Global Advanced Membrane Filtration Technologies Market By Membrane Type, By Material, By Module Configuration, By Application, By End Use Industry, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Advanced Membrane Filtration Technologies Market encompasses the development, manufacture, and commercial deployment of semipermeable barrier systems including microfiltration, ultrafiltration, nanofiltration, reverse osmosis, forward osmosis, membrane bioreactor, and gas separation membrane technologies, utilized to separate, purify, concentrate, or fractionate liquids, gases, and dissolved constituents across water treatment, pharmaceutical, food and beverage, chemical processing, biotechnology, energy, and industrial wastewater management applications worldwide.

Market Insights

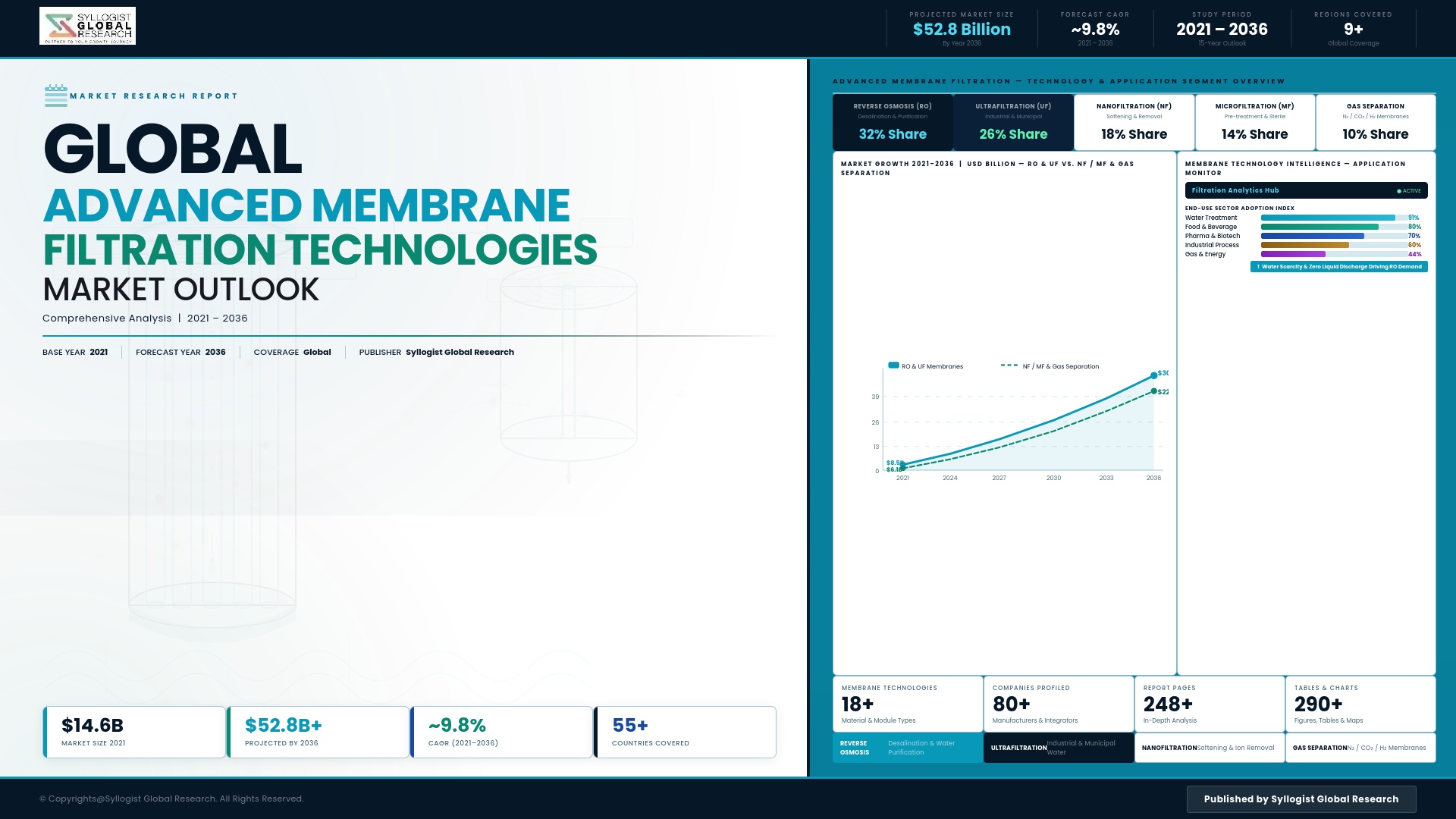

The global advanced membrane filtration technologies market is experiencing a sustained period of structural demand expansion, driven by the simultaneous intensification of freshwater scarcity pressures, tightening environmental discharge regulations, growing pharmaceutical and biopharmaceutical manufacturing complexity, and the accelerating adoption of membrane-based separation processes as energy-efficient alternatives to thermal and chemical purification technologies across a broadening range of industrial applications. The market was valued at approximately USD 31.8 billion in 2025 and is projected to grow at a compound annual growth rate of 8.9% through 2034, as membrane filtration transitions from a specialized water treatment technology into a cross-sectoral platform solution deployed across water reuse, pharmaceutical sterile filtration, food and beverage clarification, lithium battery electrolyte processing, green hydrogen production, and industrial effluent polishing applications.

Reverse osmosis membranes continue to represent the largest technology segment by revenue, anchored by their indispensable role in seawater and brackish water desalination, municipal water recycling, and ultrapure water production for semiconductor and pharmaceutical manufacturing, with ongoing innovation in thin-film composite membrane chemistry delivering progressive improvements in salt rejection efficiency, permeate flux rates, and fouling resistance that reduce the energy consumption and operational cost of large-scale desalination and water reuse plants. The membrane bioreactor segment is registering the most rapid growth rate within the broader market, driven by the superior effluent quality achievable through the integration of biological treatment with ultrafiltration membrane separation, which enables municipalities and industrial operators to meet increasingly stringent discharge standards and produce high-quality reclaimed water suitable for agricultural irrigation, industrial reuse, and indirect potable reuse applications at footprints substantially smaller than conventional activated sludge treatment infrastructure.

The pharmaceutical and biopharmaceutical manufacturing segment is emerging as a critical high-value growth driver for advanced membrane filtration, as the proliferation of monoclonal antibody therapies, mRNA vaccine production, cell and gene therapy manufacturing, and fermentation-derived biologics creates expanding demand for sterile filtration, virus removal filtration, ultrafiltration concentration and diafiltration, and tangential flow filtration systems capable of meeting stringent regulatory purity requirements at both clinical and commercial manufacturing scales. Single-use membrane filtration assemblies are gaining share within pharmaceutical applications, driven by the contamination control, changeover efficiency, and regulatory validation advantages they deliver relative to reusable systems in multi-product biomanufacturing environments. Lithium-ion battery electrolyte purification and the emerging application of membrane electrolysis in green hydrogen production are opening new high-growth industrial application vectors that are attracting dedicated product development investment from leading membrane technology manufacturers.

Asia-Pacific is the fastest-growing regional market for advanced membrane filtration technologies, driven by large-scale municipal water treatment and desalination investment in China, India, and the Middle East periphery, expanding pharmaceutical and food and beverage manufacturing capacity across Southeast Asia, and growing industrial wastewater management regulatory compliance investment across China and South Korea. North America maintains its position as the largest single regional market, supported by extensive municipal water infrastructure investment, the concentration of global biopharmaceutical manufacturing capacity, and strong research and development activity in next-generation membrane materials including graphene oxide, aquaporin-based biomimetic membranes, and mixed matrix membranes that are advancing performance boundaries beyond conventional polymeric membrane capabilities. Europe represents the third major regional market, driven by stringent water quality regulations, expanding wastewater reuse mandates, and pharmaceutical manufacturing concentration in Germany, Switzerland, Ireland, and the Nordic countries.

Key Drivers

Escalating Global Water Scarcity and Tightening Municipal and Industrial Wastewater Discharge Standards Driving Large-Scale Adoption of Reverse Osmosis, Nanofiltration, and Membrane Bioreactor Technologies

Intensifying freshwater scarcity across water-stressed regions in the Middle East, North Africa, South Asia, southern Europe, and western North America is compelling governments and utilities to invest at unprecedented scale in seawater desalination, municipal water recycling, and industrial water reuse infrastructure that is fundamentally dependent on advanced membrane filtration technology for cost-effective and energy-efficient operation. Simultaneously, progressively tightening discharge standards for nutrients, micropollutants, pharmaceutically active compounds, and emerging contaminants in treated wastewater effluent are establishing membrane filtration as the preferred treatment technology for municipalities and industrial operators requiring high-performance effluent polishing capabilities that conventional biological treatment processes alone cannot reliably achieve to meet evolving regulatory thresholds.

Rapid Expansion of Biopharmaceutical Manufacturing and Stringent Regulatory Purity Standards Generating Sustained High-Value Demand for Sterile and Virus Removal Membrane Filtration Systems

The global biopharmaceutical industry is experiencing an extended period of capacity expansion driven by the proliferation of monoclonal antibody therapies, the scaling of mRNA vaccine manufacturing infrastructure established during the pandemic response, and the commercial emergence of cell therapy, gene therapy, and advanced biologics manufacturing, each of which requires validated membrane filtration solutions including sterile filtration, virus removal filtration, and tangential flow ultrafiltration systems to achieve the purity, concentration, and sterility specifications mandated by regulatory agencies across major pharmaceutical markets. The high unit value, regulatory validation requirements, and critical quality attribute sensitivity of biopharmaceutical filtration applications generate premium pricing power and long-term supply relationship stability for qualified membrane filtration technology providers serving this segment.

Energy Efficiency Advantages and Decarbonization Imperatives Accelerating the Displacement of Thermal Separation and Chemical Treatment Processes by Membrane-Based Alternatives Across Industrial Applications

Advanced membrane filtration technologies deliver significant energy consumption advantages relative to thermal evaporation, distillation, and chemical precipitation separation processes across a range of industrial applications, positioning membrane-based separation as a preferred decarbonization pathway for energy-intensive industries facing carbon reduction obligations and rising energy costs. The adoption of membrane separation in food and beverage concentration and clarification, chemical and petrochemical product recovery, lithium brine concentration for battery materials production, and industrial gas purification is being accelerated by the combined pressure of corporate sustainability commitments, carbon pricing exposure, and process economics improvements driven by ongoing advances in membrane permeability, selectivity, and operational longevity that reduce the total cost of ownership of membrane-based separation relative to legacy thermal and chemical process alternatives.

Key Challenges

Membrane Fouling, Scaling, and Degradation Constraining Operational Performance, Increasing Maintenance Requirements, and Elevating Total Cost of Ownership Across High-Fouling Feed Water Applications

Membrane fouling caused by organic matter deposition, biological growth, mineral scaling, and colloidal particle accumulation remains the most pervasive operational challenge limiting the performance, energy efficiency, and service life of membrane filtration systems across water treatment, industrial processing, and food and beverage applications, necessitating chemical cleaning regimes, antiscalant dosing programs, and pre-treatment infrastructure that increase operational complexity, chemical consumption, and maintenance expenditure relative to theoretical membrane performance specifications. The development of chlorine-tolerant, low-fouling membrane surface chemistries and advanced antifouling coatings with demonstrated durability under real-world operating conditions at commercially viable production costs remains an ongoing materials science challenge that constrains achievable performance improvements in high-fouling application environments.

High Capital Investment Requirements and Complex Validation Processes for Pharmaceutical-Grade Membrane Filtration Systems Creating Barriers to Technology Adoption and Supplier Qualification

The deployment of membrane filtration systems in pharmaceutical and biopharmaceutical manufacturing environments requires extensive regulatory validation documentation, including installation qualification, operational qualification, and performance qualification protocols, virus removal validation studies, and extractables and leachables characterization testing, that impose substantial time and cost burdens on both membrane manufacturers seeking to qualify products for pharmaceutical use and biopharmaceutical operators implementing new filtration processes or substituting alternative membrane suppliers. These validation requirements create significant switching cost barriers that entrench incumbent qualified suppliers, limit competitive price pressure, and slow the adoption of next-generation membrane technologies offering performance improvements but requiring full revalidation before pharmaceutical manufacturing deployment.

Raw Material Price Volatility, Specialty Polymer Supply Chain Concentration, and Manufacturing Complexity Constraining Margin Stability and Capacity Expansion for Membrane Filtration Producers

Advanced membrane filtration products are manufactured from specialty polymeric and ceramic materials including polyamide, polyvinylidene fluoride, polyethersulfone, cellulose triacetate, and alumina, whose production is concentrated among a limited number of global specialty chemical and advanced materials suppliers, creating supply chain concentration risk and raw material cost volatility exposure that can materially compress membrane manufacturer margins during periods of petrochemical feedstock price escalation or specialty polymer supply disruption. The precision manufacturing processes required to achieve consistent membrane pore size distribution, defect-free selective layer formation, and module assembly integrity impose high capital equipment investment requirements and significant manufacturing yield management complexity that limit the speed at which membrane producers can expand capacity to meet accelerating demand across high-growth application segments.

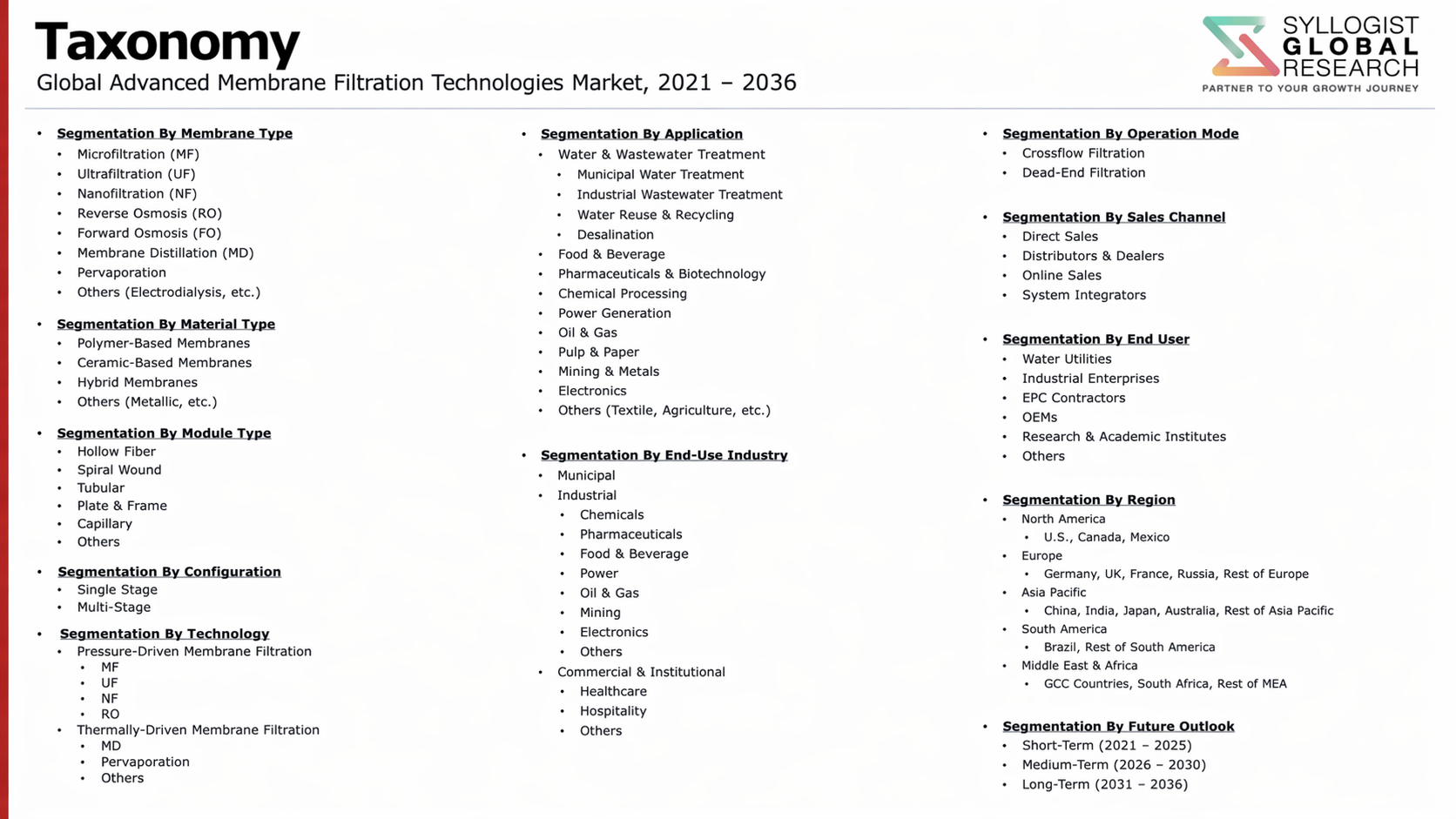

Market Segmentation

- Segmentation By Membrane Type

- Microfiltration Membranes

- Ultrafiltration Membranes

- Nanofiltration Membranes

- Reverse Osmosis Membranes

- Forward Osmosis Membranes

- Membrane Bioreactor Systems

- Gas Separation Membranes

- Others

- Segmentation By Material

- Polymeric Membranes (Polyamide, PVDF, PES, CA)

- Ceramic and Inorganic Membranes

- Mixed Matrix and Composite Membranes

- Biomimetic and Aquaporin-Based Membranes

- Graphene Oxide and Nanostructured Membranes

- Others

- Segmentation By Module Configuration

- Spiral Wound Modules

- Hollow Fiber Modules

- Flat Sheet and Plate-and-Frame Modules

- Tubular Modules

- Pleated Cartridge Modules

- Others

- Segmentation By Application

- Seawater and Brackish Water Desalination

- Municipal Wastewater Treatment and Reuse

- Ultrapure Water Production

- Industrial Process Water and Effluent Treatment

- Pharmaceutical and Biopharmaceutical Sterile Filtration

- Food and Beverage Clarification and Concentration

- Gas Separation and Hydrogen Purification

- Others

- Segmentation By End Use Industry

- Municipal Water and Wastewater Utilities

- Pharmaceutical and Biopharmaceutical Manufacturing

- Food and Beverage Processing

- Chemical and Petrochemical Processing

- Power Generation and Energy

- Semiconductor and Electronics Manufacturing

- Mining and Metals Processing

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global advanced membrane filtration technologies market valuation in 2025, projected through 2034, segmented by membrane type, material, and end use industry, enabling membrane manufacturers, investors, and procurement specialists to identify the highest-growth technology categories and most durable demand opportunities across the global membrane filtration landscape?

- How are escalating water scarcity conditions, tightening municipal wastewater discharge regulations, and expanding industrial water reuse mandates across Asia-Pacific, the Middle East, and Europe shaping investment priorities in reverse osmosis, nanofiltration, and membrane bioreactor technologies, and which regional markets are expected to generate the largest incremental infrastructure procurement volumes through 2034?

- Which membrane technology segments, specifically membrane bioreactors, virus removal filtration for biopharmaceutical manufacturing, tangential flow ultrafiltration, and gas separation membranes for hydrogen purification, are registering the highest growth rates through 2034, and what application-specific performance requirements and regulatory standards are shaping membrane material selection and module design innovation in each segment?

- How is the competitive landscape structured among global membrane filtration technology manufacturers, module assemblers, and system integrators, and what research and development investment strategies, material science innovation programs, application-specific product portfolio development, and geographic market expansion initiatives are enabling leading competitors to differentiate and capture share across high-value end use segments?

- What membrane fouling mitigation strategies, antifouling coating technologies, advanced pre-treatment process designs, and cleaning protocol innovations are proving most effective at reducing operational cost burdens and extending membrane service life across high-fouling municipal, industrial, and food processing applications, and how are these advances affecting total cost of ownership calculations and technology adoption decisions?

- How are pharmaceutical and biopharmaceutical regulatory validation requirements, extractables and leachables testing obligations, and virus removal validation protocols shaping membrane supplier qualification processes, single-use system adoption trends, and the pace at which next-generation high-performance membrane materials are achieving commercial deployment in sterile and biopharmaceutical filtration manufacturing environments?

- What emerging application opportunities in lithium brine concentration for battery materials production, green hydrogen membrane electrolysis, carbon capture gas separation, and precision fermentation downstream processing are expected to generate material new demand for advanced membrane filtration technologies through 2034, and which membrane material platforms and module configurations are best positioned to address these emerging industrial application requirements?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Membrane Fouling, Scaling & Performance Degradation Risk

- Raw Material Availability, Polymer & Specialty Chemical Supply Chain Risk

- Regulatory Tightening, Discharge Standards Divergence & Cross-Border Compliance Risk

- Technology Substitution, Competing Separation Technologies & Disruptive Innovation Risk

- High Capital Cost, Project Finance Availability & End-User Budget Constraint Risk

- Regulatory Framework & Standards

- Drinking Water Treatment Standards, Membrane Performance Requirements & NSF/ANSI & WHO Certification Frameworks

- Wastewater Reuse, Effluent Discharge & Membrane Bioreactor (MBR) Regulatory Standards by Jurisdiction

- Industrial Effluent Treatment, Zero Liquid Discharge (ZLD) Mandates & Membrane System Compliance Requirements

- Desalination Plant Permitting, Environmental Impact & Brine Disposal Regulatory Frameworks

- Food & Beverage, Pharmaceutical & Life Sciences Membrane Filtration Standards (FDA, EC, GMP & EHEDG)

- Green Procurement, ESG Disclosure & Sustainable Membrane Technology Procurement Standards

- Global Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (m2 of Membrane Area Installed & Units Shipped)

- Market Size & Forecast by Membrane Type

- Microfiltration (MF) Membranes

- Ultrafiltration (UF) Membranes

- Nanofiltration (NF) Membranes

- Reverse Osmosis (RO) Membranes

- Forward Osmosis (FO) Membranes

- Membrane Distillation (MD) Membranes

- Electrodialysis (ED) & Electrodialysis Reversal (EDR) Membranes

- Gas Separation Membranes

- Pervaporation Membranes

- Ion Exchange Membranes

- Market Size & Forecast by Material

- Polymeric Membranes (Polyethersulfone, Polyvinylidene Fluoride, Polyamide & Polypropylene)

- Ceramic & Inorganic Membranes (Alumina, Titania, Zirconia & Silicon Carbide)

- Thin-Film Composite (TFC) Membranes

- Mixed Matrix & Nanocomposite Membranes (Zeolite, Graphene Oxide & MOF-Incorporated)

- Biomimetic & Aquaporin-Based Membranes

- Hollow Fibre & Flat Sheet Membrane Formats

- Market Size & Forecast by Module Configuration

- Spiral-Wound Membrane Modules

- Hollow Fibre Membrane Modules

- Tubular Membrane Modules

- Flat Sheet & Plate-and-Frame Membrane Modules

- Submerged & Immersed Membrane Modules

- Market Size & Forecast by System & Process Technology

- Membrane Bioreactor (MBR) Systems

- Seawater Reverse Osmosis (SWRO) Desalination Systems

- Brackish Water Reverse Osmosis (BWRO) Systems

- Ultrafiltration & Microfiltration Pretreatment & Tertiary Treatment Systems

- Nanofiltration Softening & Selective Ion Removal Systems

- Zero Liquid Discharge (ZLD) & Minimal Liquid Discharge (MLD) Membrane Systems

- Membrane Distillation & Forward Osmosis Hybrid Systems

- Electrodeionisation (EDI) & Continuous Electrodeionisation (CEDI) Systems

- Market Size & Forecast by Application

- Municipal Drinking Water Treatment & Purification

- Municipal Wastewater Treatment & Water Reuse

- Seawater & Brackish Water Desalination

- Industrial Wastewater Treatment & Zero Liquid Discharge

- Food & Beverage Processing (Dairy, Juice, Wine, Beer & Edible Oil)

- Pharmaceutical, Biotech & Life Sciences (Sterile Filtration, Ultrapure Water & Biopharmaceutical Processing)

- Power Generation & Energy Sector Water Treatment

- Oil & Gas, Produced Water Treatment & Refinery Effluent

- Semiconductor & Electronics Ultrapure Water Production

- Mining & Metals Process Water & Effluent Treatment

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utilities

- Industrial & Manufacturing Facilities

- Food & Beverage Producers

- Pharmaceutical & Life Sciences Companies

- Oil & Gas & Petrochemical Operators

- Power Generation & Energy Utilities

- Semiconductor & Electronics Manufacturers

- Mining & Metals Companies

- Market Size & Forecast by Sales Channel

- Direct OEM & Membrane Manufacturer Sales

- System Integrator, EPC Contractor & Engineering Firm Channel

- Distributor & Value-Added Reseller (VAR) Network

- Equipment Rental, Leasing & Water-as-a-Service (WaaS) Channel

- Online & Digital Procurement Platforms

- North America Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Advanced Membrane Filtration Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (m2 of Membrane Area Installed & Units Shipped)

- By Membrane Type

- By Material

- By Module Configuration

- By System & Process Technology

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Thin-Film Composite (TFC) & Thin-Film Nanocomposite (TFN) Reverse Osmosis Membrane Technology Deep-Dive

- Ceramic & Inorganic Membrane Technology: High-Temperature, Harsh-Chemical & Industrial Process Applications

- Membrane Bioreactor (MBR) Technology: Submerged vs. External Configurations, Fouling Control & Operational Advances

- Graphene Oxide, Carbon Nanotube & Next-Generation Nanomaterial-Enhanced Membrane Technology

- Biomimetic, Aquaporin & Bioinspired Membrane Technology for Ultra-Low Energy Desalination & Separation

- Forward Osmosis & Membrane Distillation Technology for Brine Concentration & Zero Liquid Discharge

- AI-Driven Fouling Prediction, Digital Twin & Smart Membrane System Optimisation Technology

- Patent & IP Landscape in Advanced Membrane Filtration Technologies

- Value Chain & Supply Chain Analysis

- Polymer, Monomer & Specialty Chemical Raw Material Supply Chain

- Ceramic Precursor, Inorganic Oxide & Advanced Material Supply Chain

- Membrane Casting, Phase Inversion & Manufacturing Process Supply Chain

- Membrane Module Assembly, Spiral-Wound & Hollow Fibre Production Supply Chain

- Pressure Vessel, Housing, Pump & Auxiliary Equipment Supply Chain

- System Integrator, EPC Contractor & Project Developer Channel

- Aftermarket Membrane Replacement, Cleaning Chemical & Service Supply Chain

- End-of-Life Membrane Recycling, Valorisation & Circular Economy

- Pricing Analysis

- Membrane Element & Module Price Analysis by Membrane Type & Material

- Integrated Membrane System Capital Cost & Total Cost of Ownership (TCO) Analysis

- Levelised Cost of Water (LCOW) Analysis: RO Desalination, MBR & Ultrafiltration Systems

- Ceramic vs. Polymeric Membrane Capex & Opex Cost Comparison

- Membrane Replacement Frequency, Cleaning Cost & Operational Expenditure Structure

- Water-as-a-Service (WaaS) & Build-Operate-Transfer (BOT) Pricing Model Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Membrane Filtration Systems: Carbon Footprint, Energy Intensity & Water Recovery Efficiency

- Energy Consumption, Pressure Recovery Devices & Decarbonisation Pathway for Membrane Desalination & Filtration

- Brine Concentrate Management, Disposal & Valorisation: Environmental Impact & Emerging Zero Discharge Solutions

- Sustainable Membrane Manufacturing: Bio-Based Polymers, Green Solvents & Reduced Hazardous Chemical Use

- SDG 6 (Clean Water & Sanitation) Contribution, ESG Alignment & Green Finance Eligibility for Membrane Projects

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Membrane Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Membrane Type, Application & Geography

- Player Classification

- Large Diversified Water Technology & Membrane System Companies

- Specialist RO & NF Membrane Element Manufacturers

- Specialist MF & UF Membrane Manufacturers

- Ceramic & Inorganic Membrane Specialists

- MBR System & Technology Providers

- Next-Generation & Novel Membrane Material Companies

- Desalination Project Developers, EPC Contractors & BOT Operators

- Competitive Analysis Frameworks

- Market Share Analysis by Membrane Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Membrane Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Membrane Filtration Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Membrane Type, Material, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output