Global Water Quality Monitoring Sensors Market By Sensor Type, By Technology, By Parameter Measured, By Application, By End User, By Distribution Channel, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Water Quality Monitoring Sensors Market encompasses the design, manufacture, distribution, and deployment of electrochemical, optical, biological, and physical sensing devices used to measure, record, and transmit water quality parameters including pH, dissolved oxygen, turbidity, conductivity, temperature, total dissolved solids, heavy metal concentrations, nutrient levels, and microbial contamination indicators across drinking water treatment, wastewater management, industrial process water, environmental monitoring, and aquaculture applications worldwide.

Market Insights

The global water quality monitoring sensors market is experiencing a period of sustained and broad-based expansion, propelled by intensifying regulatory requirements for real-time water quality surveillance, the proliferating deployment of IoT-connected sensor networks in water utility infrastructure, and the growing recognition among governments, industries, and communities that reliable continuous water quality data is an essential foundation for protecting public health, managing water scarcity, and meeting environmental compliance obligations. The market was valued at approximately USD 5.3 billion in 2025 and is projected to advance at a compound annual growth rate of 8.7% through 2034, driven by accelerating smart water infrastructure investment, expanding industrial wastewater discharge regulation, and the urgent need for affordable distributed monitoring solutions in water-stressed and underserved regions across the developing world.

The transition from periodic grab sampling and laboratory-based water quality analysis toward continuous, in-situ, real-time sensor monitoring represents the defining structural shift reshaping the market, as water utilities, regulatory agencies, and industrial operators recognize that point-in-time sampling provides insufficient temporal resolution to detect contamination events, manage treatment process efficiency, or fulfill increasingly stringent continuous discharge monitoring obligations. This shift is accelerating investment in multiparameter sensor probes, autonomous monitoring buoys, pipe-mounted inline analyzers, and distributed sensor node networks capable of delivering uninterrupted water quality data streams that feed digital water management platforms and early warning systems. The integration of water quality sensors with cloud-based data analytics, AI-driven anomaly detection, and supervisory control and data acquisition systems is generating a convergence between sensor hardware and digital water management software that is expanding the total value delivered per monitoring deployment and creating recurring software and connectivity revenue streams alongside hardware sales for leading sensor manufacturers.

Drinking water safety and public health protection represent the most critical and non-discretionary demand driver within the market, as waterborne disease outbreaks, legacy infrastructure contamination events, and the detection of emerging contaminants including per- and polyfluoroalkyl substances, microplastics, and pharmaceutical residues in source water supplies are compelling water authorities globally to upgrade monitoring networks with sensors capable of detecting a broader parameter range at lower detection thresholds and higher temporal frequency than legacy monitoring infrastructure permits. The United States, European Union member states, and major Asia-Pacific economies are simultaneously tightening drinking water quality standards and mandating enhanced source water monitoring, creating compliance-driven procurement programs for advanced sensor deployments across municipal treatment plants, distribution networks, and source water bodies that provide a durable, regulatory-underpinned demand foundation independent of discretionary capital expenditure cycles.

Industrial wastewater discharge monitoring represents the fastest-growing application segment within the broader water quality sensor market, reflecting the progressive tightening of effluent quality standards across pharmaceutical, chemical, food and beverage, semiconductor, and mining industries in major manufacturing economies. Environmental regulators are increasingly mandating continuous online effluent monitoring at industrial discharge points rather than periodic compliance sampling, requiring industries to install permanent inline sensor systems capable of providing real-time discharge quality data accessible to regulatory authorities through digital reporting platforms. Asia-Pacific dominates the market by consumption volume, with China, India, Japan, South Korea, and Australia collectively representing the largest regional demand base, underpinned by the scale of industrial water use, the pace of wastewater treatment infrastructure investment, and the tightening of environmental monitoring regulatory frameworks across the region. North America and Europe represent the second and third largest regional markets respectively, characterized by high sensor technology adoption rates, advanced digital water management infrastructure, and active replacement demand as aging monitoring network hardware is upgraded to connected multiparameter sensing platforms.

Key Drivers

Tightening Drinking Water Safety Regulations and Emerging Contaminant Detection Requirements Compelling Water Utilities and Authorities to Deploy Advanced Continuous Monitoring Sensor Networks

Regulatory agencies across North America, Europe, and Asia-Pacific are progressively strengthening drinking water quality standards and mandating enhanced real-time monitoring of source water, treatment processes, and distribution network water quality parameters, driven by heightened public health awareness, emerging contaminant detection challenges, and the inadequacy of infrequent sampling regimes in detecting rapidly evolving contamination events. New regulatory frameworks targeting per- and polyfluoroalkyl substances, nitrates, heavy metals, and microbial indicators are compelling water utilities to invest in sensor platforms with expanded parameter detection capabilities, lower detection limits, and continuous data transmission functionality, creating durable compliance-driven procurement demand for advanced water quality monitoring sensors that is substantially resistant to utility budget constraints.

Smart Water Infrastructure Investment and IoT-Enabled Water Network Digitalization Driving Large-Scale Deployment of Connected Sensor Nodes Across Water Utility Operations Globally

Governments and water utilities across developed and emerging economies are investing in smart water infrastructure programs that integrate IoT-connected sensor networks, advanced metering systems, digital twin platforms, and AI-powered operational management tools into water supply and wastewater treatment operations, with water quality monitoring sensors forming the primary data collection layer of these digitalized infrastructure architectures. Multilateral development bank financing, national infrastructure stimulus programs, and public-private partnership frameworks are funding large-scale smart water network deployments across developing country urban water utilities, accelerating the geographic expansion of sensor demand beyond established high-income markets and creating significant new procurement opportunities in Latin America, South Asia, Southeast Asia, and sub-Saharan Africa.

Industrial Wastewater Discharge Regulations and Mandatory Continuous Effluent Monitoring Requirements Generating Sustained Sensor Procurement Demand Across Manufacturing and Processing Industries

The progressive replacement of periodic compliance sampling with mandatory continuous online monitoring at industrial wastewater discharge points, driven by regulatory tightening across pharmaceutical, chemical, food processing, semiconductor, textile, and mining industries in major manufacturing economies, is generating a sustained and growing wave of inline and submersible sensor procurement demand from industrial operators required to install permanent effluent quality monitoring systems meeting defined accuracy, data logging, and regulatory reporting specifications. China, India, and Southeast Asian manufacturing economies are enforcing progressively stricter industrial discharge standards with real-time monitoring obligations, opening large and structurally growing markets for water quality sensor manufacturers capable of meeting industrial-grade durability and measurement performance requirements at competitive price points.

Key Challenges

Sensor Fouling, Calibration Drift, and Maintenance Burden in Continuous Deployment Environments Limiting Measurement Reliability and Elevating Total Cost of Ownership for Water Quality Monitoring Networks

Water quality sensors deployed in continuous in-situ monitoring applications across wastewater streams, industrial effluents, and natural water bodies are subject to biofouling of sensing surfaces, reagent depletion in optical and electrochemical sensors, membrane clogging, and calibration drift caused by exposure to chemically complex and biologically active water matrices, requiring frequent manual cleaning, calibration verification, and component replacement that imposes significant operational maintenance costs and creates data reliability gaps when maintenance intervals are extended beyond recommended schedules. The labor intensity and technical skill requirements of field sensor maintenance programs constrain the scalability of continuous monitoring network deployment, particularly in remote monitoring locations and developing country water utility contexts where maintenance workforce capacity is limited.

High Upfront Equipment Costs and Connectivity Infrastructure Requirements Restricting Advanced Sensor Network Adoption Among Budget-Constrained Water Utilities in Developing Economies

The capital cost of deploying multiparameter water quality sensor systems, together with the associated data transmission infrastructure, cloud connectivity services, software platforms, and installation engineering requirements, creates a significant financial barrier to adoption among smaller water utilities, municipal water authorities in lower-income countries, and rural water supply operators that manage water quality monitoring obligations with severely constrained capital and operating budgets. The absence of reliable cellular or satellite data connectivity in remote monitoring locations further restricts the deployment of IoT-enabled sensor platforms that depend on continuous data transmission to deliver the real-time monitoring value proposition, limiting market penetration in geographies where water quality monitoring need is often greatest but infrastructure prerequisites for advanced sensor deployment are least developed.

Data Integration Complexity, Interoperability Gaps, and Cybersecurity Risks in Connected Water Quality Monitoring Systems Constraining the Realization of Smart Water Management Value

The proliferation of water quality sensor deployments from multiple manufacturers utilizing proprietary communication protocols, data formats, and software interfaces creates significant data integration complexity for water utilities and industrial operators seeking to aggregate sensor data streams into unified operational management platforms, requiring substantial systems integration investment and technical expertise that many water sector organizations lack in-house capability to manage. The connection of water quality sensor networks to operational technology and information technology systems simultaneously expands the cybersecurity attack surface of critical water infrastructure, with regulatory agencies and water security experts increasingly flagging the vulnerability of connected monitoring and control systems to cyberattack, creating compliance obligations and security investment requirements that add to the total cost of smart water monitoring deployment.

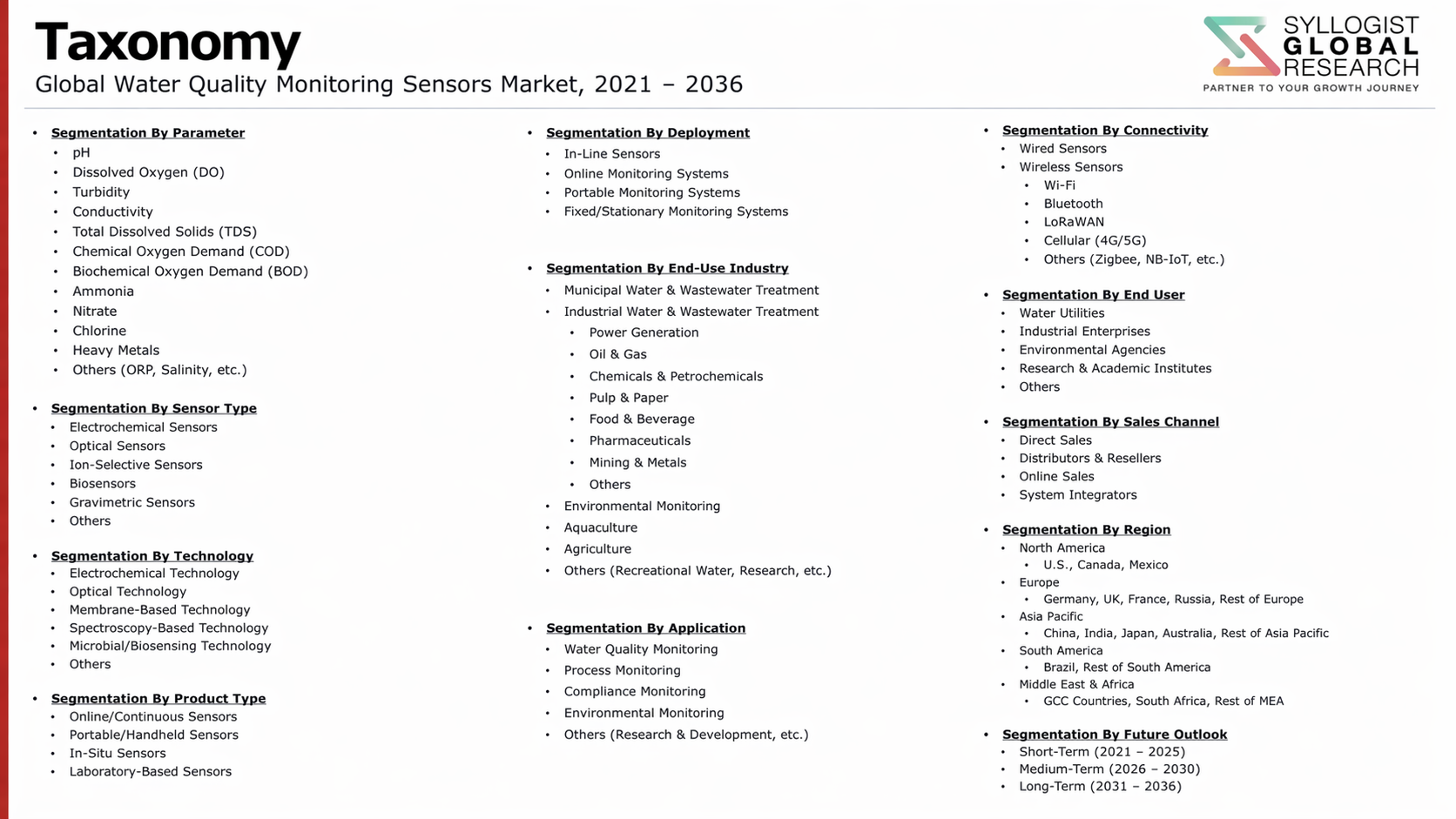

Market Segmentation

- Segmentation By Sensor Type

- Electrochemical Sensors (pH, Dissolved Oxygen, Conductivity, ORP)

- Optical Sensors (Turbidity, UV-Vis Spectroscopy, Fluorescence)

- Physical Sensors (Temperature, Pressure, Flow)

- Biosensors and Microbial Detection Sensors

- Heavy Metal and Nutrient Detection Sensors

- Multiparameter Sensor Probes and Sondes

- Others

- Segmentation By Technology

- Wired and Hardwired Sensor Systems

- Wireless and IoT-Connected Sensor Networks

- Portable and Handheld Monitoring Devices

- Autonomous Buoys and Floating Monitoring Platforms

- Inline and Pipe-Mounted Continuous Analyzers

- Others

- Segmentation By Parameter Measured

- pH and Acidity

- Dissolved Oxygen

- Turbidity and Total Suspended Solids

- Conductivity and Total Dissolved Solids

- Nutrients (Nitrates, Phosphates, Ammonia)

- Heavy Metals and Trace Contaminants

- Microbial and Biological Parameters

- Temperature and Physical Parameters

- Others

- Segmentation By Application

- Drinking Water Treatment and Distribution Monitoring

- Municipal Wastewater Treatment and Effluent Monitoring

- Industrial Process Water and Effluent Monitoring

- Environmental and Surface Water Quality Monitoring

- Groundwater and Aquifer Monitoring

- Aquaculture and Marine Environment Monitoring

- Others

- Segmentation By End User

- Municipal Water and Wastewater Utilities

- Industrial Manufacturing and Processing Facilities

- Environmental Monitoring Agencies and Regulatory Bodies

- Aquaculture and Marine Research Organizations

- Academic and Research Institutions

- Oil, Gas, and Mining Industries

- Others

- Segmentation By Distribution Channel

- Direct Sales from Manufacturers to End Users

- Distributors and Value-Added Resellers

- Online and Digital Procurement Platforms

- Systems Integrators and Engineering Service Providers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global water quality monitoring sensors market valuation in 2025, projected through 2034, segmented by sensor type, parameter measured, and application, enabling sensor manufacturers, water utilities, and technology investors to identify the highest-growth product categories and most durable demand opportunities across the global water quality monitoring landscape?

- How are tightening drinking water safety regulations, mandatory continuous industrial effluent monitoring requirements, and emerging contaminant detection standards across North America, Europe, and Asia-Pacific reshaping sensor procurement specifications, parameter detection capability requirements, and technology adoption timelines for water utilities and industrial operators in each major regulatory jurisdiction?

- Which sensor technology categories, specifically multiparameter IoT-connected probes, inline continuous analyzers, optical spectroscopy sensors, and biosensors for microbial detection, are generating the highest adoption activity and investment through 2034, and what performance, durability, connectivity, and cost factors are driving differentiated uptake across drinking water, wastewater, industrial, and environmental monitoring applications?

- How is the competitive landscape structured among global water quality sensor manufacturers, regional instrument developers, and digital water platform providers, and what product portfolio expansion, geographic market entry, software integration, and strategic acquisition strategies are leading competitors pursuing to consolidate market share across sensor hardware, connectivity infrastructure, and data analytics service categories?

- What sensor fouling, calibration maintenance, data integration, and cybersecurity challenges are most materially constraining the reliability, scalability, and total cost of ownership performance of continuous water quality monitoring deployments, and what self-cleaning sensor designs, remote diagnostics capabilities, and open-protocol interoperability standards are being developed to address these operational barriers?

- Which regional markets, specifically Asia-Pacific, Latin America, and the Middle East and Africa, are expected to generate the most substantial incremental water quality sensor procurement growth through 2034, and what combinations of regulatory tightening, smart water infrastructure investment, industrial expansion, and development finance are accelerating sensor adoption in each region?

- How is the convergence of water quality sensors with IoT connectivity platforms, AI-powered analytics, digital twin water network models, and early contamination warning systems reshaping the competitive value proposition for sensor manufacturers, and what software and services capabilities are becoming essential complements to hardware sales for sustaining customer relationships and capturing recurring revenue in connected water monitoring deployments?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Sensor Calibration Drift, Measurement Accuracy & Data Reliability Risk

- Regulatory Fragmentation, Standards Divergence & Cross-Border Compliance Risk

- Cybersecurity, Data Privacy & IoT Network Vulnerability Risk

- Supply Chain Disruption, Semiconductor Shortage & Component Availability Risk

- Budget Constraint, Public Sector Procurement Delay & Funding Uncertainty Risk

- Regulatory Framework & Standards

- Drinking Water Quality Standards, Monitoring Mandates & Sensor Certification Frameworks by Jurisdiction

- Wastewater Discharge Limits, Effluent Monitoring Requirements & Regulatory Reporting Standards

- Environmental Surface Water & Groundwater Quality Monitoring Regulations

- Sensor Accuracy, Calibration, Type Approval & Metrological Standards (ISO, IEC & Regional)

- Data Management, Telemetry Reporting & Smart Water Network Interoperability Standards

- Global Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Shipped)

- Market Size & Forecast by Sensor Type

- pH Sensors

- Dissolved Oxygen (DO) Sensors

- Turbidity Sensors

- Conductivity & Total Dissolved Solids (TDS) Sensors

- Chlorine & Disinfectant Residual Sensors

- Nitrate, Phosphate & Nutrient Sensors

- Heavy Metal & Trace Contaminant Sensors

- Biological Oxygen Demand (BOD) & Chemical Oxygen Demand (COD) Sensors

- Temperature & Pressure Sensors for Water Quality Applications

- Multi-Parameter Water Quality Sensors & Sondes

- Optical, Fluorescence & Spectroscopic Water Quality Sensors

- Microplastic & Emerging Contaminant Detection Sensors

- Market Size & Forecast by Technology

- Electrochemical Sensor Technology

- Optical & Photometric Sensor Technology

- Biosensor & Immunosensor Technology

- Ion-Selective Electrode (ISE) Technology

- Colorimetric & Reagent-Based Sensor Technology

- Acoustic & Ultrasonic Sensor Technology

- MEMS & Miniaturised Sensor Technology

- AI-Enabled & Smart Sensor Technology with Edge Analytics

- Market Size & Forecast by Connectivity & Communication

- Wired (4-20mA, RS-485, Modbus & HART Protocol) Sensors

- Wireless & IoT-Enabled (LoRaWAN, NB-IoT, Zigbee & Wi-Fi) Sensors

- Satellite-Connected & Remote Telemetry Sensors

- SCADA & DCS Integrated Sensor Systems

- Market Size & Forecast by Installation Type

- Fixed & Stationary Inline Sensors

- Portable & Handheld Water Quality Sensors

- Submersible & In-Situ Deployed Sensors

- Autonomous Underwater Vehicle (AUV) & Drone-Mounted Sensors

- Buoy-Mounted & Floating Platform Sensors

- Market Size & Forecast by Application

- Drinking Water Treatment & Distribution Monitoring

- Wastewater Treatment & Effluent Discharge Monitoring

- Surface Water (River, Lake & Reservoir) Monitoring

- Groundwater & Aquifer Quality Monitoring

- Industrial Process Water & Cooling Water Monitoring

- Aquaculture & Fish Farm Water Quality Monitoring

- Swimming Pool, Recreational Water & Spa Monitoring

- Agricultural Irrigation Water Quality Monitoring

- Coastal, Marine & Estuarine Water Quality Monitoring

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utilities

- Industrial & Manufacturing Facilities

- Government Environmental Monitoring Agencies

- Oil & Gas, Petrochemical & Refinery Operators

- Food & Beverage, Pharmaceutical & Life Sciences Industry

- Power Generation & Energy Utilities

- Aquaculture, Agriculture & Rural Water Management

- Research Institutions, Universities & Environmental Laboratories

- Market Size & Forecast by Sales Channel

- Direct OEM & Manufacturer Sales

- Distributor & Value-Added Reseller (VAR) Network

- System Integrator & EPC Contractor Channel

- Online & E-Commerce Sales Platforms

- Rental, Leasing & Sensor-as-a-Service (SaaS) Channel

- North America Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water Quality Monitoring Sensors Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Shipped)

- By Sensor Type

- By Technology

- By Connectivity & Communication

- By Installation Type

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Electrochemical Sensor Technology Deep-Dive: pH, DO, Conductivity & Ion-Selective Electrodes

- Optical, Fluorescence & UV-Vis Spectroscopic Sensor Technology for Water Quality

- Biosensor, Immunosensor & Molecular Detection Technology for Pathogen & Contaminant Monitoring

- MEMS, Miniaturisation & Lab-on-Chip Technology for Portable Water Quality Sensing

- AI, Machine Learning & Edge Analytics Integration in Smart Water Quality Sensor Platforms

- IoT Connectivity, Telemetry & Cloud-Based Water Quality Data Management Platforms

- Emerging Contaminant Detection: Microplastics, PFAS, Pharmaceuticals & Endocrine Disruptors

- Patent & IP Landscape in Water Quality Monitoring Sensor Technologies

- Value Chain & Supply Chain Analysis

- Raw Material, Chemical Reagent & Specialty Membrane Supply Chain

- Semiconductor, MEMS Chip & Electronic Component Supply Chain

- Sensor Transducer, Electrode & Optical Component Manufacturing Supply Chain

- Sensor Housing, Enclosure & Submersible Assembly Supply Chain

- OEM Sensor Assembly, Calibration & Quality Testing Channel

- Distributor, System Integrator & Value-Added Reseller Channel

- Aftermarket Calibration, Maintenance & Consumable Supply Channel

- Pricing Analysis

- Sensor Unit Price Analysis by Sensor Type & Technology

- Multi-Parameter Sonde & Integrated System Pricing Analysis

- Portable vs. Fixed Installation Sensor Price Comparison

- Total Cost of Ownership (TCO): Sensor Capex, Calibration, Maintenance & Consumables

- Sensor-as-a-Service (SaaS) & Subscription Pricing Model Analysis

- Price Trend Analysis: Impact of Miniaturisation, Volume Production & Competition on Sensor Pricing

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Water Quality Sensors: Carbon Footprint, Material Use & End-of-Life Disposal

- Reduction of Hazardous Reagents & Chemicals in Online Sensor Analysers: Green Chemistry Approaches

- Role of Water Quality Sensors in Supporting SDG 6 (Clean Water & Sanitation) & SDG 14 (Life Below Water)

- Energy Consumption, Solar-Powered & Low-Power Sensor Design for Remote Deployment

- ESG Disclosure, Responsible Manufacturing & Circular Economy for Sensor Hardware

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Sensor Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Sensor Type, Technology & Geography

- Player Classification

- Large Diversified Water Analytics & Measurement Instrument Companies

- Specialist Online & In-Situ Water Quality Sensor Manufacturers

- Portable & Handheld Water Testing Instrument Providers

- IoT, Smart Sensor & Connected Water Quality Platform Providers

- Biosensor & Emerging Contaminant Detection Specialists

- Calibration, Reagent & Consumable Suppliers for Water Quality Sensors

- Competitive Analysis Frameworks

- Market Share Analysis by Sensor Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Water Quality Sensor Products & Technology Portfolio

- Key Customer Relationships & Reference Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Water Quality Sensor Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Sensor Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)Strategic Priority Matrix & Roadmap

- Long-term (2033-2037)

- Strategic Output