Market Definition

The Global Carbon-Neutral Petrochemicals Market encompasses the production, processing, certification, and commercial supply of petrochemical products and their bio-based, recycled-content, and carbon-captured equivalents whose net lifecycle greenhouse gas emissions are reduced to zero through a combination of feedstock substitution, process decarbonization, carbon capture and utilization or storage, and verified carbon offset mechanisms applied across the full value chain from raw material extraction or generation through chemical manufacturing, product use, and end-of-life disposition. Carbon-neutral petrochemicals represent a structurally heterogeneous product category that includes bio-based olefins, aromatics, and polymers produced from renewable biological feedstocks through biological or thermochemical conversion routes; chemically recycled petrochemical intermediates derived from post-consumer plastic waste through pyrolysis, gasification, or solvolysis processes that convert waste polymers back into petrochemical-equivalent feedstocks; green hydrogen-based ammonia, methanol, and synthetic hydrocarbon chemicals produced through electrolysis-powered synthesis routes; carbon dioxide-derived chemicals including polyols, methanol, and formic acid manufactured through electrochemical or catalytic carbon dioxide utilization pathways; and conventional petrochemicals produced using fossil feedstocks whose associated process and upstream emissions are permanently sequestered through geological carbon capture and storage, with residual emissions offset through certified carbon removal credits under recognized third-party verification standards. The market encompasses the full downstream application range of these products, including carbon-neutral polyethylene, polypropylene, polyethylene terephthalate, nylon, polyurethane, polystyrene, synthetic rubber, and specialty chemicals serving the packaging, automotive, construction, textiles, electronics, and agricultural sectors. Key participants include integrated oil and chemicals majors transitioning production assets, dedicated bio-based chemical producers, chemical recycling technology developers and operators, green hydrogen producers, carbon capture technology providers, polymer converters and brand owners driving downstream supply chain decarbonization, and certification and registry bodies administering mass balance accounting standards and carbon neutrality verification frameworks that provide the commercial legitimacy underpinning premium pricing and green procurement claims across global supply chains.

Market Insights

The global carbon-neutral petrochemicals market is at an early but rapidly accelerating stage of commercial development, driven by the convergence of net-zero corporate commitments spanning the entire downstream chemicals and materials value chain, progressive regulatory frameworks in the European Union and other major markets imposing mandatory recycled content and carbon footprint disclosure obligations on plastic and chemical products, and the emergence of commercially credible technical pathways for petrochemical decarbonization that are transitioning from demonstration scale toward initial commercial deployment. The petrochemical industry collectively contributes approximately 3.6 gigatonnes of carbon dioxide equivalent emissions annually, representing approximately 7% of global industrial greenhouse gas emissions, and its structural dependency on fossil feedstocks for both energy and carbon inputs makes it among the most challenging industrial sectors to decarbonize through energy efficiency and renewable energy electrification alone, necessitating the more fundamental feedstock substitution and carbon management approaches that define the carbon-neutral petrochemicals market. The global carbon-neutral petrochemicals market was valued at approximately USD 14.8 billion in 2025, encompassing bio-based chemical revenues, certified chemically recycled content petrochemical products, green ammonia and methanol, and carbon dioxide-derived chemical products, and is projected to reach USD 62.4 billion by 2034, advancing at a compound annual growth rate of 17.3% over the forecast period from 2027 to 2034, as mandatory sustainability regulations, expanding corporate net-zero procurement commitments, and declining production cost premiums for bio-based and recycled-content chemicals collectively drive accelerating commercial adoption across the packaging, automotive, consumer goods, and industrial chemical application sectors.

The bio-based chemicals and polymers segment constitutes the most commercially mature strand of the carbon-neutral petrochemicals market, having accumulated over two decades of production experience in bio-ethanol dehydration to bio-ethylene, bio-polyethylene production from sugarcane ethanol, bio-polyethylene terephthalate incorporating bio-based monoethylene glycol, and bio-based nylon 11 and nylon 6,10 produced from castor oil and sebacic acid feedstocks, with this accumulated industrial experience providing a validated commercial template that is being extended to new bio-based chemical products and production geographies as renewable feedstock availability and production scale economics improve. The bio-based polyethylene market alone reached approximately 480,000 metric tonnes of annual production capacity in 2025, with expansion projects in Brazil, the United States, Europe, and Southeast Asia collectively representing over 1.2 million metric tonnes of additional bio-polyethylene capacity under development as of mid-2026, driven by consumer goods brand owner commitments to renewable content polymer procurement from companies including Unilever, Procter and Gamble, Nestlé, and PepsiCo that have collectively announced procurement targets for bio-based and recycled content packaging materials covering over 14 million metric tonnes of polymer annually by 2030. The feedstock landscape for bio-based petrochemical production is diversifying beyond first-generation sugar and starch platforms toward second-generation lignocellulosic biomass conversion and third-generation algal biomass pathways, with lignocellulosic bio-based chemical production beginning to achieve pilot and early commercial scale deployment in North America and Europe, and with the cost trajectory of lignocellulosic feedstock conversion to bio-ethylene, bio-propylene, and bio-aromatics projected to reach competitive cost parity with first-generation bio-based routes within the forecast period as enzymatic hydrolysis and fermentation process efficiencies continue improving.

Chemical recycling represents the most strategically significant emerging pathway for carbon-neutral petrochemicals in the medium term, addressing the structural limitation of bio-based production which is constrained by sustainable feedstock availability and land use competition, by creating a circular carbon economy in which the carbon atoms embodied in post-consumer plastic waste are recovered and reprocessed into virgin-equivalent petrochemical feedstocks through pyrolysis, advanced gasification, or solvolysis depolymerization technologies, producing certified recycled-content polymers and chemicals that carry verified carbon footprint advantages relative to conventional fossil-derived equivalents while maintaining the purity and performance specifications demanded by food-contact packaging, pharmaceutical, and automotive applications. The global chemical recycling capacity for plastic waste was approximately 340,000 metric tonnes per year of plastic processing input as of 2025, with over 4.2 million metric tonnes of additional chemical recycling capacity in various stages of development, permitting, and construction across North America, Europe, and Asia-Pacific, representing a near-order-of-magnitude scaling of the sector that would, if successfully commissioned, transform chemical recycling from a demonstration-scale technology into a meaningful industrial contributor to the carbon-neutral petrochemicals supply base. Mass balance accounting frameworks, administered under certification systems including ISCC PLUS, REDcert2, and the International Sustainability and Carbon Certification standards, are the essential commercial infrastructure enabling chemical recycling outputs to be traded as certified recycled content products across complex petrochemical value chains in which physical commingling of recycled and conventional feedstock streams is operationally unavoidable at cracker and chemical plant scale, providing the chain-of-custody verification that supports brand owner claims of recycled content packaging and products under sustainability reporting and regulatory disclosure frameworks.

From a regional standpoint, Europe is the most advanced and policy-coherent market for carbon-neutral petrochemicals globally, driven by the European Union’s comprehensive regulatory architecture encompassing the European Green Deal, the Circular Economy Action Plan’s mandatory recycled content targets for plastic packaging, the Carbon Border Adjustment Mechanism imposing carbon costs on imported chemicals produced with higher-than-EU-average emission intensities, and the proposed revision to the Industrial Emissions Directive that will progressively incorporate petrochemical production into emissions trading obligations requiring measurable decarbonization investment. European chemical industry associations have committed to collective carbon neutrality by 2050 with intermediate milestones requiring 20% reduction in absolute sector emissions by 2030, with leading integrated chemical producers including BASF, INEOS, LyondellBasell, and Dow each having announced multi-billion dollar decarbonization investment programs encompassing bio-based feedstock integration, chemical recycling capacity construction, and green hydrogen procurement infrastructure. North America is the second-most-active regional market, anchored by the Inflation Reduction Act’s production tax credits for clean hydrogen, the 45Q carbon capture and storage tax credit providing USD 85 per tonne of geologically sequestered carbon dioxide, and sustainability-driven demand from consumer goods companies and automotive manufacturers whose net-zero supply chain commitments are generating contractually supported off-take agreements for carbon-neutral petrochemical products that provide the revenue certainty enabling project financing for capital-intensive decarbonization infrastructure. Asia-Pacific, led by Japan, South Korea, and China, is investing aggressively in carbon-neutral petrochemical development through national hydrogen strategies, chemical recycling industrial policy programs, and bio-based chemical production capacity expansion, with the region representing the largest future growth opportunity as its massive conventional petrochemical production base begins the multi-decade transition toward carbon-neutral alternatives.

Key Drivers

Mandatory Sustainability Regulations, Carbon Pricing Mechanisms, and the Escalating Regulatory Cost of Conventional Fossil-Based Petrochemical Production

The most structurally powerful and commercially irreversible driver of investment and adoption in the global carbon-neutral petrochemicals market is the progressive implementation of mandatory regulatory frameworks across major economies that impose quantifiable and escalating financial costs on conventional fossil-based petrochemical production while simultaneously creating commercial advantage for carbon-neutral alternatives through mandatory content requirements, preferential procurement provisions, and carbon border adjustment mechanisms that effectively extend domestic carbon pricing obligations to imported chemical products. The European Union’s Emissions Trading System has expanded to cover additional industrial installations including larger chemical production facilities, with EU carbon allowance prices having averaged approximately USD 68 per tonne of carbon dioxide equivalent in 2025 and projected to reach USD 120 to USD 150 per tonne by 2030, creating a carbon cost burden on conventional European petrochemical production that is directly improving the relative cost competitiveness of bio-based and recycled-content alternatives whose lower emission intensities generate proportionally smaller carbon cost obligations. The EU Packaging and Packaging Waste Regulation mandating minimum recycled content of 30% for contact-sensitive plastic packaging by 2030 and 65% for all plastic packaging by 2040 creates a legally enforceable demand signal for certified recycled-content petrochemicals of unprecedented scale and durability, compelling polymer converters and brand owners across the European market to secure long-term supply agreements with chemical recycling and bio-based polymer producers years in advance of the mandate effective dates, generating the contracted revenue certainty that enables project financing for capital-intensive decarbonization production infrastructure.

Corporate Net-Zero Supply Chain Commitments and the Brand Owner-Driven Demand for Certified Carbon-Neutral Polymer and Chemical Inputs

The proliferation of Science Based Targets initiative-validated corporate net-zero commitments among the world’s largest consumer goods manufacturers, automotive OEMs, retailers, and industrial chemical users is generating a powerful and commercially immediate demand pull for carbon-neutral petrochemical products that is operating in advance of and independently from mandatory regulatory requirements, driven by the reputational, investor relations, and supply chain risk management imperatives that are compelling Scope 3 upstream emission reduction commitments alongside the Scope 1 and 2 decarbonization programs that have historically dominated corporate sustainability investment. Consumer goods conglomerates including Unilever, Nestlé, PepsiCo, Procter and Gamble, and L’Oréal have collectively committed to sourcing over 14 million metric tonnes of certified sustainable polymer annually by 2030, representing procurement volumes that substantially exceed the currently available certified bio-based and recycled-content polymer supply, creating a structural supply deficit that is incentivizing accelerated capacity investment by chemical producers seeking to capture the premium pricing and long-term contracted revenue streams that brand owner sustainability commitments represent. Automotive OEMs including BMW, Volkswagen, Mercedes-Benz, and Toyota have announced supply chain decarbonization requirements specifying minimum recycled or renewable content thresholds for polymer and chemical inputs to vehicle interior, exterior, and underhood components, with compliance timelines that are compelling Tier-1 and Tier-2 automotive material suppliers to qualify certified carbon-neutral material sources and integrate them into production supply chains within development program timelines that leave limited flexibility for extended qualification delays, creating commercially urgent demand signals that are accelerating project investment decisions at carbon-neutral petrochemical producers.

Declining Production Cost Premiums for Bio-Based and Chemically Recycled Petrochemicals and the Improving Economics of Green Hydrogen-Based Chemical Synthesis

The commercial viability and adoption pace of carbon-neutral petrochemicals is being materially advanced by technology learning curves, scale economy improvements, and enabling infrastructure cost reductions that are progressively narrowing the production cost premium of bio-based, chemically recycled, and green hydrogen-derived chemical products relative to their conventional fossil-based equivalents, improving the economics of carbon-neutral petrochemical investment from a position requiring substantial premium pricing or regulatory support toward a trajectory approaching cost-competitive production in the most favorable feedstock and production geographies. Bio-based ethylene produced from first-generation sugarcane-derived ethanol in Brazil currently carries a production cost premium of approximately 35% to 55% relative to naphtha-cracker ethylene at prevailing oil prices, a premium that has declined from over 100% a decade ago as sugarcane agricultural productivity, ethanol production efficiency, and bio-ethylene plant scale have improved, with the premium projected to decline to approximately 15% to 25% by 2030 as further process optimization and feedstock cost reduction are achieved. Chemical recycling pyrolysis oil production costs have declined by approximately 40% per tonne of plastic input processed between 2018 and 2025 as plant scale has increased from demonstration units of 5,000 metric tonnes annual capacity toward commercial-scale facilities of 50,000 to 100,000 metric tonnes capacity, with the cost of producing certified pyrolysis oil feedstock for cracker reprocessing projected to reach parity with virgin naphtha on a carbon-price-adjusted basis before 2030 in regions with favorable plastic waste collection infrastructure and competitive renewable energy costs that reduce process energy expenditure.

Key Challenges

Persistent Production Cost Premiums, Project Financing Complexity, and the Capital Intensity of Carbon-Neutral Petrochemical Production Infrastructure

The capital investment required to develop and commission commercial-scale carbon-neutral petrochemical production facilities, whether bio-based chemical plants, chemical recycling pyrolysis or gasification complexes, green hydrogen-powered ammonia or methanol synthesis units, or conventional petrochemical facilities integrated with carbon capture and storage infrastructure, is substantially higher than equivalent fossil-based production capacity on a per-tonne-of-output basis, creating a capital cost barrier that constrains the pace of capacity deployment even when the long-term economics of carbon-neutral production are commercially favorable after carbon pricing and regulatory incentives are incorporated into project economics. A commercial-scale lignocellulosic bio-based ethylene production complex of 200,000 metric tonnes annual capacity requires capital investment estimated at USD 1.8 billion to USD 3.2 billion depending on feedstock pretreatment technology, conversion process selection, and site infrastructure requirements, representing a capital intensity per tonne of nameplate capacity that is three to five times greater than equivalent naphtha-cracker ethylene production, imposing equity return requirements and leverage structures that are difficult to achieve within conventional chemical industry project financing frameworks without the support of government loan guarantees, production tax credit monetization, or contracted premium offtake agreements providing revenue certainty sufficient to underwrite the project’s debt service obligations. The combination of technology scale-up risk, carbon price trajectory uncertainty, feedstock cost variability, and the absence of established secondary market liquidity for carbon-neutral petrochemical project assets collectively creates a risk profile that many institutional investors find structurally challenging to underwrite at the project scale and financial return expectations required to attract the global capital flows necessary to deploy carbon-neutral petrochemical production capacity at the rate demanded by net-zero commitments across the chemicals and materials sector.

Feedstock Availability Constraints, Land Use Competition, and the Sustainability Integrity Challenges of Bio-Based Petrochemical Feedstock Sourcing

The scaling of bio-based petrochemical production to volumes capable of making a meaningful contribution to the decarbonization of the global petrochemicals industry faces fundamental physical constraints imposed by the finite availability of sustainably produced biological feedstocks that do not compete with food production, generate indirect land use change emissions, or deplete biodiversity and water resources in ways that undermine the net environmental benefit that bio-based petrochemical production is intended to deliver. The global petrochemicals industry processes approximately 500 million metric tonnes of fossil-derived feedstocks annually, a quantity that vastly exceeds the bio-based feedstock volumes that could be sustainably mobilized for chemical production without displacing food and feed crops, exhausting sustainably harvestable agricultural residue supplies, or requiring the conversion of natural ecosystems to energy crop cultivation at scales that would generate land use change carbon emissions potentially exceeding the production-phase carbon benefits of bio-based chemical manufacturing. Sustainability certification systems including the Roundtable on Sustainable Biomaterials, ISCC PLUS, and the EU Renewable Energy Directive’s sustainability criteria for biofuels and bioliquids provide governance frameworks for feedstock sustainability verification, but their practical application to complex bio-based chemical supply chains spanning multiple continents and involving diverse agricultural commodity markets introduces certification cost, verification complexity, and audit trail integrity challenges that add commercial friction and cost to bio-based petrochemical supply chains that are already managing a production cost premium relative to conventional fossil alternatives, limiting the ability of smaller producers and downstream users to engage with sustainable bio-based sourcing without disproportionate administrative burden.

Mass Balance Accounting Complexity, Carbon Neutrality Claim Verification Standards Fragmentation, and the Greenwashing Risk Undermining Market Credibility

The commercial functioning of the carbon-neutral petrochemicals market is fundamentally dependent on the integrity and mutual recognition of the accounting systems and certification frameworks used to verify, quantify, and communicate the carbon neutrality or recycled content credentials of chemical products that in most cases cannot be physically distinguished from their conventional fossil-derived equivalents at the point of sale, creating a systemic market credibility risk if the accounting frameworks governing these claims are found to be inconsistent, insufficiently rigorous, or susceptible to manipulation by market participants with financial incentives to overclaim sustainability credentials. The current landscape of mass balance certification standards for bio-based and chemically recycled petrochemicals is fragmented across multiple competing systems, including ISCC PLUS, REDcert2, the International Sustainability and Carbon Certification system, and various proprietary industry schemes, that differ in their allocation methodologies, audit frequency requirements, chain-of-custody documentation standards, and greenhouse gas accounting boundaries in ways that produce materially different certified sustainable content claims for identical physical product streams processed through different certification systems, undermining the comparability and credibility of sustainability claims across the market and creating confusion among downstream brand owner and consumer purchasers attempting to make informed sustainable procurement decisions. Regulatory scrutiny of greenwashing in chemical and materials sustainability claims is intensifying across the European Union under the Green Claims Directive, in the United States under Federal Trade Commission Green Guides enforcement, and in the United Kingdom under Competition and Markets Authority sustainability claim guidance, creating regulatory liability exposure for chemical producers and downstream users who make carbon-neutral product claims that cannot be substantiated through independently audited and methodologically rigorous lifecycle assessment and chain-of-custody documentation, adding compliance cost and legal risk to the commercial deployment of carbon-neutral petrochemical product portfolios.

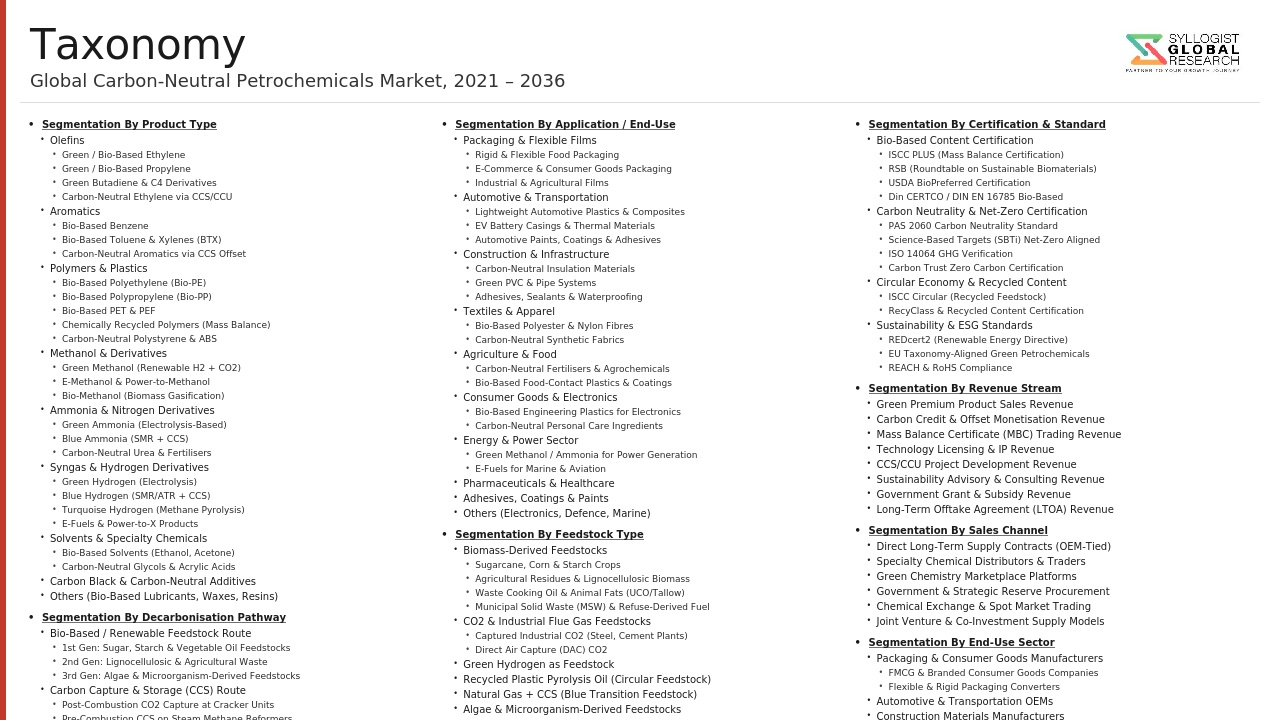

Market Segmentation

- Segmentation By Decarbonization Pathway

- Bio-Based Petrochemicals (First-Generation Sugar and Starch Feedstocks)

- Bio-Based Petrochemicals (Second-Generation Lignocellulosic Biomass)

- Bio-Based Petrochemicals (Third-Generation Algal and Waste Biomass)

- Chemically Recycled Petrochemicals (Pyrolysis-Based)

- Chemically Recycled Petrochemicals (Gasification-Based)

- Chemically Recycled Petrochemicals (Solvolysis and Depolymerization)

- Green Hydrogen-Based Chemicals (Electrolysis-Powered Synthesis)

- Carbon Dioxide-Derived Chemicals (Carbon Capture and Utilization)

- Carbon Capture and Storage-Offset Conventional Petrochemicals

- Others

- Segmentation By Product Type

- Carbon-Neutral Ethylene and Polyethylene

- Carbon-Neutral Propylene and Polypropylene

- Carbon-Neutral Benzene, Toluene, and Xylene (BTX Aromatics)

- Carbon-Neutral Polyethylene Terephthalate (PET)

- Carbon-Neutral Methanol and Derivatives

- Carbon-Neutral Ammonia and Nitrogen Fertilizer

- Carbon-Neutral Nylon and Polyamides

- Carbon-Neutral Polystyrene and Styrene Derivatives

- Carbon-Neutral Polyurethane and Isocyanates

- Carbon-Neutral Synthetic Rubber and Elastomers

- Carbon-Neutral Specialty Chemicals and Intermediates

- Others

- Segmentation By Feedstock Type

- Sugarcane and Sugar Beet

- Corn and Grain Starch

- Vegetable Oils and Fats

- Lignocellulosic Agricultural Residues

- Municipal Solid Waste and Mixed Plastic Waste

- Industrial Plastic Waste and Off-Specification Polymers

- Green Hydrogen (Renewable Electricity-Powered Electrolysis)

- Industrial Carbon Dioxide (Captured Emissions)

- Others

- Segmentation By Certification Standard

- ISCC PLUS (International Sustainability and Carbon Certification)

- REDcert2

- RSPO Mass Balance (Roundtable on Sustainable Palm Oil)

- RSB Advanced Products Standard

- Proprietary Brand Owner Chain-of-Custody Schemes

- Government-Administered Renewable Content Registries

- Others

- Segmentation By Application

- Flexible and Rigid Packaging

- Automotive Components and Interior Materials

- Construction and Building Materials

- Textiles, Fibers, and Apparel

- Consumer Electronics and Electrical Equipment

- Agricultural Films and Agrochemical Inputs

- Personal Care, Cosmetics, and Homecare Products

- Medical Devices and Pharmaceutical Packaging

- Industrial Chemicals and Process Inputs

- Others

- Segmentation By End User Industry

- Food and Beverage Packaging Manufacturers

- Automotive OEMs and Tier-1 Suppliers

- Consumer Goods and FMCG Brand Owners

- Construction and Infrastructure Developers

- Textile and Apparel Manufacturers

- Electronics and Electrical Equipment Producers

- Agriculture and Agrochemical Companies

- Pharmaceutical and Healthcare Product Manufacturers

- Others

- Segmentation By Sales Model

- Long-Term Off-Take and Supply Agreements

- Spot Market and Commodity Exchange Trading

- Direct Brand Owner Procurement Programs

- Chemical Distributor and Trader Channels

- Mass Balance Certificate (MBC) Trading Platforms

- Others

- Segmentation By Technology Readiness Level

- Commercially Deployed at Scale (TRL 9)

- Early Commercial and First-of-Kind Plants (TRL 7 to 8)

- Demonstration and Pilot Scale (TRL 5 to 6)

- Research and Development Stage (TRL 1 to 4)

- Segmentation By Region

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- Latin America

All market revenues are presented in USD

Historical Year: 2021–2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027–2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Carbon-Neutral Petrochemicals Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by decarbonization pathway, bio-based first and second generation, chemical recycling, green hydrogen-derived, carbon dioxide utilization, and carbon capture and storage-offset, and by product type, carbon-neutral ethylene, propylene, BTX aromatics, PET, methanol, and ammonia, to enable chemical producers, investors, downstream brand owners, and policy makers to identify which technology pathways and product categories will attract the largest capital flows and generate the most durable revenue growth through the forecast period?

- How are the European Union’s Carbon Border Adjustment Mechanism, the Packaging and Packaging Waste Regulation’s mandatory recycled content requirements, the Emissions Trading System carbon price trajectory toward USD 120 to USD 150 per tonne by 2030, and equivalent carbon pricing and mandatory content legislative frameworks in the United States, United Kingdom, Japan, and China expected to reshape the cost competitiveness of carbon-neutral petrochemicals relative to conventional fossil-derived alternatives on a product category and regional market basis through 2034, and at what carbon price level does each major decarbonization pathway achieve unsubsidized cost parity with its conventional fossil equivalent?

- What is the current global chemical recycling production capacity for plastic waste across pyrolysis, gasification, and solvolysis technology platforms, what additional capacity is under development or construction as of 2026, and what proportion of the mandated minimum recycled content requirements for plastic packaging under the EU Packaging and Packaging Waste Regulation and equivalent national regulations can realistically be met by certified chemical recycling output by 2030 and 2034 given current investment trajectories, technology scale-up timelines, and plastic waste feedstock collection infrastructure development rates?

- How are the fragmented mass balance accounting and carbon neutrality certification frameworks, encompassing ISCC PLUS, REDcert2, RSB, and proprietary brand owner schemes, expected to evolve toward harmonization or mutual recognition through 2034, and what is the commercial and regulatory impact of the EU Green Claims Directive’s substantiation requirements, the Federal Trade Commission’s Green Guides enforcement activity, and equivalent anti-greenwashing regulatory developments on the ability of carbon-neutral petrochemical producers and downstream users to make commercially credible and legally defensible sustainability claims in their key export and domestic markets?

- Who are the leading integrated chemical and petrochemical producers, dedicated bio-based chemical companies, chemical recycling technology developers and operators, green hydrogen producers supplying the chemical synthesis sector, and carbon capture technology providers currently defining the competitive landscape of the global carbon-neutral petrochemicals market, and what are their respective decarbonization investment programs, production capacity expansion timelines, certification portfolio strategies, key brand owner supply partnerships, geographic market priorities, and competitive positioning strategies as the market scales from its current USD 14.8 billion valuation toward the projected USD 62.4 billion by 2034?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Technology Readiness & Scalability Risk

- Carbon Accounting & Certification Risk

- Market & Commercial Risk

- Feedstock & Supply Chain Risk

- Geopolitical & Regulatory Risk

- Regulatory Framework & Standards

- Carbon Pricing & Compliance Mechanisms

- Carbon-Neutral Petrochemical Product Certification Standards

- Carbon Footprint Accounting & LCA Standards

- Green Hydrogen Regulation & Standards

- Bio-Based & Circular Feedstock Regulations

- Global Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Million Tonnes)

- Market Size & Forecast by Decarbonisation Pathway

- Power-to-X (P2X) Carbon-Neutral Petrochemicals

- Green Hydrogen + CO₂ to Methanol (e-Methanol)

- Green Hydrogen + CO₂ to Olefins via Methanol-to-Olefins (e-MTO)

- Green Hydrogen + CO₂ Fischer-Tropsch to Synthetic Naphtha

- Green Hydrogen Electrified Steam Cracking (e-Cracker)

- Green Hydrogen to Ammonia (Green Ammonia – Haber-Bosch)

- Electrochemical CO₂ Reduction to Ethylene & Ethanol

- Biogenic Feedstock-Based Carbon-Neutral Petrochemicals

- Bio-Naphtha Cracking to Bio-Based Olefins & Aromatics

- Bio-Methanol to Olefins (Bio-MTO)

- Bio-Ethanol Dehydration to Bio-Ethylene

- Biomass-to-Syngas (Gasification) Fischer-Tropsch to Bio-BTX & Bio-Naphtha

- Lignin-to-Bio-Aromatics (Bio-BTX) Production

- Bio-Based Propylene & Bio-Propylene Glycol Routes

- Carbon Capture, Utilisation & Storage (CCUS) Pathways

- CCS-Enabled Conventional Steam Cracker (Carbon-Neutral by Offset)

- CCS-Enabled Methane Reformer for Blue Hydrogen-Based Carbon-Neutral Petrochemicals

- CCU: CO₂-to-Methanol, CO₂-to-Olefins & CO₂-to-Aromatics Valorisation

- Direct Air Capture (DAC) + Green H₂ to Synthetic Petrochemicals

- Circular Carbon Petrochemicals (Chemical Recycling)

- Plastic Waste Pyrolysis Oil to Drop-In Carbon-Neutral Naphtha

- Plastic Waste Gasification Syngas to Carbon-Neutral Methanol & Olefins

- Mechanical Recycling-Enabled Carbon-Neutral Polymer Value Chain

- Solvent-Based Dissolution Recycling to Carbon-Neutral Polymer Feedstock

- Mass Balance & Certification-Based Carbon-Neutral Petrochemicals

- ISCC PLUS Mass Balance Carbon-Neutral Product Certificates

- REDcert² Mass Balance Carbon-Neutral Chemical Certificates

- Book-and-Claim Carbon-Neutral Petrochemical Attribute Certificates

- Market Size & Forecast by Product Type

- Carbon-Neutral Olefins

- Carbon-Neutral Ethylene

- Carbon-Neutral Propylene

- Carbon-Neutral Butadiene

- Carbon-Neutral Butylene / Isobutylene

- Carbon-Neutral C4 Raffinate

- Carbon-Neutral Aromatics (BTX)

- Carbon-Neutral Benzene

- Carbon-Neutral Toluene

- Carbon-Neutral Mixed Xylenes & Para-Xylene (PX)

- Carbon-Neutral Ortho-Xylene & Styrene Monomer

- Carbon-Neutral Methanol & Derivatives

- Carbon-Neutral Methanol (e-Methanol, Bio-Methanol)

- Carbon-Neutral Formaldehyde

- Carbon-Neutral Methyl Tert-Butyl Ether (MTBE)

- Carbon-Neutral Dimethyl Ether (DME)

- Carbon-Neutral Acetic Acid from Bio-Methanol

- Carbon-Neutral Syngas, Hydrogen & C1 Chemicals

- Green Hydrogen (for Petrochemical Synthesis)

- Carbon-Neutral Syngas (H₂ + CO from CO₂ + H₂O via RSOEC)

- Carbon-Neutral Carbon Monoxide (CO from CO₂ Reduction)

- Carbon-Neutral Polymers & Plastic Precursors

- Carbon-Neutral Polyethylene (PE – HDPE, LDPE, LLDPE)

- Carbon-Neutral Polypropylene (PP)

- Carbon-Neutral Polyvinyl Chloride (PVC)

- Carbon-Neutral Polystyrene (PS) & ABS

- Carbon-Neutral Polyethylene Terephthalate (PET)

- Carbon-Neutral Engineering Plastics (PA, PC, POM, PBT)

- Carbon-Neutral Nitrogen Derivatives

- Carbon-Neutral Ammonia (Green & Blue Ammonia)

- Carbon-Neutral Urea (Green Urea)

- Carbon-Neutral Nitric Acid & Nitrates

- Carbon-Neutral Ammonium Nitrate & Ammonium Sulphate

- Carbon-Neutral Chlorine & Derivatives

- Carbon-Neutral Chlorine (via Green-Powered Chlor-Alkali Electrolysis)

- Carbon-Neutral Caustic Soda (NaOH)

- Carbon-Neutral Ethylene Dichloride (EDC) & VCM

- Carbon-Neutral Solvents & Oxygenated Petrochemicals

- Carbon-Neutral Acetone & MEK

- Carbon-Neutral Propylene Oxide & Glycol

- Carbon-Neutral Ethylene Oxide & Glycol (MEG)

- Carbon-Neutral Acrylonitrile (ACN)

- Carbon-Neutral Specialty & High-Value Petrochemicals

- Carbon-Neutral Caprolactam & Cyclohexane

- Carbon-Neutral Phenol, Acetone & Bisphenol-A (BPA)

- Carbon-Neutral Adipic Acid & Nylon Precursors

- Carbon-Neutral Carbon Black & Carbon Materials

- Market Size & Forecast by Application / End-Use Industry

- Packaging & Flexible Films

- Carbon-Neutral PE & PP for Flexible Food & Beverage Packaging

- Carbon-Neutral PET for Rigid Bottle & Container Packaging

- Carbon-Neutral PS & EPS for Protective & Food Service Packaging

- Automotive & Transportation

- Carbon-Neutral Engineering Plastics for Lightweighting (PA, POM, PBT)

- Carbon-Neutral Carbon Fibre Precursors (ACN)

- Carbon-Neutral Rubber (SBR, NBR) from Carbon-Neutral Butadiene

- Carbon-Neutral Automotive Adhesives, Sealants & Coatings

- Construction & Infrastructure

- Carbon-Neutral PVC for Pipes, Profiles & Window Frames

- Carbon-Neutral EPS & XPS Insulation

- Carbon-Neutral Polyurethane (PU) Foam & Insulation

- Carbon-Neutral Construction Adhesives & Waterproofing

- Textiles, Fibres & Nonwovens

- Carbon-Neutral PET Polyester Fibre & Filament

- Carbon-Neutral Nylon (PA6, PA66) Fibre

- Carbon-Neutral Polypropylene Nonwoven Fabric

- Carbon-Neutral Elastane & Spandex (MDI / TDI)

- Agriculture & Fertilisers

- Carbon-Neutral Urea & Ammonia for Fertiliser Production

- Carbon-Neutral Agricultural Films & Greenhouse Plastics

- Carbon-Neutral Crop Protection Chemical Intermediates

- Consumer Goods, FMCG & Hygiene

- Carbon-Neutral PE & PP for Personal Care Packaging

- Carbon-Neutral Surfactant & Detergent Petrochemical Intermediates

- Carbon-Neutral ABS & PS for Appliances & Consumer Electronics

- Electronics & Electrical

- Carbon-Neutral Specialty Polymer & Engineering Plastic for PCB & Semiconductor Packaging

- Carbon-Neutral Epoxy Resin & BPA for Electrical Laminate

- Carbon-Neutral Solvents for Electronics Cleaning & Photoresist

- Energy & Clean Technology

- Carbon-Neutral Carbon Black for Battery Electrode Conductive Additive

- Carbon-Neutral Separator Polymer & Electrolyte Solvent for Li-Ion Batteries

- Carbon-Neutral Resin & Composite for Wind Turbine Blade Manufacturing

- Carbon-Neutral Polymer Membrane for Electrolysis & Fuel Cells

- Pharmaceuticals & Healthcare

- Carbon-Neutral Pharmaceutical Polymer Excipient & Packaging

- Carbon-Neutral Medical Grade PE, PP & PVC

- Carbon-Neutral Chemical Intermediate for API Synthesis

- Market Size & Forecast by Carbon Neutrality Accounting Method

- Physical Carbon-Neutral Petrochemical

- Mass Balance Allocated Carbon-Neutral Product Certificate

- Carbon Offset Compensated Carbon-Neutral Product

- Book-and-Claim Carbon-Neutral Attribute Certificate

- Carbon-Negative Petrochemical

- Market Size & Forecast by Production Scale

- Demonstration & Early Commercial Scale

- Commercial Scale

- Large Commercial Scale

- World-Scale Carbon-Neutral Petrochemical Complex

- Packaging & Flexible Films

- Carbon-Neutral Olefins

- Power-to-X (P2X) Carbon-Neutral Petrochemicals

- North America Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

- Europe Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

- Asia-Pacific Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

- Middle East & Africa Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

- Latin America Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

- Country-Wise* Carbon-Neutral Petrochemicals Market Outlook

- Market Size & Forecast

- By Value

- By Volume

- By Decarbonisation Pathway

- By Product Type

- By Application / End-Use Industry

- By Carbon Neutrality Accounting Method

- By Production Scale

- Market Size & Forecast

Countries Analyzed in the Syllogist Global Research Portfolio: United States, Canada, Germany, Netherlands, Belgium, France, United Kingdom, Norway, Sweden, Spain, Italy, Poland, Russia, Saudi Arabia, UAE, Qatar, China, Japan, South Korea, India, Singapore, Australia, Brazil, South Africa

- Carbon-Neutral Petrochemical Hub & Project Analysis

- European Carbon-Neutral Petrochemical Hubs

- North American Carbon-Neutral Petrochemical Projects

- Middle East Carbon-Neutral Petrochemical Projects

- Asia-Pacific Carbon-Neutral Petrochemical Projects

- Technology Landscape & Innovation Analysis

- Electrification of Petrochemical Processes

- Carbon Capture, Utilisation & Storage (CCUS) Technology for Petrochemicals

- Bio-Based Feedstock Technology for Carbon-Neutral Petrochemicals

- Circular Carbon Petrochemical Technology (Chemical Recycling)

- Green Hydrogen Production, Storage & Transport for Carbon-Neutral Petrochemicals

- Digital & AI Technology for Carbon-Neutral Petrochemical Operations

- Patent & IP Landscape in Carbon-Neutral Petrochemicals

- Value Chain & Supply Chain Analysis

- Renewable Energy Supply for Carbon-Neutral Petrochemicals

- Green Hydrogen Supply Chain

- Carbon Capture & CO₂ Supply Chain

- Bio-Based & Circular Feedstock Supply Chain

- Carbon-Neutral Petrochemical Production

- Carbon-Neutral Petrochemical Product Certification & Trading

- Downstream Processing & End-User Integration

- Pricing Analysis

- Carbon-Neutral Petrochemical Green Premium Analysis

- Carbon-Neutral Petrochemical Price Drivers

- Carbon-Neutral Petrochemical Price Parity Analysis

- Carbon-Neutral Attribute Certificate Pricing

- Carbon Accounting & Life Cycle Assessment Framework

- Carbon Accounting Methodologies for Carbon-Neutral Petrochemicals

- Life Cycle Assessment (LCA) of Key Carbon-Neutral Petrochemical Pathways

- Carbon Neutrality Certification & Third-Party Verification

- Additionality, Permanence & Offset Quality in Carbon-Neutral Petrochemicals

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated)

- Top 15 Players Global Carbon-Neutral Petrochemical Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Decarbonisation Pathway, Product Type & Geography

- Player Classification

- Integrated Global Petrochemical Majors Pursuing Full-Scope Carbon-Neutral Transition

- Energy Majors with Petrochemical & Carbon-Neutral Chemical Divisions

- Specialised Carbon-Neutral Petrochemical Technology Providers (e-Cracker, CCU, Bio-Feedstock)

- Chemical Recycling & Circular Carbon Petrochemical Companies

- Green Hydrogen & Power-to-X Petrochemical Developers

- Bio-Based Petrochemical Producers & Fermentation-Based Carbon-Neutral Chemical Companies

- Carbon Capture & Storage Specialists Serving Petrochemical Sector

- Certification & Carbon Accounting Service Providers for Carbon-Neutral Petrochemicals

- Competitive Analysis Frameworks

- Market Share Analysis by Product, Pathway & Geography

- Company Profile

- Company Overview & Headquarters

- Carbon-Neutral Petrochemical Product Portfolio & Decarbonisation Pathway

- Key Projects, Production Capacity & Commercial Status

- Technology IP & Patent Portfolio for Carbon-Neutral Production

- Revenue (Carbon-Neutral Chemical Segment) & Capex Commitment

- Carbon-Neutral Product Certification (ISCC PLUS, REDcert², Verified LCA)

- Key OEM & Brand Owner Customer Relationships & Offtake Agreements

- Recent Developments (Project Announcements, Partnerships, Certifications, M&A)

- SWOT Analysis

- Carbon-Neutral Petrochemical Strategy & 2030/2050 Roadmap

- Competitive Positioning Map (Decarbonisation Ambition vs. Commercial Delivery)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Output

- Market Opportunity Matrix – By Decarbonisation Pathway, Product Type & Geography

- White Space Opportunity Analysis

- Strategic Recommendations

- Technology Investment & Decarbonisation Pathway Selection Strategy

- Carbon-Neutral Product Portfolio & Commercial Strategy

- Green Hydrogen & Renewable Energy Procurement Strategy

- Carbon Accounting, Certification & Policy Engagement Strategy

- Partnership, M&A & Ecosystem Development Strategy

- Sustainability & ESG Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025–2028)

- Mid-term (2029–2032)

- Long-term (2033–2040)