Global Wastewater-to-Energy Technologies Market By Technology Type, By Energy Output, By Feedstock Type, By Scale of Operation, By End Use Application, By End User, By Region, Competition, Forecast & Opportunities, 2021-2036F

Market Definition

The Global Wastewater-to-Energy Technologies Market encompasses the design, manufacture, deployment, and operation of systems that recover thermal energy, biogas, biohydrogen, electricity, and value-added biochemicals from municipal sewage sludge, industrial effluents, agricultural wastewater, and food processing waste streams through anaerobic digestion, thermal hydrolysis, microbial fuel cells, hydrothermal liquefaction, pyrolysis, and co-generation technologies, serving municipal utilities, industrial facilities, agri-food processors, and energy developers seeking to simultaneously address wastewater treatment obligations and renewable energy generation objectives.

Market Insights

The global wastewater-to-energy technologies market is advancing through a decisive phase of commercial maturation, propelled by the convergence of decarbonization policy mandates, rising energy costs, circular economy adoption imperatives, and the growing recognition among municipal utilities and industrial operators that wastewater treatment infrastructure represents an underutilized energy and resource recovery asset of substantial strategic value. The market was valued at approximately USD 8.6 billion in 2025 and is projected to expand at a compound annual growth rate of 10.4% through 2034, as governments, utilities, and industrial enterprises accelerate investment in technologies that transform the energy liability of wastewater treatment into a net energy generating, carbon-reducing operational asset capable of delivering measurable contributions to facility-level and national renewable energy targets.

Anaerobic digestion combined with combined heat and power co-generation remains the most commercially established and widely deployed wastewater-to-energy pathway, generating biogas from the organic content of sewage sludge and high-strength industrial effluents that is combusted in co-generation engines or upgraded to biomethane for grid injection or vehicle fuel applications. The integration of thermal hydrolysis pre-treatment with anaerobic digestion is significantly elevating biogas yields from sewage sludge, improving digester throughput efficiency, and reducing sludge disposal volumes, making thermal hydrolysis a rapidly adopted process enhancement at large urban wastewater treatment plants seeking to maximize energy recovery from existing digestion assets. Advanced anaerobic digestion systems processing food waste, agri-industrial effluents, and co-digestion feedstock blends alongside sewage sludge are achieving substantially higher specific biogas yields than single-feedstock sludge digestion, reinforcing the economic case for co-digestion facility investment at municipal and regional scale across Europe, North America, and Australia.

Biomethane production through biogas upgrading is emerging as a high-priority investment category within the wastewater-to-energy sector, driven by natural gas price volatility following geopolitical supply disruptions, rapidly expanding biomethane feed-in tariff frameworks in the European Union, and growing corporate demand for certified renewable gas as a decarbonization instrument in hard-to-electrify industrial and transport applications. Wastewater treatment facilities with established anaerobic digestion infrastructure are investing in pressure swing adsorption, membrane separation, and amine scrubbing biogas upgrading systems to convert existing biogas production into pipeline-quality biomethane, accessing substantially higher revenue streams than combined heat and power generation alone while contributing directly to national renewable gas production targets. Microbial electrochemical technologies including microbial fuel cells and microbial electrolysis cells are progressing from laboratory demonstration toward pilot and early commercial deployment in industrial wastewater applications, with ongoing advances in electrode materials, reactor configuration, and microbial community optimization improving power densities and cost competitiveness relative to established biogas-based energy recovery pathways.

Europe dominates the global wastewater-to-energy market in terms of technology maturity, installed capacity, and regulatory framework sophistication, underpinned by the European Union’s renewable energy directives, biomethane production targets embedded in the REPowerEU plan, and well-established gate fee and feed-in tariff support mechanisms that underpin project economics across member states. North America represents the second largest regional market, driven by biogas co-generation investment at large municipal wastewater treatment plants, growing food waste co-digestion programs, and expanding renewable natural gas project pipelines supported by favorable tax incentives and low-carbon fuel standard credit frameworks. Asia-Pacific is projected to record the highest regional growth rate through 2034, anchored by large-scale wastewater infrastructure investment in China and India, where government-mandated improvements in wastewater treatment coverage and growing renewable energy ambitions are converging to create substantial new project development opportunities for wastewater-to-energy technology providers and project developers.

Key Drivers

Renewable Energy Mandates and Carbon Reduction Obligations Repositioning Wastewater Treatment Facilities as Strategic Renewable Energy and Biomethane Production Assets Across Major Economies

National and regional renewable energy targets, carbon neutrality commitments, and rising carbon pricing obligations are compelling municipal water utilities, industrial operators, and governments to reframe wastewater treatment infrastructure as a renewable energy generation platform rather than a purely environmental compliance expenditure, creating sustained policy-driven investment demand for anaerobic digestion, biogas upgrading, and thermal energy recovery technologies that convert wastewater organic content into biogas, biomethane, and recovered heat contributing to facility decarbonization and national renewable energy portfolios. Regulatory frameworks in the European Union, United Kingdom, and increasingly across North America and Asia-Pacific are providing financial incentives including feed-in premiums, renewable gas certificates, and low-carbon fuel standard credits that directly improve project economics and accelerate wastewater-to-energy investment decisions.

Rising Energy Costs and Operational Expenditure Pressures at Wastewater Treatment Facilities Driving Adoption of Energy Recovery Technologies to Reduce Net Energy Consumption and Utility Bills

Wastewater treatment is among the most energy-intensive municipal service operations, with aeration, pumping, sludge processing, and facility heating representing substantial and growing electricity and thermal energy expenditure for municipal utilities and industrial operators managing large treatment plants under tight operating budget constraints. The combination of sustained energy price increases, grid electricity cost volatility driven by energy market disruptions, and carbon pricing escalation is strengthening the financial case for wastewater-to-energy investment by reducing payback periods on anaerobic digestion and combined heat and power infrastructure, enabling treatment plants to offset a significant proportion of purchased energy with self-generated biogas-derived electricity and heat, and in advanced configurations achieving net energy positive treatment plant operation.

Circular Economy Policy Frameworks and Sludge Disposal Regulation Tightening Creating Integrated Resource Recovery Imperatives That Reinforce Wastewater-to-Energy Investment Rationale

The progressive tightening of sewage sludge land application regulations, landfill disposal restrictions, and agricultural use permitting requirements across the European Union, United States, and emerging economies is eliminating low-cost sludge disposal pathways and compelling wastewater treatment operators to invest in thermal and biochemical processing technologies that simultaneously achieve volume reduction, pathogen elimination, energy recovery, and nutrient concentration in forms suitable for circular economy reuse as fertilizer, biochar, or struvite-based phosphorus recovery products. Wastewater-to-energy technologies that deliver integrated energy recovery alongside sludge stabilization and resource extraction are increasingly evaluated on a combined value basis that encompasses energy revenue, disposal cost avoidance, and recovered nutrient commodity value, substantially improving overall project financial viability.

Key Challenges

High Capital Investment Requirements and Long Project Payback Periods Constraining Wastewater-to-Energy Adoption Among Smaller Municipalities and Capacity-Constrained Utilities in Developing Markets

The installation of anaerobic digestion systems, thermal hydrolysis pre-treatment, biogas upgrading infrastructure, and combined heat and power co-generation equipment represents capital expenditure that is financially accessible primarily to large municipal wastewater treatment facilities with sufficient organic loading to justify investment, while smaller treatment plants, utilities in developing economies with constrained public financing capacity, and industrial operators with intermittent or low-volume wastewater generation face unfavorable project economics that limit wastewater-to-energy adoption well below the addressable technical potential. Development finance institution support, blended finance instruments, and public-private partnership project structures are emerging to bridge this financing gap, but deployment at scale in capacity-constrained markets remains substantially below the level required to realize the sector’s full resource recovery potential.

Feedstock Variability, Contamination, and Seasonal Fluctuation in Wastewater Organic Content Reducing Biogas Yield Predictability and Complicating Energy Production Planning

The organic content, chemical composition, and hydraulic loading of wastewater feedstocks feeding anaerobic digestion and other energy recovery processes are subject to significant temporal variability driven by seasonal population dynamics, industrial discharge fluctuations, stormwater infiltration events, and changes in upstream waste generation patterns, creating biogas yield unpredictability that complicates facility energy balance planning, grid export contract management, and biomethane production volume commitments. Contamination of feedstock streams with heavy metals, persistent organic pollutants, microplastics, and pharmaceutical compounds can inhibit microbial digestion performance, compromise digestate quality for agricultural use, and impose additional pre-treatment costs that erode the energy and economic recovery efficiency achievable from available organic waste inputs.

Technology Integration Complexity and Operations and Maintenance Skill Requirements Limiting Reliable Long-Term Performance of Advanced Wastewater-to-Energy Systems Across Diverse Operating Environments

Wastewater-to-energy systems integrating anaerobic digestion with thermal hydrolysis, biogas upgrading, combined heat and power co-generation, and nutrient recovery processes involve significant mechanical, biochemical, and process control complexity that demands specialized operations and maintenance expertise, continuous process monitoring, and disciplined feedstock and co-product management to sustain design performance over extended operational lifetimes. In many municipal and developing country operating environments, workforce capability gaps in advanced biogas system operation, limited local availability of specialized maintenance services and spare parts, and inadequate process instrumentation and automation investment result in chronic underperformance of installed wastewater-to-energy assets relative to design specifications, reducing energy recovery rates, shortening equipment service lives, and undermining the financial returns that justified original capital investment.

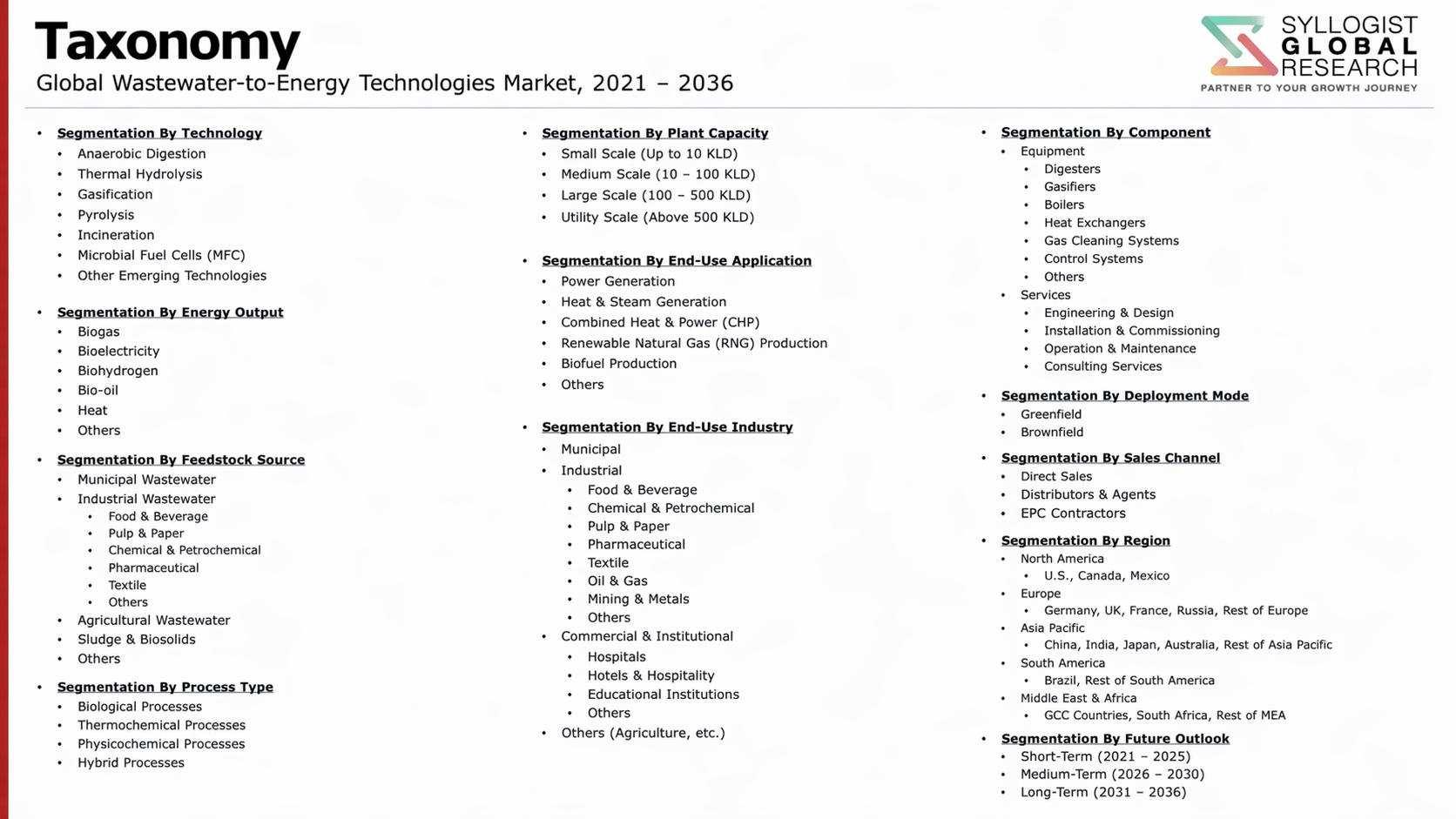

Market Segmentation

- Segmentation By Technology Type

- Anaerobic Digestion and Biogas Generation Systems

- Thermal Hydrolysis Pre-Treatment Systems

- Biogas Upgrading and Biomethane Production Systems

- Combined Heat and Power Co-Generation Systems

- Hydrothermal Liquefaction and Carbonization

- Microbial Fuel Cells and Microbial Electrolysis Cells

- Pyrolysis and Gasification of Dried Sludge

- Others

- Segmentation By Energy Output

- Biogas and Raw Biomethane

- Pipeline-Quality Biomethane and Renewable Natural Gas

- Electricity and Thermal Heat (Co-Generation)

- Biohydrogen

- Biochar and Syngas

- Others

- Segmentation By Feedstock Type

- Municipal Sewage Sludge

- Industrial and Food Processing Wastewater

- Agricultural and Livestock Effluents

- Food Waste and Organic Co-Digestion Substrates

- Mixed Urban and Industrial Co-Digestion Blends

- Others

- Segmentation By Scale of Operation

- Large-Scale Municipal Treatment Plants (above 100,000 PE)

- Medium-Scale Municipal and Industrial Facilities

- Small and Decentralized Systems

- Modular and Containerized Units

- Segmentation By End Use Application

- On-Site Energy Self-Sufficiency and Grid Export

- Biomethane Grid Injection and Vehicle Fuel

- Sludge Stabilization and Volume Reduction

- Nutrient and Phosphorus Recovery

- Industrial Steam and Process Heat Supply

- Others

- Segmentation By End User

- Municipal Water and Wastewater Utilities

- Food and Beverage Processing Facilities

- Pulp, Paper, and Chemical Industries

- Agricultural and Agri-Industrial Operators

- Independent Power and Renewable Gas Producers

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global wastewater-to-energy technologies market valuation in 2025, projected through 2034, segmented by technology type, energy output, and end user, enabling technology developers, utility operators, and infrastructure investors to identify the highest-growth solution categories and most durable project investment opportunities across the wastewater energy recovery landscape?

- How are renewable energy mandates, biomethane feed-in tariff frameworks, carbon pricing mechanisms, and sludge disposal regulations evolving across the European Union, North America, and Asia-Pacific, and how are these overlapping policy drivers reshaping investment case structures, technology selection decisions, and project financing strategies for wastewater-to-energy facility development across different regulatory jurisdictions?

- Which technology pathways, specifically thermal hydrolysis integrated anaerobic digestion, biogas upgrading to biomethane, microbial electrochemical systems, and hydrothermal liquefaction, are demonstrating the strongest commercial adoption momentum through 2034, and what feedstock characteristics, scale requirements, and energy market conditions determine technology selection and financial performance in each pathway?

- How is the competitive landscape structured among wastewater-to-energy technology providers, engineering procurement and construction contractors, and project development companies, and what technology licensing, equipment supply, service contract, and project finance structuring strategies are enabling leading players to build durable market positions across the municipal and industrial wastewater energy recovery segments?

- What capital cost barriers, feedstock variability challenges, operations and maintenance skill constraints, and project financing limitations are most significantly restraining wastewater-to-energy adoption among smaller municipalities, developing country utilities, and capacity-constrained industrial operators, and what technology design innovations and financing mechanisms are emerging to address these adoption barriers?

- Which regional markets, specifically Asia-Pacific, Latin America, and the Middle East and Africa, are expected to generate the highest incremental wastewater-to-energy project development activity through 2034, and what combinations of wastewater infrastructure expansion investment, renewable energy policy support, and municipal utility commercialization are driving technology procurement and project development in each region?

- How is the growing commercial interest in biomethane grid injection, renewable natural gas certification, and wastewater-derived nutrient recovery products reshaping the revenue model and investment economics of wastewater-to-energy projects, and what market development, offtake contracting, and certification framework advances are enabling utilities and project developers to capture value from multiple co-product revenue streams simultaneously?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Feedstock Variability, Wastewater Composition Fluctuation & Process Stability Risk

- Regulatory Uncertainty, Biogas Offtake Policy & Renewable Energy Incentive Withdrawal Risk

- Technology Performance, Digester Failure & Operational Reliability Risk

- Financing, Project Bankability & Long-Term Revenue Certainty Risk

- Public Acceptance, Odour, Emissions & Social Licence to Operate Risk

- Regulatory Framework & Standards

- Wastewater Treatment Standards, Discharge Limits & Energy Self-Sufficiency Mandates for Water Resource Recovery Facilities

- Biogas, Biomethane & Renewable Natural Gas (RNG) Quality Standards, Grid Injection & Offtake Regulatory Frameworks

- Biosolids, Digestate & Nutrient Recovery Regulations: Land Application, Beneficial Use & Export Standards

- Renewable Energy Mandates, Feed-in Tariffs, Power Purchase Agreement Frameworks & Green Certificate Schemes

- Air Emission Standards, Hydrogen Sulphide Control & Flaring Regulations for Wastewater Biogas Facilities

- Green Finance, Climate Fund Eligibility, ESG Disclosure & Sustainable Infrastructure Procurement Standards

- Global Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- Market Size & Forecast by Technology

- Anaerobic Digestion (AD) & Biogas Production at Water Resource Recovery Facilities (WRRFs)

- Combined Heat & Power (CHP) & Cogeneration from Wastewater Biogas

- Biomethane Upgrading & Renewable Natural Gas (RNG) Production from Wastewater Biogas

- Thermal Hydrolysis Process (THP) & Advanced Digestion Pre-Treatment Technology

- Sludge Thermal Treatment: Incineration, Pyrolysis & Gasification for Energy Recovery

- Microbial Fuel Cells (MFC) & Microbial Electrolysis Cells (MEC) for Bioelectrochemical Energy Recovery

- Hydrothermal Liquefaction (HTL) & Hydrothermal Carbonisation (HTC) of Wastewater Sludge

- Struvite & Nutrient Recovery Integrated with Energy Recovery Systems

- Wastewater-Sourced Green Hydrogen Production via Electrolysis & Biogas Reforming

- Heat Pump & Thermal Energy Recovery from Wastewater Effluent

- Sewer Mining & In-Sewer Thermal Energy Recovery Systems

- Market Size & Forecast by Energy Output Type

- Electrical Power Generation (Grid Export & Captive Self-Consumption)

- Thermal Energy Recovery (Heat for Process Use & District Heating)

- Biomethane & Renewable Natural Gas (RNG) Production

- Green Hydrogen Production

- Biochar, Syngas & Liquid Fuel Production from Sludge Thermal Treatment

- Market Size & Forecast by Feedstock Type

- Municipal Wastewater Sludge & Biosolids

- Industrial Wastewater & High-Strength Organic Effluent

- Food & Beverage Processing Wastewater & Organic Waste Co-Digestion Feedstock

- Agricultural Slurry, Manure & Agro-Industrial Wastewater Co-Digestion Feedstock

- Fats, Oils & Grease (FOG) & Food Waste Co-Digestion Feedstock

- Market Size & Forecast by System Component

- Anaerobic Digester Tanks, Covers & Mixing Systems

- Biogas Collection, Cleaning, Desulphurisation & Conditioning Equipment

- CHP Engines, Gas Turbines & Microturbines for Biogas Utilisation

- Biomethane Upgrading Units (Water Scrubbing, PSA, Membrane & Chemical Scrubbing)

- Thermal Hydrolysis Reactors & Sludge Pre-Treatment Equipment

- Sludge Dewatering, Thickening & Centrifuge Equipment

- Sludge Incineration, Pyrolysis & Gasification Reactors

- Heat Exchangers, Heat Recovery Systems & District Heating Interface Equipment

- SCADA, Digital Control & Energy Management Systems for WtE Facilities

- Market Size & Forecast by Project Scale

- Large-Scale Regional & Metropolitan WRRF-Based WtE Projects (Above 100,000 PE or 5 MW)

- Medium-Scale Municipal WtE Projects (20,000 to 100,000 PE or 500 kW to 5 MW)

- Small-Scale & Decentralised WtE Projects (Below 20,000 PE or 500 kW)

- Industrial & On-Site Wastewater-to-Energy Projects

- Market Size & Forecast by Application

- Municipal Water Resource Recovery Facilities (WRRFs) & Wastewater Treatment Plants

- Industrial Wastewater Treatment & On-Site Energy Recovery

- Food & Beverage & Agro-Industrial Wastewater Treatment with Energy Recovery

- Decentralised & Off-Grid Community Wastewater-to-Energy Systems

- Smart City & Urban Circular Economy Water-Energy Co-Infrastructure

- Market Size & Forecast by End-User

- Municipal Water & Wastewater Utility Operators

- Independent Power Producers (IPPs) & Renewable Energy Project Developers

- Industrial & Manufacturing Facility Operators

- Food & Beverage & Agro-Industrial Companies

- Government Agencies & National Infrastructure Authorities

- Market Size & Forecast by Sales Channel

- EPC & Turnkey Project Contract (Engineering, Procurement & Construction)

- Public-Private Partnership (PPP), BOT & Concession Contract

- Direct Equipment & Technology Supply with System Integration

- Operations & Maintenance (O&M) Service & Performance Contract

- North America Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Wastewater-to-Energy Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Installed Capacity, MW and Million m3/day Wastewater Treated)

- By Technology

- By Energy Output Type

- By Feedstock Type

- By System Component

- By Project Scale

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- *Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Mexico, Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, China, Japan, India, Australia, South Korea, Singapore, Brazil, Chile, Saudi Arabia, UAE, Egypt, South Africa, Israel

- Technology Landscape & Innovation Analysis

- Anaerobic Digestion Technology Deep-Dive: Mesophilic vs. Thermophilic, Single-Stage vs. Multi-Stage & High-Rate AD Systems

- Thermal Hydrolysis Process (THP) & Advanced Pre-Treatment Technology for Enhanced Biogas Yield

- Biomethane Upgrading Technology: Water Scrubbing, PSA, Membrane Separation & Amine Scrubbing Comparison

- Sludge Thermal Treatment Technology: Moving Grate Incineration, Fluidised Bed, Pyrolysis & Gasification

- Microbial Fuel Cell (MFC), Microbial Electrolysis Cell (MEC) & Bioelectrochemical System Technology

- Hydrothermal Liquefaction (HTL) & Hydrothermal Carbonisation (HTC): Emerging Sludge Valorisation Technology

- Wastewater-Sourced Green Hydrogen: Biogas Steam Methane Reforming (SMR), Electrolysis & Dark Fermentation

- Digital Twin, AI Process Optimisation & Smart Energy Management for Wastewater-to-Energy Facilities

- Patent & IP Landscape in Wastewater-to-Energy Technologies

- Value Chain & Supply Chain Analysis

- Anaerobic Digestion, CHP & Biogas Upgrading Equipment Manufacturing Supply Chain

- Sludge Thermal Treatment Reactor, Boiler & Emissions Control Equipment Supply Chain

- Heat Exchanger, Heat Recovery & District Heating Interface Equipment Supply Chain

- Gas Engine, Microturbine, Fuel Cell & Power Generation Equipment Supply Chain

- Instrumentation, SCADA, Control Systems & Digital Platform Supply Chain

- EPC Contractor, Project Developer & System Integrator Procurement Landscape

- Utility Operator, Government Authority & Offtake Partner Channel

- Digestate, Biochar & Nutrient Recovery Valorisation & Circular Economy Channel

- Pricing Analysis

- Anaerobic Digestion & Biogas CHP Plant Capital Cost & Operating Cost Analysis

- Biomethane Upgrading Unit Capex & Levelised Cost of Biomethane (LCOBM) Analysis

- Thermal Hydrolysis Pre-Treatment System Capital Cost & Payback Period Analysis

- Sludge Incineration, Pyrolysis & Gasification Plant Capital & Operating Cost Analysis

- Total WtE Project Economics: Levelised Cost of Energy (LCOE) & Revenue Stack Analysis

- PPP Tariff, BOT Concession Pricing & Water-Energy Nexus Project Finance Structure Analysis

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Wastewater-to-Energy Technologies: Carbon Footprint, Energy Balance & Net GHG Abatement

- Carbon Neutrality & Net Zero Pathway: Role of WtE in Achieving Energy-Neutral & Energy-Positive Water Utilities

- Digestate & Biochar Soil Amendment: Nutrient Cycling, Carbon Sequestration & Circular Economy Contribution

- Air Quality, Odour & Emission Management: NOx, SOx, H2S & Fugitive Methane Control at WtE Facilities

- SDG 6 (Clean Water), SDG 7 (Affordable Energy) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology, Application & Geography

- Player Classification

- Integrated Water Technology & Wastewater-to-Energy System Companies

- Specialist Anaerobic Digestion, Biogas & CHP Technology Providers

- Biomethane Upgrading & Renewable Gas Technology Specialists

- Sludge Thermal Treatment & Waste-to-Energy Technology Providers

- Emerging Technology Developers (MFC, HTL, Green Hydrogen & Bioelectrochemical Systems)

- EPC Contractors & Project Developers Specialising in Wastewater-to-Energy

- Digital, SCADA & Smart Energy Management Platform Providers for WtE Facilities

- Competitive Analysis Frameworks

- Market Share Analysis by Technology, Application & Region

- Company Profile

- Company Overview & Headquarters

- Wastewater-to-Energy Products & Technology Portfolio

- Key Customer Relationships & Reference Project Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Wastewater-to-Energy Segment) & Order Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology, Energy Output Type, Application, End-User & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output