Market Definition

The Global Carbon Farming Platforms Market encompasses the software platforms, measurement technologies, methodology development services, verification infrastructure, credit issuance systems, and marketplace ecosystems that enable agricultural land managers to quantify, verify, monetize, and sell greenhouse gas emissions reductions and soil carbon sequestration outcomes achieved through the adoption of regenerative and sustainable land management practices including no-till and reduced tillage, cover cropping, agroforestry, rotational and managed grazing, organic matter application, rewetting of drained agricultural peatlands, biochar incorporation, and enhanced rock weathering. Carbon farming platforms serve as the operational technology backbone of agricultural carbon markets by providing farmers with the data collection tools, soil carbon and greenhouse gas quantification models, regulatory and voluntary carbon standard methodology compliance frameworks, third-party verification facilitation, carbon credit issuance and registry connectivity, and payment disbursement mechanisms required to translate on-farm management practice changes into commercially tradeable carbon credits that can be sold to corporate voluntary carbon buyers seeking high-integrity agricultural soil carbon offsets to support their net-zero emissions commitments. The market encompasses a spectrum of platform architectures from science-based biophysical process modeling approaches that simulate soil organic carbon dynamics and nitrous oxide emissions from management practice inputs without requiring dense physical soil sampling, through hybrid approaches combining remote sensing satellite data with soil sampling verification to reduce measurement cost while maintaining quantification accuracy, to direct measurement approaches using eddy covariance flux towers, automated greenhouse gas analyzers, and dense soil core sampling networks that provide the highest integrity measurement evidence at substantially higher per-farm implementation cost. Key participants include carbon farming software developers, soil carbon measurement technology providers, carbon standard and methodology bodies, third-party verification organizations, voluntary carbon credit registries including Verra and Gold Standard whose approved methodologies govern credit issuance, corporate carbon credit buyers and aggregators, agricultural cooperative organizations, and farming organizations representing potential project participant farmer bases.

Market Insights

The global carbon farming platforms market was valued at approximately USD 920 million in 2025 and is projected to reach USD 5.4 billion by 2034, advancing at a compound annual growth rate of 21.8% over the forecast period from 2027 to 2034, reflecting the powerful and commercially durable alignment between the agricultural sector’s enormous potential as a carbon sink, the growing institutional and corporate demand for high-integrity agricultural carbon credits that deliver both carbon outcomes and verifiable co-benefits including biodiversity, water quality, and soil health improvements, the progressive development of more scientifically credible and cost-effective carbon measurement and verification methodologies that are progressively addressing the integrity criticisms that have historically limited agricultural soil carbon credit buyer confidence, and the policy frameworks emerging in the European Union, Australia, the United States, and the United Kingdom that are creating public payment streams for agricultural carbon sequestration alongside voluntary market demand. Agricultural and forestry land use globally accounts for approximately 10.8 billion hectares, of which approximately 5 billion hectares is agricultural land whose soil carbon storage potential under improved management is estimated by scientific consensus at approximately 1.5 to 4.0 billion metric tons of carbon dioxide equivalent per year if regenerative and sustainable practices were adopted at global scale, representing a mitigation potential equivalent to approximately 3% to 9% of total annual global greenhouse gas emissions and a commercially addressable carbon credit generation opportunity of extraordinary scale that is only beginning to be accessed through formal carbon market mechanisms. The verified agricultural carbon credit supply from formal carbon farming platforms reached approximately 28 million metric tons of carbon dioxide equivalent in 2025, a small fraction of the theoretically available potential whose realization is constrained by measurement and verification cost, additionality demonstration complexity, permanence uncertainty for soil carbon credits, and farmer participation barriers that platforms are progressively addressing through technological innovation and methodology evolution.

Soil organic carbon sequestration from cropland management practice change, particularly the adoption of no-till or reduced tillage, cover cropping, and organic amendment application, represents the largest and most commercially active project activity category within the global carbon farming platform market, with average soil carbon sequestration rates of approximately 0.3 to 0.6 metric tons of carbon dioxide equivalent per hectare per year achievable under favorable soil type, climate, and management intensity conditions that translate into carbon credit revenue of approximately USD 6 to USD 18 per hectare annually at prevailing agricultural soil carbon credit prices of USD 20 to USD 40 per metric ton, providing a supplementary income stream that is meaningful for large-scale grain farmers but insufficient at current price levels to drive practice adoption by smallholder farmers where the implementation cost of regenerative practice transition exceeds the carbon revenue available. The soil carbon credit permanence challenge represents the most technically and commercially significant scientific uncertainty within agricultural carbon markets, as soil organic carbon accumulated under improved management practices can be partially or wholly lost if land management reverts to conventional tillage, drought conditions reduce biomass inputs, or soil disturbance from deep tillage, infrastructure development, or land use change releases sequestered carbon back to the atmosphere, requiring platform methodology designs to incorporate multi-year crediting periods, buffer pools that withhold a percentage of issued credits as insurance against permanence reversal, and long-term monitoring commitments from participating farmers that create contractual obligations extending five to twenty-five years beyond initial credit issuance. The measurement accuracy and quantification cost of soil carbon sequestration credits are the primary technical determinants of carbon farming platform economics, with direct soil core sampling and laboratory analysis costing approximately USD 30 to USD 80 per sample and requiring 20 to 40 samples per field for statistically robust baseline and monitoring measurement, generating per-hectare quantification costs of approximately USD 15 to USD 35 that can represent 50% to 150% of annual carbon credit revenue at current credit prices for smaller farm fields, creating an unfavorable cost-revenue ratio that restricts the commercial viability of direct measurement approaches to large farm scales and driving platform investment in remote sensing, modeling, and stratified sampling approaches that reduce quantification cost per hectare to commercially viable levels.

The enteric methane reduction and manure management segment within carbon farming platforms, targeting the monetization of greenhouse gas emissions reductions from livestock management practice changes including feed additive supplementation with 3-nitrooxypropanol or bromoform-containing seaweed, anaerobic digestion of livestock manure, improved manure storage and application practices, and precision livestock nutrition optimization, represents a rapidly growing credit type whose shorter additionality demonstration complexity, easier measurement through existing livestock management data systems, and higher per-animal carbon credit generation potential relative to soil carbon makes it commercially attractive for dairy and beef cattle, swine, and poultry production operations seeking to generate carbon revenue without the multi-year soil carbon accumulation timelines of cropland sequestration projects. The California Air Resources Board’s Low Carbon Fuel Standard, which awards livestock methane capture projects Pathway Carbon Intensity scores and Protocol credits for biogas captured from covered lagoon digesters and used in transportation fuel pathways, has created one of the most commercially established agricultural methane credit frameworks globally, with California livestock manure digester projects generating approximately 2.8 million metric tons of carbon dioxide equivalent credits annually in 2025 at credit values of approximately USD 45 to USD 75 per metric ton under the Low Carbon Fuel Standard credit pricing, providing a high-value compliance carbon market pathway for dairy and swine operations in California and creating a template for similar livestock methane credit programs being developed in other jurisdictions. The emerging agroforestry and silvopasture carbon credit segment, in which trees integrated within agricultural production systems sequester atmospheric carbon in above-ground biomass and deep root systems while simultaneously providing co-benefits including wind protection, biodiversity habitat, and improved water retention, is attracting increasing platform developer and corporate buyer attention as a high-integrity credit type whose permanence characteristics are superior to soil carbon credits given the slower carbon turnover dynamics of woody biomass relative to organic matter in mineral agricultural soils.

The regulatory and policy landscape governing carbon farming is undergoing rapid evolution across major agricultural economies as governments recognize agricultural land management as a cost-effective greenhouse gas mitigation and carbon sequestration pathway within their nationally determined contributions to the Paris Agreement, progressively creating public payment frameworks that complement voluntary carbon market incentives. The European Union’s Carbon Farming initiative, launched in 2022 and progressively developing certification methodology standards under the Carbon Removal Certification Framework regulation, is creating the foundational regulatory architecture for a market-based agricultural carbon credit trading system within Europe that will provide corporate buyers with regulatory recognition for EU-certified agricultural carbon credits used in net-zero claim substantiation, substantially improving the market value and buyer confidence in European carbon farming credits relative to the currently unregulated voluntary market status. Australia’s Australian Carbon Credit Unit scheme, which includes the Soil Carbon measurement methodology under the Carbon Farming Initiative allowing commercial soil carbon projects on agricultural land to generate Australian Carbon Credit Units tradeable in the domestic compliance and voluntary carbon markets, has accumulated approximately 6,800 project registrations as of 2025 and represents the world’s most established regulatory carbon farming credit program, providing a commercial reference model for the integration of agricultural carbon sequestration into government-administered emissions reduction credit schemes that other jurisdictions including the United Kingdom Woodland Carbon Code, France’s Label Bas Carbone, and Germany’s emerging agricultural carbon framework are actively learning from in developing their own national carbon farming policy architectures.

Key Drivers

Corporate Net-Zero Commitments and Scope 3 Agricultural Supply Chain Decarbonization Targets Creating Structural Demand for High-Integrity Agricultural Carbon Credits

The wave of corporate net-zero commitments adopted by food and beverage manufacturers, retailers, agricultural input companies, and financial institutions with significant agricultural supply chain exposure is creating structural and growing demand for high-integrity agricultural carbon credits as a critical Scope 3 emissions management tool that simultaneously advances food supply chain sustainability, supports farmer transition to regenerative practices, and generates measurable biodiversity and water quality co-benefits that support broader corporate environmental, social, and governance reporting commitments. Science Based Targets initiative guidance requiring companies with agricultural supply chains to engage suppliers on Scope 3 land use emissions reduction is translating corporate sustainability commitments into specific agricultural carbon procurement strategies, with food companies including Unilever, Danone, Nestle, General Mills, and PepsiCo announcing multi-year agricultural carbon programs that collectively represent purchase commitments of hundreds of millions of dollars of agricultural carbon credits from their supply chain farming communities. The Food and Land Use Coalition estimates that agricultural supply chain emissions represent approximately 80% of the total climate impact of the global food system, making agricultural carbon reduction and sequestration credits uniquely valuable for food company Scope 3 emissions management in ways that energy efficiency or renewable electricity purchases cannot address, creating a category of corporate carbon demand that is structurally distinct from the broader voluntary carbon market and that specifically values agricultural credits for their combination of carbon outcome, supply chain relationship, and co-benefit delivery characteristics that justify premium pricing over equivalent carbon credits from industrial or energy project sources.

Advancing Remote Sensing Technology, Satellite Soil Carbon Proxies, and Machine Learning Modeling Reducing Measurement Verification Cost Toward Commercial Viability for Smallholder and Mid-Scale Farms

The progressive improvement in the accuracy and cost-effectiveness of remote sensing-based soil carbon estimation approaches, combining multispectral and hyperspectral satellite imagery with machine learning soil organic carbon prediction models calibrated against dense ground-truth soil sample datasets, is fundamentally improving the economics of carbon farming by reducing the per-hectare quantification cost from the USD 15 to USD 35 range of direct soil sampling approaches toward USD 3 to USD 8 per hectare for validated remote sensing-assisted monitoring approaches, creating a cost structure that makes agricultural carbon credit generation commercially viable for mid-scale farms of 200 to 1,000 hectares whose carbon credit revenue potential at current credit prices is insufficient to justify direct measurement cost at previous per-hectare rates. Synthetic aperture radar satellite data from Sentinel-1 and commercial SAR constellations provides soil moisture, surface roughness, and crop biomass information that correlates with soil organic carbon indicators at spatial resolutions approaching 10 to 20 meters, enabling platform developers to detect year-on-year changes in soil carbon proxy indicators at individual field level without requiring physical site access, dramatically reducing the operational complexity and cost of annual monitoring visits required under conventional sampling-based carbon credit verification protocols. The development of machine learning models trained on large paired datasets of satellite imagery and laboratory-analyzed soil samples from agricultural soil organic carbon monitoring networks including the LUCAS Topsoil Survey in Europe and the National Cooperative Soil Survey in the United States is providing the validation evidence base that carbon standard methodology bodies including Verra and Gold Standard require before approving remote sensing-assisted quantification approaches within their soil carbon credit methodology frameworks, with several platform-developed remote sensing soil carbon methodologies currently in Verra methodology review pending approval that would significantly expand the commercial addressable market for cost-effective carbon farming platform deployment.

Government Agricultural Carbon Payment Frameworks, Agri-Environment Scheme Reform, and Climate Smart Agriculture Funding Programs Creating Public Market Revenue Alongside Voluntary Market Income

National and regional government programs creating public payment mechanisms for agricultural carbon sequestration and greenhouse gas reduction outcomes are progressively emerging alongside voluntary carbon market incentives, providing carbon farming platform operators and participating farmers with revenue diversification that reduces dependency on voluntary carbon market price volatility and corporate buyer demand cycles whose variability has historically created income uncertainty for agricultural carbon credit project developers. The United Kingdom’s Sustainable Farming Incentive and Countryside Stewardship agri-environment payment schemes, which are being redesigned under post-Brexit agricultural policy reform to incorporate payments for soil organic matter improvement, cover cropping, and agroforestry establishment outcomes, are creating a government-funded demand stream for soil carbon sequestration outcomes deliverable through carbon farming platform-verified practice adoption that supplements voluntary carbon market credit revenue and improves the financial predictability of regenerative practice transition economics for English farmers. The United States Department of Agriculture’s Climate Smart Commodities program, which allocated approximately USD 3.1 billion in grants to agricultural commodity organizations implementing climate-smart farming practices and carbon market infrastructure, has funded carbon farming platform development and farmer carbon credit payment programs across grain, livestock, specialty crop, and forestry systems, demonstrating the scale of public investment available for carbon farming market infrastructure development from federal agricultural program sources that create cost-shared deployment opportunities for platform operators alongside their commercial subscription or credit aggregation revenue models. The European Union Common Agricultural Policy eco-schemes, which allocate a mandatory 25% of direct payment budgets to environmental and climate measures, are creating EUR 5.5 billion annually in member state-level funding for agricultural environmental outcomes including soil carbon and greenhouse gas management that carbon farming platforms are positioned to facilitate through verified outcome measurement and payment administration services.

Key Challenges

Soil Carbon Credit Permanence Uncertainty, Reversal Risk, and Long-Term Monitoring Commitment Requirements Creating Farmer Participation Barriers and Buyer Confidence Limitations

The fundamental scientific characteristic of agricultural soil carbon sequestration, that the carbon stored in soil organic matter under improved management practices can be partially or wholly released back to the atmosphere if land management reverts to conventional practices, drought reduces organic matter inputs, or land use changes from agricultural to developed use, creates a permanence risk profile for soil carbon credits that is structurally less secure than the engineered and physically permanent sequestration of geological carbon storage or the avoided emission finality of energy sector offset projects, generating buyer skepticism about the long-term environmental integrity of soil carbon purchases and creating contractual obligation risks for participating farmers whose land use flexibility is constrained by multi-year monitoring commitments that may extend beyond practical farm planning horizons. Carbon farming platform methodology designs typically address permanence risk through buffer pool reserve accounts that withhold 10% to 25% of issued credits from farmer payment to provide insurance against future reversal events, combined with long-term monitoring contracts that obligate farmers to maintain improved practices for five to twenty-five years post credit issuance and to notify and compensate through buffer pool deduction for any reversal events during the monitoring period, creating legal and financial obligations that some farmers find commercially unattractive relative to the incremental carbon revenue available, particularly when soil carbon accumulation rates are at the lower end of the scientific range and credit prices do not provide sufficient revenue premium to compensate for the flexibility loss and legal risk of long-term commitment. The measurement uncertainty inherent in soil carbon quantification, where the high spatial variability of soil organic carbon within individual fields requires dense sampling to achieve statistically significant baseline and monitoring measurements, creates fundamental quantification accuracy limitations that translate into credit quantity uncertainty ranges of plus or minus 20% to 40% of mean estimates for many field-scale soil carbon measurements, limiting the precision of credit issuance and creating liability risk for platform operators whose credit quantities may be challenged during third-party verification.

Low Per-Hectare Carbon Revenue at Current Credit Prices, High Platform Participation Cost, and Insufficient Financial Incentive for Practice Adoption by Smallholder and Cost-Squeezed Farm Operators

The carbon revenue available to agricultural land managers through carbon farming platform participation at current voluntary carbon market credit prices of USD 20 to USD 40 per metric ton for soil carbon credits is insufficient at prevailing soil carbon sequestration rates to justify the management practice changes, monitoring participation obligations, and contractual commitment constraints of carbon farming program participation for the majority of global farm operators whose practice adoption decisions are primarily driven by direct agronomic and financial return on the farming operation rather than supplementary income from carbon credit sales. Average soil carbon sequestration rates of 0.3 to 0.6 metric tons of carbon dioxide equivalent per hectare per year at USD 20 to USD 40 per credit generate gross farm-level carbon revenue of approximately USD 6 to USD 24 per hectare annually before deducting platform fees, verification costs, and buffer pool retention, with net farmer receipts of approximately USD 4 to USD 16 per hectare annually that represent a marginal addition to farm income for large commercial grain operations but an insufficient incentive to cover the cost of practice transition, additional labor, and management change for smallholder operators or farmers who must purchase cover crop seed, biological amendments, or specialized tillage equipment to implement the improved practices required for credit generation. Platform subscription fees of approximately USD 8 to USD 25 per hectare annually for data collection, modeling, and credit facilitation services further compress net farmer carbon income to levels that create weak participation incentives in the absence of supplementary government payments, agronomic co-benefits that independently justify practice adoption, or supply chain sustainability premiums from food company partners that augment carbon credit revenue with commercial procurement preference for regeneratively produced commodities.

Additionality Demonstration Complexity, Baseline Setting Methodology Disputes, and Leakage Assessment Requirements Creating Scientific and Regulatory Friction in Carbon Farming Credit Issuance

The additionality requirement of carbon credit methodologies, which demands that credited emissions reductions and sequestration outcomes represent genuine incremental climate benefit beyond what would have occurred in the absence of carbon market incentive, creates complex baseline setting and practice change counterfactual assessment challenges for agricultural carbon projects where the practices being incentivized including no-till, cover cropping, and rotational grazing are in many regions already being adopted by economically motivated farmers based on agronomic benefits including soil health improvement, erosion reduction, and input cost savings that are independent of carbon market incentives, raising scientific and regulatory questions about whether carbon credits issued for these practices truly represent additionality or merely reward practice changes that would have occurred anyway. The common practice additionality assessment, which carbon standard methodologies typically conduct by evaluating the regional baseline adoption rate of credited practices against adoption thresholds above which practices are considered economically standard rather than incentivized by carbon markets, creates a dynamic eligibility boundary that progressively excludes regions where regenerative practice adoption has spread widely enough to be considered common practice, creating a moving target for platform operators whose farmer participant pools may become ineligible for credit generation in high-adoption regions even as scientific understanding confirms their soil carbon sequestration outcomes are real. The leakage assessment requirement, which evaluates whether carbon farming practice changes in one location induce compensating emissions increases elsewhere through commodity market effects, input supply chain shifts, or land use displacement, adds further scientific complexity to agricultural carbon credit issuance and is a growing focus of methodology scrutiny by carbon standard bodies as the scale of agricultural carbon market participation increases to levels where commodity market effects of practice change at regional scales become potentially measurable.

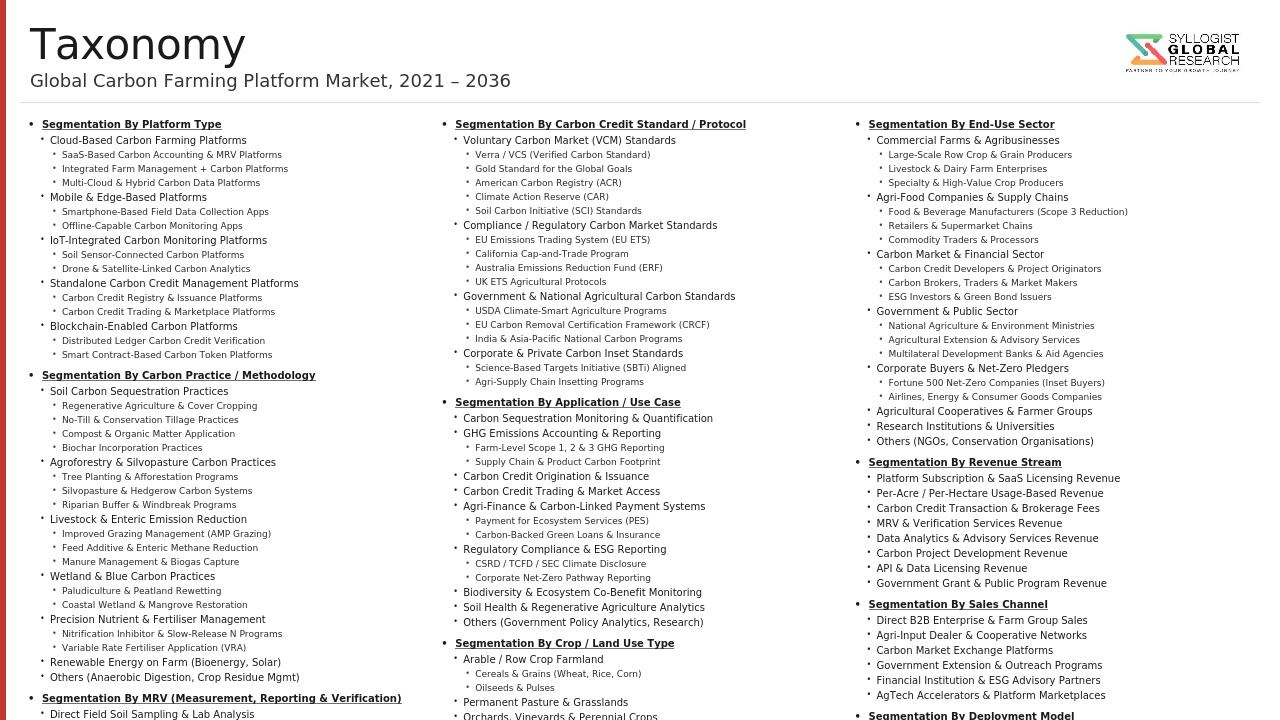

Market Segmentation

- Segmentation By Platform Type

- Soil Carbon Measurement and Credit Issuance Platforms

- Greenhouse Gas Emissions Reduction and Avoided Emission Platforms

- Agroforestry and Silvopasture Carbon Credit Platforms

- Livestock Methane Reduction and Manure Management Platforms

- Wetland and Peatland Rewetting Carbon Platforms

- Enhanced Rock Weathering and Biochar Carbon Removal Platforms

- Integrated Multi-Practice Carbon Farming Platforms

- Government Agri-Environment Payment Administration Platforms

- Others

- Segmentation By Measurement and Verification Approach

- Direct Soil Sampling and Laboratory Analysis

- Remote Sensing and Satellite-Assisted Quantification

- Biophysical Process Modeling (Without Physical Sampling)

- Hybrid Modeling and Stratified Sampling Approaches

- Eddy Covariance and Flux Tower Measurement

- IoT Sensor and Automated Greenhouse Gas Analyzer Networks

- Others

- Segmentation By Agricultural Practice

- No-Till and Reduced Tillage

- Cover Cropping and Green Manure

- Agroforestry and Silvopasture

- Rotational and Managed Grazing

- Organic Matter and Biochar Application

- Peatland and Wetland Rewetting

- Enhanced Rock Weathering

- Precision Fertilizer Management and Nitrous Oxide Reduction

- Livestock Feed Additive and Manure Management

- Others

- Segmentation By Carbon Market Channel

- Voluntary Carbon Market Credits

- Compliance Carbon Market Credits (Government ETS)

- Government Agri-Environment Payment Schemes

- Corporate Supply Chain Sustainability Payments

- Food Company Farm Transition Programs

- Others

- Segmentation By End User

- Large-Scale Commercial Grain and Oilseed Farmers

- Livestock and Dairy Farm Operators

- Smallholder and Family Farm Operators

- Agricultural Cooperatives and Farmer Organizations

- Farmland Investment and Management Companies

- Corporate Food and Beverage Supply Chain Partners

- Government Agricultural Policy Agencies

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Carbon Farming Platforms Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by platform type including soil carbon sequestration, greenhouse gas emissions reduction, agroforestry, livestock methane, peatland rewetting, enhanced rock weathering, and integrated multi-practice platforms, by measurement approach including direct sampling, remote sensing-assisted, process modeling, and hybrid quantification methodologies, and by carbon market channel including voluntary market credits, compliance market credits, government agri-environment payments, and corporate supply chain sustainability programs, to enable platform developers, corporate carbon buyers, agricultural cooperatives, farmland investors, carbon credit registries, and government agricultural policy agencies to identify the highest-growth platform categories and geographic markets generating the most commercially durable demand trajectories through 2034?

- How are remote sensing-based soil carbon estimation approaches using multispectral and hyperspectral satellite imagery combined with machine learning soil organic carbon prediction models advancing toward accuracy levels sufficient for adoption within Verra and Gold Standard approved soil carbon credit methodology frameworks, what is the current measurement accuracy, spatial resolution, temporal monitoring frequency, and per-hectare cost performance of leading remote sensing soil carbon estimation platforms being developed for methodology approval, and what reduction in per-hectare quantification cost from the USD 15 to USD 35 direct sampling range to commercially viable levels of USD 3 to USD 8 would be required to make carbon farming financially attractive for mid-scale farms of 200 to 500 hectares where current direct sampling cost-to-revenue ratios make platform participation economically marginal at prevailing soil carbon credit prices?

- What are the specific policy frameworks, payment rate structures, eligible practice definitions, monitoring and verification requirements, and farmer participation program designs of the European Union Carbon Farming initiative and Carbon Removal Certification Framework, the United Kingdom Sustainable Farming Incentive and Countryside Stewardship agri-environment schemes, the Australian Carbon Credit Unit soil carbon methodology, the United States USDA Climate Smart Commodities program, and France’s Label Bas Carbone and Germany’s emerging agricultural carbon framework, and how are these public payment and regulatory certification programs complementing voluntary carbon market incentives to improve the total financial return available to farmers adopting regenerative practices in ways that improve participation economics and address the insufficiency of carbon credit revenue alone as a practice adoption incentive?

- How are major food and agricultural companies including Unilever, Nestle, General Mills, PepsiCo, Danone, and Cargill structuring their agricultural carbon programs within farmer supply chain relationships, what are the specific procurement volumes, credit price premiums, technical and financial support structures, and additionality and co-benefit verification requirements of their supply chain carbon programs, how are these programs integrating with third-party carbon farming platforms versus developing proprietary platform capabilities, and what is the aggregate corporate agricultural carbon credit demand these programs are generating annually in terms of metric tons of carbon dioxide equivalent, credit types including soil carbon, emissions reduction, and agroforestry, and geographic sourcing concentration in their primary agricultural supply chain regions?

- What are the scientific evidence quality, additionality demonstration robustness, permanence risk management approach, leakage assessment methodology, and buyer confidence status of soil carbon credits, livestock methane reduction credits, agroforestry sequestration credits, and enhanced rock weathering removal credits issued through the major voluntary carbon farming platform registries, and how are the Integrity Council for the Voluntary Carbon Market Core Carbon Principles and the Voluntary Carbon Markets Integrity Initiative guidance on corporate agricultural carbon claims creating quality differentiation between high-integrity and lower-integrity agricultural carbon credits, and what price premium are Core Carbon Principles-approved agricultural credits commanding over non-certified equivalents in the current voluntary carbon market as corporate buyers rebuild agricultural carbon procurement programs on elevated integrity foundations following the voluntary market credibility crisis of 2023 to 2024?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Carbon Credit Additionality, Permanence & Reversal Risk in Agricultural Soil & Land-Use Projects

- MRV Methodology Uncertainty, Soil Sampling Cost & Measurement Accuracy Risk

- Voluntary Carbon Market Price Volatility, Demand Contraction & Greenwashing Scrutiny Risk

- Farmer Adoption, Behaviour Change, Practice Switching Cost & Income Risk

- Regulatory, Standard Revision & Carbon Credit Certification Credibility Risk

- Regulatory Framework & Standards

- Voluntary Carbon Market Integrity Frameworks: ICVCM Core Carbon Principles (CCP), VCMI Code of Practice for High-Integrity Agricultural Carbon Claims & ICROA Code of Best Practice

- Agricultural Carbon Credit Standards & Methodologies: Verra VCS Agricultural Land Management (ALM) Protocols, Gold Standard Soil Carbon, ACR & CAR Soil Enrichment & Grassland Protocol

- Government-Administered Agricultural Carbon Compliance Programme: Australia Emissions Reduction Fund (ERF) Soil Carbon & Vegetation Methods, UK Woodland & Peatland Carbon Code & EU Carbon Farming Initiative Regulatory Framework

- Paris Agreement Article 6 & ITMO Framework: National-Level Agricultural Mitigation Accounting, Corresponding Adjustment for Agri Carbon Credits & UNFCCC REDD+ Agricultural Linkage

- Farm Data Governance, Soil Data Ownership & ESG Reporting Standards: EU Agricultural Data Act, IFRS S2 Agricultural Supply Chain Scope 3 Disclosure, SBTN Nature Targets & Corporate Net Zero Claim Standards for Agricultural Offsets

- Global Carbon Farming Platforms Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Carbon Credits Issued in tCO2e & Hectares Enrolled)

- Market Size & Forecast by Platform Type

- End-to-End Carbon Farming Platform (MRV, Registry, Aggregation & Credit Sale in One)

- MRV (Monitoring, Reporting & Verification) Software Platform

- Carbon Credit Origination, Aggregation & Project Development Platform

- Farm Carbon Footprint Calculator & Supply Chain Emission Advisory Platform

- Voluntary Carbon Credit Marketplace & Trading Platform for Agricultural Credits

- Regenerative Agriculture Data, Insights & Nature-Based Solution Platform

- Government-Administered Agricultural Carbon Programme Platform

- Soil Health, Nutrient & Carbon Co-Benefit Analytics Platform

- Market Size & Forecast by Carbon Practice & Land Use Activity

- Soil Carbon Sequestration (Cover Crop, No-Till, Reduced Tillage & Compost Application)

- Agroforestry, Silvopasture & On-Farm Tree Planting Carbon Sequestration

- Grassland, Rangeland & Permanent Pasture Restoration & Carbon Sequestration

- Wetland, Peatland & Blue Carbon (Mangrove & Coastal Ecosystem) Restoration

- Livestock Methane Reduction: Enteric Fermentation Inhibitor, Feed Additive & Manure Management

- Biochar Production, Soil Application & Long-Term Carbon Removal

- Reduced Nitrogen & Synthetic Fertiliser Use for Nitrous Oxide (N2O) Emission Reduction

- Rice Paddy Methane Reduction via Alternate Wetting & Drying (AWD) Water Management

- Anaerobic Digestion, Biomethane & Agri-Biogas Carbon Project

- Market Size & Forecast by MRV Technology

- Satellite Remote Sensing & AI-Based Soil Organic Carbon Proxy Estimation

- IoT In-Field Sensor & Eddy Covariance Flux Tower Real-Time Carbon Monitoring

- Machine Learning & Biogeochemical Process Model (RothC, CENTURY, DayCent)

- Direct Soil Sampling, Core Analysis & VNIR/NIR Spectroscopy Lab Integration

- LiDAR, Drone & Aerial Biomass Estimation for Agroforestry & Woody Carbon

- Activity-Based Accounting, LCA & Farm Management Record Integration

- Market Size & Forecast by Carbon Standard & Protocol

- Verra VCS (Verified Carbon Standard) Agricultural Land Management Protocols

- Gold Standard for Global Goals Agricultural & Land Use Methodology

- American Carbon Registry (ACR) Soil Carbon & Grassland Protocol

- Climate Action Reserve (CAR) Soil Enrichment Protocol

- Government Compliance Programme Credit (Australia ERF, UK Woodland Carbon Code, EU Carbon Farming)

- Corporate Net Zero, Science-Based Target & Supply Chain Scope 3 Agricultural Protocol

- Market Size & Forecast by Crop & Land Use Type

- Arable & Row Crop Farmland (Wheat, Corn, Soybean & Cotton)

- Grassland, Pasture & Rangeland

- Forestry, Agroforestry & Silvopasture

- Horticulture, Vineyard & Permanent Crop

- Wetland, Peatland & Coastal Blue Carbon

- Degraded & Marginal Land Restoration

- Market Size & Forecast by End-User

- Individual Farmer & Smallholder Enrolled in Carbon Programme

- Commercial Farm, Agribusiness & Large-Scale Operator

- Agricultural Cooperative, Farmer Group & Aggregator

- Food, Beverage & Retail Company (Agricultural Scope 3 Buyer & Supply Chain Programme)

- Corporate Carbon Buyer & Net Zero Programme Operator

- Government, Public Agriculture Authority & National Carbon Farming Programme

- Carbon Project Developer, Fund Manager & Nature-Based Solutions Investor

- Market Size & Forecast by Sales Channel

- Direct Farmer Enrolment & SaaS Subscription

- Agribusiness, Cooperative & Corporate Supply Chain Programme Channel

- Government Programme, Policy-Linked & Development Finance Channel

- API Integration, White-Label Licence & Carbon Registry Partnership Channel

- North America Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Carbon Farming Platforms Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Credits Issued in tCO2e & Hectares Enrolled)

- By Platform Type

- By Carbon Practice & Land Use Activity

- By MRV Technology

- By Carbon Standard & Protocol

- By Crop & Land Use Type

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Australia, Germany, France, United Kingdom, Netherlands, Belgium, Sweden, Denmark, China, India, Indonesia, Brazil, Argentina, Colombia, Kenya, Ethiopia, Ghana, South Africa, New Zealand, Japan, Ukraine

- Technology Landscape & Innovation Analysis

- Satellite Remote Sensing & AI-Based Soil Organic Carbon Estimation Technology Deep-Dive

- IoT In-Field Carbon Flux Sensor, Eddy Covariance Tower & Real-Time Soil Carbon Monitoring Technology

- Machine Learning, Biogeochemical Process Modelling (RothC, DayCent, CENTURY) & Predictive Soil Carbon Stock Change Technology

- Drone-Based Biomass Estimation, LiDAR Canopy Mapping & Agroforestry Carbon Quantification Technology

- Blockchain, Distributed Ledger & Digital MRV Record for Tamper-Proof Carbon Credit Issuance & Chain of Custody

- Life Cycle Assessment (LCA), Activity-Based Accounting & Farm Carbon Footprint Calculation Platform Technology

- Carbon Credit Marketplace Smart Contract, Registry API Integration & Automated Credit Settlement Technology

- Patent & IP Landscape in Carbon Farming Platform Technologies

- Value Chain & Supply Chain Analysis

- Farmer Onboarding, Practice Verification, Baseline Assessment & Enrolment Supply Chain

- Data Collection Layer: Satellite Imagery, Drone Survey, IoT Sensor & Soil Sampling Service Provider

- MRV Software, AI Model, Biogeochemical Model & Cloud Analytics Infrastructure Supply Chain

- Carbon Standard Body, Registry, Validation & Verification (VVB) Organisation Landscape

- Carbon Farming Platform Company, Aggregator & Project Developer Landscape

- Carbon Credit Offtake: Voluntary Market Buyer, Corporate Supply Chain Programme & Government Channel

- Co-Benefit, Biodiversity Credit, Soil Health Premium & Agri-Finance Integration Layer

- Pricing Analysis

- Agricultural Soil Carbon Credit Price Analysis by Standard, Protocol, Geography & Co-Benefit Premium (USD per tCO2e)

- Agroforestry, Grassland & Blue Carbon Credit Price Benchmark vs. Soil Carbon & Technology Removal Credit

- Platform SaaS Fee, Per-Hectare Enrolment & Revenue Share Pricing Model Analysis by Platform Type & End-User

- MRV Cost Analysis: Soil Sampling & Lab Analysis, Drone Survey & Satellite Monitoring Cost per Hectare by Protocol

- Carbon Farmer Income Analysis: Net Carbon Payment per Hectare After Platform Fee, Sampling Cost & Standard Issuance Cost Deduction

- Corporate Supply Chain Programme & Agricultural Scope 3 Credit Premium vs. Spot Voluntary Carbon Market Price

- Sustainability & Environmental Analysis

- Soil Health Co-Benefit of Carbon Farming Practices: Organic Matter Increase, Water Retention, Nutrient Cycling & Biodiversity Improvement Beyond Carbon Sequestration

- Permanence, Reversal Risk & Long-Term Carbon Storage Integrity: Scientific Assessment of Soil, Agroforestry & Wetland Carbon Permanence in Carbon Farming Programmes

- Food Security & Yield Co-Benefit: Evidence for Regenerative Practice Yield Impact, Resilience Building & Input Cost Reduction for Enrolled Farmers

- Smallholder Farmer Livelihoods, Gender Inclusion & Just Transition: Social Sustainability of Carbon Farming Enrolment in Developing Country Agricultural Contexts

- Regulatory-Driven Sustainability: ICVCM CCP Compliance, EU Carbon Farming Initiative Standards, SBTN Agricultural Land Target & Corporate Nature Disclosure (TNFD) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Platform Type & Geography)

- Top 10 Players Market Share by Revenue, Credits Issued & Hectares Enrolled

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Platform Type, Carbon Practice & Geography

- Player Classification

- Dedicated End-to-End Carbon Farming Platform Company (Pure-Play AgCarbon Tech)

- MRV Software & Soil Carbon Measurement Technology Specialist

- Voluntary Carbon Market Exchange & Marketplace with Agricultural Credit Focus

- Agricultural Input Company & Agribusiness with Embedded Carbon Programme

- Carbon Project Developer & Nature-Based Solution (NbS) Fund with Farm Carbon Vertical

- Government-Run Agricultural Carbon Programme & National Registry Operator

- Satellite Data, Remote Sensing & Geospatial AI Company with Agri Carbon Analytics

- ESG FinTech, Blockchain & Digital Carbon Registry Infrastructure Provider

- Competitive Analysis Frameworks

- Market Share Analysis by Platform Type, Carbon Practice & Region

- Company Profile

- Company Overview & Headquarters

- Carbon Farming Platform Products, Services & Protocol Portfolio

- Key Customer, Farmer & Corporate Buyer Relationships

- Platform Footprint: Hectares Enrolled, Credits Issued & Countries Deployed

- Revenue (Carbon Farming Segment) & ARR Growth

- Technology Differentiators, MRV Methodology & IP Portfolio

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Credit Issuances, Platform Launches, Funding Rounds)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (MRV Rigour vs. Farmer Enrolment Scale)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Platform Type, Carbon Practice, MRV Technology, Standard & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & MRV Technology Investment Strategy

- Platform Development, Data Quality & Carbon Integrity Assurance Strategy

- Geographic Expansion & Farmer Enrolment Scale-Up Strategy

- Corporate Buyer, Supply Chain & Government Programme Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Carbon Integrity, Co-Benefit & Nature-Positive Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)