Market Definition

The Europe Soil Health Monitoring Technologies Market encompasses the development, manufacturing, deployment, and servicing of sensor systems, analytical instruments, remote sensing platforms, digital data management solutions, and integrated decision-support tools used to measure, track, and interpret the physical, chemical, biological, and hydrological properties of agricultural and non-agricultural soils across European farmland, forestry land, protected natural areas, and urban green infrastructure. Soil health monitoring technologies enable farmers, land managers, agronomists, government agencies, environmental consultants, and scientific research institutions to assess soil condition across key indicator parameters including soil organic carbon content, microbial biomass and biodiversity, nutrient availability and cycling rates, pH, electrical conductivity, bulk density, aggregate stability, water holding capacity, compaction depth, erosion susceptibility, and contamination levels from heavy metals, pesticide residues, and industrial pollutants.

The market encompasses in-situ soil sensor technologies including electrochemical sensors, dielectric soil moisture probes, ion-selective electrodes, and optical reflectance sensors deployed at field level for continuous or periodic soil condition measurement; laboratory-based analytical services including near-infrared spectroscopy, X-ray fluorescence, DNA metabarcoding for soil biological analysis, and inductively coupled plasma mass spectrometry for trace element quantification; proximal soil sensing platforms including on-the-go sensor arrays mounted on agricultural vehicles for high-resolution field-scale soil mapping; remote sensing technologies including satellite multispectral and hyperspectral imagery, aerial drone platforms, and airborne LiDAR systems providing landscape-scale soil surface condition assessment; and digital agriculture platforms incorporating soil health data streams alongside weather, crop, and management data to generate precision agriculture recommendations and carbon accounting outputs. Key participants include precision agriculture technology companies, environmental monitoring instrument manufacturers, satellite earth observation providers, agricultural advisory and laboratory testing service companies, agrochemical and crop science corporations integrating soil health into digital farming ecosystems, and European government agencies administering soil monitoring programs under the Common Agricultural Policy and the forthcoming EU Soil Monitoring Law.

Market Insights

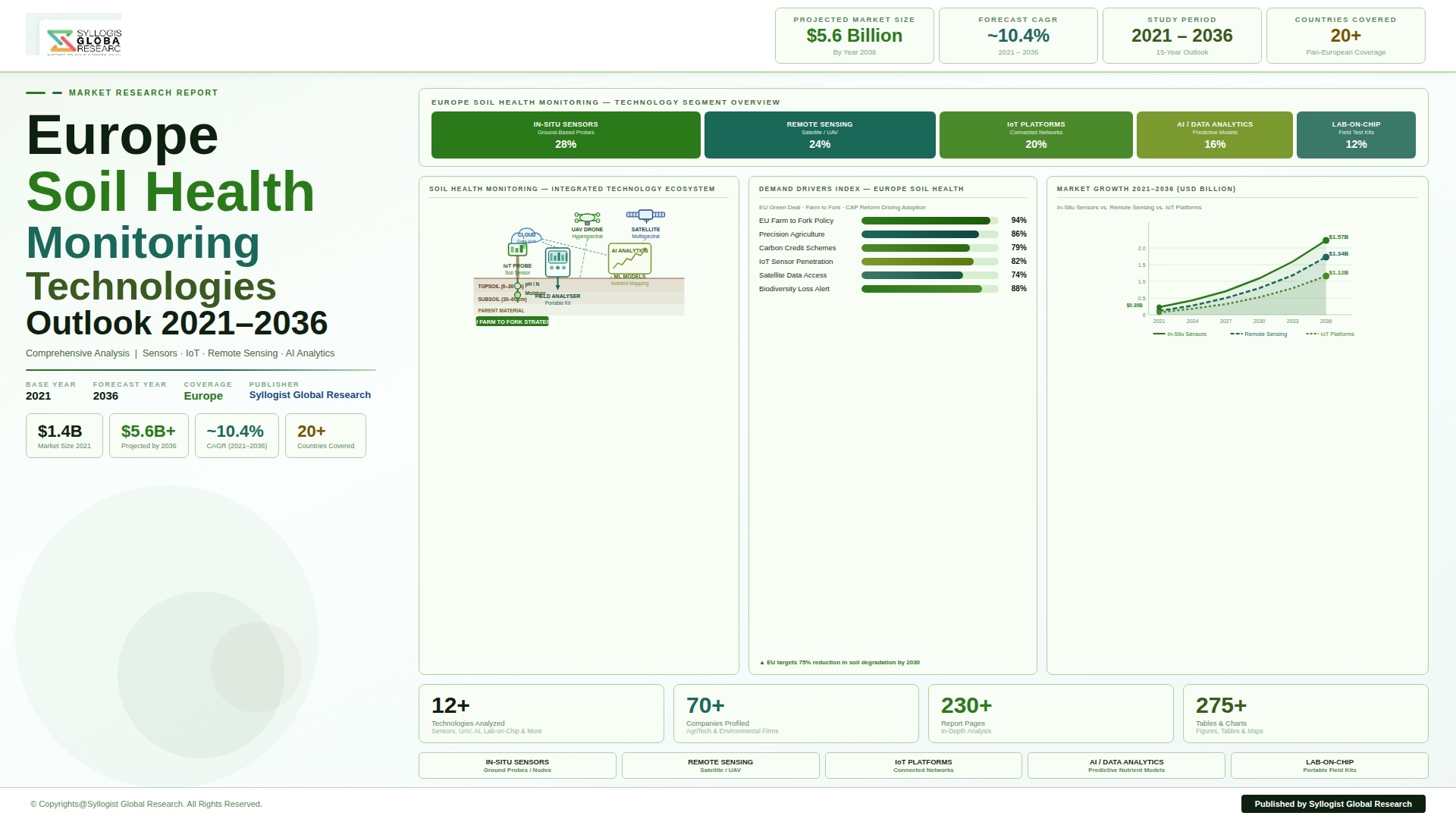

The Europe soil health monitoring technologies market is entering a period of accelerated structural growth driven by the convergence of regulatory obligation, agricultural policy incentive, and precision farming technology maturation that is collectively elevating soil health measurement from a periodic laboratory service conducted on a field-by-field basis into a continuous, digitally integrated, and farm-wide data management function whose outputs are becoming central to crop production decision-making, agri-environment scheme compliance verification, and voluntary carbon market participation by European farmers. The Europe soil health monitoring technologies market was valued at approximately USD 1.6 billion in 2025 and is projected to reach USD 3.2 billion by 2034, advancing at a compound annual growth rate of 8.1% over the forecast period from 2027 to 2034, underpinned by the binding soil assessment requirements introduced under the European Union Soil Monitoring Law proposed in 2023 and advancing through legislative adoption, the expanding eco-scheme payment architecture of the reformed Common Agricultural Policy that links direct payment eligibility to demonstrable soil health management practices, and the growing commercial deployment of on-farm continuous soil sensor networks by precision agriculture technology providers across the German, French, Dutch, and British agricultural markets.

The sensor and in-situ monitoring hardware segment is experiencing the most dynamic technology evolution within the European soil health monitoring landscape, driven by the convergence of miniaturized electrochemical sensing, low-power wireless communication, and edge computing capabilities that are enabling the deployment of cost-effective, field-embedded soil sensor networks capable of delivering real-time or near-real-time soil moisture, temperature, electrical conductivity, pH, and nitrate concentration data streams to farm management platforms without the logistical complexity and cost of periodic laboratory sample collection and analysis. Soil moisture monitoring represents the largest volume hardware deployment category, with European precision irrigation adopters in the Mediterranean, Iberian, and Southern French agricultural regions deploying capacitance and TDR-based soil moisture sensor arrays across vegetable, fruit, and wine grape production systems to optimize irrigation scheduling, reduce water consumption, and comply with water use efficiency requirements under national and EU water framework regulations. The emergence of multi-parameter in-situ sensor probes capable of simultaneously measuring soil moisture, temperature, electrical conductivity, and volumetric water content at multiple depth horizons within a single installation unit is substantially improving the cost-per-data-point economics of continuous soil monitoring and accelerating adoption among arable farmers in Northwestern Europe, where soil water management, compaction monitoring, and nitrogen leaching risk assessment are primary precision farming priorities. Companies including Sentek, IMKO, Delta-T Devices, Stevens Water, and Decagon have established significant European distribution networks for field-deployed soil sensor hardware, while the integration of soil sensor data streams into digital farming platforms from John Deere, CLAAS, Trimble, and CNH Industrial is progressively embedding soil monitoring as a standard component of precision farming system architecture across large arable and mixed farming operations in Western and Central Europe.

The soil biological monitoring and microbiome analysis segment represents the most technically sophisticated and rapidly commercializing frontier of the European soil health monitoring market, reflecting the scientific consensus that soil microbial diversity, biomass, and functional activity are the most sensitive and diagnostically meaningful indicators of soil health trajectory, and that the restoration and maintenance of soil biological vitality is fundamental to achieving the productivity, carbon sequestration, and ecosystem service outcomes that both farmers and policymakers are seeking from soil health improvement programs. DNA metabarcoding technologies, which enable comprehensive soil microbiome characterization through next-generation sequencing of environmental DNA extracted from soil samples, are transitioning from exclusively academic research applications toward commercially available soil health diagnostic services offered by agricultural laboratory companies including Earthwatch, NovaBiome, and Microbiome Insights, whose analytical platforms provide farmers with quantitative assessments of bacterial and fungal community diversity, pathogen presence, and beneficial organism abundance that inform biological soil amendment and cover cropping management decisions. The European Commission’s Mission Soil initiative, which has allocated EUR 280 million toward research and innovation programs targeting soil health monitoring methodologies, biological indicator development, and farmer-accessible soil assessment tools, is accelerating the scientific validation and commercial readiness of biological soil health indicators that will form the analytical foundation of the EU Soil Monitoring Law’s mandatory soil health assessment framework when it enters full implementation. The integration of soil biological data with earth observation data, proximal sensing outputs, and farm management records within unified soil health intelligence platforms is creating a new category of high-value soil health advisory service that is attracting investment from both agricultural input companies seeking data-driven customer engagement platforms and agri-food supply chain actors seeking verifiable soil health credentials for sustainability-linked procurement programs.

From a national market perspective, Germany represents the largest single country market for soil health monitoring technologies in Europe, reflecting its combination of the continent’s largest agricultural land area under professional management, a highly developed precision agriculture technology adoption culture among large arable farming operations in the eastern German states, and the stringent national soil protection legislation under the Bundes-Bodenschutzgesetz that has maintained a substantial environmental soil monitoring market for contamination assessment and remediation verification services. France constitutes the second-largest national market, driven by the extensive coverage of the French agricultural land area by the Programme National de Surveillance des Sols monitoring network, the growing adoption of precision viticulture soil mapping technologies across the Bordeaux, Burgundy, and Champagne wine regions where soil variability mapping directly translates into vineyard management quality and wine appellation value, and the Agroecological Transition Plan incentives directing French farmers toward soil organic matter management practices requiring baseline and periodic soil health assessment. The Netherlands, despite its relatively small agricultural land area, represents a disproportionately sophisticated and technically advanced soil monitoring market driven by the intensive horticulture and greenhouse sector’s dependence on precision substrate and root zone monitoring, the high-value permanent crop and bulb flower production systems requiring exacting soil nutrient and pH management, and the national nitrogen and phosphorus deposition regulatory regime requiring detailed soil nutrient balance monitoring as a condition of agricultural production license compliance at Dutch farm enterprises.

Key Drivers

EU Soil Monitoring Law and Common Agricultural Policy Eco-Scheme Requirements Creating Mandatory and Incentivized Soil Assessment Demand Across European Member States

The European Union’s proposed Soil Monitoring Law, advancing through the legislative process following the European Commission’s 2023 proposal under the European Green Deal framework, will upon adoption require all EU member states to establish systematic soil health monitoring programs covering agricultural, forest, and other managed land areas, to assess soil health against a defined set of physical, chemical, and biological descriptors, and to report soil condition status and trend data to national and EU-level authorities on a regular cycle, creating a legally mandated demand foundation for soil health monitoring technologies, laboratory analytical services, and digital data reporting platforms that does not depend on voluntary farmer adoption or market price signals to generate a durable procurement pipeline. The reformed Common Agricultural Policy for the 2023 to 2027 programming period has introduced a mandatory eco-scheme architecture through which member states allocate a minimum 25% of their direct payment budget to voluntary but financially incentivized eco-scheme measures, with soil health-related interventions including organic matter management, reduced tillage, cover cropping, and precision nutrient management featuring prominently in the national eco-scheme menus of Germany, France, Spain, Poland, and Italy, creating a financial incentive structure that makes soil health monitoring investments directly remunerable through CAP payment premia available to farmers who can document and verify their soil management practices. The forthcoming Carbon Farming Initiative under the EU Carbon Removal Certification Framework is further amplifying policy-driven soil monitoring demand by establishing the measurement, reporting, and verification methodology requirements for agricultural soil carbon sequestration credits, for which continuous or high-frequency soil organic carbon monitoring using proximal sensing, remote sensing, and laboratory validation methodologies is a prerequisite for generating independently verifiable carbon credit claims.

Precision Agriculture Technology Maturation and Digital Farming Platform Integration Reducing the Cost and Complexity of Continuous Soil Health Data Collection

The convergence of low-cost miniaturized sensor hardware, ubiquitous cellular and LoRaWAN wireless connectivity across European agricultural landscapes, cloud-based data processing infrastructure, and artificial intelligence-powered agronomic interpretation algorithms is systematically reducing the per-hectare cost and operational complexity of deploying and maintaining continuous soil monitoring systems on commercial farm operations, crossing the economic accessibility threshold at which soil health monitoring transitions from a specialist precision agriculture investment available only to the largest and most technologically advanced farm businesses into a broadly adopted operational practice within reach of medium-scale arable, horticultural, and livestock farming enterprises. The integration of soil sensor data streams into established digital farming platforms including the John Deere Operations Center, Trimble Ag Software, CNH’s AFS Connect, and independent platforms including Agworld, Cropio, and FarmEye is creating network effects that increase the utility of soil monitoring data by combining it with satellite-derived vegetation indices, weather station data, machinery telemetry, and crop growth modeling outputs to generate contextually rich agronomic recommendations that individual soil data streams cannot produce in isolation. The commercialization of on-the-go proximal soil sensing systems mounted on agricultural vehicles, including the Veris MSP, AgroCares Scanner, and ISARIA active canopy sensor platforms, is enabling European farmers to generate high-resolution soil variability maps covering entire farm areas in a single field pass at a fraction of the cost of grid-based laboratory soil sampling, providing the foundational soil spatial data required for variable rate fertilizer and lime application prescription development that delivers both agronomic performance and input cost efficiency benefits measurable in the first growing season following mapping.

European Green Deal Farm to Fork Strategy and Corporate Sustainability Reporting Obligations Generating Supply Chain-Driven Soil Health Monitoring Demand

The European Green Deal’s Farm to Fork Strategy, which targets a 20% reduction in fertilizer use, a 50% reduction in pesticide use, and a 25% expansion of organic farming area across the EU by 2030, is creating a comprehensive policy environment in which soil health monitoring technologies are positioned as essential enabling tools for farmers seeking to demonstrate progress toward these targets while maintaining crop production profitability through the precision application efficiency and biological soil fertility management approaches that high-quality soil health data supports. The Corporate Sustainability Reporting Directive, which from 2024 onwards requires large European companies and from 2026 onwards extends to a broader range of listed and mid-sized companies to report on material sustainability impacts including land use, soil degradation, and supply chain agricultural practices, is generating upstream supply chain demand for verifiable soil health data from food and beverage manufacturers, textile and fiber processors, bioenergy producers, and retailer private label agricultural sourcing programs that need to substantiate soil health performance claims in their sustainability disclosures with independently verifiable field measurement data. Major European food companies including Danone, Nestle, Unilever, and AB InBev have established supplier engagement programs specifically targeting soil health improvement across their contracted agricultural supply bases in France, Germany, the Netherlands, and Central and Eastern Europe, and these programs typically include soil health baseline assessment requirements, monitoring protocol specifications, and performance verification frameworks that generate funded demand for soil assessment services from the farmer supply chain participants enrolled in corporate regenerative agriculture commitments.

Key Challenges

Lack of Standardized Soil Health Indicator Frameworks and Measurement Protocols Creating Comparability and Adoption Barriers Across European Markets

The Europe soil health monitoring technologies market is significantly constrained by the absence of a harmonized, EU-wide standardized framework defining which soil health indicators must be measured, what analytical methodologies are accepted for each indicator, what sampling protocols ensure spatial and temporal comparability of results, and what performance thresholds distinguish healthy from degraded soil condition across the diverse soil types, climatic zones, and land management systems represented within the European agricultural landscape, creating a fragmented and technically inconsistent monitoring landscape in which soil health data generated under different national, regional, and corporate assessment protocols cannot be reliably compared, aggregated, or used interchangeably for regulatory compliance, carbon market verification, or supply chain sustainability reporting purposes. The EU Soil Monitoring Law’s indicator framework, while providing a legislative mandate for harmonization, is still under technical development through the Joint Research Centre’s scientific advisory process, and the timeline for finalizing EU-standardized analytical protocols and laboratory accreditation requirements for biological soil health indicators in particular, including soil microbial biomass carbon, enzyme activity assays, and earthworm population density metrics whose measurement methodology remains scientifically contested, creates regulatory uncertainty for technology providers and laboratory service companies seeking to invest in capacity aligned with future EU compliance requirements. The divergence between the extensive and expensive soil health indicator sets specified in scientific and regulatory frameworks and the practical cost and logistical constraints facing individual farm operators seeking commercially viable monitoring solutions is creating a significant implementation gap that risks undermining farmer engagement with soil health monitoring programs even where policy financial incentives are available, particularly for smaller farm enterprises in Southern and Eastern European member states where advisory infrastructure and precision farming adoption rates are lower than in Northwestern Europe.

High Cost of Comprehensive Biological and Chemical Soil Analysis Limiting Monitoring Frequency and Spatial Coverage on Commercial Farm Operations

The cost of comprehensive soil health analysis encompassing the full spectrum of physical, chemical, and biological indicators required by advanced soil health assessment frameworks remains prohibitively high for routine application across entire farm areas at the sampling frequencies needed to detect management-induced soil health changes within commercially relevant timeframes, with a complete biological soil health panel including microbial biomass, DNA metabarcoding-based community analysis, enzyme activity profiling, and nematode community assessment costing between EUR 150 and EUR 400 per sample at current European laboratory commercial pricing, creating a fundamental economic barrier to the high-resolution, temporally repeated spatial sampling designs that would provide the statistically robust soil health trend data required for confident management decision-making and regulatory compliance verification. The sampling design challenge is compounded by the high natural spatial variability of soil health indicators across typical European agricultural field landscapes, where soil organic carbon, pH, biological activity, and nutrient availability can vary by factors of two to five across distances of 10 to 50 meters within a single field, requiring dense sample collection grids of one sample per hectare or higher to adequately characterize field-average conditions and detect management treatment effects against the background of natural spatial variability, and implying that comprehensive soil health monitoring of even a modestly sized 200-hectare arable farm at scientifically adequate resolution would require several hundred samples per assessment cycle at costs that represent a significant proportion of total farm input expenditure. The commercial viability of soil health monitoring technology adoption is therefore critically dependent on the continued development and field validation of cost-reduction pathways including near-infrared spectroscopy calibration models capable of predicting multiple soil health parameters from single low-cost scans, proximal sensor-based field mapping calibrated against sparse laboratory reference points, and satellite remote sensing indices correlated with surface soil organic carbon and biological activity that collectively reduce the required laboratory sample density while maintaining acceptable prediction accuracy.

Data Ownership, Privacy, and Interoperability Concerns Limiting Farmer Willingness to Share Soil Health Data with Technology Platforms and Supply Chain Actors

European farmers are exhibiting increasing concern and in many cases active resistance toward the data sharing requirements embedded in the commercial terms of precision agriculture platforms, soil monitoring service subscriptions, and corporate supply chain sustainability programs that seek access to farm-level soil health data for platform improvement, commercial analytics, and supply chain reporting purposes, creating a trust and governance challenge that is limiting the adoption of connected soil monitoring technologies and the formation of the aggregated soil data commons that would substantially improve the analytical value of individual farm soil health datasets through benchmarking, spatial interpolation, and regional trend analysis. The General Data Protection Regulation framework, while primarily designed for personal data protection, has created heightened general awareness among European farmers of their data rights and the commercial value of farm-level data, and agricultural industry bodies in Germany, France, the Netherlands, and the United Kingdom have issued guidance documents and model contractual frameworks for agricultural data governance that explicitly address soil health monitoring data ownership, portability, and third-party sharing consent requirements in ways that constrain the default data aggregation practices of commercial precision agriculture platform operators. The interoperability challenge, arising from the proliferation of incompatible data formats, communication protocols, and application programming interfaces across the diverse landscape of soil sensor hardware manufacturers, laboratory information management systems, and digital farming platform operators active in the European market, creates practical integration complexity that increases the technical cost and expertise requirement for farmers seeking to combine soil monitoring data from multiple sources within a unified farm management information system, and represents a structural market friction that technology standardization initiatives including the European Agricultural Data Space framework and the AgroXML data standard are working to address but have not yet resolved at the commercial deployment scale required for broad farmer adoption.

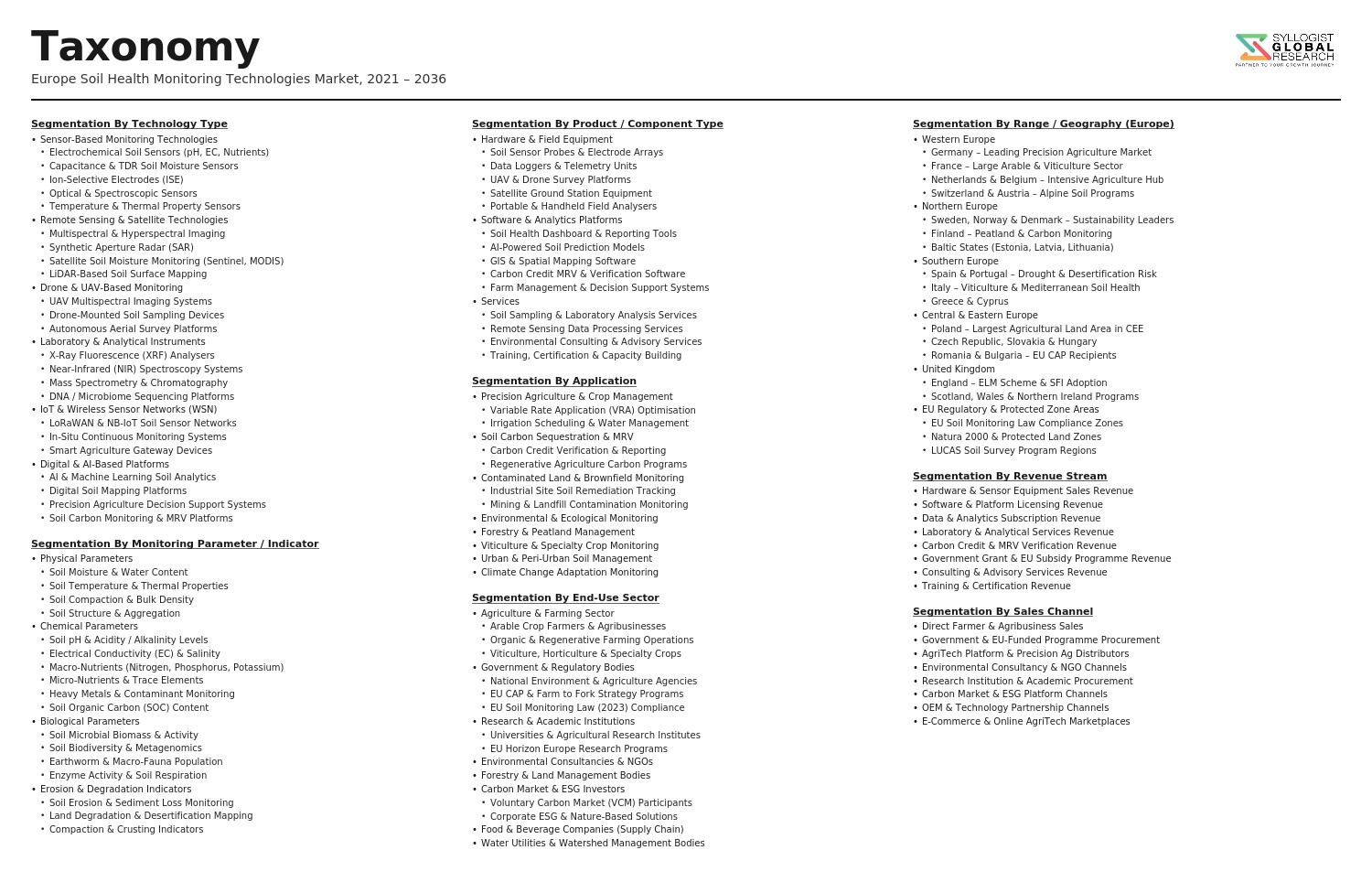

Market Segmentation

Segmentation By Technology Type

- In-Situ Soil Sensor Systems (Electrochemical, Dielectric, Optical)

- Proximal Soil Sensing Platforms (On-the-Go Vehicle-Mounted Sensors)

- Satellite Remote Sensing and Earth Observation Platforms

- Aerial Drone and UAV-Based Soil Sensing

- Near-Infrared Spectroscopy (NIR and NIRS) Analytical Systems

- X-Ray Fluorescence (XRF) Soil Elemental Analysis

- DNA Metabarcoding and Soil Microbiome Sequencing Platforms

- Gamma-Ray Spectrometry Soil Mapping Systems

- Electrical Resistivity Tomography (ERT) Systems

- Digital Soil Mapping and Modelling Software Platforms

- Others

Segmentation By Soil Health Indicator

- Soil Organic Carbon and Organic Matter Content

- Soil Moisture and Water Holding Capacity

- Soil pH and Electrical Conductivity

- Macronutrient and Micronutrient Availability (N, P, K, Mg, Ca, S)

- Soil Biological Indicators (Microbial Biomass, Biodiversity, Enzyme Activity)

- Soil Structure, Compaction, and Bulk Density

- Heavy Metal and Contaminant Detection

- Erosion and Sediment Loss Assessment

- Others

Segmentation By Land Use

- Arable and Cropland

- Permanent Grassland and Pasture

- Viticulture and Permanent Horticulture

- Forestry and Woodland

- Protected Natural Areas and Peatlands

- Urban and Peri-Urban Green Infrastructure

- Contaminated and Brownfield Land

- Others

Segmentation By End User

- Farmers and Agricultural Land Managers

- Agricultural Advisory and Consultancy Services

- Soil and Environmental Testing Laboratories

- Government Environmental and Agricultural Agencies

- Academic and Scientific Research Institutions

- Agri-Food Supply Chain Companies and Food Processors

- Carbon Market Verification and MRV Service Providers

- Environmental Remediation and Land Rehabilitation Companies

- Others

Segmentation By Deployment Mode

- Continuous Fixed Field Sensor Networks

- Periodic Manual and Semi-Automated Field Sampling

- Mobile and Tractor-Mounted On-the-Go Survey Systems

- Aerial and Satellite Remote Sensing Survey Programs

- Laboratory-Based Analytical Services

- Cloud-Based Digital Soil Intelligence Platforms

- Others

Segmentation By Country

- Germany

- France

- Netherlands

- United Kingdom

- Spain

- Italy

- Poland

- Scandinavia (Sweden, Denmark, Finland, Norway)

- Rest of Europe

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the Europe Soil Health Monitoring Technologies Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by technology type, soil health indicator, land use category, end user, and country, to enable precision agriculture technology developers, environmental instrument manufacturers, laboratory service providers, and investors to identify which monitoring technology segments and national markets will generate the highest absolute revenue and the most durable demand growth across the forecast period?

- How are the EU Soil Monitoring Law’s mandatory soil health assessment requirements, the Common Agricultural Policy eco-scheme payment architecture, and the EU Carbon Removal Certification Framework’s measurement, reporting, and verification standards collectively shaping the technical specification, sampling frequency, analytical methodology, and spatial coverage requirements of soil health monitoring programs across European member states, and what is the projected additional monitoring service and technology procurement demand generated by each regulatory instrument through 2034?

- What is the current state of commercial adoption of continuous in-situ soil sensor networks, on-the-go proximal sensing systems, and satellite remote sensing-based soil health mapping across European arable, horticultural, and permanent crop farming systems by country and farm size category, what economic return on investment evidence is driving or constraining adoption decisions among different farmer segments, and what technology cost reduction and performance improvement trajectories are needed to extend economically viable soil monitoring adoption to medium and smaller scale farm operations in Southern and Eastern European markets?

- How is the soil biological monitoring and microbiome analysis segment evolving in terms of commercial service availability, analytical cost reduction, indicator standardization, and farmer accessibility across European markets, which biological soil health indicator methodologies are emerging as the most likely candidates for inclusion in the EU Soil Monitoring Law’s mandatory assessment framework, and what investment is being directed by instrument manufacturers, laboratory companies, and digital agriculture platforms toward commercializing biological soil health monitoring at the scale and cost point required for broad agricultural adoption?

- Who are the leading precision agriculture technology companies, environmental instrument manufacturers, earth observation service providers, soil laboratory service companies, and digital farming platform operators currently defining the competitive landscape of the Europe soil health monitoring technologies market, and what are their respective product and service portfolios, technology development roadmaps, regulatory engagement strategies, partnership structures with agricultural input companies and food supply chains, and competitive positioning in response to the structural growth opportunity presented by the convergence of EU policy mandates, corporate sustainability demand, and precision farming technology adoption across European agricultural markets through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Data Accuracy, Sensor Calibration Drift & Field Variability Risk in Soil Health Monitoring

- High Upfront Capital Cost, Farmer Affordability & Technology Adoption Barrier Risk

- Fragmented Regulatory Standards, Interoperability & Data Sovereignty Risk Across European Member States

- Competition from Low-Cost Alternatives, Manual Sampling & Laboratory Testing Substitution Risk

- Climate Variability, Extreme Weather Event Impact & Long-Term Soil Monitoring Data Continuity Risk

- Regulatory Framework & Standards

- European Union Soil Health Law, EU Soil Strategy 2030 & Mission-Driven Soil Monitoring Requirements

- EU Common Agricultural Policy (CAP) Reform, Eco-Scheme Conditionality & Soil Health Monitoring Compliance Requirements

- European Green Deal, Farm to Fork Strategy & Soil Carbon Sequestration Measurement, Reporting & Verification (MRV) Frameworks

- ISO, CEN & National Standards for Soil Sampling, Sensor Calibration, Data Quality & Laboratory Reference Method Equivalence

- GDPR, Agricultural Data Governance, Open Data Mandates & Digital Agriculture Platform Regulatory Frameworks in Europe

- Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Units Deployed)

- Market Size & Forecast by Technology Type

- In-Situ Soil Sensors & IoT-Based Continuous Monitoring Systems

- Proximal Soil Sensing Technologies (Vis-NIR, MIR & XRF Spectroscopy)

- Remote Sensing & Satellite-Based Soil Health Monitoring Platforms

- Unmanned Aerial Vehicle (UAV / Drone) Based Soil Sensing & Imaging

- Electrochemical & Ion-Selective Electrode (ISE) Soil Sensors

- Biosensor & Biological Indicator-Based Soil Health Monitoring Systems

- Electromagnetic Induction (EMI) & Ground-Penetrating Radar (GPR) Soil Survey Technologies

- Laboratory-on-a-Chip & Rapid Field-Portable Soil Analysis Devices

- Integrated Digital Soil Mapping & AI-Driven Soil Health Analytics Platforms

- Market Size & Forecast by Monitoring Parameter

- Soil Moisture & Water Content Monitoring

- Soil Organic Carbon (SOC) & Organic Matter Monitoring

- Soil Nutrient Monitoring (Nitrogen, Phosphorus, Potassium & Micronutrients)

- Soil pH & Electrical Conductivity (EC) Monitoring

- Soil Temperature Monitoring

- Soil Compaction & Bulk Density Monitoring

- Soil Biological Activity, Microbial Biomass & Biodiversity Monitoring

- Soil Erosion, Salinisation & Contamination Monitoring

- Soil Greenhouse Gas (CO2, N2O & CH4) Flux Monitoring

- Market Size & Forecast by Deployment Mode

- Permanently Installed In-Field Sensor Networks

- Mobile & Tractor-Mounted Proximal Sensing Systems

- Drone & Aerial Survey-Based Monitoring

- Satellite & Remote Sensing Subscription Platforms

- Laboratory & Portable Field Analysis Devices

- Market Size & Forecast by Component

- Hardware (Sensors, Probes, Data Loggers & Gateway Devices)

- Software & Analytics Platforms (Cloud-Based Dashboards, AI Models & Decision Support Tools)

- Connectivity & Communication Infrastructure (LoRaWAN, NB-IoT & Satellite)

- Professional Services (Installation, Calibration, Maintenance & Training)

- Market Size & Forecast by Application

- Arable Crop Farming & Precision Agriculture

- Viticulture & Permanent Crop Management

- Grassland, Pasture & Livestock Farming

- Horticulture, Vegetable & Fruit Production

- Forestry & Woodland Soil Monitoring

- Environmental Monitoring, Land Reclamation & Contaminated Site Management

- Carbon Market, Soil Carbon Credit Verification & Nature-Based Solutions

- Research Institutions, Government Agencies & National Soil Survey Programmes

- Market Size & Forecast by End-User

- Farmers & Agricultural Cooperatives

- Agri-Food Companies & Food & Beverage Processors

- Precision Agriculture Service Providers & Farm Advisory Companies

- Government Agencies & National Environmental Monitoring Bodies

- Research Institutes, Universities & Soil Science Organisations

- Carbon Market Platforms, ESG Investors & Nature-Based Solution Developers

- Environmental Consultancies & Land Management Companies

- Market Size & Forecast by Sales Channel

- Direct Sales to Farmers & Agricultural Cooperatives

- Agri-Input Dealer, Distributor & Retailer Network

- Precision Agriculture Service Provider & Farm Management Platform

- Government Subsidy, CAP-Funded & Grant-Assisted Procurement

- Online & Digital Commerce Platform

- Western Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Northern Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Eastern Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Southern Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Central Europe Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

- Country-Wise* Soil Health Monitoring Technologies Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Units Deployed)

- By Technology Type

- By Monitoring Parameter

- By Deployment Mode

- By Application

- By End-User

- By Country

- By Sales Channel

- Market Size & Forecast

*Countries Analyzed in the Syllogist Global Research Portfolio: Germany, France, United Kingdom, Netherlands, Spain, Italy, Norway, Sweden, Denmark, Finland, Poland, Czech Republic, Hungary, Romania, Belgium, Austria, Switzerland, Portugal, Greece, Ireland

- Technology Landscape & Innovation Analysis

- In-Situ IoT Soil Sensor Network Technology: Multi-Parameter Probes, Low-Power Communication & Edge Computing Deep-Dive

- Vis-NIR & MIR Spectroscopy for Soil Organic Carbon, Nutrient & Texture Prediction Technology

- Satellite Remote Sensing & SAR-Based Soil Moisture, Organic Carbon & Land Degradation Monitoring Technology

- Drone-Based Multispectral, Hyperspectral & LiDAR Soil Health Imaging Technology

- AI, Machine Learning & Digital Soil Mapping Technology for Spatial Soil Health Prediction & Decision Support

- Biosensor & eDNA Technology for Soil Biological Health, Microbial Diversity & Fauna Monitoring

- Soil Carbon MRV Technology for Carbon Market Compliance & Nature-Based Solution Verification in Europe

- Patent & IP Landscape in Soil Health Monitoring Technologies Relevant to Europe

- Value Chain & Supply Chain Analysis

- Soil Sensor Component, MEMS Chip & Electrochemical Cell Manufacturing Supply Chain

- Optical Sensor, Spectrometer & Imaging Module Assembly Supply Chain

- IoT Gateway, Data Logger & Connectivity Hardware Manufacturing Supply Chain

- Software Development, Cloud Platform & AI Model Supply Chain

- System Integration, Installation & Calibration Services Supply Chain

- Agri-Input Dealer, Distributor & Precision Agriculture Service Provider Channel

- Spent Sensor, Battery & Electronic Waste Recycling & Disposal Value Chain

- Pricing Analysis

- In-Situ Soil Sensor & IoT Network Hardware Capital Cost & Total Cost of Ownership (TCO) Analysis

- Proximal Sensing Device & Portable Soil Analyser Purchase & Leasing Cost Analysis

- Satellite & Remote Sensing Soil Monitoring Subscription Pricing Analysis

- Software & Analytics Platform Licensing, SaaS & Per-Hectare Pricing Model Analysis

- Service Contract, Calibration & Maintenance Fee Structure Analysis

- Total Soil Health Monitoring Cost per Hectare Across Technology Routes & Deployment Models

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Soil Health Monitoring Technologies: Carbon Footprint, Electronic Waste & Resource Use

- Soil Health Monitoring Contribution to Soil Carbon Sequestration Measurement & EU Net Zero Agriculture Targets

- Role of Soil Health Monitoring in Reducing Fertiliser Overuse, Nitrate Leaching & Agricultural GHG Emissions in Europe

- Biodiversity, Soil Ecosystem Services & Nature-Based Solution Monitoring: Environmental Co-Benefits

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger), SDG 15 (Life on Land) & SDG 13 (Climate Action) Alignment & Green Finance Eligibility

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Technology Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Technology Type, Monitoring Parameter & Country

- Player Classification

- Integrated Precision Agriculture & Digital Farming Platform Companies

- Specialist In-Situ Soil Sensor & IoT Network Manufacturers

- Proximal Sensing, Spectroscopy & Portable Soil Analyser Manufacturers

- Satellite & Remote Sensing Data & Analytics Platform Providers

- Drone & UAV-Based Soil Sensing System Providers

- Soil Laboratory & Rapid Testing Service Companies Transitioning to Digital Platforms

- AI, Data Analytics & Digital Soil Mapping Software Providers

- Carbon Market, MRV & Nature-Based Solution Platform Providers Incorporating Soil Monitoring

- Competitive Analysis Frameworks

- Market Share Analysis by Technology Type, Monitoring Parameter & Country

- Company Profile

- Company Overview & Headquarters

- Soil Health Monitoring Products, Sensors & Platform Portfolio

- Key Customer Relationships & Reference Deployments in Europe

- Manufacturing Footprint & Production Capacity

- Revenue (Soil Health Monitoring Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Contract Wins, Product Launches, Platform Updates)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Technology Capability vs. Market Penetration)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Technology Type, Monitoring Parameter, Application, End-User & Country

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output