Market Definition

The Global Petrochemical Industry Decarbonization Technologies Market encompasses the development, commercialization, deployment, and operational servicing of technological systems and process solutions designed to reduce or eliminate greenhouse gas emissions and carbon intensity across the full spectrum of petrochemical manufacturing operations, including steam cracker complexes, aromatics extraction and purification units, polymer production facilities, olefin derivatives plants, methanol and ammonia synthesis operations, and refinery-integrated petrochemical assets that collectively represent one of the most energy-intensive and carbon-emitting segments of the global industrial economy. Decarbonization technologies within this market context include carbon capture, utilization, and storage systems applied to process heaters and crackers; green and blue hydrogen production and integration technologies that substitute fossil fuel combustion heat with electrolytic or steam methane reforming with carbon capture derived hydrogen; electrification of process heating through electric steam crackers and resistance-heated reactor systems; advanced heat integration and energy recovery technologies; biomass and bio-based feedstock substitution programs; circular economy-enabling mechanical and chemical plastic recycling technologies that reduce virgin hydrocarbon feedstock demand; and industrial carbon accounting, monitoring, verification, and reporting software platforms that support regulatory compliance and corporate decarbonization commitment disclosure. The market encompasses the complete value chain from technology licensing and engineering design through equipment manufacturing, system integration, project construction, and long-term operational services, with participants including integrated oil and gas majors, specialty chemical companies, dedicated clean technology developers, engineering procurement and construction firms, industrial gas companies, carbon capture technology licensors, electrolyzer manufacturers, equipment suppliers, and government agencies whose grant funding, concessional loan programs, and regulatory mandates create the financial and policy architecture within which commercial deployment decisions are made by petrochemical operators globally.

Market Insights

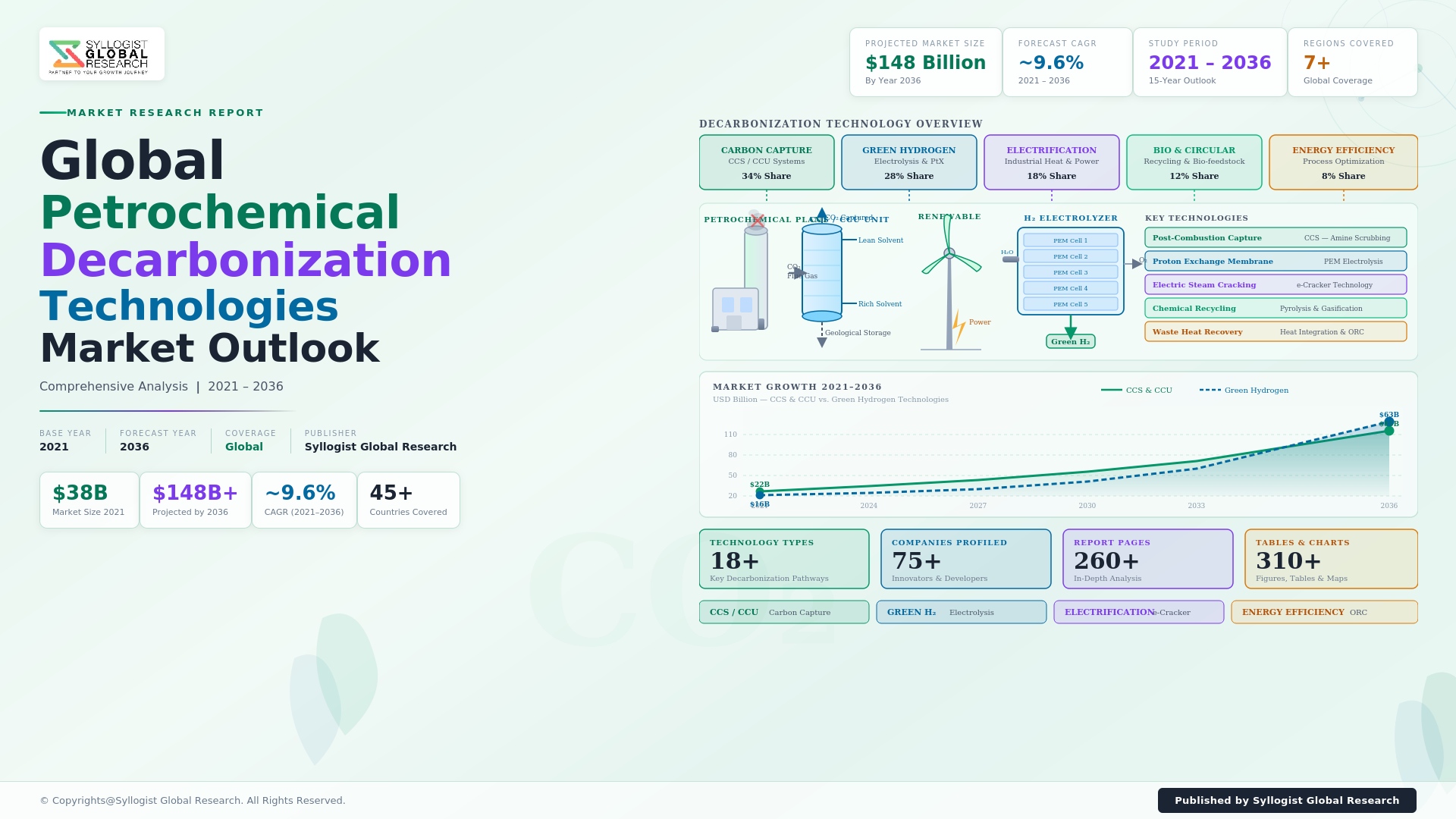

The global petrochemical industry decarbonization technologies market was valued at approximately USD 8.3 billion in 2025 and is projected to reach USD 31.7 billion by 2034, advancing at a compound annual growth rate of 16.1% over the forecast period from 2027 to 2034. This expansion is driven by converging regulatory pressure, accelerating corporate net-zero commitments from major petrochemical operators, and maturing cost curves across carbon capture and green hydrogen technologies. The European Union Emissions Trading System, which sustained carbon prices above USD 65 per metric tonne in 2024, is fundamentally reordering investment economics in favor of on-site decarbonization infrastructure across integrated refinery and petrochemical complexes, creating a durable commercial incentive that extends well beyond near-term compliance horizons and compelling operators to treat decarbonization capital expenditure as a core strategic requirement rather than a discretionary sustainability initiative.

Carbon capture, utilization, and storage represents the largest technology segment by deployed capital value within the petrochemical decarbonization market. Global installed carbon capture capacity serving petrochemical applications reached approximately 4.2 million metric tonnes of CO2 per year in 2025, against a technically addressable opportunity of approximately 680 million metric tonnes annually across the global petrochemical asset base. Post-combustion and oxyfuel capture systems applied to steam cracker furnaces and process heaters remain the most commercially near-term abatement pathway for operating facilities with asset lives extending to 2040 and beyond. Point-source capture costs declined to approximately USD 35 to USD 55 per metric tonne of CO2 for best-practice installations in 2025, with further reduction expected as modular capture system designs achieve standardization and series manufacturing scale across an expanding pipeline of committed project deployments.

Green hydrogen produced via water electrolysis using renewable electricity represents the most structurally transformative decarbonization vector for petrochemical operations, with the capacity to simultaneously eliminate combustion emissions from process heating and decarbonize hydrogen-intensive refinery processes including hydroprocessing, hydrotreating, and ammonia synthesis. Global electrolyzer manufacturing capacity additions accelerated in 2024 and 2025, with total installed green hydrogen production capacity reaching approximately 1.8 gigawatts globally by end of 2025. Multiple large-scale green hydrogen supply agreements between electrolyzer project developers and petrochemical operators in the Netherlands, Germany, Saudi Arabia, and Australia are positioning commercially meaningful hydrogen volumes for process integration beginning in 2027, marking the transition of green hydrogen from pilot demonstration to operational deployment across flagship petrochemical assets.

From a regional perspective, Europe leads the global market by policy maturity and per-facility investment intensity, supported by the Carbon Border Adjustment Mechanism taking full effect in 2026 and substantial co-financing available through the European Innovation Fund and national industrial decarbonization grant programs that are de-risking first-of-kind commercial deployments across the continent. Asia-Pacific, anchored by China’s expanding domestic carbon market and India’s emerging industrial decarbonization policy framework, represents the highest-growth regional opportunity by absolute investment volume through 2034, as the region’s disproportionately large petrochemical asset base and its expanding new capacity additions create a vast addressable opportunity for decarbonization technology integration across both brownfield retrofit and greenfield project applications.

Key Drivers

Mandatory Carbon Pricing and Emissions Trading System Expansion Creating Financial Imperative for Petrochemical Decarbonization Investment

The expansion of mandatory carbon pricing mechanisms across major economies is creating an inescapable financial incentive for petrochemical operators to invest in decarbonization technologies as an alternative to absorbing escalating carbon compliance costs that directly erode operating margins and competitive positioning. The European Union Emissions Trading System reached average prices above USD 65 per metric tonne of CO2 equivalent in 2024, with forward curve projections indicating sustained pricing above USD 80 per tonne through 2030 as allowance supply progressively tightens under the EU ETS Market Stability Reserve mechanism and the accelerated linear reduction factor introduced under Fit for 55 legislation. China’s national carbon market is progressively extending its coverage to petrochemical and chemical manufacturing sectors, with Phase 3 inclusion of petrochemical producers scheduled to materially expand the volume of CO2 emissions subject to mandatory allowance purchasing obligations from Chinese operators. Canada’s carbon price trajectory, legislated to reach CAD 170 per tonne by 2030, and the United Kingdom’s post-Brexit ETS alignment with European pricing levels collectively reinforce a global trend toward sufficiently high carbon pricing that commercial deployment of carbon capture, hydrogen switching, and process electrification technologies is entering positive net present value territory for major petrochemical facility operators across multiple jurisdictions simultaneously.

Green Hydrogen Cost Reduction and Scale-Up Unlocking Economically Viable Petrochemical Process Decarbonization

The capital and operating cost trajectory of green hydrogen production through proton exchange membrane and alkaline water electrolysis has followed a steep learning curve over the 2018 to 2025 period, with installed electrolyzer system costs declining from approximately USD 1,400 per kilowatt of electrolyzer capacity in 2018 to approximately USD 650 per kilowatt by 2025, driven by manufacturing scale-up in China, Europe, and North America, supply chain localization, and improvements in membrane durability and system efficiency. Green hydrogen production costs in regions with access to low-cost renewable electricity, including the US Gulf Coast, the Middle East, Australia, and Northern Chile, are approaching USD 2.50 to USD 3.80 per kilogram in best-practice project configurations, creating an economically plausible substitution case against conventional grey hydrogen from steam methane reforming. The petrochemical industry consumes approximately 45 million metric tonnes of hydrogen annually on a global basis for feedstock and process heating applications, establishing a very large addressable decarbonization market for green hydrogen integration that is beginning to attract committed procurement agreements from petrochemical majors seeking to establish verifiable Scope 1 emissions reductions from hydrogen substitution programs across their refinery and petrochemical integrated sites.

Corporate Net-Zero Commitment Obligations and Investor ESG Expectations Accelerating Decarbonization Technology Adoption

The accelerating adoption of science-based net-zero targets by major petrochemical operators under the Science Based Targets initiative framework, and the corresponding escalation of investor, lender, and insurance market expectations for credible transition plans aligned with 1.5 degree Celsius decarbonization pathways, is transforming corporate capital allocation decisions and creating a structural demand catalyst for decarbonization technology investment that operates in parallel with, and in some cases ahead of, regulatory compliance obligations. Major petrochemical companies have publicly committed to net-zero operational emissions targets with interim milestones that require demonstration of material progress through tangible capital deployment in carbon capture, electrification, and hydrogen transition programs visible to equity investors, rating agencies, and sustainability-linked loan lenders whose financing terms are increasingly calibrated to measurable decarbonization performance metrics. The emergence of sustainability-linked bond and loan financing instruments that tie coupon rates and margin adjustments to verified greenhouse gas emission reduction milestones is creating a direct cost of capital incentive for petrochemical operators to accelerate decarbonization technology procurement and deployment, as failure to meet contractually defined sustainability key performance indicators triggers interest rate step-up penalties that materially increase the financial cost of underperformance relative to committed transition pathways.

Key Challenges

Capital Intensity and Long Project Development Timelines of Large-Scale Carbon Capture and Storage Infrastructure

Large-scale carbon capture, utilization, and storage projects at petrochemical facilities are among the most capital-intensive industrial decarbonization investments per tonne of CO2 abated, with integrated capture, compression, transport, and geological storage systems for a major steam cracker complex requiring total capital expenditure of approximately USD 400 million to USD 900 million per facility depending on scale, capture efficiency specification, and geographic proximity to suitable geological storage formations or CO2 transport infrastructure. Project development timelines from feasibility study through engineering, procurement, and construction to first CO2 injection typically extend to eight to twelve years for greenfield CCS infrastructure in jurisdictions where permitting, environmental impact assessment, and geological storage site characterization processes are comprehensive, creating a significant execution timeline mismatch relative to the urgency implied by 2030 interim decarbonization milestones. The challenge is compounded by the geological storage liability, pore space ownership, and long-term monitoring obligation frameworks that remain incompletely defined in several key petrochemical producing jurisdictions, creating legal uncertainty that is delaying investment decisions by petrochemical operators who require clear regulatory frameworks and commercially structured risk allocation before committing the capital required for first-of-kind full-chain CCS projects at operating petrochemical sites.

Intermittency and Cost Volatility of Renewable Electricity Supply Constraining Green Hydrogen Production Economics

Green hydrogen production economics for petrochemical applications are highly sensitive to the cost, reliability, and temporal availability profile of dedicated renewable electricity supply, with the electrolyzer capacity factor achieved in practice heavily determining the levelized cost of hydrogen production per kilogram and the capital efficiency of electrolyzer assets whose fixed cost structures require high utilization rates to achieve competitive hydrogen production costs versus grey hydrogen alternatives. The intermittency of solar and wind power generation creates structural mismatches between renewable electricity availability and the continuous, high-volume hydrogen demand profile of petrochemical operations that consume hydrogen around the clock for hydroprocessing and synthesis reactions, requiring either significant hydrogen storage buffer capacity, grid electricity backstop arrangements that reintroduce carbon and cost variability, or oversized electrolyzer installation relative to average operational capacity. Electricity grid connection constraints and transmission infrastructure limitations in regions with abundant renewable energy resources but underdeveloped grid infrastructure, including parts of the Middle East, North Africa, and Australia, are creating practical bottlenecks to the co-location of large-scale electrolysis capacity with renewable generation assets at the scale required to supply meaningful hydrogen volumes to adjacent petrochemical complexes, introducing project development risks and cost escalation factors that are limiting the pace of green hydrogen integration into commercial petrochemical operations.

Technology Readiness and Reliability Gaps in Electric Cracker and Process Electrification Systems at Commercial Scale

The electrification of steam cracking, which is the single most energy-intensive and CO2-emitting process in the petrochemical industry consuming approximately 8 gigajoules of thermal energy per tonne of ethylene produced from naphtha feedstock, represents the highest-impact but most technically demanding decarbonization pathway available to the sector, with resistance heating and direct electrification of cracker furnaces requiring both validated long-term operational reliability at commercial throughput scales and access to clean electricity volumes substantially exceeding what has been demonstrated in pilot-scale projects to date. Electric steam cracker demonstrations represent important proof-of-concept programs, but commercial-scale electric cracker units capable of processing 500,000 to 1,000,000 tonnes per year of naphtha equivalent feedstock have not yet been commissioned and face materials durability, electrical resistance heating element lifetime, and process control challenges requiring additional engineering development before large-scale deployment can proceed with the operational reliability standards demanded by continuous-process petrochemical facility operators. The capital cost premium of electric cracker systems relative to conventional gas-fired cracker furnaces, estimated at approximately 25% to 45% depending on electricity infrastructure requirements and facility configuration, presents a further adoption barrier in competitive petrochemical markets where operator margins are subject to feedstock price volatility and product price pressure from overcapacity in global polymer markets.

Market Segmentation

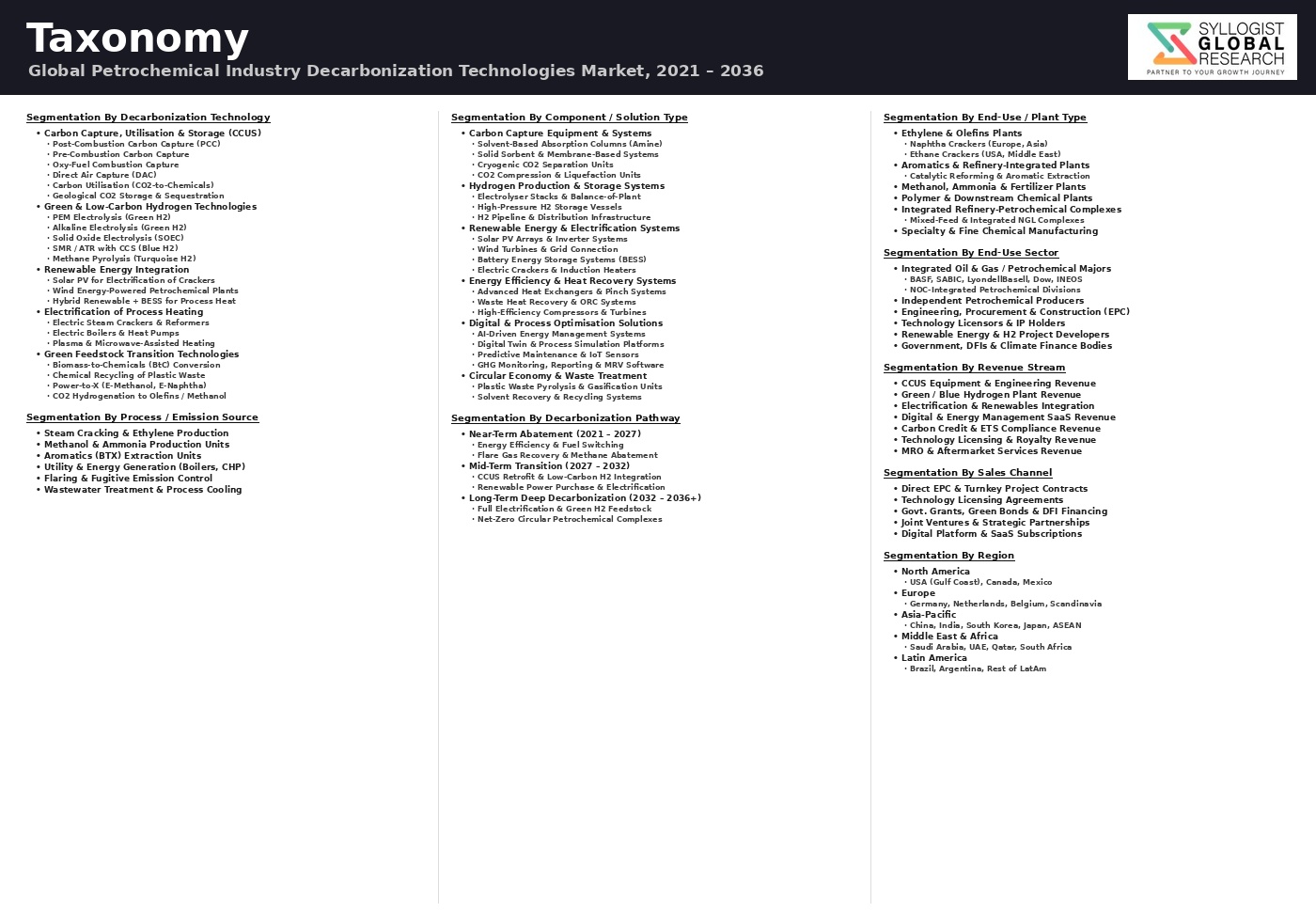

- Segmentation By Technology Type

- Carbon Capture, Utilization, and Storage (CCUS)

- Green Hydrogen Production via Water Electrolysis

- Blue Hydrogen Production (Steam Methane Reforming with CCS)

- Process Electrification and Electric Steam Crackers

- Biomass and Bio-Based Feedstock Substitution

- Chemical and Mechanical Plastic Recycling Technologies

- Energy Efficiency, Heat Integration, and Waste Heat Recovery

- Carbon Monitoring, Reporting, and Verification Software

- Others

- Segmentation By Application

- Steam Cracking and Ethylene Production

- Aromatics Extraction and Purification

- Methanol Synthesis

- Ammonia and Fertilizer Production

- Hydroprocessing and Hydrotreating

- Polymer and Plastics Manufacturing

- Refinery-Integrated Petrochemical Operations

- Others

- Segmentation By Carbon Abatement Mechanism

- Direct Emissions Avoidance (Electrification and Fuel Switching)

- Post-Combustion Carbon Capture

- Pre-Combustion Carbon Capture

- Industrial Carbon Utilization (CO2-to-Chemicals)

- Geological Carbon Storage

- Others

- Segmentation By Facility Type

- Greenfield Petrochemical Complex Integration

- Brownfield Retrofit and Upgrade Programs

- Refinery-Petrochemical Integrated Facilities

- Standalone Polymer Production Plants

- Methanol and Ammonia Production Facilities

- Others

- Segmentation By Deployment Scale

- Large-Scale Industrial Installations (above 500,000 tCO2/year)

- Medium-Scale Industrial Installations (100,000 to 500,000 tCO2/year)

- Small and Modular Systems (below 100,000 tCO2/year)

- Segmentation By End User

- Integrated Oil and Gas Majors with Petrochemical Operations

- Dedicated Petrochemical Companies

- Specialty Chemical Manufacturers

- Fertilizer and Agrochemical Producers

- Industrial Gas Companies

- Others

- Segmentation By Component and Service

- Technology Licensing and Intellectual Property

- Engineering, Procurement, and Construction Services

- Equipment and System Supply

- Operations and Maintenance Services

- Project Finance and Green Bond Instruments

- Others

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Petrochemical Industry Decarbonization Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, carbon capture, green hydrogen, process electrification, and chemical recycling, and by application, steam cracking, ammonia production, hydroprocessing, and polymers manufacturing, to enable technology developers, petrochemical operators, project financiers, and industrial policy makers to identify which decarbonization technology segments will generate the highest absolute revenue and the most durable growth trajectory across the forecast period?

- How are evolving mandatory carbon pricing frameworks across the European Union, China, Canada, and the United Kingdom expected to reshape the investment economics of petrochemical decarbonization technologies through 2034, and at what carbon price thresholds do carbon capture, green hydrogen integration, and process electrification technologies each achieve positive net present value for brownfield retrofit applications at representative steam cracker, ammonia synthesis, and methanol production facilities across major petrochemical producing regions?

- What is the projected market size, compound annual growth rate, and competitive landscape of the green hydrogen production and integration segment serving petrochemical applications through 2034, including analysis of electrolyzer technology cost trajectories, renewable electricity availability and pricing by region, committed offtake agreements between hydrogen producers and petrochemical operators, and the regulatory and infrastructure prerequisites that will determine the pace of green hydrogen displacement of conventional grey hydrogen across petrochemical process applications globally?

- How is the technology readiness, commercial deployment pipeline, and cost reduction trajectory of electric steam cracking and process electrification technologies expected to evolve through 2034, which petrochemical operators and technology developers are leading commercial-scale demonstration programs, and what is the realistic addressable market for process electrification retrofits across the global operating steam cracker asset base given electricity infrastructure requirements, capital cost premiums, and competitive electricity price availability across key petrochemical producing regions?

- Who are the leading technology licensors, carbon capture system developers, electrolyzer manufacturers, engineering procurement and construction firms, and industrial gas companies currently defining the competitive landscape of the global petrochemical decarbonization technologies market, and what are their respective technology portfolios, project delivery track records, geographic market positioning, strategic partnership ecosystems, and differentiated capabilities in carbon capture, green hydrogen, process electrification, and chemical recycling that will determine competitive advantage as the market scales from early commercial deployment toward mainstream industrial adoption through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- High Capital Cost of Decarbonization Technology Deployment & Return on Investment Uncertainty Risk

- Green Hydrogen Cost, Renewable Electricity Price & Infrastructure Availability Risk for Feedstock & Fuel Switching

- Carbon Price Volatility, Policy Discontinuity & Regulatory Timeline Uncertainty Risk

- Technology Maturity, Scale-Up Risk & First-of-a-Kind (FOAK) Project Execution Risk for Novel Decarbonization Pathways

- Carbon Leakage, Competitiveness & Stranded Asset Risk from Uneven Global Decarbonization Policy Implementation

- Regulatory Framework & Standards

- Carbon Pricing & Emissions Trading: EU ETS (Industrial Sector Phase 4 & Phase 5), CBAM for Petrochemicals, UK ETS, China National ETS & National Carbon Tax Frameworks Applicable to Petrochemical Plants

- Industrial Decarbonization Policy: EU Industrial Carbon Management Strategy, US Inflation Reduction Act (IRA) 45Q CCUS Tax Credit, 45V Green Hydrogen Credit & EU Net Zero Industry Act Petrochemical Provisions

- Green Hydrogen Certification & Low-Carbon Fuel Standard: EU Delegated Acts on Renewable Hydrogen (RFNBO), US DOE Hydrogen Scoring Methodology & National Green Hydrogen Certification Frameworks

- Chemical Recycling & Circular Economy Regulation: EU Packaging & Packaging Waste Regulation Recycled Content Mandate, Mass Balance Certification Standards (ISCC Plus, REDcert2) & Chemical Recycling Feedstock Classification

- GHG Emission Reporting, TCFD & Industrial Emission Standards: EU IED Best Available Technique (BAT) for Petrochemicals, ISSB S2 Climate Disclosure, SEC Climate Rule & MoEFCC Emission Norms for Petrochemical Plants in Developing Markets

- Global Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Capacity Installed & CO2 Abated, Million Tonnes per Year)

- Market Size & Forecast by Decarbonization Technology Type

- Carbon Capture, Utilisation & Storage (CCUS): Post-Combustion, Oxyfuel & Chemical Looping for Petrochemical Plants

- Green & Blue Hydrogen Production & Feedstock Substitution (Electrolysis, SMR with CCS & ATR with CCS)

- Electric Steam Cracker & Process Furnace Electrification (Resistance, Inductive & Plasma Heating)

- Industrial Heat Pump, Electric Boiler & Mechanical Vapour Recompression (MVR) for Steam Decarbonization

- Bio-Based Feedstock Integration (Bio-Naphtha, Bio-Ethanol, Biomass Gasification & Biogas Upgrading)

- Chemical Recycling & Waste Plastic Pyrolysis for Circular Feedstock Supply

- CO2 Utilisation: Power-to-X, CO2-to-Methanol, CO2-to-Olefin & Carbon Mineralisation

- Energy Efficiency, Heat Integration, Process Optimisation & Waste Heat Recovery Technology

- Renewable Energy Integration: Captive Solar, Onsite Wind, Power Purchase Agreement & BESS for Petrochemical Site

- Methane Leak Detection, Fugitive Emission Monitoring & CH4 Abatement Technology

- Market Size & Forecast by Process Unit & Application

- Steam Cracker & Ethylene Plant Decarbonization

- Ammonia Plant Decarbonization (Green Ammonia & Blue Ammonia Route)

- Methanol & Syngas Plant Decarbonization (Green Methanol & E-Methanol)

- Aromatics Complex (BTX, Paraxylene) Decarbonization

- Chlor-Alkali & EDC/VCM/PVC Production Decarbonization

- Polymer Production (Polyethylene, Polypropylene & PET) Decarbonization

- Utility & Off-Site: Steam Generation, Cooling, Compressed Air & Flare Minimisation

- Market Size & Forecast by Decarbonization Scope

- Scope 1: Direct Process & Combustion Emission Reduction at Plant Level

- Scope 2: Purchased Energy Decarbonization via Renewable Electricity & Green Steam

- Scope 3: Feedstock Carbon Intensity Reduction & Product End-of-Life Circularity

- Market Size & Forecast by Technology Readiness Level (TRL)

- TRL 1 to 3: Fundamental Research, Novel Concept & Lab-Scale Validation

- TRL 4 to 6: Pilot, Demonstration & Pre-Commercial Scale-Up

- TRL 7 to 9: Commercial Deployment, Proven Technology & Operational Scale

- Market Size & Forecast by Component

- CCUS Equipment: Capture System, Amine Scrubber, Compressor, Pipeline & Storage

- Green Hydrogen Electrolyser, H2 Storage & Distribution Infrastructure

- Electric Furnace, Process Heater & Plasma Reactor for Cracker Electrification

- Industrial Heat Pump, Electric Boiler & Steam Decarbonization Equipment

- Chemical Recycling & Pyrolysis Plant Equipment

- Carbon Accounting, MRV & Decarbonization Digital Platform

- Market Size & Forecast by End-User

- Integrated Petrochemical & Refining Complex

- Standalone Cracker, Olefin & Aromatic Producer

- Ammonia, Methanol & Fertiliser Producer

- Polymer, Plastics & Fibre Manufacturer

- Specialty Chemical & Intermediate Producer

- National Petrochemical Company & Government Industrial Enterprise

- Market Size & Forecast by Sales Channel

- Technology Licence & Process Design Package (Licensor Channel)

- EPC & EPCM Turnkey Contract

- Equipment, Catalyst & Long-Term Service Supply Agreement

- Carbon Advisory, Digital Platform, MRV & Net Zero Roadmap Consulting

- North America Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Petrochemical Industry Decarbonization Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (CO2 Abated, Million Tonnes per Year)

- By Decarbonization Technology Type

- By Process Unit & Application

- By Decarbonization Scope

- By Technology Readiness Level

- By Component

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, France, Netherlands, Belgium, United Kingdom, Norway, Sweden, China, Japan, South Korea, India, Singapore, Taiwan, Saudi Arabia, UAE, Kuwait, Qatar, Brazil, Indonesia, Australia, Russia

- Technology Landscape & Innovation Analysis

- Electric Steam Cracker & Process Furnace Electrification Technology Deep-Dive: Resistance, Inductive, Plasma & Microwave Heating Route Comparison for Ethylene & Propylene Production

- CCUS for Petrochemical Plants: Post-Combustion Amine Scrubbing, Oxyfuel, Chemical Looping & Solid Sorbent Capture Technology for Cracker & Boiler Flue Gas

- Green Hydrogen & Low-Carbon Hydrogen Technology for Petrochemical Feedstock & Fuel Substitution: PEM, Alkaline & SOEC Electrolyser Selection & H2 Integration Design

- Bio-Based Feedstock & Chemical Biorefinery Technology: Bio-Naphtha Co-Processing, Bio-Ethanol Dehydration to Ethylene & Biomass Gasification to Syngas Integration

- Chemical Recycling, Waste Plastic Pyrolysis & Mass Balance Accounting Technology for Circular Feedstock in Petrochemical Production

- Industrial Heat Pump, Mechanical Vapour Recompression (MVR), Electric Boiler & Steam Network Decarbonization Technology

- CO2 Utilisation Technology: E-Methanol Synthesis, CO2-to-Olefin, Power-to-Chemicals & Carbon Mineralisation Technology for Petrochemical Site CO2 Conversion

- Patent & IP Landscape in Petrochemical Industry Decarbonization Technologies

- Value Chain & Supply Chain Analysis

- Low-Carbon Feedstock Supply Chain: Green Hydrogen, Blue Hydrogen, Bio-Naphtha & Recycled Pyrolysis Oil Sourcing & Logistics

- CCUS Equipment & Infrastructure Supply Chain: Capture System, Amine Regeneration, CO2 Compression & Pipeline Supplier Landscape

- Electrolyser, Renewable Energy Equipment & Green Power Infrastructure Supply Chain

- Technology Licensor, Process Design Package Provider & Decarbonization Engineering Consultant Landscape

- EPC Contractor & Systems Integrator for Petrochemical Decarbonization Project

- Petrochemical Operator, NOC & Chemical Company Decarbonization Programme

- Carbon Accounting Platform, MRV Service, Third-Party Verifier & ESG Disclosure Ecosystem

- Pricing Analysis

- Marginal Abatement Cost (MAC) Analysis by Decarbonization Technology: USD per Tonne CO2 Avoided for CCUS, Electrification, Green H2 & Energy Efficiency at Petrochemical Plant

- Electric Cracker Capex Premium vs. Conventional Gas-Fired Furnace: Breakeven Electricity Price & Carbon Price for Technology Parity

- Green Hydrogen Cost at Petrochemical Plant Gate: Electrolyser CAPEX, RE Electricity Cost, H2 Transport & Storage Cost Trajectory to 2035

- CCUS Cost Analysis for Petrochemical Plant: Capture, Compression, Transport & Storage Cost per Tonne CO2 Captured vs. Carbon Price

- Bio-Based & Recycled Feedstock Price Premium vs. Fossil Naphtha: Mass Balance Certificate Value & Green Product Price Premium Analysis

- Total Decarbonization Investment & Programme Cost: Levelised Cost of Decarbonization (LCOD) per Tonne CO2 Abated Across Technology Portfolio Mix

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Petrochemical Decarbonization Pathways: Scope 1, 2 & 3 GHG Emission Reduction Potential by Technology Route & Feedstock Switch

- Paris Agreement 1.5 Degree Celsius Compatibility: Science-Based Targets (SBTi) for Chemicals Sector, Net Zero Commitment Alignment & Long-Term Decarbonization Trajectory

- Circular Economy Contribution: Chemical Recycling, Bio-Based Plastics & Product Carbon Footprint Reduction Along the Petrochemical Value Chain

- Co-Benefits of Petrochemical Decarbonization: Air Quality Improvement, NOx & SOx Reduction, Industrial Community Health Impact & Just Transition for Chemical Workers

- Regulatory-Driven Sustainability: EU CBAM Financial Exposure, ISSB S2 & SEC Climate Disclosure Requirements, EU Taxonomy Green Activity Criteria for Petrochemical Decarbonization Investment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Concentrated by Technology Type & Application)

- Top 10 Players Market Share by Revenue, Deployed Capacity & Technology Portfolio

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Process Application & Geography

- Player Classification

- Integrated Technology Licensor & Engineering Company with Decarbonization Portfolio (Linde, Air Liquide, BASF, Topsoe, Technip Energies)

- CCUS Technology Provider & Industrial CO2 Capture Specialist

- Green & Blue Hydrogen Technology Provider & Electrolyser Manufacturer

- Electric Furnace, Plasma Cracker & Process Electrification Technology Developer

- Chemical Recycling & Pyrolysis Technology Company

- Industrial Energy Efficiency, Heat Pump & Process Optimisation Technology Provider

- Carbon Accounting, MRV, Digital Decarbonization Platform & Net Zero Advisory Company

- EPC Contractor & Decarbonization Project Developer for Petrochemical Industry

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Decarbonization Technology Products, Services & Patent Portfolio

- Key Customer Relationships & Reference Decarbonization Project Installations

- Manufacturing & Service Footprint, Installed Capacity & CO2 Abatement Track Record

- Revenue (Decarbonization Technology Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Project Awards, Technology Milestones, Certifications)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Decarbonization Depth vs. Commercial Deployment Scale)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Decarbonization Technology Type, Process Application, TRL, End-User & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Technology Portfolio & Decarbonization Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Market Development Strategy

- Customer & Industrial Operator Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability, Net Zero Alignment & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)