Global Pipeline Infrastructure Market By Pipeline Type, By Material, By Diameter, By Application, By Service Type, By End Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Pipeline Infrastructure Market encompasses the engineering, procurement, construction, operation, maintenance, and rehabilitation of onshore and offshore pipeline systems designed to transport crude oil, refined petroleum products, natural gas, liquefied natural gas, hydrogen, carbon dioxide, water, and industrial process fluids across production fields, processing facilities, storage terminals, and end use distribution networks, including associated compression and pumping stations, metering systems, cathodic protection infrastructure, leak detection systems, and integrity management programs procured by energy companies, utilities, and industrial operators globally.

Market Insights

The global pipeline infrastructure market is undergoing a structural transition of exceptional complexity, simultaneously managing the sustained operational and capital investment requirements of the world’s vast existing hydrocarbon pipeline network, navigating the regulatory and reputational pressures associated with pipeline safety and environmental integrity in an era of heightened public and institutional scrutiny, and confronting the long-term strategic question of how pipeline infrastructure assets can be repurposed, extended, or replaced to serve the energy carriers of decarbonizing economies including hydrogen, carbon dioxide for geological storage, and green ammonia. The market was valued at approximately USD 19.6 billion in 2025 and is projected to grow at a compound annual growth rate of 4.8% through 2034, as the combination of new pipeline capacity requirements in developing economy energy infrastructure expansion programs, the multi-decade maintenance and integrity management obligation of the global installed pipeline base, and the emerging hydrogen and carbon capture transport pipeline investment cycle collectively sustain pipeline infrastructure procurement across a broadening range of fluid types and operating environments.

Natural gas transmission and distribution pipelines represent the largest single segment within the global pipeline infrastructure market, reflecting the foundational role of gas pipeline networks in energy supply security across every major economy and the growing investment in gas pipeline capacity expansion in Asia, the Middle East, and Africa driven by natural gas demand growth, LNG regasification terminal connection requirements, and industrial and power sector gas consumption expansion. The acceleration of United States LNG export capacity has generated particularly significant midstream pipeline infrastructure investment demand, as new liquefaction train capacity on the Gulf Coast requires connecting pipeline infrastructure from domestic production basins, expanded compression capacity to maintain throughput economics, and storage and processing infrastructure upgrades that collectively represent multi-year capital programs for pipeline infrastructure contractors and equipment suppliers operating in the North American midstream sector.

Hydrogen pipeline infrastructure is emerging as the most strategically significant long-term growth segment within the global pipeline market, as the scaling of green and low-carbon hydrogen production across Europe, Australia, the Middle East, and the United States creates demand for dedicated hydrogen transport infrastructure connecting production sites to industrial consumers, hydrogen blending injection points in existing natural gas networks, and port facilities serving hydrogen export through ammonia and liquid organic hydrogen carrier shipping. The European Hydrogen Backbone initiative, which envisions a pan-European dedicated hydrogen transmission network exceeding forty thousand kilometers in length developed primarily through repurposing of existing natural gas pipelines complemented by new-build hydrogen pipe capacity, represents the most advanced programmatic framework for large-scale hydrogen pipeline infrastructure development and is establishing the technical standards, regulatory frameworks, and business models that hydrogen pipeline programs in other regions will reference. Carbon dioxide pipeline infrastructure for carbon capture and storage transport is similarly attracting growing investment attention as carbon capture programs scale from pilot demonstrations toward industrial decarbonization projects requiring dedicated pipeline networks to transport captured carbon from emission sources to geological storage sites at the volumes required for commercially meaningful carbon abatement contribution.

North America dominates the global pipeline infrastructure market by installed network length and annual capital expenditure, anchored by the world’s most extensive natural gas and liquids pipeline network, an active midstream capital investment cycle supporting growing LNG export infrastructure, and a large pipeline integrity management and replacement expenditure base driven by ageing infrastructure compliance programs and federal pipeline safety regulations. The Middle East and Asia-Pacific represent the second and third largest regional markets, driven respectively by hydrocarbons export pipeline infrastructure expansion connecting producing fields to export terminals and the large natural gas transmission and distribution network buildout programs under execution across China, India, Southeast Asia, and Pakistan to support gas demand growth and clean cooking fuel access expansion. Europe’s pipeline market is characterized by the complex task of managing the strategic transition of existing natural gas infrastructure toward hydrogen and carbon dioxide transport readiness while maintaining gas transmission security for the remaining period of gas system operation.

Key Drivers

Natural Gas Infrastructure Expansion in Developing Economies and LNG Export Capacity Growth Sustaining Large-Scale Gas Pipeline Construction and Midstream Investment Programs

The buildout of natural gas transmission and distribution networks across South and Southeast Asia, the Middle East, and Africa is generating sustained pipeline construction demand as governments and utilities invest in gas infrastructure that expands clean cooking fuel access, connects industrial zones to pipeline gas supply, integrates LNG regasification terminal output into national grid systems, and develops cross-border gas trade links supporting regional energy security objectives. Simultaneously, the expansion of LNG export liquefaction capacity in the United States, Qatar, Mozambique, and Canada is driving midstream pipeline infrastructure investment in upstream gathering and transportation systems, high-pressure long-distance transmission corridors, and marine terminal approach pipelines that collectively represent large capital programs for pipeline engineering, procurement, and construction contractors across multiple concurrent project locations.

Hydrogen Transport Pipeline Infrastructure Development and Natural Gas Pipeline Repurposing for Energy Transition Creating a Structurally New Long-Term Investment Cycle for Pipeline Asset Owners and Contractors

The scaling of green hydrogen production across Europe, Australia, the Middle East, and North America is creating demand for dedicated hydrogen transmission pipeline infrastructure connecting electrolysis production sites to industrial consumers, hydrogen blending networks, and export terminals, with the European Hydrogen Backbone initiative representing the most programmatically advanced framework for developing a continental hydrogen transport network through a combination of repurposed natural gas pipelines and new-build hydrogen pipe capacity. Carbon dioxide transport pipeline infrastructure for carbon capture and storage projects is simultaneously emerging as a growing investment category, as industrial decarbonization programs requiring geological carbon storage scale from feasibility study toward construction, creating dedicated pipeline requirements connecting industrial emission sources across steel, cement, chemical, and power generation facilities to offshore or onshore geological storage reservoirs.

Ageing Pipeline Infrastructure Replacement Obligations and Pipeline Integrity Management Regulation Tightening Generating Non-Discretionary Rehabilitation and Upgrade Investment Across Mature Network Markets

The global installed pipeline base includes substantial inventories of pipelines installed during the mid-to-late twentieth century energy infrastructure expansion period whose age, material condition, coating degradation, and metallurgical characteristics create elevated failure risk profiles that pipeline integrity regulations in North America, Europe, and Australia mandate be managed through systematic inspection, condition assessment, and where necessary pipe segment replacement programs generating significant and recurring capital expenditure obligations for pipeline operators. Regulatory tightening of pipeline safety standards, increased inspection frequency requirements, and the imposition of consequence-based assessment frameworks that require proactive repair of anomalies detected by inline inspection tools before regulatory thresholds are breached are collectively expanding the non-discretionary pipeline integrity management expenditure base across the global midstream industry, providing a durable foundation of maintenance and rehabilitation procurement demand that is independent of new pipeline capacity investment cycles.

Key Challenges

Pipeline Permitting, Right-of-Way Acquisition, and Community Opposition Creating Severe Project Development Timeline Extensions and Cost Escalation Risks for New Pipeline Construction Programs

New pipeline projects in North America, Europe, and Australia face increasingly contentious and protracted permitting processes driven by environmental impact assessment requirements, Indigenous and local community consultation obligations, judicial challenges from environmental advocacy organizations, and in some cases fundamental disagreements over whether new fossil fuel pipeline capacity is consistent with national climate commitments, collectively creating project development timelines that can extend from initial permitting application to construction commencement by five to ten years or more for major interstate or cross-border pipelines and introducing investment uncertainty that raises financing costs and in some cases results in project abandonment after years of development expenditure. The expansion of environmental and social governance risk assessment frameworks applied by infrastructure lenders and institutional investors to pipeline project financing is further tightening the conditions under which new pipeline construction projects can secure the bank lending and capital market financing required for construction.

Long-Term Hydrocarbon Pipeline Asset Stranding Risk Under Accelerating Energy Transition Scenarios Creating Capital Allocation Uncertainty and Investor Appetite Constraints for New Long-Life Pipeline Infrastructure

Pipeline infrastructure assets are characterized by operational design lives of forty to sixty years and require throughput volume assumptions extending across multi-decade periods to justify the capital investment required for construction and financing, creating a fundamental tension between the long asset life required for project economics and the uncertain trajectory of hydrocarbon demand under accelerating energy transition scenarios where natural gas and oil consumption may peak and decline within the economic life of pipeline assets currently seeking investment. Infrastructure lenders, pension funds, and institutional investors with fiduciary obligations to manage portfolio climate transition risk are applying heightened scrutiny to the long-term revenue and throughput assumptions embedded in new hydrocarbon pipeline project financial models, raising the cost of capital and in some markets effectively limiting the availability of long-term project finance for new pipeline construction on commercial terms that meet project developer return requirements.

Hydrogen Embrittlement, Material Compatibility, and Technical Standards Uncertainty for Hydrogen Pipeline Infrastructure Creating Engineering and Certification Complexity for Repurposed Gas Network Assets

The repurposing of existing natural gas pipelines for hydrogen service introduces material compatibility challenges including hydrogen embrittlement of high-strength steels used in transmission pipelines, seal and gasket material compatibility with hydrogen at elevated pressures, compressor adaptation requirements for hydrogen gas properties that differ significantly from natural gas, and the potential for hydrogen permeation through pipe wall materials and coatings not designed for hydrogen service, requiring comprehensive pipeline condition assessment, material qualification testing, and potentially selective segment replacement before repurposed pipelines can be certified for hydrogen operation at the pressures required for commercially viable hydrogen transport. The incomplete state of international technical standards for hydrogen pipeline design, material qualification, operating pressure limits, and leak detection system performance at hydrogen service conditions creates certification uncertainty that complicates regulatory approval processes and equipment procurement decisions for hydrogen pipeline developers.

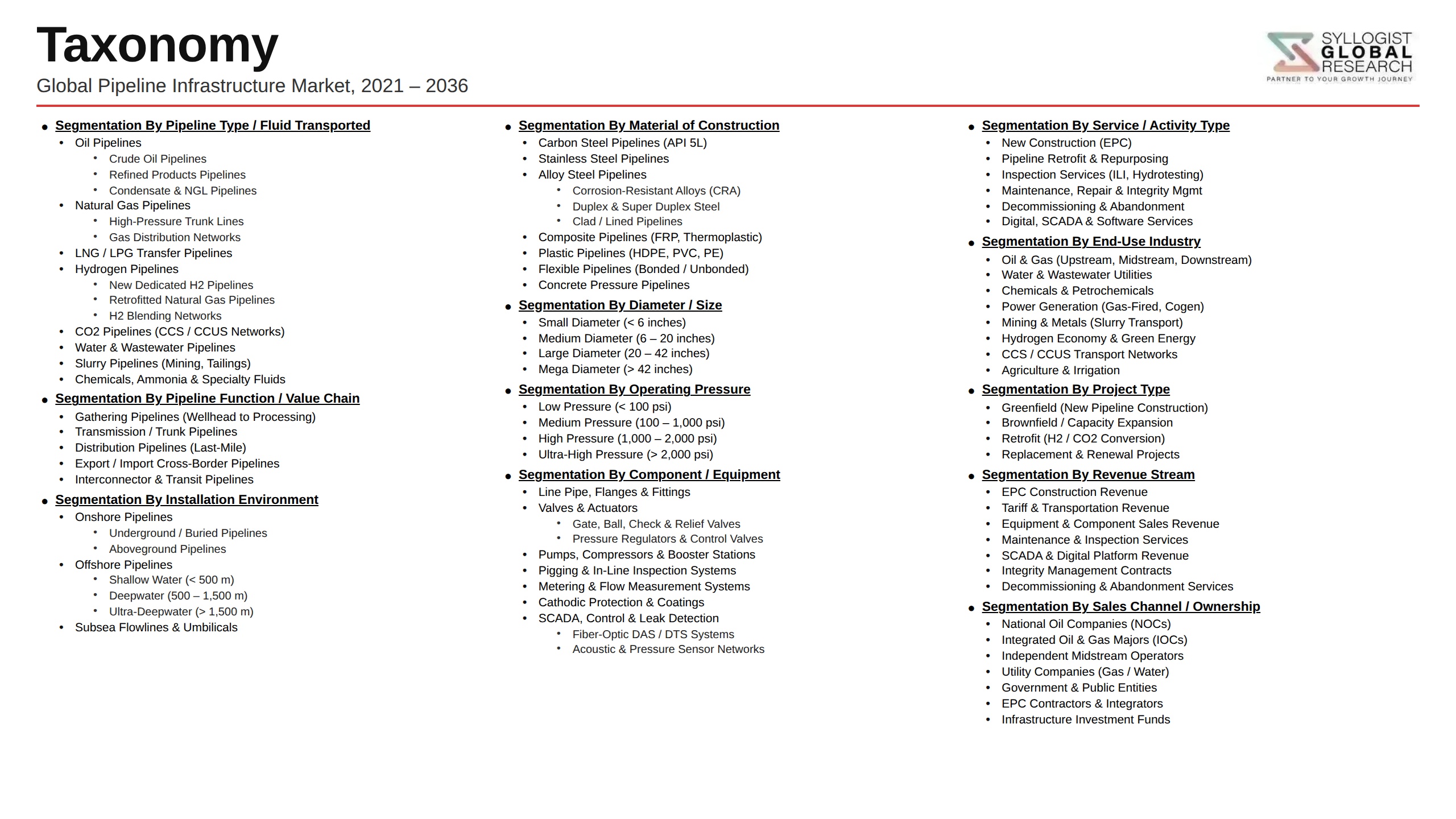

Market Segmentation

- Segmentation By Pipeline Type

- Natural Gas Transmission Pipelines

- Natural Gas Distribution Pipelines

- Crude Oil and Liquids Transmission Pipelines

- Refined Petroleum Product Pipelines

- Hydrogen Transmission and Distribution Pipelines

- Carbon Dioxide Transport Pipelines

- Water and Industrial Process Fluid Pipelines

- Others

- Segmentation By Material

- Carbon Steel and High-Strength Low-Alloy Steel

- Stainless Steel and Corrosion-Resistant Alloys

- High-Density Polyethylene and Thermoplastic Pipes

- Composite and Fiber-Reinforced Polymer Pipes

- Ductile Iron and Cast Iron Pipes

- Others

- Segmentation By Diameter

- Small Diameter Pipelines (Below 12 Inches)

- Medium Diameter Pipelines (12 to 24 Inches)

- Large Diameter Pipelines (24 to 48 Inches)

- Very Large Diameter Pipelines (Above 48 Inches)

- Segmentation By Application

- Onshore Transmission and Long-Distance Transport

- Offshore Subsea Pipeline Systems

- Urban Gas Distribution Networks

- Industrial Plant and Facility Piping

- Cross-Border and Export Pipeline Infrastructure

- Pipeline Integrity Management and Rehabilitation

- Others

- Segmentation By Service Type

- New Pipeline Construction

- Pipeline Maintenance and Inspection Services

- Pipeline Rehabilitation and Replacement

- Pipeline Repurposing and Conversion

- Integrity Management and Monitoring Systems

- Others

- Segmentation By End Use Industry

- Oil and Gas Upstream and Midstream

- Natural Gas Utilities and Distribution Companies

- Petrochemical and Refining Industry

- Hydrogen Production and Energy Transition

- Carbon Capture and Storage Programs

- Water and Sanitation Utilities

- Industrial and Mining Operations

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global pipeline infrastructure market valuation in 2025, projected through 2034, segmented by pipeline type, application, and end use industry, enabling pipeline operators, engineering contractors, equipment suppliers, and infrastructure investors to identify the highest-growth segments and most durable capital expenditure opportunities across the global pipeline construction, maintenance, and energy transition conversion landscape?

- How are natural gas infrastructure expansion programs in South and Southeast Asia, the Middle East, and Africa, combined with LNG export midstream investment in the United States, Qatar, and Mozambique, shaping pipeline construction volume, diameter and material specification requirements, and engineering procurement and construction contractor workload distribution across regional and international pipeline project development programs through 2034?

- What technical standards gaps, material qualification requirements, hydrogen embrittlement assessment methodologies, and regulatory certification frameworks are most critically constraining the pace of natural gas pipeline repurposing for hydrogen service, and what pipeline condition assessment programs, material testing protocols, and certification pathways are operators and regulators developing to advance hydrogen pipeline readiness across major European and North American network portfolios?

- How is the competitive landscape structured among global pipeline engineering procurement and construction contractors, regional pipeline construction specialists, and pipeline integrity management service providers, and what technology capability development, geographic market expansion, energy transition service portfolio extension, and strategic acquisition strategies are enabling leading competitors to maintain market share across both conventional hydrocarbon and emerging hydrogen and carbon dioxide pipeline segments?

- What pipeline permitting reform initiatives, environmental impact assessment streamlining programs, Indigenous and community consultation framework improvements, and judicial review process modifications are governments and regulatory agencies implementing to reduce the project development timeline and approval risk exposure that currently constrains new pipeline construction investment in North America, Europe, and Australia?

- How are long-term hydrocarbon demand uncertainty, energy transition scenario range, and climate policy trajectory influencing pipeline infrastructure asset valuation, project financing availability, institutional investor appetite for new pipeline construction commitments, and the strategic decisions of oil and gas companies regarding long-life pipeline capacity investment versus shorter-life or repurposable infrastructure alternatives through 2034?

- Which regional pipeline infrastructure markets, specifically the Middle East, Asia-Pacific, and North America, are expected to generate the most significant incremental construction and maintenance investment through 2034, and what combinations of hydrocarbon production growth, natural gas demand expansion, hydrogen infrastructure development programs, and aging network replacement obligations are defining the capital expenditure trajectory and technology procurement priorities in each regional market?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Pipeline Corrosion, Integrity Failure, Leak & Rupture Risk

- Geopolitical Instability, Cross-Border Route Disruption & Sanctions Risk

- Regulatory Permitting Delay, Environmental Opposition & Right-of-Way Acquisition Risk

- Energy Transition, Stranded Asset & Long-Term Hydrocarbon Demand Decline Risk

- Cybersecurity, SCADA Attack & Critical Infrastructure Vulnerability Risk

- Steel & Material Cost Volatility, Construction Labour Shortage & Project Cost Overrun Risk

- Regulatory Framework & Standards

- Pipeline Safety Standards: ASME B31.8, B31.4, DOT 49 CFR & National Pipeline Safety Regulatory Frameworks

- Pipeline Integrity Management, In-Line Inspection (ILI) & PHMSA/API 1160 Corrosion Management Standards

- Environmental Impact Assessment, Spill Prevention, SPCC & Pipeline Routing Regulatory Frameworks

- Hydrogen Pipeline Embrittlement, Material Compatibility & H2-Ready Pipeline Standards

- CO2 Pipeline Standards for CCS & CCUS Transport: ISO 27913, DNV-RP-F104 & EU CCS Directive

- Methane Emission Monitoring, Leak Detection & Repair (LDAR) Regulatory Requirements for Pipeline Operations

- Global Pipeline Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (km of Pipeline & Diameter-Inches)

- Market Size & Forecast by Pipeline Type

- Natural Gas Transmission & High-Pressure Gas Pipelines

- Natural Gas Distribution & City Gas Network Pipelines

- Crude Oil Transmission & Gathering Pipelines

- Refined Petroleum Product Pipelines (Diesel, Gasoline, Jet Fuel & LPG)

- Water & Wastewater Transmission & Distribution Pipelines

- Hydrogen Pipeline Infrastructure (New-Build & Repurposed Gas Pipelines)

- CO2 Pipeline Infrastructure for CCS & CCUS Transport

- Slurry, Mining & Industrial Process Fluid Pipelines

- District Heating & Cooling Pipeline Networks

- Market Size & Forecast by Material

- Carbon Steel & Line Pipe (API 5L Grade B, X42 to X80 & X100)

- Stainless Steel & Duplex Stainless Steel Pipelines

- High-Density Polyethylene (HDPE) & Polyethylene (PE) Pipelines

- Glass-Reinforced Plastic (GRP) & Fibre-Reinforced Polymer (FRP) Pipelines

- Ductile Iron & Cast Iron Pipelines

- Concrete & Reinforced Concrete Pipelines

- Composite & Flexible Pipe Systems

- Market Size & Forecast by Diameter

- Small-Diameter Pipelines (Below 6 inches)

- Medium-Diameter Pipelines (6 inches to 16 inches)

- Large-Diameter Pipelines (16 inches to 36 inches)

- Very Large-Diameter Pipelines (Above 36 inches)

- Market Size & Forecast by Activity Type

- New Pipeline Construction & Greenfield Projects

- Pipeline Replacement, Rehabilitation & Renewal Projects

- Pipeline Integrity Management, Inspection & Maintenance Services

- Pipeline Repurposing & Conversion (Gas-to-Hydrogen & Gas-to-CO2)

- Pipeline Decommissioning & Abandonment Services

- Market Size & Forecast by Installation Method

- Open Cut & Trench Excavation Pipeline Installation

- Horizontal Directional Drilling (HDD) & Trenchless Technology

- Pipe Jacking, Microtunnelling & Auger Boring Installation

- Offshore & Subsea Pipeline Lay (S-Lay, J-Lay & Reel Lay)

- Market Size & Forecast by Application

- Oil & Gas Upstream Gathering & Trunk Line Systems

- Midstream Gas Transmission & Cross-Country Pipeline Systems

- Downstream Petroleum Product & Terminal Distribution Systems

- Municipal Water Supply, Drinking Water & Wastewater Networks

- Industrial Process, Chemical Plant & Refinery Piping Systems

- Hydrogen Transportation & Green Hydrogen Backbone Networks

- CO2 Capture, Transportation & Storage (CCS) Pipeline Networks

- Market Size & Forecast by End-User

- National Oil Companies (NOCs) & International Oil Companies (IOCs)

- Midstream Pipeline Operators & Gas Transmission System Operators (TSOs)

- City Gas Distribution (CGD) Companies & Local Distribution Companies (LDCs)

- Municipal Water Utilities & Wastewater Authorities

- Industrial & Chemical Process Facility Operators

- Government & National Infrastructure Authorities

- Market Size & Forecast by Sales Channel

- EPC Contractor & Turnkey Project Delivery Channel

- Direct Pipe Manufacturer & Material Supply Channel

- Integrity Management, Inspection & Service Contract Channel

- Government Tender & Public Infrastructure Procurement Channel

- North America Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Pipeline Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (km of Pipeline & Diameter-Inches)

- By Pipeline Type

- By Material

- By Diameter

- By Activity Type

- By Installation Method

- By Application

- By End-User

- By Country

- By Sales Channel

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Italy, Norway, Russia, China, Japan, India, Australia, South Korea, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, Iraq, Qatar, Nigeria, South Africa, Egypt, Kazakhstan

- Market Size & Forecast

- Technology Landscape & Innovation Analysis

- In-Line Inspection (ILI) Technology Deep-Dive: Magnetic Flux Leakage (MFL), Ultrasonic Testing (UT), Geometry & Multi-Channel ILI Tools

- Hydrogen Pipeline Technology: Material Compatibility, Embrittlement Testing, Repurposing Assessment & Dedicated H2 Pipeline Design

- CO2 Pipeline Technology: Dense Phase CO2 Transport, Material Selection, Fracture Control & CCS Backbone Design

- Trenchless Installation Technology: HDD Advances, Pipe Bursting, Cured-In-Place Lining (CIPP) & Microtunnelling Innovations

- Digital Pipeline Technology: Digital Twin, AI-Powered Leak Detection, SCADA Analytics & Integrity Management Platforms

- Composite, Flexible Pipe & Thermoplastic Composite Pipe (TCP) Technology for Offshore & Corrosive Fluid Applications

- Advanced Corrosion Protection: FBE Coating, 3-Layer PE/PP Coating, Cathodic Protection & Internal Lining Technology

- Patent & IP Landscape in Pipeline Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Steel Plate, Coil, Seamless Tube & Line Pipe Manufacturing Supply Chain

- Pipe Coating, FBE, 3-Layer PE/PP & Internal Lining Application Supply Chain

- Pipe Fittings, Flanges, Valves, Actuators & Pipeline Accessory Supply Chain

- Compressor Station, Pump Station, Metering & Pressure Regulation Equipment Supply Chain

- Construction Equipment, Trenching, HDD Rig & Welding Equipment Supply Chain

- EPC Contractor, Civil & Mechanical Engineering & Pipeline Construction Channel

- Integrity Management, ILI Vendor, Inspection & Testing Service Channel

- Pipeline Operator, TSO, Utility & End-User Procurement Channel

- Pricing Analysis

- Pipeline Construction Cost Analysis by Diameter, Material & Installation Method (USD per km)

- Onshore vs. Offshore Pipeline Capital Cost & Unit Rate Comparison

- Pipeline Integrity Management & ILI Service Cost Analysis by Technology & Diameter

- Hydrogen vs. Natural Gas Pipeline Capex Comparison: New-Build vs. Repurposing Cost Analysis

- Pipeline Transportation Tariff, Regulated Access & Third-Party Access (TPA) Pricing Structure Analysis

- Impact of Steel Price, Labour Cost & Right-of-Way Acquisition on Pipeline Project Economics

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Pipeline Infrastructure: Carbon Footprint of Steel Production, Construction & Operations

- Methane Emission Quantification, LDAR Programme Effectiveness & Fugitive Emission Reduction from Gas Pipeline Networks

- Pipeline Right-of-Way Ecology, Land Restoration, Soil & Groundwater Protection Standards

- Role of Pipeline Infrastructure in Enabling Hydrogen Economy, CCS Networks & Energy Transition

- ESG Disclosure, Responsible Pipeline Operations & Green Finance Eligibility for Pipeline Infrastructure

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Pipeline Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Pipeline Type, Activity Type & Geography

- Player Classification

- Global Integrated Pipeline EPC Contractors & Engineering Companies

- Line Pipe, Steel Pipe & Tube Manufacturers

- Pipeline Integrity Management, ILI & Inspection Service Providers

- Trenchless Technology & Specialist Installation Contractors

- Pipeline Valves, Fittings, Compressor & Pump Equipment Manufacturers

- Digital Pipeline, SCADA & Integrity Management Platform Providers

- Competitive Analysis Frameworks

- Market Share Analysis by Pipeline Type, Activity Type & Region

- Company Profile

- Company Overview & Headquarters

- Pipeline Products, Services & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Pipeline Infrastructure Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technical Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Pipeline Type, Material, Activity Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Integrity & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output