Global Petrochemical Conventional Feedstocks Market By Feedstock Type, By Sourcing Route, By Cracker Technology, By Derivative Output, By End Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Petrochemical Conventional Feedstocks Market encompasses the extraction, processing, trading, and supply of petroleum-derived and natural gas-derived hydrocarbon feedstocks including naphtha, ethane, propane, butane, liquefied petroleum gas, gas oil, and condensate, utilized as primary raw materials in steam crackers, catalytic reformers, fluid catalytic cracking units, and dehydrogenation plants to produce olefins, aromatics, and other petrochemical building blocks for plastics, synthetic fibers, rubber, resins, solvents, and specialty chemical manufacturing across integrated and standalone petrochemical complexes globally.

Market Insights

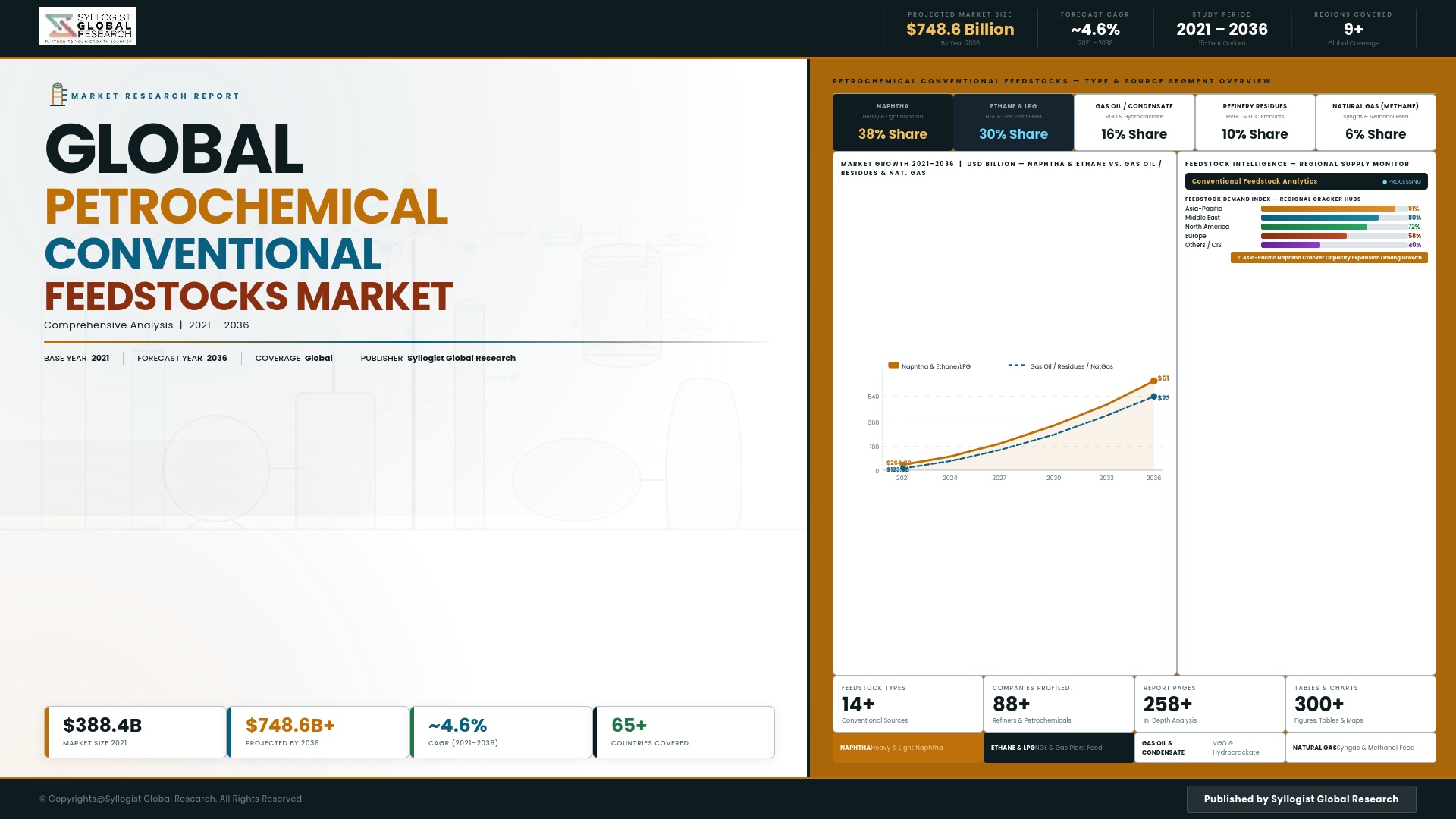

The global petrochemical conventional feedstocks market is experiencing a structural realignment of exceptional strategic significance, as the convergence of shale gas-driven ethane abundance in North America, the accelerating development of integrated crude-to-chemicals complexes in the Middle East and Asia, and the long-term strategic pressure of energy transition policy on naphtha availability from conventional petroleum refinery operations collectively reshape the feedstock cost competitiveness map, production location economics, and capital allocation priorities of the global petrochemical industry. The market was valued at approximately USD 342.6 billion in 2025 and is projected to expand at a compound annual growth rate of 3.8% through 2034, supported by continued growth in developing economy polymer and chemical demand that sustains feedstock volume requirements despite the long-term uncertainty introduced by bio-based and recycled feedstock development programs and the potential moderation of virgin petrochemical demand growth in regulated plastic markets.

Naphtha retains its position as the world’s largest-volume petrochemical feedstock by market value, serving as the primary cracker input for ethylene and propylene production across European, Asian, and established petrochemical complexes where natural gas liquid infrastructure is limited and crude oil refinery integration provides the primary naphtha supply mechanism. However, naphtha’s competitive position is under sustained pressure from the advantaged economics of ethane cracking in North America, where the shale gas revolution has established ethane as a structurally cheap and abundantly available feedstock delivering ethylene production costs substantially below those achievable with naphtha-based European and Asian crackers, creating a persistent competitive advantage for North American ethylene producers that has driven multi-cycle waves of ethane cracker investment on the United States Gulf Coast. The integration of naphtha cracking with high-value aromatics extraction from pyrolysis gasoline co-product streams partially offsets the naphtha ethylene production cost disadvantage relative to ethane, as the aromatics and propylene co-products generated by naphtha cracking represent significant additional revenue streams that pure ethane crackers cannot access, maintaining naphtha cracking commercial viability for producers with integrated aromatics extraction capability serving regional propylene and aromatic derivative demand.

The Middle East maintains its position as the global leader in advantaged petrochemical feedstock economics, with Saudi Arabia, Iran, Qatar, the United Arab Emirates, and Kuwait accessing low-cost ethane and natural gas liquids from associated and non-associated gas production that enables ethylene production at cost positions representing a substantial discount to naphtha-based competitors in Asia and Europe. The progressive shift of Middle Eastern petrochemical strategy from pure commodity ethylene and polyethylene production toward integrated crude-to-chemicals complexes that maximize chemical yield from crude oil processing, reduce refinery fuel oil production, and access higher-value specialty chemical and engineering polymer markets is generating substantial investment in mixed feedstock crackers and integrated refinery petrochemical configurations. China’s large-scale coal-to-olefins and coal-to-methanol production capacity represents a structurally distinct petrochemical feedstock route whose economics are governed by domestic coal pricing rather than crude oil and natural gas markets, providing Chinese chemical producers with feedstock cost insulation from international oil and gas price cycles at the cost of substantially higher carbon dioxide emission intensity per unit of chemical product compared to petroleum and natural gas-derived alternatives.

Asia-Pacific dominates the global petrochemical conventional feedstocks market by consumption volume, reflecting the massive scale of naphtha cracker capacity in China, South Korea, Japan, Taiwan, and Southeast Asia that collectively process the largest share of globally traded naphtha for ethylene, propylene, and aromatics production. The Middle East represents the second most significant regional feedstock market by value, characterized by low-cost gas-based feedstock advantage and growing integrated complex development. North America is the most dynamic regional market for ethane feedstock economics, with the sustained productivity of Permian Basin, Marcellus, and Appalachian shale plays maintaining high ethane availability and low gas processing liquid prices that continue supporting new ethane cracker investment at advantaged economics relative to global alternatives.

Key Drivers

Developing Economy Polymer and Chemical Demand Growth Sustaining Long-Term Conventional Feedstock Volume Requirements Despite Emerging Sustainability and Bio-Based Substitution Pressures

Rising per capita income and expanding manufacturing activity across South and Southeast Asia, Africa, the Middle East, and Latin America are driving sustained growth in polyethylene, polypropylene, PVC, and specialty chemical consumption for packaging, construction, agriculture, automotive, and consumer goods applications that collectively sustain conventional petrochemical feedstock demand growth at rates substantially exceeding the demand contraction visible in regulated European and North American markets where plastic substitution and circular economy policies are progressively moderating virgin polymer consumption. The structural gap between per capita plastics consumption in developing economies and the levels achieved in established industrial markets implies multi-decade volume growth runway for conventional petrochemical feedstock demand in these regions that no currently available bio-based or recycled alternative supply can address at the required scale, cost, and technical performance level.

North American Shale Gas Ethane Abundance and Integrated Crude-to-Chemicals Complex Development Driving Advantaged Feedstock Investment Cycles That Reshape Global Production Cost Competitiveness

The persistent structural abundance of ethane recovered from Permian Basin, Marcellus, and Utica shale gas processing operations is sustaining the cost-competitive economics of United States Gulf Coast ethane cracker operations at levels that continue attracting new steam cracker investment, expanding ethylene export capacity, and maintaining American ethylene and polyethylene production cost advantages relative to naphtha-based competitors in Asia and Europe. Simultaneously, the strategic development of fully integrated crude-to-chemicals complexes in Saudi Arabia, the United Arab Emirates, and China is creating new categories of feedstock cost efficiency by maximizing chemical yield from crude oil processing while minimizing lower-value refined product output, progressively shifting the optimal feedstock strategy for major petrochemical producers toward deep integration of refinery and chemical operations rather than standalone cracker configurations.

Rising Chemical Complexity Requirements in Automotive, Electronics, and Medical Applications Sustaining Premium Feedstock Demand for Specialty Olefin and Aromatic Derivative Production

The increasing complexity and performance requirements of polymers and specialty chemicals used in electric vehicle battery components, lightweight automotive composites, advanced electronics packaging, medical device materials, and high-performance coatings are sustaining demand for petrochemical building blocks derived from conventional feedstock processing that bio-based and recycled alternative supply chains cannot currently provide at the required purity, consistency, and performance specification levels. High-value specialty olefins including butadiene, isobutylene, and higher alpha-olefins, and aromatic derivatives including aniline, caprolactam, and specialty epoxy resins, command significant market premiums over commodity polyethylene and polypropylene that support the economics of mixed feedstock cracker configurations optimized for co-product value capture alongside base ethylene and propylene production.

Key Challenges

Crude Oil and Natural Gas Price Volatility and Feedstock Cost Transmission Creating Margin Compression Cycles That Periodically Undermine Petrochemical Complex Operating Economics

Petrochemical producers utilizing naphtha, gas oil, and condensate feedstocks sourced from crude oil refinery operations face feedstock cost structures that are directly exposed to crude oil price volatility, with naphtha prices tracking crude oil market movements closely while downstream polymer and chemical product prices adjust more slowly and incompletely to feedstock cost increases, creating margin compression periods during crude oil price spikes that reduce petrochemical complex profitability and in extreme cases generate negative variable cost margins that motivate cracker rate reduction or shutdown. The difficulty of fully passing through feedstock cost increases to polymer and chemical buyers operating in competitive markets with alternative supply options or demand elasticity limits the ability of conventional feedstock-dependent petrochemical producers to maintain stable margins across the full range of crude oil price scenarios.

Long-Term Demand Displacement Risk from Bio-Based Feedstocks, Chemical Recycling, and Circular Economy Policy Creating Strategic Investment Uncertainty for Conventional Feedstock-Dependent Petrochemical Assets

The scaling of bio-based ethylene from bioethanol dehydration, bio-based propylene from biomass conversion, and chemically recycled olefins and aromatics from plastic waste pyrolysis and gasification is progressively introducing alternative supply streams into petrochemical feedstock markets that compete directly with conventional petroleum-derived feedstocks for derivative production capacity, creating long-term strategic uncertainty about the proportion of current virgin petrochemical feedstock demand that will be displaced by alternative sources within the thirty-to-forty-year operational lifespan of petrochemical asset investments being made today. Regulatory mandates for minimum recycled content in plastic products and packaging in the European Union and progressively other jurisdictions are accelerating the demand pull for chemically recycled feedstocks that will structurally reduce virgin feedstock consumption requirements in affected product markets regardless of conventional feedstock price competitiveness.

Carbon Pricing, Scope 1 and 2 Emission Reduction Obligations, and Steam Cracker Decarbonization Investment Requirements Elevating Operating Costs and Capital Expenditure Burdens for Conventional Feedstock Processors

Steam cracking is one of the most energy-intensive and carbon-emitting industrial processes in the chemical industry, generating substantial carbon dioxide from combustion of the fuels required to achieve the high-temperature endothermic cracking reactions that convert naphtha, ethane, and other feedstocks into olefins and aromatics, and the progressive tightening of carbon pricing under European Union Emissions Trading System benchmarks and emerging carbon border adjustment mechanisms is escalating the carbon compliance cost burden on conventional steam cracker operations at rates that materially affect the comparative economics of European naphtha crackers relative to non-carbon-priced competitors in Asia, the Middle East, and North America. Decarbonizing steam crackers through electrification, hydrogen firing, or carbon capture and storage requires capital investment at a scale that imposes substantial additional cost burden on existing cracker infrastructure whose profitability at current polymer market margins may be insufficient to support both operating cost competitiveness and decarbonization investment simultaneously.

Market Segmentation

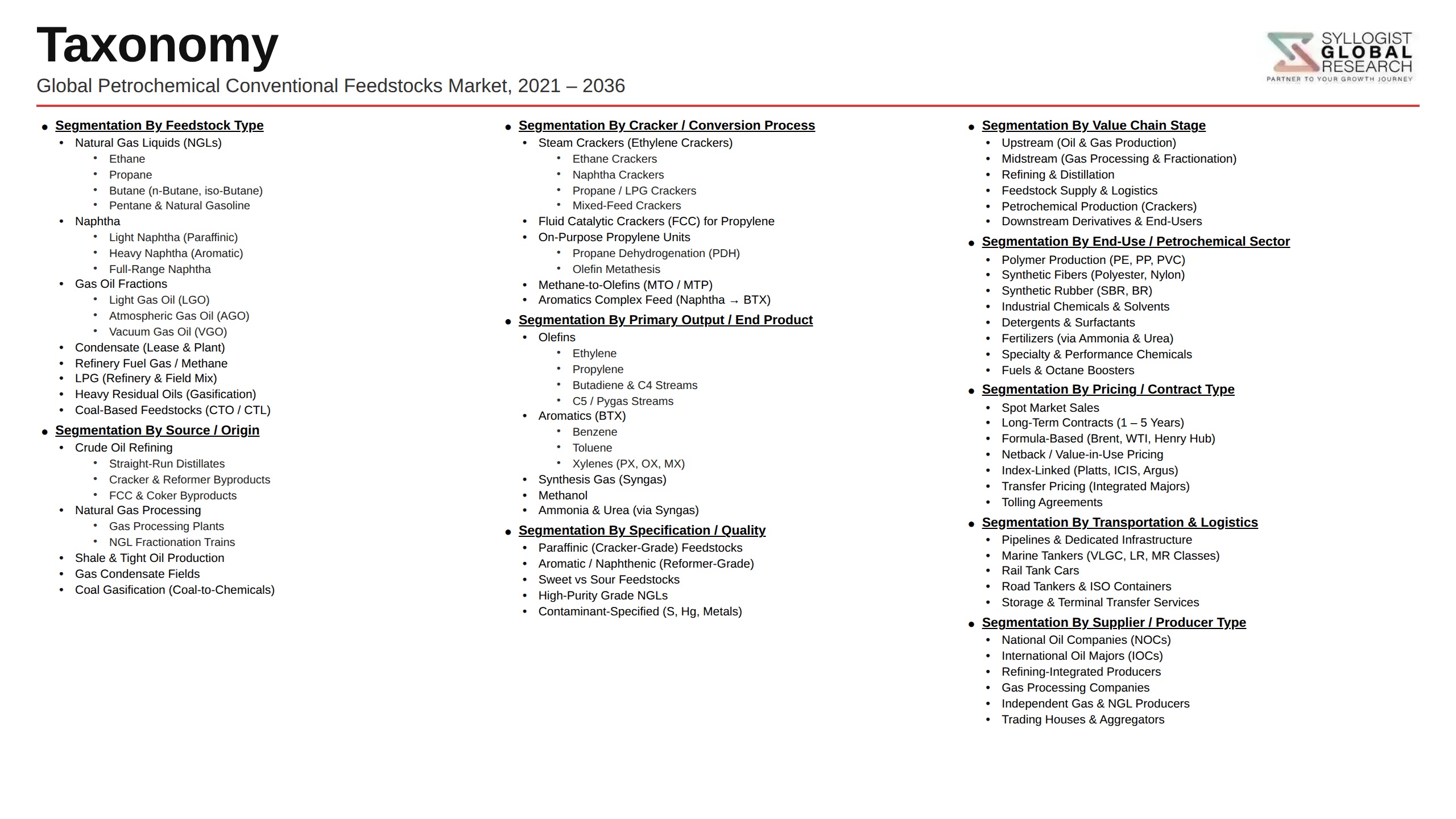

- Segmentation By Feedstock Type

- Naphtha

- Ethane

- Propane and Butane (LPG)

- Gas Oil and Vacuum Gas Oil

- Condensate and Natural Gas Condensate

- Refinery Off-Gases

- Others

- Segmentation By Sourcing Route

- Petroleum Refinery Naphtha and Gas Oil

- Natural Gas Processing Plant Liquids

- Shale Gas and Tight Oil Associated Liquids

- Coal-Derived Methanol and Syngas Feedstocks

- Associated Gas from Crude Oil Production

- Others

- Segmentation By Cracker Technology

- Steam Cracking (Ethane, Naphtha, Gas Oil)

- Fluid Catalytic Cracking

- Catalytic Reforming

- Propane Dehydrogenation

- Methanol-to-Olefins and Coal-to-Olefins

- Others

- Segmentation By Derivative Output

- Ethylene and Polyethylene

- Propylene and Polypropylene

- Butadiene and Synthetic Rubber

- Benzene, Toluene, and Xylenes

- Methanol and Methanol Derivatives

- Specialty Olefins and Higher Alpha-Olefins

- Others

- Segmentation By End Use Industry

- Packaging and Flexible Films

- Construction and Infrastructure Materials

- Automotive and Transportation

- Consumer Goods and Household Products

- Agriculture and Agrochemicals

- Textiles and Synthetic Fibers

- Electronics and Electrical

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global petrochemical conventional feedstocks market valuation in 2025, projected through 2034, segmented by feedstock type, sourcing route, and derivative output, enabling petrochemical producers, feedstock traders, and infrastructure investors to identify the highest-value feedstock categories and most strategically significant production cost competitiveness trends shaping capital allocation across the global petrochemical feedstock landscape?

- How are United States Gulf Coast ethane cracker economics, sustained by shale gas liquid abundance, comparing against naphtha cracker cost positions in Asia and Europe across different crude oil and natural gas price scenarios, and what feedstock cost gap dynamics and co-product value differentials are shaping investment decisions for new cracker capacity across major producing regions through 2034?

- How is the strategic development of integrated crude-to-chemicals complexes in Saudi Arabia, the United Arab Emirates, and China changing the optimal feedstock economics and derivative output mix for large-scale petrochemical investment programs, and what chemical yield maximization targets, crude oil conversion depth ambitions, and specialty derivative portfolio strategies are differentiating leading integrated complex developers from conventional steam cracker investment approaches?

- What carbon pricing escalation trajectories, European Union Emissions Trading System benchmark revisions, carbon border adjustment mechanism implementation timelines, and steam cracker decarbonization investment requirements are most significantly affecting the operating cost competitiveness and long-term capital investment viability of conventional naphtha-based petrochemical complexes in Europe, Japan, and South Korea relative to lower-carbon-cost competitors in the Middle East and North America?

- How are chemical recycling capacity expansion, bio-based olefin production scaling, and mandatory recycled content regulations in the European Union and other jurisdictions expected to displace conventional virgin petrochemical feedstock demand volumes across polyethylene, polypropylene, and aromatic polymer applications through 2034, and what market share transition timelines and feedstock volume displacement magnitudes are realistic given current technology readiness and cost trajectory projections?

- How is the competitive landscape structured among global integrated oil and chemical companies, national oil company petrochemical subsidiaries, and independent petrochemical producers competing for feedstock access and downstream derivative market share, and what feedstock sourcing security strategies, cracker technology investment programs, and derivative portfolio specialization approaches are enabling leading producers to sustain competitive margins across volatile feedstock and product price environments?

- Which regional petrochemical feedstock markets, specifically Asia-Pacific, the Middle East, and North America, are expected to generate the highest incremental feedstock processing investment and derivative capacity additions through 2034, and what combinations of feedstock cost advantage, downstream demand proximity, government industrial policy support, and integration depth economics are defining capital investment attractiveness and competitive positioning across regional petrochemical development programs?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Crude Oil & Natural Gas Price Volatility, Feedstock Cost Fluctuation & Margin Compression Risk

- Refinery Run Rate Variability, Naphtha Availability & Competing Fuel Blending Demand Risk

- Energy Transition, Petrochemical Demand Erosion & Long-Term Fossil Feedstock Displacement Risk

- Geopolitical Supply Disruption, Sanctions, Trade Restriction & Feedstock Route Risk

- Feedstock Quality Variability, Contaminant Specification & Cracker Yield Uncertainty Risk

- New Capacity Additions, Ethane Advantage Shifts & Naphtha Competitiveness Erosion Risk

- Regulatory Framework & Standards

- Petrochemical Feedstock Quality Standards: Naphtha, Ethane, Propane & LPG Specification & ASTM/EN Test Methods

- Pipeline Tariff, Natural Gas Processing & NGL Extraction Regulatory Frameworks by Jurisdiction

- Refinery Product Slate, Naphtha Export & Import Regulatory Frameworks & Customs Classification

- LPG & NGL Export/Import Licensing, Terminal Handling & Storage Safety Regulatory Standards

- Environmental Emission Standards for Feedstock Handling, Storage & Transportation Facilities

- Carbon Pricing, Emissions Trading & Fossil Feedstock Carbon Cost Regulatory Frameworks

- Global Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes per Annum, MTPA)

- Market Size & Forecast by Feedstock Type

- Naphtha (Full-Range, Light & Heavy Naphtha)

- Ethane

- Propane

- Butane & Mixed C4 Streams

- LPG (Liquefied Petroleum Gas: Propane-Butane Mix)

- Gas Oil & Vacuum Gas Oil (VGO)

- Condensate & Ultra-Light Crude

- Refinery Off-Gas & Fuel Gas Streams

- Natural Gasoline & Pentane Plus (C5+)

- Market Size & Forecast by Source

- Crude Oil Refinery-Derived Naphtha & Petrochemical Feedstocks

- Natural Gas Processing & NGL Fractionation-Derived Ethane, Propane & Butane

- Associated Gas & Gas Field Condensate-Derived Feedstocks

- Shale Gas & Tight Oil-Derived Ethane & NGL Feedstocks

- Coal-Derived Naphtha & Synthetic Feedstocks (Coal-to-Olefins Route)

- Steam Cracker Pyrolysis Gasoline (Pygas) Recycle & By-Product Feedstocks

- Market Size & Forecast by Processing Route

- Steam Cracking (Naphtha, Ethane, Propane & Gas Oil)

- Fluid Catalytic Cracking (FCC) Propylene & C4 Production

- Catalytic Naphtha Reforming for Aromatics Production

- Propane Dehydrogenation (PDH) & Butane Dehydrogenation (BDH)

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP) from Natural Gas

- Coal-to-Olefins (CTO) via Methanol Intermediate Route

- Market Size & Forecast by Primary Product Output

- Ethylene

- Propylene

- Butadiene & C4 Mixed Stream

- Benzene, Toluene & Xylenes (BTX Aromatics)

- Mixed C5 Olefins & Isoprene

- Market Size & Forecast by Application

- Polyolefin Production (Polyethylene & Polypropylene)

- PVC, Vinyl Chloride Monomer (VCM) & Chlorinated Petrochemical Production

- Aromatic Derivative Production (PTA, Styrene, Cumene, Phenol & Caprolactam)

- Synthetic Rubber & Elastomer Production

- Specialty Chemical, Oxygenate & Solvent Production

- Fertiliser Feedstock (Ammonia & Urea via Natural Gas SMR)

- Market Size & Forecast by End-User

- Integrated Refinery-Petrochemical Complex Operators

- Standalone Ethylene Cracker & Olefin Producer Operators

- Aromatics Complex & Reformer Operators

- Propane Dehydrogenation (PDH) Plant Operators

- Coal-to-Chemicals & MTO/MTP Plant Operators

- Specialty Chemical & Polymer Producers

- Market Size & Forecast by Sales Channel

- Integrated Producer Self-Supply & Intra-Company Transfer Channel

- Long-Term Bilateral Contract & Feedstock Supply Agreement Channel

- Spot & Short-Term Trading Channel

- Pipeline, Terminal & Logistics Network Supply Channel

- LPG & Naphtha Marine Tanker & Import Terminal Channel

- North America Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Petrochemical Conventional Feedstocks Market Outlook

- Market Size & Forecast

- By Value

- By Volume (MTPA)

- By Feedstock Type

- By Source

- By Processing Route

- By Primary Product Output

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Belgium, Spain, Italy, China, Japan, South Korea, India, Singapore, Thailand, Taiwan, Malaysia, Iran, Saudi Arabia, UAE, Kuwait, Qatar, Russia, Brazil, South Africa, Egypt

- Technology Landscape & Innovation Analysis

- Advanced Steam Cracker Technology: Furnace Design, Coil Materials, Energy Integration & Ethylene Yield Optimisation

- Naphtha Cracker vs. Ethane Cracker Economics: Feedstock Flexibility, By-Product Slate & Integrated Margin Analysis

- Propane Dehydrogenation (PDH) Technology: Oleflex, CATOFIN, FCDh & Star Process Comparison & Catalyst Advances

- Methanol-to-Olefins (MTO) & Methanol-to-Propylene (MTP) Technology: Process Design, Catalyst & Feedstock Economics

- NGL Fractionation & Ethane Recovery Technology: Deep Cut Extraction, Cryogenic Processing & Gas Plant Design

- Refinery-Petrochemical Integration Technology: Crude-to-Chemicals, Maximising Liquid Yield & Naphtha Optimisation

- Digital Twin, Advanced Process Control (APC) & AI-Based Feedstock Optimisation Technology for Crackers & Reformers

- Patent & IP Landscape in Petrochemical Feedstock Processing Technologies

- Value Chain & Supply Chain Analysis

- Crude Oil, Condensate & Natural Gas Upstream Production & Field Supply Chain

- Refinery Naphtha, VGO & By-Product Feedstock Production & Allocation Supply Chain

- Gas Processing, NGL Extraction, Fractionation & Ethane/LPG Product Supply Chain

- Naphtha & LPG Marine Transportation, Tanker Fleet & Import Terminal Supply Chain

- Pipeline, Storage Terminal & Feedstock Logistics Infrastructure Supply Chain

- Commodity Trader, Broker & Feedstock Marketing Channel

- Cracker Operator, Aromatic Complex & Downstream Petrochemical Manufacturer Channel

- Pricing Analysis

- Global Feedstock Benchmark Price Analysis: Naphtha CIF NWE/Japan, Ethane Mont Belvieu & Propane Saudi CP

- Naphtha-to-Ethylene Cracking Margin & Ethane-to-Ethylene Variable Cost Analysis

- Propane Dehydrogenation (PDH) Margin: Propane CP vs. Propylene CFR Analysis

- LPG vs. Naphtha Feedstock Competitiveness & Regional Price Differential Analysis

- Feedstock Cost as Percentage of Total Variable Cost Analysis by Process Route & Region

- Price Cycle Analysis: Historical Feedstock Spread Cycles, Capacity Additions & Crude Linkage

- Sustainability & Environmental Analysis

- Carbon Intensity of Petrochemical Feedstocks: GHG Emissions per Tonne of Feedstock Processed by Route

- Decarbonisation of Steam Cracking: Electric Cracker Technology, Green Hydrogen & CCS Integration

- Role of Conventional Feedstocks vs. Bio-Naphtha, Recycled Feedstock & Green Methanol in Future Petrochemical Supply

- Methane Leakage, Flaring & Venting from Upstream Gas Processing & NGL Supply Chain

- EU CBAM, Carbon Border Adjustment & Scope 3 Emission Reporting Impact on Conventional Feedstock Trade Flows

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Feedstock Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Feedstock Type, Processing Route & Geography

- Player Classification

- Integrated Oil & Gas Majors & National Oil Companies with Refinery-Petrochemical Complex Operations

- Standalone Petrochemical Naphtha Cracker & Ethane Cracker Operators

- NGL Processor, Fractionator & Ethane Extractor Companies

- LPG & Naphtha Commodity Traders, Marketers & Import Terminal Operators

- PDH Plant Operators & Propylene-Focused Petrochemical Producers

- Coal-to-Chemicals & MTO/MTP Producers (Primarily China-Based)

- Competitive Analysis Frameworks

- Market Share Analysis by Feedstock Type, Processing Route & Region

- Company Profile

- Company Overview & Headquarters

- Feedstock Supply Portfolio, Processing Assets & Value Chain Integration

- Key Customer Relationships & Feedstock Offtake Agreements

- Manufacturing & Processing Footprint, Cracker Capacity & Feedstock Volume

- Revenue (Petrochemical Feedstock Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansions, New Projects, Feedstock Strategy Shifts)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Feedstock Cost Advantage vs. Market Integration Depth)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Feedstock Type, Processing Route, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Feedstock Portfolio, Flexibility & Procurement Strategy

- Processing Capacity, Integration & Operational Excellence Strategy

- Geographic Expansion & Supply Chain Diversification Strategy

- Customer, Offtake Partner & End-User Engagement Strategy

- Partnership, M&A & Petrochemical Ecosystem Strategy

- Sustainability, Decarbonisation & Feedstock Transition Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output