Global Oil Storage Tanks Market By Tank Type, By Material, By Capacity, By Roof Type, By Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Oil Storage Tanks Market encompasses the engineering, fabrication, installation, and maintenance of above-ground and underground atmospheric and pressurized storage vessels designed to receive, hold, and dispatch crude oil, refined petroleum products, petrochemicals, and liquid hydrocarbons across upstream production facilities, midstream terminals, refineries, fuel depots, pipeline breakout stations, and strategic petroleum reserves, including fixed-roof, floating-roof, and dome-roof tank designs fabricated from carbon steel, stainless steel, and fiberglass materials, procured by oil and gas operators, refining companies, terminal operators, and government strategic reserve agencies globally.

Market Insights

The global oil storage tanks market is navigating a dynamic investment environment shaped by the simultaneous forces of sustained hydrocarbon production growth in major oil-exporting regions, the strategic buildup of national petroleum reserves by energy-importing governments seeking supply security buffers against geopolitical disruption, the rapid expansion of refined product distribution infrastructure in developing economies, and the growing requirement to upgrade and rehabilitate aging tank farms in mature refining and terminal infrastructure markets where structural integrity compliance programs are generating non-discretionary capital expenditure obligations. The market was valued at approximately USD 6.9 billion in 2025 and is projected to grow at a compound annual growth rate of 4.6% through 2034, as crude oil and refined product storage capacity investment continues across upstream, midstream, and downstream segments of the global oil supply chain despite the long-term uncertainty introduced by energy transition policy and alternative fuel development programs.

Floating roof tank designs represent the largest procurement segment within the global oil storage tanks market, reflecting their mandatory adoption for storing volatile hydrocarbons including crude oil, gasoline, naphtha, and light distillate products where vapor emission control regulations require the floating roof mechanism to maintain continuous contact with the stored liquid surface and minimize hydrocarbon evaporative losses to atmosphere. External floating roof tanks constructed from carbon steel are the dominant configuration for large-volume crude oil and refined product terminal storage, with tank diameters reaching one hundred meters and individual capacities exceeding one million barrels at major crude oil export terminal and strategic reserve facilities where storage economy of scale is a critical infrastructure design parameter. The strategic petroleum reserve segment is generating elevated new tank construction activity in several Asian economies including China, India, South Korea, and Japan, where governments are significantly expanding national emergency oil reserve storage capacity in response to energy security policy reassessments following supply chain vulnerability exposure during recent geopolitical disruption events.

The refinery and petrochemical sector represents a large and structurally stable demand source for oil storage tanks, as new refinery capacity additions in the Middle East, Asia, and Africa require extensive product storage tank farms accommodating crude oil feed, intermediate process streams, and finished product segregation requirements across complex multi-product refining configurations. Refinery tank farm expansion and rehabilitation is simultaneously generating maintenance and upgrade investment in existing tank infrastructure, as regulatory inspection programs identify corrosion, floor plate degradation, and structural settlement conditions in aging tank floors and shells that require repair or full tank replacement to maintain fitness for service certification. The expansion of petroleum product import terminal infrastructure in coastal markets across West Africa, South and Southeast Asia, and Latin America is driving new tank construction procurement as independent terminal operators and national oil companies invest in import storage capacity enabling bulk vessel receipt, product blending, and downstream distribution supply security for rapidly growing domestic fuel consumption markets.

The Middle East dominates global oil storage tank construction by new capacity volume, anchored by the massive crude oil export terminal infrastructure of Saudi Arabia, the United Arab Emirates, Iraq, Kuwait, and Qatar, where national oil companies are investing in tank farm expansion programs supporting growing production capacity and export volume objectives. Asia-Pacific represents the largest regional market by procurement value, driven by China’s strategic reserve expansion program, India’s hydrocarbon storage infrastructure development under national energy security policies, and the rapid growth of petroleum product import and distribution terminal infrastructure across Southeast Asian markets. North America maintains a substantial oil storage tank maintenance, inspection, and rehabilitation market driven by the large installed base of aging aboveground storage tanks subject to API 653 inspection requirements and environmental leak detection compliance programs enforced by federal and state regulatory agencies.

Key Drivers

Strategic Petroleum Reserve Expansion Programs and National Energy Security Policies Driving Large-Scale Oil Storage Tank Construction Investment Across Asian and Emerging Economy Governments

Energy security policy reassessments prompted by supply disruption vulnerability exposure are compelling oil-importing governments across Asia, including China, India, South Korea, Japan, Indonesia, and Vietnam, to materially expand national strategic petroleum reserve storage capacities through new tank farm construction programs at designated strategic reserve sites, underground cavern storage development, and commercial storage leasing arrangements that collectively represent substantial procurement demand for large-diameter floating roof tanks, underground storage cavern lining systems, and associated receipt and dispatch pipeline infrastructure. The International Energy Agency oil stockholding obligation framework, which requires member nation compliance with minimum ninety-day net import coverage in strategic reserves, similarly motivates member nation governments to maintain and expand above-ground tank storage capacity within national reserve programs as populations and petroleum consumption continue growing.

New Refinery and Petrochemical Complex Capacity Additions in the Middle East, Asia, and Africa Generating Large-Scale Tank Farm Construction Requirements Across Integrated Downstream Facilities

The construction of large integrated refinery and petrochemical complexes across Saudi Arabia, the United Arab Emirates, Kuwait, India, China, Nigeria, and Tanzania is generating substantial tank farm construction procurement as each new refinery requires extensive storage infrastructure encompassing crude oil receiving tanks, intermediate process storage, product segregation tankage, and blend component storage totaling millions of barrels of combined capacity per facility. New refinery projects configured as export-oriented facilities serving regional petroleum product import markets require product storage capacities substantially exceeding domestic consumption refineries due to the vessel loading and sailing schedule management requirements that determine optimal minimum product inventory levels for consistent export program execution, further amplifying per-refinery tank farm investment requirements relative to domestic market supply facilities.

Petroleum Product Import Terminal Infrastructure Expansion in Coastal Developing Markets Driving Independent Terminal Operator and National Oil Company Tank Construction Investment

The rapid growth of petroleum product consumption in coastal developing markets across West Africa, East Africa, South Asia, and Southeast Asia is driving investment in petroleum product import terminal infrastructure enabling bulk cargo receipt from large product tankers, product quality management through blending and additive injection, and downstream distribution supply chain management through connected transport and distribution networks. Independent terminal operators and national oil companies in these markets are constructing multi-product tank farms capable of storing gasoline, diesel, jet fuel, kerosene, and fuel oil in segregated tanks meeting international product quality and contamination prevention standards, with individual terminal capacities ranging from fifty thousand to several hundred thousand cubic meters depending on the market consumption scale and competitive positioning strategy of the terminal developer.

Key Challenges

Stringent Environmental Regulations Governing Hydrocarbon Vapor Emissions, Soil Contamination Prevention, and Tank Farm Secondary Containment Requirements Elevating Construction and Compliance Costs

Oil storage tank facilities are subject to comprehensive environmental regulatory requirements governing hydrocarbon vapor emission control from tank roofs and seals, secondary containment bund construction for spill containment, groundwater and soil contamination prevention through impermeable floor liner systems and leak detection infrastructure, and stormwater management from contaminated bund areas, collectively adding substantial engineering and construction cost to new tank farm development programs and imposing ongoing operational compliance expenditure on tank operators managing existing facilities under environmental permit conditions. The tightening of vapor emission standards in developed markets and the progressive adoption of stricter environmental permitting requirements in previously lightly regulated developing country markets are progressively elevating the minimum technical specification and construction cost of compliant oil storage tank installations globally.

Aboveground Storage Tank Structural Integrity Inspection Obligations and API 653 Compliance Costs Creating Substantial Maintenance Expenditure Burdens for Operators of Large Aging Tank Farm Inventories

The large inventory of aboveground oil storage tanks constructed during the mid-to-late twentieth century petroleum infrastructure expansion period in North America, Europe, and the Middle East is subject to periodic out-of-service inspection under API 653 and equivalent national standards that require tank floor sampling and ultrasonic thickness measurement, shell corrosion assessment, roof structural inspection, and fitness-for-service evaluation at intervals determined by corrosion rate calculations and risk-based inspection programs. The discovery of floor plate corrosion, shell deformation, foundation settlement, or structural deficiency during scheduled inspections frequently requires repair or partial reconstruction work that is difficult to budget in advance, creating unplanned capital expenditure obligations that coincide with extended tank out-of-service periods reducing terminal throughput capacity and potentially disrupting supply chain commitments to downstream customers.

Long-Term Oil Demand Uncertainty Under Energy Transition Scenarios Creating Investment Horizon Risk for New Tank Farm Capital Programs With Multi-Decade Asset Life Expectations

Oil storage tank construction projects require capital investment amortized over operational asset lives of twenty-five to forty years, and the uncertainty surrounding the trajectory of global oil demand under accelerating energy transition scenarios where electric vehicle adoption, renewable energy penetration, and energy efficiency improvement could reduce petroleum product consumption materially within the anticipated asset life of new tank investments is introducing investment horizon risk that creates hesitation among independent terminal operators and financial investors evaluating the long-term revenue and asset value assumptions embedded in new large-scale tank farm development business cases. This risk calculus is particularly acute for petroleum product storage infrastructure in European markets where policy-driven fuel demand decline scenarios are more proximate and aggressive than in developing economy markets where petroleum consumption growth trajectories remain positive across virtually all credible energy transition scenarios.

Market Segmentation

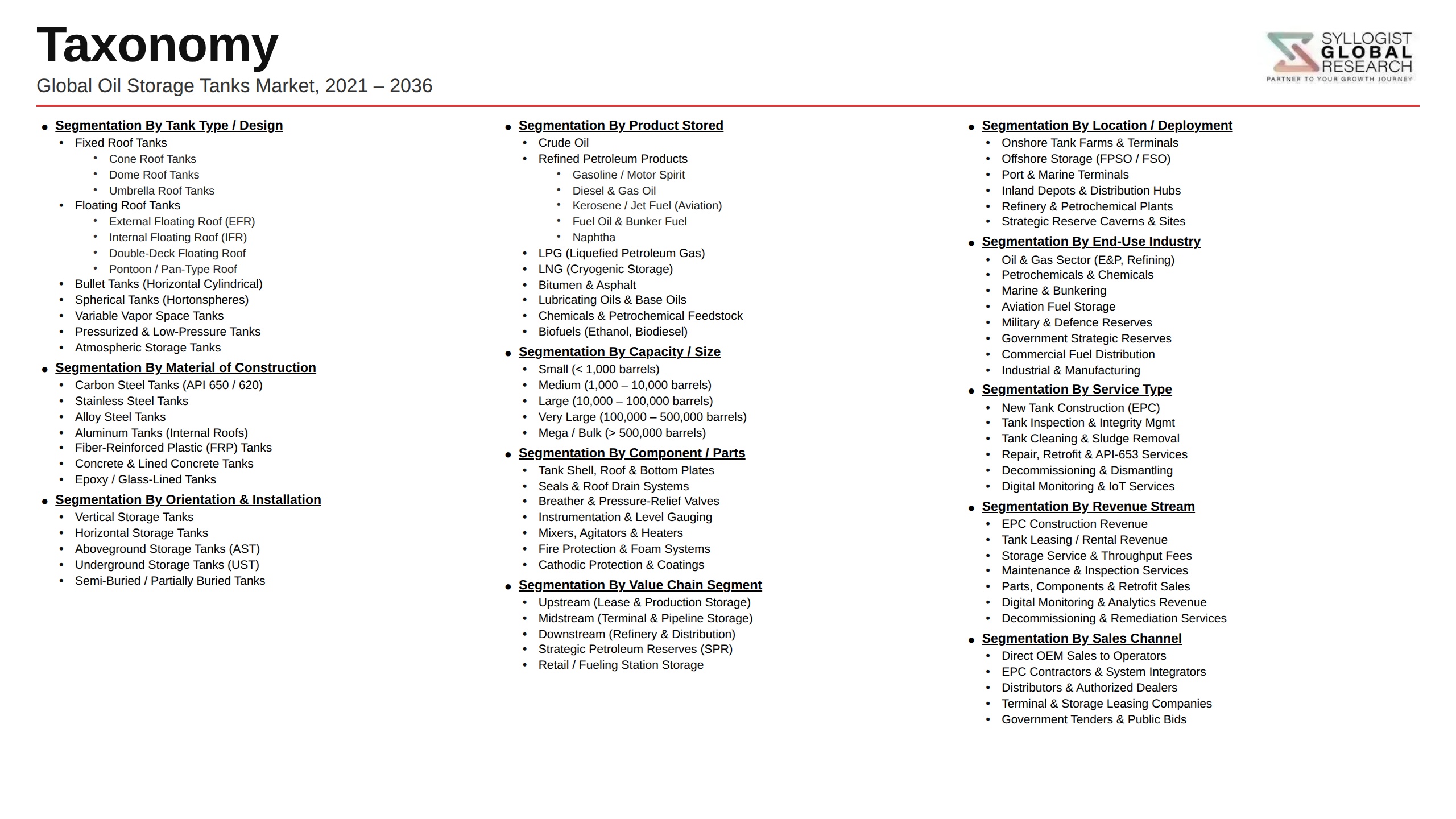

- Segmentation By Tank Type

- Aboveground Storage Tanks

- Underground Storage Tanks

- Floating Roof Tanks (External and Internal)

- Fixed Roof Tanks

- Pressurized and Spherical Storage Vessels

- Cryogenic Storage Tanks

- Others

- Segmentation By Material

- Carbon Steel Tanks

- Stainless Steel Tanks

- Fiberglass Reinforced Plastic Tanks

- Coated and Lined Carbon Steel Tanks

- Aluminum Tanks

- Others

- Segmentation By Capacity

- Small Capacity (Below 1,000 Cubic Meters)

- Medium Capacity (1,000 to 10,000 Cubic Meters)

- Large Capacity (10,000 to 100,000 Cubic Meters)

- Very Large Capacity (Above 100,000 Cubic Meters)

- Segmentation By Roof Type

- External Floating Roof

- Internal Floating Roof

- Fixed Cone Roof

- Fixed Dome Roof

- Open-Top Tanks

- Others

- Segmentation By Application

- Crude Oil Storage and Export Terminal Operations

- Refined Petroleum Product Storage

- Strategic Petroleum Reserve Storage

- Petrochemical Feedstock and Intermediate Storage

- Aviation Fuel and Marine Bunker Storage

- Lubricants and Specialty Petroleum Products

- Others

- Segmentation By End User

- National and International Oil Companies

- Independent Petroleum Product Terminal Operators

- Refinery and Petrochemical Complex Operators

- Government Strategic Reserve Agencies

- Pipeline and Midstream Infrastructure Operators

- Aviation and Marine Fuel Suppliers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global oil storage tanks market valuation in 2025, projected through 2034, segmented by tank type, capacity, and end user, enabling tank fabricators, terminal operators, refining companies, and infrastructure investors to identify the highest-growth procurement segments and most strategically significant construction and maintenance investment opportunities across the global oil storage landscape?

- How are national strategic petroleum reserve expansion programs in China, India, South Korea, Japan, and Southeast Asian economies reshaping large-capacity floating roof tank construction procurement volumes, preferred tank farm site configurations, and construction contracting models, and what aggregate new storage capacity investment is projected across government-backed strategic reserve programs through 2034?

- Which new refinery and petrochemical complex construction programs in the Middle East, Africa, and Asia are generating the largest associated tank farm construction requirements, and how are integrated refinery product slate complexity, export orientation, and proximity to marine terminals influencing tank farm capacity design, product segregation requirements, and blending infrastructure specifications for new facility developments?

- How is the competitive landscape structured among global tank fabrication and construction contractors, regional steel storage tank manufacturers, and specialist tank lining and coating service providers, and what engineering design capability, fabrication capacity, international project execution experience, and environmental compliance technology differentiation are enabling leading contractors to win large tank farm construction and rehabilitation contracts?

- What API 653 inspection compliance requirements, tank floor corrosion remediation obligations, secondary containment upgrade mandates, and vapor emission control regulation tightening are driving the most significant maintenance and rehabilitation capital expenditure programs among operators of large aging aboveground storage tank inventories in North America, Europe, and the Middle East through 2034?

- How are long-term oil demand uncertainty under energy transition scenarios, declining refining capacity investment in European markets, and growing investor sensitivity to hydrocarbon infrastructure stranded asset risk influencing capital allocation decisions, asset life extension strategies, and new tank construction investment appraisal assumptions among independent terminal operators and integrated oil companies with large tank farm infrastructure portfolios?

- Which regional oil storage tank markets, specifically the Middle East, Asia-Pacific, and West and East Africa, are expected to generate the highest incremental new construction procurement through 2034, and what combinations of crude oil export capacity expansion, strategic reserve policy investment, refinery capacity addition, and petroleum product import terminal development are driving tank farm construction activity in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Tank Corrosion, Structural Failure, Leak & Spill Liability Risk

- Oil Price Volatility, Refinery Utilisation Fluctuation & Storage Demand Cycle Risk

- Environmental Contamination, Soil & Groundwater Pollution & Clean-Up Liability Risk

- Regulatory Tightening, EPA SPCC, API 650 Compliance & Inspection Mandate Risk

- Energy Transition, Long-Term Petroleum Product Demand Decline & Stranded Asset Risk

- Steel Price Volatility, Fabrication Labour Shortage & Construction Cost Overrun Risk

- Regulatory Framework & Standards

- API 650, API 620 & API 653 Welded Tank Design, Construction & Inspection Standards

- EPA Spill Prevention, Control & Countermeasure (SPCC) Rule & Aboveground Storage Tank (AST) Regulatory Frameworks

- NFPA 30, EN 14015 & National Fire Safety Standards for Flammable Liquid Storage Tanks

- API 2000, API 2350 Overfill Protection & Venting Standards for Petroleum Storage Tanks

- VOC Emission Control, Vapour Recovery Unit (VRU) Standards & Clean Air Act Compliance for Oil Storage

- Cathodic Protection, Lining Inspection & Integrity Management Standards: API 651, API 652 & STI SP001

- Global Oil Storage Tanks Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units & Total Storage Capacity, Million Barrels)

- Market Size & Forecast by Tank Type

- Aboveground Storage Tanks (ASTs)

- Underground Storage Tanks (USTs)

- Floating Roof Tanks (External & Internal Floating Roof)

- Fixed Roof Tanks (Cone Roof & Dome Roof)

- Horizontal & Bullet Tanks (Cylindrical & Pressure Vessels)

- Spherical & Spheroid Tanks for LPG & High-Vapour-Pressure Products

- Floating Storage Units (FSUs) & Offshore Floating Storage

- Cryogenic & Low-Temperature Storage Tanks

- Market Size & Forecast by Material

- Carbon Steel & Structural Steel Tanks

- Stainless Steel & Duplex Stainless Steel Tanks

- Aluminium Tanks

- Glass-Reinforced Plastic (GRP) & FRP Tanks

- Coated & Internally Lined Steel Tanks

- Concrete & Reinforced Concrete Tanks

- Market Size & Forecast by Capacity

- Small-Capacity Tanks (Below 1,000 Barrels)

- Medium-Capacity Tanks (1,000 to 100,000 Barrels)

- Large-Capacity Tanks (100,000 to 500,000 Barrels)

- Very Large Capacity Tanks (Above 500,000 Barrels)

- Market Size & Forecast by Product Stored

- Crude Oil Storage Tanks

- Gasoline & Motor Spirit Storage Tanks

- Diesel & Gasoil Storage Tanks

- Aviation Fuel (Jet A-1 & Avgas) Storage Tanks

- Fuel Oil & Residual Oil Storage Tanks

- LPG & NGL Storage Tanks

- Petrochemical & Chemical Feedstock Storage Tanks

- Biofuel, Renewable Diesel & SAF Storage Tanks

- Market Size & Forecast by Activity Type

- New Tank Construction & Greenfield Terminal Projects

- Tank Inspection, Repair & Maintenance Services

- Tank Rehabilitation, Relining & Life Extension

- Tank Decommissioning & Removal Services

- Market Size & Forecast by Application

- Upstream Crude Oil Field Storage & Gathering Terminals

- Midstream Pipeline & Marine Terminal Storage

- Refinery & Petrochemical Plant On-Site Storage

- Strategic Petroleum Reserve (SPR) & National Buffer Stock Storage

- Retail Fuel Distribution Terminal & Depot Storage

- Aviation Fuel Depot & Airport Hydrant Storage

- Marine Bunkering & Port Terminal Storage

- Market Size & Forecast by End-User

- International Oil Companies (IOCs) & National Oil Companies (NOCs)

- Refinery & Petrochemical Plant Operators

- Independent Tank Terminal Operators & Storage Companies

- Government Strategic Reserve Agencies

- Fuel Retail & Distribution Companies

- Port Authorities & Marine Terminal Operators

- Mining & Industrial Companies

- Market Size & Forecast by Sales Channel

- EPC Contractor & Turnkey Tank Farm Construction Channel

- Direct Tank Fabricator & Manufacturer Sales Channel

- Inspection, Maintenance & Integrity Service Contract Channel

- Government Tender & National Infrastructure Procurement Channel

- North America Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Oil Storage Tanks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units & Total Storage Capacity, Million Barrels)

- By Tank Type

- By Material

- By Capacity

- By Product Stored

- By Activity Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Italy, Spain, China, Japan, India, South Korea, Singapore, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Iraq, Kuwait, Russia, Nigeria, South Africa, Egypt

- Technology Landscape & Innovation Analysis

- Floating Roof Tank Technology Deep-Dive: Pontoon, Double-Deck & Internal Floating Roof Design, Seal Systems & Emission Reduction Performance

- Tank Inspection Technology: Ultrasonic Floor Scanning, MFL, AE Testing, Robotic Crawlers & Drone-Based Tank Inspection Systems

- Tank Coating & Lining Technology: High-Performance Epoxy, Glass Flake, Novolac & Thermoplastic Lining Systems for Corrosion Protection

- Vapour Recovery Unit (VRU) & VOC Emission Control Technology for Floating & Fixed Roof Tanks

- Smart Tank Monitoring: IoT Level Gauging, Temperature Sensing, Leak Detection & Tank Farm Automation Systems

- Advanced Tank Farm SCADA, Inventory Management & Terminal Automation Platform Technology

- Modular & Bolt-Assembled Tank Technology for Rapid Deployment & Remote Location Installation

- Patent & IP Landscape in Oil Storage Tank Technologies

- Value Chain & Supply Chain Analysis

- Steel Plate, Coil, Structural Steel & Speciality Alloy Supply Chain for Tank Fabrication

- Tank Coating, Lining Material, Cathodic Protection & Corrosion Prevention Supply Chain

- Tank Accessories: Valves, Nozzles, Vents, Gauges, Mixers & Floating Roof Components Supply Chain

- Tank Fabrication, Shop Welding, Site Erection & Quality Inspection Supply Chain

- Civil & Foundation Works, Bund Construction & Site Preparation Supply Chain

- EPC Contractor, Tank Farm Designer & Systems Integration Channel

- Aftermarket Inspection, Repair, Lining Renewal & Maintenance Service Channel

- Pricing Analysis

- Oil Storage Tank Capital Cost Analysis by Tank Type, Capacity & Material

- Tank Construction Cost per Barrel of Storage Capacity Analysis

- Tank Inspection, Maintenance & Repair Cost Structure Analysis

- Tank Rehabilitation & Relining Cost vs. New-Build Cost Comparison Analysis

- Independent Tank Terminal Storage Lease Rate & Tariff Structure Analysis

- Impact of Steel Plate Prices & Labour Costs on Tank Fabrication & Construction Pricing

- Sustainability & Environmental Analysis

- VOC Emissions & Hydrocarbon Vapour Loss from Oil Storage Tanks: Quantification, Regulation & Abatement Technology

- Tank Leak & Spill Environmental Impact: Soil Contamination, Groundwater Pollution & Remediation Cost Analysis

- Lifecycle Assessment (LCA) of Oil Storage Tanks: Embodied Carbon, Operational Emissions & End-of-Life Recycling

- Tank Farm Adaptation for Biofuels, Renewable Diesel, SAF & Low-Carbon Liquid Fuel Storage

- ESG Disclosure, Responsible Asset Management & Green Finance Standards for Oil Storage Infrastructure

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Tank Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Tank Type, Application & Geography

- Player Classification

- Global Integrated EPC Contractors & Tank Farm Construction Companies

- Specialist Aboveground Storage Tank (AST) Fabricators & Erectors

- Specialist Pressure Vessel, Sphere & Bullet Tank Manufacturers

- Tank Inspection, Integrity Management & Rehabilitation Service Providers

- Tank Coating, Lining & Corrosion Protection Specialists

- Smart Tank Monitoring, SCADA & Terminal Automation Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Tank Type, Activity Type & Region

- Company Profile

- Company Overview & Headquarters

- Oil Storage Tank Products, Services & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Fabrication Capacity

- Revenue (Oil Storage Tank Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technical Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Tank Type, Material, Product Stored, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Compliance & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output