Global Water Management in Mining Industry Market By Solution Type, By Water Source, By Mining Type, By Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Water Management in Mining Industry Market encompasses the procurement, deployment, and operational management of water treatment systems, recycling and recirculation infrastructure, dewatering equipment, tailings water recovery technologies, wastewater discharge management platforms, and real-time water quality monitoring solutions utilized across metallic, non-metallic, coal, and energy mineral extraction operations to optimize water use efficiency, ensure regulatory compliance, and minimize freshwater consumption and environmental discharge across the full mining project lifecycle.

Market Insights

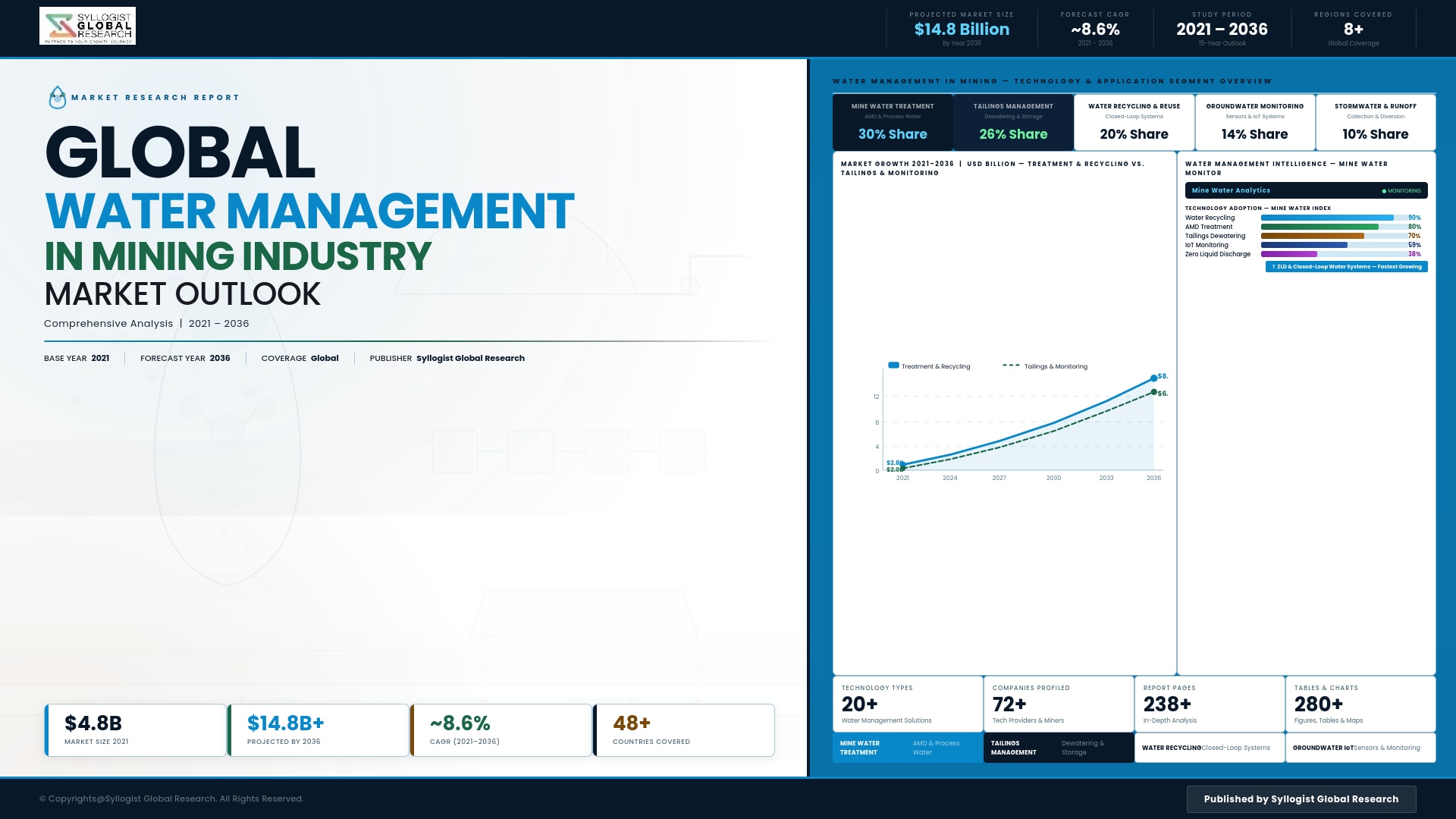

The global water management in mining industry market is navigating a period of intensified strategic relevance, as mounting freshwater scarcity, escalating environmental regulatory requirements, and the accelerating expansion of mining operations into arid and water-stressed regions collectively redefine water stewardship from a peripheral compliance function into a central operational and risk management priority for mining enterprises worldwide. The market was valued at approximately USD 9.8 billion in 2025 and is projected to grow at a compound annual growth rate of 9.6% through 2034, driven by the convergence of stricter discharge standards, rising water procurement costs, investor ESG scrutiny, and the structural demand for critical minerals that is pushing new mining development into geographically challenging water-scarce environments.

Water availability and management quality are increasingly determining the feasibility, social license, and long-term operational continuity of mining projects, particularly in high-growth mining regions such as the Atacama Desert in Chile, the arid zones of Western Australia, the semi-arid mining corridors of southern Africa, and parts of northern India. In these environments, the capacity to achieve near-zero freshwater intake through advanced recycling and recirculation systems is no longer a premium capability but an operational necessity, compelling operators to invest in closed-loop water circuits, high-efficiency thickeners, paste tailings technology, and atmospheric water harvesting solutions that dramatically reduce dependence on freshwater sources subject to competing agricultural, municipal, and ecological demands.

The tailings water recovery and management segment is registering the most rapid investment acceleration within the broader water management market, reflecting the dual imperative of reclaiming process water embedded in tailings slurries to reduce freshwater intake and retrofitting legacy tailings storage facilities to meet revised structural integrity and environmental containment standards introduced in response to high-profile tailings dam failures. Membrane filtration, reverse osmosis, and electrocoagulation technologies are simultaneously expanding in application across mine water treatment, acid mine drainage remediation, and produced water polishing, as operators seek to achieve discharge quality meeting increasingly stringent environmental permit thresholds. Digital water management platforms incorporating IoT sensor networks, predictive flow modeling, and AI-assisted water balance optimization are emerging as a fast-growing software segment, enabling operators to manage complex multi-source water inputs, recycled water inventories, and discharge volumes with a precision that manual water balance management cannot achieve.

Asia-Pacific is projected to record the highest regional compound annual growth rate through 2034, underpinned by the scale and pace of mining expansion in Australia, Indonesia, China, and India, where environmental regulatory standards are progressively converging toward international best practice and water stress conditions in key mining regions are intensifying procurement urgency. Latin America represents the second most dynamic regional market, driven by the copper and lithium production intensity in Chile and Peru where operational water scarcity is a sector-defining constraint. North America maintains the largest absolute market revenue base, supported by comprehensive federal and state water quality regulatory frameworks, active mine water management research programs, and significant investment in acid mine drainage treatment infrastructure across legacy coal and metallic mining regions.

Key Drivers

Intensifying Freshwater Scarcity and Water Stress in Key Mining Regions Compelling Operators to Invest in Advanced Recycling, Recirculation, and Zero-Liquid Discharge Technologies

The progressive depletion of freshwater resources in major global mining regions, driven by the combined pressures of climate change-induced precipitation variability, rising agricultural and municipal water demand, and the geographic concentration of new mining development in arid environments, is establishing water scarcity as a structural operational constraint that mining enterprises must address through capital investment in water recycling, recirculation, and near-zero freshwater intake technologies. Regulatory authorities in water-stressed jurisdictions including Chile, Australia, and South Africa are tightening freshwater extraction allocations, imposing higher water use efficiency standards, and conditioning mine operating permits on demonstrated adoption of water minimization technologies, creating compliance-driven procurement mandates for advanced water management solutions that persist independently of commodity price cycles.

Stringent Environmental Discharge Regulations and Acid Mine Drainage Remediation Obligations Generating Sustained Investment in Water Treatment and Quality Management Infrastructure

Expanding environmental regulatory frameworks governing mine water discharge quality, including limits on suspended solids, heavy metal concentrations, acidity levels, and total dissolved solids in effluent released to receiving water bodies, are compelling mining operators to invest in advanced water treatment infrastructure encompassing chemical precipitation systems, membrane filtration units, ion exchange technologies, and constructed wetland passive treatment systems. Acid mine drainage remediation from legacy and active mining sites represents a particularly significant and non-discretionary expenditure driver, as environmental regulators enforce stricter liability frameworks for long-term drainage management and operators confront the financial and reputational consequences of untreated acid drainage contaminating downstream freshwater resources and agricultural land.

Critical Minerals Expansion and New Mine Development in Water-Constrained Geographies Creating Structural Demand for Fit-for-Purpose Water Management Infrastructure Across the Project Lifecycle

The global clean energy transition is generating unprecedented investment in new mine development targeting lithium, cobalt, nickel, copper, and rare earth elements, with a significant share of prospective new mining projects located in arid or semi-arid geographies where surface and groundwater availability is severely limited and community and regulatory tolerance for freshwater appropriation by mining operations is diminishing. This spatial mismatch between critical mineral resource endowment and water availability is making advanced water management infrastructure, including seawater desalination systems, atmospheric water capture, and ultra-high efficiency tailings dewatering, a fundamental project feasibility requirement from the earliest stages of mine design and permitting, embedding water management capital expenditure directly into project development economics.

Key Challenges

High Capital and Operating Costs of Advanced Water Treatment Technologies Creating Financial Barriers to Adoption Particularly Among Small and Mid-Scale Mining Operations

The capital expenditure and ongoing operating costs associated with deploying high-performance water treatment technologies including reverse osmosis membranes, electrochemical treatment systems, and zero-liquid discharge evaporation infrastructure are substantial, creating significant adoption barriers for smaller and mid-tier mining operators with constrained capital budgets, limited technical capacity to operate complex water treatment systems, and shorter project mine lives that reduce the net present value justification for major water infrastructure investments. The energy intensity of advanced membrane treatment and desalination technologies further compounds operating cost burdens in remote mining locations with limited grid access, where power must be generated through diesel generation at elevated cost.

Complexity of Managing Highly Variable Mine Water Chemistry and Multi-Contaminant Streams Limiting the Scalability and Reliability of Standardized Water Treatment Solutions

Mine water streams are characterized by highly variable and site-specific chemical compositions, encompassing acid mine drainage with elevated heavy metal loads, process water containing residual reagents and mineral fines, saline groundwater encountered during deep mining, and stormwater with variable suspended solids and sediment contamination. This chemical complexity makes standardized water treatment solution deployment unreliable and frequently necessitates bespoke treatment train design, extended piloting programs, and specialized engineering expertise for each project, extending implementation timelines, elevating project development costs, and limiting the ability of technology providers to deploy scalable, repeatable water management solutions across diverse mining operating contexts.

Community Opposition, Indigenous Water Rights Frameworks, and Competing Stakeholder Water Claims Complicating Mine Water Allocation and Discharge Permitting Processes

Mining operations in many jurisdictions face intensifying community and indigenous stakeholder opposition to freshwater abstraction and mine water discharge activities, rooted in concerns over impacts on local water availability, agricultural water security, aquatic ecosystem health, and culturally significant water bodies. Indigenous water rights frameworks in Australia, Canada, Chile, and parts of Africa are progressively strengthening legal protections for traditional water use and ecosystem water entitlements, adding complexity to mine water permitting processes, conditioning approvals on enhanced community benefit arrangements, and in some cases restricting operational water access in ways that fundamentally affect mine site water balance planning and treatment infrastructure design.

Market Segmentation

- Segmentation By Solution Type

- Mine Dewatering Systems and Pumping Infrastructure

- Water Treatment and Purification Technologies

- Tailings Water Recovery and Management Systems

- Water Recycling and Recirculation Infrastructure

- Acid Mine Drainage Treatment Solutions

- Digital Water Monitoring and Management Platforms

- Others

- Segmentation By Water Source

- Groundwater and Aquifer Water

- Surface Water and Precipitation Runoff

- Process and Recycled Water

- Seawater and Brackish Water

- Tailings Pond Water

- Others

- Segmentation By Mining Type

- Underground Mining

- Open-Pit Surface Mining

- Solution and In-Situ Leaching Mining

- Placer and Alluvial Mining

- Others

- Segmentation By Application

- Ore Processing and Mineral Beneficiation

- Dust Suppression and Haul Road Management

- Tailings Slurry Transport and Management

- Potable Water Supply for Mine Camps

- Effluent Treatment and Discharge Management

- Mine Closure and Rehabilitation Water Management

- Others

- Segmentation By End User

- Integrated Major Mining Corporations

- Mid-Tier and Junior Mining Companies

- Contract Mining and Mine Management Operators

- State-Owned Mining Enterprises

- Environmental Engineering and Remediation Firms

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Water Management in Mining Industry Market in 2025, projected through 2034, segmented by solution type and application, enabling mining operators, water technology investors, and environmental service providers to identify highest-growth solution categories and most durable procurement opportunities across the mining water management landscape?

- How are freshwater scarcity conditions, tightening mine water discharge regulations, and indigenous and community water rights frameworks evolving across key mining jurisdictions including Chile, Australia, South Africa, and Canada, and how are these environmental and regulatory dynamics reshaping water infrastructure investment priorities for mine operators at the project feasibility, development, and operational stages?

- Which water management solution categories, specifically tailings water recovery systems, acid mine drainage treatment technologies, advanced membrane filtration, and digital water balance platforms, are generating the highest adoption activity and capital investment through 2034, and what technical performance, cost efficiency, and regulatory compliance factors are driving differentiated uptake across mining type and geography?

- How is the competitive landscape structured among global water treatment equipment manufacturers, mining-specialist environmental engineering firms, and digital water management platform developers, and what acquisition, partnership, and service contract strategies are enabling technology providers to build durable positions across the fragmented and geographically dispersed mining water management market?

- What capital expenditure barriers, operational complexity constraints, and workforce capability gaps are limiting the pace of advanced water treatment and recycling technology adoption among mid-tier and junior mining operators, and what modular technology designs, managed service models, and development finance instruments are emerging to accelerate adoption in cost-sensitive and capacity-constrained operating environments?

- Which regional mining markets, specifically Latin America, Asia-Pacific, and Africa, are expected to generate the most substantial incremental water management infrastructure investment through 2034, and what combinations of water stress severity, regulatory tightening, critical minerals project development, and community stakeholder pressure are shaping water technology procurement priorities and supplier selection in each region?

- How is the structural expansion of critical minerals mining for electric vehicle and clean energy supply chains altering the water management requirements and investment profiles of new mine development projects, and what water stewardship standards, supply chain due diligence requirements, and responsible sourcing frameworks imposed by downstream manufacturers are accelerating adoption of advanced water management technologies among upstream mining producers?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Water Scarcity, Drought & Climate-Driven Supply Risk

- Acid Mine Drainage, Legacy Contamination & Perpetual Treatment Risk

- Regulatory, Discharge Permit & Tailings Seepage Compliance Risk

- Community, Indigenous Water Rights & Social License Risk

- Capital Investment, Remote Site Logistics & Water Infrastructure Financing Risk

- Regulatory Framework & Standards

- National Water Allocation, Mine Dewatering & Groundwater Abstraction Licensing Frameworks

- Acid Mine Drainage, Heavy Metal Discharge & Industrial Wastewater Standards

- Tailings Dam Safety, Global Industry Standard on Tailings Management (GISTM) & Seepage Regulations

- Mine Closure, Post-Closure Water Management & Long-Term Liability Frameworks

- Green Finance, ICMM, IRMA Certification & Sustainable Mining Water Procurement Standards

- Global Water Management in Mining Industry Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Treatment Capacity, Million m3/day)

- Market Size & Forecast by Infrastructure Type

- Mine Dewatering Systems (Pit, Underground & Groundwater Abstraction)

- Process Water Supply, Clarification & Distribution Infrastructure

- Acid Mine Drainage (AMD) & Mine Effluent Treatment Systems

- Heavy Metal, Selenium, Arsenic & Cyanide Treatment Systems

- Tailings Thickening, Dewatering & Water Recovery Systems

- Water Recycling, Reuse & Zero Liquid Discharge (ZLD) Systems

- Stormwater Management, Runoff Diversion & Sediment Pond Infrastructure

- Mine Closure, Post-Closure & Passive Water Treatment Systems

- Real-Time Water Quality Monitoring, Smart Metering & Digital Water Platform

- Market Size & Forecast by Technology

- Membrane Technology (Reverse Osmosis, Nanofiltration & Ultrafiltration)

- Thermal Evaporation, Mechanical Vapour Recompression (MVR) & Crystallisation Technology

- Chemical Precipitation, Lime Neutralisation & Sulphide Precipitation Technology

- Biological Treatment (Sulphate-Reducing Bacteria & Anaerobic Bioreactor) Technology

- Ion Exchange & Selective Adsorption Technology

- Electrocoagulation, Electrodialysis & Electrochemical Treatment Technology

- Advanced Oxidation, Ozonation & UV Disinfection Technology

- High-Rate Thickener, Filter Press & Paste Tailings Dewatering Technology

- Digital Twin, AI Water Balance & SCADA Integration Platform Technology

- Market Size & Forecast by Water Output Type

- Potable & Fresh Water Production for Mine Site Use

- Process Water Supply for Mineral Processing & Beneficiation

- Dust Suppression, Non-Contact & Utility Water

- Treated Effluent Compliant for Environmental Discharge

- Reclaimed & Recycled Water for Closed-Loop Reuse

- Market Size & Forecast by Project Scale

- Large-Scale Mine Water Infrastructure (Above 100,000 m3/day)

- Medium-Scale Mine Water Systems (10,000 to 100,000 m3/day)

- Small-Scale & Remote Site Water Systems (Below 10,000 m3/day)

- Market Size & Forecast by Application

- Copper, Gold & Precious Metal Mining

- Iron Ore, Nickel & Base Metal Mining

- Critical & Battery Mineral Mining (Lithium, Cobalt, Rare Earths & Graphite)

- Coal & Industrial Minerals Mining

- Uranium & Radioactive Mineral Mining

- Construction Aggregates, Quarrying & Building Materials

- Oil Sands & Unconventional Extractive Operations

- Market Size & Forecast by End-User

- Major Mining Company & Tier-1 Operator

- Mid-Tier & Junior Mining Company

- Mining EPC Contractor & Water Service Provider

- Government Mining Authority & State-Owned Enterprise

- Oil Sands, Coal Seam Gas & Unconventional Extractive Operator

- Market Size & Forecast by Sales Channel

- Direct Equipment Supply, Chemical Dosing & Long-Term Supply Contract

- EPC & Turnkey Water Treatment Project Contract

- Build-Own-Operate (BOO), Water-as-a-Service (WaaS) & Concession Contract

- Operations & Maintenance (O&M), Chemical Service & Performance Contract

- North America Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Water Management in Mining Industry Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Treatment Capacity, Million m3/day)

- By Infrastructure Type

- By Technology

- By Water Output Type

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analysed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Mine Dewatering, Pit Pumping & Groundwater Abstraction Technology Deep-Dive

- Acid Mine Drainage (AMD) Treatment & Long-Term Passive Treatment Technology

- Heavy Metal, Selenium & Arsenic Removal Technology (Precipitation, Adsorption & Ion Exchange)

- Membrane Technology (RO, NF & UF) for Mine Water Treatment

- Thermal Evaporation, MVR, Crystallisation & Zero Liquid Discharge Technology

- Tailings Thickening, Paste Backfill & Filtered Tailings Water Recovery Technology

- Biological Treatment, SRB Bioreactor & Constructed Wetland Technology

- Patent & IP Landscape in Mining Water Management Technologies

- Value Chain & Supply Chain Analysis

- Water Treatment Equipment, Pump & Membrane Manufacturing Supply Chain

- Specialty Chemical (Lime, Flocculant, Precipitant & Cyanide Destruction) Supply Chain

- Tailings Thickener, Filter Press & Dewatering Equipment Supply Chain

- Digital, SCADA, Sensor & Water Quality Monitoring Technology Supply Chain

- EPC Contractor, Water Engineer & System Integrator Procurement Landscape

- Mining Operator, Government Authority & Offtake Partner Channel

- Sludge Management, Brine Disposal & Residual Handling Supply Chain

- Pricing Analysis

- Mine Dewatering & Groundwater Abstraction Capital and Operating Cost Analysis

- AMD Treatment & Heavy Metal Removal Capital and Lifecycle Cost Analysis

- Membrane, Thermal Evaporation & ZLD System Capex and Operating Cost Analysis

- Tailings Dewatering & Filter Press Capital and Operating Cost Analysis

- Mine Water Management Long-Term Service Contract, Indexation & Tariff Structure Analysis

- Total Mine Water Project Economics: Cost per m3 Treated & Learning Curve Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Mining Water Management Technologies: Carbon Footprint, Energy Intensity & Freshwater Footprint Across Treatment Routes

- Carbon Neutrality & Net Zero Contribution: Pathway to Low-Energy, Renewable-Powered Mine Water Treatment

- Responsible Water Stewardship, Alliance for Water Stewardship (AWS) & ICMM Water Reporting

- Environmental Compliance, AMD Management, Tailings Seepage & Biodiversity Consideration

- Regulatory-Driven Sustainability, GISTM, SDG 6 (Clean Water) & SDG 12 (Responsible Consumption) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Infrastructure Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Infrastructure Type, Technology & Geography

- Player Classification

- Integrated Water Technology & Mining Water Solution Companies

- Specialist Mine Dewatering, Pump & Pipeline Equipment Manufacturers

- Membrane, Reverse Osmosis & ZLD Technology Providers

- Chemical Precipitation, Specialty Reagent & Cyanide Treatment Specialists

- Tailings Thickener, Filter Press & Paste Backfill Equipment Providers

- Biological Treatment, Constructed Wetland & Passive Treatment Innovators

- Digital Water, Real-Time Monitoring & SCADA Platform Vendors

- EPC, Water-as-a-Service (WaaS) & Mine Water Contract Operation Specialists

- Competitive Analysis Frameworks

- Market Share Analysis by Infrastructure Type, Technology & Region

- Company Profile

- Company Overview & Headquarters

- Mining Water Management Products & Technology Portfolio

- Key Customer Relationships & Reference Mine Water Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Mining Water Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Infrastructure Type, Technology, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output