Market Definition

The India Irrigation Pipes Market encompasses the manufacturing, distribution, and installation of pipeline systems used to convey water from source points including canals, rivers, reservoirs, tube wells, check dams, and rainwater harvesting structures to agricultural fields, orchards, horticulture farms, plantations, and allied rural water management infrastructure across India’s diverse agro-climatic zones. Irrigation pipes form the foundational conveyance infrastructure enabling surface irrigation, drip irrigation, sprinkler irrigation, and micro-irrigation systems to function efficiently by transporting pressurized and gravity-fed water across field layouts of varying topography, soil type, and crop configuration with minimal conveyance losses, pressure drop, and structural failure risk under the thermal, ultraviolet exposure, chemical, and mechanical stress conditions encountered in Indian agricultural field environments.

The market encompasses rigid thermoplastic pipes manufactured from unplasticized polyvinyl chloride, high-density polyethylene, low-density polyethylene, linear low-density polyethylene, and polypropylene materials across a spectrum of nominal diameters from 16 millimeters to above 630 millimeters and pressure ratings from 2.5 kilogram per square centimeter to 16 kilogram per square centimeter suited to different irrigation system hydraulic requirements; flexible lay-flat hose and irrigation tubing used for field distribution and lateral lines; mainline, submain, and lateral pipe assemblies for drip and sprinkler irrigation networks; concrete and asbestos cement pipes used in gravity-flow canal lining and distribution systems; and galvanized iron and mild steel pipes used in overhead and pressurized distribution applications. The market further encompasses fittings, couplers, end caps, reducers, tees, elbows, and filter holders that constitute the jointing and distribution system components of complete irrigation pipe networks. Key participants include polymer pipe manufacturers, irrigation system integrators and dealers, government agencies administering irrigation development programs, agricultural cooperative procurement organizations, and the farmer and contractor end user community whose investment decisions across Pradhan Mantri Krishi Sinchayee Yojana subsidy frameworks, state government micro-irrigation programs, and private agricultural development projects define the annual volume and value of irrigation pipe demand across India’s eighteen agro-climatic zones.

Market Insights

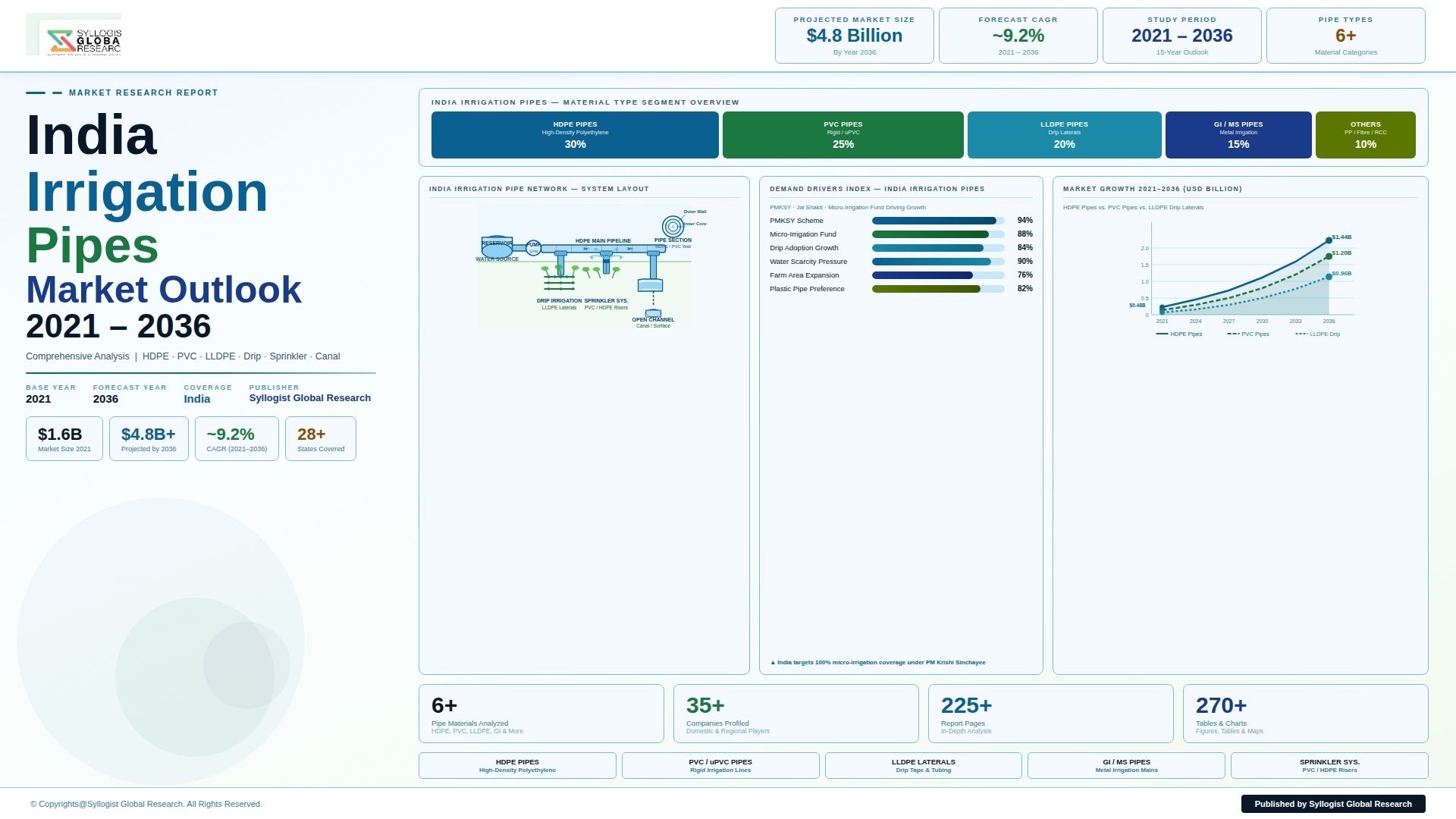

The India irrigation pipes market is positioned at the intersection of three powerful structural demand forces that are collectively ensuring a sustained and expanding commercial growth trajectory through the forecast period: the Indian government’s determined policy commitment to achieving Har Khet Ko Pani and More Crop Per Drop objectives under the Pradhan Mantri Krishi Sinchayee Yojana, which is channeling multi-thousand-crore rupee annual capital expenditure into irrigation infrastructure creation and micro-irrigation system expansion across previously underserved agricultural regions; the progressive depletion of groundwater aquifers across Punjab, Haryana, Rajasthan, and peninsular India that is compelling a national shift from flood irrigation toward pressurized drip and sprinkler systems requiring extensive pipeline networks; and the rapid expansion of horticulture, floriculture, and high-value crop cultivation that demands precision water delivery infrastructure unavailable through traditional flood or furrow irrigation methods. The India irrigation pipes market was valued at approximately USD 2.8 billion in 2025 and is projected to reach USD 4.9 billion by 2034, advancing at a compound annual growth rate of 6.4% over the forecast period from 2027 to 2034, underpinned by the expanding pipe installation volumes under PMKSY and state micro-irrigation schemes, the ongoing replacement of aging unlined earthen canal distributary networks with concrete-lined and piped distribution systems, and the growing commercial farmer investment in turnkey drip and sprinkler irrigation systems incorporating HDPE mainline, LLDPE lateral, and LDPE drip line components across horticulture-intensive states including Maharashtra, Gujarat, Karnataka, Andhra Pradesh, and Telangana.

High-density polyethylene pipes constitute the dominant material segment of the India irrigation pipes market by both volume and revenue, accounting for approximately 44% of total market revenue in 2025, driven by HDPE’s superior pressure rating capability, chemical resistance to fertilizer solutions and soil chemicals, flexibility enabling trenchless installation across rocky and undulating terrain, UV stabilization for above-ground application, and long service life exceeding 50 years under normal field conditions that collectively make HDPE the preferred mainline material for pressurized drip and sprinkler irrigation systems across India’s diverse agricultural environments. The Bureau of Indian Standards IS 4984 and IS 14151 specifications governing HDPE irrigation pipe quality have been progressively tightened to align with international standards, raising the technical floor for compliant pipe supply and creating procurement quality differentiation between ISI-marked pipes from organized sector manufacturers and the substantial volumes of non-compliant pipe supplied through unorganized regional manufacturers that continue to operate in price-sensitive rural agricultural markets. UPVC irrigation pipes, governed by IS 4985 and IS 12235 standards, retain a significant market position in underground mainline and submain applications where their higher rigidity, dimensional stability, and lower cost relative to HDPE for non-flexible installation scenarios provide a cost-competitive supply option for state government irrigation canal lining and piped distribution network projects, with UPVC pipe demand particularly concentrated in the canal command area modernization programs of Uttar Pradesh, Madhya Pradesh, Maharashtra, and Andhra Pradesh where gravity-fed and low-pressure distribution from modernized canal headworks to farm field outlets is the primary irrigation delivery paradigm. The drip lateral and inline drip line segment, encompassing the thin-walled LLDPE and LDPE tubing through which water is delivered directly to the plant root zone in drip irrigation systems, represents the highest annual replacement volume segment of the Indian irrigation pipe market given the two to five year functional replacement cycle of drip laterals exposed to UV degradation, physical damage, and emitter clogging in field conditions.

The Pradhan Mantri Krishi Sinchayee Yojana and its component schemes including the Accelerated Irrigation Benefits Programme, the Per Drop More Crop micro-irrigation component, and the Har Khet Ko Pani groundwater development component collectively represent the single most powerful demand catalyst in the India irrigation pipes market, with the central and state government expenditure committed under PMKSY during the 2021-2026 implementation period totaling approximately INR 93,068 crore, of which a substantial proportion flows directly into irrigation pipe procurement through project implementing agencies, water user associations, and farmer beneficiary direct procurement channels. The Per Drop More Crop component, which subsidizes drip and sprinkler irrigation system installation at 55% of unit cost for small and marginal farmers and 45% for other farmers through the National Mission on Micro Irrigation administered through state horticulture mission agencies, generated the installation of approximately 7.2 lakh hectares of new micro-irrigated area in fiscal year 2024-25, with each hectare of drip-irrigated horticulture requiring approximately 500 to 2,500 meters of lateral and submain pipe depending on crop spacing and field configuration, translating NMMI target achievement directly into tens of millions of meters of annual irrigation pipe procurement. The Jal Jeevan Mission, while primarily targeting rural drinking water supply, is simultaneously creating irrigation-adjacent pipe infrastructure demand through its Har Ghar Jal program investments in village-level water supply piping networks, groundwater recharge structures, and multi-purpose water conveyance infrastructure that utilizes HDPE and UPVC pipe products from the same manufacturing and distribution supply chain serving the agricultural irrigation market, creating positive spillover demand effects for pipe manufacturers with broad product range capabilities serving both agricultural and rural infrastructure segments.

The competitive landscape of the India irrigation pipes market is defined by a three-tier structure comprising large organized sector polymer pipe manufacturers with national distribution reach and BIS certification across multiple product categories, mid-size regional manufacturers serving state-level government procurement and commercial farmer markets within defined geographic territories, and a large unorganized sector of small-scale pipe extruders producing non-certified pipe products for price-sensitive smallholder markets in rural agricultural districts. The organized sector leaders including Finolex Industries, Astral Limited, Prince Pipes and Fittings, Supreme Industries, Jain Irrigation Systems, and Netafim India (now Rivulis) occupy dominant positions in the HDPE mainline and UPVC pipe categories through their combination of large-diameter extrusion capacity, ISI certification across the full product range, national dealer networks extending into rural agricultural markets, and technical sales force capabilities enabling turnkey drip and sprinkler system specification and supply. The market is experiencing progressive consolidation driven by government procurement quality requirements that favor ISI-certified suppliers, the capital cost advantages of large-scale polymer extrusion, and the growing commercial farmer preference for integrated irrigation system supply from a single technically capable source rather than component-wise procurement through multiple suppliers. Maharashtra, Gujarat, Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, and Rajasthan collectively represent the highest-value state markets for irrigation pipes due to their combination of large horticulture production areas, active state government micro-irrigation subsidy program disbursement, water scarcity pressure incentivizing adoption of efficient irrigation, and commercially progressive farming communities with demonstrated willingness to invest in productivity-enhancing agricultural infrastructure.

Key Drivers

Government Policy Commitment Under PMKSY and National Micro-Irrigation Mission Generating Sustained Subsidy-Backed Pipe Infrastructure Investment

The Pradhan Mantri Krishi Sinchayee Yojana framework, backed by central government capital allocation of INR 93,068 crore for the 2021 to 2026 implementation period and complemented by state government matching grants across major agricultural states, represents the most consequential demand driver in the India irrigation pipes market by transforming irrigation infrastructure investment from a discretionary farmer decision constrained by capital availability into a subsidized and institutionally supported national development priority with dedicated procurement mechanisms, implementation timelines, and performance accountability frameworks. The Per Drop More Crop micro-irrigation subsidy component, which covers 45% to 55% of system installation cost for farmer beneficiaries and has been extended to cover fertigation system components and solar pump integration alongside pipe and emitter hardware, reduces the effective farmer investment requirement for a one-hectare drip irrigation system for horticulture crops from approximately INR 60,000 to INR 80,000 to approximately INR 27,000 to INR 44,000, crossing the commercial viability threshold for a significantly larger farmer population than would invest in drip irrigation infrastructure without subsidy support. The NMMI target of bringing 10 million additional hectares under micro-irrigation by 2026, combined with state government top-up subsidies in Maharashtra, Andhra Pradesh, Telangana, and Rajasthan that in some schemes cover up to 100% of system cost for scheduled caste and scheduled tribe beneficiary farmers, is generating a multi-year secured procurement pipeline for irrigation pipe manufacturers whose production planning and capacity investment decisions can be calibrated against government program targets with a degree of demand visibility unavailable in purely commercial market segments. The convergence of PMKSY with the Atal Bhujal Yojana groundwater conservation program, which mandates irrigation efficiency improvement as a condition of program benefit in water-stressed districts across seven states, is further reinforcing the policy architecture driving irrigation pipe demand growth.

Acute Groundwater Depletion and Water Scarcity Across Key Agricultural Regions Compelling Transition From Flood to Pressurized Pipe-Based Irrigation

India’s agricultural water crisis, characterized by the depletion of groundwater tables at rates of 0.3 to 1.0 meter per year across the critically over-exploited aquifer zones of Punjab, Haryana, western Uttar Pradesh, Rajasthan, and peninsular India’s hard rock formations, is creating an agronomically and economically irreversible imperative for Indian farmers to transition from the inefficient flood and furrow irrigation practices that account for approximately 60% of total agricultural water application to pressurized drip and sprinkler systems that deliver water use efficiency improvements of 40% to 60%, and whose installation requires substantial investments in mainline HDPE pipe, submain distribution networks, and lateral systems that directly generate irrigation pipe market demand. The Central Ground Water Authority has designated 1,592 assessment units across India as over-exploited, critical, or semi-critical in terms of groundwater extraction relative to recharge, and state governments in Punjab, Haryana, Maharashtra, and Tamil Nadu have enacted legislation restricting groundwater extraction, mandating water meters on agricultural tube wells, and in certain blocks requiring the adoption of drip or micro-sprinkler irrigation as a condition of continued pump operation licensing, creating regulatory compliance-driven adoption pressure for pipe-based irrigation systems that supplements the economic incentive for water use efficiency improvement. The direct water cost savings from drip irrigation adoption, including reduced electricity expenditure for pumping, deferred tube well deepening costs, and the crop yield improvements of 25% to 40% documented for vegetables, fruits, and cash crops under drip irrigation relative to flood irrigation, provide a compelling three to five year financial payback on drip system investment for commercially oriented farmers whose decision framework extends beyond the initial capital outlay to encompass the full operational economics of water-efficient crop production.

Rapid Horticulture Expansion and High-Value Crop Cultivation Growth Driving Precision Irrigation Pipe Infrastructure Investment Across India

India’s horticulture sector has emerged as the fastest-growing agricultural production segment by value, with total horticulture output reaching approximately 355 million metric tonnes in fiscal year 2023-24 and horticulture’s contribution to total agricultural gross value added exceeding 33%, driven by rising domestic consumption of fruits and vegetables, growing export revenue from grapes, pomegranates, mangoes, and processed horticulture products, and the commercial attractiveness of high-value horticulture relative to staple cereal farming for smallholders seeking improved farm income from limited land holdings. The expansion of horticulture cultivation across new geographies enabled by drip irrigation, including the dramatic growth of grape cultivation in Nashik and Sangli districts of Maharashtra, pomegranate orchards across Solapur and Pune districts, banana cultivation in Jalgaon and Thane, and tomato and capsicum production in Karnataka and Andhra Pradesh, has been fundamentally enabled by the availability of pressurized drip irrigation pipe infrastructure that allows commercially viable crop production on the undulating, shallow-soil, and rain-shadow area terrain that characterizes much of peninsular India’s expanding horticulture geography. Government initiatives including the Agricultural and Processed Food Products Export Development Authority export promotion programs for fresh horticultural produce, the Horticulture Mission for North-East and Himalayan States, and the Integrated Development of Horticulture in Jammu and Kashmir and Ladakh are extending horticulture development investment into new geographic frontiers where the adoption of drip irrigation pipe infrastructure is simultaneously a production enabler and a water management necessity in fragile mountain and semi-arid ecosystems with limited water availability and soil moisture retention capacity.

Key Challenges

Unorganized Sector Competition and Non-Compliant Pipe Supply Undermining Quality Standards and Market Pricing Across Rural Agricultural Districts

The India irrigation pipes market is significantly impacted by the widespread availability of substandard and non-ISI-certified pipe products manufactured by unorganized small-scale extruders operating across rural industrial estates in Rajasthan, Gujarat, Maharashtra, and Andhra Pradesh, whose lower production cost structures arising from inferior raw material quality, absence of quality testing infrastructure, regulatory non-compliance, and informally structured labor arrangements enable them to supply irrigation pipe products at 15% to 30% price discounts relative to BIS-certified organized sector products, creating a persistent price competition dynamic that constrains the revenue realization and market share of compliant manufacturers while simultaneously exposing farmer buyers to the risk of premature pipe failure, elevated leakage losses, and irrigation system performance shortfalls that erode the agronomic and economic benefits expected from drip and sprinkler system investments. The challenge of quality enforcement is compounded by the geographic distribution of the unorganized pipe supply network through thousands of rural agricultural input dealers and hardware retailers who are neither equipped nor motivated to verify BIS certification compliance in the pipe products they source and resell, and by the limited field presence of state Quality Control Authority inspectors relative to the scale of the informal pipe manufacturing industry across India’s major pipe-producing states. The price sensitivity of smallholder and marginal farmers, who constitute the majority of subsidized micro-irrigation program beneficiaries in terms of number, creates a structural buyer preference for lower-cost pipe options that organized sector manufacturers can address only through cost efficiency investment, rural channel expansion, and government procurement quality enforcement rather than product differentiation alone.

Subsidy Disbursement Delays and Implementation Bottlenecks in State Government Micro-Irrigation Programs Creating Cash Flow Stress and Demand Uncertainty

The dependence of a substantial portion of Indian irrigation pipe demand on government subsidy disbursement through state horticulture mission agencies, agriculture departments, and district-level implementation committees introduces a structural demand volatility and cash flow risk dimension into the commercial planning of irrigation pipe manufacturers and dealers that is not present in purely market-driven demand segments, as delays in state government budget allocation, subsidy application processing backlogs, inspection agency capacity constraints, and beneficiary documentation verification requirements create extended periods of demand suppression followed by concentrated procurement bursts that are operationally challenging to serve efficiently and financially stressful for dealers carrying inventory in anticipation of subsidy release. Several major micro-irrigation market states including Maharashtra, Andhra Pradesh, and Karnataka have experienced recurring subsidy disbursement delays of six months to over two years in specific program years due to state fiscal constraints, administrative reorganization during election cycles, and procedural disputes over beneficiary eligibility criteria that have created uncertainty in farmer investment decisions, dealer receivable accumulation, and manufacturer forward order planning across the subsidy-dependent market segment. The transition of subsidy delivery toward direct benefit transfer mechanisms, which require farmer beneficiaries to invest full system cost upfront and receive reimbursement after installation verification by government inspectors, creates a capital access barrier for the small and marginal farmers who constitute the priority beneficiary category of national and state micro-irrigation programs, as the working capital requirements of full upfront investment exceed the financial capacity of farmers with limited bank credit access and constrained own capital resources.

Raw Material Price Volatility for Polymer Resins and Dependence on Petrochemical Import Pricing Compressing Irrigation Pipe Manufacturer Margins

Irrigation pipe manufacturers in India are exposed to significant and structurally recurring raw material cost volatility arising from the price dynamics of HDPE, UPVC, and LLDPE polymer resin supply, whose pricing is determined by global petrochemical feedstock costs, domestic polymer production capacity utilization at facilities operated by Reliance Industries, GAIL, HPCL-Mittal, and ONGC Petro Additions, and import prices from Middle Eastern and Asian commodity polymer exporters whose competitive pricing directly influences the landed cost of polymer resins available to Indian pipe extruders through the import parity mechanism that governs domestic polymer pricing. The price of HDPE pipe grade resin in India fluctuated between INR 80 per kilogram and INR 125 per kilogram across the 2020 to 2024 period, representing a price range of 56% that, given that polymer resin constitutes 55% to 70% of total pipe manufacturing cost for typical HDPE pipe products, translated directly into gross margin compression episodes that were commercially damaging for manufacturers operating under fixed-price government supply contracts with limited price escalation clause protections. The limited ability of irrigation pipe manufacturers to pass through full polymer cost increases to farmer and government procurement customers in price-sensitive agricultural markets, where buyer willingness to pay is anchored to historical price expectations and government subsidy unit cost norms that are revised infrequently relative to the pace of raw material market movements, creates asymmetric margin risk exposure for pipe manufacturers during commodity price escalation cycles and constrains their pricing flexibility relative to the commodity input cost volatility they face across procurement cycles.

Market Segmentation

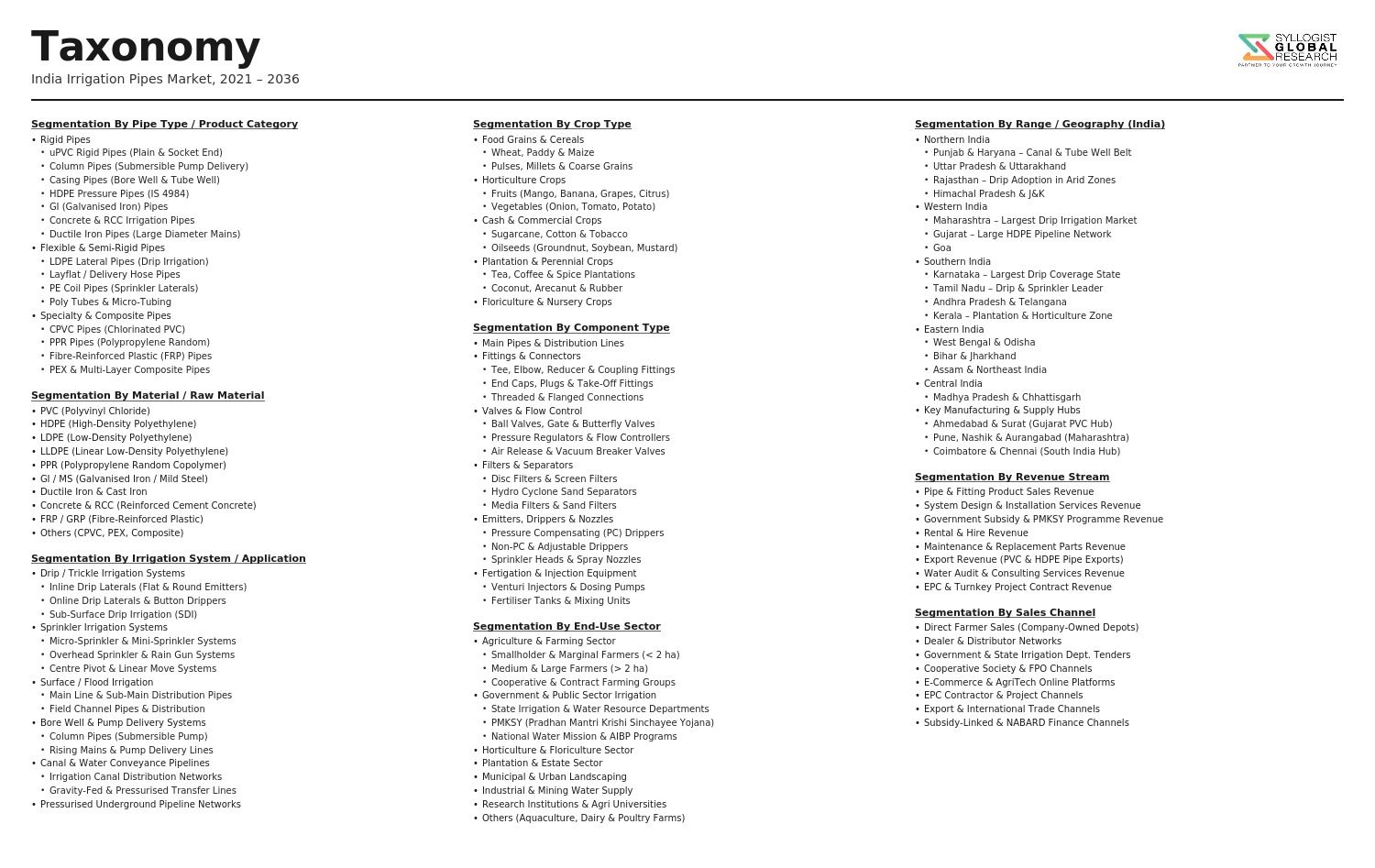

Segmentation By Pipe Material

- High-Density Polyethylene (HDPE) Pipes

- Unplasticized Polyvinyl Chloride (UPVC) Pipes

- Low-Density Polyethylene (LDPE) Pipes and Drip Laterals

- Linear Low-Density Polyethylene (LLDPE) Lateral Tubing

- Polypropylene (PP) Pipes

- Galvanized Iron (GI) and Mild Steel Pipes

- Concrete and Reinforced Cement Concrete (RCC) Pipes

- Others

Segmentation By Irrigation System Type

- Drip Irrigation System Pipes (Mainline, Submain, Lateral)

- Sprinkler Irrigation System Pipes (Mainline, Riser Pipes)

- Micro-Sprinkler and Mini-Sprinkler System Pipes

- Surface and Flood Irrigation Canal Distribution Pipes

- Pressurized Pipe Irrigation Networks for Canal Command Areas

- Others

Segmentation By Diameter

- Small Diameter Pipes (Below 32 mm)

- Medium Diameter Pipes (32 mm to 110 mm)

- Large Diameter Pipes (110 mm to 250 mm)

- Very Large Diameter Pipes (Above 250 mm)

- Others

Segmentation By Pressure Rating

- Low Pressure (Up to 2.5 kg/sq cm)

- Medium Pressure (2.5 to 6 kg/sq cm)

- High Pressure (6 to 10 kg/sq cm)

- Very High Pressure (Above 10 kg/sq cm)

- Others

Segmentation By Crop Type

- Vegetables and Salad Crops

- Fruit Crops (Mango, Banana, Pomegranate, Grapes, Citrus)

- Cereal and Grain Crops (Wheat, Maize, Paddy)

- Cash Crops (Sugarcane, Cotton, Groundnut)

- Flowers, Herbs, and Plantation Crops

- Pulses and Oilseeds

- Others

Segmentation By End User

- Smallholder and Marginal Farmers (Below 2 Hectares)

- Small and Medium Farmers (2 to 10 Hectares)

- Large and Commercial Farmers (Above 10 Hectares)

- Government Irrigation Departments and Agencies

- Agricultural Cooperatives and Farmer Producer Organizations

- Irrigation System Contractors and Integrators

- Agri-Exporters and Contract Farming Enterprises

- Others

Segmentation By Distribution Channel

- Authorized Irrigation Dealer and Distributor Network

- Government Procurement and Tender Supply

- Direct Sales Through Irrigation System Integrators

- Agricultural Cooperative and Society Supply

- E-Commerce and Online Agricultural Input Platforms

- Others

Segmentation By Region

- Western India (Maharashtra, Gujarat, Rajasthan, Goa)

- Southern India (Andhra Pradesh, Telangana, Karnataka, Tamil Nadu, Kerala)

- Northern India (Punjab, Haryana, Uttar Pradesh, Himachal Pradesh, Uttarakhand)

- Central India (Madhya Pradesh, Chhattisgarh)

- Eastern India (West Bengal, Odisha, Bihar, Jharkhand)

- Northeastern India

All market revenues are presented in USD

Historical Year: 2021-2024 | Base Year: 2025 | Estimated Year: 2026 | Forecast Period: 2027-2034

Key Questions this Study Will Answer

- What is the total market valuation of the India Irrigation Pipes Market in the base year 2025, and what is the projected market size and compound annual growth rate through 2034, disaggregated by pipe material, irrigation system type, diameter, pressure rating, crop type, and region, to enable polymer pipe manufacturers, irrigation system integrators, raw material suppliers, and investors to identify which pipe categories, irrigation system segments, and state markets will generate the highest absolute revenue and the most durable demand growth across the forecast period?

- How are the central government’s PMKSY expenditure commitments, the Per Drop More Crop micro-irrigation subsidy program targets, and state government matching grant structures across Maharashtra, Andhra Pradesh, Telangana, Karnataka, Gujarat, and Rajasthan translating into annual irrigation pipe procurement volumes and value by pipe material and irrigation system type through 2034, and what is the projected incremental pipe demand generated by each additional lakh hectare brought under micro-irrigation under national program targets?

- How is the accelerating depletion of groundwater across Punjab, Haryana, Rajasthan, and peninsular India’s hard rock aquifer zones reshaping farmer investment behavior in pressurized drip and sprinkler irrigation systems requiring HDPE mainline and LLDPE lateral pipe infrastructure, what is the projected rate of flood-to-drip irrigation conversion in water-stressed districts under different groundwater regulatory enforcement scenarios, and how does this conversion trajectory translate into incremental pipe demand volume and value through 2034?

- What is the current market share distribution between organized ISI-certified pipe manufacturers and unorganized sector producers across major state markets, what enforcement mechanisms are central and state governments deploying to improve quality compliance in government-subsidized irrigation pipe supply chains, and how is the competitive balance between organized and unorganized sector pipe supply expected to evolve through 2034 as government procurement quality requirements tighten and farmer awareness of pipe quality performance differentials improves?

- Who are the leading organized sector irrigation pipe manufacturers including Finolex Industries, Astral Limited, Prince Pipes and Fittings, Supreme Industries, Jain Irrigation Systems, and other regional players currently defining the competitive landscape of the India irrigation pipes market, and what are their respective manufacturing capacity and product range, BIS certification status across pipe categories, state government approved vendor empanelment, dealer network geographic coverage, technical sales force capabilities, capital expenditure plans for capacity expansion, and strategic positioning in response to the combined growth opportunity from PMKSY program expansion, horticulture sector growth, and groundwater depletion-driven drip irrigation adoption through the forecast period?

- Product Definition

- Research Methodology

- Research Design & Framework

- Overall Research Approach: Descriptive, Exploratory & Quantitative Mixed-Method Design

- Market Definition & Scope Boundaries: What is Included and Excluded

- Segmentation Framework

- Key Research Assumptions & Limitations

- Secondary Research

- Primary Research Design & Execution

- Data Triangulation & Validation

- Market Sizing & Forecasting Methodology

- Competitive Intelligence Methodology

- Quality Assurance & Peer Review

- Definitions, Abbreviations & Data Notes

- Research Design & Framework

- Executive Summary

- Market Snapshot & Headline Numbers

- Key Findings & Research Highlights

- Market Dynamics

- Regional Market Summary

- Competitive Landscape Snapshot

- Technology & Innovation Highlights

- Market Dynamics

- Drivers

- Restraints

- Opportunities

- Challenges

- Porter’s Five Forces Analysis

- PESTLE Analysis

- Market Trends & Developments

- Emerging Trends

- Technological Developments

- Regulatory & Policy Changes

- Supply Chain & Sourcing Trends

- Manufacturing & Process Trends

- Investment & Funding Activity

- Sustainability & ESG Trends

- Risk Assessment Framework

- Monsoon Variability, Drought Frequency & Groundwater Depletion Risk Affecting Irrigation Infrastructure Investment

- Raw Material Price Volatility: PVC Resin, HDPE & Polymer Feedstock Import Dependency & Cost Risk

- Government Subsidy Policy Continuity, PMKSY Budget Allocation & Scheme Implementation Delay Risk

- Counterfeit & Substandard Pipe Flooding, BIS Compliance Enforcement & Market Disruption Risk

- Farmer Income Variability, Credit Access & Discretionary Irrigation Infrastructure Spending Risk

- Regulatory Framework & Standards

- Pradhan Mantri Krishi Sinchai Yojana (PMKSY), Per Drop More Crop & Har Khet Ko Pani Scheme Frameworks Governing Irrigation Pipe Demand

- BIS Standards for Irrigation Pipes: IS 4985 (UPVC), IS 4984 (HDPE), IS 12786 (LDPE Laterals) & Related Specifications

- Bureau of Indian Standards (BIS) Mandatory Certification, Quality Control Orders & Enforcement for Irrigation Pipes

- Central Ground Water Authority (CGWA) Regulations, Water Use Efficiency Mandates & Micro-Irrigation Promotion Policies

- State Irrigation Department Procurement Standards, Tender Specifications & Subsidy Eligibility Criteria for Irrigation Pipes

- India Irrigation Pipes Market Outlook

- Market Size & Forecast by Value

- Market Size & Forecast by Volume (Metric Tonnes & Kilometres)

- Market Size & Forecast by Pipe Type

- Rigid PVC (UPVC) Irrigation Pipes

- High-Density Polyethylene (HDPE) Pipes

- Low-Density Polyethylene (LDPE) Lateral Pipes

- Linear Low-Density Polyethylene (LLDPE) Pipes

- Layflat & Hose Pipes

- Sprinkler Lateral & Riser Pipes

- Drip Irrigation Lateral & Sub-Main Pipes

- Aluminium & Metal Irrigation Pipes

- Concrete & Asbestos Cement (AC) Replacement Pipes

- Market Size & Forecast by Material

- Polyvinyl Chloride (PVC / UPVC)

- High-Density Polyethylene (HDPE)

- Low-Density & Linear Low-Density Polyethylene (LDPE & LLDPE)

- Polypropylene (PP)

- Aluminium & Galvanised Steel

- Concrete & Other Materials

- Market Size & Forecast by Diameter

- Small Diameter (Below 63 mm)

- Medium Diameter (63 mm to 160 mm)

- Large Diameter (160 mm to 315 mm)

- Extra-Large Diameter (Above 315 mm)

- Market Size & Forecast by Pressure Rating

- Low Pressure (Below 4 kg/cm2)

- Medium Pressure (4 to 8 kg/cm2)

- High Pressure (Above 8 kg/cm2)

- Market Size & Forecast by Irrigation System

- Drip Irrigation Systems

- Sprinkler Irrigation Systems

- Surface & Flood Irrigation Conveyance Pipes

- Centre Pivot & Linear Move Irrigation Systems

- Underground Pipeline Irrigation Networks

- Market Size & Forecast by Application

- Agricultural Field Crop Irrigation

- Horticulture, Vegetable & Fruit Crop Irrigation

- Plantation & Cash Crop Irrigation

- Greenhouse & Protected Cultivation Irrigation

- Public Irrigation Canal Lining & Command Area Distribution Networks

- Landscaping, Golf Course & Turf Irrigation

- Market Size & Forecast by End-User

- Individual Farmers & Farmer Producer Organisations (FPOs)

- State Irrigation & Water Resource Departments

- Agricultural Cooperatives & Irrigation Societies

- Horticulture Development Agencies & Plantation Companies

- Real Estate, Infrastructure & Landscaping Contractors

- Market Size & Forecast by Sales Channel

- Agri-Input Dealer & District-Level Distributor Network

- Direct Government & State Department Tender Supply

- Irrigation Equipment & System Integrator Channel

- Cooperative & Farmer Producer Organisation Procurement

- Online & E-Commerce Platform

- Northern India Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Western India Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Southern India Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Eastern India Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- Central India Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- State-Wise* Irrigation Pipes Market Outlook

- Market Size & Forecast

- By Value

- By Volume (Metric Tonnes & kilometres)

- By Pipe Type

- By Material

- By Diameter

- By Application

- By End-User

- By State

- By Sales Channel

- Market Size & Forecast

- *Key States Analyzed in the Syllogist Global Research Portfolio: Maharashtra, Gujarat, Rajasthan, Madhya Pradesh, Uttar Pradesh, Punjab, Haryana, Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, Kerala, West Bengal, Odisha, Chhattisgarh, Bihar, Jharkhand, Assam, Himachal Pradesh, Uttarakhand

- Technology Landscape & Innovation Analysis

- Advanced HDPE Pipe Extrusion Technology: Bimodal & Multimodal Resin, Co-Extrusion & Wall Thickness Optimisation Deep-Dive

- UPVC Pipe Manufacturing Technology: Compound Formulation, High-Speed Extrusion & Pressure Rating Enhancement

- Drip Lateral & Inline Emitter Manufacturing Technology: In-Line, On-Line & Subsurface Drip Pipe Production

- Layflat & Flexible Hose Technology: Multi-Layer Construction, Burst Pressure & Field Durability Improvements

- UV Stabilisation, Anti-Microbial Additive & Long-Life Pipe Formulation Technology for Indian Climatic Conditions

- IoT-Enabled Smart Pipe & Sensor-Integrated Irrigation Network Monitoring Technology

- Recycled & Bio-Based Polymer Technology for Sustainable Irrigation Pipe Manufacturing in India

- Patent & IP Landscape in Irrigation Pipe Technologies Relevant to India

- Value Chain & Supply Chain Analysis

- PVC Resin, HDPE & LDPE Polymer Feedstock & Petrochemical Raw Material Supply Chain

- Pipe Additive, Stabiliser, Carbon Black & Colour Masterbatch Supply Chain

- Irrigation Pipe Extrusion, Fitting Manufacturing & Quality Testing Supply Chain in India

- Packaging, Coiling & Logistics Supply Chain for Irrigation Pipe Distribution

- Agri-Input Dealer, District Distributor & Cooperative Procurement Channel

- Government Tender, State Department Direct Supply & PMKSY Subsidy Disbursement Channel

- Pipe Waste, Scrap Recycling & Circular Economy Value Chain

- Pricing Analysis

- UPVC Irrigation Pipe Unit Price Benchmarking by Diameter, Pressure Class & State

- HDPE Pipe Unit Price & Per-Metre Cost Analysis by SDR Rating & Diameter

- LDPE & LLDPE Drip Lateral Price: Per-Metre Cost, Wall Thickness & Emitter Spacing Analysis

- Layflat Hose & Sprinkler Lateral Pricing: Bore Size, Working Pressure & Material Grade Comparison

- Subsidy-Adjusted vs. Open Market Price Analysis under PMKSY & State Micro-Irrigation Schemes

- Total Irrigation Pipe System Cost per Hectare Across Drip, Sprinkler & Surface Irrigation Configurations

- Sustainability & Environmental Analysis

- Lifecycle Assessment (LCA) of Irrigation Pipes: Carbon Footprint, Energy Intensity & End-of-Life Recyclability Across Materials

- Water Use Efficiency Contribution: Drip & Sprinkler Pipe Systems vs. Surface Irrigation Water Saving Quantification

- Groundwater Conservation, Soil Health & Waterlogging Prevention Benefits of Pressurised Irrigation Pipe Networks

- Recycled Polymer & Bio-Based Resin Adoption in Irrigation Pipe Manufacturing: Green Chemistry & Circular Economy

- Regulatory-Driven Sustainability, SDG 2 (Zero Hunger), SDG 6 (Clean Water) & SDG 12 (Responsible Consumption) Alignment

- Competitive Landscape

- Market Structure & Concentration

- Market Consolidation Level (Fragmented vs. Consolidated by Pipe Type & Geography)

- Top 10 Players Market Share

- HHI (Herfindahl-Hirschman Index) Concentration Analysis

- Competitive Intensity Map by Pipe Type, Material & State

- Player Classification

- Large Integrated Plastic Pipe Manufacturers with Irrigation Pipe Divisions

- Dedicated Irrigation Pipe & Micro-Irrigation System Manufacturers

- Regional & State-Level Irrigation Pipe Manufacturers

- HDPE Pipe Specialists Serving Agricultural & Infrastructure Markets

- Drip & Sprinkler Lateral Pipe & Emitter Specialists

- Layflat Hose & Flexible Pipe Manufacturers

- Agri-Input Distributors & Trading Companies with Private Label Irrigation Pipe Brands

- Government-Supported & Cooperative Sector Irrigation Pipe Suppliers

- Competitive Analysis Frameworks

- Market Share Analysis by Pipe Type, Material & State

- Company Profile

- Company Overview & Headquarters

- Irrigation Pipe Products & System Portfolio

- Key Customer Relationships & Reference Projects in India

- Manufacturing Footprint & Production Capacity in India

- Revenue (India Irrigation Pipe Segment) & Order Book

- Technology Differentiators & IP

- Key Strategic Partnerships, JVs & M&A Activity

- Recent Developments (Capacity Expansion, Product Launches, Government Contract Wins)

- SWOT Analysis

- Strategic Focus Areas & Roadmap

- Competitive Positioning Map (Product Breadth vs. Geographic Reach)

- Key Company Profiles

- Market Structure & Concentration

- Strategic Opportunity Analysis

- Strategic Output

- Market Opportunity Matrix: By Pipe Type, Material, Irrigation System, Application, End-User & State

- White Space Opportunity Analysis

- Strategic Recommendations

- Product Portfolio & Technology Investment Strategy

- Manufacturing & Operational Excellence Strategy

- Geographic Expansion & Localisation Strategy

- Customer & End-User Engagement Strategy

- Partnership, M&A & Ecosystem Strategy

- Sustainability & Circular Economy Strategy

- Risk Mitigation & Future Roadmap

- Strategic Priority Matrix & Roadmap

- Near-term (2025-2028)

- Mid-term (2029-2032)

- Long-term (2033-2037)

- Strategic Output