Market Definition

The Global Subsea Equipment Market encompasses the design, engineering, manufacturing, installation, commissioning, inspection, maintenance, and repair of specialized hardware, systems, and technology platforms deployed on or beneath the seabed or within the water column to support the exploration, development, production, and transportation of offshore oil and natural gas resources, the installation and operation of offshore renewable energy infrastructure including floating offshore wind and wave energy, and the deployment of subsea telecommunications and data transmission cable networks. Subsea equipment is distinguished by its requirement to function reliably in an extreme operating environment characterized by hydrostatic pressures ranging from below 100 bar in shallow water continental shelf developments to over 1,000 bar in ultra-deepwater fields at depths exceeding 3,000 meters, near-freezing water temperatures of two to four degrees Celsius, corrosive seawater chemistry, marine biofouling, and complete inaccessibility for routine human inspection or intervention, demanding engineering standards of reliability, material durability, and system redundancy that substantially exceed those required for equivalent surface or onshore hydrocarbon production equipment. The market encompasses the complete subsea production and processing system portfolio including subsea wellheads and wellhead connectors, subsea trees and horizontal and vertical Christmas trees, subsea manifolds and pipeline end manifolds, subsea umbilicals carrying hydraulic control, chemical injection, and electrical power to subsea production systems, subsea production risers and flexible flowlines, subsea control systems and subsea distribution units, subsea boosting and multiphase pumping systems, subsea compression systems, subsea gas and liquid separation systems, subsea power distribution and conversion equipment, subsea connectors and jumpers, pipeline end terminations and inline structures, remotely operated vehicles for installation and intervention, autonomous underwater vehicles for inspection and survey, installation vessels and diving support vessels, and the digital monitoring, flow assurance, and integrity management systems that enable remote operation of subsea assets throughout their twenty-five to thirty-year design lifetimes. Key participants include subsea equipment original equipment manufacturers, umbilical and flexible pipe producers, installation contractors, remotely operated vehicle operators, inspection maintenance and repair service providers, and offshore oil and gas operators.

Market Insights

The global subsea equipment market was valued at approximately USD 18.6 billion in 2025 and is projected to reach USD 36.4 billion by 2034, advancing at a compound annual growth rate of 7.8% over the forecast period from 2027 to 2034, driven by the sustained deepwater and ultra-deepwater exploration and development activity in high-prolific frontier basins including the pre-salt offshore Brazil, Guyana-Suriname, Mozambique and Tanzania, East Africa, and West Africa deepwater province, the accelerating development of subsea tieback projects that maximize production from existing offshore infrastructure at lower capital cost than standalone new developments, the growing deployment of subsea processing and boosting systems that extend field economic life and improve recovery factors, and the emerging application of subsea equipment in offshore renewable energy infrastructure including subsea power export cables and floating offshore wind mooring and dynamic cable systems. Global offshore oil and gas capital expenditure reached approximately USD 195 billion in 2025, of which subsea-specific investment accounted for approximately 28% at approximately USD 54.6 billion, with deepwater projects in water depths exceeding 500 meters commanding a disproportionate subsea equipment content per dollar of total project investment relative to shallow water fixed platform developments whose simpler wellhead and riser architectures require less sophisticated subsea equipment. The order book for subsea trees, which are the most commercially tracked indicator of subsea equipment market activity, reached approximately 480 units awarded in 2025, the highest annual award level since 2013, driven by major project final investment decisions at Petrobras pre-salt developments offshore Brazil, ExxonMobil and Hess Stabroek block developments offshore Guyana, TotalEnergies Uganda Lake Albert tie-in and Mozambique Coral FLNG Phase 2, and an active pipeline of North Sea late-life tieback developments connecting satellite fields to existing infrastructure at costs competitive with greenfield alternatives even in a carbon-constrained investment environment.

The deepwater and ultra-deepwater segment constitutes the dominant and highest-growth component of the global subsea equipment market, accounting for approximately 62% of total market revenue in 2025, anchored by the extraordinary productivity and low finding and development cost per barrel of the pre-salt offshore Brazil basins where Petrobras has discovered and is developing multiple giant fields with recoverable resources exceeding 50 billion barrels of oil equivalent across the Santos and Campos Basin pre-salt polygon, and the Stabroek block offshore Guyana where ExxonMobil has announced over 30 discoveries since 2015 with gross recoverable resources estimated at over 11 billion barrels of oil equivalent, collectively driving sustained subsea equipment demand across subsea trees, manifolds, umbilicals, flexible flowlines, subsea boosters, and floating production storage and offloading vessel subsea systems that represent individually substantial procurement programs measured in hundreds of millions to several billion dollars per project phase. The subsea tieback development model, in which new satellite discoveries are connected to existing host facilities using long-distance subsea flowlines, umbilicals, and boosting systems rather than developing standalone production facilities, is gaining commercial traction across the North Sea, Gulf of Mexico, and West Africa deepwater where host infrastructure networks create tieback development economics with lower capital expenditure and shorter time-to-first-production that are financially superior to standalone development for discoveries below 100 million barrels of oil equivalent recoverable resources, with North Sea tieback development spending projected to reach approximately USD 8.4 billion annually by 2028 as an aging field infrastructure base with spare processing capacity creates a compelling economic environment for satellite tieback investment. The increasing tieback step-out distances enabled by advances in subsea processing including subsea multiphase boosting, subsea gas compression, and subsea water separation and injection are extending the economic reach of tieback development to satellite fields located 50 to 150 kilometers from host facilities that were previously beyond tieback feasibility, substantially expanding the addressable development opportunity available to tieback equipment providers.

The subsea processing and production optimization equipment segment, encompassing subsea multiphase boosting pumps, subsea gas compression trains, subsea water separation and injection systems, and subsea chemical injection systems, represents the highest unit-value and most technically sophisticated component category within the global subsea equipment market, growing at approximately 12.4% annually in 2025 as operators recognize that subsea processing can substantially extend the productive life of mature offshore fields by maintaining wellhead pressures above minimum lift requirements as reservoir pressure declines, separate and reinject produced water subsea rather than processing it topside, and enable economic development of low-pressure reservoir accumulations that would not produce naturally at commercial flow rates without downhole pressure augmentation. Equinor’s Askeladd and Midgard field developments on the Norwegian continental shelf, where long-distance subsea gas compression systems deliver incremental recovery of approximately 300 million barrels of oil equivalent that would be unrecoverable without subsea boosting, demonstrate the transformative impact of subsea processing technology on field economics and provide commercially validated reference cases for subsea processing adoption at other mature offshore provinces including the Gulf of Mexico, Brazilian deepwater, and West African deepwater where declining reservoir pressure in producing fields creates similar incremental production recovery opportunities that justify subsea processing capital investment. The integration of digital twins, fiber optic distributed sensing along subsea production flowlines, and machine learning-based flow assurance modeling into subsea production system operations is creating a new layer of intelligent monitoring and optimization capability that enables operators to predict hydrate, wax, and scale deposition events in subsea flowlines, optimize chemical injection dosing in real time, and detect early-stage equipment degradation through continuous vibration and acoustic emission monitoring that substantially reduces unplanned production downtime and extends the maintenance interval of subsea equipment requiring expensive remotely operated vehicle intervention.

The subsea equipment market is experiencing an increasingly important demand dimension from offshore renewable energy infrastructure, with floating offshore wind technology creating novel subsea equipment requirements including dynamic power export cables, mooring systems using chain, wire, and synthetic fiber rope for semi-submersible and tension leg platform wind turbine foundation designs, subsea power cable protection systems, subsea high-voltage alternating and direct current connectors, and inter-array cable systems that must withstand dynamic loading from the continuous motion of floating structures and the fatigue-inducing wave and current environment of deep and intermediate water depth deployment locations. The global floating offshore wind installation pipeline is projected to require approximately USD 12.4 billion of subsea cable, connector, and mooring equipment through 2034 as projects in Scotland, Norway, Portugal, Japan, South Korea, and the United States advance from demonstration scale toward commercial array deployment at water depths of 60 to 1,000 meters that exceed the monopile installation depth limits of conventional bottom-fixed offshore wind technology. The competitive landscape of the global subsea equipment market is concentrated among a small number of large integrated equipment manufacturers and service providers including TechnipFMC, Subsea 7, Saipem, Baker Hughes, OneSubsea, Aker Solutions, and SLB whose combined revenue represents approximately 65% of total subsea equipment and service market value and whose scale, technology portfolios, installed base relationships, and global installation vessel assets create significant barriers to entry for new competitors seeking to address the most technically demanding deepwater and ultra-deepwater project segments.

Key Drivers

Pre-Salt Brazil and Guyana Deepwater Giant Field Development Programs Generating Multi-Billion-Dollar Annual Subsea Equipment Procurement Cycles Through the Forecast Period

The ongoing and expanding development of the pre-salt offshore Brazil and Guyana deepwater oil provinces, whose combined recoverable resource base of approximately 60 billion barrels of oil equivalent exceeds that of any other offshore basin currently under active development globally, is generating a sustained and multi-decade subsea equipment procurement cycle that provides the most commercially significant structural demand driver for the global subsea equipment market through the forecast period as Petrobras, ExxonMobil, Hess, Shell, TotalEnergies, and their joint venture partners execute sequential project final investment decisions across multiple giant field developments requiring complete subsea production system installations at water depths of 1,800 to 3,000 meters. Petrobras’s five-year investment plan allocates approximately USD 73 billion to offshore exploration and production through 2029, of which approximately 65% is directed at pre-salt development projects whose subsea equipment content per billion dollars of total project investment is among the highest in the global offshore industry given the full-field subsea architecture, long-distance flexible flowlines and umbilicals connecting wells to floating production units, and subsea boosting requirements at water depths and tieback distances that preclude conventional fixed platform development. The Stabroek block offshore Guyana, operated by ExxonMobil with Hess and CNOOC as co-venturers, has sanctioned five floating production storage and offloading vessel developments including Liza Phase 1 and 2, Payara, Yellowtail, and Hammerhead at aggregate peak production capacity exceeding 900,000 barrels per day, with each vessel requiring a complete subsea production system comprising subsea trees, manifolds, umbilicals, flowlines, and subsea control systems representing subsea equipment content of approximately USD 1.5 to USD 2.8 billion per floating production storage and offloading development phase and creating a highly concentrated subsea equipment order flow from a single basin that is sustaining supplier manufacturing capacity utilization and limiting the competitive bidding pressure that constrained subsea equipment pricing during the oil price downturn of 2015 to 2020.

Mature Offshore Basin Life Extension, Subsea Tieback Economics, and Production Enhancement Investment Sustaining Subsea Equipment Demand Independent of Greenfield Project Cycles

The increasing economic attractiveness of subsea tieback developments connecting satellite discoveries to existing offshore infrastructure as an alternative to standalone greenfield project sanctioning in mature offshore basins including the North Sea, Gulf of Mexico, and West Africa is sustaining a structural baseline of subsea equipment procurement activity that is partially independent of the volatile large greenfield project sanction cycle and provides subsea equipment manufacturers with a more predictable volume of tieback-specific orders for subsea trees, flowlines, umbilicals, subsea control systems, and boosting equipment. The North Sea’s approximately 350 producing offshore platforms provide an established infrastructure host network whose spare processing capacity and remaining field life create a persistent economic case for tieback development of satellite discoveries and undeveloped segments of existing fields, with the United Kingdom North Sea Transition Authority tracking over 200 subsea tieback development opportunities with combined contingent resources exceeding 5 billion barrels of oil equivalent whose development decisions represent a substantial and multiyear order pipeline for subsea equipment suppliers. Mature field production enhancement investment, including subsea multiphase boosting system retrofits at declining fields, subsea water injection system installations to maintain reservoir pressure, subsea flowline inspection and remediation programs, and chemical injection system upgrades to manage hydrate and scale deposition in aging flowlines, is generating aftermarket and brownfield subsea equipment demand estimated at approximately USD 6.2 billion annually in 2025 that is growing at approximately 9.8% per year as the global inventory of subsea-completed wells, now exceeding 8,500 subsea trees on the seabed globally, requires increasing levels of inspection, maintenance, repair, and production optimization investment to maintain commercial production rates through their extended operating lives.

Offshore Energy Transition Opportunities Including Subsea Carbon Storage Infrastructure, Floating Offshore Wind Power Export Systems, and Subsea Hydrogen Transport Creating New Equipment Demand Categories

The offshore environment is emerging as a critical enabler of multiple dimensions of the global energy transition, creating new and structurally growing demand for subsea equipment beyond conventional oil and gas applications as carbon capture and storage projects inject supercritical carbon dioxide into depleted offshore reservoirs through subsea injection infrastructure, floating offshore wind farms export power to shore through subsea high-voltage cable systems, offshore green hydrogen production pilots connect to mainland infrastructure through subsea hydrogen pipeline systems, and offshore renewable energy and oil and gas hybrid infrastructure development creates novel subsea equipment integration requirements that extend the addressable market for subsea engineering and equipment capabilities into energy transition technology segments. Carbon capture and storage projects utilizing offshore geological formations for carbon dioxide storage, including the Northern Lights project in Norway whose subsea injection infrastructure for receiving and injecting captured industrial carbon dioxide into the Johansen formation represents the first commercial offshore carbon storage project globally, require subsea wellheads, subsea trees, subsea manifolds, and injection umbilicals engineered for carbon dioxide service conditions whose material compatibility, seal performance, and corrosion protection requirements differ from conventional hydrocarbon production applications and are creating a new equipment qualification and development program at established subsea equipment manufacturers. The United Kingdom’s planned offshore carbon storage hub developments including Acorn, HyNet North Sea, and Viking CCS, Norway’s Northern Lights Phase 2 expansion, and the Netherlands’s Porthos project collectively represent an emerging pipeline of subsea carbon injection infrastructure investment valued at approximately USD 4.8 billion through 2034 that is creating the first commercial market for offshore carbon dioxide injection subsea equipment alongside an active technology qualification program developing the material specifications, pressure ratings, and leak integrity standards appropriate for permanent offshore carbon dioxide containment applications.

Key Challenges

Supply Chain Capacity Constraints, Skilled Workforce Shortages, and Lead Time Extensions for Critical Subsea Equipment Components Creating Project Schedule Risk

The rapid recovery and acceleration of global offshore investment following the capital expenditure downturn of 2015 to 2020 has outpaced the recovery of subsea equipment supply chain capacity, creating extended manufacturing lead times, constrained fabrication yard scheduling, and specialized workforce shortages that are generating project schedule risk and cost escalation for operators seeking to execute multiple simultaneous deepwater developments whose subsea equipment procurement timelines are critical path activities for first oil delivery. Subsea tree manufacturing lead times have extended from approximately 18 to 24 months in the 2019 to 2022 period to approximately 30 to 42 months in 2025 for complex ultra-deepwater configurations requiring extensive material qualification, subsea control system integration, and factory acceptance testing, with the limited number of qualified subsea tree manufacturing facilities globally at Baker Hughes, TechnipFMC, OneSubsea, and Aker Solutions creating a concentrated supply bottleneck whose expansion requires three to five years of capital investment and workforce training before additional certified manufacturing capacity is available to the market. The offshore installation vessel fleet, which includes specialized pipelaying vessels, flexible pipelaying ships, and heavy-lift crane vessels required for subsea infrastructure installation and which contracted to severely during the 2015 to 2020 period with multiple vessels retired or converted, faces a capacity constraint that is manifesting as vessel charter rate escalation and schedule availability challenges for projects requiring specific vessel capabilities including ultra-deepwater flexible pipelaying and heavy subsea lift that only a limited number of vessels globally are equipped to perform, with vessel charter rates for specialized deepwater pipelaying and installation vessels increasing by approximately 35% to 55% between 2022 and 2025 as demand recovery from Brazil, Guyana, and West Africa simultaneously competes for scarce installation capacity.

Extreme Water Depth and High-Pressure High-Temperature Reservoir Conditions Pushing Equipment Performance Boundaries and Requiring Extensive Technology Qualification Programs

The frontier deepwater developments entering the global project pipeline increasingly involve water depths exceeding 2,500 meters, reservoir pressures above 1,000 bar, and reservoir temperatures exceeding 150 to 200 degrees Celsius in high-pressure high-temperature reservoir settings that approach or exceed the design envelope of currently qualified subsea equipment generations, requiring extensive new technology qualification programs that add three to five years and hundreds of millions of dollars of development cost to the project timeline and budget of operators seeking to deploy subsea production systems in the most technically challenging frontier environments. Ultra-deepwater hydrostatic pressure at 3,000 meter water depth of approximately 300 bar imposes extreme requirements on subsea wellhead and tree pressure containment, connector sealing integrity, hydraulic control line working pressure, and umbilical collapse resistance that require metallurgical material upgrades to super duplex stainless steel and high-nickel alloy grades, thickened pressure vessel wall designs, and enhanced connector locking mechanisms that significantly increase subsea equipment unit cost and weight compared to conventional deepwater specifications, with ultra-deepwater subsea tree prices reaching approximately USD 12 to USD 18 million per unit compared to USD 4 to USD 8 million for conventional deepwater trees. High-pressure high-temperature subsea completions in reservoirs where static pressure exceeds 1,035 bar and temperature exceeds 177 degrees Celsius, as encountered in emerging deepwater developments in the Gulf of Mexico, North Sea, and offshore Namibia, require complete redesign of elastomeric seal materials, hydraulic fluid formulations, electrical penetrator designs, and valve actuator mechanisms whose performance has not been validated at these extreme conditions, with industry qualification programs coordinated through the subsea equipment industry consortium requiring three to seven years to complete and delaying commercial deployment of these reservoir development opportunities.

Energy Transition Headwinds, Carbon Emission Intensity of Offshore Operations, and Lender ESG Requirements Creating Financing and Social License Complexity for Deepwater Projects

Deepwater oil and gas development projects face increasing financing complexity arising from the intersection of energy transition policy pressure, institutional lender environmental, social, and governance requirements, and the carbon emission intensity of offshore floating production operations that is drawing regulatory and investor scrutiny in major capital markets, with multiple international banks having adopted policies restricting project finance lending to new offshore oil and gas developments that do not demonstrate Paris Agreement alignment or integration with host country net-zero transition plans. The carbon emission footprint of offshore production platforms, which can emit 50 to 150 kilograms of carbon dioxide equivalent per barrel of oil produced from diesel and gas turbine power generation, flaring, and process venting, is subject to progressive regulatory tightening under the Norwegian carbon tax, UK Emissions Trading Scheme offshore sector inclusion, and the European Union Offshore Petroleum Emissions Directive that increases the operating cost of carbon-intensive offshore facilities and incentivizes electrification of offshore platforms from shore-based renewable power through subsea power transmission cables. The long-term demand uncertainty for deepwater oil production over the twenty-five to thirty-year operating life of subsea infrastructure investments creates portfolio allocation challenges for both oil company operators and their equipment suppliers, as scenario planning under accelerated energy transition assumptions projects peak oil demand in the mid-2020s to late 2020s followed by structural decline that introduces financial obsolescence risk for deepwater infrastructure sanctioned today on the basis of sustained production into the 2050s, complicating the board-level approval and lender credit assessment processes for multi-billion-dollar deepwater project commitments whose economics depend on production revenue streams whose long-term price trajectory is subject to unprecedented policy and technology uncertainty.

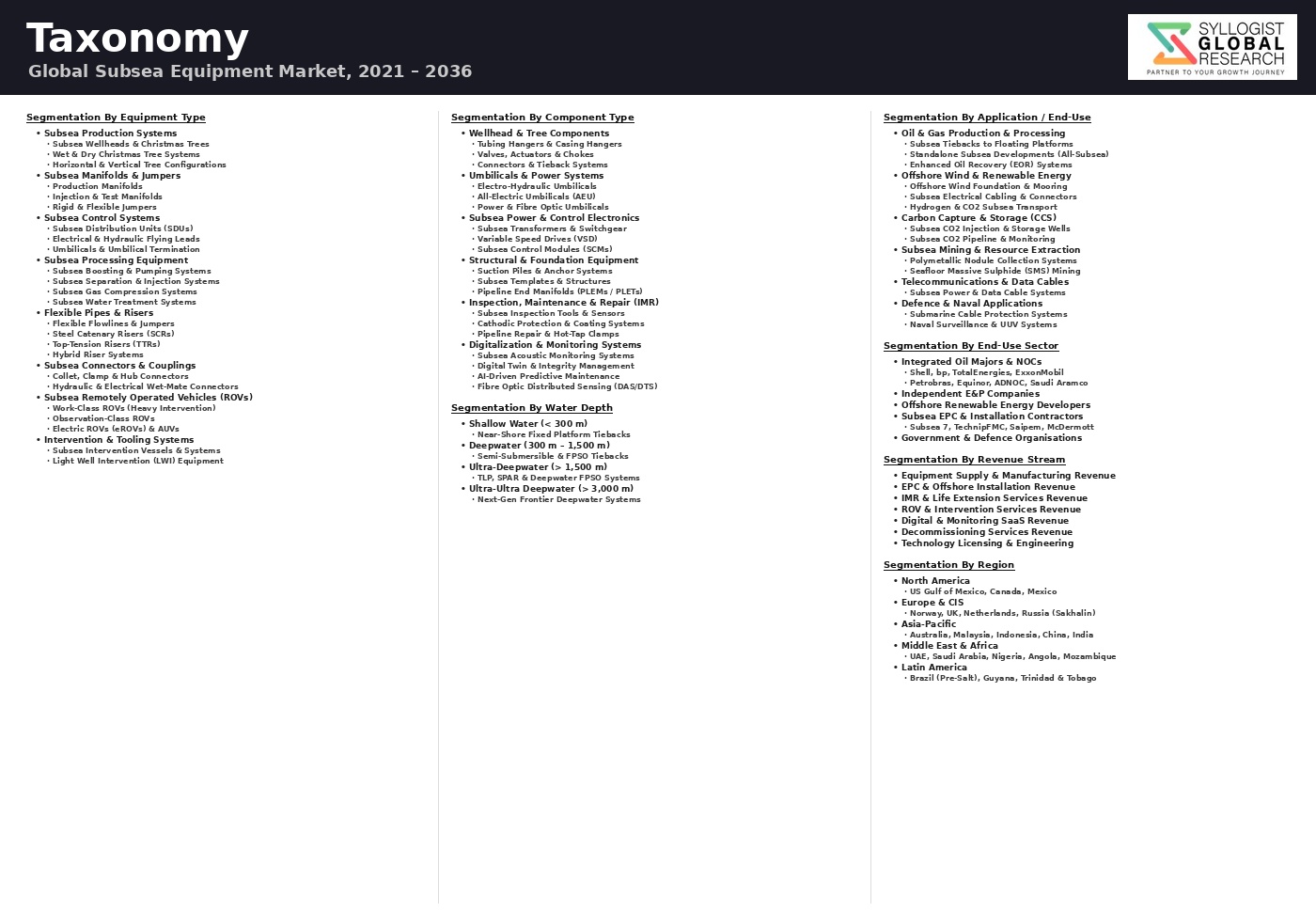

Market Segmentation

- Segmentation By Equipment Type

- Subsea Trees (Horizontal and Vertical Christmas Trees)

- Subsea Wellheads and Wellhead Connectors

- Subsea Manifolds and Pipeline End Manifolds (PLEMs)

- Umbilicals (Hydraulic, Electrical, and Hybrid)

- Flexible Flowlines, Risers, and Jumpers

- Rigid Pipelines and Subsea Pipe-in-Pipe Systems

- Subsea Control Systems and Subsea Distribution Units (SDUs)

- Subsea Processing Systems (Boosting, Compression, and Separation)

- Subsea Power Systems and Electrical Distribution

- Remotely Operated Vehicles (ROVs) and Autonomous Underwater Vehicles (AUVs)

- Subsea Connectors, Pipeline End Terminations (PLETs), and Inline Structures

- Installation and Construction Vessels

- Others

- Segmentation By Water Depth

- Shallow Water (Below 300 Meters)

- Deepwater (300 to 1,500 Meters)

- Ultra-Deepwater (1,500 to 3,000 Meters)

- Frontier Deepwater (Above 3,000 Meters)

- Segmentation By Application

- Subsea Oil and Gas Production and Processing

- Subsea Tieback Developments

- Subsea Well Intervention and Workover

- Pipeline and Flowline Installation and Repair

- Subsea Inspection, Maintenance, and Repair (IMR)

- Offshore Carbon Capture and Storage (CCS) Injection Infrastructure

- Floating Offshore Wind Mooring and Power Export Cables

- Subsea Telecommunications Cable Systems

- Others

- Segmentation By Service Type

- Engineering, Procurement, and Construction (EPC)

- Equipment Supply and Manufacturing

- Installation and Commissioning Services

- Inspection, Maintenance, and Repair (IMR) Services

- Subsea Integrity Management and Digital Monitoring

- Decommissioning Services

- Others

- Segmentation By End User

- International Oil Companies (IOCs)

- National Oil Companies (NOCs)

- Independent Exploration and Production Companies

- Offshore Renewable Energy Developers

- Carbon Storage Project Operators

- Subsea Telecommunications Cable Operators

- Others

- Segmentation By Region

- North America (Gulf of Mexico)

- Europe (North Sea, Norwegian Continental Shelf, and Atlantic Margin)

- Asia-Pacific (Southeast Asia, Australia, and India)

- Latin America (Brazil, Guyana, and Trinidad)

- Middle East and Africa (West Africa, East Africa, and Arabian Gulf)

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total global market valuation of the Subsea Equipment Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by equipment type including subsea trees, wellheads, manifolds, umbilicals, flexible flowlines, subsea control systems, subsea processing systems, remotely operated vehicles, and installation vessels, by water depth including shallow water, deepwater, ultra-deepwater, and frontier deepwater, and by application including offshore oil and gas production, subsea tiebacks, subsea processing, inspection maintenance and repair, carbon storage injection, floating offshore wind, and telecommunications, to enable equipment manufacturers, installation contractors, offshore operators, subsea engineering firms, infrastructure investors, and energy transition project developers to identify the highest-growth equipment categories and geographic markets generating the most commercially durable demand trajectories across the forecast period to 2034?

- What is the aggregate subsea equipment procurement pipeline value, project final investment decision timeline, subsea system architecture, water depth, and tieback distance of the major deepwater and ultra-deepwater development projects currently advancing toward sanction across pre-salt offshore Brazil including the Petrobras five-year plan projects, the Stabroek block Guyana developments including Yellowtail, Hammerhead, and subsequent phases, TotalEnergies Mozambique Coral FLNG Phase 2, and West Africa deepwater projects in Angola, Nigeria, and Namibia, and how are the combined subsea equipment procurement requirements of these projects determining manufacturing lead times, installation vessel scheduling, and subcomponent supply chain capacity utilization at subsea tree, umbilical, flexible pipe, and subsea control system manufacturers through 2034?

- How are subsea processing technologies including multiphase boosting, subsea gas compression, subsea water separation, and subsea chemical injection creating economically viable development cases for satellite discoveries and declining fields at tieback distances of 50 to 150 kilometers from existing host infrastructure, what are the incremental recovery volumes, capital expenditure requirements, production uplift economics, and payback period benchmarks demonstrated at reference projects including Equinor Askeladd and Midgard subsea compression in Norway, and how are these validated economics driving the specification and procurement of subsea processing systems within the North Sea, Gulf of Mexico, and Brazilian deepwater tieback development pipelines through 2034 as declining reservoir pressure in mature producing fields creates growing installed base opportunities for subsea production enhancement equipment?

- What is the current fleet capacity, vessel charter rate trajectory, new build order book, and geographic deployment distribution of specialized subsea installation vessels including deepwater flexible pipelaying ships, rigid pipelaying vessels, heavy-lift crane vessels, and remotely operated vehicle support vessels, and how is the documented 35% to 55% increase in specialized vessel charter rates between 2022 and 2025 driven by concurrent demand from Brazil, Guyana, and West Africa affecting project economics, installation schedule risk, and offshore operator contracting strategies for upcoming deepwater campaign execution, and what new installation vessel construction programs are being advanced by Subsea 7, Saipem, and other installation contractors to address the vessel capacity constraint that represents a critical delivery risk for the growing deepwater project pipeline through 2034?

- How are subsea equipment manufacturers, offshore operators, installation contractors, and energy transition project developers adapting their technology qualification programs, material selection strategies, equipment design standards, and project development approaches to address the combined challenges of extreme high-pressure high-temperature reservoir conditions in frontier deepwater fields requiring equipment qualification beyond current certified envelopes, the growing demand for subsea carbon dioxide injection equipment for offshore carbon capture and storage projects, the floating offshore wind mooring and dynamic cable requirements at intermediate water depths of 60 to 1,000 meters, and the institutional lender environmental, social, and governance requirements and carbon pricing frameworks that are reshaping the financial viability and social license assessment of new deepwater oil and gas development project sanctions through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Oil & Gas Price Volatility & Upstream Capex Cycle Risk Impacting Subsea Equipment Demand

- Deepwater Project Sanction, FID Delay & Operator Capital Allocation Risk

- Technology Qualification, Reliability & Subsea Equipment Failure in Harsh Environment Risk

- Supply Chain Concentration, Long Lead Item & Specialised Material Availability Risk

- Energy Transition, Portfolio Divestment & Stranded Subsea Asset Risk

- Regulatory Framework & Standards

- API & ISO Subsea Equipment Standards: API 17D (Subsea Wellhead & Christmas Tree), API 17E (Umbilicals), API 17F (Subsea Control Systems), API 17G (Well Intervention), ISO 13628 Series

- Offshore Safety Regulation & Well Integrity: Offshore Safety Directive (EU 2013/30/EU), UK OPRED Offshore Installation Regulations, BSEE Regulations (US), NORSOK Standard Series (Norway)

- Subsea Pipeline & Riser Design Standards: DNV-ST-F101 (Submarine Pipeline Systems), ASME B31.4, B31.8 & DNVGL-ST-F201 Riser Standard

- Environmental Regulation for Offshore Operations: MARPOL, OSPAR Convention, HELCOM, IMO Ballast Water Management & National EIA Requirements for Subsea Infrastructure Projects

- Classification Society Requirements & Certification: DNV, Lloyd’s Register, Bureau Veritas, ABS & ClassNK Type Approval & In-Service Inspection Requirements for Subsea Equipment

- Global Subsea Equipment Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Supplied & Installed)

- Market Size & Forecast by Equipment Type

- Subsea Wellheads & Wellhead Equipment

- Subsea Christmas Trees (Vertical, Horizontal & Compact Tree)

- Subsea Manifolds, Pipeline End Manifolds (PLEMs) & Pipeline End Terminations (PLETs)

- Subsea Control Systems (SCS), Umbilicals & Flying Leads

- Subsea Distribution Units (SDUs), Jumpers & Flexjoints

- Flexible Risers, Flexible Flowlines & Umbilical Termination Assemblies

- Rigid Risers: Top Tensioned Riser (TTR), Steel Catenary Riser (SCR) & Hybrid Riser

- Subsea Processing Systems: Pumps, Compressors & Separation Modules

- Subsea Power Distribution & Long-Distance Subsea Power Cable Infrastructure

- Remotely Operated Vehicles (ROVs): Work Class, Observation & Trenching ROV

- Autonomous Underwater Vehicles (AUVs) & Uncrewed Underwater Systems

- Subsea Connectors, Couplings, Clamps, Valves & Choke Systems

- Market Size & Forecast by Application

- Offshore Oil & Gas Exploration & Production: Deepwater & Ultra-Deepwater Development

- Offshore Wind: Subsea Inter-Array Cable, Export Cable & Foundation Subsea Interface

- Subsea Carbon Capture & Storage (CCS): CO2 Injection Well & Pipeline Infrastructure

- Subsea Mining & Polymetallic Nodule Resource Extraction

- Submarine Telecommunications Cable: Laying, Repair & Protection Equipment

- Marine Scientific Research, Oceanographic Survey & Defence Subsea Systems

- Market Size & Forecast by Water Depth

- Shallow Water (Up to 500m)

- Deepwater (500m to 1,500m)

- Ultra-Deepwater (1,500m to 3,000m)

- Beyond Ultra-Deepwater (Above 3,000m)

- Market Size & Forecast by Operation Type

- Drilling & Well Completion Equipment Supply

- Field Development & Installation (Greenfield & Brownfield)

- Production & Processing (Life-of-Field Equipment)

- Inspection, Maintenance & Repair (IMR)

- Well Intervention & Workover

- Decommissioning & Removal

- Market Size & Forecast by Material

- Duplex & Super Duplex Stainless Steel

- Low Alloy Carbon Steel with Corrosion Inhibition & Coating

- Titanium & High-Performance Nickel Alloys

- Thermoplastic Composite Pipe (TCP) & Reinforced Thermoplastic Pipe (RTP)

- Polymers, Elastomers & Advanced Sealing Materials

- Market Size & Forecast by End-User

- International Oil Company (IOC) & Major Integrated Energy Company

- National Oil Company (NOC) & State Energy Enterprise

- Independent E&P Operator & Deepwater Specialist

- Offshore Wind Developer & Renewable Energy Operator

- Subsea EPCI Contractor & Offshore Service Company

- Government, Defence & Oceanographic Research Organisation

- Market Size & Forecast by Sales Channel

- Direct OEM Supply to Operator (Long-Term Frame Agreement & Preferred Supplier Contract)

- EPCI & Offshore Contractor Procurement Channel

- Aftermarket, Spare Parts, Overhaul & Life Extension Service

- Technology Licensing, Joint Development Agreement & Engineering Service Channel

- North America Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Europe Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Asia-Pacific Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Latin America Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Middle East & Africa Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Subsea Equipment Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Supplied & Installed)

- By Equipment Type

- By Application

- By Water Depth

- By Operation Type

- By Material

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: United States, Mexico, Brazil, Norway, United Kingdom, Netherlands, France, Italy, Angola, Nigeria, Mozambique, Saudi Arabia, UAE, Qatar, Kuwait, Australia, Malaysia, Indonesia, India, China, Egypt, Guyana, Argentina

- Technology Landscape & Innovation Analysis

- Subsea Christmas Tree & Wellhead Architecture Technology Deep-Dive

- Subsea Control System (SCS), All-Electric Subsea & Long-Distance Tie-Back Control Technology

- Subsea Processing, Multiphase Boosting, Separation & Compression Technology

- ROV, AUV, Resident Subsea Drone & Autonomous Inspection Technology

- Flexible Pipe, Flexible Riser, Thermoplastic Composite Pipe & Dynamic Flowline Technology

- Subsea Power Distribution, High-Voltage Subsea Cable & Long-Distance Electrical Infrastructure Technology

- Digital Twin, Condition Monitoring, Subsea Asset Integrity Management & Predictive Maintenance Technology

- Patent & IP Landscape in Subsea Equipment Technologies

- Value Chain & Supply Chain Analysis

- Raw Material & Specialised Alloy Supply Chain: Duplex Steel, Titanium, Nickel Alloy Forgings & Composite Pipe Material

- Subsea Equipment Component Manufacturing Supply Chain: Forged Body, Actuator, Seal & Connector Supplier

- Subsea Control System, Umbilical & Electrical Component Manufacturing Supply Chain

- Tier-1 Subsea Equipment OEM & System Integrator Landscape

- EPCI Contractor, Offshore Installation Vessel Operator & Marine Service Provider

- Operator & End-User Project Procurement, FAT, Commissioning & Ongoing Support

- Aftermarket Service, Refurbishment, Life Extension, Plug & Abandonment

- Pricing Analysis

- Subsea Christmas Tree Average Selling Price Analysis by Tree Type, Pressure Rating & Water Depth

- Subsea Manifold & Pipeline End Manifold (PLEM) Pricing Analysis by Slot Count & Complexity

- Flexible Riser & Flexible Flowline Pricing per Metre by Bore Diameter & Pressure Rating

- Subsea Umbilical Pricing per Metre by Conductor Count, Fibre Optic Content & Depth Rating

- ROV & AUV Capital Equipment & Day-Rate Service Pricing Analysis by Vehicle Class

- Total Subsea Field Development Cost Analysis: Equipment, Installation & Life-of-Field Service per Development Concept

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Subsea Equipment: Carbon Footprint of Manufacture, Installation, Operation & Decommissioning

- Subsea Leak Prevention, Spill Risk Reduction & Pipeline Integrity Contribution to Offshore Environmental Protection

- Decommissioning & End-of-Life Material Recovery: Subsea Steel & Alloy Recycling, Platform Removal & Seabed Restoration

- Subsea Equipment Role in Offshore Wind & CCS Infrastructure: Enabling Net Zero Energy Systems

- Regulatory-Driven Sustainability: OSPAR Decommissioning Guidance, IMO Guidelines, Operator HSSE Target & ESG Disclosure for Subsea Equipment Manufacturers

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Equipment Type & Application)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Equipment Type, Application & Geography

- Player Classification

- Global Integrated Subsea Equipment & Systems OEMs (Full Portfolio Providers)

- Specialist Subsea Christmas Tree & Wellhead Equipment Manufacturers

- Flexible Pipe, Riser & Umbilical Specialist Manufacturers

- Subsea Control System & All-Electric Subsea Technology Providers

- ROV & AUV Manufacturer, Operator & Autonomous Inspection Technology Company

- Subsea Processing, Boosting & Compression Technology Specialists

- Subsea Connector, Valve, Choke & Specialty Component Manufacturers

- EPCI Contractor & Offshore Service Company with Subsea Equipment Installation Capability

- Competitive Analysis Frameworks

- Market Share Analysis by Equipment Type, Application & Region

- Company Profile

- Company Overview & Headquarters

- Subsea Equipment Products & Technology Portfolio

- Key Operator Customer Relationships & Reference Field Installations

- Manufacturing Footprint & Production Capacity

- Revenue (Subsea Equipment Segment) & Backlog

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Awards, Capacity Expansion, Product Launches)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Technology Landscape & Innovation Analysis

- Strategic Output

- Market Opportunity Matrix: By Equipment Type, Application, Water Depth, Operation Type & Geography

- White Space Opportunity Analysis

- Strategic Output

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & Operator Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)