deployment speed, relocation flexibility, storage and send-out capability, reliability, emissions intensity, counterparty strength, and contract duration?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Consumer & Demand Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Geographic & Regional Trends

- Risk Assessment Framework

- Political / Geopolitical Risk

- Fuel & Component Supply Risk

- Environmental and Regulatory Risk

- Financial / Market Risk

- Regulatory Framework & Standards

- Global Floating LNG Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume

- Market Size & Forecast by Asset

- Floating Storage & Regasification Unit

- Offshore Liquefaction & Production

- Power Vessels & Barges

- Floating Liquefaction Platform

- Barge-Based / Hybrid FLNG

- Market Size & Forecast by Liquefaction Technology

- Mixed Refrigerant (MR)

- Nitrogen-Based (N₂ Expander)

- Shell Prelude FLNG Tech

- Barge-Based Systems

- Petronas PFLNG Tech

- Market Size & Forecast by Capacity

- Small-scale (≤500k TPA / <72 MW)

- Mid-scale (500k–1 MTPA / 72–400 MW)

- Large-Scale (>1 MTPA / >200 MW)

- Market Size & Forecast by Vessel Design

- New-Build (Purpose-Built)

- Converted LNG Carriers

- Storage System

- Storage System

- Market Size & Forecast by Application

- LNG Export Terminal

- LNG Import / Regas Terminal

- Offshore Gas Field Monetisation

- Marine Bunkering / LNG-As-Fuel

- Market Size & Forecast by Deployment Type

- Deep water Fields

- Remote Gas

- Marginal Fields

- Associated / Flare Gas Capture

- Early Production Schemes

- Market Size & Forecast by Contract

- Lease / Hire

- Build-Own-Operate (BOO)

- JV / Public-Private Partnership

- Market Size & Forecast by End Use Industry

- LNG + Diesel Backup

- Gas Turbine

- Steam Turbine

- Hybrid LNG + Renewables

- Asia-Pacific Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- Europe Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use Industry

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- North America Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use Industry

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- Latin America Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use Industry

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- Middle East & Africa Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use Industry

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- Country Wise* Genset Market Outlook

- Market Size & Forecast

- By Value

- By Volume / Units

- By Asset

- By Liquefaction Technology

- By Capacity

- By Vessel Design

- By End Use Industry

- By Deployment Type

- By Contract

- By Application

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, China, Germany, India, Japan, United Kingdom, Saudi Arabia, UAE, Australia, South Korea, Canada, Brazil, Nigeria, South Africa, Indonesia, Malaysia, Thailand, France, Italy, Mexico, Turkey, Egypt, Vietnam, Qatar, Kenya, Bangladesh, Philippines, Poland, Netherlands, Singapore

- Technology Landscape & Innovation Analysis

- Technology Overview & Maturity Mapping

- Liquefaction Technology & Process Innovation

- Vessel Design, Hull & Containment Technology

- Mooring, Subsea & Riser Technology

- Power Generation & Propulsion Technology

- Digitalisation, Automation & Smart Operations

- Emerging & Next Generation FLNG Technologies

- Value Chain & Supply Chain Analysis

- End-to-End Value Chain Mapping

- Upstream Supply Analysis-Inputs, Raw Material & Components

- Production, Manufacturing and Operation Landscape

- Distribution Channel, Logistics & Go-to-Market

- Downstream Demand & End-User Analysis

- Cost Structure & Margin Distribution Across the Value Chain

- Supply Chain Risk Assessment

- Supply Chain Trend & Strategic Implications

- Pricing Analysis

- LNG Price Formation & Benchmarks

- FLNG & FSRU Asset Pricing: Charter Rates & Day Rates

- Capital & Operating Cost Analysis

- Pricing Dynamics & Market Influences

- Price Forecast & Scenario Analysis

- Pricing Strategy & Commercial Structuring

- Sustainability & Energy Efficiency

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented Vs Consolidated)

- Top 5 Players Market Share

- HHI (Herfindahl–Hirschman Index) Concentration Analysis

- Competitive Intensity Map

- Player Classification

- Market Leaders

- Strong Challengers

- Specialist / Niche Players

- Emerging Players

- Regional Players

- Competitive Analysis Frameworks

- Market Share Analysis

- Company Profile

- Company Overview & HQ

- Products & Solutions Portfolio

- Overall Revenue & Segmental Revenue

- Geographic Presence

- Recent Developments (M&A, Launches, Partnerships)

- SWOT Analysis

- Strategic Focus Areas

- Competitive Positioning Map

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix

- White Space Opportunity Analysis

- Strategic Recommendations

- For Operators & Developers

- For Investors, Government & Shipbuilders

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2036)