Market Definition

The Global Water-Energy Nexus Infrastructure Market encompasses the planning, engineering, financing, construction, and operation of integrated physical and digital infrastructure systems that simultaneously manage, optimize, and reduce the interdependent resource consumption and environmental impact of water and energy across municipal, industrial, agricultural, and utility-scale applications. The water-energy nexus recognizes the profound and inseparable mutual dependency between the two resource systems: water is required in substantial quantities for energy production through thermoelectric cooling, hydropower generation, bioenergy feedstock cultivation, hydrogen production, and fossil fuel extraction, while energy is required at every stage of the water cycle including abstraction, treatment, distribution, end-use heating and cooling, wastewater collection and treatment, and water resource recovery, with the energy embedded in global water and wastewater systems estimated to represent approximately 4% of total global electricity consumption and a substantially higher proportion of total energy consumption in arid and water-scarce regions relying on energy-intensive desalination and long-distance water conveyance. The market encompasses a broad and technically diverse infrastructure portfolio including integrated water and energy management systems combining smart metering, advanced analytics, and demand response platforms, energy recovery systems within wastewater treatment facilities including biogas combined heat and power from anaerobic digestion, hydropower turbines in water transmission mains and gravity pipelines, and osmotic energy recovery, pumped hydro energy storage using water infrastructure assets, renewable energy-powered water treatment and distribution systems including solar-powered pumping and desalination, precision irrigation systems integrating soil moisture sensing with energy-optimized variable-speed pumping, industrial water-energy integration programs at power generation and manufacturing facilities, and digital twin platforms modeling combined water and energy network performance for integrated optimization. Key participants include water and energy utilities, integrated infrastructure developers, industrial water and energy managers, digital platform providers, engineering firms, development finance institutions, and regulatory bodies overseeing both water and energy sector performance.

Market Insights

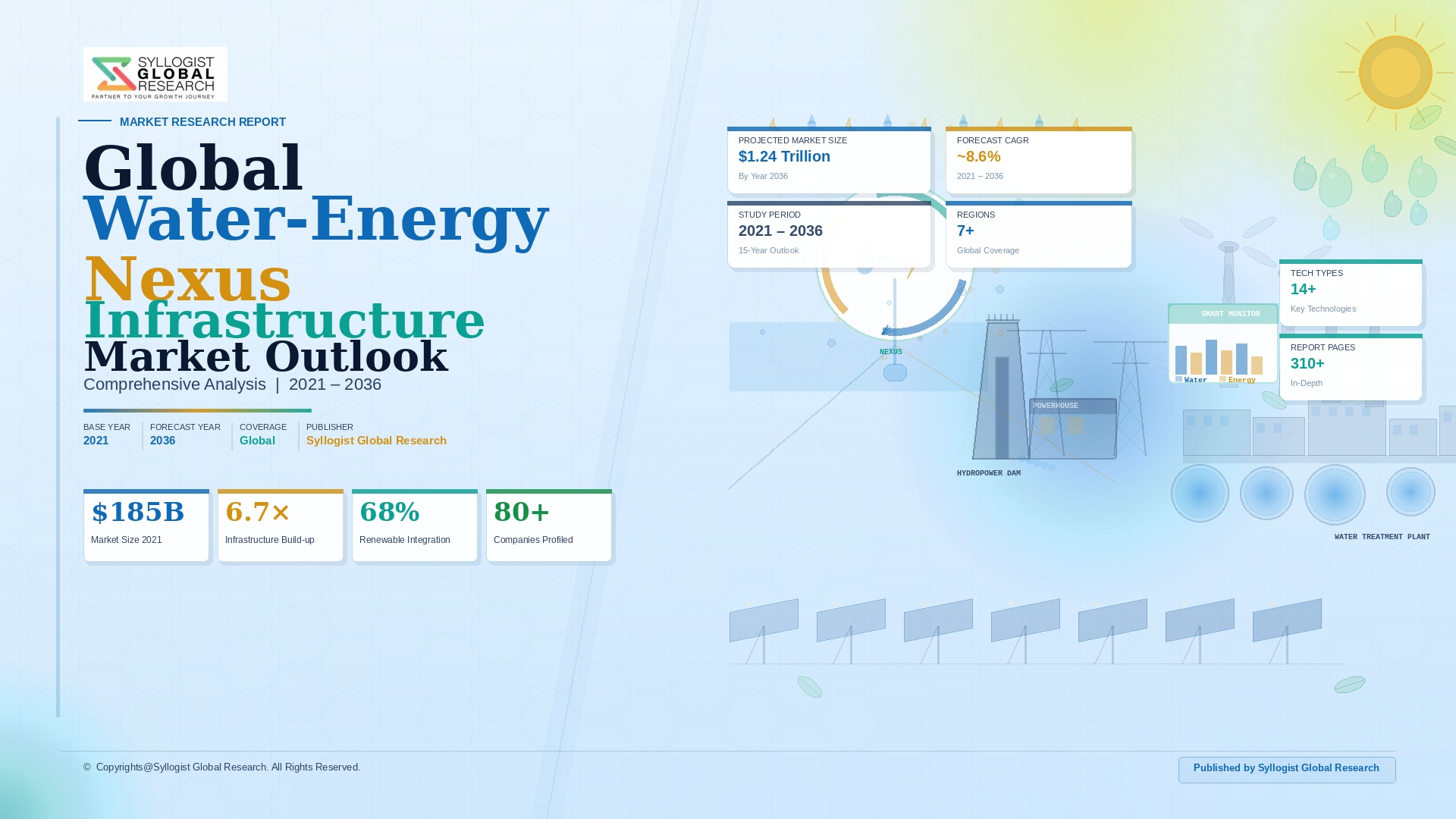

The global water-energy nexus infrastructure market was valued at approximately USD 62.4 billion in 2025 and is projected to reach USD 148.6 billion by 2034, advancing at a compound annual growth rate of 10.1% over the forecast period from 2027 to 2034, reflecting the accelerating policy recognition across national governments, multilateral development banks, and corporate sustainability frameworks that water and energy infrastructure must be planned, financed, and operated as an integrated system rather than independently managed sectoral utilities if the simultaneous goals of water security, clean energy transition, climate resilience, and economic development are to be achieved within the resource and carbon constraints defining the sustainability boundaries of the global economy through the middle of the twenty-first century. The energy cost of water and wastewater services in the United States alone is estimated at approximately USD 21 billion per year, representing the single largest electricity end use in many municipal and state budgets, while the water requirements of thermoelectric power generation account for approximately 40% of total freshwater withdrawals in the United States at approximately 500 billion liters per day, establishing the profound scale of mutual resource dependency that makes water-energy nexus infrastructure optimization not merely an environmental priority but a fundamental economic efficiency and resource security imperative for governments, utilities, and industrial operators globally. Climate change is intensifying the operational interdependency of water and energy systems by simultaneously reducing freshwater availability in water-stressed regions, increasing cooling water requirements for thermoelectric power plants during heat events, reducing hydropower generation capacity during drought periods, and increasing water treatment energy intensity as source water quality deteriorates due to temperature elevation and altered precipitation patterns, creating compounding vulnerability at the intersection of water and energy that demands integrated infrastructure responses rather than independent sectoral adaptation strategies.

The wastewater-to-energy segment represents one of the most commercially mature and rapidly scaling components of the global water-energy nexus infrastructure market, with advanced wastewater resource recovery facilities progressively transforming from energy-intensive waste disposal operations into net energy-producing and resource-generating infrastructure assets that recover biogas for combined heat and power generation, extract nutrients for agricultural use, and produce treated water for non-potable reuse, with the global wastewater treatment sector estimated to contain sufficient organic energy content to generate approximately 2.3 times the electrical energy currently consumed by the sector if the organic matter in wastewater were fully converted to biogas through optimized anaerobic digestion processes. A standard wastewater treatment plant serving 100,000 population equivalents with primary and secondary treatment consumes approximately 30 to 45 gigawatt-hours of electricity annually, while the organic content of its incoming wastewater contains sufficient energy to generate approximately 15 to 25 gigawatt-hours of electricity through anaerobic digestion of primary and secondary sludge to biogas and subsequent combined heat and power generation, with advanced energy optimization including thermal hydrolysis pre-treatment, co-digestion of external organic waste, and heat pump integration enabling progressive wastewater treatment facilities to achieve energy self-sufficiency and in optimal configurations generate net electricity export to the grid. The Aarhus Water utility in Denmark and the DC Water Blue Plains facility in Washington demonstrate that energy-positive wastewater treatment is achievable at utility scale through thermal hydrolysis, enhanced anaerobic digestion, and combined heat and power integration, with DC Water’s CAMBI thermal hydrolysis system at Blue Plains generating approximately 10 megawatts of electrical power from digester gas, reducing biosolids volume by 30%, and eliminating approximately USD 10 million in annual biosolids management costs, establishing a benchmark for water-energy nexus value creation within utility-scale wastewater infrastructure.

The energy-for-water efficiency and renewable-powered water infrastructure segment is experiencing sustained and accelerating investment driven by the critical importance of energy cost reduction for water utility financial sustainability, the availability of low-cost renewable electricity procurement options through power purchase agreements and on-site generation, and the operational and carbon footprint benefits of transitioning water distribution and treatment energy supply from fossil fuel-derived grid electricity to renewable sources that simultaneously reduce operating costs and advance water utility net-zero commitments. Water and wastewater utilities are among the largest institutional electricity consumers in most municipalities, with energy typically representing 30% to 40% of total operating expenditure for water utilities, making energy efficiency and renewable energy procurement strategic financial priorities whose return on investment is directly linked to the same capital cost reduction trajectory in solar photovoltaic, battery storage, and variable frequency drive pump control technology that is simultaneously driving renewable energy adoption across broader infrastructure sectors. The integration of pumped hydropower energy storage within existing water supply infrastructure assets, including reservoirs, water towers, and elevated storage tanks with controllable inflow and outflow infrastructure, represents a commercially innovative water-energy nexus application that provides grid balancing and energy arbitrage revenue streams to water utilities while simultaneously delivering grid stability services to electricity system operators, with pilot programs in Scotland, California, and Australia demonstrating the technical feasibility and revenue potential of water infrastructure pumped storage that could unlock billions of dollars in latent grid services value from existing water supply assets without requiring dedicated energy storage capital investment.

The industrial water-energy nexus optimization segment, encompassing water and energy integration programs at power generation facilities, petrochemical plants, semiconductor fabrication facilities, mining operations, food and beverage manufacturers, and data centers, represents the highest unit-value application category within the global market, accounting for approximately 38% of total market revenue in 2025, driven by the combination of high absolute water and energy costs at large industrial facilities creating substantial financial returns on integration investment, stringent industrial sustainability and environmental disclosure obligations requiring demonstrated progress on water consumption intensity and energy efficiency metrics simultaneously, and the availability of sophisticated industrial digital energy and water management platforms enabling real-time optimization of combined resource flows across complex multi-unit process plants. Power generation remains the most water-intensive industrial sector globally, with thermoelectric cooling water withdrawals at coal, nuclear, gas, and concentrated solar power plants representing approximately 40% of total global freshwater withdrawals, making the transition to dry cooling, hybrid wet-dry cooling, and alternative cooling water sources including treated wastewater reuse, seawater, and mine water a critical water-energy nexus investment priority for power sector decarbonization programs whose water supply security in water-stressed regions directly constrains generation capacity reliability and long-term operational viability under projected climate change scenarios. The semiconductor manufacturing sector represents an emerging high-priority water-energy nexus optimization market, with leading chip fabrication facilities consuming approximately 10 to 15 million gallons of ultrapure water daily per fabrication plant at an energy intensity for water purification and recirculation of approximately 0.3 to 0.5 kilowatt-hours per gallon, making water recycling system investment both an energy efficiency measure and a supply security strategy as semiconductor fabrication clusters in Taiwan, South Korea, and Arizona face growing water availability constraints.

Key Drivers

Simultaneous Water Scarcity and Energy Transition Imperatives Compelling Integrated Infrastructure Investment That Resolves Both Resource Challenges Through Shared Digital and Physical Infrastructure Platforms

The convergence of worsening global water scarcity affecting over 4 billion people annually and the accelerating clean energy transition creating unprecedented investment in renewable electricity infrastructure is generating a structurally unique market development condition in which integrated water-energy nexus infrastructure programs offer superior economic, environmental, and resource security outcomes relative to independent sectoral investment, creating compelling investment cases for integrated approaches that address both imperatives simultaneously through shared infrastructure assets, combined resource optimization algorithms, and integrated financing structures that capture synergies unavailable to separately planned water and energy programs. The energy cost of water production and distribution is rising in water-scarce regions as utilities are compelled to access increasingly remote, deeper, or more saline water sources requiring greater pumping lifts, longer conveyance distances, or more energy-intensive treatment including desalination, water recycling, or advanced oxidation, creating a self-reinforcing dynamic in which water stress increases energy demand for water supply precisely as energy system decarbonization requires the reduction of energy consumption to constrained renewable electricity budgets, making energy efficiency within water infrastructure a priority investment that simultaneously reduces operating costs, carbon emissions, and renewable energy system capacity requirements. Governments committing to both water security and net-zero energy transition objectives under the Paris Agreement and Sustainable Development Goals are increasingly recognizing that siloed sectoral infrastructure planning systematically misses optimization opportunities at the water-energy interface, with integrated national water-energy master plans emerging in Singapore, the Netherlands, Israel, Australia, and California as policy frameworks that explicitly mandate joint planning, cross-sectoral investment evaluation, and integrated regulatory oversight of water and energy infrastructure development.

Escalating Energy Costs, Carbon Pricing Obligations, and Water Utility Financial Sustainability Pressures Driving Wastewater-to-Energy and Energy Recovery Infrastructure Investment

The combination of rising grid electricity prices, expanding carbon pricing mechanisms that increase the effective cost of fossil fuel-derived electricity consumed by water and wastewater utilities, and the growing financial pressure on water utility balance sheets from aging infrastructure investment requirements, regulatory compliance obligations, and ratepayer affordability constraints is creating a compelling financial imperative for water utilities to pursue energy recovery and energy efficiency investments that reduce operating expenditure, generate new revenue streams from biogas and renewable energy assets, and improve balance sheet sustainability through reduced exposure to volatile electricity market pricing. Wastewater treatment utilities operating anaerobic digestion infrastructure can reduce their net electricity consumption by 40% to 80% through optimized biogas combined heat and power deployment, with advanced configurations including thermal hydrolysis pre-treatment and co-digestion of external organic waste streams enabling net energy positive operations that generate electricity revenue offsetting water treatment tariff requirements and improving utility financial resilience, with the additional carbon offset value of avoided grid electricity emissions providing supplementary revenue through carbon markets or regulatory credit programs in jurisdictions with emissions trading systems. The growing deployment of European Union Emissions Trading System carbon pricing at levels approaching USD 70 to USD 80 per metric ton of carbon dioxide equivalent is directly increasing the financial attractiveness of energy recovery investments within water and wastewater infrastructure by elevating the effective cost of continuing fossil electricity consumption at the same time as it provides carbon revenue for biogas-derived electricity displacing grid fossil power, creating a double financial incentive for accelerated water-energy nexus investment by utilities operating within carbon-priced electricity markets that is expected to intensify as carbon prices increase through the forecast period.

Digital Transformation of Water and Energy Utility Operations, Internet of Things Sensor Proliferation, and Advanced Analytics Enabling Real-Time Integrated Resource Optimization

The progressive digitalization of both water and energy utility operations through smart metering infrastructure, Internet of Things sensor networks, supervisory control and data acquisition systems upgrades, and cloud-based analytics platform deployment is creating the data acquisition, communication, and computational infrastructure required to move from independent sectoral resource management toward real-time integrated water-energy nexus optimization, enabling utility operators to identify and capture efficiency opportunities at the intersection of water and energy flows that are invisible within conventional siloed monitoring and management systems. Advanced analytics platforms integrating water network hydraulic models with energy consumption data at individual pump stations, treatment processes, and distribution zone levels are enabling water utility energy managers to optimize pump scheduling against time-of-use electricity tariff structures, shift flexible energy loads away from peak pricing periods, maximize solar self-consumption through coordinated reservoir filling and drawdown, and participate in demand response programs that provide grid balancing revenue while reducing net electricity costs, with utilities implementing advanced energy optimization programs reporting energy cost reductions of 15% to 35% relative to baseline without capital investment in new physical infrastructure. The emergence of digital twin platforms that simultaneously model water network hydraulic performance and energy consumption across entire distribution system footprints, integrating real-time sensor data with predictive demand forecasting, renewable energy generation forecasting, and electricity market pricing signals, is enabling a new category of integrated water-energy management capability that transforms individual infrastructure assets into intelligent nodes within a coordinated resource optimization network, with technology platform providers including Xylem, Itron, Siemens, and IBM advancing commercial water-energy nexus digital twin offerings that are progressively penetrating large and medium-scale water utility customer bases globally.

Key Challenges

Deeply Fragmented Regulatory and Institutional Governance of Water and Energy Sectors Across Separate Agencies Creating Planning, Investment, and Operational Integration Barriers

The structural fragmentation of water and energy sector governance across separate and often non-communicating regulatory agencies, distinct legislative frameworks, independent planning cycles, segregated financial accounting requirements, and different performance metrics and reporting obligations represents the most fundamental institutional barrier to the development of integrated water-energy nexus infrastructure, as the organizational and regulatory architecture governing both sectors was designed for independent management of each resource system and actively impedes the cross-sectoral collaboration, joint investment appraisal, shared data access, and integrated operational optimization that water-energy nexus infrastructure programs require. In the United States, water utilities are regulated by state drinking water primacy agencies, environmental protection offices, and public utility commissions, while energy utilities are regulated by the Federal Energy Regulatory Commission, state public utility commissions, and regional transmission organizations, with overlapping and sometimes conflicting jurisdictional boundaries, cost recovery frameworks, and investment approval processes that create substantial regulatory uncertainty for water-energy nexus projects seeking to earn revenue from both water service delivery and energy market participation simultaneously. The financial accounting separation required of water and energy utilities by their respective regulatory frameworks in most jurisdictions prevents the pooling of capital expenditure budgets, the allocation of shared infrastructure costs across water and energy rate bases, and the cross-subsidization of integrated project economics that would make many water-energy nexus investments financially viable on a combined sector basis even where individual sector standalone returns are insufficient, forcing project developers to construct complex multi-party ownership, revenue sharing, and service agreement structures that add transaction cost, legal complexity, and execution risk to integrated nexus infrastructure programs.

High Upfront Capital Requirements for Integrated Infrastructure Modernization, Long Payback Periods, and Competing Investment Priorities Within Constrained Utility Capital Budgets

Water and wastewater utilities globally are operating within capital investment environments of extraordinary pressure, simultaneously managing aging infrastructure replacement obligations, regulatory compliance investment requirements for water quality and environmental discharge standards, climate resilience upgrades for flood and drought adaptation, and digital transformation programs, within utility capital budgets constrained by ratepayer affordability concerns, debt capacity limitations, and regulatory capital allowance frameworks that in many cases do not adequately provide for the additional investment in water-energy nexus optimization that would generate the greatest long-term financial and environmental value. Wastewater treatment plant energy recovery upgrades including thermal hydrolysis systems, enhanced anaerobic digestion expansion, combined heat and power installation, and associated electrical interconnection infrastructure require capital investments of USD 15 to USD 80 million for medium to large treatment facilities serving 100,000 to 500,000 population equivalents, with project payback periods of eight to fifteen years that extend beyond typical utility capital budget planning horizons and require long-term revenue certainty from biogas generation, electricity export, and carbon credit markets that is difficult to guarantee within volatile energy market environments. The competition between water-energy nexus optimization investment and the more pressing and regulatorily mandated priorities of water mains rehabilitation, lead service line replacement, wastewater collection system renewal, and stormwater management infrastructure investment consistently results in water-energy integration programs being deferred within utility capital allocation processes, with energy recovery and efficiency projects frequently losing priority sequencing to asset replacement programs whose regulatory compliance deadlines impose externally mandated investment timelines that water-energy nexus projects cannot match absent equivalent regulatory mandates.

Data Sharing Constraints, Cybersecurity Risks in Interconnected Water and Energy Operational Technology Systems, and Interoperability Gaps Between Legacy Infrastructure and Digital Integration Platforms

The realization of water-energy nexus infrastructure optimization benefits requires the continuous sharing of operational data across water and energy system boundaries, including real-time electricity consumption data from water utility pump stations, treatment processes, and distribution assets, energy generation output from water utility renewable energy and biogas assets, water system demand forecasts informing flexible load scheduling, and electricity market pricing signals governing optimal pump scheduling and energy storage operation, creating data integration requirements that span the operational technology systems of multiple utility organizations whose legacy control systems were not designed for inter-organizational data exchange and whose cybersecurity policies may actively prohibit the network connectivity required for integrated real-time data sharing. Water utility supervisory control and data acquisition systems and energy management systems were designed as isolated control networks whose operational technology cybersecurity architecture relies on physical and network isolation from external systems as a primary security control, and the integration of these systems with cloud-based water-energy nexus optimization platforms, energy market participation interfaces, and cross-organizational data sharing arrangements introduces internet connectivity and external access pathways that expand the cybersecurity attack surface of critical national infrastructure in ways that regulators and utility security managers are increasingly scrutinizing under mandatory critical infrastructure protection frameworks. The interoperability challenge is compounded by the diversity of legacy control system vintages, communication protocols, data formats, and vendor-specific system architectures across water and energy infrastructure assets whose replacement cycles span thirty to fifty years, creating a persistent installed base of legacy operational technology that lacks the sensor resolution, communication bandwidth, and data accessibility required to feed integrated water-energy nexus analytics platforms with the granularity and timeliness of operational data needed for real-time optimization rather than retrospective performance analysis.

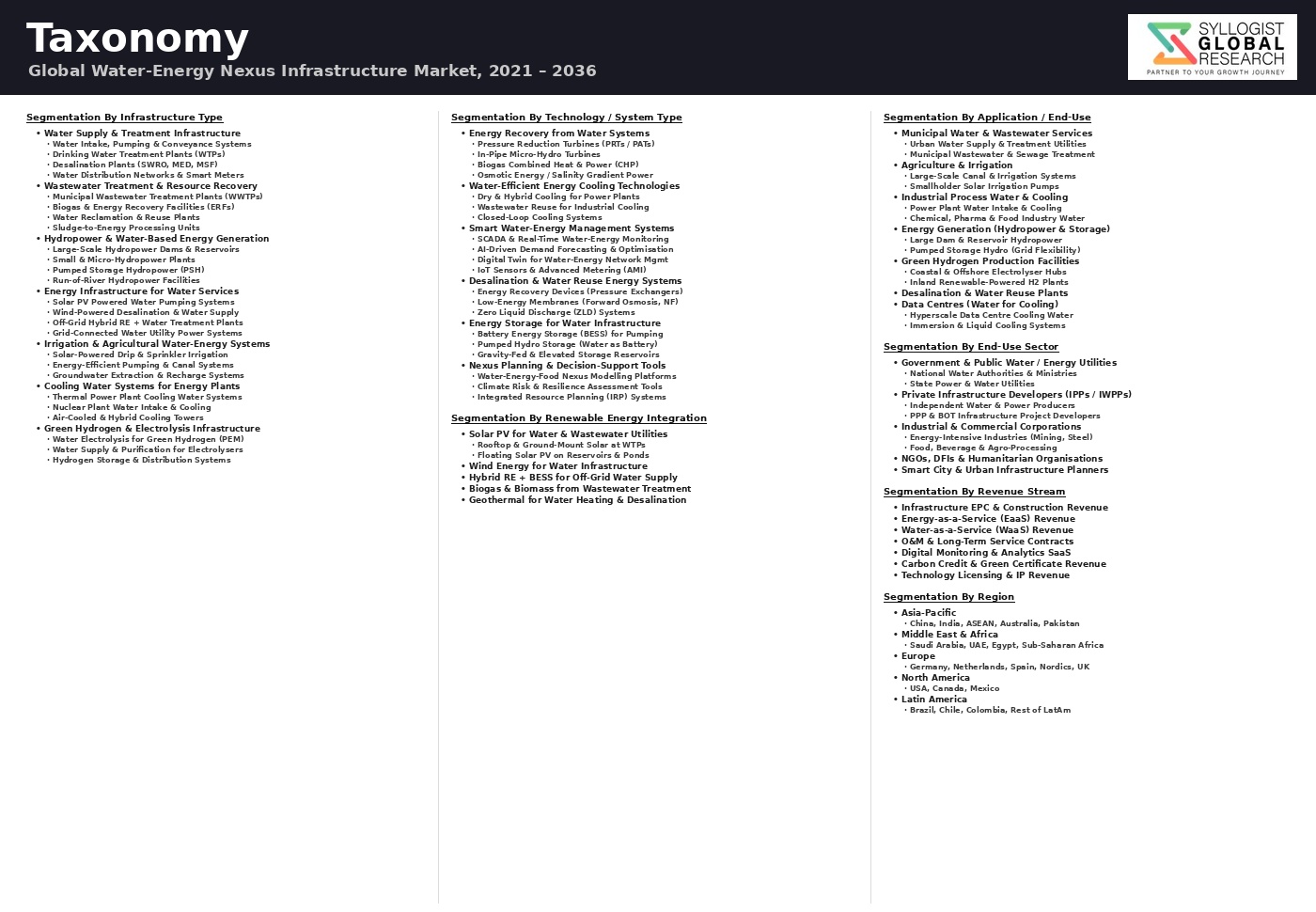

Market Segmentation

- Segmentation By Nexus Application Category

- Wastewater-to-Energy (Biogas Combined Heat and Power, Thermal Hydrolysis, and Co-Digestion)

- Energy Recovery in Water Distribution (In-Pipe Hydropower and Pressure Reducing Valve Turbines)

- Renewable Energy-Powered Water Treatment and Distribution (Solar Pumping and Desalination)

- Water-for-Energy (Thermoelectric Cooling Water Management and Dry Cooling Systems)

- Pumped Hydropower Storage Using Water Supply Infrastructure

- Precision Irrigation and Agricultural Water-Energy Optimization

- Industrial Water-Energy Integration and Process Optimization

- Digital Water-Energy Nexus Management and Analytics Platforms

- Others

- Segmentation By Infrastructure Type

- Wastewater Treatment and Resource Recovery Facilities

- Water Distribution Networks and Pumping Infrastructure

- Water Treatment and Desalination Plants

- Irrigation and Agricultural Water Infrastructure

- Thermoelectric and Hydroelectric Power Generation Facilities

- Industrial Process Facilities (Semiconductor, Petrochemical, and Food Processing)

- Data Centers and Digital Infrastructure

- Integrated Smart City Water and Energy Systems

- Others

- Segmentation By Technology Component

- Anaerobic Digestion and Biogas Systems

- Combined Heat and Power and Cogeneration Systems

- In-Pipe and In-Conduit Hydropower Turbines

- Variable Frequency Drive Pump Control Systems

- Solar Photovoltaic and Renewable Energy Integration Systems

- Battery Energy Storage and Demand Response Systems

- Thermal Hydrolysis and Pre-Treatment Systems

- Digital Twin and Integrated Analytics Platforms

- Advanced Metering Infrastructure and Internet of Things Sensor Networks

- Others

- Segmentation By End-Use Sector

- Municipal Water and Wastewater Utilities

- Power Generation and Energy Utilities

- Industrial Manufacturing (Semiconductor, Petrochemical, Mining, and Food)

- Agriculture and Irrigation Sector

- Data Centers and Telecommunications

- Commercial Buildings and Real Estate

- Government and Military Installations

- Others

- Segmentation By Project Delivery Model

- Engineering-Procurement-Construction (Turnkey)

- Public-Private Partnership and Concession

- Design-Build-Finance-Operate

- Energy Performance Contracting and Guaranteed Savings

- Technology Licensing and Equipment Supply

- Managed Service and Platform-as-a-Service

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Water-Energy Nexus Infrastructure Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by nexus application category including wastewater-to-energy, energy recovery in water distribution, renewable energy-powered water treatment, water-for-energy efficiency at thermoelectric plants, pumped hydro storage using water assets, industrial water-energy integration, and digital nexus optimization platforms, and by end-use sector including municipal utilities, power generation, industrial manufacturing, agriculture, and data centers, to enable integrated infrastructure developers, technology providers, utility operators, development finance institutions, industrial sustainability managers, and infrastructure investors to quantify growth trajectories and identify the highest-value nexus application combinations by sector and geography through 2034?

- What are the quantified energy consumption benchmarks, energy recovery potential, and achievable net energy balance of wastewater treatment facilities at different scales and treatment configurations, including the energy savings achievable through variable frequency drive pump optimization, biogas combined heat and power generation from anaerobic digestion, thermal hydrolysis and co-digestion enhancement, in-pipe hydropower recovery, and solar photovoltaic integration, and what capital investment profiles, operational performance data, and financial return metrics from leading energy-positive wastewater treatment reference facilities including the DC Water Blue Plains facility and Aarhus Water operations establish the commercial viability and replication pathway for energy-neutral and net energy-producing wastewater infrastructure across different utility scales, climate zones, and regulatory environments globally?

- How are the most advanced water-energy nexus infrastructure programs being structured, financed, and governed across leading implementation geographies including Singapore, Denmark, the Netherlands, Israel, Australia, California, and the United Kingdom, and what institutional frameworks including joint water-energy regulatory oversight, cross-sectoral capital budget pooling, integrated infrastructure master planning mandates, energy performance contracting models, and sustainability-linked financing structures are proving most effective in overcoming the regulatory fragmentation, investment horizon mismatches, and competing utility capital allocation priorities that structurally impede water-energy nexus infrastructure investment, and what policy and financing innovations from leading jurisdictions are most transferable to developing economies and emerging market geographies where water-energy nexus infrastructure investment potential is highest but institutional capacity is most constrained?

- What is the water consumption profile, water stress exposure, cooling water technology transition investment program, and water recycling and reuse strategy of the global thermoelectric power generation sector across coal, natural gas, nuclear, and concentrated solar power plant categories, and how are climate change-driven reductions in cooling water availability, water stress regulatory restrictions on thermal discharge, and corporate water stewardship commitments compelling power sector operators to invest in dry cooling, hybrid wet-dry cooling, treated wastewater reuse for cooling, and water efficiency programs at scale, and what are the capital investment requirements, water consumption reduction performance benchmarks, and energy efficiency cost implications of transitioning the global thermoelectric fleet toward lower water intensity cooling configurations through 2034?

- What are the data integration architecture requirements, cybersecurity framework obligations under the European Union Network and Information Security Directive 2 and equivalent critical infrastructure protection regulations, operational technology and information technology convergence design principles, and interoperability standards enabling water utilities, energy utilities, and industrial operators to safely and effectively share the real-time operational data required for integrated water-energy nexus optimization, and which digital platform providers are advancing commercial water-energy nexus management platforms that successfully integrate water network hydraulic modeling, wastewater treatment energy management, renewable energy generation forecasting, electricity market price optimization, and demand response participation within unified operational intelligence environments accessible to water utility operators without specialist energy market or data science expertise?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Water Resource Availability, Scarcity & Climate Change Risk

- Energy Price Volatility, Grid Reliability & Transition Risk

- Regulatory, Permitting & Cross-Sector Policy Coordination Risk

- Technology Integration, Interoperability & Cybersecurity Risk

- Financing, Project Development & Stranded Asset Risk

- Regulatory Framework & Standards

- National Water Security, Water Allocation & Integrated Water-Energy Planning Policy Frameworks

- Renewable Energy Mandates, Grid Integration Standards & Power Purchase Agreement Frameworks Applicable to Water Infrastructure

- Wastewater Treatment, Biogas Recovery & Energy Self-Sufficiency Standards for Water Utilities

- Environmental, Permitting & Cross-Sector Impact Assessment Regulations for Water-Energy Co-Infrastructure Projects

- Green Finance, Climate Fund, ESG Disclosure & Sustainable Infrastructure Procurement Standards

- Global Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Capacity, MW and Million m3/day)

- Market Size & Forecast by Infrastructure Type

- Energy Recovery from Wastewater (Biogas, CHP & Thermal Energy Recovery at WRRFs)

- Hydropower & Pumped Hydro Energy Storage (PHES) Facilities

- Water Supply Conveyance Pipelines with Integrated In-Pipe Hydropower

- Renewable Energy-Powered Desalination Facilities (Solar PV, Wind & Hybrid RE-RO)

- Renewable Energy-Powered Water Pumping, Irrigation & Distribution Infrastructure

- Cooling Water Systems for Power Generation (Once-Through, Recirculating & Dry Cooling)

- Green Hydrogen Production Integrated with Water Electrolysis & Purification Infrastructure

- Smart Water-Energy Microgrid & Off-Grid Co-Generation Systems

- Carbon-Neutral Water Recycling & Reuse Plants with On-Site Renewable Energy

- Market Size & Forecast by Technology

- Anaerobic Digestion & Biogas-to-Energy (CHP, Biomethane & Hydrogen) at Water Resource Recovery Facilities

- Pumped Hydroelectric Energy Storage (PHES) Technology

- In-Conduit & Run-of-River Micro and Small Hydropower Technology

- Solar Photovoltaic (PV) Systems Integrated with Water Treatment & Supply Infrastructure

- Wind Energy Systems Co-Located with Water Infrastructure

- Battery Energy Storage Systems (BESS) for Water Utility Load Shifting & Demand Response

- Heat Pump & Thermal Energy Recovery from Wastewater Effluent

- Pressure Reducing Valve (PRV) Turbines & Inline Hydropower in Water Distribution Networks

- Digital Twin, AI Energy Management & Water-Energy SCADA Integration Platforms

- Market Size & Forecast by Energy Output Type

- Electrical Power Generation (Grid Export & Captive Self-Consumption)

- Thermal Energy Recovery (Heat & Cold for District Heating and Cooling)

- Biomethane & Renewable Natural Gas (RNG) Production from Biosolids

- Green Hydrogen Production (PEM & Alkaline Electrolysis)

- Energy Storage (Pumped Hydro, BESS & Thermal Storage)

- Market Size & Forecast by Project Scale

- Large-Scale National & Regional Infrastructure Projects (Above 50 MW or 100,000 m3/day)

- Medium-Scale Municipal & Industrial Projects (5 MW to 50 MW or 10,000 to 100,000 m3/day)

- Small-Scale Decentralised & Off-Grid Projects (Below 5 MW or 10,000 m3/day)

- Market Size & Forecast by Application

- Municipal Water & Wastewater Utilities

- Agricultural Irrigation & Rural Water Supply

- Industrial Process Water & Cooling Water for Power Generation

- Mining, Oil & Gas Water Management

- Coastal & Island Water Security Infrastructure

- Smart City & Urban Resilience Water-Energy Co-Infrastructure

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utility Operators

- Independent Power Producers (IPPs) & Water-Energy Project Developers

- Industrial & Mining Operators

- Agricultural Cooperatives & Irrigation Scheme Operators

- Government Agencies & National Infrastructure Authorities

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), BOT & Concession Contract

- Direct Equipment & Technology Supply with System Integration

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water-Energy Nexus Infrastructure Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day)

- By Infrastructure Type

- By Technology

- By Energy Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Anaerobic Digestion & Energy Recovery at Water Resource Recovery Facilities (WRRFs) Technology Deep-Dive

- Pumped Hydroelectric Energy Storage (PHES) & Hydropower Technology

- In-Conduit, PRV Turbine & Small Hydropower Technology for Water Distribution Networks

- Solar PV & Wind Integration with Water Treatment, Pumping & Desalination Infrastructure

- Battery Energy Storage, Demand Response & Smart Grid Technology for Water Utilities

- Heat Pump, Thermal Energy Recovery & Wastewater-Source District Energy Technology

- Digital Twin, AI-Based Water-Energy Optimisation & Integrated SCADA Platform Technology

- Patent & IP Landscape in Water-Energy Nexus Infrastructure Technologies

- Value Chain & Supply Chain Analysis

- Anaerobic Digestion, CHP & Biogas Upgrading Equipment Manufacturing Supply Chain

- Hydroturbine, Generator, Pump & Rotating Machinery Supply Chain

- Renewable Energy Equipment (Solar PV, Wind Turbine, BESS & Inverter) Supply Chain for Water Infrastructure

- Water Treatment Process Equipment, Membrane & Chemical Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- Utility Operator, Government Authority & Offtake Partner Channel

- Residuals Management, Biosolids Valorisation & Circular Economy

- Pricing Analysis

- Anaerobic Digestion & Biogas CHP Plant Capital and Operating Cost Analysis

- Pumped Hydroelectric Energy Storage (PHES) Levelised Cost of Storage (LCOS) Analysis

- In-Conduit Hydropower & PRV Turbine Capital and Payback Period Analysis

- Solar PV & Renewable Energy Integration Capex and LCOE Analysis for Water Infrastructure

- Water-Energy Nexus Project Finance, PPP Tariff & Revenue Structure Analysis

- Total Water-Energy Nexus Project Economics: Levelised Cost of Water (LCOW) and Energy (LCOE) Co-Optimisation Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Water-Energy Nexus Infrastructure: Carbon Footprint, Energy Intensity & Water Footprint Across Technology Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Energy-Neutral and Energy-Positive Water Utilities

- Water-Energy-Food Nexus: Integrated Resource Efficiency and Climate Resilience Contribution of Water-Energy Co-Infrastructure

- Environmental Compliance, Aquatic Ecosystem Impact & Biodiversity Consideration in Water-Energy Infrastructure Siting

- Regulatory-Driven Sustainability, SDG 6 (Clean Water) & SDG 7 (Affordable Energy) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Water & Energy Utility Technology Companies

- Specialist Anaerobic Digestion, Biogas & Energy Recovery Technology Providers

- Hydropower, Turbine & PHES Equipment Manufacturers

- Renewable Energy Companies Integrating into Water Infrastructure Projects

- Water Treatment OEMs with Energy Optimisation & Self-Sufficiency Capability

- Digital Twin, AI Energy Management & Smart Water-Energy Platform Providers

- EPC Contractors & Project Developers Specialising in Water-Energy Co-Infrastructure

- Green Hydrogen, Electrolyser & Water Purification Integration Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Water-Energy Nexus Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Water-Energy Nexus Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)